Business Finance Report - MOD003319, Anglia Ruskin University

VerifiedAdded on 2023/01/05

|12

|3099

|33

Report

AI Summary

This business finance report delves into key financial concepts and their practical applications. The report begins with an analysis of financial statements, including the statement of profit and loss and the balance sheet, along with the calculation and interpretation of crucial financial ratios such as q...

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

PART 1............................................................................................................................................3

Statement of profit and loss........................................................................................................3

Statement of Balance sheet.........................................................................................................4

PART 2............................................................................................................................................5

Concept of accrual accounting v/s cash accounting....................................................................5

Meaning and difference between profit and cash flow...............................................................6

PART 3............................................................................................................................................7

Meaning and purpose of budget..................................................................................................7

Benefits of forming limited company and registration of it over stock exchange......................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

Table of Contents.............................................................................................................................2

PART 1............................................................................................................................................3

Statement of profit and loss........................................................................................................3

Statement of Balance sheet.........................................................................................................4

PART 2............................................................................................................................................5

Concept of accrual accounting v/s cash accounting....................................................................5

Meaning and difference between profit and cash flow...............................................................6

PART 3............................................................................................................................................7

Meaning and purpose of budget..................................................................................................7

Benefits of forming limited company and registration of it over stock exchange......................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

PART 1

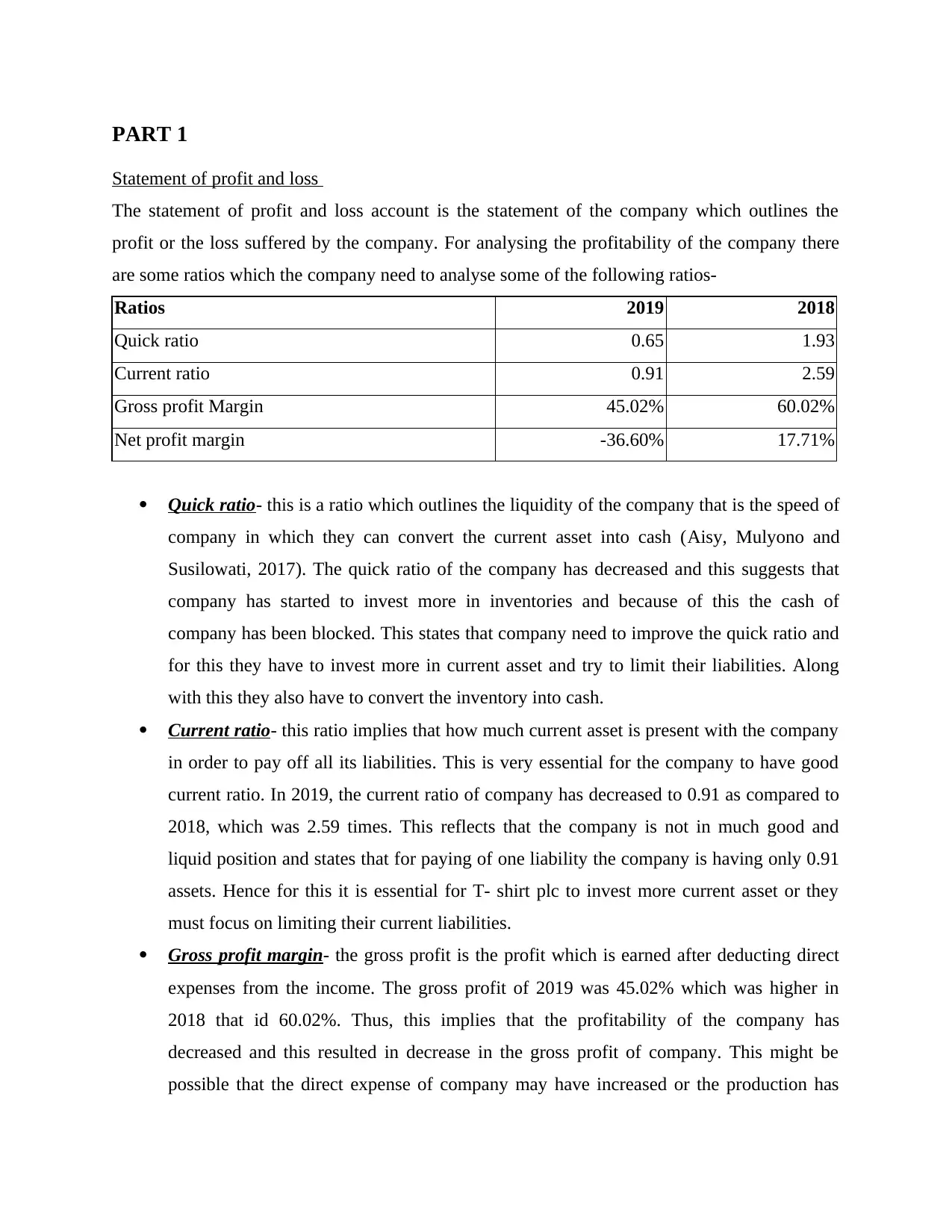

Statement of profit and loss

The statement of profit and loss account is the statement of the company which outlines the

profit or the loss suffered by the company. For analysing the profitability of the company there

are some ratios which the company need to analyse some of the following ratios-

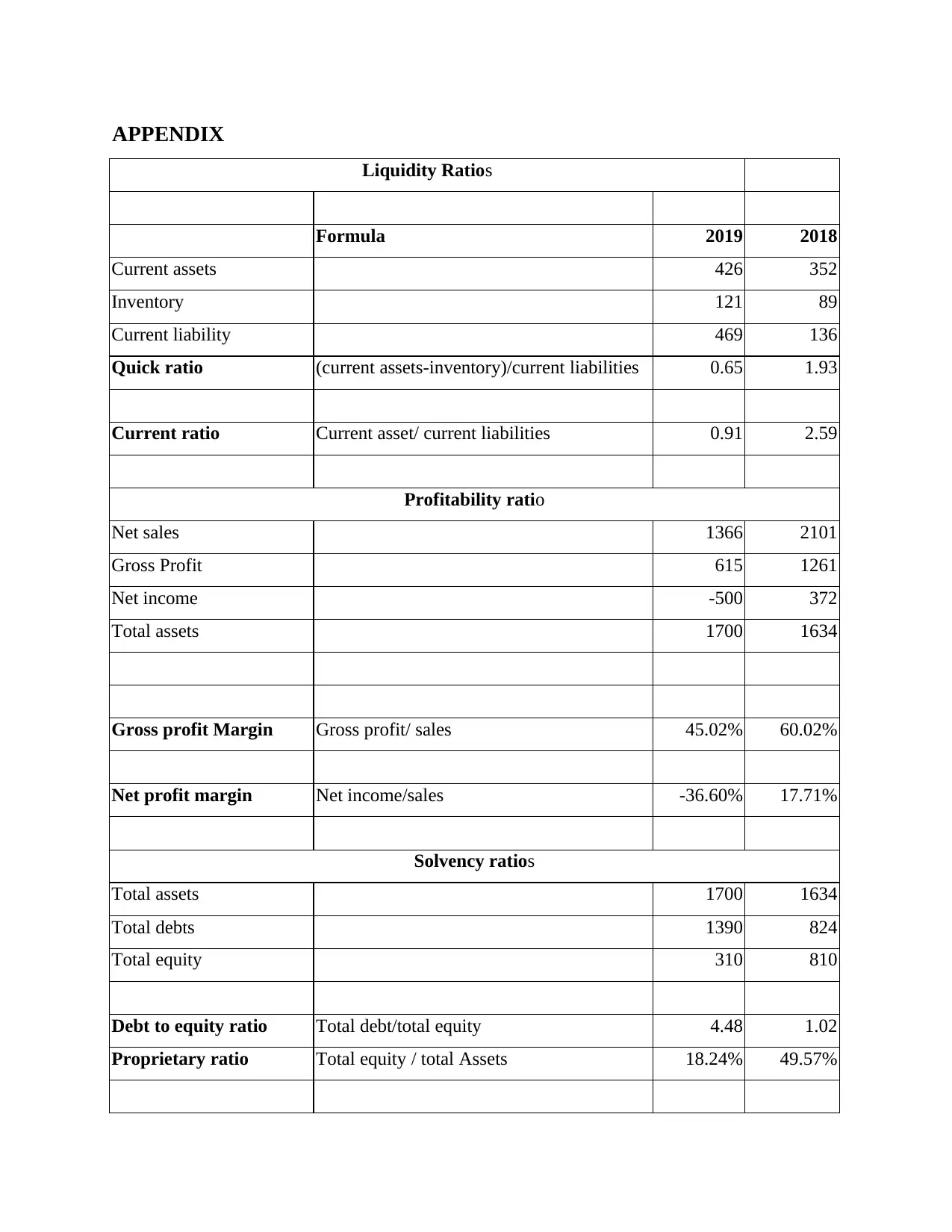

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Quick ratio- this is a ratio which outlines the liquidity of the company that is the speed of

company in which they can convert the current asset into cash (Aisy, Mulyono and

Susilowati, 2017). The quick ratio of the company has decreased and this suggests that

company has started to invest more in inventories and because of this the cash of

company has been blocked. This states that company need to improve the quick ratio and

for this they have to invest more in current asset and try to limit their liabilities. Along

with this they also have to convert the inventory into cash.

Current ratio- this ratio implies that how much current asset is present with the company

in order to pay off all its liabilities. This is very essential for the company to have good

current ratio. In 2019, the current ratio of company has decreased to 0.91 as compared to

2018, which was 2.59 times. This reflects that the company is not in much good and

liquid position and states that for paying of one liability the company is having only 0.91

assets. Hence for this it is essential for T- shirt plc to invest more current asset or they

must focus on limiting their current liabilities.

Gross profit margin- the gross profit is the profit which is earned after deducting direct

expenses from the income. The gross profit of 2019 was 45.02% which was higher in

2018 that id 60.02%. Thus, this implies that the profitability of the company has

decreased and this resulted in decrease in the gross profit of company. This might be

possible that the direct expense of company may have increased or the production has

Statement of profit and loss

The statement of profit and loss account is the statement of the company which outlines the

profit or the loss suffered by the company. For analysing the profitability of the company there

are some ratios which the company need to analyse some of the following ratios-

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Quick ratio- this is a ratio which outlines the liquidity of the company that is the speed of

company in which they can convert the current asset into cash (Aisy, Mulyono and

Susilowati, 2017). The quick ratio of the company has decreased and this suggests that

company has started to invest more in inventories and because of this the cash of

company has been blocked. This states that company need to improve the quick ratio and

for this they have to invest more in current asset and try to limit their liabilities. Along

with this they also have to convert the inventory into cash.

Current ratio- this ratio implies that how much current asset is present with the company

in order to pay off all its liabilities. This is very essential for the company to have good

current ratio. In 2019, the current ratio of company has decreased to 0.91 as compared to

2018, which was 2.59 times. This reflects that the company is not in much good and

liquid position and states that for paying of one liability the company is having only 0.91

assets. Hence for this it is essential for T- shirt plc to invest more current asset or they

must focus on limiting their current liabilities.

Gross profit margin- the gross profit is the profit which is earned after deducting direct

expenses from the income. The gross profit of 2019 was 45.02% which was higher in

2018 that id 60.02%. Thus, this implies that the profitability of the company has

decreased and this resulted in decrease in the gross profit of company. This might be

possible that the direct expense of company may have increased or the production has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decreased. For managing this company need to limit their direct expenses. For this

company has already initiated giving more credit period which will result in increase in

profit.

Net profit margin- this is defined as the profit which the company has earned after

deducting the indirect expense from the gross profit and the taxes and interest as well.

The net profit has changes drastically from 17.71% to -36.60% which is very high

change. This is very critical situation for the profitability of the company as profits of

company has been converted into losses. For this company need to work hard on limiting

their expenses and try to produce and sell more of the product and services. Further the

company also need to work more on marketing of the goods and services so that more

consumers are attracted towards it.

Statement of Balance sheet

The balance sheet is a statement which reflects the position of company at a point of

time. This simply means that this statement highlights all the liabilities and asset which are there

with company. Hence, for the analysis of the financial position of company some of the ratios are

being evaluated which are as follows-

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

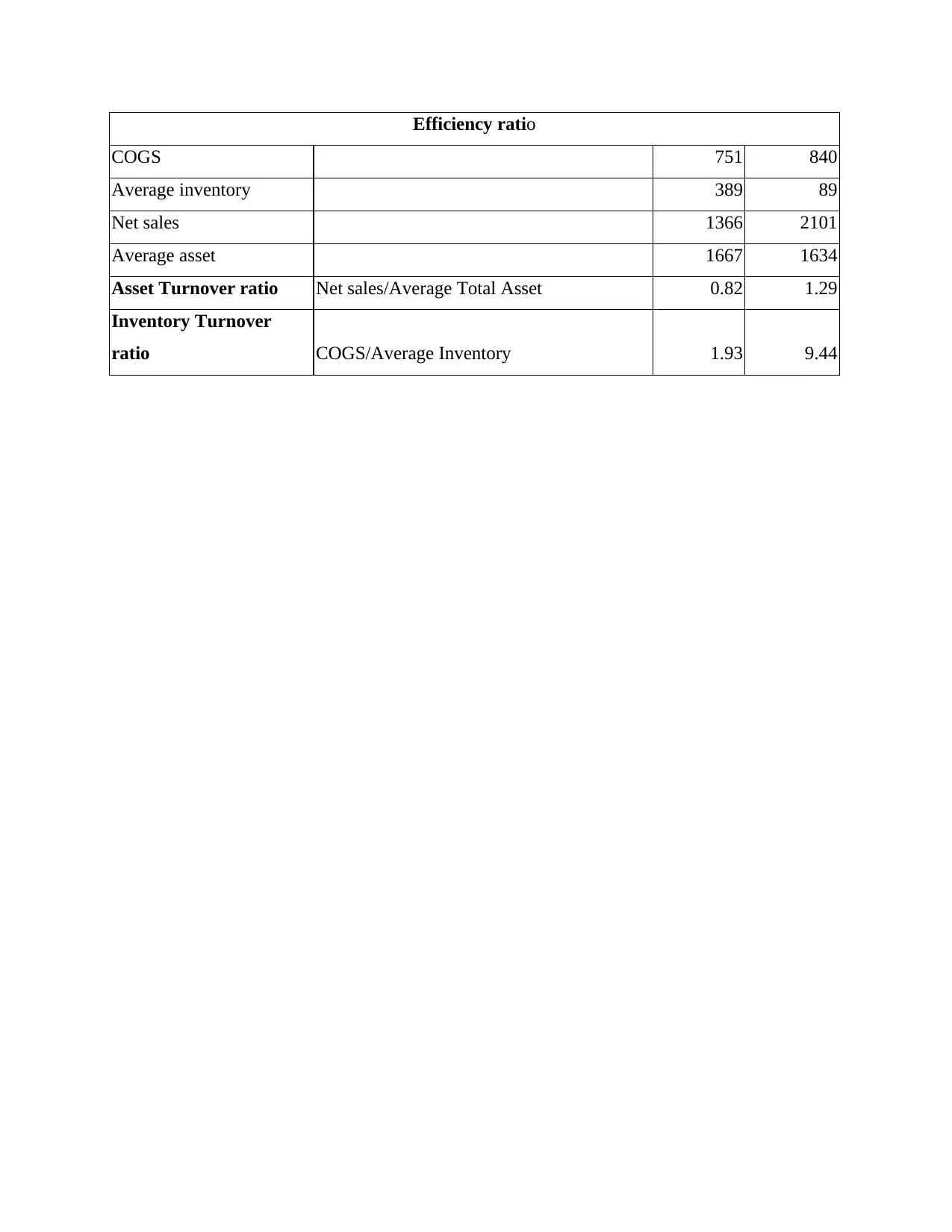

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio- this is the ratio which suggest the ratio of borrowed fund as

compared to the owners fund. In the current year the DE ratio is 4.48 and has been

increased from 1.02 and this suggests that the debt fund has increased. This clearly

reflects that the company has shifted more towards the debt financing as compared to the

equity financing. This means that company has to pay more of the interest and this is not

good for company.

Proprietary ratio- this is a ratio which suggest the estimation about the money which is

capitalized for meeting the requirement of the business. As compared to the last year the

the proprietary ratio has decreased from 49.57 % to 18.24 % which is not good for

company has already initiated giving more credit period which will result in increase in

profit.

Net profit margin- this is defined as the profit which the company has earned after

deducting the indirect expense from the gross profit and the taxes and interest as well.

The net profit has changes drastically from 17.71% to -36.60% which is very high

change. This is very critical situation for the profitability of the company as profits of

company has been converted into losses. For this company need to work hard on limiting

their expenses and try to produce and sell more of the product and services. Further the

company also need to work more on marketing of the goods and services so that more

consumers are attracted towards it.

Statement of Balance sheet

The balance sheet is a statement which reflects the position of company at a point of

time. This simply means that this statement highlights all the liabilities and asset which are there

with company. Hence, for the analysis of the financial position of company some of the ratios are

being evaluated which are as follows-

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio- this is the ratio which suggest the ratio of borrowed fund as

compared to the owners fund. In the current year the DE ratio is 4.48 and has been

increased from 1.02 and this suggests that the debt fund has increased. This clearly

reflects that the company has shifted more towards the debt financing as compared to the

equity financing. This means that company has to pay more of the interest and this is not

good for company.

Proprietary ratio- this is a ratio which suggest the estimation about the money which is

capitalized for meeting the requirement of the business. As compared to the last year the

the proprietary ratio has decreased from 49.57 % to 18.24 % which is not good for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company. This is particularly because of the reason that this suggests that 18.24 % of

financing involves the capital arranged from investors and other by the loan providers.

Asset turnover ratio- this ratio illustrates the relation between the facts that how

effectively the assets are being used in order to increase the sales of the company. In the

current year the asset turnover ratio is 0.82 and in 2018 it was 1.29. This reflects that the

ability of company in using the asset to increase the sales has reduced to a great extent.

Thus, this means that the company has to work more effectively in order to increase the

usage of asset to improve the sales of the company (Bjorklund, 2019).

Inventory turnover ratio- this is a ratio which depicts the fact that inventory turnover

ratio is the one which suggest the time period in which the inventory is converted in cash.

In 2018 the inventory turnover ratio was 9.44 which have reduced to 1.93 in the year

2019. This is good for the company as the reduction in this ratio suggest that the

company can speedily convert the inventory in cash and again invest in inventory to

again convert it in cash.

PART 2

Concept of accrual accounting v/s cash accounting

Accrual accounting- the accrual accounting concept is the one which states the revenue or

the expense is recorded at the time when the transaction actually occurs and not the time when

payment is paid or received. This method of accounting follows the principle of matching

principle which states that the revenue and expenses must be recognized at the same time at

which they have been incurred.

Benefits

The major benefit of using this method of accounting is that this allows for much easy

planning of the activities of business. The major reason for this is that company records

the transaction at time when it occurs then they know how they have to make future

strategies. This is assistive in making budget in proper and effective manner (6

advantages and disadvantages of accrual basis accounting, 2016).

Another major benefit is that this concept of accounting is complied with GAAP which is

generally accepted accounting principles. Thus, this will assist the company in making

financing involves the capital arranged from investors and other by the loan providers.

Asset turnover ratio- this ratio illustrates the relation between the facts that how

effectively the assets are being used in order to increase the sales of the company. In the

current year the asset turnover ratio is 0.82 and in 2018 it was 1.29. This reflects that the

ability of company in using the asset to increase the sales has reduced to a great extent.

Thus, this means that the company has to work more effectively in order to increase the

usage of asset to improve the sales of the company (Bjorklund, 2019).

Inventory turnover ratio- this is a ratio which depicts the fact that inventory turnover

ratio is the one which suggest the time period in which the inventory is converted in cash.

In 2018 the inventory turnover ratio was 9.44 which have reduced to 1.93 in the year

2019. This is good for the company as the reduction in this ratio suggest that the

company can speedily convert the inventory in cash and again invest in inventory to

again convert it in cash.

PART 2

Concept of accrual accounting v/s cash accounting

Accrual accounting- the accrual accounting concept is the one which states the revenue or

the expense is recorded at the time when the transaction actually occurs and not the time when

payment is paid or received. This method of accounting follows the principle of matching

principle which states that the revenue and expenses must be recognized at the same time at

which they have been incurred.

Benefits

The major benefit of using this method of accounting is that this allows for much easy

planning of the activities of business. The major reason for this is that company records

the transaction at time when it occurs then they know how they have to make future

strategies. This is assistive in making budget in proper and effective manner (6

advantages and disadvantages of accrual basis accounting, 2016).

Another major benefit is that this concept of accounting is complied with GAAP which is

generally accepted accounting principles. Thus, this will assist the company in making

the financial statements more accurate and proper representation of the financial health of

the company.

Limitation

The major limitation of the accrual accounting concept is that this leads to deception of

the financial statements. The major reason for this is that there might be confusion at time

of using this principle as sometimes it considers the transaction at that time only and

sometimes not. Thus, this may provide some negative or confusing image of company

financial position.

Another limitation of this concept is that the switching cost of the company for this

concept is high. The major reason for this is that when the company is using the cash

accounting and then switches over the accrual then this increases the cost.

Example- with respect to the present case study it can be seen that the credit period was

increased from 30 to 60 days. Hence, in this present situation even if cash is not received it will

be shown in books of account as a debtor.

Cash accounting- this is a method of accounting in which payment is recorded at the time

in which it is received and expenses are recorded at the time when they are paid. In other words

it can be said that the transaction is recorded at the time when the payment is made or received

and not when they occur.

Benefit

The major benefit of using the cash accounting is that it is very easy to use and

implement in order to conduct proper accounting. The major reason for this is that this

does not involve much steps and formalities and hence is easy to use.

Another major benefit is that this provides a tax advantage because of the reason that the

transaction is only recorded when it occurs and rest it is not recorded in books of

accounts.

Limitation

The major drawback of cash accounting is that this does not list out the complete picture.

The major reason for this is that the transaction is recorded only when cash is involves

that is either in case of payment or receipt of cash.

Another limitation is that the use of this is very restricted as the transaction is only

recorded at time when the cash payment of receipt is involved. If the credit is provided to

the company.

Limitation

The major limitation of the accrual accounting concept is that this leads to deception of

the financial statements. The major reason for this is that there might be confusion at time

of using this principle as sometimes it considers the transaction at that time only and

sometimes not. Thus, this may provide some negative or confusing image of company

financial position.

Another limitation of this concept is that the switching cost of the company for this

concept is high. The major reason for this is that when the company is using the cash

accounting and then switches over the accrual then this increases the cost.

Example- with respect to the present case study it can be seen that the credit period was

increased from 30 to 60 days. Hence, in this present situation even if cash is not received it will

be shown in books of account as a debtor.

Cash accounting- this is a method of accounting in which payment is recorded at the time

in which it is received and expenses are recorded at the time when they are paid. In other words

it can be said that the transaction is recorded at the time when the payment is made or received

and not when they occur.

Benefit

The major benefit of using the cash accounting is that it is very easy to use and

implement in order to conduct proper accounting. The major reason for this is that this

does not involve much steps and formalities and hence is easy to use.

Another major benefit is that this provides a tax advantage because of the reason that the

transaction is only recorded when it occurs and rest it is not recorded in books of

accounts.

Limitation

The major drawback of cash accounting is that this does not list out the complete picture.

The major reason for this is that the transaction is recorded only when cash is involves

that is either in case of payment or receipt of cash.

Another limitation is that the use of this is very restricted as the transaction is only

recorded at time when the cash payment of receipt is involved. If the credit is provided to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the consumer then this will not be recorded at time of credit but will be recorded when

payment will be made.

Example- with respect to the above example of the goods is sold to consumer on credit that if 60

days then the transaction will be recorded at the time when cash will be received from the

consumers.

Meaning and difference between profit and cash flow

Meaning of profit and cash flow

Profit- the profit is referred to as remain of money which is left after deducting all the

cost and expenses from the income. The profit is calculated and showed in the income statement

after deducting all the direct and indirect expenses from the income. This profit is required for

the survival of the business.

Cash flow- this is the amount of cash which the company receives or pay during a certain

period of time. The cash can have two different flows that is cash inflow and cash outflow. The

cash outflow means cash going out of business and cash inflow means cash coming within the

business. For business to be successful the most essential thing is having a positive cash inflow

so that business is having good amount of cash.

Difference between cash flow and profits

Cash flow Profit

Cash flow is the amount and movement of cash

from within and outside of the business (What

is the difference between the cash basis and the

accrual basis of accounting? 2020).

On the flip side profit is defined as the money

which is left after deducting all the expenses

from the income.

The cash flow highlights the movement of cash

which is incurred from business activities.

On the other side profit indicates the amount of

cash which is generated from the selling of

product in which company deals.

The cash flow highlights the liquidity of the

company.

The profit depicts the profitability of the

company that is what the company earns after

applying for all expenses.

The cash flow includes the total of cash inflow

and outflow from the operating, investing and

financing activities.

The profit is referred to as the variation

between the revenue and the expenses which

the company incurs during the certain period of

payment will be made.

Example- with respect to the above example of the goods is sold to consumer on credit that if 60

days then the transaction will be recorded at the time when cash will be received from the

consumers.

Meaning and difference between profit and cash flow

Meaning of profit and cash flow

Profit- the profit is referred to as remain of money which is left after deducting all the

cost and expenses from the income. The profit is calculated and showed in the income statement

after deducting all the direct and indirect expenses from the income. This profit is required for

the survival of the business.

Cash flow- this is the amount of cash which the company receives or pay during a certain

period of time. The cash can have two different flows that is cash inflow and cash outflow. The

cash outflow means cash going out of business and cash inflow means cash coming within the

business. For business to be successful the most essential thing is having a positive cash inflow

so that business is having good amount of cash.

Difference between cash flow and profits

Cash flow Profit

Cash flow is the amount and movement of cash

from within and outside of the business (What

is the difference between the cash basis and the

accrual basis of accounting? 2020).

On the flip side profit is defined as the money

which is left after deducting all the expenses

from the income.

The cash flow highlights the movement of cash

which is incurred from business activities.

On the other side profit indicates the amount of

cash which is generated from the selling of

product in which company deals.

The cash flow highlights the liquidity of the

company.

The profit depicts the profitability of the

company that is what the company earns after

applying for all expenses.

The cash flow includes the total of cash inflow

and outflow from the operating, investing and

financing activities.

The profit is referred to as the variation

between the revenue and the expenses which

the company incurs during the certain period of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

time.

PART 3

Meaning and purpose of budget

Budget is defined as the estimation of the expected income and expenses which the

company may incur within the time frame of one year. This budget can be prepared for any

purpose that is for estimating the income and expense, sales, production, activity based zero

based and many other types of budget (Yaxin, 2018). These entire budgets provide a basis for

decision making for the manager. The major reason for this is that this budget provides

estimation that this much income or expense will be incurred. Thus, this provides an idea to the

manager and other people that they will have to spend this much amount in order to be in

profitable situation. The budget is also a basis for planning for effective future strategies and this

assist the manager in developing good and realistic strategies for optimum utilisation of the

budget. Another major reason for the effective use of budgeting is that this assists the company

in spending the amount in very optimal and effective manner. Thus, for this the manager can

make better strategies for the optimum and effective management of the limited finance in such a

manner that all expenses and requirements are being met.

Benefits of forming limited company and registration of it over stock exchange

The forming of a limited company is defined as forming a company wherein the

shareholders of the company have limited liability in the company unlike the partnership or a

company. Under this the shareholders have the liability limited up to the capital which they have

invested or as decided by all the shareholders. Further the registering of the company over stock

exchange is defined as listing the company over the stock exchange of the country or any

international stock exchanges. For a company there are many different types of benefits which

the company enjoys when they get themselves registered over the stock exchange (Firdaus and

Endri, 2020). These benefits are listed as below-

The most important benefit which the company enjoys after listing is the increase in

goodwill and market reputation of the company. This is the major benefit as when the

company list itself over stock exchange then the buyers in stock market comes to know

PART 3

Meaning and purpose of budget

Budget is defined as the estimation of the expected income and expenses which the

company may incur within the time frame of one year. This budget can be prepared for any

purpose that is for estimating the income and expense, sales, production, activity based zero

based and many other types of budget (Yaxin, 2018). These entire budgets provide a basis for

decision making for the manager. The major reason for this is that this budget provides

estimation that this much income or expense will be incurred. Thus, this provides an idea to the

manager and other people that they will have to spend this much amount in order to be in

profitable situation. The budget is also a basis for planning for effective future strategies and this

assist the manager in developing good and realistic strategies for optimum utilisation of the

budget. Another major reason for the effective use of budgeting is that this assists the company

in spending the amount in very optimal and effective manner. Thus, for this the manager can

make better strategies for the optimum and effective management of the limited finance in such a

manner that all expenses and requirements are being met.

Benefits of forming limited company and registration of it over stock exchange

The forming of a limited company is defined as forming a company wherein the

shareholders of the company have limited liability in the company unlike the partnership or a

company. Under this the shareholders have the liability limited up to the capital which they have

invested or as decided by all the shareholders. Further the registering of the company over stock

exchange is defined as listing the company over the stock exchange of the country or any

international stock exchanges. For a company there are many different types of benefits which

the company enjoys when they get themselves registered over the stock exchange (Firdaus and

Endri, 2020). These benefits are listed as below-

The most important benefit which the company enjoys after listing is the increase in

goodwill and market reputation of the company. This is the major benefit as when the

company list itself over stock exchange then the buyers in stock market comes to know

about the company and this increase goodwill of company. Thus, this results in boost in

the market profile of the company to a great extent.

Further another major benefit of listing is that when the company trades over the stock

market then it can easily get access to better financial options for raising capital. The

major reason for this is that when the company operates over stock market then people

trust the company and this increases the credibility of the company. Thus, as a result of

this company can arrange for easy access to the capital and at lower rates as well.

Another major benefit is that there is more liquidity as the company register itself over

the stock market. The major reason for this is that when the company list itself over stock

market then this increases the investor investing in the company and as and when the

company requires money they can float their shares within the market. Thus, this result in

increase in the liquidity of company and they can arrange finance very quickly.

Further another major benefit of registering over stock market is that this increases

transparency and efficiency of the company (Easton and et.al, 2018). The major

underlying this fact is that when the company is in stock market then they have to reveal

their financial position at least every year and because of this there is transparency among

company and its shareholders.

In addition to this another major benefit of listing the company over stock exchange is

that this leads in more ethical and effective working. The major reason underlying this

fact is that when the company works over stock exchange then they come in contact with

much higher authorities. Thus, this result in more ethical and effective working.

the market profile of the company to a great extent.

Further another major benefit of listing is that when the company trades over the stock

market then it can easily get access to better financial options for raising capital. The

major reason for this is that when the company operates over stock market then people

trust the company and this increases the credibility of the company. Thus, as a result of

this company can arrange for easy access to the capital and at lower rates as well.

Another major benefit is that there is more liquidity as the company register itself over

the stock market. The major reason for this is that when the company list itself over stock

market then this increases the investor investing in the company and as and when the

company requires money they can float their shares within the market. Thus, this result in

increase in the liquidity of company and they can arrange finance very quickly.

Further another major benefit of registering over stock market is that this increases

transparency and efficiency of the company (Easton and et.al, 2018). The major

underlying this fact is that when the company is in stock market then they have to reveal

their financial position at least every year and because of this there is transparency among

company and its shareholders.

In addition to this another major benefit of listing the company over stock exchange is

that this leads in more ethical and effective working. The major reason underlying this

fact is that when the company works over stock exchange then they come in contact with

much higher authorities. Thus, this result in more ethical and effective working.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Aisy, H.R., Mulyono, I. and Susilowati, K.D.S., 2017. Compilation of Financial Statements and

Financial Analysis for Non Profit

Organizations. JurnalMahasiswaAkuntansiManajemen. 3(1).

Bjorklund, P.R., 2019. The Financial Statements of a Property & Casualty Company. J. Legal

Econ. 25. p.101.

Easton, P.D. and et.al., 2018. Financial statement analysis & valuation. Boston, MA: Cambridge

Business Publishers.

Firdaus, F. and Endri, E., 2020. Financial Statement Analysis: Evidence from Indonesian Bank

BUKU IV. International Journal of Innovative Science and Research Technology. 5(4).

pp.455-461.

Yaxin, H., 2018. Analysis of financial statements of listed companies: a case study of Gree's

2016 annual report. Jiangsu Science & Technology Information. (15). p.4.

Online

6 advantages and disadvantages of accrual basis accounting. 2016. [Online]. Available through:

< https://connectusfund.org/6-advantages-and-disadvantages-of-accrual-basis-

accounting >

What is the difference between the cash basis and the accrual basis of accounting? 2020.

[Online]. Available Through:<https://www.accountingcoach.com/blog/cash-basis-

accrual-basis-of-accounting>.

Books and Journals

Aisy, H.R., Mulyono, I. and Susilowati, K.D.S., 2017. Compilation of Financial Statements and

Financial Analysis for Non Profit

Organizations. JurnalMahasiswaAkuntansiManajemen. 3(1).

Bjorklund, P.R., 2019. The Financial Statements of a Property & Casualty Company. J. Legal

Econ. 25. p.101.

Easton, P.D. and et.al., 2018. Financial statement analysis & valuation. Boston, MA: Cambridge

Business Publishers.

Firdaus, F. and Endri, E., 2020. Financial Statement Analysis: Evidence from Indonesian Bank

BUKU IV. International Journal of Innovative Science and Research Technology. 5(4).

pp.455-461.

Yaxin, H., 2018. Analysis of financial statements of listed companies: a case study of Gree's

2016 annual report. Jiangsu Science & Technology Information. (15). p.4.

Online

6 advantages and disadvantages of accrual basis accounting. 2016. [Online]. Available through:

< https://connectusfund.org/6-advantages-and-disadvantages-of-accrual-basis-

accounting >

What is the difference between the cash basis and the accrual basis of accounting? 2020.

[Online]. Available Through:<https://www.accountingcoach.com/blog/cash-basis-

accrual-basis-of-accounting>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Efficiency ratio

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover

ratio COGS/Average Inventory 1.93 9.44

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover

ratio COGS/Average Inventory 1.93 9.44

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.