BAF-5-FOF Coursework: Analysis of Project Evaluation Techniques

VerifiedAdded on 2022/08/23

|17

|689

|17

Report

AI Summary

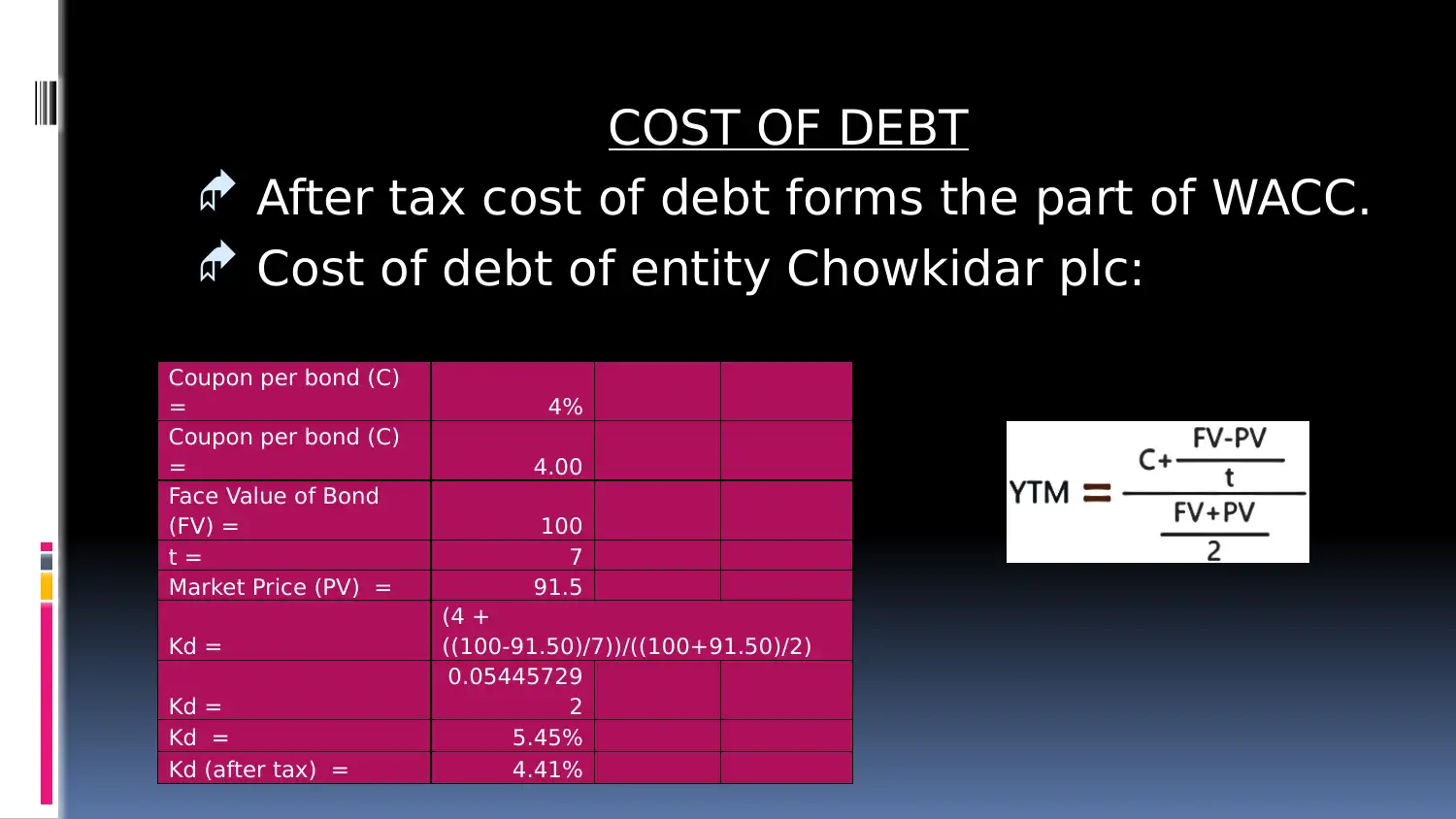

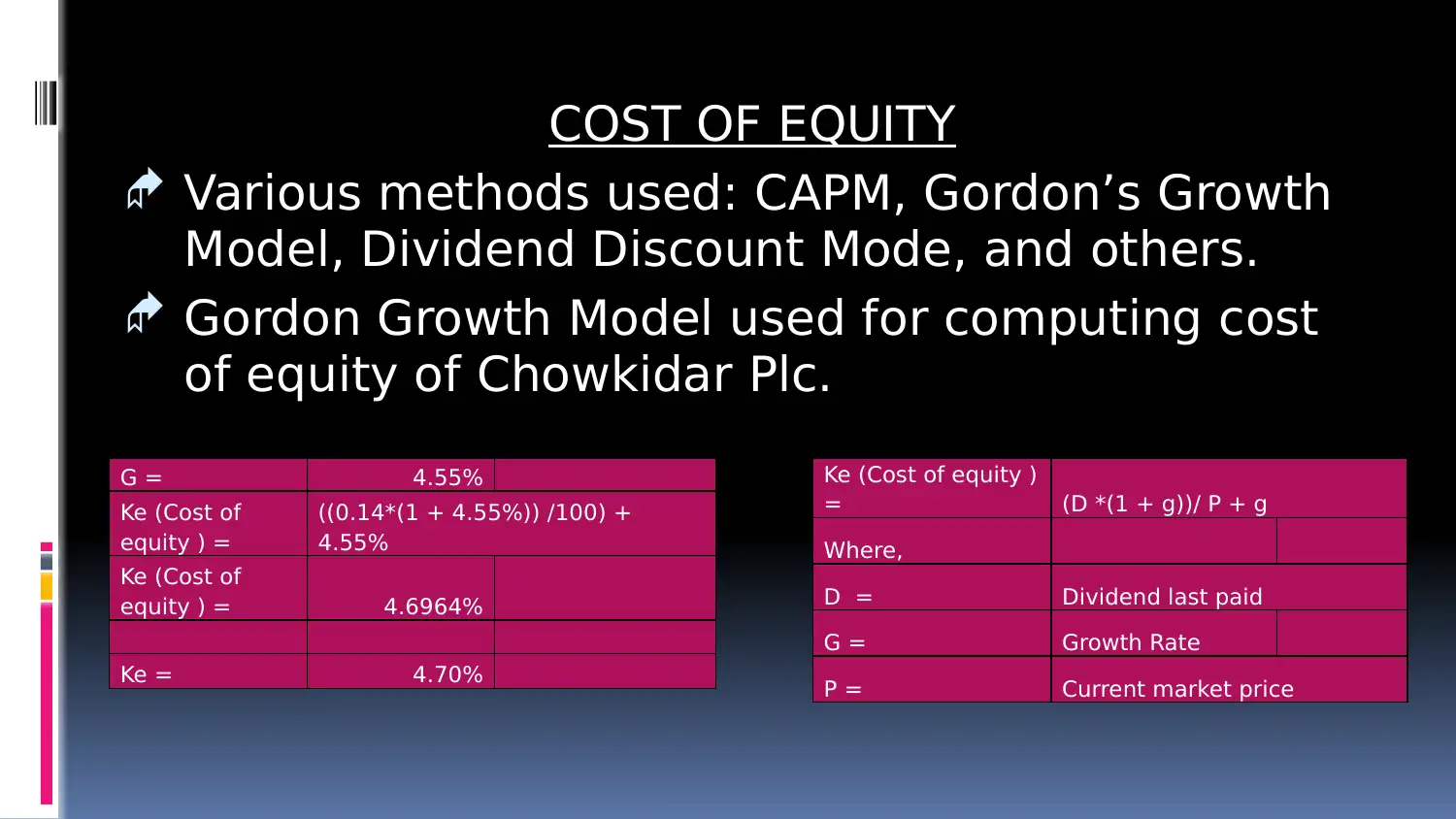

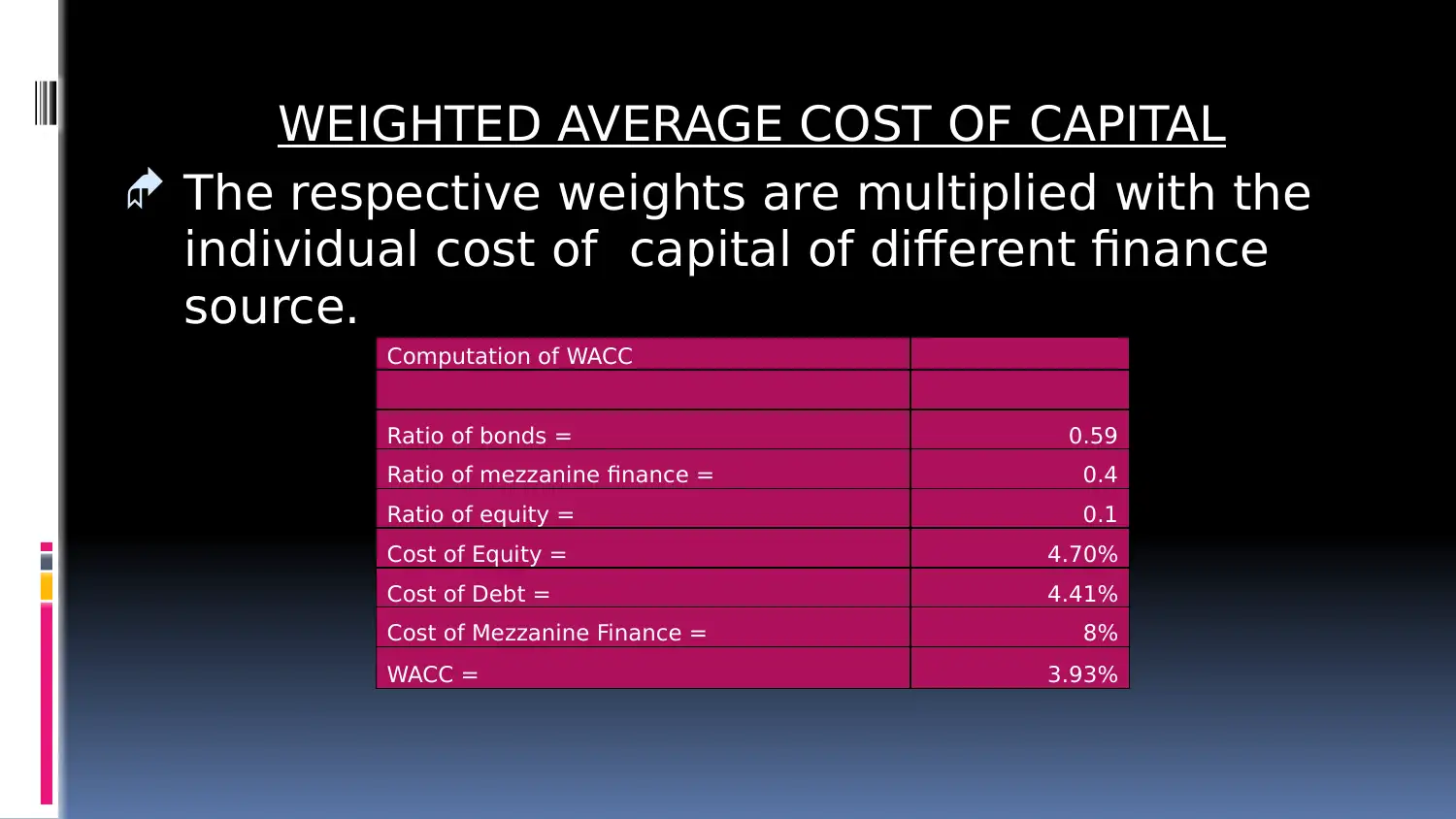

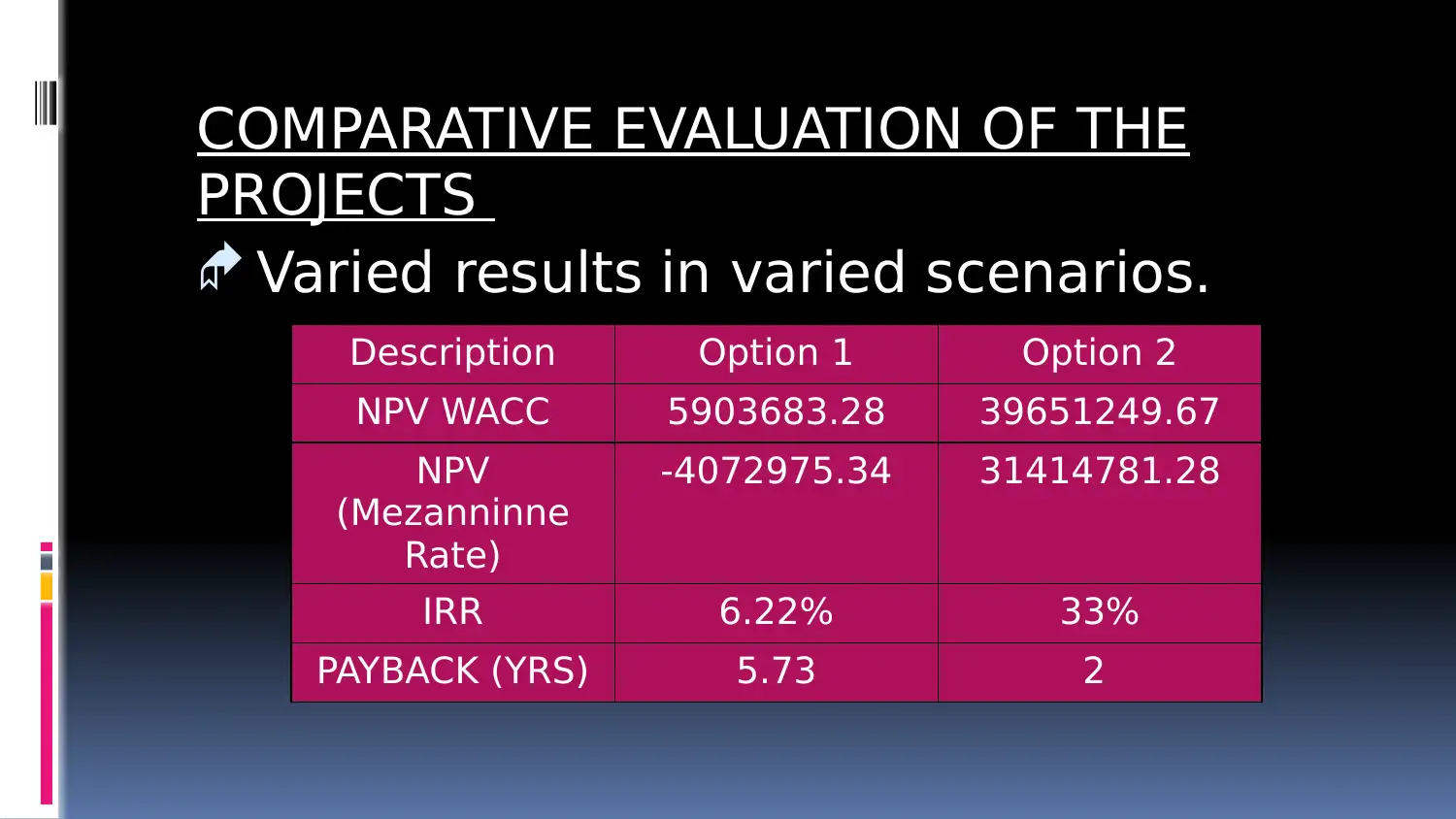

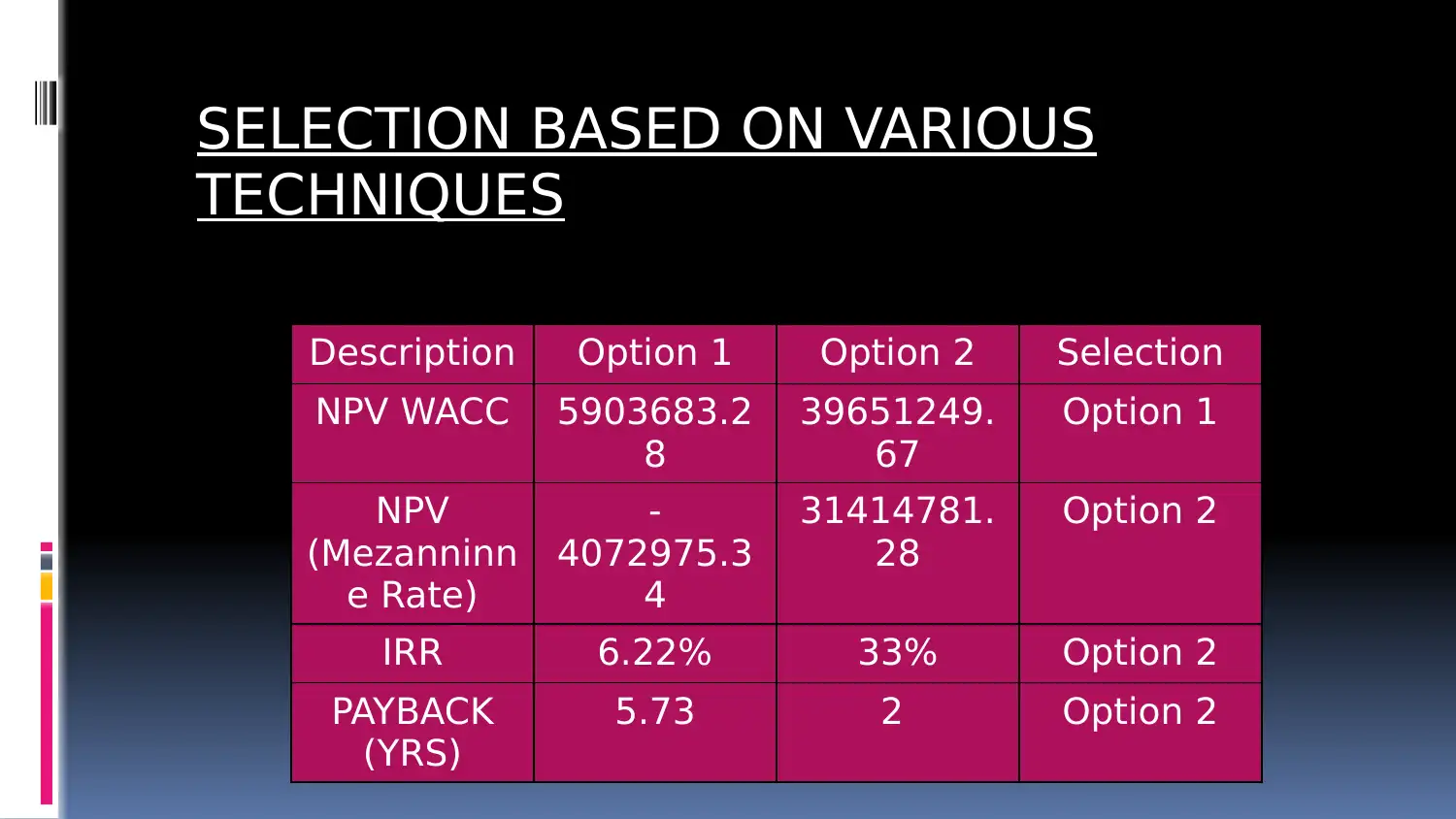

This report provides a comprehensive analysis of project evaluation techniques, focusing on the assessment of single and mutually exclusive projects. It examines the characteristics of project evaluation, emphasizing the involvement of significant funds and irreversible decisions. The report explores various evaluation methods, including Cash Payback Period, Net Present Value (NPV), Internal Rate of Return (IRR), and Profitability Index, along with the Weighted Average Cost of Capital (WACC) calculation. It utilizes the Gordon Growth Model to determine the cost of equity and compares different projects using NPV, IRR, and Payback methods. The analysis highlights the benefits and shortcomings of each technique, recommending the selection of Option 1 based on a higher NPV with the WACC and considering qualitative factors. The report concludes by emphasizing the importance of careful evaluation, the impact of different methods on results, and the need for input from departmental heads in investment decisions. References to relevant academic sources are also included.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.