Time-Driven Activity Based Costing

VerifiedAdded on 2020/05/16

|12

|2522

|88

AI Summary

This assignment delves into the intricacies of Time-Driven Activity Based Costing (TDABC), a modern approach to cost accounting. It highlights how TDABC differs from traditional ABC by focusing on capacity and time instead of resources. The document analyzes its advantages, such as reduced data requirements and improved cost accuracy, and provides real-world examples to illustrate its application in diverse industries.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Business Management 1

Business Management

Business Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business Management 2

Executive summary:

Activity based costing (ABC) technique is popular in business writing and management circles.

However, calculating baselines related to activities, developing model in this context, and test the

model on continuous basis are the reasons because of which it is considered as time consuming

and costly technique. Various improvements are developed by the Kaplan and Anderson in this

original model of ABC and named it as time-driven ABC. This new and improved model of

ABC reduce the requirement of data, and it consider two significant factors of organization that

are capacity and cost in lieu of resources, and time required for the purpose of performing any

activity.

This report mainly states the suitability of the TDABC model in private organizations operated in

Australia, and how this model is different from other costing techniques.

Executive summary:

Activity based costing (ABC) technique is popular in business writing and management circles.

However, calculating baselines related to activities, developing model in this context, and test the

model on continuous basis are the reasons because of which it is considered as time consuming

and costly technique. Various improvements are developed by the Kaplan and Anderson in this

original model of ABC and named it as time-driven ABC. This new and improved model of

ABC reduce the requirement of data, and it consider two significant factors of organization that

are capacity and cost in lieu of resources, and time required for the purpose of performing any

activity.

This report mainly states the suitability of the TDABC model in private organizations operated in

Australia, and how this model is different from other costing techniques.

Business Management 3

Contents

Executive summary:....................................................................................................................................2

Introduction:...............................................................................................................................................3

About Wesfarmers:.....................................................................................................................................4

TDABC & its different aspects:.....................................................................................................................5

Difference:...................................................................................................................................................6

TDABC & ABC:..........................................................................................................................................6

Traditional costing system & TDABC:.......................................................................................................7

TDABC and Wesfarmers:.............................................................................................................................9

Conclusion:................................................................................................................................................10

References:................................................................................................................................................10

Introduction:

Activity based costing method was originally introduced in the year of 1980, and it address

various issues related to traditional standard-cost systems. Traditional methods of costing only

Contents

Executive summary:....................................................................................................................................2

Introduction:...............................................................................................................................................3

About Wesfarmers:.....................................................................................................................................4

TDABC & its different aspects:.....................................................................................................................5

Difference:...................................................................................................................................................6

TDABC & ABC:..........................................................................................................................................6

Traditional costing system & TDABC:.......................................................................................................7

TDABC and Wesfarmers:.............................................................................................................................9

Conclusion:................................................................................................................................................10

References:................................................................................................................................................10

Introduction:

Activity based costing method was originally introduced in the year of 1980, and it address

various issues related to traditional standard-cost systems. Traditional methods of costing only

Business Management 4

use three categories of cost that were labor, materials, and overhead. It must be noted that

manufacturing companies generally smidgen the factors related to labor and materials which

were used by the products on individual basis. Cost systems of these companies allocate the

indirect and support cost with those measures which had been already decided such as direct

hours of labor and direct labor dollars. Later, various issues are faced by the organization

because of which new approach related to ABC model was introduced by the experts. This new

approach was developed by Kaplan and Anderson and it was named as Time-Driven Activity-

Based Costing (TDABC) (Kaplan & Anderson, 2004).

TDABC is a simple and elegant option available for companies for the purpose of determining

the cost and capacity utilization of their process and it also help the companies in determining the

profitability of orders, products, and customers. It provides better cost management which

automatically improves the cost management systems and address all issues related to this

system. Managers obtain accurate information in context of cost and profitability which help the

managers in managing the project. TDABC also justify the product variety and mix, price

customer orders, and it also manage the relationship between customer and company which

provide benefits to both the parties (Akhavan, ward & Bozic, 2016).

This paper states meaning and different elements related to TDABC and also discuss the

reliability of private organization in Australia on this model of costing. For the purpose of

understanding this new approach in better way, we chose Wesfarmers Limited as case study.

use three categories of cost that were labor, materials, and overhead. It must be noted that

manufacturing companies generally smidgen the factors related to labor and materials which

were used by the products on individual basis. Cost systems of these companies allocate the

indirect and support cost with those measures which had been already decided such as direct

hours of labor and direct labor dollars. Later, various issues are faced by the organization

because of which new approach related to ABC model was introduced by the experts. This new

approach was developed by Kaplan and Anderson and it was named as Time-Driven Activity-

Based Costing (TDABC) (Kaplan & Anderson, 2004).

TDABC is a simple and elegant option available for companies for the purpose of determining

the cost and capacity utilization of their process and it also help the companies in determining the

profitability of orders, products, and customers. It provides better cost management which

automatically improves the cost management systems and address all issues related to this

system. Managers obtain accurate information in context of cost and profitability which help the

managers in managing the project. TDABC also justify the product variety and mix, price

customer orders, and it also manage the relationship between customer and company which

provide benefits to both the parties (Akhavan, ward & Bozic, 2016).

This paper states meaning and different elements related to TDABC and also discuss the

reliability of private organization in Australia on this model of costing. For the purpose of

understanding this new approach in better way, we chose Wesfarmers Limited as case study.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business Management 5

About Wesfarmers:

Wesfarmer is originally incorporated in the year 1914 and it incorporated as Western Australian

farmers' cooperative, and later this company has grown as one the largest listed companies in

Australia. Headquarter of this company is situated in Western Australia and diverse business

operations of this company includes supermarkets, hotels, liquor, and convenience stores. It also

includes home improvement, office supplies, department stores, etc. Wesfarmers also diversified

its business in different industries that are chemicals, energy and fertilizers, industrial and safety

products and coal. Wesfarmers is considered as largest private sector employers with almost

220,000 employees employed in Australia. It must be noted that this company has shareholder

base of almost 530,000 employees (Wesfarmers, n.d.).

The main object of this company is to provide satisfactory returns to its shareholders by ensuring

discipline in financial matters and effective management of a diversified portfolio of businesses.

Wesfarmers mainly focus on effective and efficient management of each activity of the group

which is ensured through strategy development and execution of strategy and also through the

day to day operational performance. Each and every decision of the organization is taken and

guided by the divisional board of directors or relevant committee which includes the Wesfarmers

Managing Director and Finance Director (Wesfarmers, n.d.).

TDABC & its different aspects:

Traditional model of ABC creates issues for various organizations, especially for those

organizations which operated its business on large scale. It is difficult to implement this model

because of high cost related to interviews and survey or people. This model is costly because it

About Wesfarmers:

Wesfarmer is originally incorporated in the year 1914 and it incorporated as Western Australian

farmers' cooperative, and later this company has grown as one the largest listed companies in

Australia. Headquarter of this company is situated in Western Australia and diverse business

operations of this company includes supermarkets, hotels, liquor, and convenience stores. It also

includes home improvement, office supplies, department stores, etc. Wesfarmers also diversified

its business in different industries that are chemicals, energy and fertilizers, industrial and safety

products and coal. Wesfarmers is considered as largest private sector employers with almost

220,000 employees employed in Australia. It must be noted that this company has shareholder

base of almost 530,000 employees (Wesfarmers, n.d.).

The main object of this company is to provide satisfactory returns to its shareholders by ensuring

discipline in financial matters and effective management of a diversified portfolio of businesses.

Wesfarmers mainly focus on effective and efficient management of each activity of the group

which is ensured through strategy development and execution of strategy and also through the

day to day operational performance. Each and every decision of the organization is taken and

guided by the divisional board of directors or relevant committee which includes the Wesfarmers

Managing Director and Finance Director (Wesfarmers, n.d.).

TDABC & its different aspects:

Traditional model of ABC creates issues for various organizations, especially for those

organizations which operated its business on large scale. It is difficult to implement this model

because of high cost related to interviews and survey or people. This model is costly because it

Business Management 6

involves costly-to-validate time allocations. Maintenance and updating of this model is also

difficult in following manner:

Difficult to change the processes and resource spending.

Addition of new activities.

It is complex to diversify the individual orders, channels, and customers (Kaplan &

Anderson, 2007) .

For the purpose of dealing with the above stated issues, Kaplan and Anderson introduce new

version of traditional model of ABC, and this model mainly consider only two elements:

Unit cost related to supplying capacity of resources.

Required time for performing any activity.

In other words, TDABC is the updated version of original model of ABC which helps the

organization in identifying the cost and profit enhancement opportunities. Some relevant features

of the TDABC are stated below:

TDABC helps the organization in easy estimation of costa and it is easy to install this

model.

It is easy to update this model for the purpose of showing changes in processes, order

variety, and resource costs

It incorporates the resource capacity and also highlights the unused resource capacity for

the action of the management.

It reflects thee time equations which ensures variation in orders and handle customer

behavior.

involves costly-to-validate time allocations. Maintenance and updating of this model is also

difficult in following manner:

Difficult to change the processes and resource spending.

Addition of new activities.

It is complex to diversify the individual orders, channels, and customers (Kaplan &

Anderson, 2007) .

For the purpose of dealing with the above stated issues, Kaplan and Anderson introduce new

version of traditional model of ABC, and this model mainly consider only two elements:

Unit cost related to supplying capacity of resources.

Required time for performing any activity.

In other words, TDABC is the updated version of original model of ABC which helps the

organization in identifying the cost and profit enhancement opportunities. Some relevant features

of the TDABC are stated below:

TDABC helps the organization in easy estimation of costa and it is easy to install this

model.

It is easy to update this model for the purpose of showing changes in processes, order

variety, and resource costs

It incorporates the resource capacity and also highlights the unused resource capacity for

the action of the management.

It reflects thee time equations which ensures variation in orders and handle customer

behavior.

Business Management 7

TDABC simplifies the process of costing by removing the requirement of interview and survey

employees for the purpose of distributing the cost to the activities before taking them to the

objects of cost. This model helps the organization by directly assigning the resource cost to the

cost objects by using an elegant framework which considers only two factors. First it calculates

the cost related to supply resource capacity, and secondly it uses the capacity cost rate for driving

departmental resource cost to cost objects by estimating the demand for resource capacity which

is required by each cost object (Santana, et al. 2014).

Difference:

Above stated section of this report states different features of the TDABC which help the

organization in achieving effective cost management in the organization. This costing technique

is considered as updated version of traditional method of ABC model and it is completely

different from other techniques of costing. Difference between TDABC and ABC & TDABC

and other traditional methods of costing is discussed in detail below:

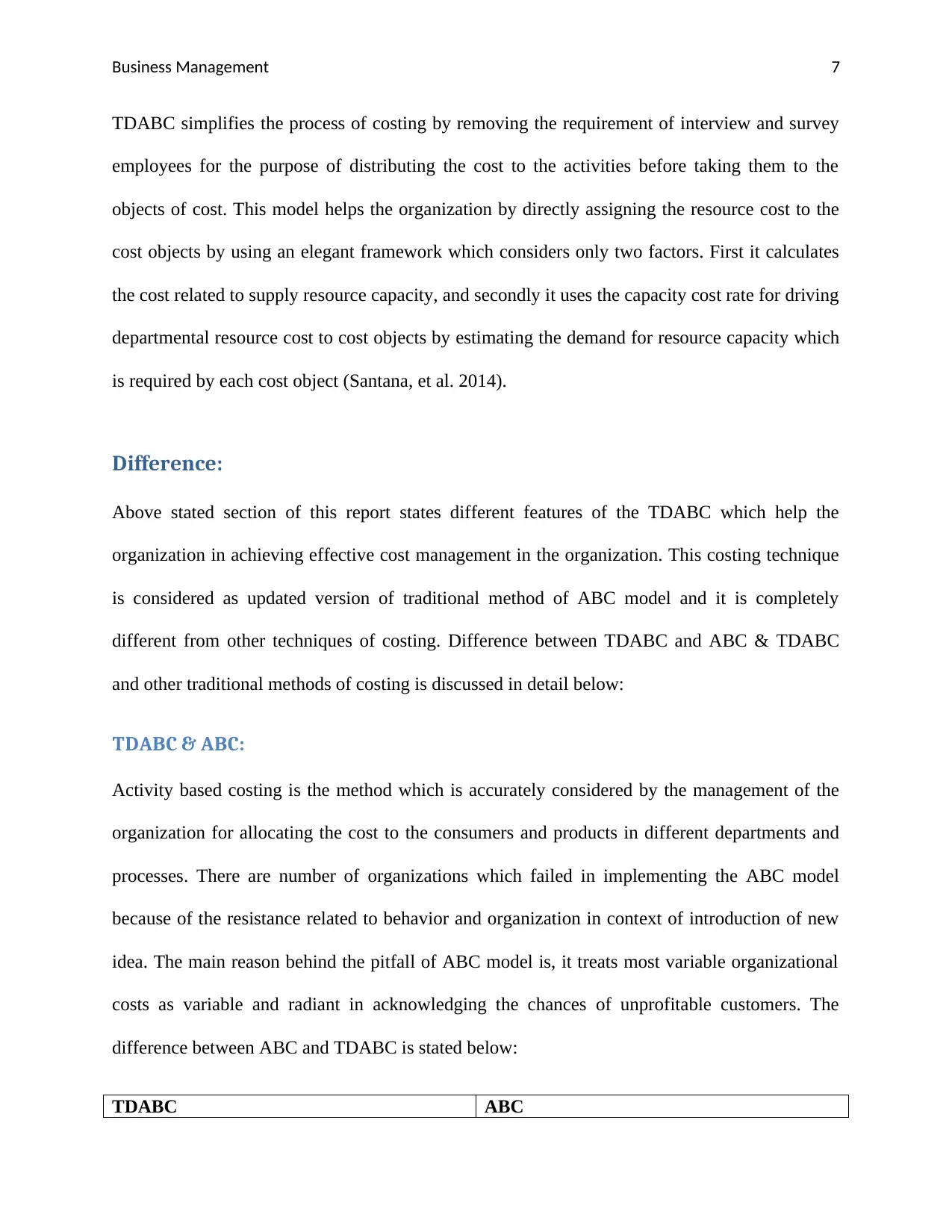

TDABC & ABC:

Activity based costing is the method which is accurately considered by the management of the

organization for allocating the cost to the consumers and products in different departments and

processes. There are number of organizations which failed in implementing the ABC model

because of the resistance related to behavior and organization in context of introduction of new

idea. The main reason behind the pitfall of ABC model is, it treats most variable organizational

costs as variable and radiant in acknowledging the chances of unprofitable customers. The

difference between ABC and TDABC is stated below:

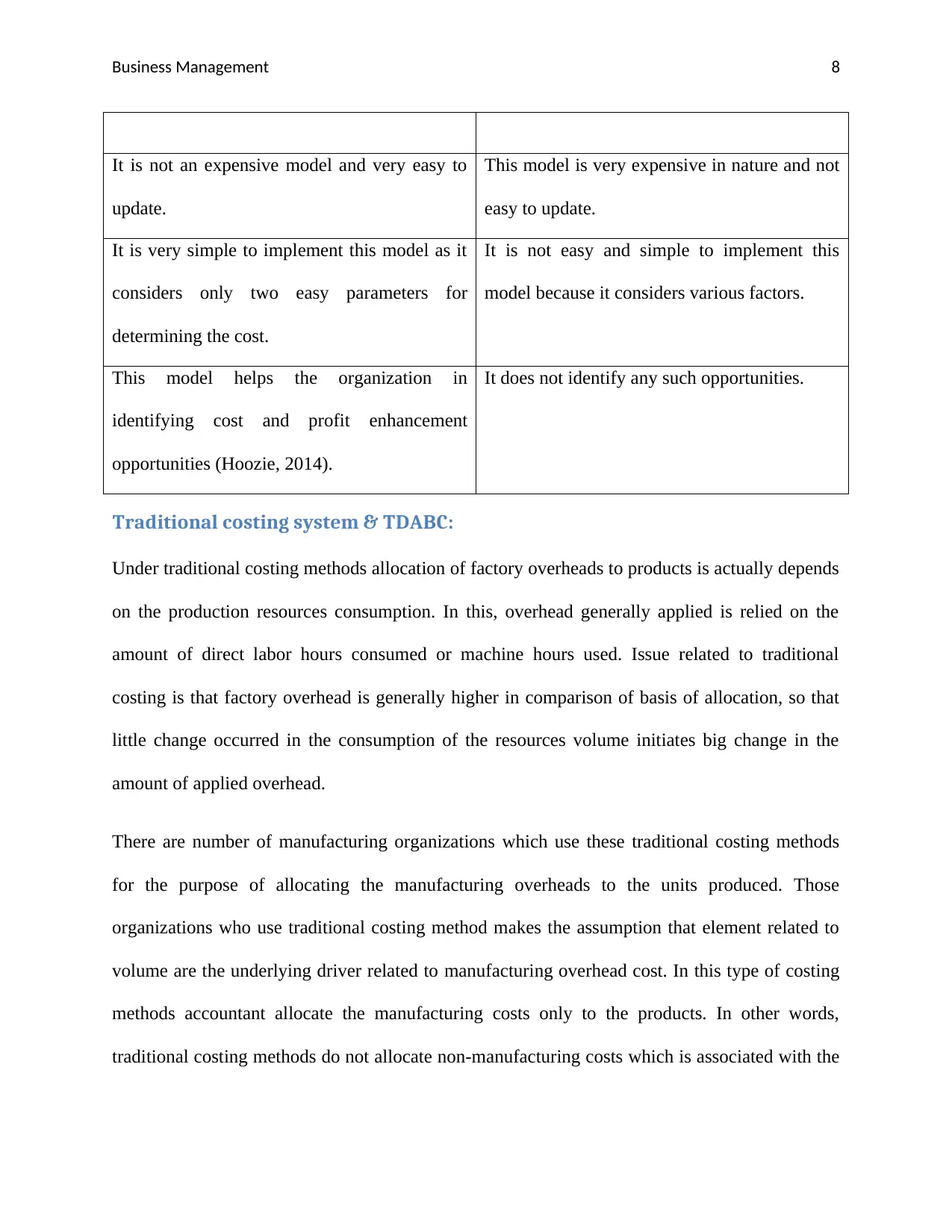

TDABC ABC

TDABC simplifies the process of costing by removing the requirement of interview and survey

employees for the purpose of distributing the cost to the activities before taking them to the

objects of cost. This model helps the organization by directly assigning the resource cost to the

cost objects by using an elegant framework which considers only two factors. First it calculates

the cost related to supply resource capacity, and secondly it uses the capacity cost rate for driving

departmental resource cost to cost objects by estimating the demand for resource capacity which

is required by each cost object (Santana, et al. 2014).

Difference:

Above stated section of this report states different features of the TDABC which help the

organization in achieving effective cost management in the organization. This costing technique

is considered as updated version of traditional method of ABC model and it is completely

different from other techniques of costing. Difference between TDABC and ABC & TDABC

and other traditional methods of costing is discussed in detail below:

TDABC & ABC:

Activity based costing is the method which is accurately considered by the management of the

organization for allocating the cost to the consumers and products in different departments and

processes. There are number of organizations which failed in implementing the ABC model

because of the resistance related to behavior and organization in context of introduction of new

idea. The main reason behind the pitfall of ABC model is, it treats most variable organizational

costs as variable and radiant in acknowledging the chances of unprofitable customers. The

difference between ABC and TDABC is stated below:

TDABC ABC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Management 8

It is not an expensive model and very easy to

update.

This model is very expensive in nature and not

easy to update.

It is very simple to implement this model as it

considers only two easy parameters for

determining the cost.

It is not easy and simple to implement this

model because it considers various factors.

This model helps the organization in

identifying cost and profit enhancement

opportunities (Hoozie, 2014).

It does not identify any such opportunities.

Traditional costing system & TDABC:

Under traditional costing methods allocation of factory overheads to products is actually depends

on the production resources consumption. In this, overhead generally applied is relied on the

amount of direct labor hours consumed or machine hours used. Issue related to traditional

costing is that factory overhead is generally higher in comparison of basis of allocation, so that

little change occurred in the consumption of the resources volume initiates big change in the

amount of applied overhead.

There are number of manufacturing organizations which use these traditional costing methods

for the purpose of allocating the manufacturing overheads to the units produced. Those

organizations who use traditional costing method makes the assumption that element related to

volume are the underlying driver related to manufacturing overhead cost. In this type of costing

methods accountant allocate the manufacturing costs only to the products. In other words,

traditional costing methods do not allocate non-manufacturing costs which is associated with the

It is not an expensive model and very easy to

update.

This model is very expensive in nature and not

easy to update.

It is very simple to implement this model as it

considers only two easy parameters for

determining the cost.

It is not easy and simple to implement this

model because it considers various factors.

This model helps the organization in

identifying cost and profit enhancement

opportunities (Hoozie, 2014).

It does not identify any such opportunities.

Traditional costing system & TDABC:

Under traditional costing methods allocation of factory overheads to products is actually depends

on the production resources consumption. In this, overhead generally applied is relied on the

amount of direct labor hours consumed or machine hours used. Issue related to traditional

costing is that factory overhead is generally higher in comparison of basis of allocation, so that

little change occurred in the consumption of the resources volume initiates big change in the

amount of applied overhead.

There are number of manufacturing organizations which use these traditional costing methods

for the purpose of allocating the manufacturing overheads to the units produced. Those

organizations who use traditional costing method makes the assumption that element related to

volume are the underlying driver related to manufacturing overhead cost. In this type of costing

methods accountant allocate the manufacturing costs only to the products. In other words,

traditional costing methods do not allocate non-manufacturing costs which is associated with the

Business Management 9

production of an item such as administrative expenses. Generally, organizations use this method

in external financial reports because it defines the cost of goods sold.

TDABC is the model which determines the cost by identifying the capacity of department and

process. Under this technique of costing, cost is mainly allocated by relying on the capacity of

resources and time required for performing any activity of transaction. This model is very

effective in nature and eliminates all the issues raised by traditional methods of costing. If

demand or work in context of these activities reduced, then also TDABC performed its work

effectively by estimating the volume related to resources released. After considering various

aspects of TDABC, it can be said that this model of costing is very simple in nature and it is easy

to update this model. This model shows different characteristics of an activity such as capacity of

resources and time equations. TDABC model is suitable for both large and small scale

organizations and also a best technique for present environment of business. Difference between

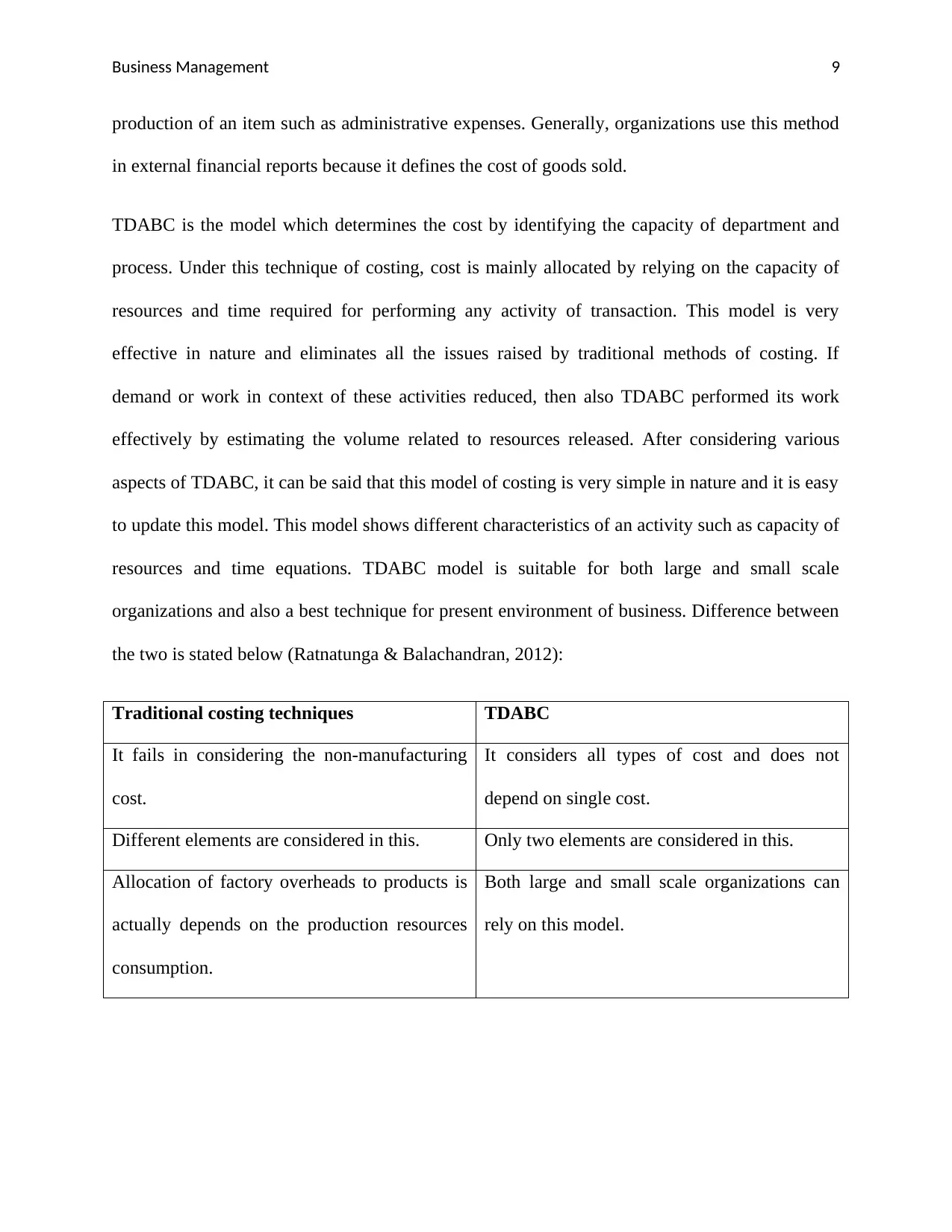

the two is stated below (Ratnatunga & Balachandran, 2012):

Traditional costing techniques TDABC

It fails in considering the non-manufacturing

cost.

It considers all types of cost and does not

depend on single cost.

Different elements are considered in this. Only two elements are considered in this.

Allocation of factory overheads to products is

actually depends on the production resources

consumption.

Both large and small scale organizations can

rely on this model.

production of an item such as administrative expenses. Generally, organizations use this method

in external financial reports because it defines the cost of goods sold.

TDABC is the model which determines the cost by identifying the capacity of department and

process. Under this technique of costing, cost is mainly allocated by relying on the capacity of

resources and time required for performing any activity of transaction. This model is very

effective in nature and eliminates all the issues raised by traditional methods of costing. If

demand or work in context of these activities reduced, then also TDABC performed its work

effectively by estimating the volume related to resources released. After considering various

aspects of TDABC, it can be said that this model of costing is very simple in nature and it is easy

to update this model. This model shows different characteristics of an activity such as capacity of

resources and time equations. TDABC model is suitable for both large and small scale

organizations and also a best technique for present environment of business. Difference between

the two is stated below (Ratnatunga & Balachandran, 2012):

Traditional costing techniques TDABC

It fails in considering the non-manufacturing

cost.

It considers all types of cost and does not

depend on single cost.

Different elements are considered in this. Only two elements are considered in this.

Allocation of factory overheads to products is

actually depends on the production resources

consumption.

Both large and small scale organizations can

rely on this model.

Business Management 10

TDABC and Wesfarmers:

Wesfarmers Annual report for the year 2016 states that resource business of the company faces

various difficulties in this year. Organization is focusing on reducing the cost and take actions to

manage their cash flow at the time when prices related to coal are low. Organization considers

the fact that it is possible to create value in the industrial division and its business. Wesfarmers

operate their business in such a way so that they can derive the best value for their shareholders.

It is possible for Wesfarmers to achieve all their targets and maintain all their cost by

implementing time-driven activity-based costing system. This system of costing helps the

organization in reducing their cost and managing their business in better way. TDABC helps the

Wesfarmers in following way (Wesfarmers, 2016):

After implementing the TDABC, organization eliminates the requirement of interview-

and-survey process in context of different resources.

This method of costing helps the organization in maintaining reliable accounts which are

accurate in nature by dealing with different issues occurred in manufacturing process.

Organization can reduce the time of processing needed for analyzing the data.

It simplifies the cost management system of the organization which helps the

organization in addressing different issues.

Updating and maintenance of this costing method is very easy (Pernot, Roodhooft &

Abbeele, 2007).

Conclusion:

TDABC and Wesfarmers:

Wesfarmers Annual report for the year 2016 states that resource business of the company faces

various difficulties in this year. Organization is focusing on reducing the cost and take actions to

manage their cash flow at the time when prices related to coal are low. Organization considers

the fact that it is possible to create value in the industrial division and its business. Wesfarmers

operate their business in such a way so that they can derive the best value for their shareholders.

It is possible for Wesfarmers to achieve all their targets and maintain all their cost by

implementing time-driven activity-based costing system. This system of costing helps the

organization in reducing their cost and managing their business in better way. TDABC helps the

Wesfarmers in following way (Wesfarmers, 2016):

After implementing the TDABC, organization eliminates the requirement of interview-

and-survey process in context of different resources.

This method of costing helps the organization in maintaining reliable accounts which are

accurate in nature by dealing with different issues occurred in manufacturing process.

Organization can reduce the time of processing needed for analyzing the data.

It simplifies the cost management system of the organization which helps the

organization in addressing different issues.

Updating and maintenance of this costing method is very easy (Pernot, Roodhooft &

Abbeele, 2007).

Conclusion:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Business Management 11

Activity based costing is the traditional and important method of costing, but it has various

shortcomings. ABC is considered as original model of costing and it is not suitable for every

organization. New version of original model of ABC is introduced by Kaplan and Anderson, and

this new version is named as time-driven ABC. This new and improved model of ABC reduce

the requirement of data, and it consider two significant factors of organization that are capacity

and cost in lieu of resources, and time required for the purpose of performing any activity.

Activity based costing is the traditional and important method of costing, but it has various

shortcomings. ABC is considered as original model of costing and it is not suitable for every

organization. New version of original model of ABC is introduced by Kaplan and Anderson, and

this new version is named as time-driven ABC. This new and improved model of ABC reduce

the requirement of data, and it consider two significant factors of organization that are capacity

and cost in lieu of resources, and time required for the purpose of performing any activity.

Business Management 12

References:

Akhavan, S. ward, L. & Bozic, K. (2016). Time-driven Activity-based Costing More Accurately

Reflects Costs in Arthroplasty Surgery. Clin Orthop Relat Resv., Volume 474(1).

Hoozie, S. (2014). A comparison of activity-based costing and time-driven activity-based

costing. Available at: https://calhoun.nps.edu/bitstream/handle/10945/47751/Hansen-A-

Comparison_2014-08.pdf?sequence=1. Accessed on 23rd January 2018.

Kaplan R. & Anderson S. (2007). The innovation of time-driven activity-based costing. Journal

of Cost Management.

Kaplan R. & Anderson, S. (2006). The competitive advantage of management accounting. J

Manage Account Res 18:127–135.

Kaplan, R. & Anderson, S. (2004). Time-Driven Activity Based Costing. Available at:

https://www.ncbi.nlm.nih.gov/pubmed/15559451. Accessed on 23rd January 2018.

Pernot, E., Roodhooft, F., & Abbeele, A. (2007). Time-Driven Activity-Based Costing for Inter-

Library Services: A Case Study in a University. The Journal of Academic Librarianship, Volume

33(5), 551 – 560.

Ratnatunga, J., Tse, M. S. C., & Balachandran, K. R. (2012). Cost Management in Sri Lanka: A

Case Study on Volume, Activity and Time as Cost Drivers. The International Journal of

Accounting, 47(3), 281 – 301.

Santana, A. et. al. (2014). Activity Based Costing And Time-Driven Activity Based Costing:

Towards An Integrated Approach. Available at:

http://www.academia.edu/14932706/ACTIVITY_BASED_COSTING_AND_TIME-

DRIVEN_ACTIVITY_BASED_COSTING_TOWARDS_AN_INTEGRATED_APPROACH.

Accessed on 23rd January 2018.

Wesfarmers, (2016). 2016 Annual Report. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=4.

Accessed on 23rd January 2018.

Wesfarmers. Our Businesses. Available at: http://www.wesfarmers.com.au/our-businesses/our-

businesses. Accessed on 23rd January 2018.

Wesfarmers. Who We Are. Available at: http://www.wesfarmers.com.au/who-we-are/who-we-

are. Accessed on 23rd January 2018.

References:

Akhavan, S. ward, L. & Bozic, K. (2016). Time-driven Activity-based Costing More Accurately

Reflects Costs in Arthroplasty Surgery. Clin Orthop Relat Resv., Volume 474(1).

Hoozie, S. (2014). A comparison of activity-based costing and time-driven activity-based

costing. Available at: https://calhoun.nps.edu/bitstream/handle/10945/47751/Hansen-A-

Comparison_2014-08.pdf?sequence=1. Accessed on 23rd January 2018.

Kaplan R. & Anderson S. (2007). The innovation of time-driven activity-based costing. Journal

of Cost Management.

Kaplan R. & Anderson, S. (2006). The competitive advantage of management accounting. J

Manage Account Res 18:127–135.

Kaplan, R. & Anderson, S. (2004). Time-Driven Activity Based Costing. Available at:

https://www.ncbi.nlm.nih.gov/pubmed/15559451. Accessed on 23rd January 2018.

Pernot, E., Roodhooft, F., & Abbeele, A. (2007). Time-Driven Activity-Based Costing for Inter-

Library Services: A Case Study in a University. The Journal of Academic Librarianship, Volume

33(5), 551 – 560.

Ratnatunga, J., Tse, M. S. C., & Balachandran, K. R. (2012). Cost Management in Sri Lanka: A

Case Study on Volume, Activity and Time as Cost Drivers. The International Journal of

Accounting, 47(3), 281 – 301.

Santana, A. et. al. (2014). Activity Based Costing And Time-Driven Activity Based Costing:

Towards An Integrated Approach. Available at:

http://www.academia.edu/14932706/ACTIVITY_BASED_COSTING_AND_TIME-

DRIVEN_ACTIVITY_BASED_COSTING_TOWARDS_AN_INTEGRATED_APPROACH.

Accessed on 23rd January 2018.

Wesfarmers, (2016). 2016 Annual Report. Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=4.

Accessed on 23rd January 2018.

Wesfarmers. Our Businesses. Available at: http://www.wesfarmers.com.au/our-businesses/our-

businesses. Accessed on 23rd January 2018.

Wesfarmers. Who We Are. Available at: http://www.wesfarmers.com.au/who-we-are/who-we-

are. Accessed on 23rd January 2018.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.