Business Management Accounting Assignment - UGB106, Term 1

VerifiedAdded on 2022/12/29

|13

|3428

|45

Homework Assignment

AI Summary

This assignment solution addresses key concepts in business management accounting, including cash budgeting, cash position analysis, and the behavioral aspects of budgeting. It presents a detailed cash budget for Woodrock Limited, assessing its liquidity and financial position. The solution also explores the relevance of behavioral factors in budgeting, discussing dysfunctional budgeting, participative budgeting, budgetary slack, and pressure. Furthermore, the assignment delves into cost accounting, covering contribution, break-even analysis, and the assumptions of the break-even model, and the impact of advertising on profit. The analysis encompasses overhead absorption rates, production costs, and the advantages and disadvantages of using a single absorption rate versus departmental rates. The document is a comprehensive resource for students studying management accounting, providing practical examples and in-depth explanations of core concepts. This assignment also provides a detailed analysis of the break-even point, margin of safety, and profit calculations, along with a discussion of the assumptions underlying the break-even model. Finally, the assignment examines the impact of changes in sales price and advertising expenditure on profitability.

BUSINESS MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................4

Cash budget ................................................................................................................................4

Cash position of company...........................................................................................................5

Issue of relevance in behavioral aspects of budgeting................................................................7

Overhead cost rate.....................................................................................................................10

Total production cost ................................................................................................................11

Advantage and disadvantage of single absorbing rate..............................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................4

Cash budget ................................................................................................................................4

Cash position of company...........................................................................................................5

Issue of relevance in behavioral aspects of budgeting................................................................7

Overhead cost rate.....................................................................................................................10

Total production cost ................................................................................................................11

Advantage and disadvantage of single absorbing rate..............................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

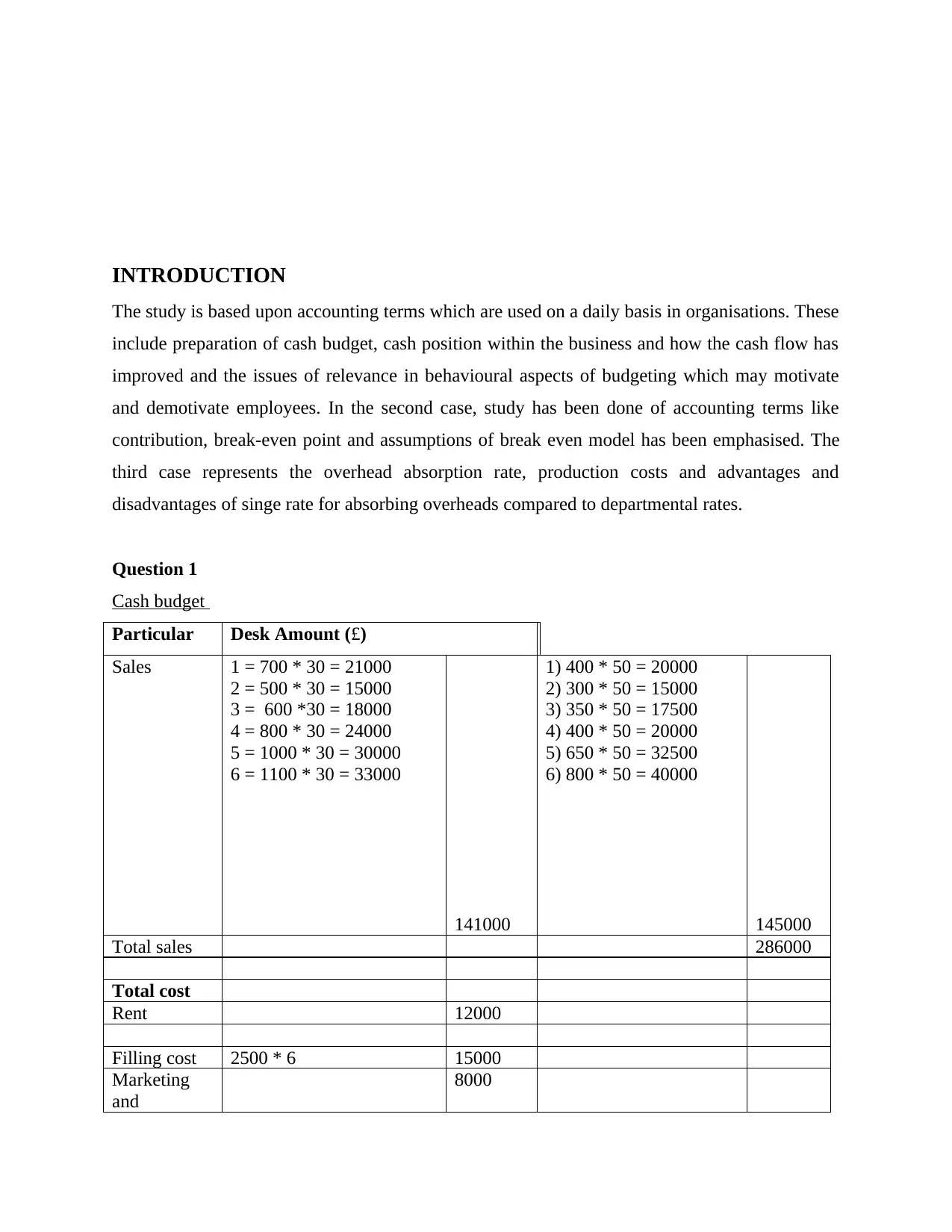

INTRODUCTION

The study is based upon accounting terms which are used on a daily basis in organisations. These

include preparation of cash budget, cash position within the business and how the cash flow has

improved and the issues of relevance in behavioural aspects of budgeting which may motivate

and demotivate employees. In the second case, study has been done of accounting terms like

contribution, break-even point and assumptions of break even model has been emphasised. The

third case represents the overhead absorption rate, production costs and advantages and

disadvantages of singe rate for absorbing overheads compared to departmental rates.

Question 1

Cash budget

Particular Desk Amount (£)

Sales 1 = 700 * 30 = 21000

2 = 500 * 30 = 15000

3 = 600 *30 = 18000

4 = 800 * 30 = 24000

5 = 1000 * 30 = 30000

6 = 1100 * 30 = 33000

141000

1) 400 * 50 = 20000

2) 300 * 50 = 15000

3) 350 * 50 = 17500

4) 400 * 50 = 20000

5) 650 * 50 = 32500

6) 800 * 50 = 40000

145000

Total sales 286000

Total cost

Rent 12000

Filling cost 2500 * 6 15000

Marketing

and

8000

The study is based upon accounting terms which are used on a daily basis in organisations. These

include preparation of cash budget, cash position within the business and how the cash flow has

improved and the issues of relevance in behavioural aspects of budgeting which may motivate

and demotivate employees. In the second case, study has been done of accounting terms like

contribution, break-even point and assumptions of break even model has been emphasised. The

third case represents the overhead absorption rate, production costs and advantages and

disadvantages of singe rate for absorbing overheads compared to departmental rates.

Question 1

Cash budget

Particular Desk Amount (£)

Sales 1 = 700 * 30 = 21000

2 = 500 * 30 = 15000

3 = 600 *30 = 18000

4 = 800 * 30 = 24000

5 = 1000 * 30 = 30000

6 = 1100 * 30 = 33000

141000

1) 400 * 50 = 20000

2) 300 * 50 = 15000

3) 350 * 50 = 17500

4) 400 * 50 = 20000

5) 650 * 50 = 32500

6) 800 * 50 = 40000

145000

Total sales 286000

Total cost

Rent 12000

Filling cost 2500 * 6 15000

Marketing

and

8000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

advertising

cost

Manager

salary

3000 * 6 18000

Insurance

cost

4000

Labor cost 4700 (700 + 500 + 600 +

800 + 1000 + 1100) * 30 /

60 * 12

2900 ( 400 + 300 + 350 +

400 + 650 + 800) * 30 / 60

* 12

28200

17400 102600

Total cost 102600

Cash budget 286000-102600

Cash position of company

The above mentioned cash budget indicate about the expected liquidity situation of

organization. The budget comprises with the expected sales and also the potential amount of

expenditure which organization needed to entertain against operations of company. The above

mentioned cash budget indicate that Woodrock Limited Company hold very strong liquidity

position. The expected sales of company indicate that it could address favorable inflow of cash

revenue in the next six months of business operations and also the revenue of organization could

cover up the potential level of outflow of financial resources of the organization. As the cash

budget mostly indicate the expected cash company will hold against the business operations

channelize by organization (Eschelbach, 2017). The expected amount of sales Woodrock

Limited Company will address in the next six month of tenure is 286000 and the expenditure the

organization will require to incurred is amount to total 102640. The cash balance in between the

income and expenditure is shown the liquidity position of organization that will hold by the

organization. The targeted amount of sales inflow is more than the expected amount of outflow

against the business operations incurred by the organization. Expenditure or the cash outflow

which organization will be addressed summarizes rent, fixed cost, marketing and advertising

cost, manager salary, insurance cost and labor cost. All these cost are different and will entertain

a certain amount of cash outflow. The basic aim behind the formation of cash budget is to

identify the level of cash entity will generate out of the operations it has entertained in the

cost

Manager

salary

3000 * 6 18000

Insurance

cost

4000

Labor cost 4700 (700 + 500 + 600 +

800 + 1000 + 1100) * 30 /

60 * 12

2900 ( 400 + 300 + 350 +

400 + 650 + 800) * 30 / 60

* 12

28200

17400 102600

Total cost 102600

Cash budget 286000-102600

Cash position of company

The above mentioned cash budget indicate about the expected liquidity situation of

organization. The budget comprises with the expected sales and also the potential amount of

expenditure which organization needed to entertain against operations of company. The above

mentioned cash budget indicate that Woodrock Limited Company hold very strong liquidity

position. The expected sales of company indicate that it could address favorable inflow of cash

revenue in the next six months of business operations and also the revenue of organization could

cover up the potential level of outflow of financial resources of the organization. As the cash

budget mostly indicate the expected cash company will hold against the business operations

channelize by organization (Eschelbach, 2017). The expected amount of sales Woodrock

Limited Company will address in the next six month of tenure is 286000 and the expenditure the

organization will require to incurred is amount to total 102640. The cash balance in between the

income and expenditure is shown the liquidity position of organization that will hold by the

organization. The targeted amount of sales inflow is more than the expected amount of outflow

against the business operations incurred by the organization. Expenditure or the cash outflow

which organization will be addressed summarizes rent, fixed cost, marketing and advertising

cost, manager salary, insurance cost and labor cost. All these cost are different and will entertain

a certain amount of cash outflow. The basic aim behind the formation of cash budget is to

identify the level of cash entity will generate out of the operations it has entertained in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization. Projection of cash budget is totally based on the amount of inflow organization will

address in the name of any such particular and also the amount of cash outflow organization will

be required to address in the respective time frame in future on the basis of expected figures will

conclude in the budget. The estimation of cash budget is based on the inflow of cash in

organization and also the outflow of cash organization needed to entertain in order to channelize

the business operations for the respective time frame.

In context to Woodrock Limited Company it can be projected that level of cash inflow in

organization is more than the expected amount of outflow organization needed to address for the

first six month of time frame that indicate that company hold a very strong liquidity or cash

position in business. In the next six month of business operations Woodrock Limited Company

will only consider the inflow of cash in form of sales outcomes of organization. In cash budget

all types of potential inflow organization will witness are included in the budget. In case of

Woodrock Limited Company only the inflow of company for the next six months of doing

business transactions is in form of sales only so only the sales revenue expected for next six

months for both the segment like desk and cabinet are included to identify the level of inflow

organization will address against the business operations entertained by entity. Woodrock

Limited Company can focus over improving the income in from of collection from debtors if any

to boost the cash position of firm in the next six months. Liquidity condition always reflect the

amount of cash organization contain in its bank so that all kind of potential expenditure

organization can bear against the liquidity situation it hold in business (Javed and Zhuquan,

2018). The expected amount of cash outflow which business entity is going to address in the next

six months’ time frame are approximately half the total amount of inflow organization is going

to entertain in against to deliver business operations. Woodrock Limited Company has also

controlled its overall cost incurred in the next six months that also denote that company is

sustaining an effective level of control in between the overall inflow and the outflow which is

expected to be incurred by entity in the next six-month time frame. Some of the cash outflow of

organization can also controlled by organization such as marketing ad advertising cost that is

controllable in nature (Ahmed and Adnan, 2018). If the company control its level of cash

outflow than it will further boost to overall liquidity position of organization as it further boosts

up the cash positon of business entity. On the basis of the overall evaluation about the cash

position of organization it can analysis that Woodrock Limited Company hold very strong

address in the name of any such particular and also the amount of cash outflow organization will

be required to address in the respective time frame in future on the basis of expected figures will

conclude in the budget. The estimation of cash budget is based on the inflow of cash in

organization and also the outflow of cash organization needed to entertain in order to channelize

the business operations for the respective time frame.

In context to Woodrock Limited Company it can be projected that level of cash inflow in

organization is more than the expected amount of outflow organization needed to address for the

first six month of time frame that indicate that company hold a very strong liquidity or cash

position in business. In the next six month of business operations Woodrock Limited Company

will only consider the inflow of cash in form of sales outcomes of organization. In cash budget

all types of potential inflow organization will witness are included in the budget. In case of

Woodrock Limited Company only the inflow of company for the next six months of doing

business transactions is in form of sales only so only the sales revenue expected for next six

months for both the segment like desk and cabinet are included to identify the level of inflow

organization will address against the business operations entertained by entity. Woodrock

Limited Company can focus over improving the income in from of collection from debtors if any

to boost the cash position of firm in the next six months. Liquidity condition always reflect the

amount of cash organization contain in its bank so that all kind of potential expenditure

organization can bear against the liquidity situation it hold in business (Javed and Zhuquan,

2018). The expected amount of cash outflow which business entity is going to address in the next

six months’ time frame are approximately half the total amount of inflow organization is going

to entertain in against to deliver business operations. Woodrock Limited Company has also

controlled its overall cost incurred in the next six months that also denote that company is

sustaining an effective level of control in between the overall inflow and the outflow which is

expected to be incurred by entity in the next six-month time frame. Some of the cash outflow of

organization can also controlled by organization such as marketing ad advertising cost that is

controllable in nature (Ahmed and Adnan, 2018). If the company control its level of cash

outflow than it will further boost to overall liquidity position of organization as it further boosts

up the cash positon of business entity. On the basis of the overall evaluation about the cash

position of organization it can analysis that Woodrock Limited Company hold very strong

liquidity position in against to deliver business operations. Cash and liquidity situation of

organization impact over every single functional direction associated with the company. In the

regular trading activities liquidity situation play strong role in the overall business operations

entertained by the business entity.

The current cash budget indicate that company hold a very strengthened liquidity and

cash position against the business operations delivered by organization. Henceforth, it can be

stated that it ca further boost up the overall liquidity against the business operations entertained

by organization with the support of limiting the overall expected cash outflow against the inflow

of cash in business. Controlling cost is also a key factor that impact over the business operations

which support the entity to deliver business objectives in the most profitable way possible.

Issue of relevance in behavioural aspects of budgeting

Dysfunctional budgeting

When the budget goals are same as manager goals, the budget can increase the positive

behaviour. It is a sort of matching between organisation goals and managerial goals. They are

said to be as goal congruence. This infuses motivation in employees and helps in excelling of

performance. Managers participating in the budget process will also feel motivated to make a fair

budget meeting the organisation's objectives. It happens at times that due to improper

implementation and unreasonable management expectations the reaction of subordinates can

become negative. This causes conflict and interferes with the goals of the organisation (Brink,

Coats and Rankin, 2018).

Participative budgeting: The top management prepares the budget and does not take in

inclusion other subordinates and employees. They do not take their suggestions and there is no

involvement of employee in budget making. There exist communication gap between the

management and subordinates. Employees cannot suggest their grievances regarding lack of

machinery and other facilities directly to the management but only to their line managers. The

subordinates are left out of their creative suggestions to be incorporated in the budget making.

By making a participative approach in budget making, employees feel motivated to voice their

opinions and committed to the organisational objectives. By making employees participate in the

budget making, employees can consider the goals as their own goals and this can increase the

organization impact over every single functional direction associated with the company. In the

regular trading activities liquidity situation play strong role in the overall business operations

entertained by the business entity.

The current cash budget indicate that company hold a very strengthened liquidity and

cash position against the business operations delivered by organization. Henceforth, it can be

stated that it ca further boost up the overall liquidity against the business operations entertained

by organization with the support of limiting the overall expected cash outflow against the inflow

of cash in business. Controlling cost is also a key factor that impact over the business operations

which support the entity to deliver business objectives in the most profitable way possible.

Issue of relevance in behavioural aspects of budgeting

Dysfunctional budgeting

When the budget goals are same as manager goals, the budget can increase the positive

behaviour. It is a sort of matching between organisation goals and managerial goals. They are

said to be as goal congruence. This infuses motivation in employees and helps in excelling of

performance. Managers participating in the budget process will also feel motivated to make a fair

budget meeting the organisation's objectives. It happens at times that due to improper

implementation and unreasonable management expectations the reaction of subordinates can

become negative. This causes conflict and interferes with the goals of the organisation (Brink,

Coats and Rankin, 2018).

Participative budgeting: The top management prepares the budget and does not take in

inclusion other subordinates and employees. They do not take their suggestions and there is no

involvement of employee in budget making. There exist communication gap between the

management and subordinates. Employees cannot suggest their grievances regarding lack of

machinery and other facilities directly to the management but only to their line managers. The

subordinates are left out of their creative suggestions to be incorporated in the budget making.

By making a participative approach in budget making, employees feel motivated to voice their

opinions and committed to the organisational objectives. By making employees participate in the

budget making, employees can consider the goals as their own goals and this can increase the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

morale and performance of the employee. Facilities such as refreshments or just a snooker game

addition can also give a message to the employee that they are being cared for and looked after

well in organisation. When setting targets, the interaction with the employee will help realise the

management whether the targets set are achievable and it will also help in knowing the

perspective of management to the employees.

Budgetary slack: In this approach the managers induce a padding up of budget by under

estimating the revenues and over estimating the costs and resources needed. This is basically

done so because if the budget exceeds the requirement then there is a provision for the same. It

often happens that managers do it in most of the industries in which thee occurs a difference in

allocated resources and actual resources needed. It is seen that they are able to meet their targets

within budget but actually they have crossed the actual requirements and are only saved due to

padding up of resources. This is not a positive sign as it can lead to a misuse of resources.

Managers also do the padding up to generate incentives for completing the targets (Jones, 2017).

Budgetary pressure: Budgets should not induce excessive pressure on the line managers,

subordinates and employees. The budget making should not be too high on restrictions and not

too low also. It should give ample space for the line managers to make its employees function

with available resources and produce desired results. It is necessary to have a balance in goal

setting of budget as this will ease of unnecessary pressure on employees and managers and

motivate them to do better. If the goals can be easily achieved the managers will lose interest and

this will lead to a decrease in motivation and thus decrease performance. The upper level

managers have to be careful in charting out goals and responsibilities to be accomplished by the

managers and their subordinates.

Absence of top management support: There should be participation and cooperation extended

by top management to lower and middle management. It helps in the preparation and execution

of budgets. Top management need to show their commitment in addressing the issues faced by

the low level managers and thus this will motivate them to carry on with their tasks. Planning

and control function will get affected if there is a lack of attention by the top management to

their subordinates.

addition can also give a message to the employee that they are being cared for and looked after

well in organisation. When setting targets, the interaction with the employee will help realise the

management whether the targets set are achievable and it will also help in knowing the

perspective of management to the employees.

Budgetary slack: In this approach the managers induce a padding up of budget by under

estimating the revenues and over estimating the costs and resources needed. This is basically

done so because if the budget exceeds the requirement then there is a provision for the same. It

often happens that managers do it in most of the industries in which thee occurs a difference in

allocated resources and actual resources needed. It is seen that they are able to meet their targets

within budget but actually they have crossed the actual requirements and are only saved due to

padding up of resources. This is not a positive sign as it can lead to a misuse of resources.

Managers also do the padding up to generate incentives for completing the targets (Jones, 2017).

Budgetary pressure: Budgets should not induce excessive pressure on the line managers,

subordinates and employees. The budget making should not be too high on restrictions and not

too low also. It should give ample space for the line managers to make its employees function

with available resources and produce desired results. It is necessary to have a balance in goal

setting of budget as this will ease of unnecessary pressure on employees and managers and

motivate them to do better. If the goals can be easily achieved the managers will lose interest and

this will lead to a decrease in motivation and thus decrease performance. The upper level

managers have to be careful in charting out goals and responsibilities to be accomplished by the

managers and their subordinates.

Absence of top management support: There should be participation and cooperation extended

by top management to lower and middle management. It helps in the preparation and execution

of budgets. Top management need to show their commitment in addressing the issues faced by

the low level managers and thus this will motivate them to carry on with their tasks. Planning

and control function will get affected if there is a lack of attention by the top management to

their subordinates.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Q2. a) Revenue generated= 13*53000=689000

Direct cost per unit= Materials+ Labour+Variable overheads=5.25+2.95+1.85=10.05

Total direct costs=10.05*53000=532650

Contribution=689000-532650=156350

Contribution can be defined as the total direct costs subtracted from revenues which can

also be said to cover the fixed costs the business incurs during a reporting period. An excess of

money earned over direct costs denotes contribution.

b) Break even point (units)= Total Fixed costs/ Revenue per individual unit-Variable costs per

individual unit= 59000+47600/13-10.05=36135.59

Break even point (sales)= 36135.59*13=469762.67

Margin of safety(sales)= Current sales-Break even sales=689000-469762.67=219237.33

Margin of Safety(units)=Current sales per units-Break even point=53000-36135.59=16864.41

c)Profit=53000*13-53000*10.05=156350

Profit after fixed cost expenses=156350-(59000+47600)=49750

d)Profit=90000

Let x denote the total required units.

X(13-10.05)=90000

2.95x=90000

x=90000/2.95=30508.

e) Let selling price be x.

Profit=53000*x-53000*10.05

90000=53000(x-10.05)

90000/53000=x-10.05

x=11.74

f) The sales price currently=13

desired increase=9/100*13=1.17

Direct cost per unit= Materials+ Labour+Variable overheads=5.25+2.95+1.85=10.05

Total direct costs=10.05*53000=532650

Contribution=689000-532650=156350

Contribution can be defined as the total direct costs subtracted from revenues which can

also be said to cover the fixed costs the business incurs during a reporting period. An excess of

money earned over direct costs denotes contribution.

b) Break even point (units)= Total Fixed costs/ Revenue per individual unit-Variable costs per

individual unit= 59000+47600/13-10.05=36135.59

Break even point (sales)= 36135.59*13=469762.67

Margin of safety(sales)= Current sales-Break even sales=689000-469762.67=219237.33

Margin of Safety(units)=Current sales per units-Break even point=53000-36135.59=16864.41

c)Profit=53000*13-53000*10.05=156350

Profit after fixed cost expenses=156350-(59000+47600)=49750

d)Profit=90000

Let x denote the total required units.

X(13-10.05)=90000

2.95x=90000

x=90000/2.95=30508.

e) Let selling price be x.

Profit=53000*x-53000*10.05

90000=53000(x-10.05)

90000/53000=x-10.05

x=11.74

f) The sales price currently=13

desired increase=9/100*13=1.17

new sale price=13+1.17=14.17

sales revenue increase estimated=17/100*689000=117130.

New sales revenue=117130+689000=806130.

Profit after advertising deduction=53000*14.17- 53000*10.05-45000=173360

Earlier profit=156350.

It can be a good strategy for the company to focus on advertising expenditure and increasing

sales rate by 9%. It will increase the profit even after deducting advertising expenses.

g) Assumptions to the Break even model

The fixed costs are assumed to be constant at all output levels.

The costs have to be taken as fixed or variable costs.

The cost and revenue functions are taken as linear.

The model assumes constant rate of increase in variable cost (Calabrò , 2017).

The factor price is taken to be constant. Factors are anticipated revenue and costs of

doing business.

It is assumed that changes in input prices such as material, wages, rent and advertisement

can be ruled out.

The sales price per unit is taken to be constant throughout the output level.

The business is assumed to have a constant product mix and produces one kind of

product.

Inventory is assumed to be constant at the start and end of the accounting period.

Costs and sales revenue is affected only by sales volume.

Unit variable cost is taken as constant as the change in total variable cost ids considered

to be proportionate at output level.

Factors such as efficiency, production and technology are not prone to change (Morano

and Tajani, 2017).

sales revenue increase estimated=17/100*689000=117130.

New sales revenue=117130+689000=806130.

Profit after advertising deduction=53000*14.17- 53000*10.05-45000=173360

Earlier profit=156350.

It can be a good strategy for the company to focus on advertising expenditure and increasing

sales rate by 9%. It will increase the profit even after deducting advertising expenses.

g) Assumptions to the Break even model

The fixed costs are assumed to be constant at all output levels.

The costs have to be taken as fixed or variable costs.

The cost and revenue functions are taken as linear.

The model assumes constant rate of increase in variable cost (Calabrò , 2017).

The factor price is taken to be constant. Factors are anticipated revenue and costs of

doing business.

It is assumed that changes in input prices such as material, wages, rent and advertisement

can be ruled out.

The sales price per unit is taken to be constant throughout the output level.

The business is assumed to have a constant product mix and produces one kind of

product.

Inventory is assumed to be constant at the start and end of the accounting period.

Costs and sales revenue is affected only by sales volume.

Unit variable cost is taken as constant as the change in total variable cost ids considered

to be proportionate at output level.

Factors such as efficiency, production and technology are not prone to change (Morano

and Tajani, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

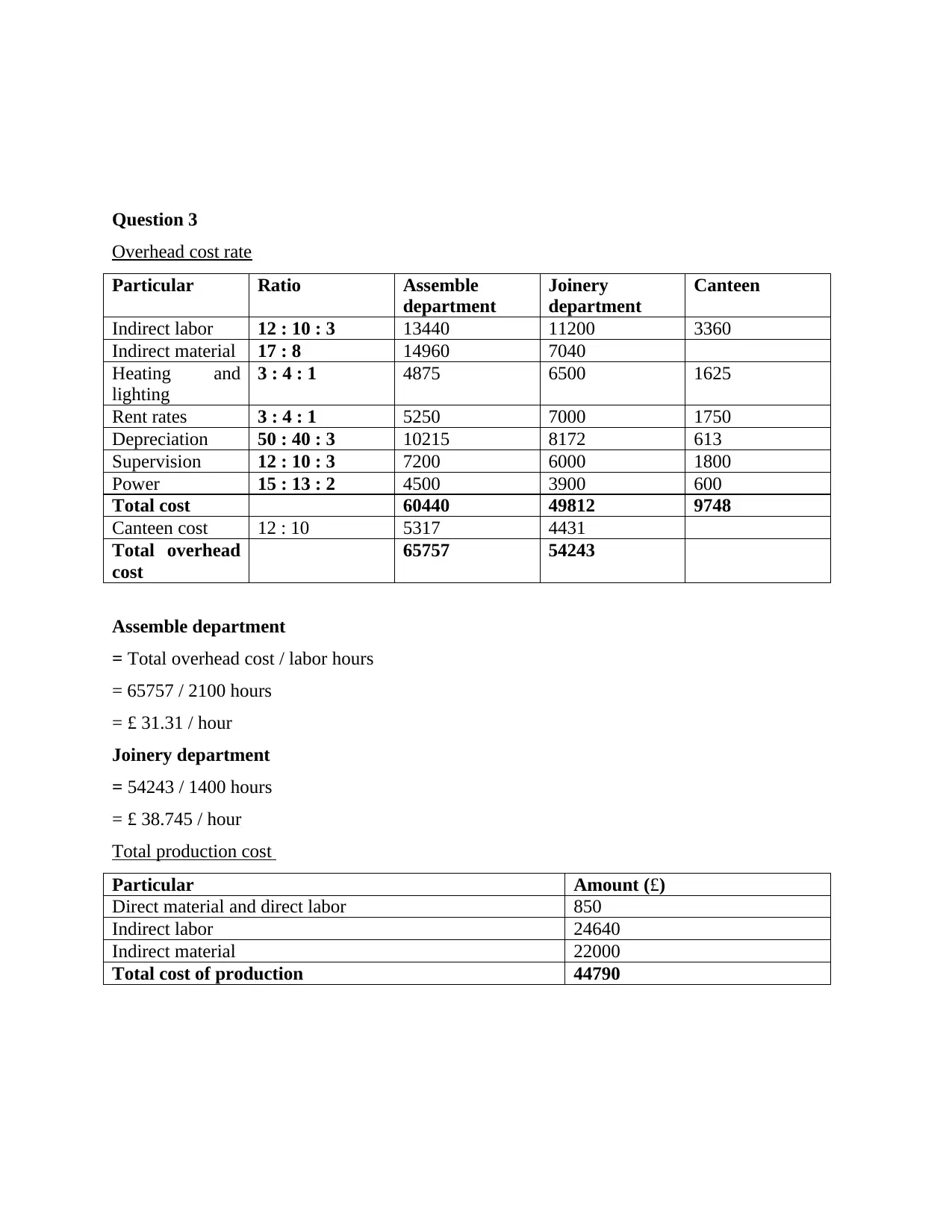

Question 3

Overhead cost rate

Particular Ratio Assemble

department

Joinery

department

Canteen

Indirect labor 12 : 10 : 3 13440 11200 3360

Indirect material 17 : 8 14960 7040

Heating and

lighting

3 : 4 : 1 4875 6500 1625

Rent rates 3 : 4 : 1 5250 7000 1750

Depreciation 50 : 40 : 3 10215 8172 613

Supervision 12 : 10 : 3 7200 6000 1800

Power 15 : 13 : 2 4500 3900 600

Total cost 60440 49812 9748

Canteen cost 12 : 10 5317 4431

Total overhead

cost

65757 54243

Assemble department

= Total overhead cost / labor hours

= 65757 / 2100 hours

= £ 31.31 / hour

Joinery department

= 54243 / 1400 hours

= £ 38.745 / hour

Total production cost

Particular Amount (£)

Direct material and direct labor 850

Indirect labor 24640

Indirect material 22000

Total cost of production 44790

Overhead cost rate

Particular Ratio Assemble

department

Joinery

department

Canteen

Indirect labor 12 : 10 : 3 13440 11200 3360

Indirect material 17 : 8 14960 7040

Heating and

lighting

3 : 4 : 1 4875 6500 1625

Rent rates 3 : 4 : 1 5250 7000 1750

Depreciation 50 : 40 : 3 10215 8172 613

Supervision 12 : 10 : 3 7200 6000 1800

Power 15 : 13 : 2 4500 3900 600

Total cost 60440 49812 9748

Canteen cost 12 : 10 5317 4431

Total overhead

cost

65757 54243

Assemble department

= Total overhead cost / labor hours

= 65757 / 2100 hours

= £ 31.31 / hour

Joinery department

= 54243 / 1400 hours

= £ 38.745 / hour

Total production cost

Particular Amount (£)

Direct material and direct labor 850

Indirect labor 24640

Indirect material 22000

Total cost of production 44790

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage and disadvantage of single absorbing rate

Single rate of absorbing rate indicates about utilizing same rate for absorbing different

overhead cost in organization. Advantage and disadvantage associated with utilizing single rate

of absorbing can be demonstrated in the following points.

Advantage of using single absorbing rate

There are several advantage cater if the overhead cost is absorbed on the basis of single

rate of overhead. It enables the management to absorb overhead cost immediately after the

production of good in organization. This technique provide opportunity for absorbing overhead

cost immediately irrespective of the level of business entity. This method favors the immediate

treatment of overhead cost in the accounting books. This is the key advantage associated with the

overhead cost of production where the accountant and production manager do not require to face

any confusion in absorbing the overall overhead cost and also in calculating the total production

cost of good produced in the organization. It further makes it easier for the entity to calculate the

total per unit cost of overhead. By segregating the total overhead cost incurred the per unit cost

of overhead is calculated by the business entity (Gamkrelidze and Japaridze, 2020). It also

provides the scope of segregating cost over an even basis as compare to other tactics of

absorbing overhead cost of production of the organization. All the advantage demonstrated are

among the key and primary advantage against the overhead cost of producing the total unit in the

organization. This technique makes it more simple to crate and identify the total production cost

and also to determine the selling price of the per unit product. It also clears all the doubts and

issues related to charging overhead cost of production in the industry.

The disadvantages of using single rate for overhead absorption are:

It is hard to know which of the cost centres is consuming the money allocated. It does not give a

specific allocation of resources being allocated to different sections as is in the case of

departmental rate of costing (Argade, S.L., 2020).

It is not suitable for a factory where there are a number of departments and jobs are not spending

equal amount of time in each department. In some of the cases, the jobs or units do not pass

through all the departments in the factory. Comparing to departmental rates, it is applied to the

jobs or units depending on the time spent in each department instead of single overhead

absorption rate. The single overhead rate can be applied in factories where only one major

product is treated on continuous basis.

Single rate of absorbing rate indicates about utilizing same rate for absorbing different

overhead cost in organization. Advantage and disadvantage associated with utilizing single rate

of absorbing can be demonstrated in the following points.

Advantage of using single absorbing rate

There are several advantage cater if the overhead cost is absorbed on the basis of single

rate of overhead. It enables the management to absorb overhead cost immediately after the

production of good in organization. This technique provide opportunity for absorbing overhead

cost immediately irrespective of the level of business entity. This method favors the immediate

treatment of overhead cost in the accounting books. This is the key advantage associated with the

overhead cost of production where the accountant and production manager do not require to face

any confusion in absorbing the overall overhead cost and also in calculating the total production

cost of good produced in the organization. It further makes it easier for the entity to calculate the

total per unit cost of overhead. By segregating the total overhead cost incurred the per unit cost

of overhead is calculated by the business entity (Gamkrelidze and Japaridze, 2020). It also

provides the scope of segregating cost over an even basis as compare to other tactics of

absorbing overhead cost of production of the organization. All the advantage demonstrated are

among the key and primary advantage against the overhead cost of producing the total unit in the

organization. This technique makes it more simple to crate and identify the total production cost

and also to determine the selling price of the per unit product. It also clears all the doubts and

issues related to charging overhead cost of production in the industry.

The disadvantages of using single rate for overhead absorption are:

It is hard to know which of the cost centres is consuming the money allocated. It does not give a

specific allocation of resources being allocated to different sections as is in the case of

departmental rate of costing (Argade, S.L., 2020).

It is not suitable for a factory where there are a number of departments and jobs are not spending

equal amount of time in each department. In some of the cases, the jobs or units do not pass

through all the departments in the factory. Comparing to departmental rates, it is applied to the

jobs or units depending on the time spent in each department instead of single overhead

absorption rate. The single overhead rate can be applied in factories where only one major

product is treated on continuous basis.

CONCLUSION

To conclude the study, it can be said that analysis of the accounting terms leads to an

understanding of their prominence and their utility in decision-making. The cash budget

relevance for the company has been illustrated and apart from this cash flow prominence in

maintenance of working capital has been highlighted. The budget issues relating to management

and its influence on the employees and other low level managers has been discussed. The break

even analysis and its assumptions regarding various key factors have been discussed with

company's approach of using advertising and increasing revenue. The overhead costs were

numerically illustrated and merits and demerits of single rate use in organisations for calculating

absorption rates were discussed.

To conclude the study, it can be said that analysis of the accounting terms leads to an

understanding of their prominence and their utility in decision-making. The cash budget

relevance for the company has been illustrated and apart from this cash flow prominence in

maintenance of working capital has been highlighted. The budget issues relating to management

and its influence on the employees and other low level managers has been discussed. The break

even analysis and its assumptions regarding various key factors have been discussed with

company's approach of using advertising and increasing revenue. The overhead costs were

numerically illustrated and merits and demerits of single rate use in organisations for calculating

absorption rates were discussed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.