Business Accounting: Journals, Ledgers, and Financial Statements

VerifiedAdded on 2020/12/09

|19

|4416

|485

Homework Assignment

AI Summary

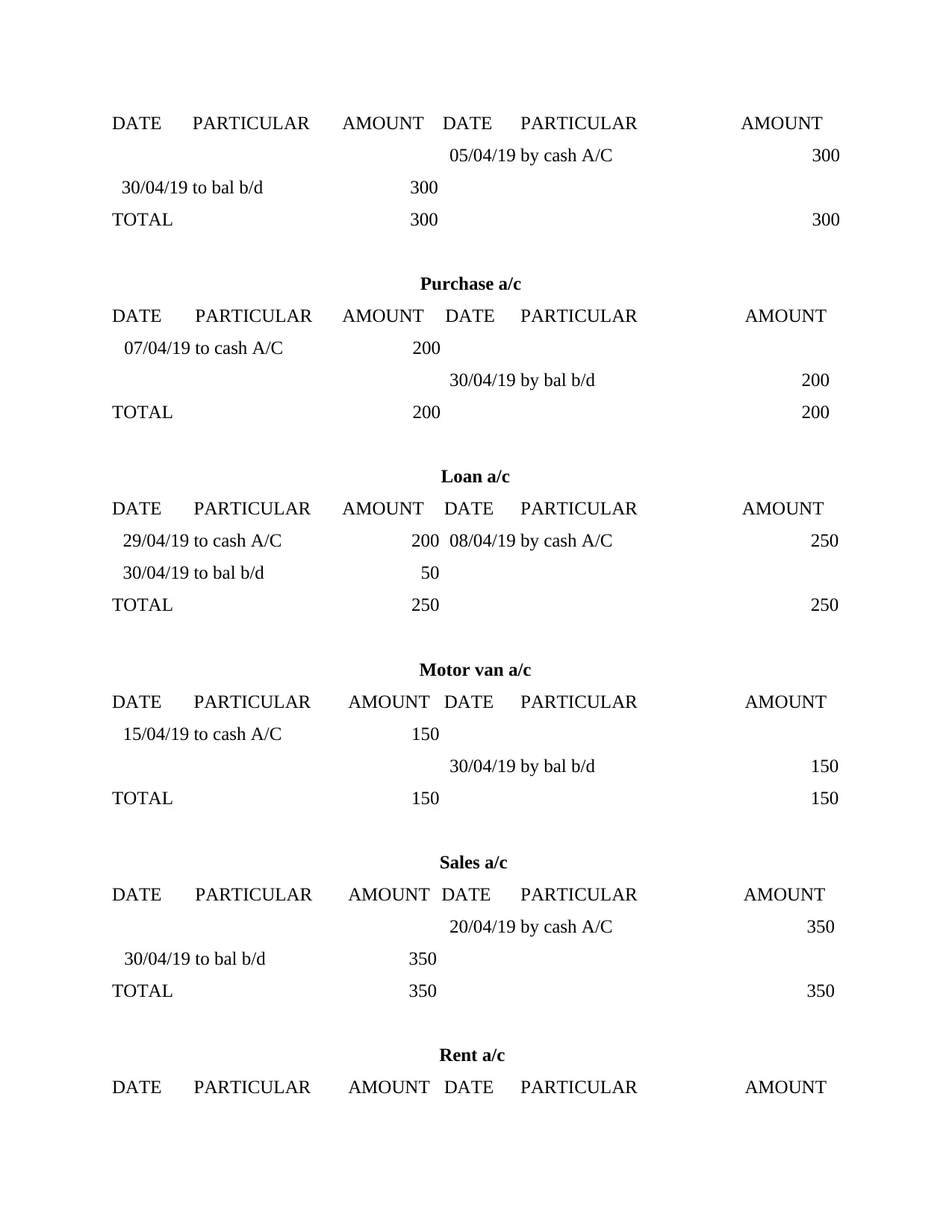

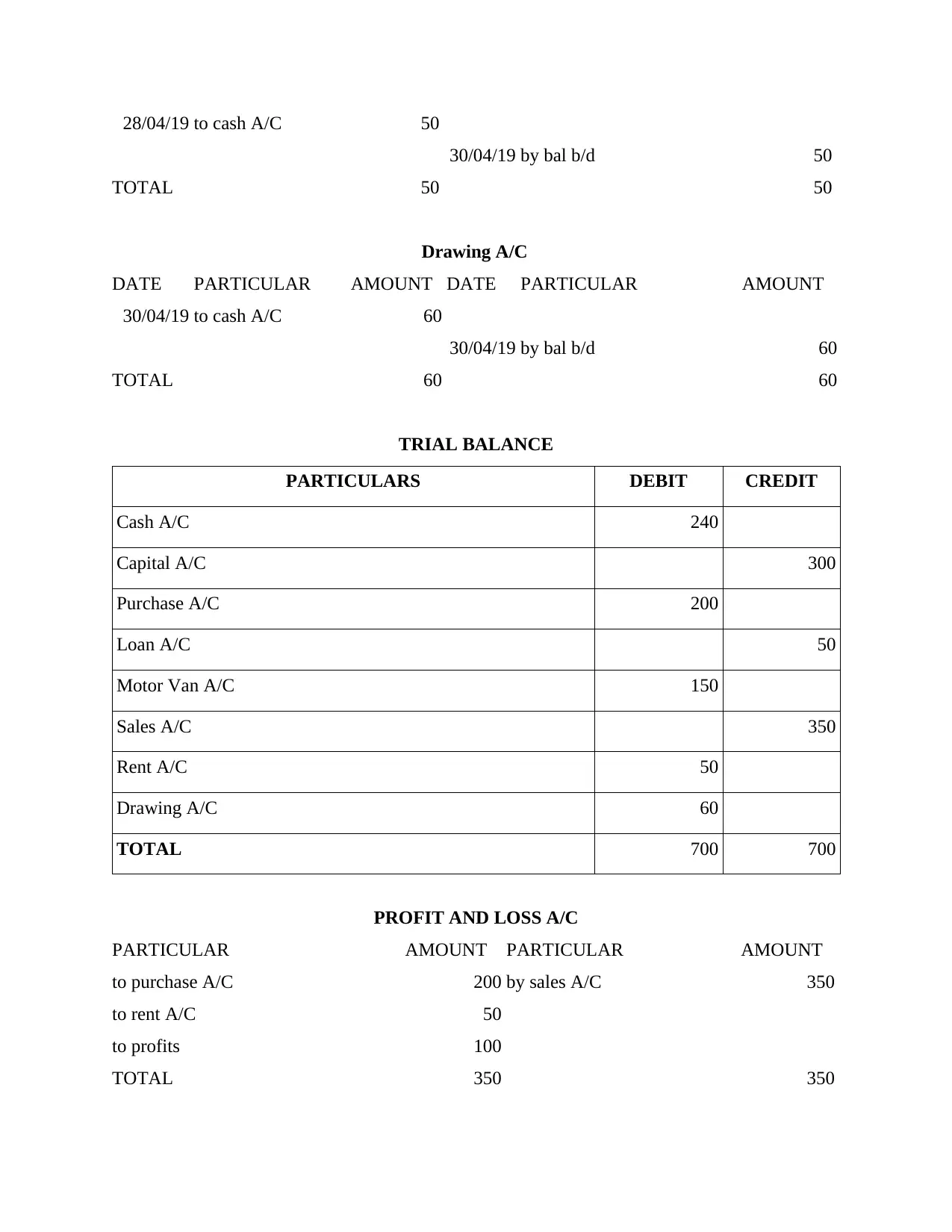

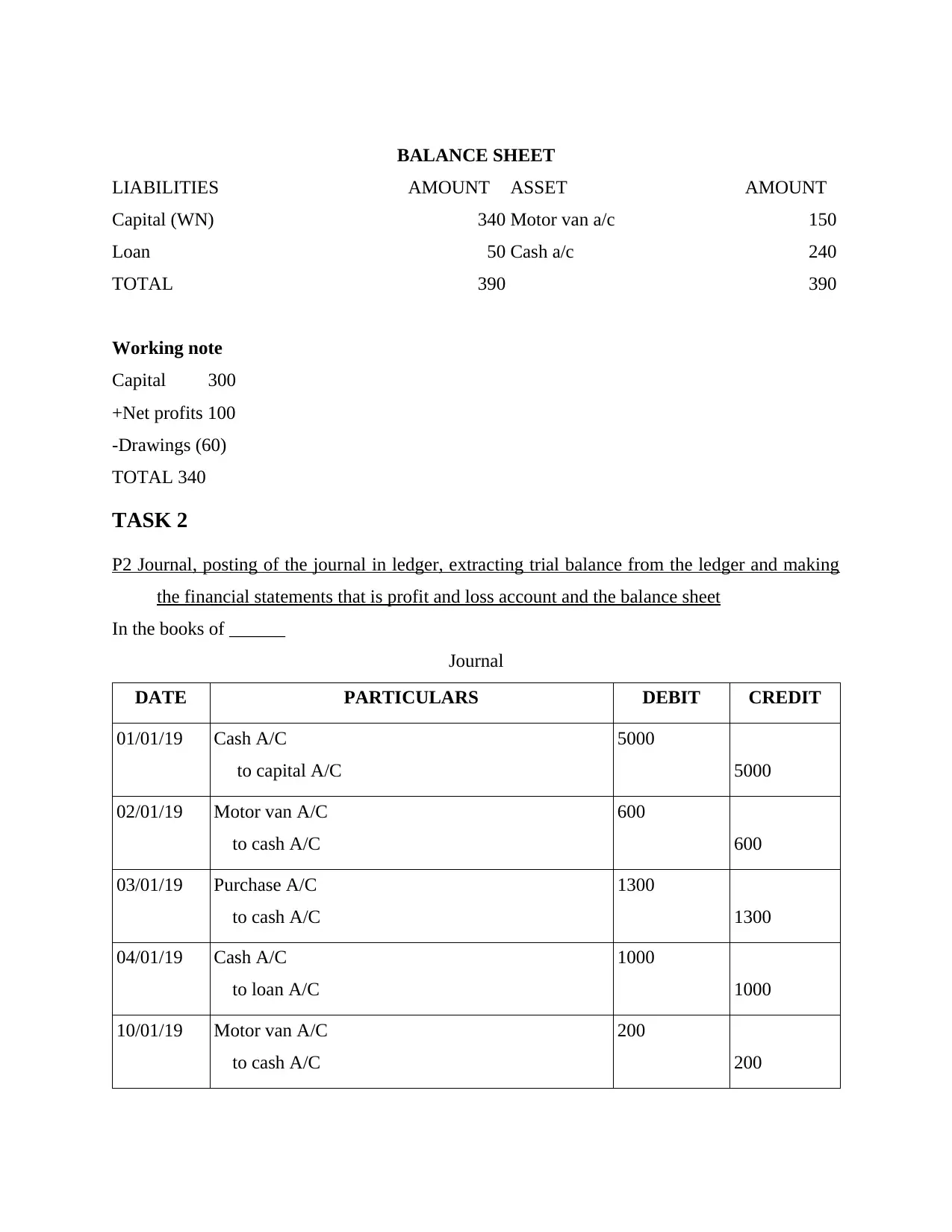

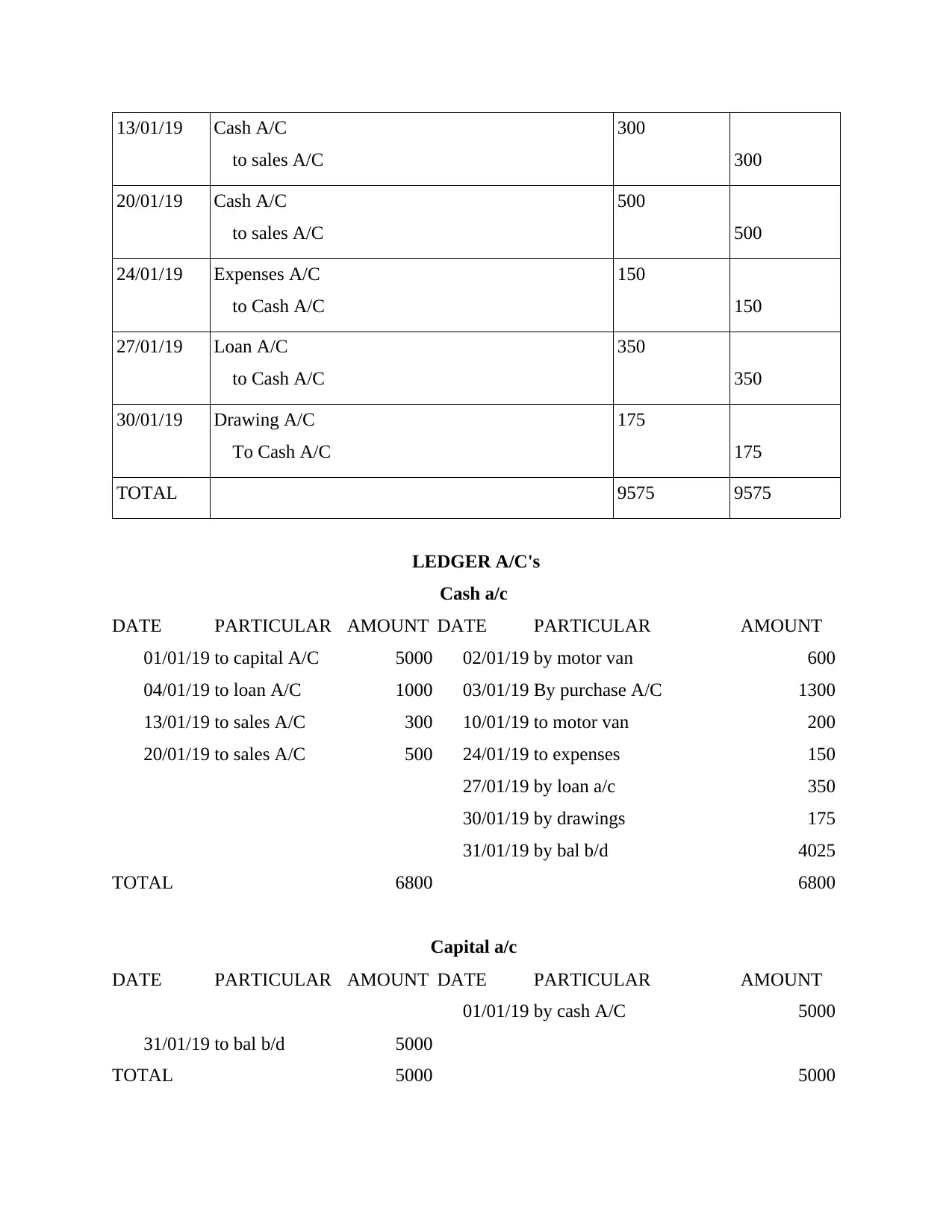

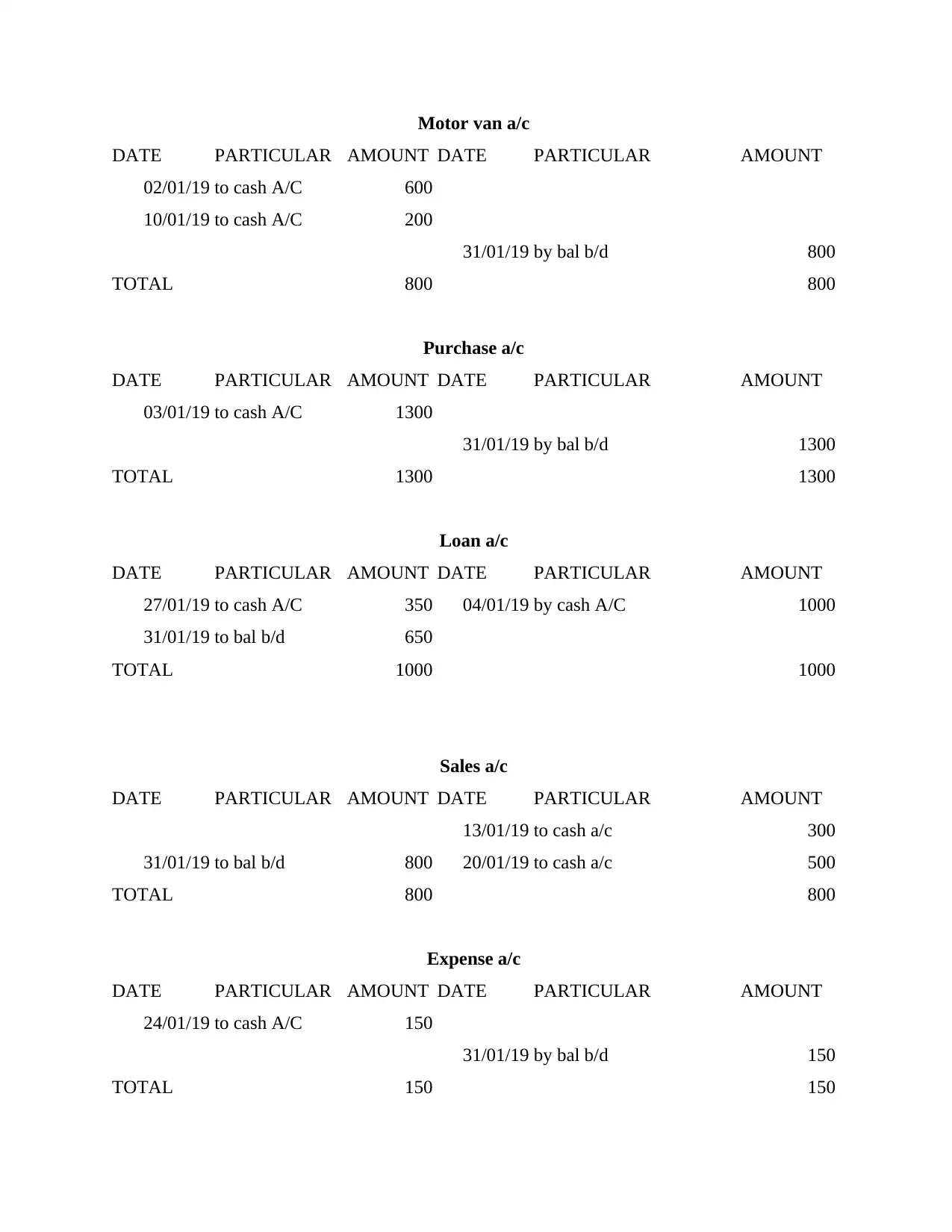

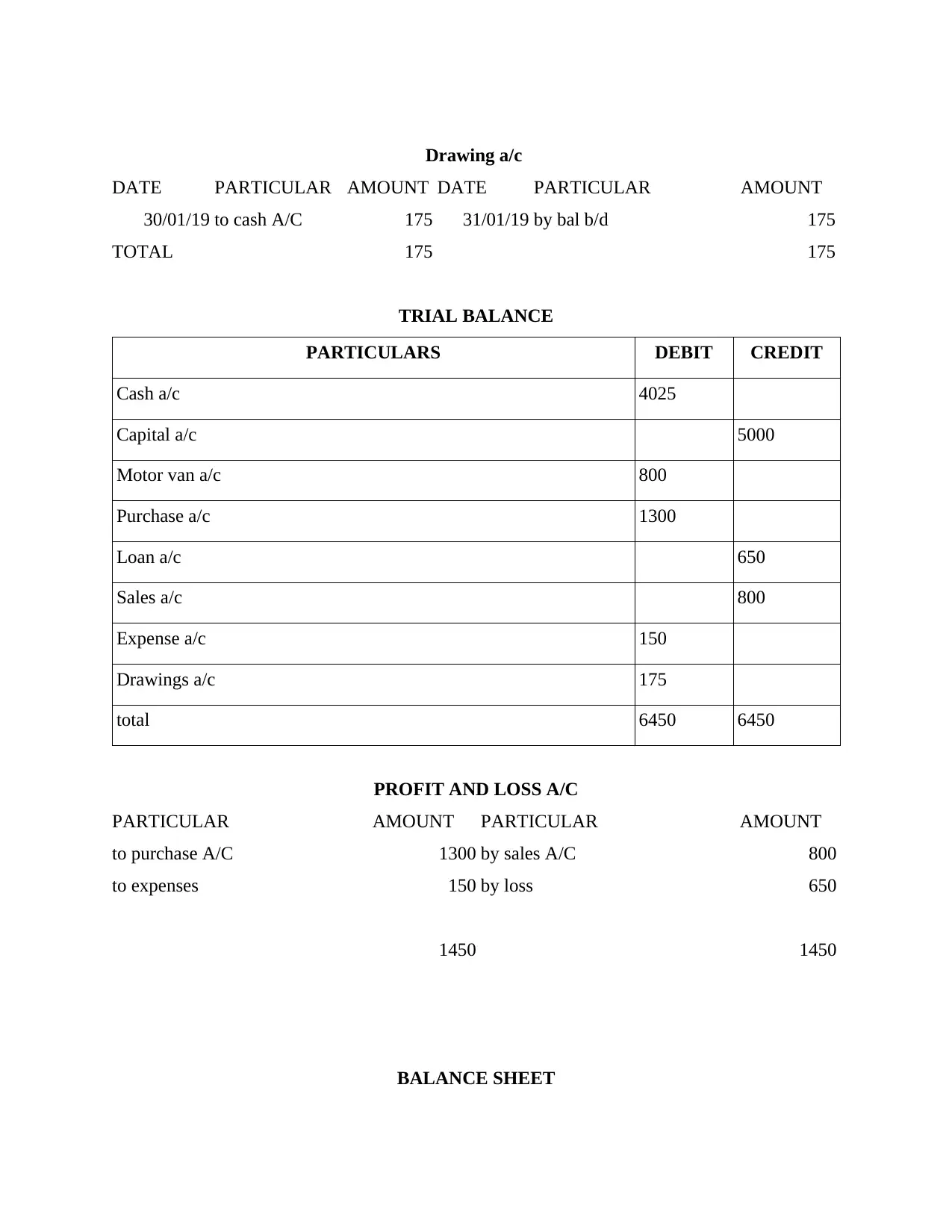

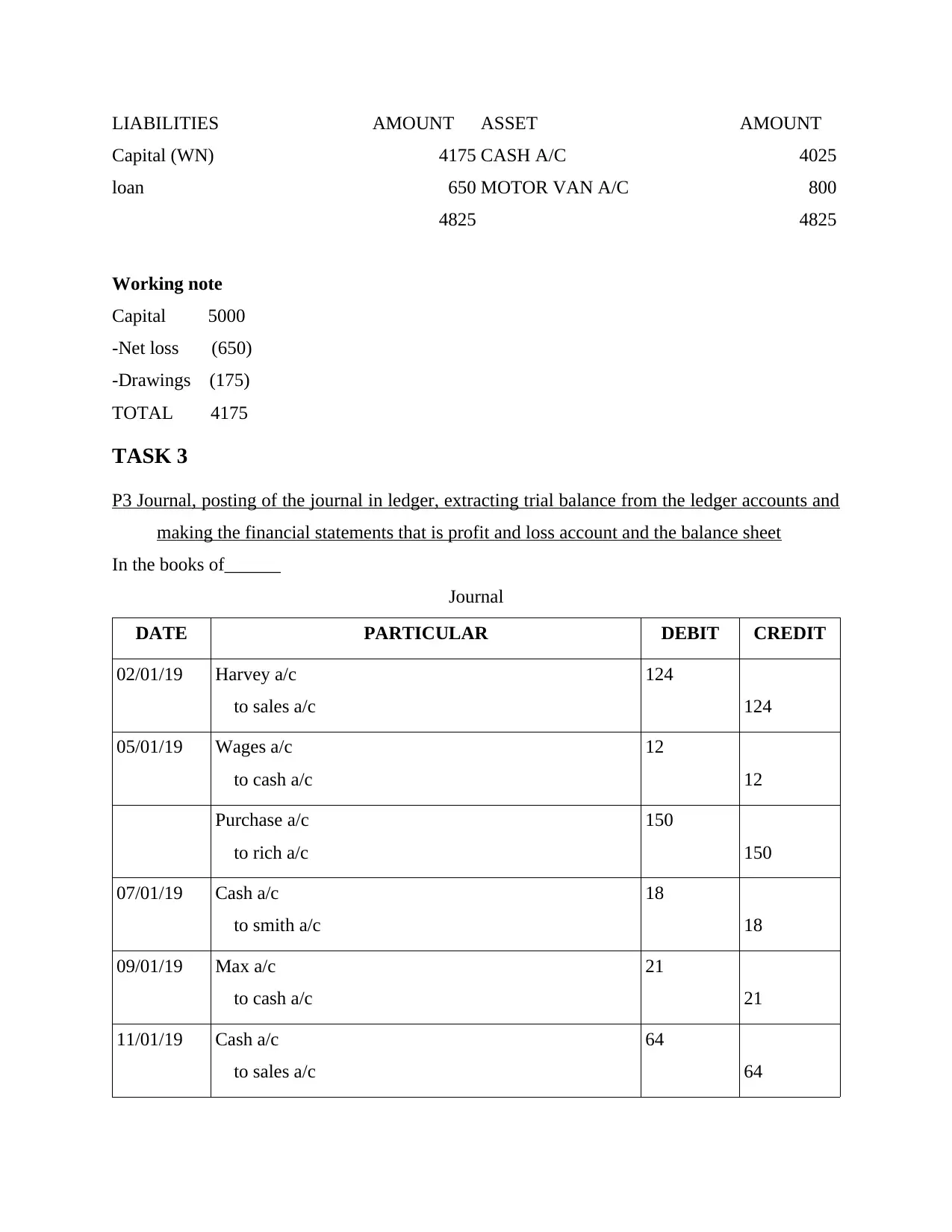

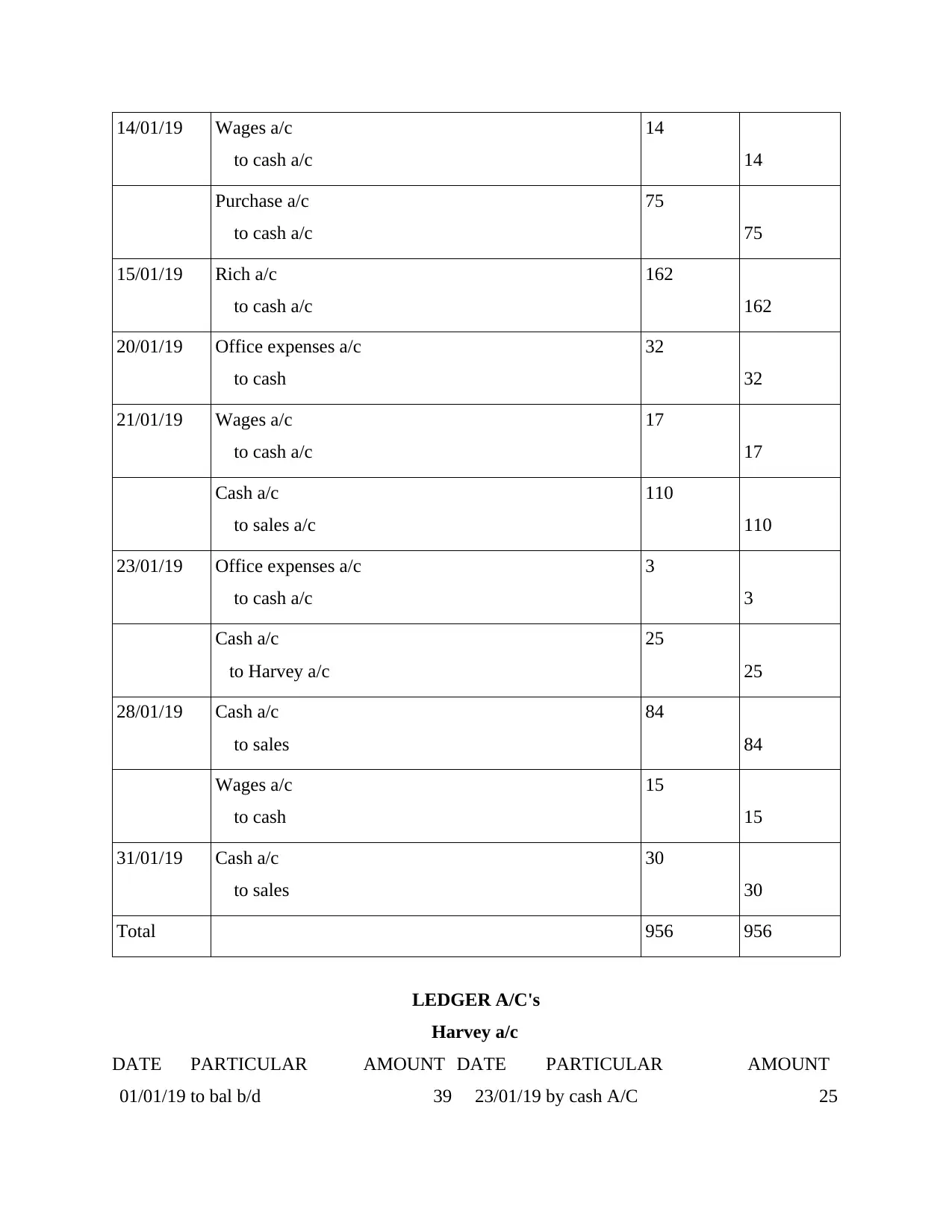

This document provides a comprehensive overview of fundamental accounting principles and practices. It details the process of recording financial transactions in journals, posting them to ledgers, and extracting trial balances. The assignment further demonstrates the creation of key financial statements, including the profit and loss account and the balance sheet, using the trial balance data. The content covers various accounting tasks across multiple scenarios, including the differences between capital and revenue expenditures, providing a practical understanding of accounting procedures. This assignment is a valuable resource for students learning the core concepts of accounting and financial statement analysis, offering practical examples and detailed explanations of each step involved in the accounting cycle.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.