Business Maths and Statistics | Assignment

VerifiedAdded on 2022/09/09

|9

|1221

|26

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS MATHS AND STATISTICS 1

BUSINESS MATHS AND STATISTICS

BUSINESS MATHS AND STATISTICS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Running head: BUSINESS MATHS AND STATISTICS

Table of Contents

PART A...........................................................................................................................................3

A).................................................................................................................................................3

B), C), D).....................................................................................................................................3

E)..................................................................................................................................................3

3)..................................................................................................................................................3

4)..................................................................................................................................................4

Part B...............................................................................................................................................5

1)..................................................................................................................................................5

2)..................................................................................................................................................5

3)..................................................................................................................................................5

4)..................................................................................................................................................6

a)...............................................................................................................................................6

c)...............................................................................................................................................6

d)...............................................................................................................................................6

5)..................................................................................................................................................7

6)..................................................................................................................................................7

References........................................................................................................................................9

Table of Contents

PART A...........................................................................................................................................3

A).................................................................................................................................................3

B), C), D).....................................................................................................................................3

E)..................................................................................................................................................3

3)..................................................................................................................................................3

4)..................................................................................................................................................4

Part B...............................................................................................................................................5

1)..................................................................................................................................................5

2)..................................................................................................................................................5

3)..................................................................................................................................................5

4)..................................................................................................................................................6

a)...............................................................................................................................................6

c)...............................................................................................................................................6

d)...............................................................................................................................................6

5)..................................................................................................................................................7

6)..................................................................................................................................................7

References........................................................................................................................................9

Running head: BUSINESS MATHS AND STATISTICS

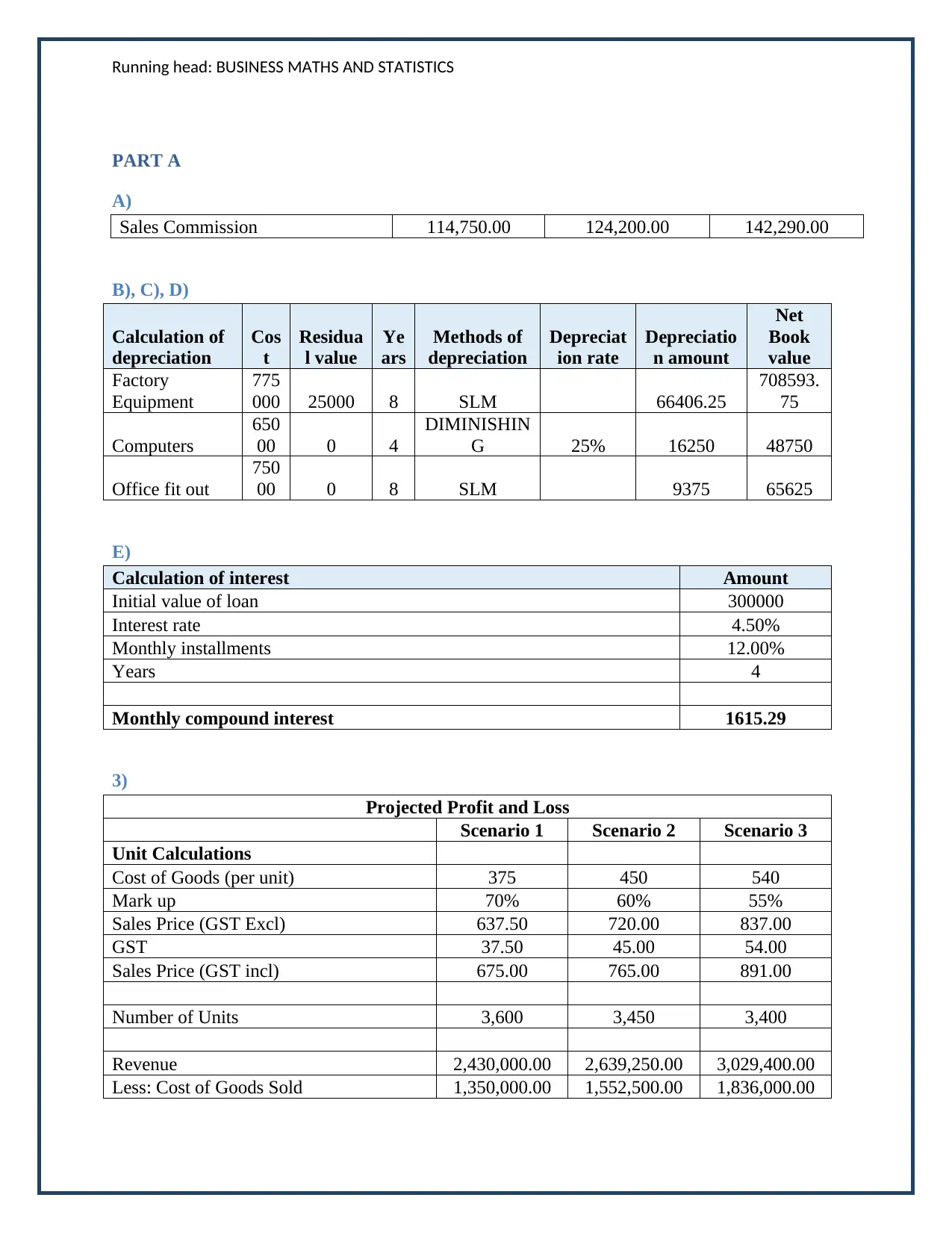

PART A

A)

Sales Commission 114,750.00 124,200.00 142,290.00

B), C), D)

Calculation of

depreciation

Cos

t

Residua

l value

Ye

ars

Methods of

depreciation

Depreciat

ion rate

Depreciatio

n amount

Net

Book

value

Factory

Equipment

775

000 25000 8 SLM 66406.25

708593.

75

Computers

650

00 0 4

DIMINISHIN

G 25% 16250 48750

Office fit out

750

00 0 8 SLM 9375 65625

E)

Calculation of interest Amount

Initial value of loan 300000

Interest rate 4.50%

Monthly installments 12.00%

Years 4

Monthly compound interest 1615.29

3)

Projected Profit and Loss

Scenario 1 Scenario 2 Scenario 3

Unit Calculations

Cost of Goods (per unit) 375 450 540

Mark up 70% 60% 55%

Sales Price (GST Excl) 637.50 720.00 837.00

GST 37.50 45.00 54.00

Sales Price (GST incl) 675.00 765.00 891.00

Number of Units 3,600 3,450 3,400

Revenue 2,430,000.00 2,639,250.00 3,029,400.00

Less: Cost of Goods Sold 1,350,000.00 1,552,500.00 1,836,000.00

PART A

A)

Sales Commission 114,750.00 124,200.00 142,290.00

B), C), D)

Calculation of

depreciation

Cos

t

Residua

l value

Ye

ars

Methods of

depreciation

Depreciat

ion rate

Depreciatio

n amount

Net

Book

value

Factory

Equipment

775

000 25000 8 SLM 66406.25

708593.

75

Computers

650

00 0 4

DIMINISHIN

G 25% 16250 48750

Office fit out

750

00 0 8 SLM 9375 65625

E)

Calculation of interest Amount

Initial value of loan 300000

Interest rate 4.50%

Monthly installments 12.00%

Years 4

Monthly compound interest 1615.29

3)

Projected Profit and Loss

Scenario 1 Scenario 2 Scenario 3

Unit Calculations

Cost of Goods (per unit) 375 450 540

Mark up 70% 60% 55%

Sales Price (GST Excl) 637.50 720.00 837.00

GST 37.50 45.00 54.00

Sales Price (GST incl) 675.00 765.00 891.00

Number of Units 3,600 3,450 3,400

Revenue 2,430,000.00 2,639,250.00 3,029,400.00

Less: Cost of Goods Sold 1,350,000.00 1,552,500.00 1,836,000.00

Running head: BUSINESS MATHS AND STATISTICS

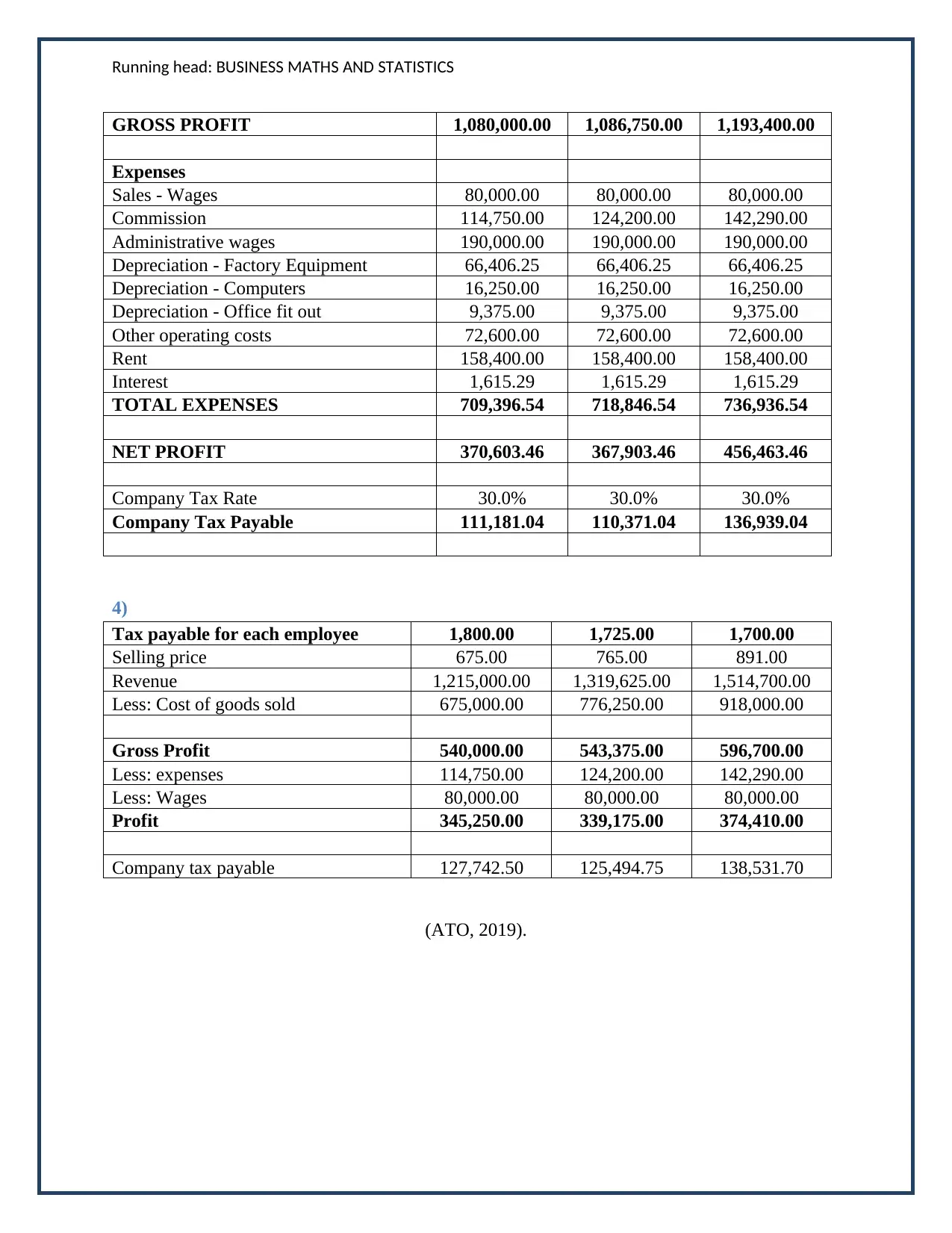

GROSS PROFIT 1,080,000.00 1,086,750.00 1,193,400.00

Expenses

Sales - Wages 80,000.00 80,000.00 80,000.00

Commission 114,750.00 124,200.00 142,290.00

Administrative wages 190,000.00 190,000.00 190,000.00

Depreciation - Factory Equipment 66,406.25 66,406.25 66,406.25

Depreciation - Computers 16,250.00 16,250.00 16,250.00

Depreciation - Office fit out 9,375.00 9,375.00 9,375.00

Other operating costs 72,600.00 72,600.00 72,600.00

Rent 158,400.00 158,400.00 158,400.00

Interest 1,615.29 1,615.29 1,615.29

TOTAL EXPENSES 709,396.54 718,846.54 736,936.54

NET PROFIT 370,603.46 367,903.46 456,463.46

Company Tax Rate 30.0% 30.0% 30.0%

Company Tax Payable 111,181.04 110,371.04 136,939.04

4)

Tax payable for each employee 1,800.00 1,725.00 1,700.00

Selling price 675.00 765.00 891.00

Revenue 1,215,000.00 1,319,625.00 1,514,700.00

Less: Cost of goods sold 675,000.00 776,250.00 918,000.00

Gross Profit 540,000.00 543,375.00 596,700.00

Less: expenses 114,750.00 124,200.00 142,290.00

Less: Wages 80,000.00 80,000.00 80,000.00

Profit 345,250.00 339,175.00 374,410.00

Company tax payable 127,742.50 125,494.75 138,531.70

(ATO, 2019).

GROSS PROFIT 1,080,000.00 1,086,750.00 1,193,400.00

Expenses

Sales - Wages 80,000.00 80,000.00 80,000.00

Commission 114,750.00 124,200.00 142,290.00

Administrative wages 190,000.00 190,000.00 190,000.00

Depreciation - Factory Equipment 66,406.25 66,406.25 66,406.25

Depreciation - Computers 16,250.00 16,250.00 16,250.00

Depreciation - Office fit out 9,375.00 9,375.00 9,375.00

Other operating costs 72,600.00 72,600.00 72,600.00

Rent 158,400.00 158,400.00 158,400.00

Interest 1,615.29 1,615.29 1,615.29

TOTAL EXPENSES 709,396.54 718,846.54 736,936.54

NET PROFIT 370,603.46 367,903.46 456,463.46

Company Tax Rate 30.0% 30.0% 30.0%

Company Tax Payable 111,181.04 110,371.04 136,939.04

4)

Tax payable for each employee 1,800.00 1,725.00 1,700.00

Selling price 675.00 765.00 891.00

Revenue 1,215,000.00 1,319,625.00 1,514,700.00

Less: Cost of goods sold 675,000.00 776,250.00 918,000.00

Gross Profit 540,000.00 543,375.00 596,700.00

Less: expenses 114,750.00 124,200.00 142,290.00

Less: Wages 80,000.00 80,000.00 80,000.00

Profit 345,250.00 339,175.00 374,410.00

Company tax payable 127,742.50 125,494.75 138,531.70

(ATO, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Running head: BUSINESS MATHS AND STATISTICS

Part B

1)

Profit plays a vital role while choosing the best alternative and hence, if the profit is highest it

determines that the company is able to pay to its investors and the shareholders. The scenario

that shall be selected is the Scenario C as the net profit is the highest and thereafter the profit

after giving the tax component is also highest at $319524.42. Despite having the same rate of tax

at 30%, the highest tax is paid under Scenario C and at the same time, the highest profit is also

acquired under scenario C.

2)

The major variance that can be observed between the scenarios, are in terms of the commission

as there is a difference in the number of sales units. As per the table it can be seen that in

Scenario 1, the sales have been made for only 3600 units, whereas in scenario B, the sales have

been made were 3450 units and 3400 units in Scenario C respectively. Further the sales price

inclusive GST has also been higher than the above two at $891 per product (Robinson, et al

2015).

3)

The straight line method of the depreciation is a method under which the fixed asset is

depreciated over the useful life of an asset after deducting the salvage value, whereas in case of

the diminishing method, the depreciation is calculating on the book value which arrives after

deducting the depreciation. The same can be found in the case study on account of example,

where factory equipment’s depreciation is calculated on SLM basis and the depreciation on

computer is calculated on diminishing vale method.

Part B

1)

Profit plays a vital role while choosing the best alternative and hence, if the profit is highest it

determines that the company is able to pay to its investors and the shareholders. The scenario

that shall be selected is the Scenario C as the net profit is the highest and thereafter the profit

after giving the tax component is also highest at $319524.42. Despite having the same rate of tax

at 30%, the highest tax is paid under Scenario C and at the same time, the highest profit is also

acquired under scenario C.

2)

The major variance that can be observed between the scenarios, are in terms of the commission

as there is a difference in the number of sales units. As per the table it can be seen that in

Scenario 1, the sales have been made for only 3600 units, whereas in scenario B, the sales have

been made were 3450 units and 3400 units in Scenario C respectively. Further the sales price

inclusive GST has also been higher than the above two at $891 per product (Robinson, et al

2015).

3)

The straight line method of the depreciation is a method under which the fixed asset is

depreciated over the useful life of an asset after deducting the salvage value, whereas in case of

the diminishing method, the depreciation is calculating on the book value which arrives after

deducting the depreciation. The same can be found in the case study on account of example,

where factory equipment’s depreciation is calculated on SLM basis and the depreciation on

computer is calculated on diminishing vale method.

Running head: BUSINESS MATHS AND STATISTICS

4)

a)

Breakeven analysis

Fixed costs 514,646.54 1,466.23

Contribution per unit 351.00 units

c)

Break even analysis is an analysis that displays a situation where there is no profit and no loss in

terms of units and also in dollars. In current scenarios, the breakeven unit are 1466 units which

implies that the company has to make this much units in order to avoid any losses. It is one of the

important financial techniques as it helps to analyze the position of the company with respect to

the revenues and the expenses (Robinson, et al 2015).

d)

Break-even analysis is an important aspect of a good business plan, since it helps the business

determine the cost structures, and the number of units that need to be sold in order to cover the

cost or make a profit (Schroeder, Clark and Cathey, 2019).

4)

a)

Breakeven analysis

Fixed costs 514,646.54 1,466.23

Contribution per unit 351.00 units

c)

Break even analysis is an analysis that displays a situation where there is no profit and no loss in

terms of units and also in dollars. In current scenarios, the breakeven unit are 1466 units which

implies that the company has to make this much units in order to avoid any losses. It is one of the

important financial techniques as it helps to analyze the position of the company with respect to

the revenues and the expenses (Robinson, et al 2015).

d)

Break-even analysis is an important aspect of a good business plan, since it helps the business

determine the cost structures, and the number of units that need to be sold in order to cover the

cost or make a profit (Schroeder, Clark and Cathey, 2019).

Running head: BUSINESS MATHS AND STATISTICS

5)

Expenses

Sales - Wages Commission

Administratve wages Depreciation - Factory

Equipment

Depreciation - Computers Depreciation - Office fit out

Other operating costs Rent

Interest

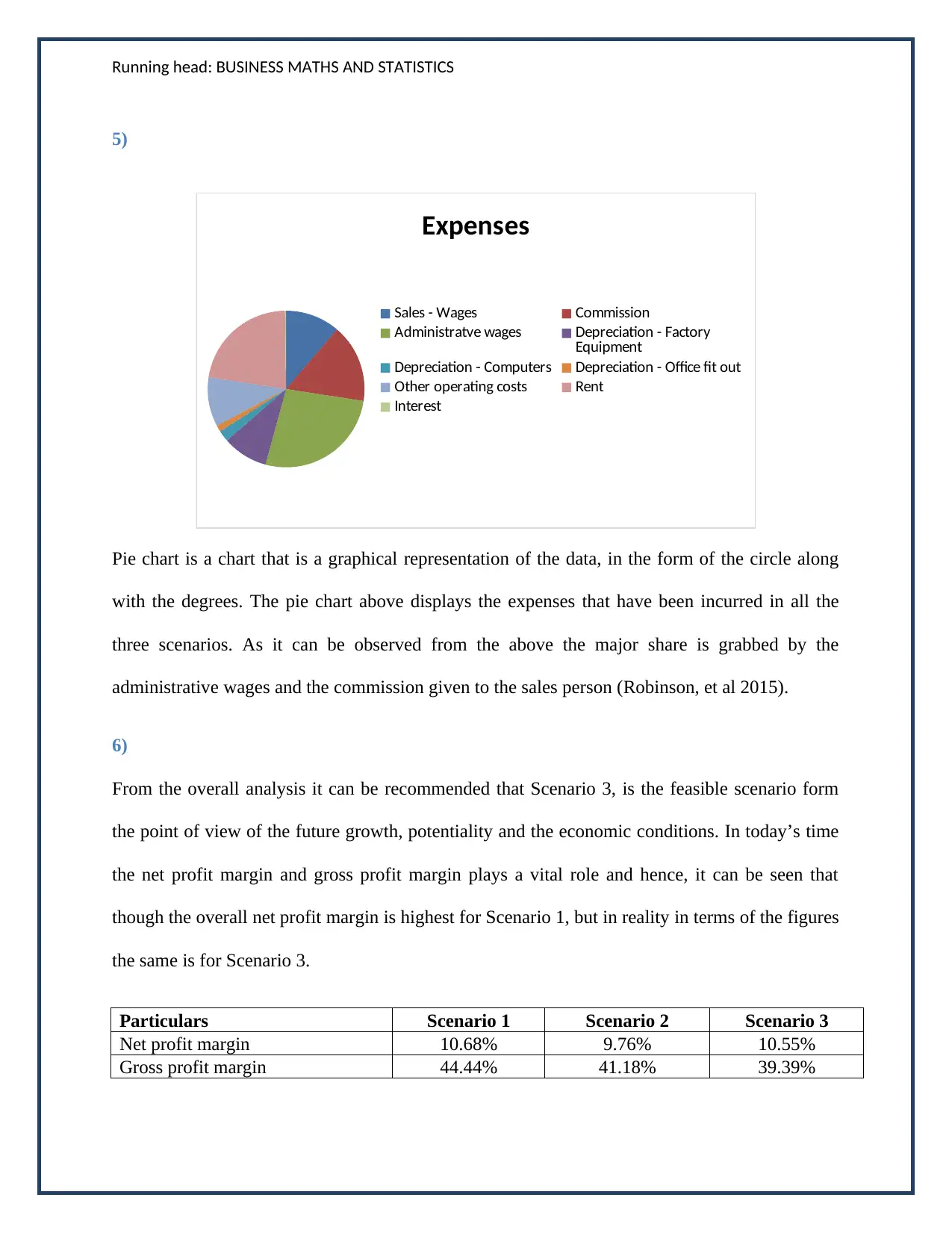

Pie chart is a chart that is a graphical representation of the data, in the form of the circle along

with the degrees. The pie chart above displays the expenses that have been incurred in all the

three scenarios. As it can be observed from the above the major share is grabbed by the

administrative wages and the commission given to the sales person (Robinson, et al 2015).

6)

From the overall analysis it can be recommended that Scenario 3, is the feasible scenario form

the point of view of the future growth, potentiality and the economic conditions. In today’s time

the net profit margin and gross profit margin plays a vital role and hence, it can be seen that

though the overall net profit margin is highest for Scenario 1, but in reality in terms of the figures

the same is for Scenario 3.

Particulars Scenario 1 Scenario 2 Scenario 3

Net profit margin 10.68% 9.76% 10.55%

Gross profit margin 44.44% 41.18% 39.39%

5)

Expenses

Sales - Wages Commission

Administratve wages Depreciation - Factory

Equipment

Depreciation - Computers Depreciation - Office fit out

Other operating costs Rent

Interest

Pie chart is a chart that is a graphical representation of the data, in the form of the circle along

with the degrees. The pie chart above displays the expenses that have been incurred in all the

three scenarios. As it can be observed from the above the major share is grabbed by the

administrative wages and the commission given to the sales person (Robinson, et al 2015).

6)

From the overall analysis it can be recommended that Scenario 3, is the feasible scenario form

the point of view of the future growth, potentiality and the economic conditions. In today’s time

the net profit margin and gross profit margin plays a vital role and hence, it can be seen that

though the overall net profit margin is highest for Scenario 1, but in reality in terms of the figures

the same is for Scenario 3.

Particulars Scenario 1 Scenario 2 Scenario 3

Net profit margin 10.68% 9.76% 10.55%

Gross profit margin 44.44% 41.18% 39.39%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: BUSINESS MATHS AND STATISTICS

The gross margins are favorable for Scenario 1 and Scenario 2, hence in the basis of the overall

performance, Scenario 3 tends to be more feasible from the aspects of both the net profit as well

as gross profit of the business, which might be lower than Scenario 1, but still is preferred over it

due to the selling price (Goldmann, 2017).

The gross margins are favorable for Scenario 1 and Scenario 2, hence in the basis of the overall

performance, Scenario 3 tends to be more feasible from the aspects of both the net profit as well

as gross profit of the business, which might be lower than Scenario 1, but still is preferred over it

due to the selling price (Goldmann, 2017).

Running head: BUSINESS MATHS AND STATISTICS

References

ATO, (2019). Individual income tax rates [online]Available from

https://www.ato.gov.au/rates/individual-income-tax-rates/?=top_10_rates#Residents [Accessed

on 5th April 2020].

Goldmann, K., (2017) Financial liquidity and profitability management in practice of polish

business. In Financial Environment and Business Development (pp. 103-112). Springer, Cham.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., (2015) International financial

statement analysis. John Wiley & Sons.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., (2019) Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

References

ATO, (2019). Individual income tax rates [online]Available from

https://www.ato.gov.au/rates/individual-income-tax-rates/?=top_10_rates#Residents [Accessed

on 5th April 2020].

Goldmann, K., (2017) Financial liquidity and profitability management in practice of polish

business. In Financial Environment and Business Development (pp. 103-112). Springer, Cham.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., (2015) International financial

statement analysis. John Wiley & Sons.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., (2019) Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.