Statement of Profit Comparison and Break Even Analysis

VerifiedAdded on 2022/10/16

|12

|1895

|409

AI Summary

This document discusses the statement of profit comparison and break even analysis in Business Maths and Statistics. It includes tables and graphs to explain the scenarios and variances. The document also explains the difference between diminishing method and straight-line method of depreciation. The break-even analysis is explained in detail along with its uses and applications.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Maths and Statistics

0

0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

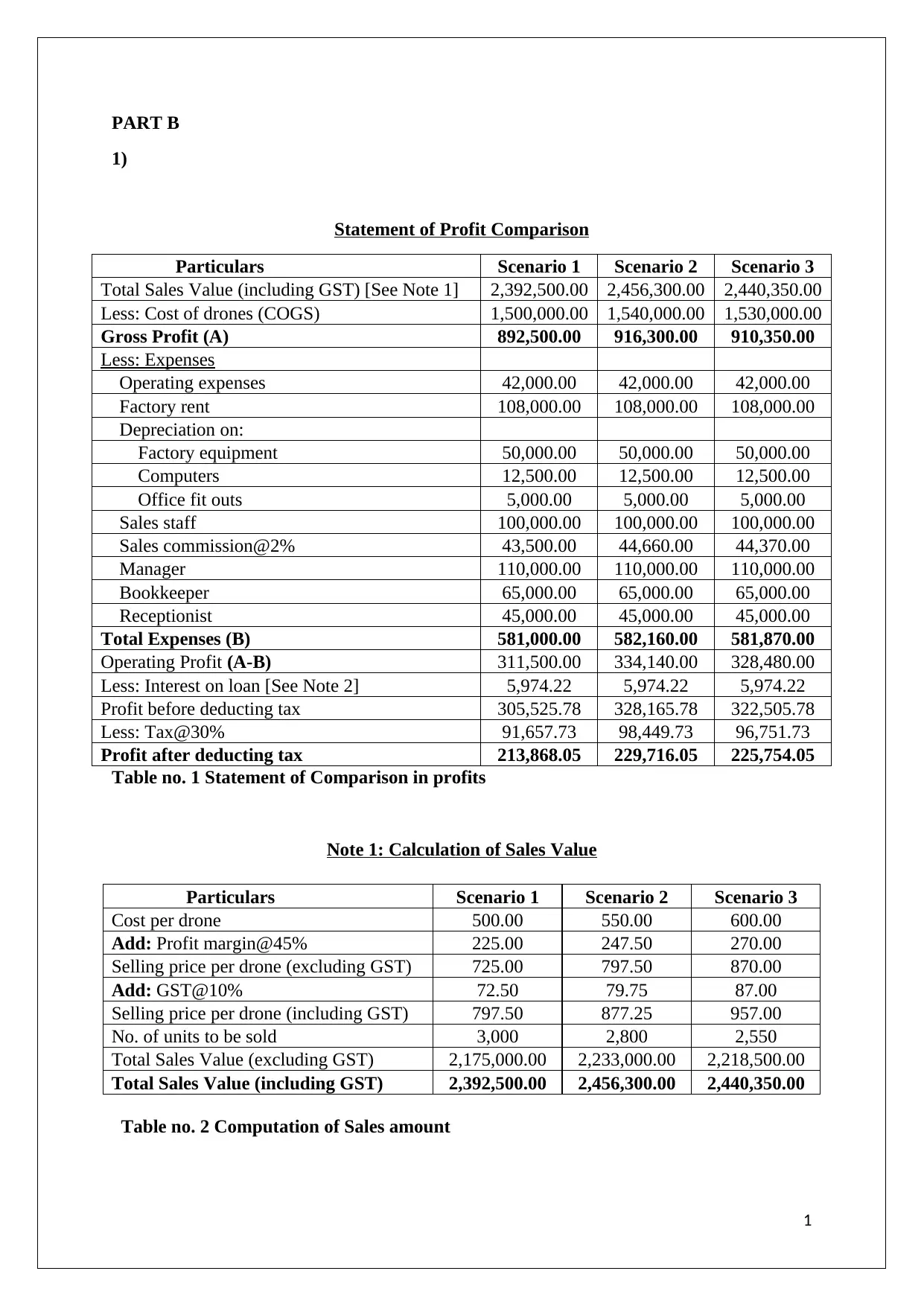

PART B

1)

Statement of Profit Comparison

Particulars Scenario 1 Scenario 2 Scenario 3

Total Sales Value (including GST) [See Note 1] 2,392,500.00 2,456,300.00 2,440,350.00

Less: Cost of drones (COGS) 1,500,000.00 1,540,000.00 1,530,000.00

Gross Profit (A) 892,500.00 916,300.00 910,350.00

Less: Expenses

Operating expenses 42,000.00 42,000.00 42,000.00

Factory rent 108,000.00 108,000.00 108,000.00

Depreciation on:

Factory equipment 50,000.00 50,000.00 50,000.00

Computers 12,500.00 12,500.00 12,500.00

Office fit outs 5,000.00 5,000.00 5,000.00

Sales staff 100,000.00 100,000.00 100,000.00

Sales commission@2% 43,500.00 44,660.00 44,370.00

Manager 110,000.00 110,000.00 110,000.00

Bookkeeper 65,000.00 65,000.00 65,000.00

Receptionist 45,000.00 45,000.00 45,000.00

Total Expenses (B) 581,000.00 582,160.00 581,870.00

Operating Profit (A-B) 311,500.00 334,140.00 328,480.00

Less: Interest on loan [See Note 2] 5,974.22 5,974.22 5,974.22

Profit before deducting tax 305,525.78 328,165.78 322,505.78

Less: Tax@30% 91,657.73 98,449.73 96,751.73

Profit after deducting tax 213,868.05 229,716.05 225,754.05

Table no. 1 Statement of Comparison in profits

Note 1: Calculation of Sales Value

Particulars Scenario 1 Scenario 2 Scenario 3

Cost per drone 500.00 550.00 600.00

Add: Profit margin@45% 225.00 247.50 270.00

Selling price per drone (excluding GST) 725.00 797.50 870.00

Add: GST@10% 72.50 79.75 87.00

Selling price per drone (including GST) 797.50 877.25 957.00

No. of units to be sold 3,000 2,800 2,550

Total Sales Value (excluding GST) 2,175,000.00 2,233,000.00 2,218,500.00

Total Sales Value (including GST) 2,392,500.00 2,456,300.00 2,440,350.00

Table no. 2 Computation of Sales amount

1

1)

Statement of Profit Comparison

Particulars Scenario 1 Scenario 2 Scenario 3

Total Sales Value (including GST) [See Note 1] 2,392,500.00 2,456,300.00 2,440,350.00

Less: Cost of drones (COGS) 1,500,000.00 1,540,000.00 1,530,000.00

Gross Profit (A) 892,500.00 916,300.00 910,350.00

Less: Expenses

Operating expenses 42,000.00 42,000.00 42,000.00

Factory rent 108,000.00 108,000.00 108,000.00

Depreciation on:

Factory equipment 50,000.00 50,000.00 50,000.00

Computers 12,500.00 12,500.00 12,500.00

Office fit outs 5,000.00 5,000.00 5,000.00

Sales staff 100,000.00 100,000.00 100,000.00

Sales commission@2% 43,500.00 44,660.00 44,370.00

Manager 110,000.00 110,000.00 110,000.00

Bookkeeper 65,000.00 65,000.00 65,000.00

Receptionist 45,000.00 45,000.00 45,000.00

Total Expenses (B) 581,000.00 582,160.00 581,870.00

Operating Profit (A-B) 311,500.00 334,140.00 328,480.00

Less: Interest on loan [See Note 2] 5,974.22 5,974.22 5,974.22

Profit before deducting tax 305,525.78 328,165.78 322,505.78

Less: Tax@30% 91,657.73 98,449.73 96,751.73

Profit after deducting tax 213,868.05 229,716.05 225,754.05

Table no. 1 Statement of Comparison in profits

Note 1: Calculation of Sales Value

Particulars Scenario 1 Scenario 2 Scenario 3

Cost per drone 500.00 550.00 600.00

Add: Profit margin@45% 225.00 247.50 270.00

Selling price per drone (excluding GST) 725.00 797.50 870.00

Add: GST@10% 72.50 79.75 87.00

Selling price per drone (including GST) 797.50 877.25 957.00

No. of units to be sold 3,000 2,800 2,550

Total Sales Value (excluding GST) 2,175,000.00 2,233,000.00 2,218,500.00

Total Sales Value (including GST) 2,392,500.00 2,456,300.00 2,440,350.00

Table no. 2 Computation of Sales amount

1

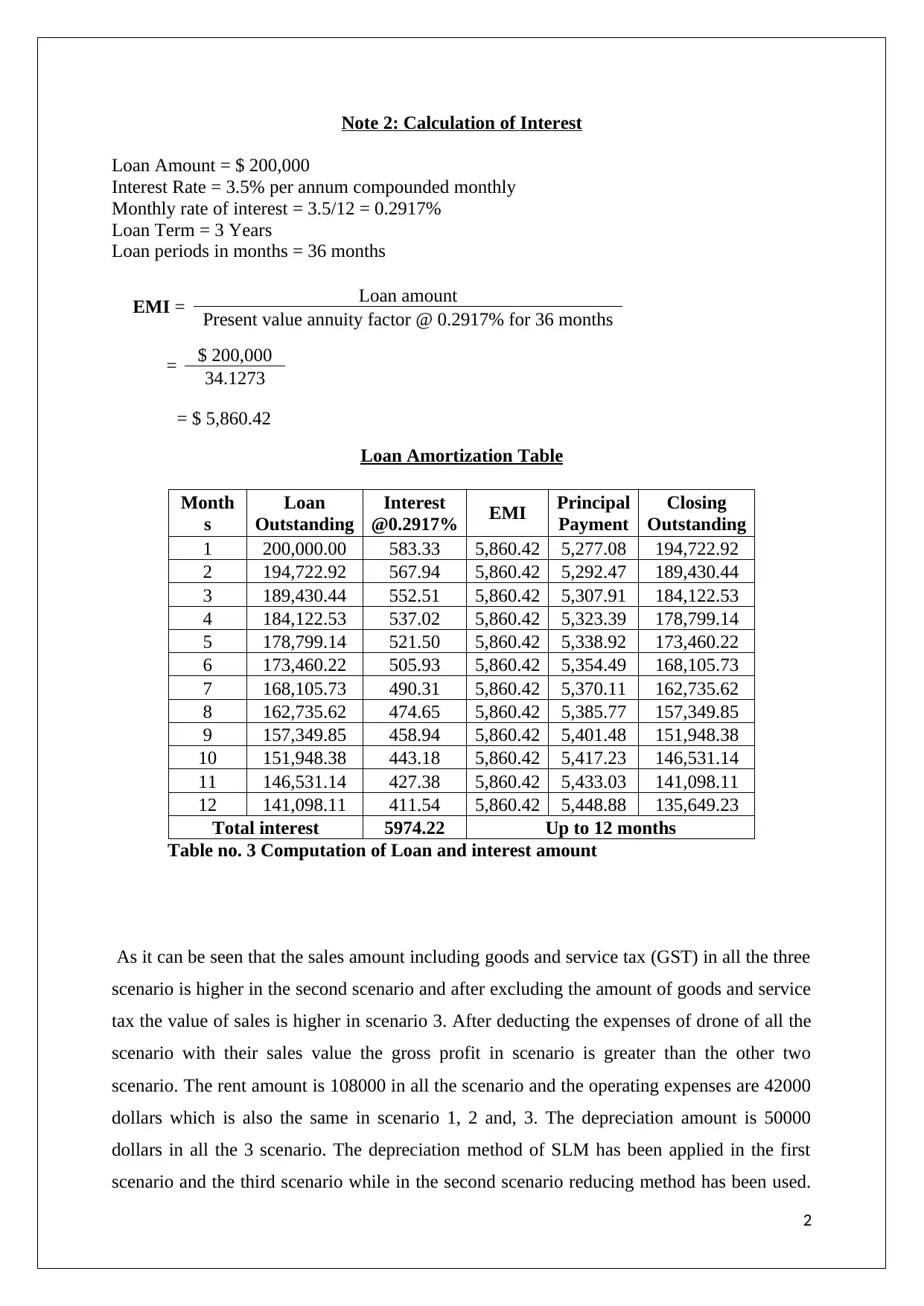

Note 2: Calculation of Interest

Loan Amount = $ 200,000

Interest Rate = 3.5% per annum compounded monthly

Monthly rate of interest = 3.5/12 = 0.2917%

Loan Term = 3 Years

Loan periods in months = 36 months

EMI = Loan amount

Present value annuity factor @ 0.2917% for 36 months

= $ 5,860.42

Loan Amortization Table

Month

s

Loan

Outstanding

Interest

@0.2917% EMI Principal

Payment

Closing

Outstanding

1 200,000.00 583.33 5,860.42 5,277.08 194,722.92

2 194,722.92 567.94 5,860.42 5,292.47 189,430.44

3 189,430.44 552.51 5,860.42 5,307.91 184,122.53

4 184,122.53 537.02 5,860.42 5,323.39 178,799.14

5 178,799.14 521.50 5,860.42 5,338.92 173,460.22

6 173,460.22 505.93 5,860.42 5,354.49 168,105.73

7 168,105.73 490.31 5,860.42 5,370.11 162,735.62

8 162,735.62 474.65 5,860.42 5,385.77 157,349.85

9 157,349.85 458.94 5,860.42 5,401.48 151,948.38

10 151,948.38 443.18 5,860.42 5,417.23 146,531.14

11 146,531.14 427.38 5,860.42 5,433.03 141,098.11

12 141,098.11 411.54 5,860.42 5,448.88 135,649.23

Total interest 5974.22 Up to 12 months

Table no. 3 Computation of Loan and interest amount

As it can be seen that the sales amount including goods and service tax (GST) in all the three

scenario is higher in the second scenario and after excluding the amount of goods and service

tax the value of sales is higher in scenario 3. After deducting the expenses of drone of all the

scenario with their sales value the gross profit in scenario is greater than the other two

scenario. The rent amount is 108000 in all the scenario and the operating expenses are 42000

dollars which is also the same in scenario 1, 2 and, 3. The depreciation amount is 50000

dollars in all the 3 scenario. The depreciation method of SLM has been applied in the first

scenario and the third scenario while in the second scenario reducing method has been used.

2

= $ 200,000

34.1273

Loan Amount = $ 200,000

Interest Rate = 3.5% per annum compounded monthly

Monthly rate of interest = 3.5/12 = 0.2917%

Loan Term = 3 Years

Loan periods in months = 36 months

EMI = Loan amount

Present value annuity factor @ 0.2917% for 36 months

= $ 5,860.42

Loan Amortization Table

Month

s

Loan

Outstanding

Interest

@0.2917% EMI Principal

Payment

Closing

Outstanding

1 200,000.00 583.33 5,860.42 5,277.08 194,722.92

2 194,722.92 567.94 5,860.42 5,292.47 189,430.44

3 189,430.44 552.51 5,860.42 5,307.91 184,122.53

4 184,122.53 537.02 5,860.42 5,323.39 178,799.14

5 178,799.14 521.50 5,860.42 5,338.92 173,460.22

6 173,460.22 505.93 5,860.42 5,354.49 168,105.73

7 168,105.73 490.31 5,860.42 5,370.11 162,735.62

8 162,735.62 474.65 5,860.42 5,385.77 157,349.85

9 157,349.85 458.94 5,860.42 5,401.48 151,948.38

10 151,948.38 443.18 5,860.42 5,417.23 146,531.14

11 146,531.14 427.38 5,860.42 5,433.03 141,098.11

12 141,098.11 411.54 5,860.42 5,448.88 135,649.23

Total interest 5974.22 Up to 12 months

Table no. 3 Computation of Loan and interest amount

As it can be seen that the sales amount including goods and service tax (GST) in all the three

scenario is higher in the second scenario and after excluding the amount of goods and service

tax the value of sales is higher in scenario 3. After deducting the expenses of drone of all the

scenario with their sales value the gross profit in scenario is greater than the other two

scenario. The rent amount is 108000 in all the scenario and the operating expenses are 42000

dollars which is also the same in scenario 1, 2 and, 3. The depreciation amount is 50000

dollars in all the 3 scenario. The depreciation method of SLM has been applied in the first

scenario and the third scenario while in the second scenario reducing method has been used.

2

= $ 200,000

34.1273

The useful life of the factory equipment, office fit out, and computers are 10 years and 5

years and 4 years. This depreciation method will not affect the profit as the depreciation

amount has been computed for only 1st year. The total expenses in the first scenario are

581000 and in the second scenario are 582160 dollars and in the third scenario the expenses

are 581870 dollars. Thus the total expenses is higher in case of scenario 2 in comparison to

other scenario. The operating profit in scenario 1 after deducting gross profit with total

expenses comes to 311500 and it scenario 2 it comes to 582160 while in the third scenario the

operating profit is 328480. As it can be analysed that the operating profit of the second

scenario is much higher than the first one. The reason behind the higher amount of operating

profit in scenario 2 is due to the less amount of fixed expenses and also less amount of

operational expenses incurred. The profit before the deduction of the tax amount in the

second scenario comes to 328165.78 which is the highest amount as compared to scenario 3

and scenario 1. The net profit after reducing the tax amount is lower in case of scenario 1 and

scenario 3 while in scenario 1 the profit is 229716.05. So after examining the scenario it has

been concluded that client should select scenario 2 which has been considered the best

scenario in all aspects.

2) The first variance which has been noticed in the scenario is that the first scenario spent less

amount of expenditure with respect to cost of drone when compared to second and third

scenario. No variance has been noticed in gross profit. The ratio of gross profit in each

scenario is 37.30%. A difference of 1160 dollars in the total expense has been identified

between first and second scenario and a very less amount of difference has been evaluated

when compared between third and second case. A huge variance has been examined in

scenario when its profit amount compared with the last scenario that is third scenario. No

amount of variance has been determined in the interest amount of the scenario. Also, no

variance has been observed in case of fixed cost after examining the cases. But there was a

huge dissimilarity in the profits after decreasing the taxes in al the three cases. A variance of

15848 dollars has been recognized while analysing the profits between first and second cases.

3

years and 4 years. This depreciation method will not affect the profit as the depreciation

amount has been computed for only 1st year. The total expenses in the first scenario are

581000 and in the second scenario are 582160 dollars and in the third scenario the expenses

are 581870 dollars. Thus the total expenses is higher in case of scenario 2 in comparison to

other scenario. The operating profit in scenario 1 after deducting gross profit with total

expenses comes to 311500 and it scenario 2 it comes to 582160 while in the third scenario the

operating profit is 328480. As it can be analysed that the operating profit of the second

scenario is much higher than the first one. The reason behind the higher amount of operating

profit in scenario 2 is due to the less amount of fixed expenses and also less amount of

operational expenses incurred. The profit before the deduction of the tax amount in the

second scenario comes to 328165.78 which is the highest amount as compared to scenario 3

and scenario 1. The net profit after reducing the tax amount is lower in case of scenario 1 and

scenario 3 while in scenario 1 the profit is 229716.05. So after examining the scenario it has

been concluded that client should select scenario 2 which has been considered the best

scenario in all aspects.

2) The first variance which has been noticed in the scenario is that the first scenario spent less

amount of expenditure with respect to cost of drone when compared to second and third

scenario. No variance has been noticed in gross profit. The ratio of gross profit in each

scenario is 37.30%. A difference of 1160 dollars in the total expense has been identified

between first and second scenario and a very less amount of difference has been evaluated

when compared between third and second case. A huge variance has been examined in

scenario when its profit amount compared with the last scenario that is third scenario. No

amount of variance has been determined in the interest amount of the scenario. Also, no

variance has been observed in case of fixed cost after examining the cases. But there was a

huge dissimilarity in the profits after decreasing the taxes in al the three cases. A variance of

15848 dollars has been recognized while analysing the profits between first and second cases.

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

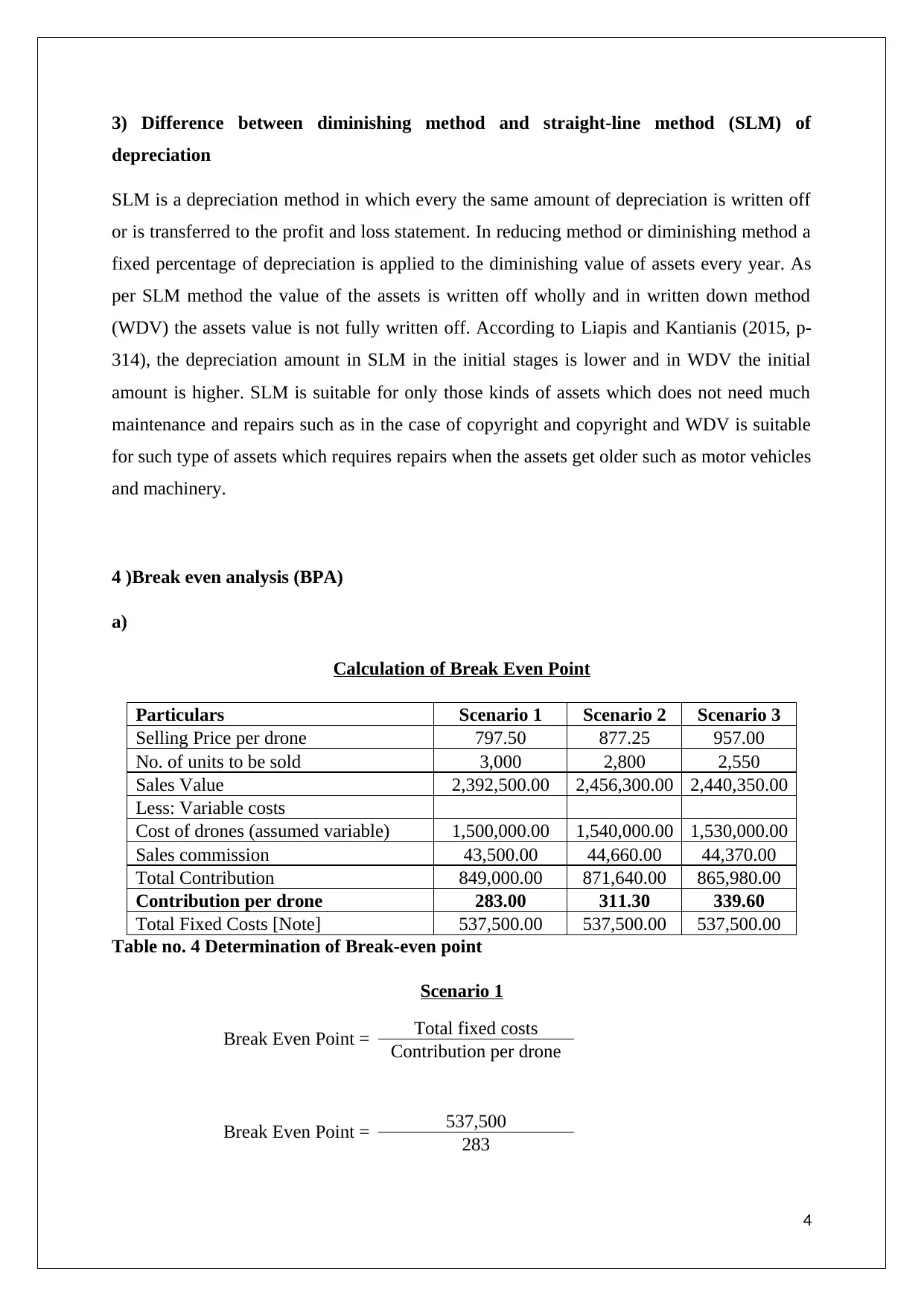

3) Difference between diminishing method and straight-line method (SLM) of

depreciation

SLM is a depreciation method in which every the same amount of depreciation is written off

or is transferred to the profit and loss statement. In reducing method or diminishing method a

fixed percentage of depreciation is applied to the diminishing value of assets every year. As

per SLM method the value of the assets is written off wholly and in written down method

(WDV) the assets value is not fully written off. According to Liapis and Kantianis (2015, p-

314), the depreciation amount in SLM in the initial stages is lower and in WDV the initial

amount is higher. SLM is suitable for only those kinds of assets which does not need much

maintenance and repairs such as in the case of copyright and copyright and WDV is suitable

for such type of assets which requires repairs when the assets get older such as motor vehicles

and machinery.

4 )Break even analysis (BPA)

a)

Calculation of Break Even Point

Particulars Scenario 1 Scenario 2 Scenario 3

Selling Price per drone 797.50 877.25 957.00

No. of units to be sold 3,000 2,800 2,550

Sales Value 2,392,500.00 2,456,300.00 2,440,350.00

Less: Variable costs

Cost of drones (assumed variable) 1,500,000.00 1,540,000.00 1,530,000.00

Sales commission 43,500.00 44,660.00 44,370.00

Total Contribution 849,000.00 871,640.00 865,980.00

Contribution per drone 283.00 311.30 339.60

Total Fixed Costs [Note] 537,500.00 537,500.00 537,500.00

Table no. 4 Determination of Break-even point

Scenario 1

Break Even Point = Total fixed costs

Contribution per drone

Break Even Point = 537,500

283

4

depreciation

SLM is a depreciation method in which every the same amount of depreciation is written off

or is transferred to the profit and loss statement. In reducing method or diminishing method a

fixed percentage of depreciation is applied to the diminishing value of assets every year. As

per SLM method the value of the assets is written off wholly and in written down method

(WDV) the assets value is not fully written off. According to Liapis and Kantianis (2015, p-

314), the depreciation amount in SLM in the initial stages is lower and in WDV the initial

amount is higher. SLM is suitable for only those kinds of assets which does not need much

maintenance and repairs such as in the case of copyright and copyright and WDV is suitable

for such type of assets which requires repairs when the assets get older such as motor vehicles

and machinery.

4 )Break even analysis (BPA)

a)

Calculation of Break Even Point

Particulars Scenario 1 Scenario 2 Scenario 3

Selling Price per drone 797.50 877.25 957.00

No. of units to be sold 3,000 2,800 2,550

Sales Value 2,392,500.00 2,456,300.00 2,440,350.00

Less: Variable costs

Cost of drones (assumed variable) 1,500,000.00 1,540,000.00 1,530,000.00

Sales commission 43,500.00 44,660.00 44,370.00

Total Contribution 849,000.00 871,640.00 865,980.00

Contribution per drone 283.00 311.30 339.60

Total Fixed Costs [Note] 537,500.00 537,500.00 537,500.00

Table no. 4 Determination of Break-even point

Scenario 1

Break Even Point = Total fixed costs

Contribution per drone

Break Even Point = 537,500

283

4

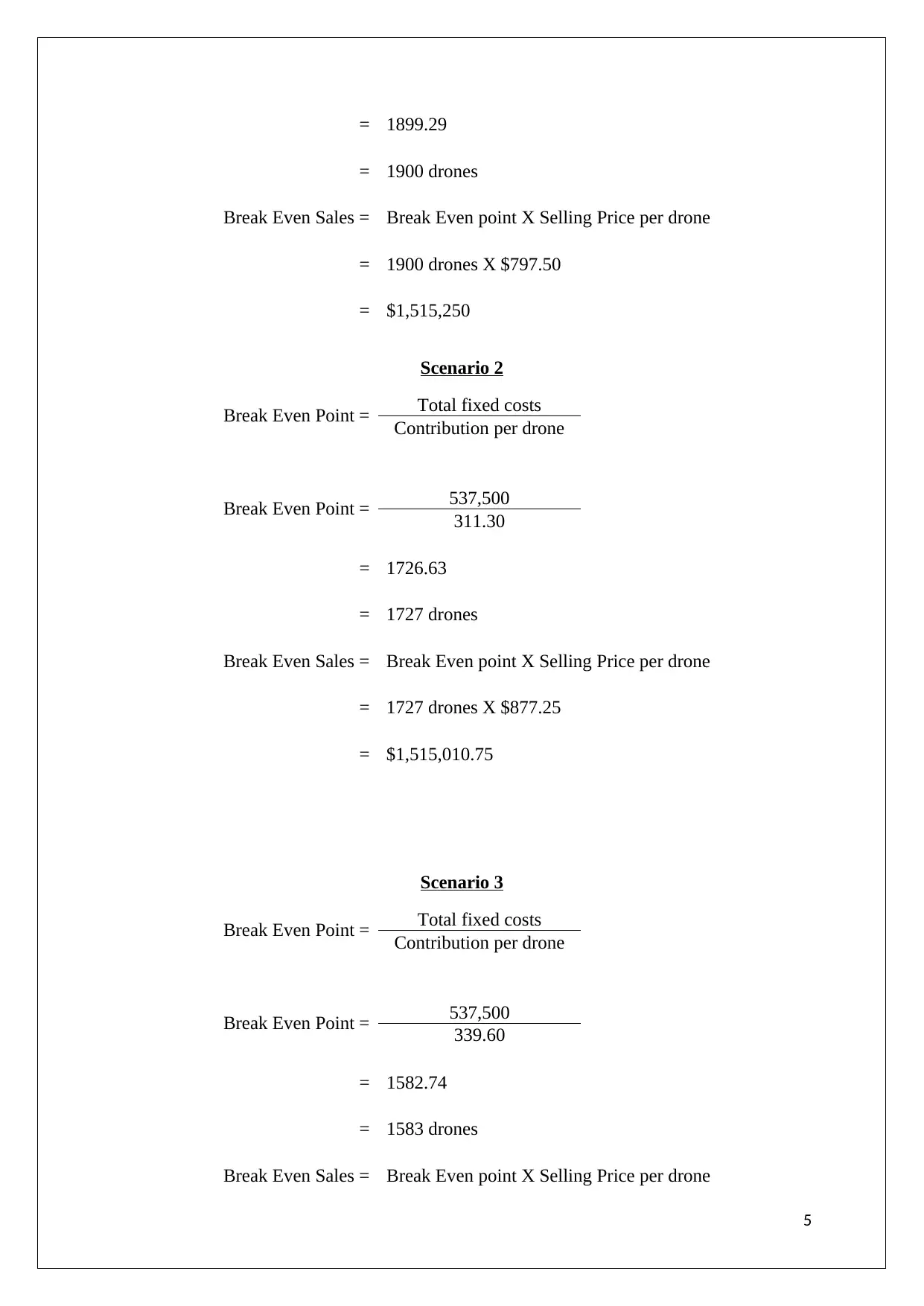

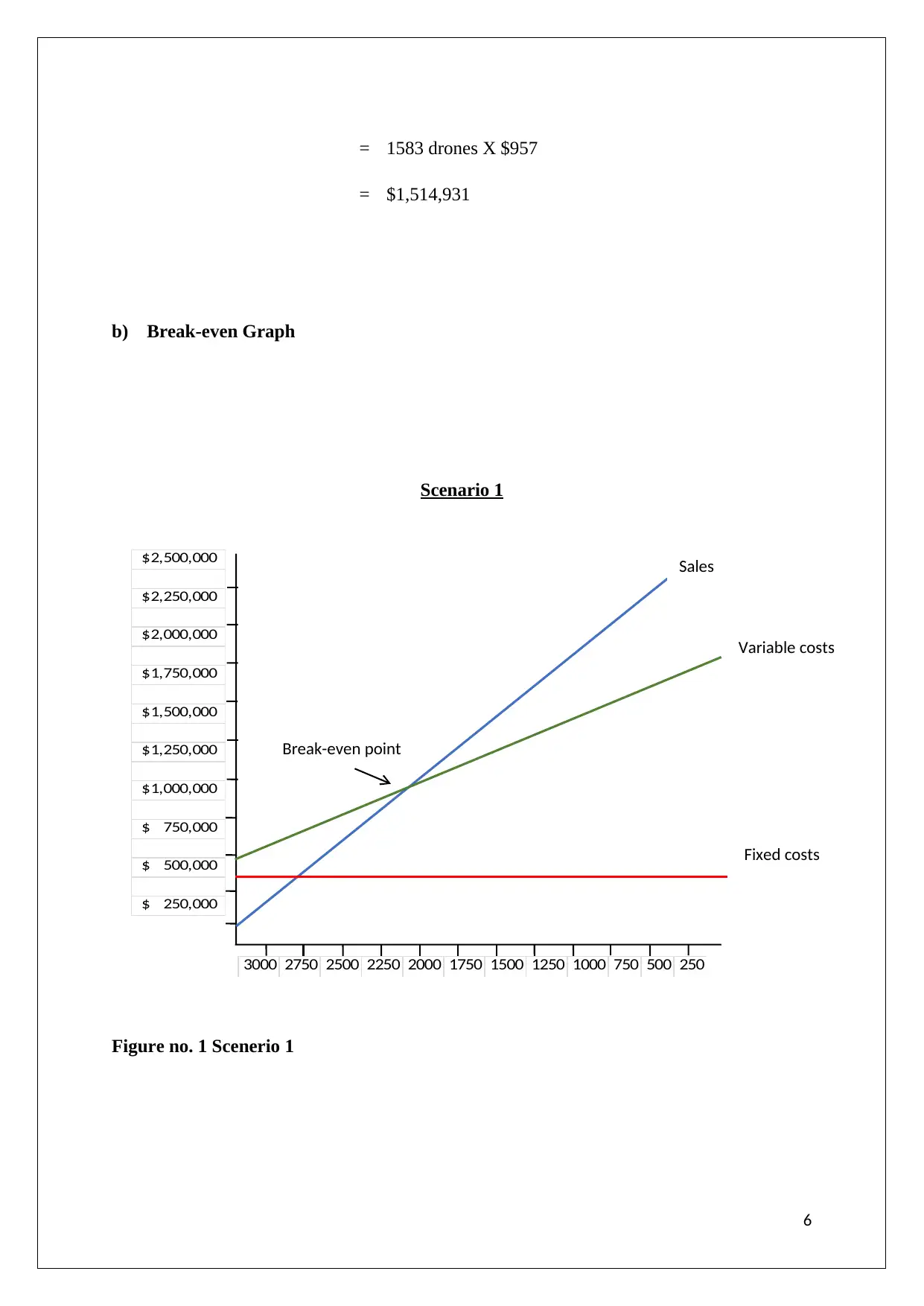

= 1899.29

= 1900 drones

Break Even Sales = Break Even point X Selling Price per drone

= 1900 drones X $797.50

= $1,515,250

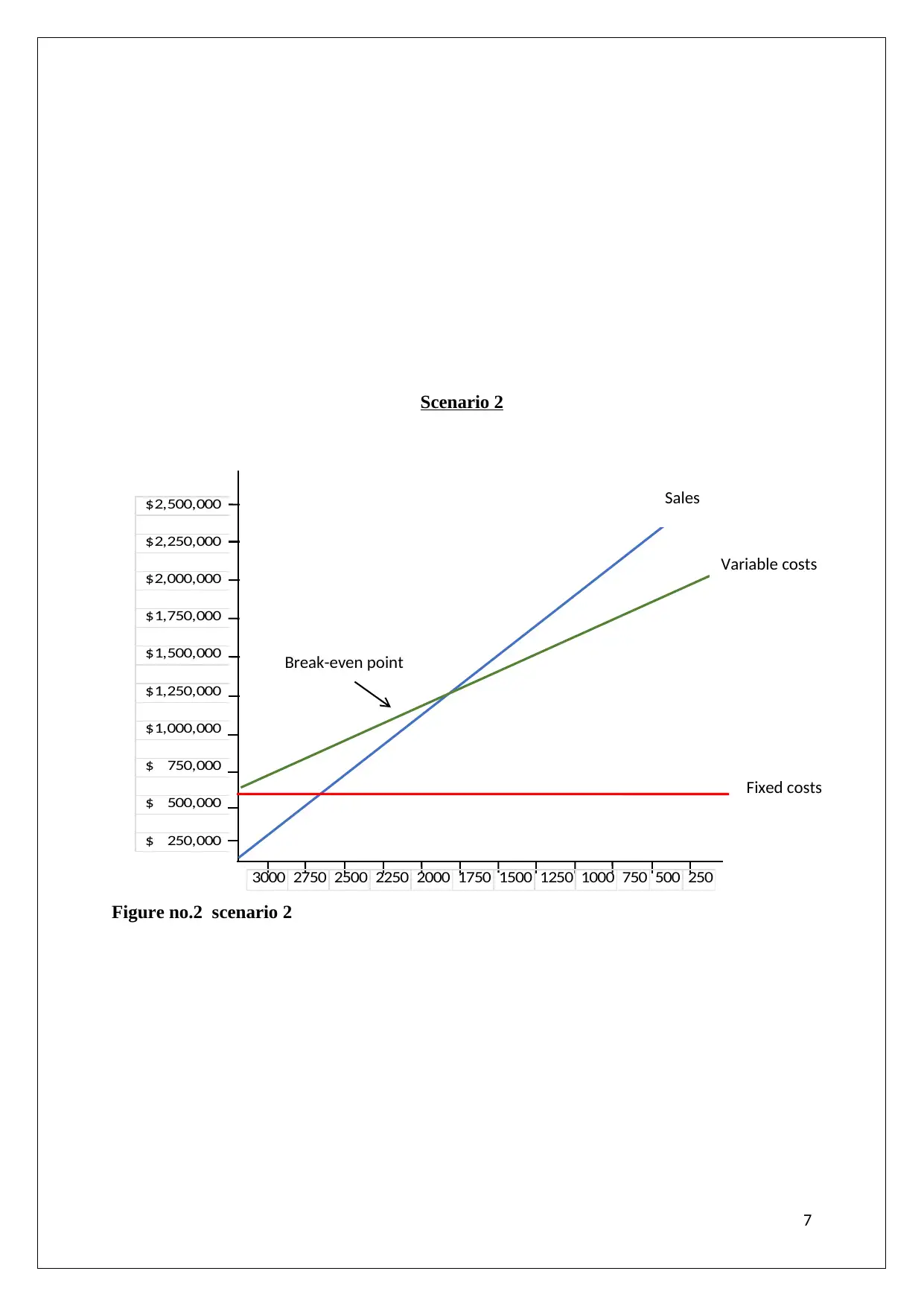

Scenario 2

Break Even Point = Total fixed costs

Contribution per drone

Break Even Point = 537,500

311.30

= 1726.63

= 1727 drones

Break Even Sales = Break Even point X Selling Price per drone

= 1727 drones X $877.25

= $1,515,010.75

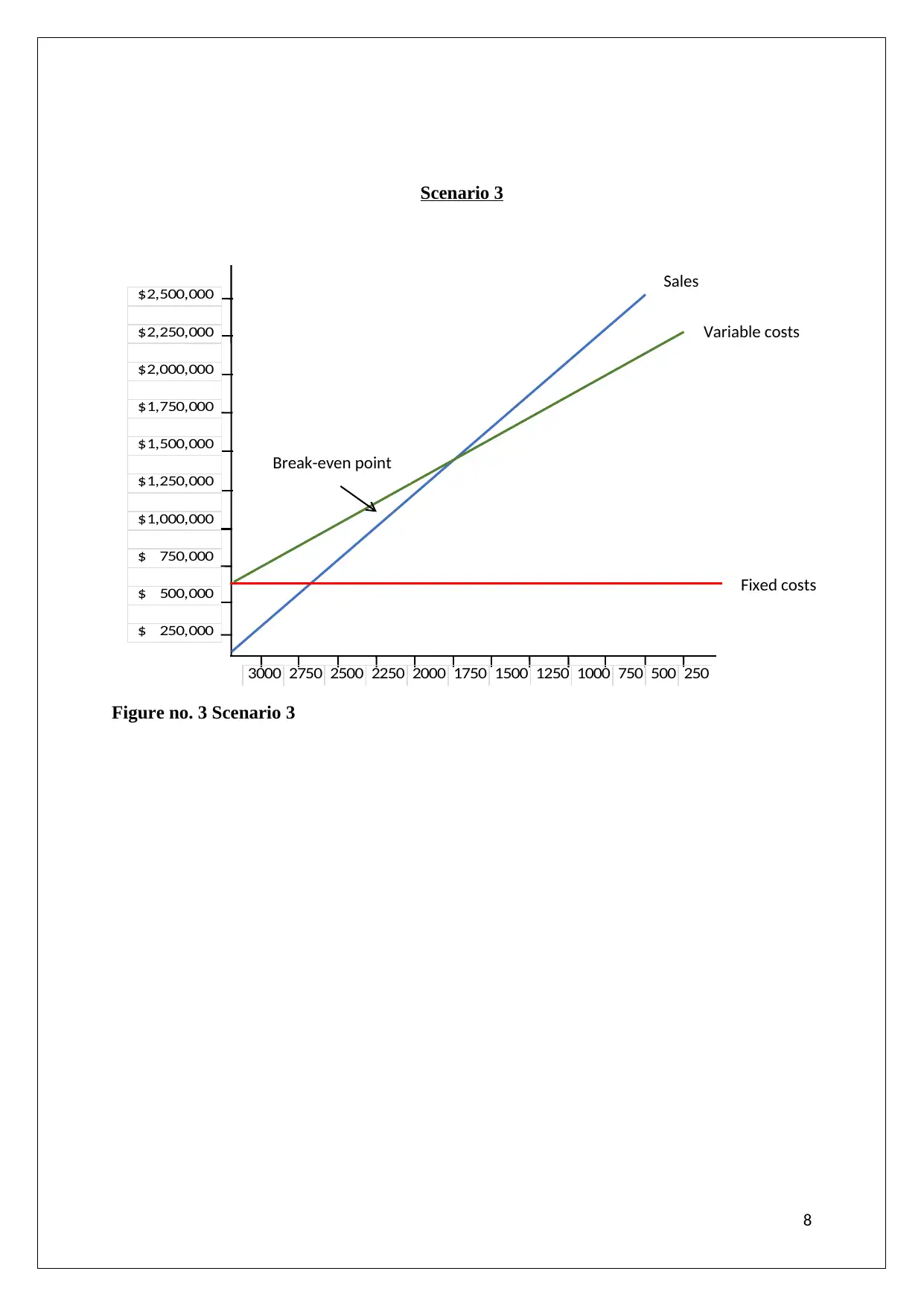

Scenario 3

Break Even Point = Total fixed costs

Contribution per drone

Break Even Point = 537,500

339.60

= 1582.74

= 1583 drones

Break Even Sales = Break Even point X Selling Price per drone

5

= 1900 drones

Break Even Sales = Break Even point X Selling Price per drone

= 1900 drones X $797.50

= $1,515,250

Scenario 2

Break Even Point = Total fixed costs

Contribution per drone

Break Even Point = 537,500

311.30

= 1726.63

= 1727 drones

Break Even Sales = Break Even point X Selling Price per drone

= 1727 drones X $877.25

= $1,515,010.75

Scenario 3

Break Even Point = Total fixed costs

Contribution per drone

Break Even Point = 537,500

339.60

= 1582.74

= 1583 drones

Break Even Sales = Break Even point X Selling Price per drone

5

= 1583 drones X $957

= $1,514,931

b) Break-even Graph

Scenario 1

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Figure no. 1 Scenerio 1

6

3000 2750 2500 2250 2000 1750 1500 1250 1000 750 500 250

Sales

Variable costs

Fixed costs

Break-even point

= $1,514,931

b) Break-even Graph

Scenario 1

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Figure no. 1 Scenerio 1

6

3000 2750 2500 2250 2000 1750 1500 1250 1000 750 500 250

Sales

Variable costs

Fixed costs

Break-even point

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Scenario 2

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Figure no.2 scenario 2

7

3000 2750 2500 2250 2000 1750 1500 1250 1000 750 500 250

Sales

Variable costs

Fixed costs

Break-even point

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Figure no.2 scenario 2

7

3000 2750 2500 2250 2000 1750 1500 1250 1000 750 500 250

Sales

Variable costs

Fixed costs

Break-even point

Scenario 3

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Figure no. 3 Scenario 3

8

3000 2750 2500 2250 2000 1750 1500 1250 1000 750 500 250

Fixed costs

Variable costs

Sales

Break-even point

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Figure no. 3 Scenario 3

8

3000 2750 2500 2250 2000 1750 1500 1250 1000 750 500 250

Fixed costs

Variable costs

Sales

Break-even point

c) BPA is applied in case where the dollars are required to cover the variable and fixed cost.

According to Kampf et al. (2016, p-126), the point where the total revenue is same as the

total cost is known as the point of break-even. Break-even point is computed by dividing the

fixed cost by the total contribution margin. For example, if the amount of fixed cost is 50000

dollars and the contribution margin is 50 dollars then the point of break-even is 1000 units. If

the entity sale all the 1000 units then the entity will be able to cover all the fixed cost amount

and the entity will neither gain anything nor they will lose anything that means no loss or

profit.

d) Break-even analysis is considered an essential tool for the organization because it used to

analyse that sales level which can cover the whole fixed expenses of the company. It

computes the level the entity must invest to recover its cash outflow. Break-even point is also

used to measure the safety margin. BPA is broadly used in options and derivatives and also to

prepare organizational budget. According to Laitinen (2018, p-4), many organization uses it

to measure the target sales mix and the production level to know the actual sales from where

they can start earning the profit after recovering the cost. The break-even point will be lower

for those organizations whose fixed costs are lower. The concept is useful for management

only and not for regulators, investors, and financial institutions. The other use of break-even

point is to evaluate the pricing strategy for a business plan.

9

According to Kampf et al. (2016, p-126), the point where the total revenue is same as the

total cost is known as the point of break-even. Break-even point is computed by dividing the

fixed cost by the total contribution margin. For example, if the amount of fixed cost is 50000

dollars and the contribution margin is 50 dollars then the point of break-even is 1000 units. If

the entity sale all the 1000 units then the entity will be able to cover all the fixed cost amount

and the entity will neither gain anything nor they will lose anything that means no loss or

profit.

d) Break-even analysis is considered an essential tool for the organization because it used to

analyse that sales level which can cover the whole fixed expenses of the company. It

computes the level the entity must invest to recover its cash outflow. Break-even point is also

used to measure the safety margin. BPA is broadly used in options and derivatives and also to

prepare organizational budget. According to Laitinen (2018, p-4), many organization uses it

to measure the target sales mix and the production level to know the actual sales from where

they can start earning the profit after recovering the cost. The break-even point will be lower

for those organizations whose fixed costs are lower. The concept is useful for management

only and not for regulators, investors, and financial institutions. The other use of break-even

point is to evaluate the pricing strategy for a business plan.

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

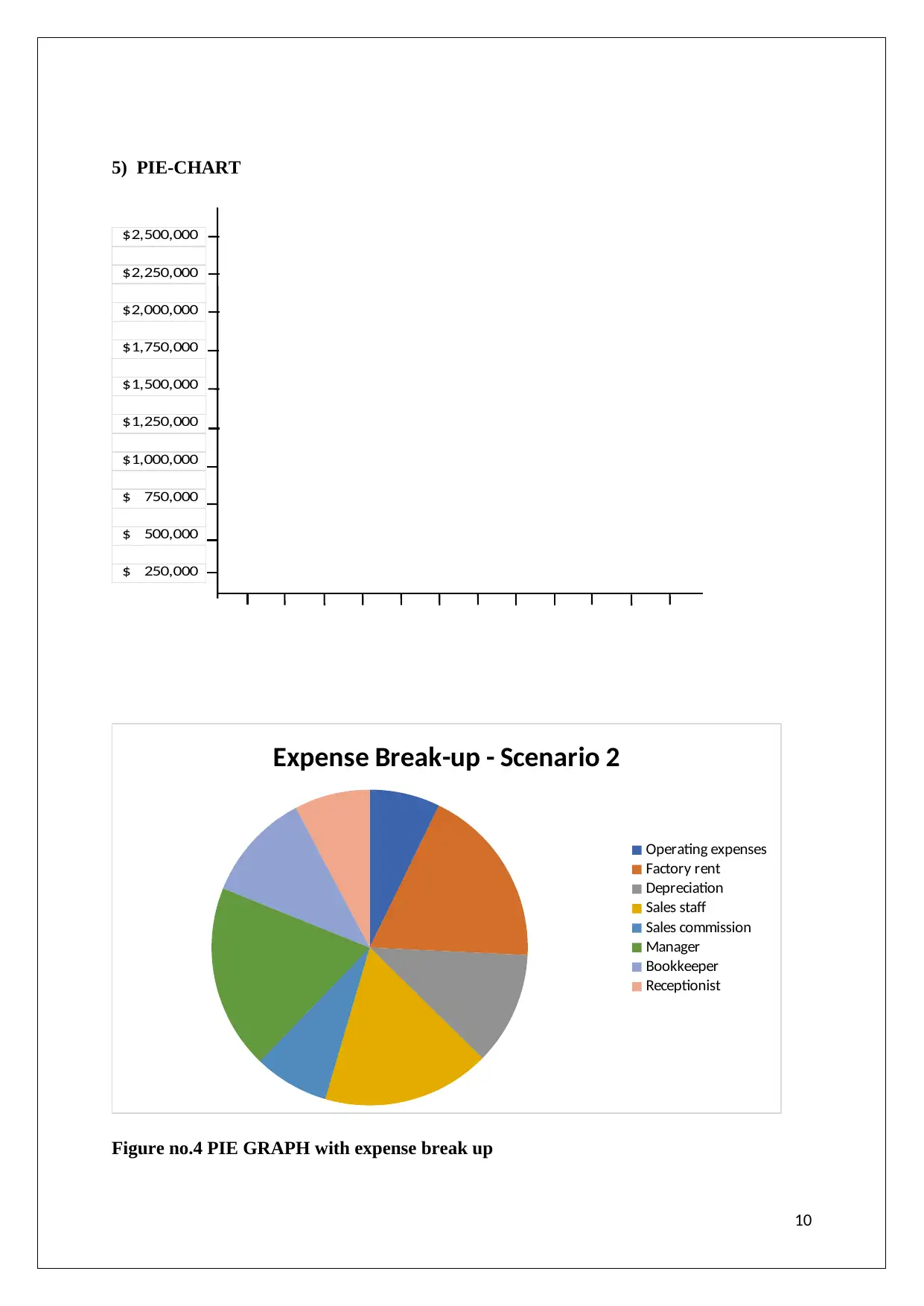

5) PIE-CHART

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Expense Break-up - Scenario 2

Operating expenses

Factory rent

Depreciation

Sales staff

Sales commission

Manager

Bookkeeper

Receptionist

Figure no.4 PIE GRAPH with expense break up

10

2,500,000$

2,250,000$

2,000,000$

1,750,000$

1,500,000$

1,250,000$

1,000,000$

750,000$

500,000$

250,000$

Expense Break-up - Scenario 2

Operating expenses

Factory rent

Depreciation

Sales staff

Sales commission

Manager

Bookkeeper

Receptionist

Figure no.4 PIE GRAPH with expense break up

10

References

Kampf, R., Majerčák, P. and Švagr, P., (2016). Application of break-even point analysis.

NAŠE MORE: znanstveno-stručni časopis za more i pomorstvo, 63(3 Special Issue), pp.126-

128.

Laitinen, E.K., (2018). Extension of break-even analysis for payment default prediction:

evidence from small firms. Innovations, 8, p.4.

Liapis, K.J. and Kantianis, D.D., (2015). Depreciation methods and life-cycle costing (LCC)

methodology. Procedia Economics and Finance, 19, pp.314-324.

11

Kampf, R., Majerčák, P. and Švagr, P., (2016). Application of break-even point analysis.

NAŠE MORE: znanstveno-stručni časopis za more i pomorstvo, 63(3 Special Issue), pp.126-

128.

Laitinen, E.K., (2018). Extension of break-even analysis for payment default prediction:

evidence from small firms. Innovations, 8, p.4.

Liapis, K.J. and Kantianis, D.D., (2015). Depreciation methods and life-cycle costing (LCC)

methodology. Procedia Economics and Finance, 19, pp.314-324.

11

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.