Comprehensive Financial Performance Analysis Report of a Business Plan

VerifiedAdded on 2022/12/30

Paraphrase This Document

Report summary..........................................................................................................................................3

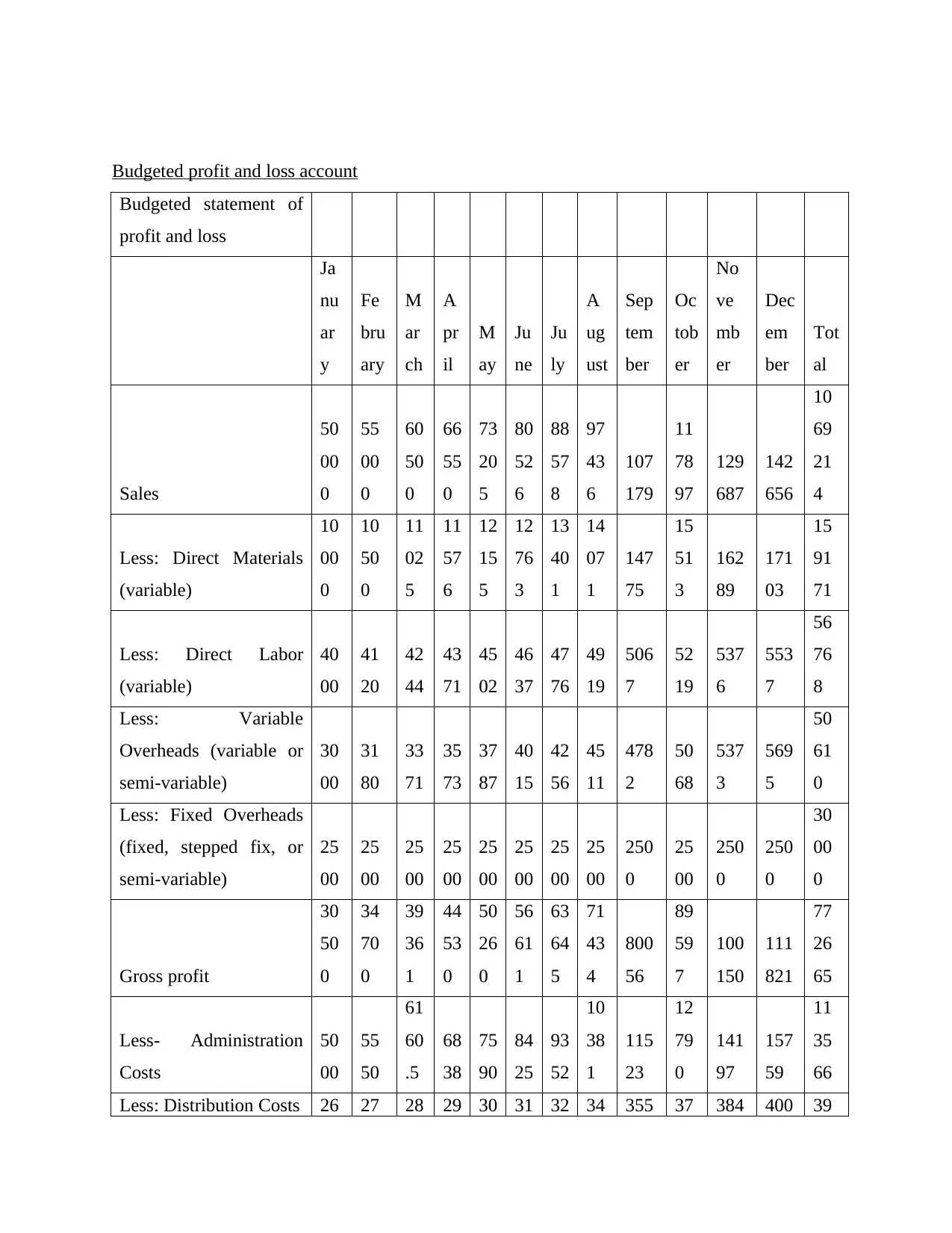

Budgeted profit and loss account.............................................................................................................4

Actual profit and loss account.................................................................................................................5

A pie chart showing the relative size of each of the costs for the year.....................................................7

Graphs for comparing actual outcome with budgeted..............................................................................8

Cost variances........................................................................................................................................11

Actual and budgeted financial statement of position.............................................................................13

Ratio calculation....................................................................................................................................14

Bar charts for different ratios.................................................................................................................15

The report summarizes financial analysis of a factionary company under which data are assumed

to prepare balance sheet and income statement for 12 months. From below done analysis, this

can be stated that company’s performance is better in actual as compared to budgeted data. It has

been proved by help of range of ratios and variances. The report contains detailed information

about analysis of ratio for each aspect including liquidity, profitability and many more. Apart

from this, in the report a detailed statement of balance sheet and profit & loss account is

produced that shows that company’s performance is better under each aspect. Though, there are

some variances which are stating negative result but cannot affect to company’s performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgeted statement of

profit and loss

Ja

nu

ar

y

Fe

bru

ary

M

ar

ch

A

pr

il

M

ay

Ju

ne

Ju

ly

A

ug

ust

Sep

tem

ber

Oc

tob

er

No

ve

mb

er

Dec

em

ber

Tot

al

Sales

50

00

0

55

00

0

60

50

0

66

55

0

73

20

5

80

52

6

88

57

8

97

43

6

107

179

11

78

97

129

687

142

656

10

69

21

4

Less: Direct Materials

(variable)

10

00

0

10

50

0

11

02

5

11

57

6

12

15

5

12

76

3

13

40

1

14

07

1

147

75

15

51

3

162

89

171

03

15

91

71

Less: Direct Labor

(variable)

40

00

41

20

42

44

43

71

45

02

46

37

47

76

49

19

506

7

52

19

537

6

553

7

56

76

8

Less: Variable

Overheads (variable or

semi-variable)

30

00

31

80

33

71

35

73

37

87

40

15

42

56

45

11

478

2

50

68

537

3

569

5

50

61

0

Less: Fixed Overheads

(fixed, stepped fix, or

semi-variable)

25

00

25

00

25

00

25

00

25

00

25

00

25

00

25

00

250

0

25

00

250

0

250

0

30

00

0

Gross profit

30

50

0

34

70

0

39

36

1

44

53

0

50

26

0

56

61

1

63

64

5

71

43

4

800

56

89

59

7

100

150

111

821

77

26

65

Less- Administration

Costs

50

00

55

50

61

60

.5

68

38

75

90

84

25

93

52

10

38

1

115

23

12

79

0

141

97

157

59

11

35

66

Less: Distribution Costs 26 27 28 29 30 31 32 34 355 37 384 400 39

Paraphrase This Document

06

7

Less: Selling Costs

10

00

11

00

12

10

13

31

14

64

16

11

17

72

19

49

214

4

23

58

259

4

285

3

21

38

4

Operating Profit

21

90

0

25

34

6

29

17

8

33

43

6

38

16

4

43

41

2

49

23

2

55

68

4

628

32

70

74

8

795

10

892

06

59

86

48

Less: Finance Costs

40

00

40

40

40

80

41

21

41

62

42

04

42

46

42

89

433

1

43

75

441

8

446

3

50

73

0

Profit Before Tax

17

90

0

21

30

6

25

09

8

29

31

5

34

00

2

39

20

8

44

98

6

51

39

5

585

00

66

37

3

750

92

847

43

54

79

18

Less: Tax (10%)

17

90

21

31

25

10

29

31

34

00

39

21

44

99

51

39

585

0

66

37

750

9

847

4

54

79

2

Profit After Tax

16

11

0

19

17

5

22

58

8

26

38

3

30

60

2

35

28

7

40

48

7

46

25

5

526

50

59

73

6

675

83

762

69

49

31

26

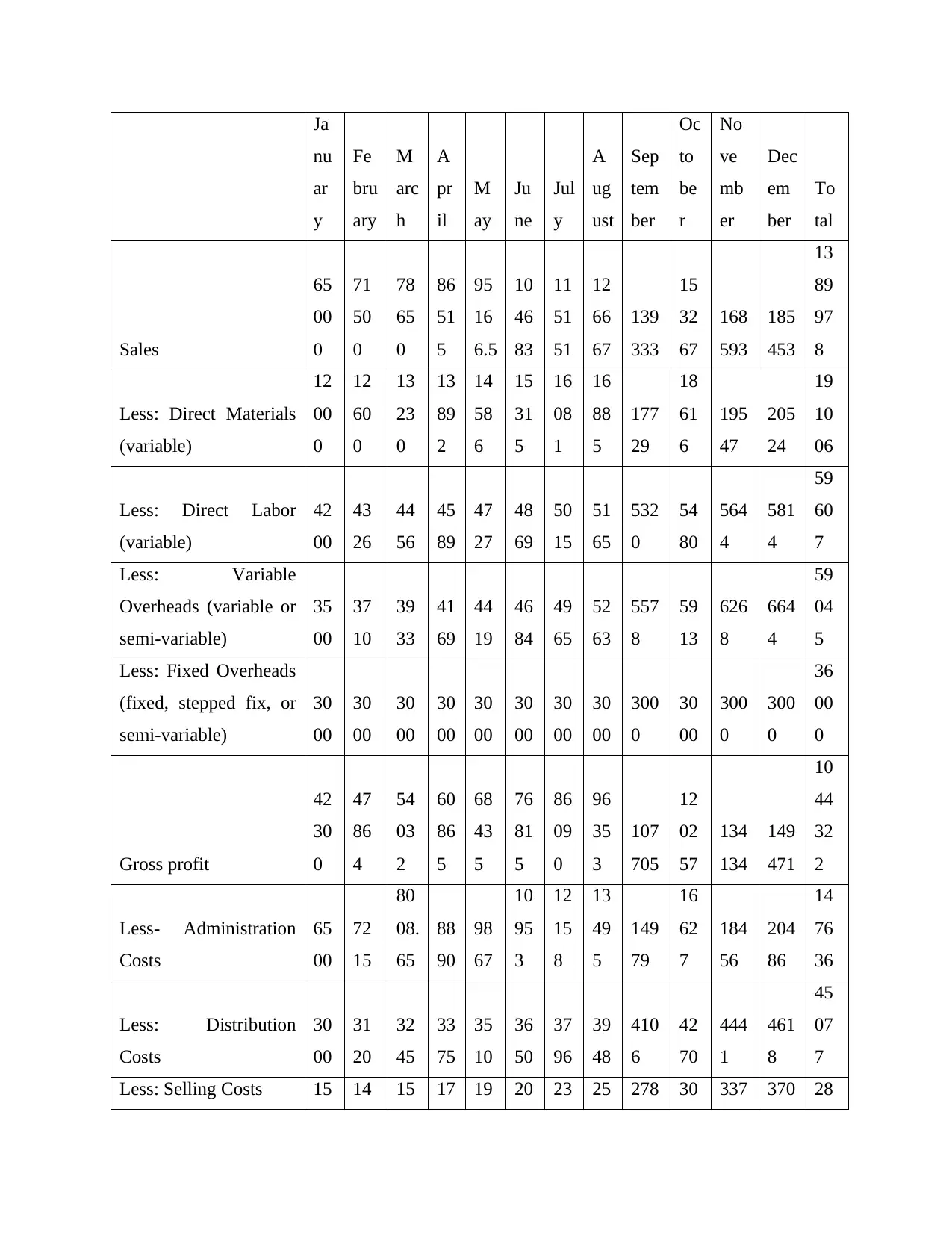

Actual profit and loss account

Actual statement of

profit and loss

nu

ar

y

Fe

bru

ary

M

arc

h

A

pr

il

M

ay

Ju

ne

Jul

y

A

ug

ust

Sep

tem

ber

Oc

to

be

r

No

ve

mb

er

Dec

em

ber

To

tal

Sales

65

00

0

71

50

0

78

65

0

86

51

5

95

16

6.5

10

46

83

11

51

51

12

66

67

139

333

15

32

67

168

593

185

453

13

89

97

8

Less: Direct Materials

(variable)

12

00

0

12

60

0

13

23

0

13

89

2

14

58

6

15

31

5

16

08

1

16

88

5

177

29

18

61

6

195

47

205

24

19

10

06

Less: Direct Labor

(variable)

42

00

43

26

44

56

45

89

47

27

48

69

50

15

51

65

532

0

54

80

564

4

581

4

59

60

7

Less: Variable

Overheads (variable or

semi-variable)

35

00

37

10

39

33

41

69

44

19

46

84

49

65

52

63

557

8

59

13

626

8

664

4

59

04

5

Less: Fixed Overheads

(fixed, stepped fix, or

semi-variable)

30

00

30

00

30

00

30

00

30

00

30

00

30

00

30

00

300

0

30

00

300

0

300

0

36

00

0

Gross profit

42

30

0

47

86

4

54

03

2

60

86

5

68

43

5

76

81

5

86

09

0

96

35

3

107

705

12

02

57

134

134

149

471

10

44

32

2

Less- Administration

Costs

65

00

72

15

80

08.

65

88

90

98

67

10

95

3

12

15

8

13

49

5

149

79

16

62

7

184

56

204

86

14

76

36

Less: Distribution

Costs

30

00

31

20

32

45

33

75

35

10

36

50

37

96

39

48

410

6

42

70

444

1

461

8

45

07

7

Less: Selling Costs 15 14 15 17 19 20 23 25 278 30 337 370 28

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

30

.3 03 94 03 33 7 65 2 9

00

0

Operating Profit

31

30

0

36

09

9

41

20

5

46

87

1

53

15

4

60

11

9

67

83

4

76

37

7

858

33

96

29

5

107

865

120

657

82

36

09

Less: Finance Costs

46

00

46

46

46

92

47

39

47

87

48

35

48

83

49

32

498

1

50

31

508

1

513

2

58

34

0

Profit Before Tax

26

70

0

31

45

3

36

51

3

42

13

2

48

36

7

55

28

4

62

95

1

71

44

5

808

52

91

26

4

102

784

115

525

76

52

69

Less: Tax (10%)

26

70

31

45

36

51

42

13

48

37

55

28

62

95

71

45

808

5

91

26

102

78

115

52

76

52

7

Profit After Tax

24

03

0

28

30

8

32

86

1

37

91

8

43

53

1

49

75

5

56

65

6

64

30

1

727

67

82

13

8

925

06

103

972

68

87

42

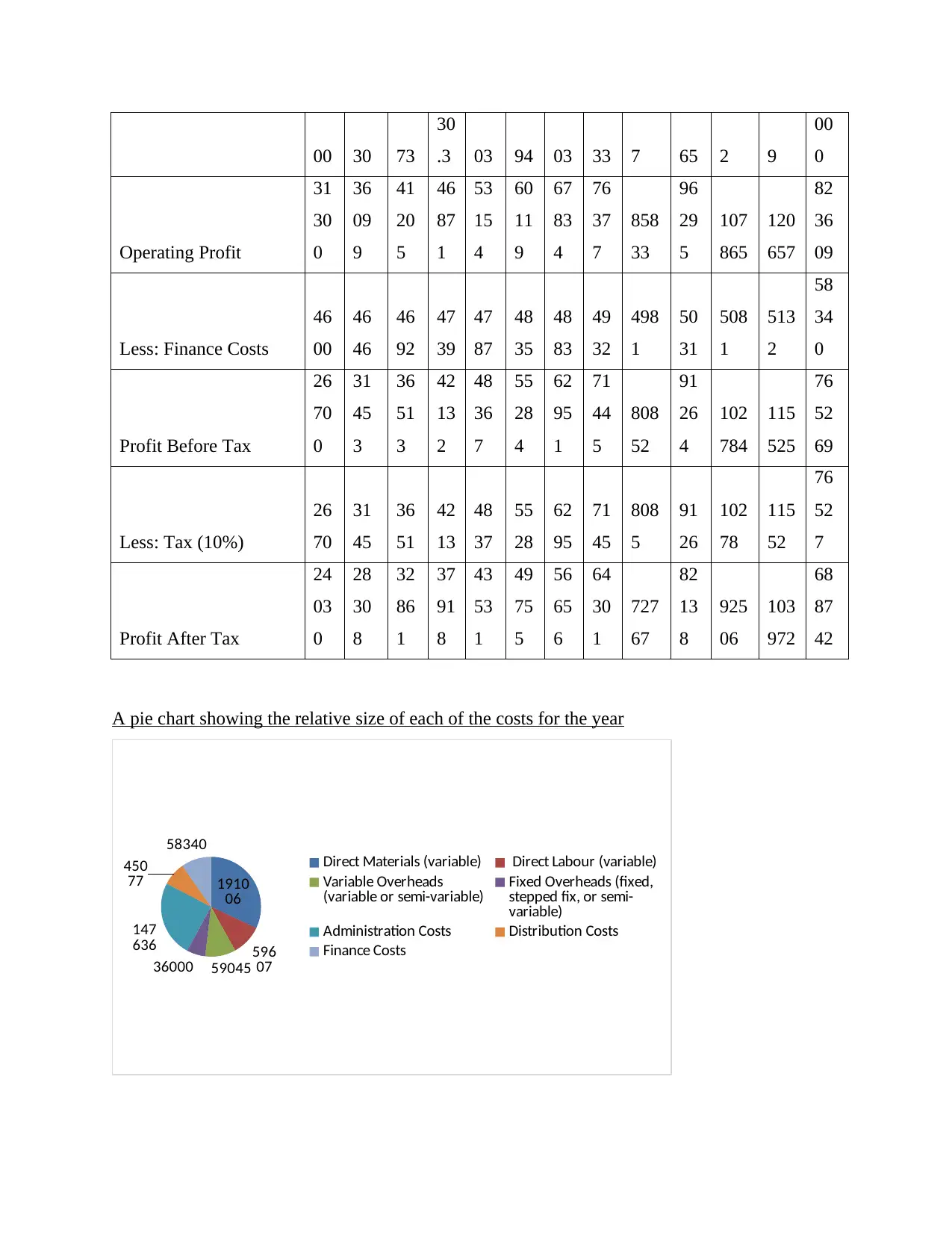

A pie chart showing the relative size of each of the costs for the year

1910

06

596

075904536000

147

636

450

77

58340

Direct Materials (variable) Direct Labour (variable)

Variable Overheads

(variable or semi-variable) Fixed Overheads (fixed,

stepped fix, or semi-

variable)

Administration Costs Distribution Costs

Finance Costs

Paraphrase This Document

higher cost is of direct material that is of 191006 pounds. While lower cost is of 36000 that are

fixed overheads. The pie chart contains information of actual cost that occurred in order to gain

net margin. Each cost volume varies from each other due to different nature and importance.

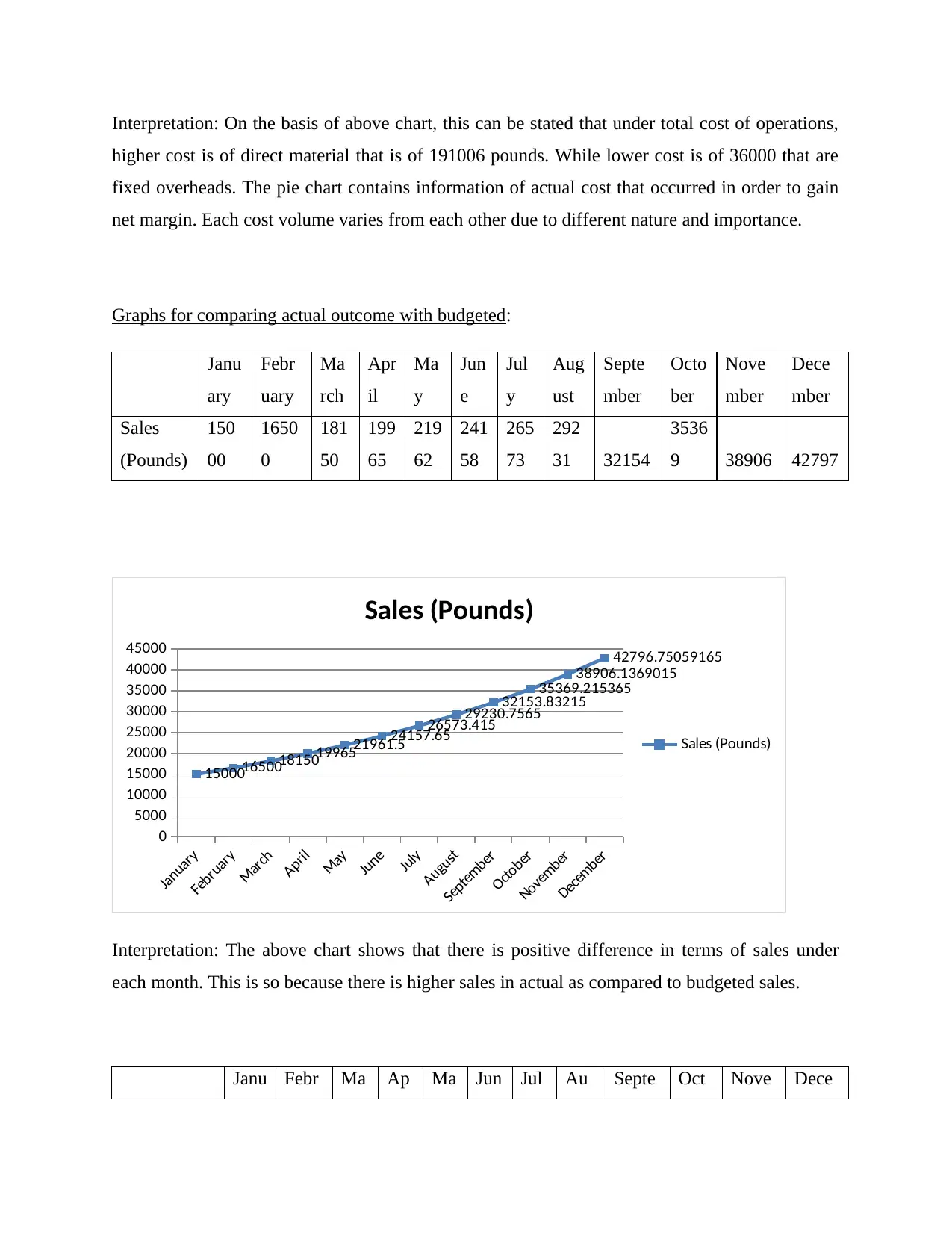

Graphs for comparing actual outcome with budgeted:

Janu

ary

Febr

uary

Ma

rch

Apr

il

Ma

y

Jun

e

Jul

y

Aug

ust

Septe

mber

Octo

ber

Nove

mber

Dece

mber

Sales

(Pounds)

150

00

1650

0

181

50

199

65

219

62

241

58

265

73

292

31 32154

3536

9 38906 42797

January

February

March

April

May

June

July

August

September

October

November

December

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

15000165001815019965

21961.5

24157.65

26573.415

29230.7565

32153.83215

35369.215365

38906.1369015

42796.75059165

Sales (Pounds)

Sales (Pounds)

Interpretation: The above chart shows that there is positive difference in terms of sales under

each month. This is so because there is higher sales in actual as compared to budgeted sales.

Janu Febr Ma Ap Ma Jun Jul Au Septe Oct Nove Dece

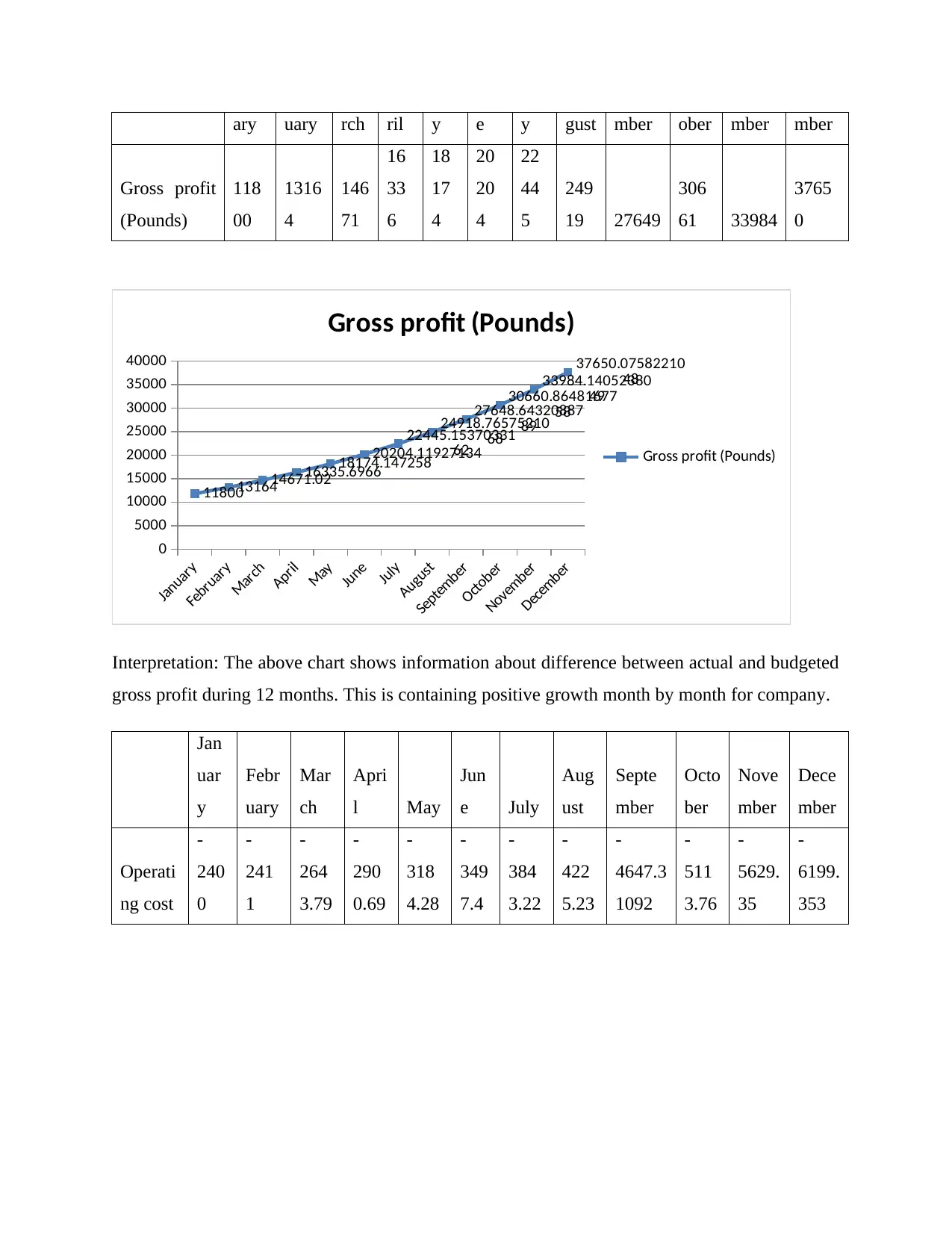

Gross profit

(Pounds)

118

00

1316

4

146

71

16

33

6

18

17

4

20

20

4

22

44

5

249

19 27649

306

61 33984

3765

0

January

February

March

April

May

June

July

August

September

October

November

December

0

5000

10000

15000

20000

25000

30000

35000

40000

118001316414671.0216335.6966

18174.147258

20204.11927134

22445.15370331

62

24918.76575210

68

27648.64320887

89

30660.86481677

58

33984.14052380

49

37650.07582210

48

Gross profit (Pounds)

Gross profit (Pounds)

Interpretation: The above chart shows information about difference between actual and budgeted

gross profit during 12 months. This is containing positive growth month by month for company.

Jan

uar

y

Febr

uary

Mar

ch

Apri

l May

Jun

e July

Aug

ust

Septe

mber

Octo

ber

Nove

mber

Dece

mber

Operati

ng cost

-

240

0

-

241

1

-

264

3.79

-

290

0.69

-

318

4.28

-

349

7.4

-

384

3.22

-

422

5.23

-

4647.3

1092

-

511

3.76

-

5629.

35

-

6199.

353

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

February

March

April

May

June

July

August

September

October

November

December

-7000

-6000

-5000

-4000

-3000

-2000

-1000

0

-2400 -2411 -2643.79

-2900.6921

-3184.279039

-3497.40139361

-3843.2177356399

-4225.2280710424

-

4647.31091773846-

5113.76441884835-

5629.35193110086

-

6199.35257616395

Operating cost

Operating cost

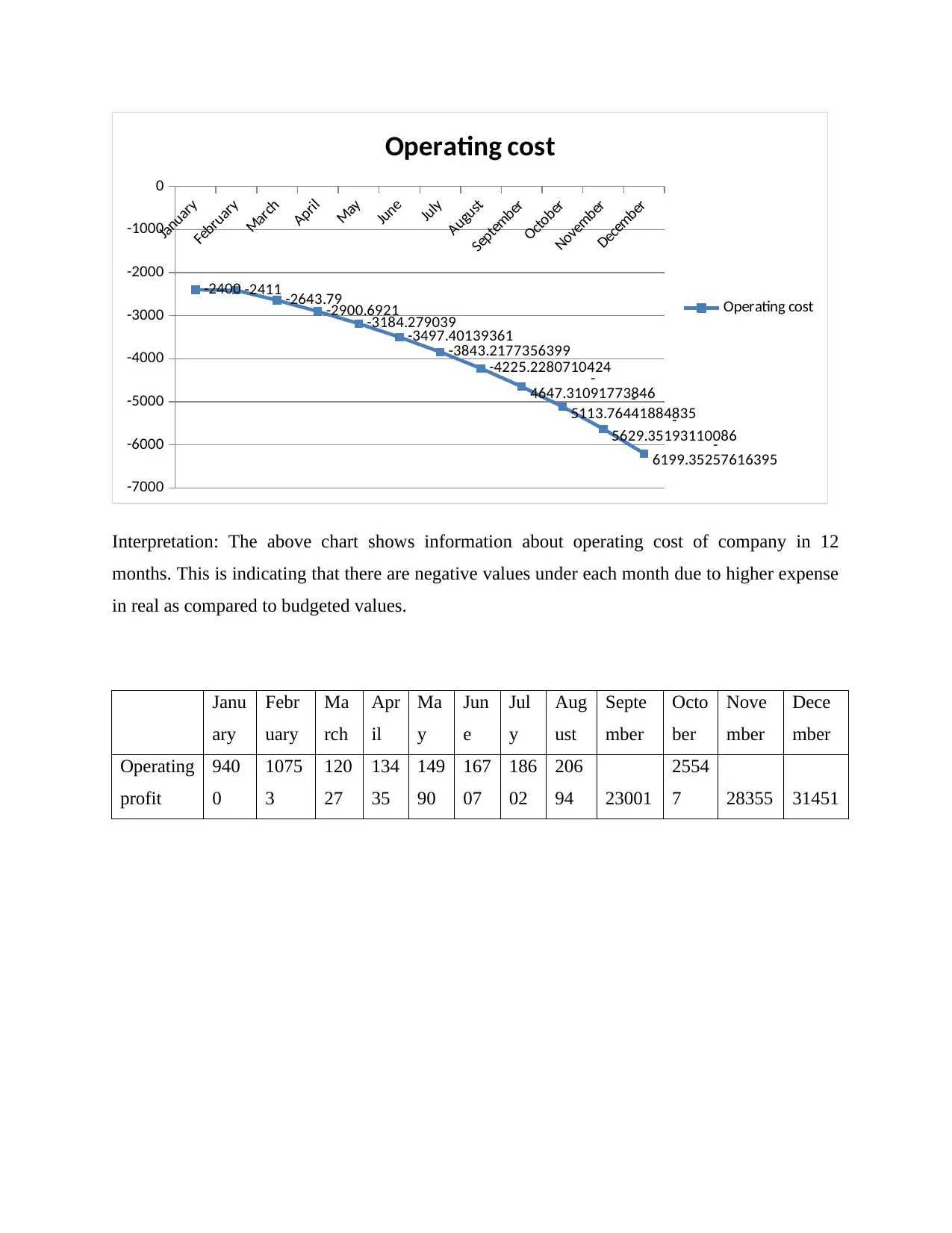

Interpretation: The above chart shows information about operating cost of company in 12

months. This is indicating that there are negative values under each month due to higher expense

in real as compared to budgeted values.

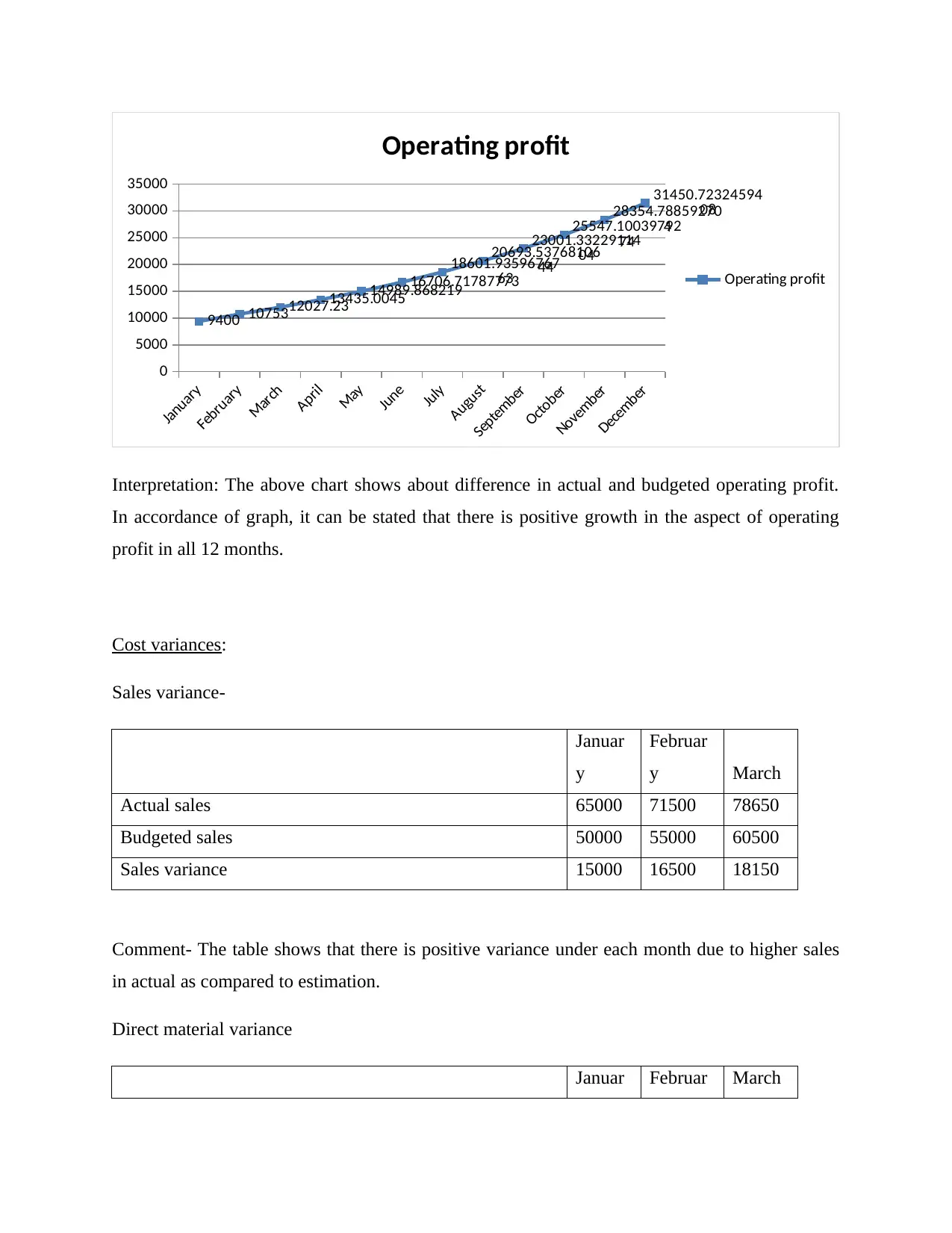

Janu

ary

Febr

uary

Ma

rch

Apr

il

Ma

y

Jun

e

Jul

y

Aug

ust

Septe

mber

Octo

ber

Nove

mber

Dece

mber

Operating

profit

940

0

1075

3

120

27

134

35

149

90

167

07

186

02

206

94 23001

2554

7 28355 31451

Paraphrase This Document

February

March

April

May

June

July

August

September

October

November

December

0

5000

10000

15000

20000

25000

30000

35000

9400 1075312027.2313435.0045

14989.868219

16706.71787773

18601.93596767

63

20693.53768106

44

23001.33229114

04

25547.10039792

74

28354.78859270

4

31450.72324594

08

Operating profit

Operating profit

Interpretation: The above chart shows about difference in actual and budgeted operating profit.

In accordance of graph, it can be stated that there is positive growth in the aspect of operating

profit in all 12 months.

Cost variances:

Sales variance-

Januar

y

Februar

y March

Actual sales 65000 71500 78650

Budgeted sales 50000 55000 60500

Sales variance 15000 16500 18150

Comment- The table shows that there is positive variance under each month due to higher sales

in actual as compared to estimation.

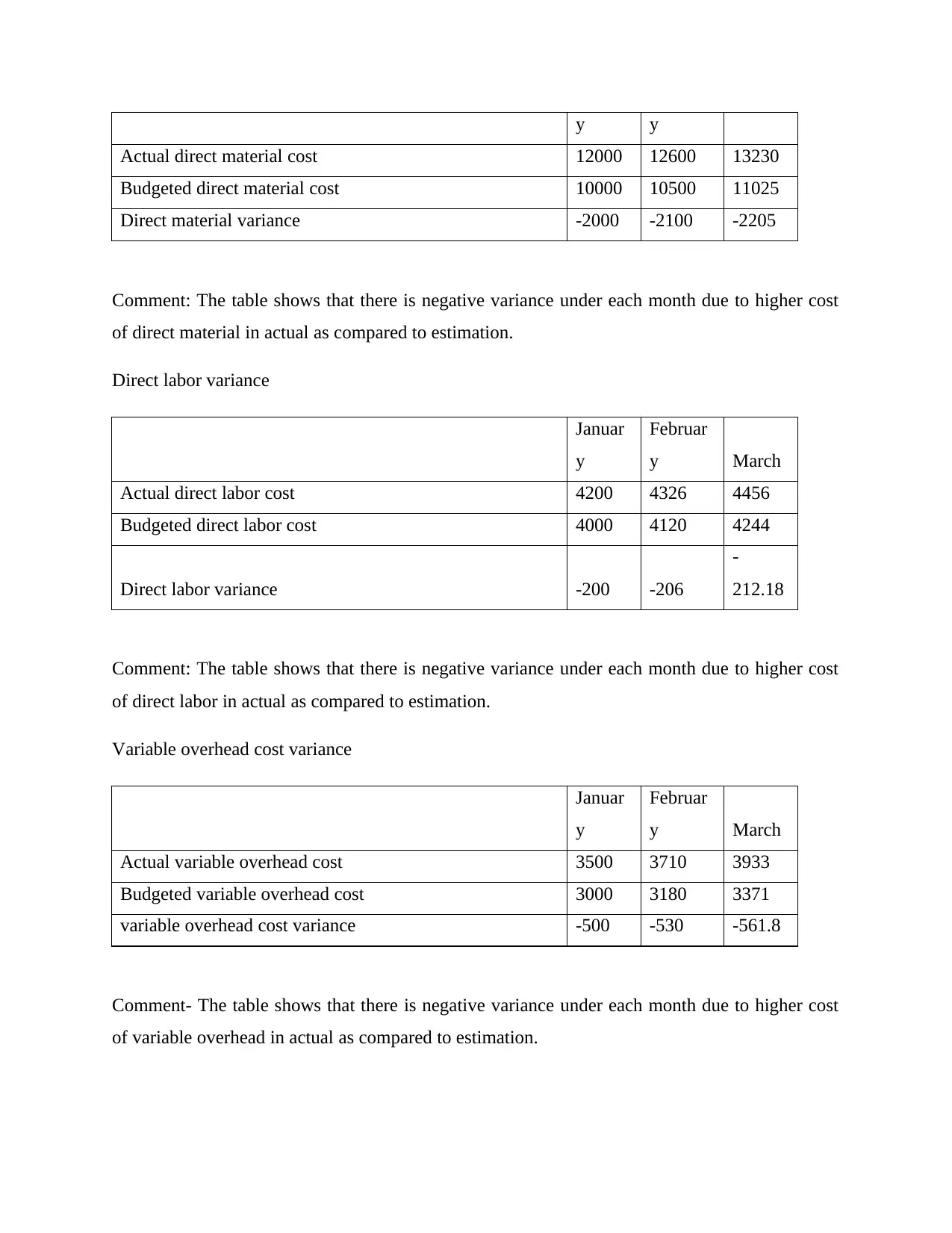

Direct material variance

Januar Februar March

Actual direct material cost 12000 12600 13230

Budgeted direct material cost 10000 10500 11025

Direct material variance -2000 -2100 -2205

Comment: The table shows that there is negative variance under each month due to higher cost

of direct material in actual as compared to estimation.

Direct labor variance

Januar

y

Februar

y March

Actual direct labor cost 4200 4326 4456

Budgeted direct labor cost 4000 4120 4244

Direct labor variance -200 -206

-

212.18

Comment: The table shows that there is negative variance under each month due to higher cost

of direct labor in actual as compared to estimation.

Variable overhead cost variance

Januar

y

Februar

y March

Actual variable overhead cost 3500 3710 3933

Budgeted variable overhead cost 3000 3180 3371

variable overhead cost variance -500 -530 -561.8

Comment- The table shows that there is negative variance under each month due to higher cost

of variable overhead in actual as compared to estimation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

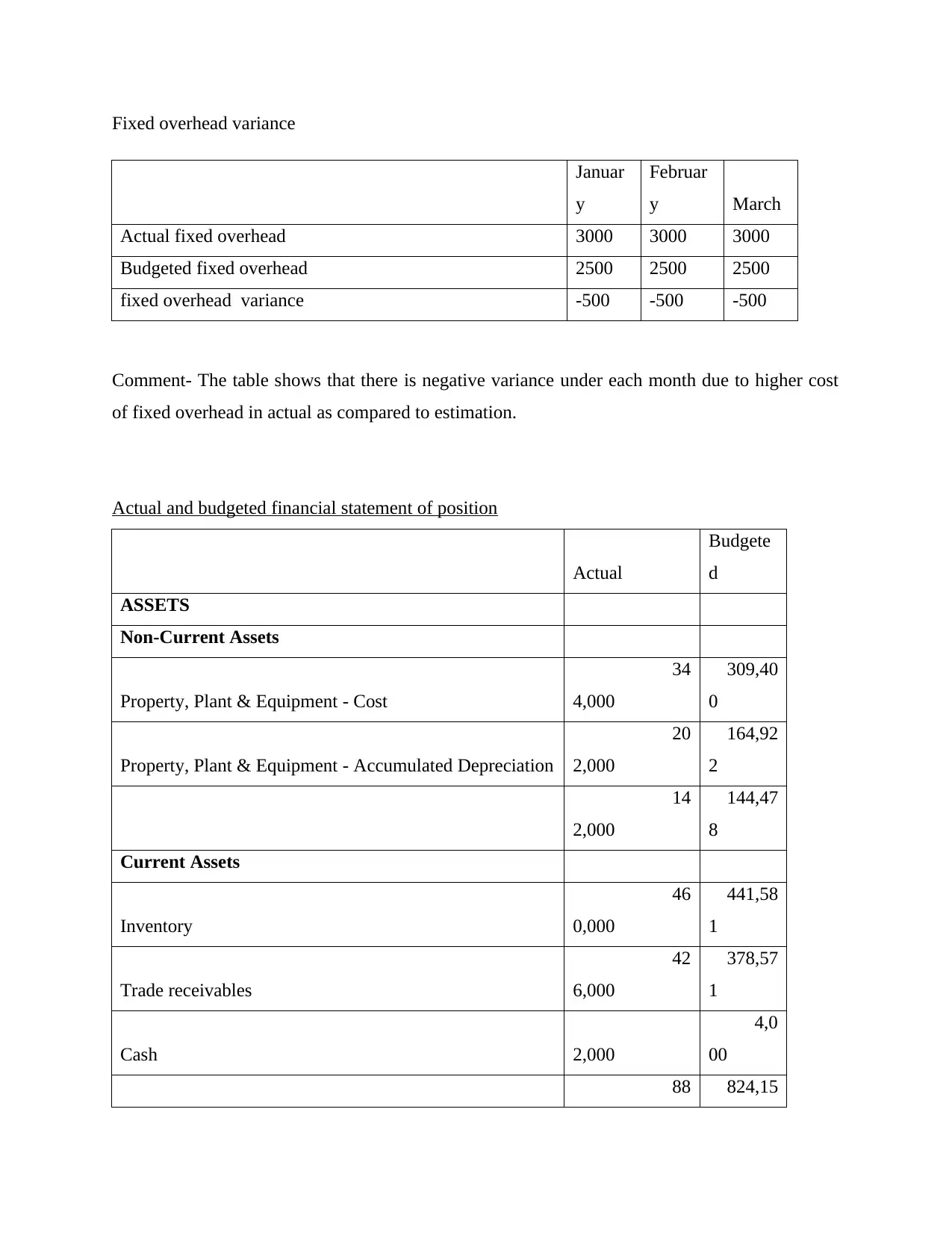

Januar

y

Februar

y March

Actual fixed overhead 3000 3000 3000

Budgeted fixed overhead 2500 2500 2500

fixed overhead variance -500 -500 -500

Comment- The table shows that there is negative variance under each month due to higher cost

of fixed overhead in actual as compared to estimation.

Actual and budgeted financial statement of position

Actual

Budgete

d

ASSETS

Non-Current Assets

Property, Plant & Equipment - Cost

34

4,000

309,40

0

Property, Plant & Equipment - Accumulated Depreciation

20

2,000

164,92

2

14

2,000

144,47

8

Current Assets

Inventory

46

0,000

441,58

1

Trade receivables

42

6,000

378,57

1

Cash 2,000

4,0

00

88 824,15

Paraphrase This Document

Total Assets

1,03

0,000

968,63

0

EQUITY & LIABILITIES

Equity

Shareholders' Capital

35

0,000

380,00

0

Non-Current Liabilities

Bank loan

43

5,000

316,50

0

78

5,000

490,00

0

Current Liabilities

Trade payables

24

5,000

478,63

0

Total equity and Liabilities

1,03

0,000

968,63

0

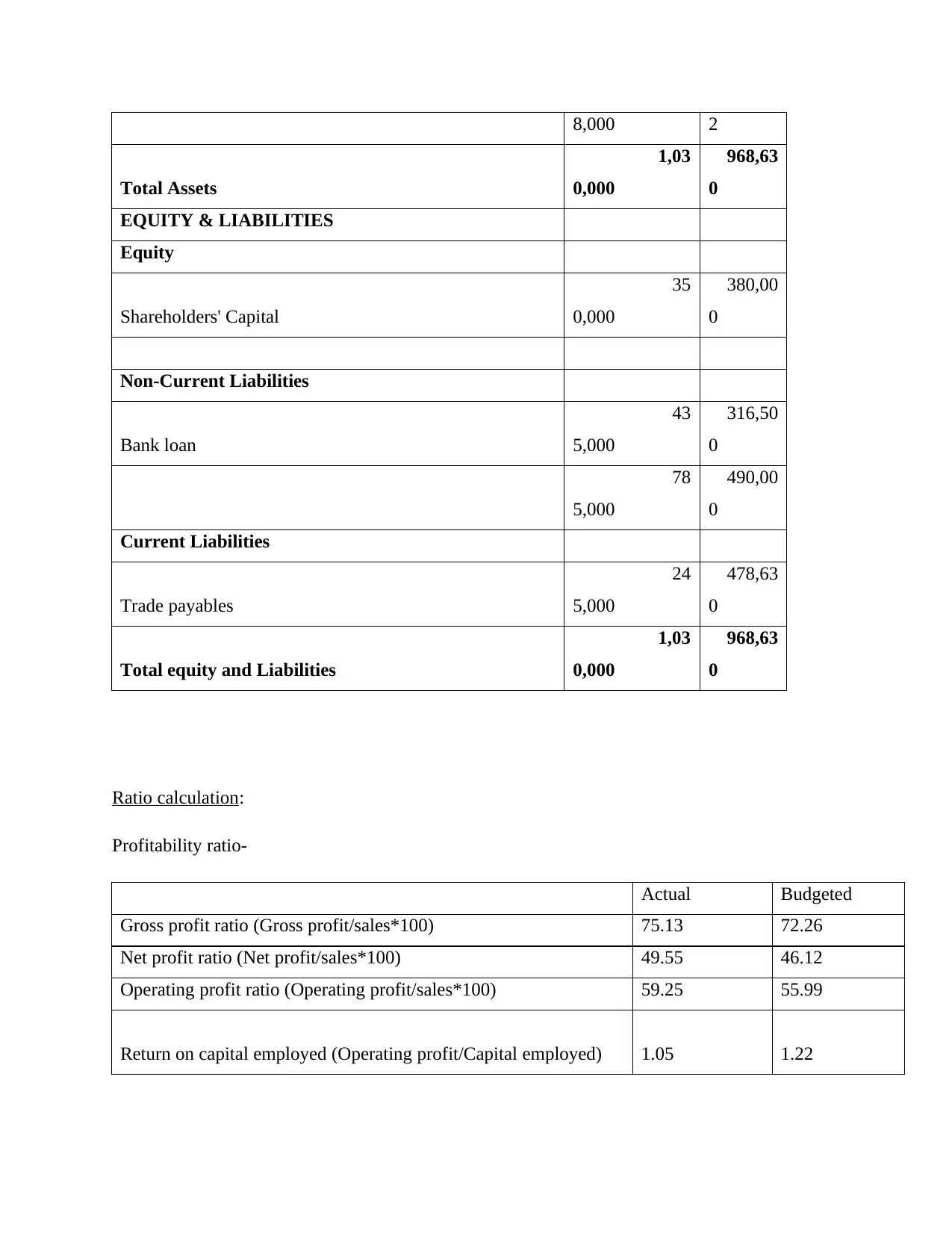

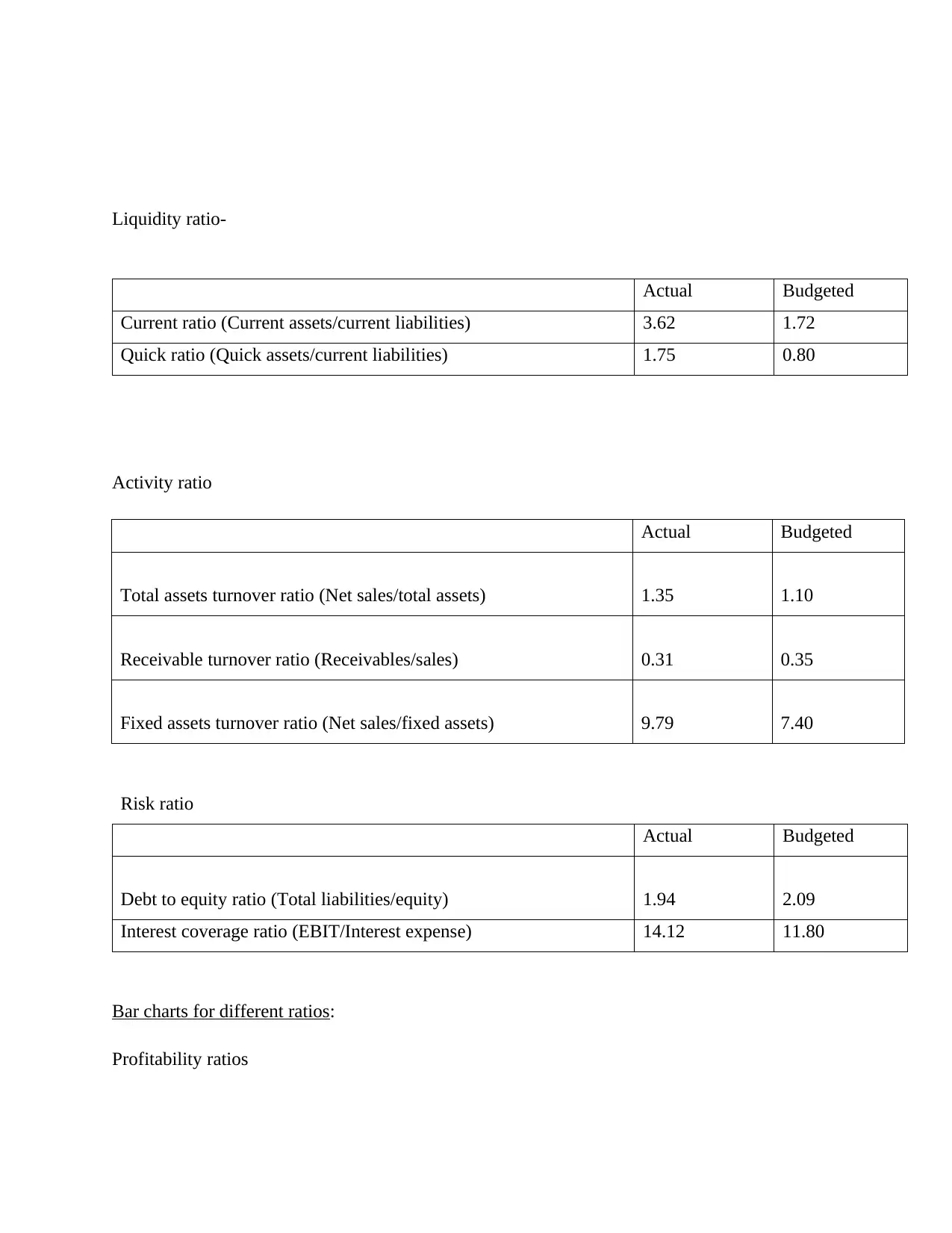

Ratio calculation:

Profitability ratio-

Actual Budgeted

Gross profit ratio (Gross profit/sales*100) 75.13 72.26

Net profit ratio (Net profit/sales*100) 49.55 46.12

Operating profit ratio (Operating profit/sales*100) 59.25 55.99

Return on capital employed (Operating profit/Capital employed) 1.05 1.22

Actual Budgeted

Current ratio (Current assets/current liabilities) 3.62 1.72

Quick ratio (Quick assets/current liabilities) 1.75 0.80

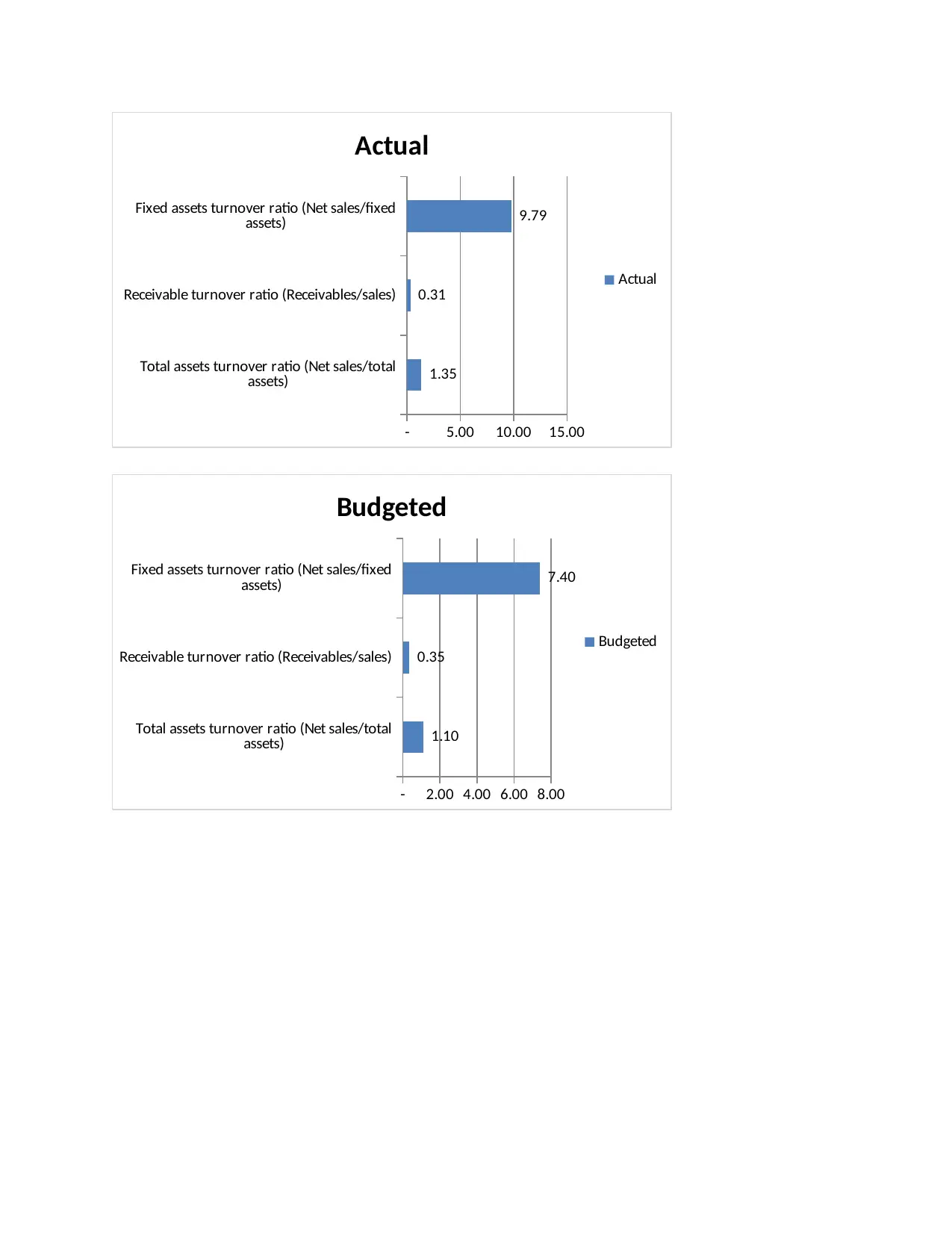

Activity ratio

Actual Budgeted

Total assets turnover ratio (Net sales/total assets) 1.35 1.10

Receivable turnover ratio (Receivables/sales) 0.31 0.35

Fixed assets turnover ratio (Net sales/fixed assets) 9.79 7.40

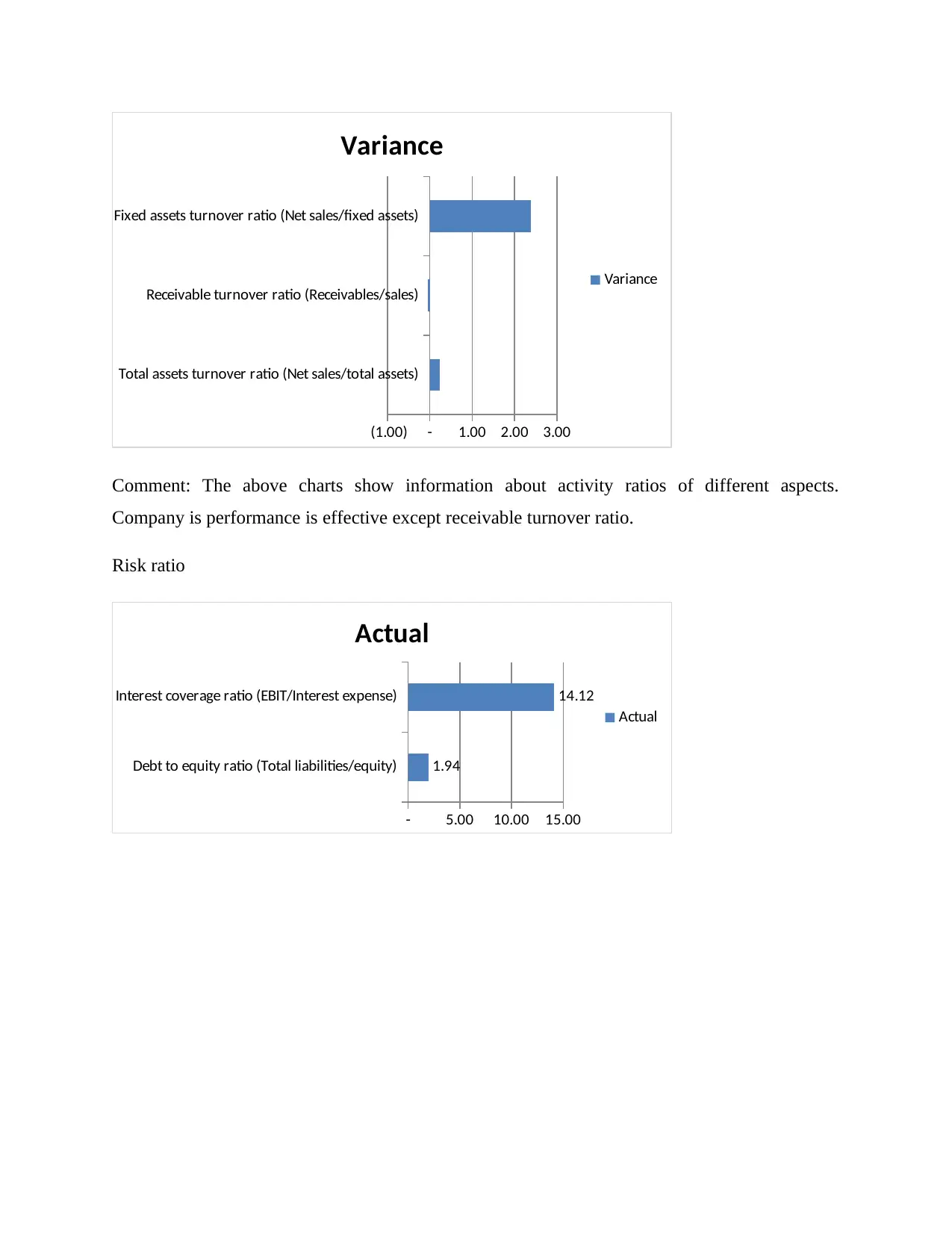

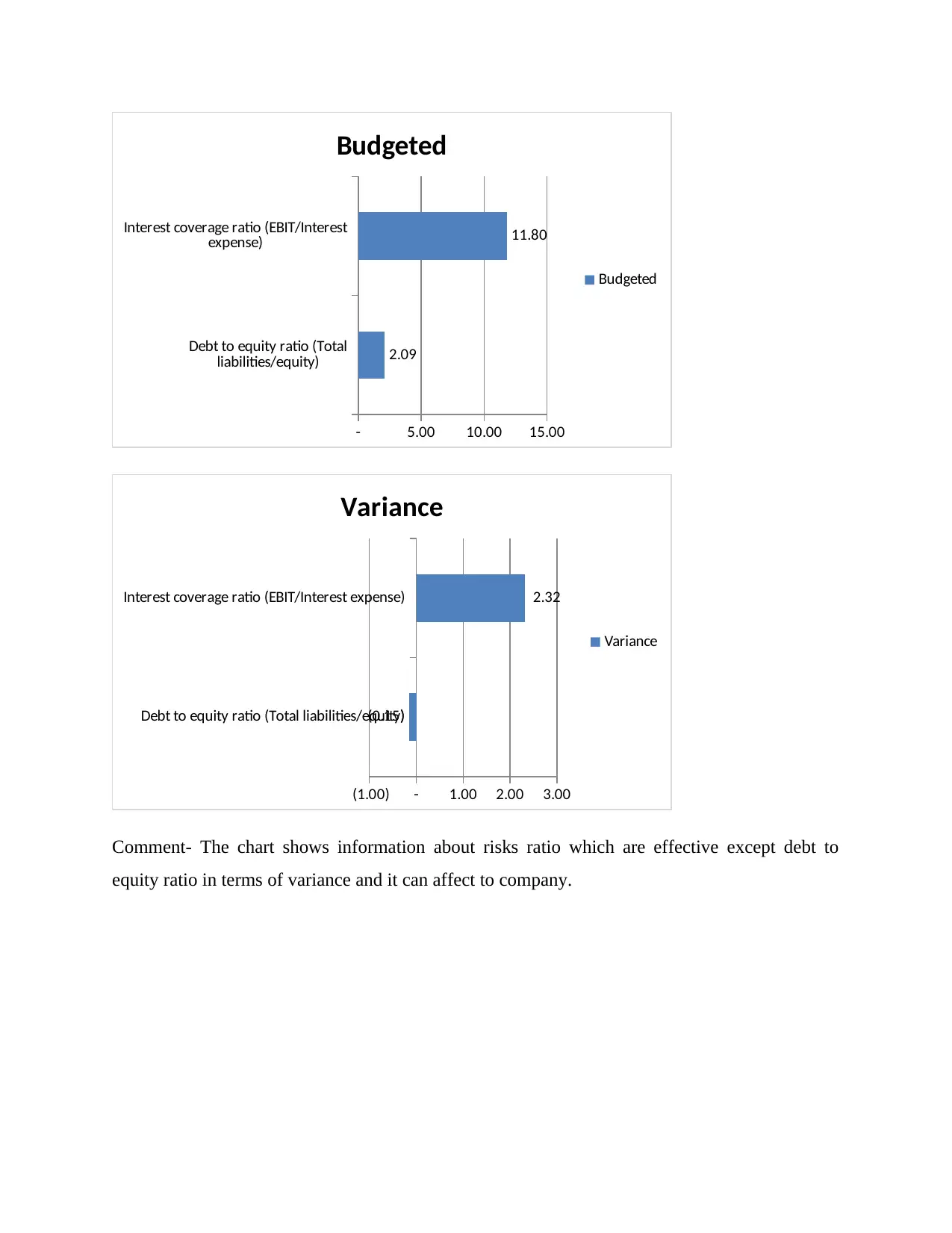

Risk ratio

Actual Budgeted

Debt to equity ratio (Total liabilities/equity) 1.94 2.09

Interest coverage ratio (EBIT/Interest expense) 14.12 11.80

Bar charts for different ratios:

Profitability ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit ratio (Net profit/sales*100)

Operating profit ratio (Operating

profit/sales*100)

Return on capital employed (Operating

profit/Capital employed)

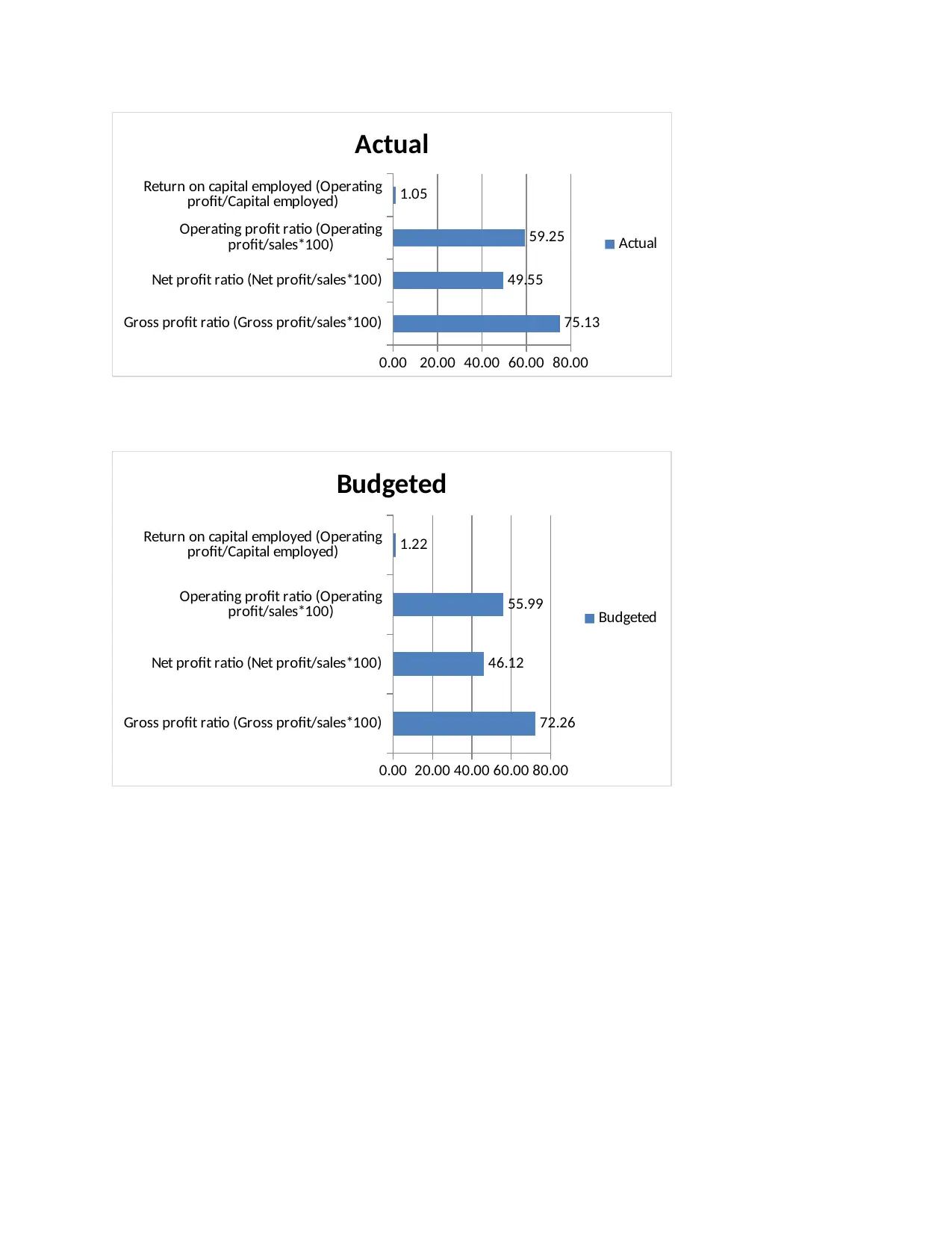

0.00 20.00 40.00 60.00 80.00

75.13

49.55

59.25

1.05

Actual

Actual

Gross profit ratio (Gross profit/sales*100)

Net profit ratio (Net profit/sales*100)

Operating profit ratio (Operating

profit/sales*100)

Return on capital employed (Operating

profit/Capital employed)

0.00 20.00 40.00 60.00 80.00

72.26

46.12

55.99

1.22

Budgeted

Budgeted

Paraphrase This Document

Net profit ratio (Net profit/sales*100)

Operating profit ratio (Operating profit/sales*100)

Return on capital employed (Operating profit/Capital

employed)

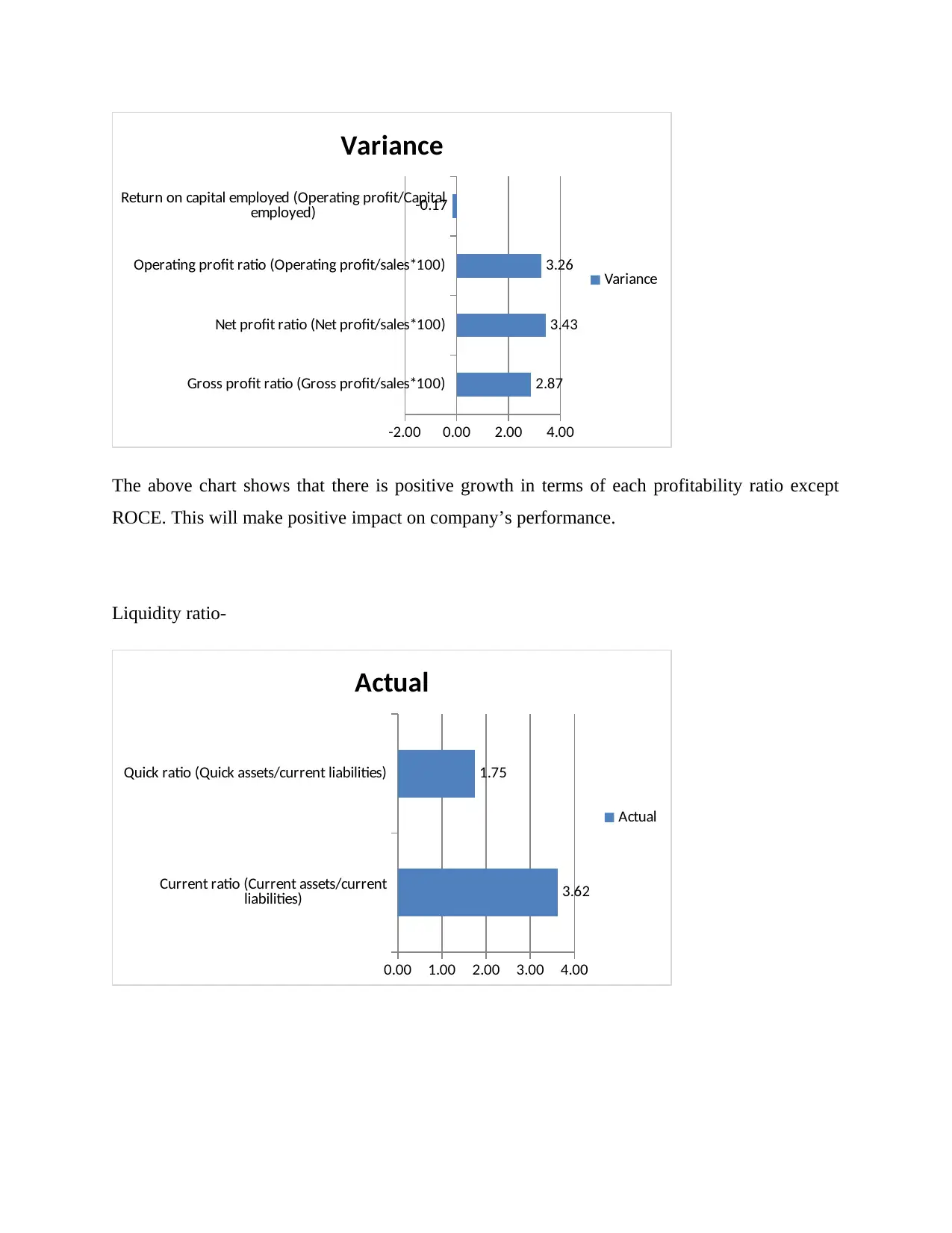

-2.00 0.00 2.00 4.00

2.87

3.43

3.26

-0.17

Variance

Variance

The above chart shows that there is positive growth in terms of each profitability ratio except

ROCE. This will make positive impact on company’s performance.

Liquidity ratio-

Current ratio (Current assets/current

liabilities)

Quick ratio (Quick assets/current liabilities)

0.00 1.00 2.00 3.00 4.00

3.62

1.75

Actual

Actual

liabilities)

Quick ratio (Quick assets/current liabilities)

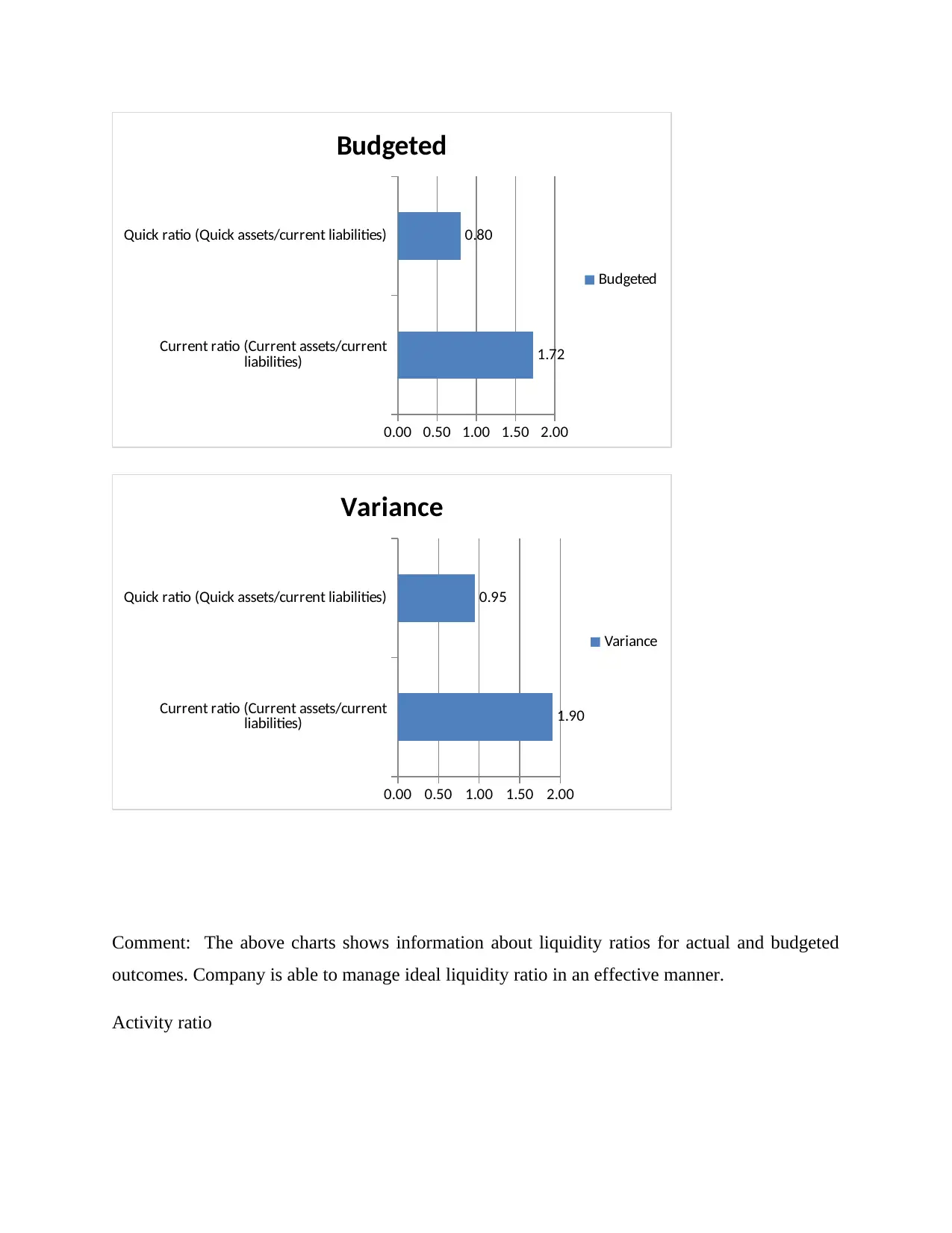

0.00 0.50 1.00 1.50 2.00

1.72

0.80

Budgeted

Budgeted

Current ratio (Current assets/current

liabilities)

Quick ratio (Quick assets/current liabilities)

0.00 0.50 1.00 1.50 2.00

1.90

0.95

Variance

Variance

Comment: The above charts shows information about liquidity ratios for actual and budgeted

outcomes. Company is able to manage ideal liquidity ratio in an effective manner.

Activity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assets)

Receivable turnover ratio (Receivables/sales)

Fixed assets turnover ratio (Net sales/fixed

assets)

- 5.00 10.00 15.00

1.35

0.31

9.79

Actual

Actual

Total assets turnover ratio (Net sales/total

assets)

Receivable turnover ratio (Receivables/sales)

Fixed assets turnover ratio (Net sales/fixed

assets)

- 2.00 4.00 6.00 8.00

1.10

0.35

7.40

Budgeted

Budgeted

Paraphrase This Document

Receivable turnover ratio (Receivables/sales)

Fixed assets turnover ratio (Net sales/fixed assets)

(1.00) - 1.00 2.00 3.00

Variance

Variance

Comment: The above charts show information about activity ratios of different aspects.

Company is performance is effective except receivable turnover ratio.

Risk ratio

Debt to equity ratio (Total liabilities/equity)

Interest coverage ratio (EBIT/Interest expense)

- 5.00 10.00 15.00

1.94

14.12

Actual

Actual

liabilities/equity)

Interest coverage ratio (EBIT/Interest

expense)

- 5.00 10.00 15.00

2.09

11.80

Budgeted

Budgeted

Debt to equity ratio (Total liabilities/equity)

Interest coverage ratio (EBIT/Interest expense)

(1.00) - 1.00 2.00 3.00

(0.15)

2.32

Variance

Variance

Comment- The chart shows information about risks ratio which are effective except debt to

equity ratio in terms of variance and it can affect to company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.