Business Report: Investment Appraisal, Funding & Procurement for K plc

VerifiedAdded on 2023/06/16

|15

|3826

|133

Report

AI Summary

This business report provides a comprehensive analysis of K plc's investment appraisal, funding options, cost variance, and procurement strategies. Task A evaluates several investment projects using payback period and net present value (NPV) methods, ranking them and recommending a project based on these analyses while also discussing the strengths and weaknesses of each method and qualitative factors for consideration. Task B suggests and discusses alternative funding methods for K plc's acquisition plans. Task C presents a full variance analysis of variable cost elements, offering possible explanations for the identified variances. Finally, Task D distinguishes between centralized and decentralized procurement, discussing the benefits of each approach. The report concludes with key findings and recommendations for K plc.

Business Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK A...........................................................................................................................................3

a) Calculation of Payback period for all projects........................................................................3

b) Calculation of Net present value for all projects. ..................................................................4

c) Ranking the projects on the basis of payback and net present value......................................5

d) Which project may be selected if projects are mutually exclusive? Explain your

recommendation..........................................................................................................................6

e) Discuss the strengths and weakness of payback and net present value methods in the

context of investment appraisal...................................................................................................6

f) Discuss five qualitative factors which the directors may need to consider before making a

final Decision..............................................................................................................................7

TASK B...........................................................................................................................................8

a) Suggest 3 alternative methods of funding...............................................................................8

b) Critically discuss the link between the above financing decision..........................................9

TASK C...........................................................................................................................................9

a) Prepare a full variance analysis statement of the variable cost elements................................9

b) From the available information suggest possible explanations for the variances identified.

...................................................................................................................................................11

TASK D.........................................................................................................................................11

Distinguish between centralised and decentralised procurement. Discuss the benefits of

centralised purchasing and decentralised purchasing...............................................................11

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

TASK A...........................................................................................................................................3

a) Calculation of Payback period for all projects........................................................................3

b) Calculation of Net present value for all projects. ..................................................................4

c) Ranking the projects on the basis of payback and net present value......................................5

d) Which project may be selected if projects are mutually exclusive? Explain your

recommendation..........................................................................................................................6

e) Discuss the strengths and weakness of payback and net present value methods in the

context of investment appraisal...................................................................................................6

f) Discuss five qualitative factors which the directors may need to consider before making a

final Decision..............................................................................................................................7

TASK B...........................................................................................................................................8

a) Suggest 3 alternative methods of funding...............................................................................8

b) Critically discuss the link between the above financing decision..........................................9

TASK C...........................................................................................................................................9

a) Prepare a full variance analysis statement of the variable cost elements................................9

b) From the available information suggest possible explanations for the variances identified.

...................................................................................................................................................11

TASK D.........................................................................................................................................11

Distinguish between centralised and decentralised procurement. Discuss the benefits of

centralised purchasing and decentralised purchasing...............................................................11

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Business report refers to a series of information about a company's operations, production and

insights about what the company plans for future. This report contains mostly the historical data

about the company's working (Grefen and et. al., 2019). It helps the different users of this report

to critically analyse the options that they are available with to conclude a decision. It is taking

future decisions on the factual historical data present in the business report. In this report, the

main focus is on the different information which is accounting and operational of K plc. The

report is divided into four parts, part A researches the project which k plc. should invest in. part

B talks about the financing that the company can go with. Part C evaluates the company's cost

variances and Part D highlights the general overview of centralised and decentralised

procurement.

TASK A

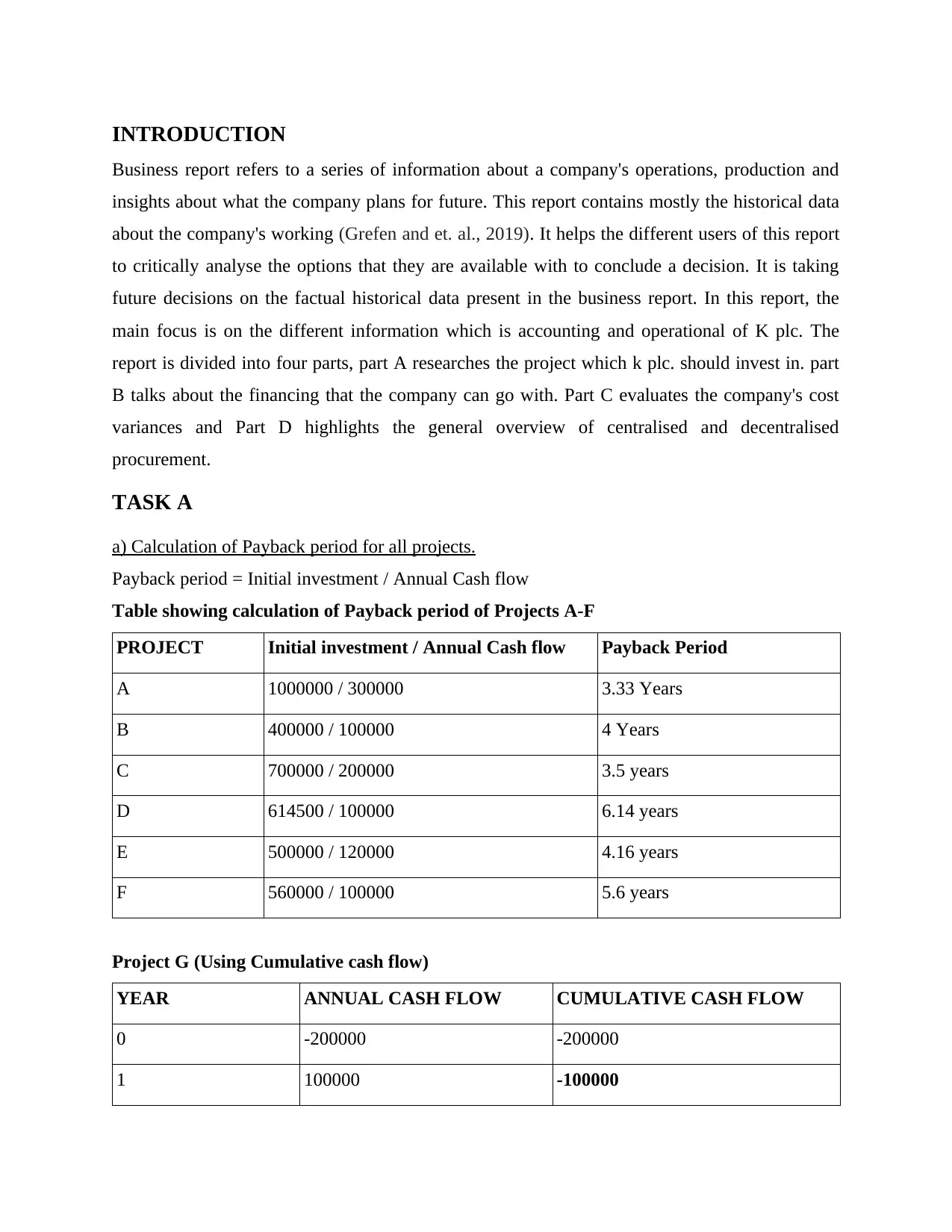

a) Calculation of Payback period for all projects.

Payback period = Initial investment / Annual Cash flow

Table showing calculation of Payback period of Projects A-F

PROJECT Initial investment / Annual Cash flow Payback Period

A 1000000 / 300000 3.33 Years

B 400000 / 100000 4 Years

C 700000 / 200000 3.5 years

D 614500 / 100000 6.14 years

E 500000 / 120000 4.16 years

F 560000 / 100000 5.6 years

Project G (Using Cumulative cash flow)

YEAR ANNUAL CASH FLOW CUMULATIVE CASH FLOW

0 -200000 -200000

1 100000 -100000

Business report refers to a series of information about a company's operations, production and

insights about what the company plans for future. This report contains mostly the historical data

about the company's working (Grefen and et. al., 2019). It helps the different users of this report

to critically analyse the options that they are available with to conclude a decision. It is taking

future decisions on the factual historical data present in the business report. In this report, the

main focus is on the different information which is accounting and operational of K plc. The

report is divided into four parts, part A researches the project which k plc. should invest in. part

B talks about the financing that the company can go with. Part C evaluates the company's cost

variances and Part D highlights the general overview of centralised and decentralised

procurement.

TASK A

a) Calculation of Payback period for all projects.

Payback period = Initial investment / Annual Cash flow

Table showing calculation of Payback period of Projects A-F

PROJECT Initial investment / Annual Cash flow Payback Period

A 1000000 / 300000 3.33 Years

B 400000 / 100000 4 Years

C 700000 / 200000 3.5 years

D 614500 / 100000 6.14 years

E 500000 / 120000 4.16 years

F 560000 / 100000 5.6 years

Project G (Using Cumulative cash flow)

YEAR ANNUAL CASH FLOW CUMULATIVE CASH FLOW

0 -200000 -200000

1 100000 -100000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

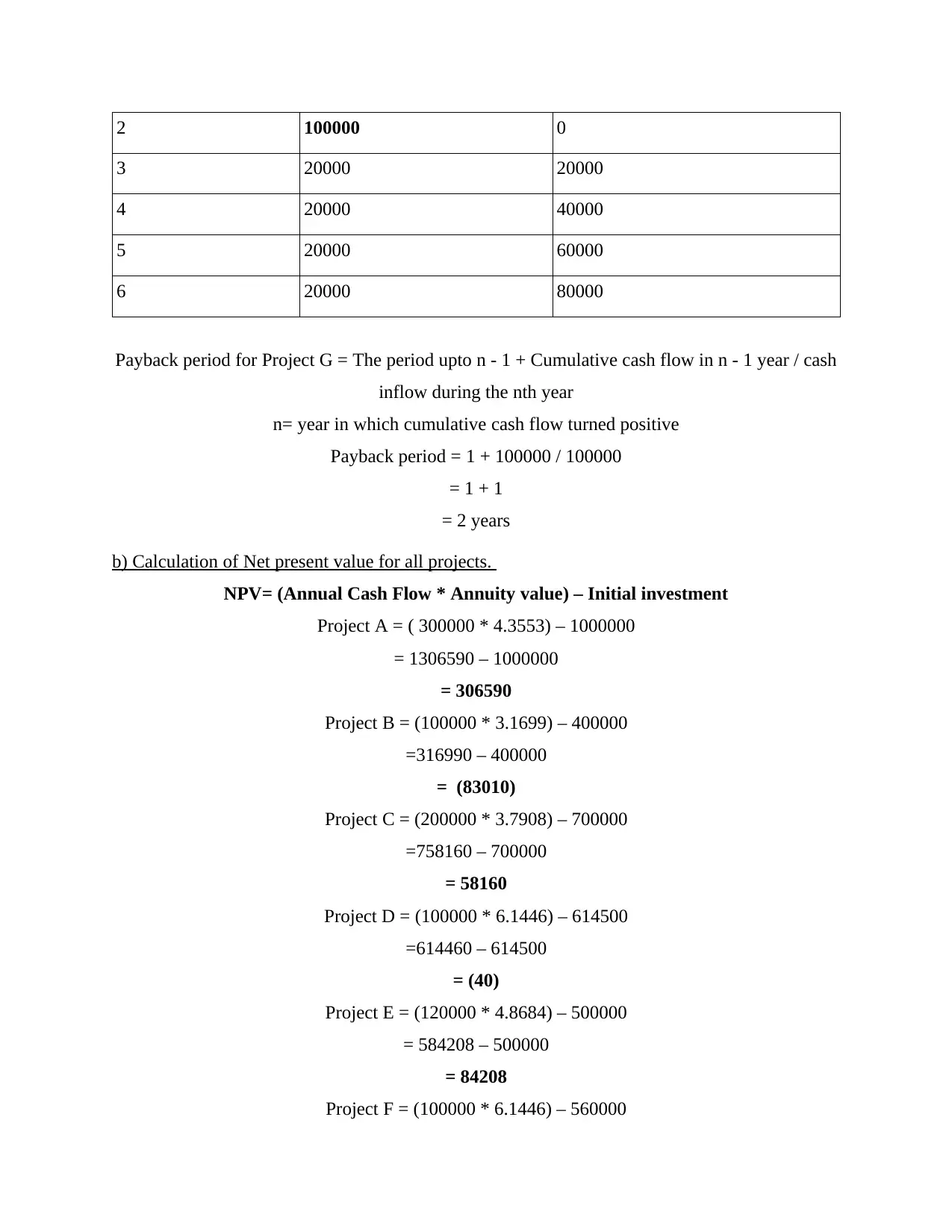

2 100000 0

3 20000 20000

4 20000 40000

5 20000 60000

6 20000 80000

Payback period for Project G = The period upto n - 1 + Cumulative cash flow in n - 1 year / cash

inflow during the nth year

n= year in which cumulative cash flow turned positive

Payback period = 1 + 100000 / 100000

= 1 + 1

= 2 years

b) Calculation of Net present value for all projects.

NPV= (Annual Cash Flow * Annuity value) – Initial investment

Project A = ( 300000 * 4.3553) – 1000000

= 1306590 – 1000000

= 306590

Project B = (100000 * 3.1699) – 400000

=316990 – 400000

= (83010)

Project C = (200000 * 3.7908) – 700000

=758160 – 700000

= 58160

Project D = (100000 * 6.1446) – 614500

=614460 – 614500

= (40)

Project E = (120000 * 4.8684) – 500000

= 584208 – 500000

= 84208

Project F = (100000 * 6.1446) – 560000

3 20000 20000

4 20000 40000

5 20000 60000

6 20000 80000

Payback period for Project G = The period upto n - 1 + Cumulative cash flow in n - 1 year / cash

inflow during the nth year

n= year in which cumulative cash flow turned positive

Payback period = 1 + 100000 / 100000

= 1 + 1

= 2 years

b) Calculation of Net present value for all projects.

NPV= (Annual Cash Flow * Annuity value) – Initial investment

Project A = ( 300000 * 4.3553) – 1000000

= 1306590 – 1000000

= 306590

Project B = (100000 * 3.1699) – 400000

=316990 – 400000

= (83010)

Project C = (200000 * 3.7908) – 700000

=758160 – 700000

= 58160

Project D = (100000 * 6.1446) – 614500

=614460 – 614500

= (40)

Project E = (120000 * 4.8684) – 500000

= 584208 – 500000

= 84208

Project F = (100000 * 6.1446) – 560000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=614460 – 560000

= 54460

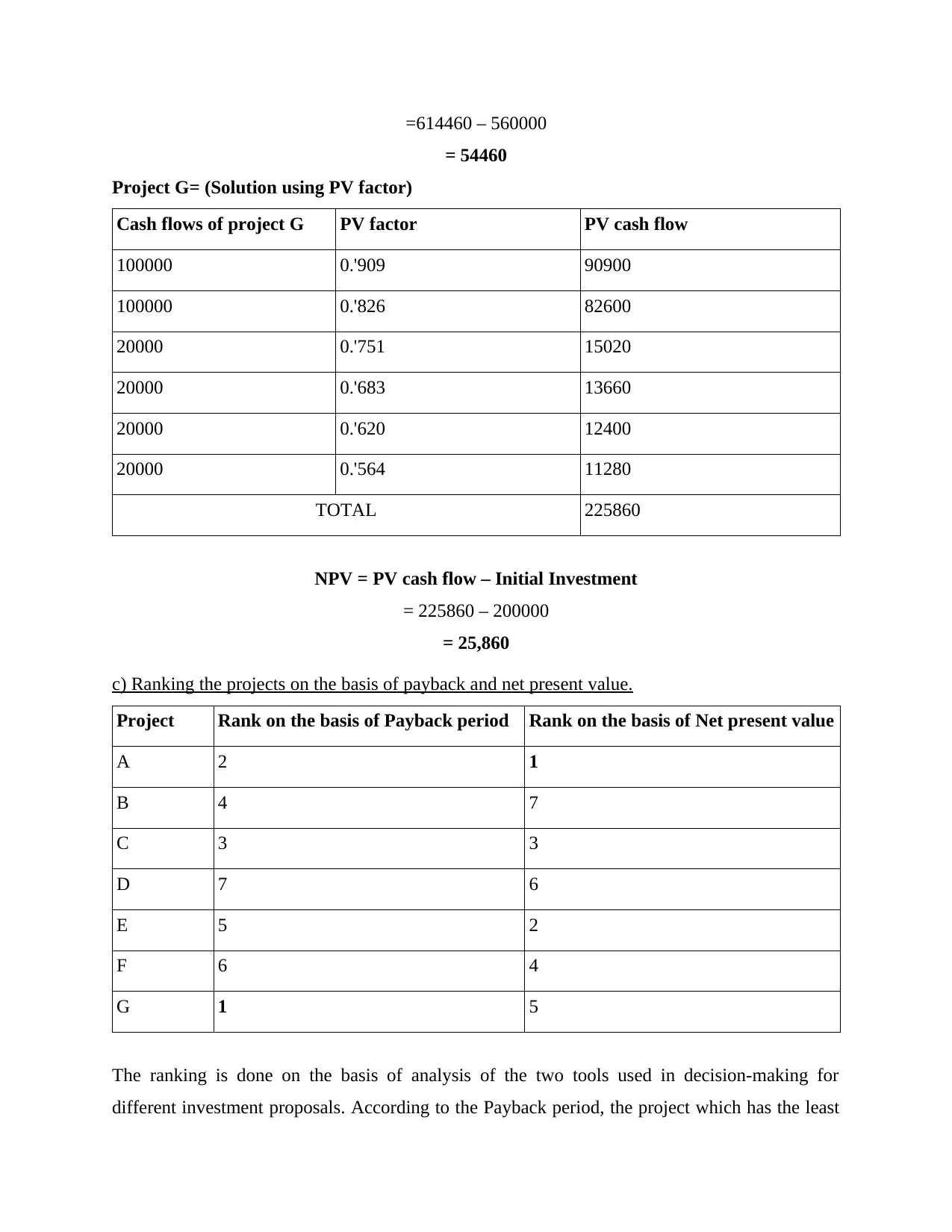

Project G= (Solution using PV factor)

Cash flows of project G PV factor PV cash flow

100000 0.'909 90900

100000 0.'826 82600

20000 0.'751 15020

20000 0.'683 13660

20000 0.'620 12400

20000 0.'564 11280

TOTAL 225860

NPV = PV cash flow – Initial Investment

= 225860 – 200000

= 25,860

c) Ranking the projects on the basis of payback and net present value.

Project Rank on the basis of Payback period Rank on the basis of Net present value

A 2 1

B 4 7

C 3 3

D 7 6

E 5 2

F 6 4

G 1 5

The ranking is done on the basis of analysis of the two tools used in decision-making for

different investment proposals. According to the Payback period, the project which has the least

= 54460

Project G= (Solution using PV factor)

Cash flows of project G PV factor PV cash flow

100000 0.'909 90900

100000 0.'826 82600

20000 0.'751 15020

20000 0.'683 13660

20000 0.'620 12400

20000 0.'564 11280

TOTAL 225860

NPV = PV cash flow – Initial Investment

= 225860 – 200000

= 25,860

c) Ranking the projects on the basis of payback and net present value.

Project Rank on the basis of Payback period Rank on the basis of Net present value

A 2 1

B 4 7

C 3 3

D 7 6

E 5 2

F 6 4

G 1 5

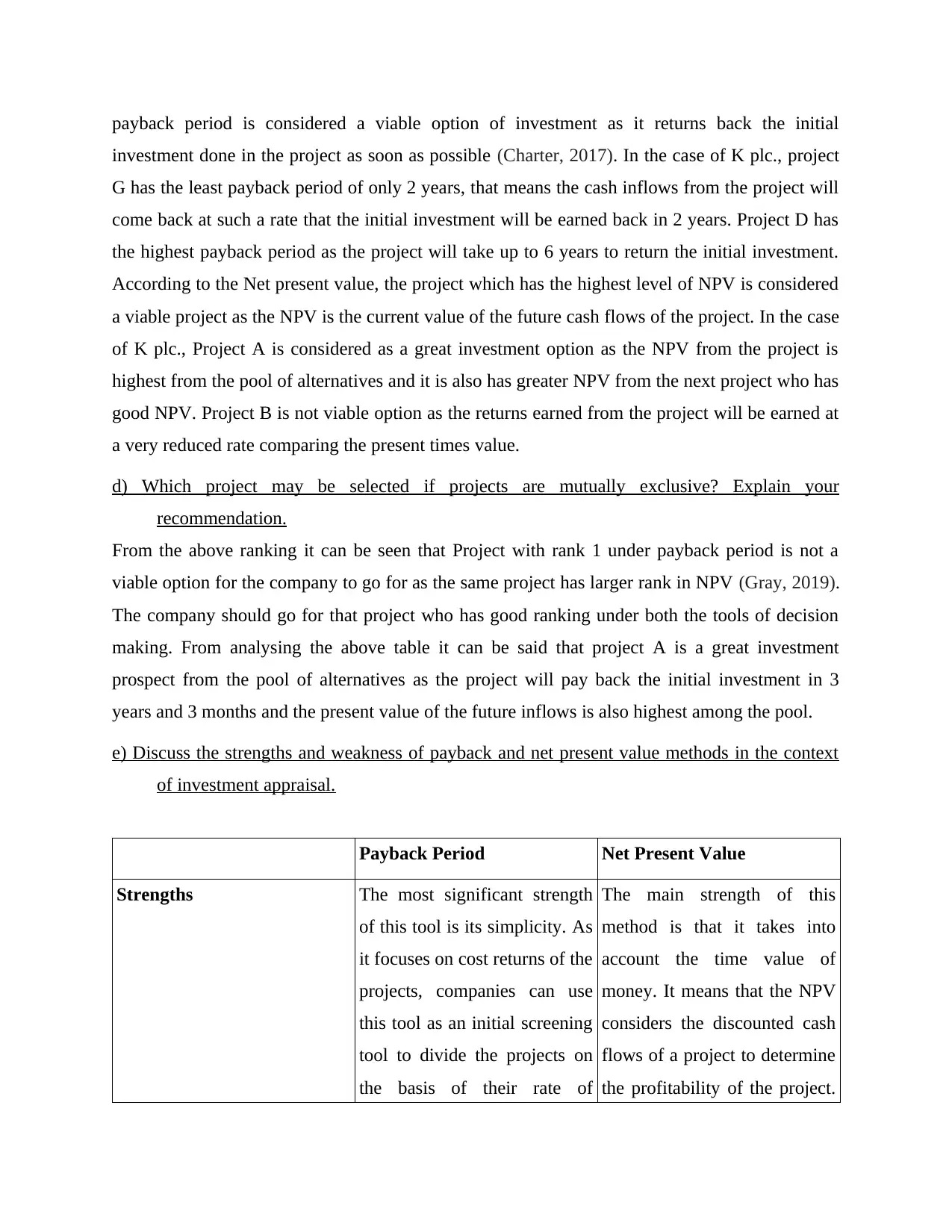

The ranking is done on the basis of analysis of the two tools used in decision-making for

different investment proposals. According to the Payback period, the project which has the least

payback period is considered a viable option of investment as it returns back the initial

investment done in the project as soon as possible (Charter, 2017). In the case of K plc., project

G has the least payback period of only 2 years, that means the cash inflows from the project will

come back at such a rate that the initial investment will be earned back in 2 years. Project D has

the highest payback period as the project will take up to 6 years to return the initial investment.

According to the Net present value, the project which has the highest level of NPV is considered

a viable project as the NPV is the current value of the future cash flows of the project. In the case

of K plc., Project A is considered as a great investment option as the NPV from the project is

highest from the pool of alternatives and it is also has greater NPV from the next project who has

good NPV. Project B is not viable option as the returns earned from the project will be earned at

a very reduced rate comparing the present times value.

d) Which project may be selected if projects are mutually exclusive? Explain your

recommendation.

From the above ranking it can be seen that Project with rank 1 under payback period is not a

viable option for the company to go for as the same project has larger rank in NPV (Gray, 2019).

The company should go for that project who has good ranking under both the tools of decision

making. From analysing the above table it can be said that project A is a great investment

prospect from the pool of alternatives as the project will pay back the initial investment in 3

years and 3 months and the present value of the future inflows is also highest among the pool.

e) Discuss the strengths and weakness of payback and net present value methods in the context

of investment appraisal.

Payback Period Net Present Value

Strengths The most significant strength

of this tool is its simplicity. As

it focuses on cost returns of the

projects, companies can use

this tool as an initial screening

tool to divide the projects on

the basis of their rate of

The main strength of this

method is that it takes into

account the time value of

money. It means that the NPV

considers the discounted cash

flows of a project to determine

the profitability of the project.

investment done in the project as soon as possible (Charter, 2017). In the case of K plc., project

G has the least payback period of only 2 years, that means the cash inflows from the project will

come back at such a rate that the initial investment will be earned back in 2 years. Project D has

the highest payback period as the project will take up to 6 years to return the initial investment.

According to the Net present value, the project which has the highest level of NPV is considered

a viable project as the NPV is the current value of the future cash flows of the project. In the case

of K plc., Project A is considered as a great investment option as the NPV from the project is

highest from the pool of alternatives and it is also has greater NPV from the next project who has

good NPV. Project B is not viable option as the returns earned from the project will be earned at

a very reduced rate comparing the present times value.

d) Which project may be selected if projects are mutually exclusive? Explain your

recommendation.

From the above ranking it can be seen that Project with rank 1 under payback period is not a

viable option for the company to go for as the same project has larger rank in NPV (Gray, 2019).

The company should go for that project who has good ranking under both the tools of decision

making. From analysing the above table it can be said that project A is a great investment

prospect from the pool of alternatives as the project will pay back the initial investment in 3

years and 3 months and the present value of the future inflows is also highest among the pool.

e) Discuss the strengths and weakness of payback and net present value methods in the context

of investment appraisal.

Payback Period Net Present Value

Strengths The most significant strength

of this tool is its simplicity. As

it focuses on cost returns of the

projects, companies can use

this tool as an initial screening

tool to divide the projects on

the basis of their rate of

The main strength of this

method is that it takes into

account the time value of

money. It means that the NPV

considers the discounted cash

flows of a project to determine

the profitability of the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

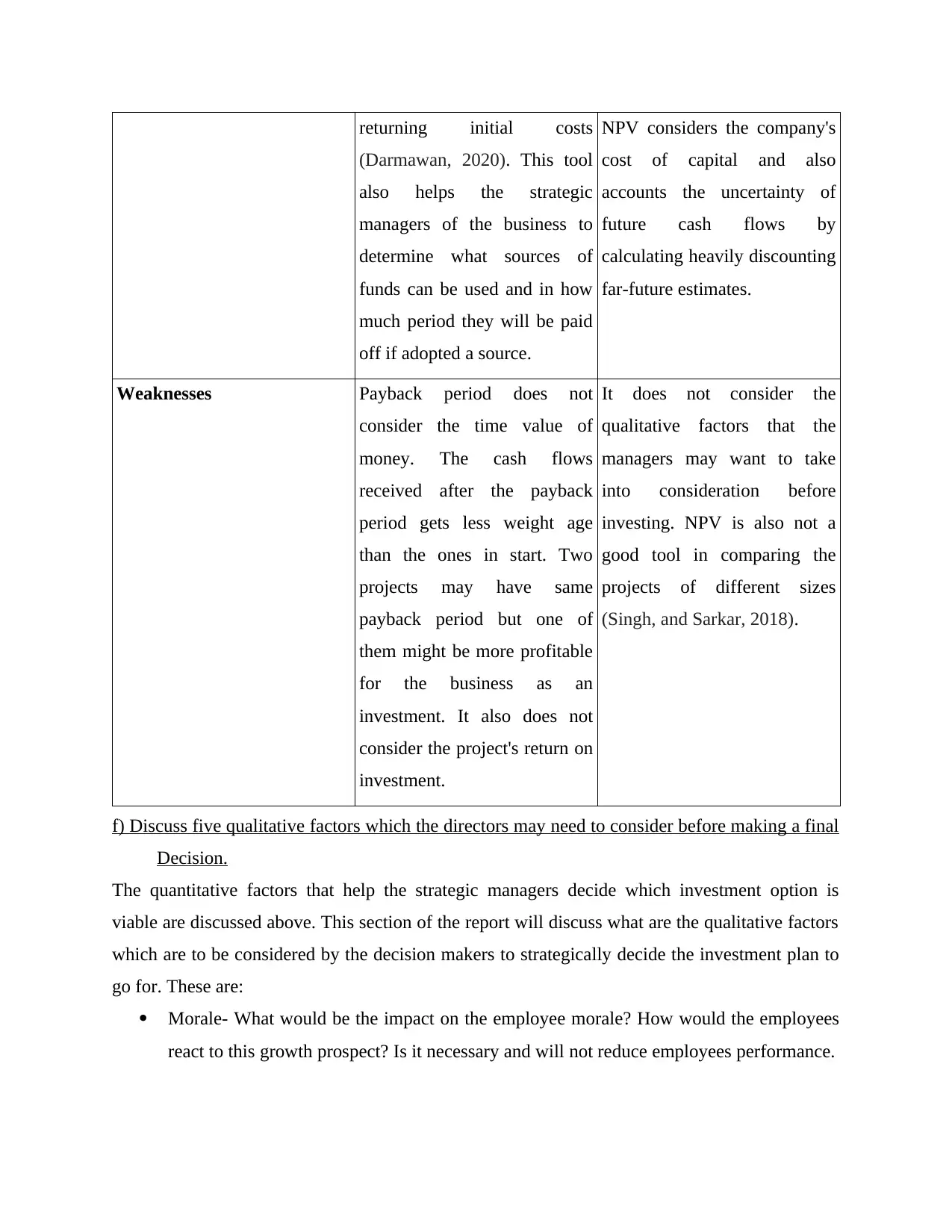

returning initial costs

(Darmawan, 2020). This tool

also helps the strategic

managers of the business to

determine what sources of

funds can be used and in how

much period they will be paid

off if adopted a source.

NPV considers the company's

cost of capital and also

accounts the uncertainty of

future cash flows by

calculating heavily discounting

far-future estimates.

Weaknesses Payback period does not

consider the time value of

money. The cash flows

received after the payback

period gets less weight age

than the ones in start. Two

projects may have same

payback period but one of

them might be more profitable

for the business as an

investment. It also does not

consider the project's return on

investment.

It does not consider the

qualitative factors that the

managers may want to take

into consideration before

investing. NPV is also not a

good tool in comparing the

projects of different sizes

(Singh, and Sarkar, 2018).

f) Discuss five qualitative factors which the directors may need to consider before making a final

Decision.

The quantitative factors that help the strategic managers decide which investment option is

viable are discussed above. This section of the report will discuss what are the qualitative factors

which are to be considered by the decision makers to strategically decide the investment plan to

go for. These are:

Morale- What would be the impact on the employee morale? How would the employees

react to this growth prospect? Is it necessary and will not reduce employees performance.

(Darmawan, 2020). This tool

also helps the strategic

managers of the business to

determine what sources of

funds can be used and in how

much period they will be paid

off if adopted a source.

NPV considers the company's

cost of capital and also

accounts the uncertainty of

future cash flows by

calculating heavily discounting

far-future estimates.

Weaknesses Payback period does not

consider the time value of

money. The cash flows

received after the payback

period gets less weight age

than the ones in start. Two

projects may have same

payback period but one of

them might be more profitable

for the business as an

investment. It also does not

consider the project's return on

investment.

It does not consider the

qualitative factors that the

managers may want to take

into consideration before

investing. NPV is also not a

good tool in comparing the

projects of different sizes

(Singh, and Sarkar, 2018).

f) Discuss five qualitative factors which the directors may need to consider before making a final

Decision.

The quantitative factors that help the strategic managers decide which investment option is

viable are discussed above. This section of the report will discuss what are the qualitative factors

which are to be considered by the decision makers to strategically decide the investment plan to

go for. These are:

Morale- What would be the impact on the employee morale? How would the employees

react to this growth prospect? Is it necessary and will not reduce employees performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Customers- who are the targeted customers of the planned project? How would this

project add to the economy (Freeman, Parmar, and Martin, 2020).

Investors- what does the investors think about the proposed project? What are the

monetary requirements of the proposed project.

Community- what part of the community is focused that would indulge in the proposed

project.

Products- what are the new products that the company is going to produce in this new

investment proposal. How are the demands of same in the market.

TASK B

a) Suggest 3 alternative methods of funding

Financing refers to the series of action taken up by the owners/ managers of the business to raise

funds for the business activities, pruchasing or for investment. K plc wants to acquire shares of

an unlisted company for the growth prospects which would help the business enjoy a new

geographical area (Warwick, Wyness, and Conway, 2017). The company want to understand

what are the other different ways available in the market that can be accessed by the business to

purchase all the shares of the unlisted company. This section will now discuss the other three

factors available in the market that can be accessed by the company.

Bank Loans- Bank Loans refers to the finance extensions that have been provided by the

banks to the businesses. These funds are are extended to the business on a collateral

security. The company who uses these funds are required to pay the interest on these

funds over a period of time. The principal amount is required to be paid back after the

period which has been already decided by the bank and the company. The features of this

are: It is a short term source of finance. The company is required to pay back within a

financial accounting period. The bank loan can be secured or either unsecured totally

depending on the clause of loan. The interest which is charged by the bank can be fixed

or variable. Some kind of mortgage is required to be provided by the business in order to

use the funds. K plc can go with this type of finance as the company requires to purchase

the shares of a company at a point of time and does not require any continued flow of

funds. The main advantage of using such finance is that these funds can be considered as

a short or medium term financing.

project add to the economy (Freeman, Parmar, and Martin, 2020).

Investors- what does the investors think about the proposed project? What are the

monetary requirements of the proposed project.

Community- what part of the community is focused that would indulge in the proposed

project.

Products- what are the new products that the company is going to produce in this new

investment proposal. How are the demands of same in the market.

TASK B

a) Suggest 3 alternative methods of funding

Financing refers to the series of action taken up by the owners/ managers of the business to raise

funds for the business activities, pruchasing or for investment. K plc wants to acquire shares of

an unlisted company for the growth prospects which would help the business enjoy a new

geographical area (Warwick, Wyness, and Conway, 2017). The company want to understand

what are the other different ways available in the market that can be accessed by the business to

purchase all the shares of the unlisted company. This section will now discuss the other three

factors available in the market that can be accessed by the company.

Bank Loans- Bank Loans refers to the finance extensions that have been provided by the

banks to the businesses. These funds are are extended to the business on a collateral

security. The company who uses these funds are required to pay the interest on these

funds over a period of time. The principal amount is required to be paid back after the

period which has been already decided by the bank and the company. The features of this

are: It is a short term source of finance. The company is required to pay back within a

financial accounting period. The bank loan can be secured or either unsecured totally

depending on the clause of loan. The interest which is charged by the bank can be fixed

or variable. Some kind of mortgage is required to be provided by the business in order to

use the funds. K plc can go with this type of finance as the company requires to purchase

the shares of a company at a point of time and does not require any continued flow of

funds. The main advantage of using such finance is that these funds can be considered as

a short or medium term financing.

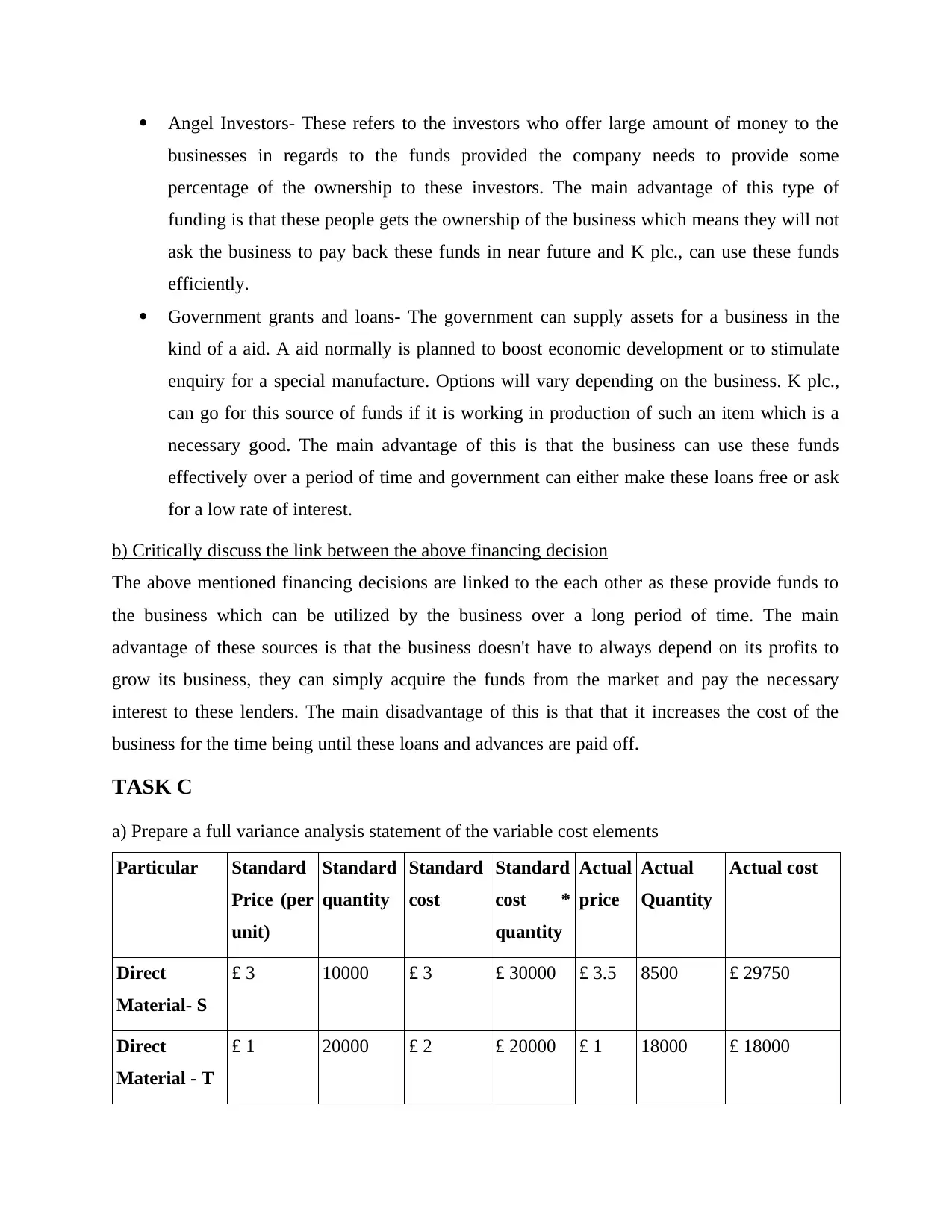

Angel Investors- These refers to the investors who offer large amount of money to the

businesses in regards to the funds provided the company needs to provide some

percentage of the ownership to these investors. The main advantage of this type of

funding is that these people gets the ownership of the business which means they will not

ask the business to pay back these funds in near future and K plc., can use these funds

efficiently.

Government grants and loans- The government can supply assets for a business in the

kind of a aid. A aid normally is planned to boost economic development or to stimulate

enquiry for a special manufacture. Options will vary depending on the business. K plc.,

can go for this source of funds if it is working in production of such an item which is a

necessary good. The main advantage of this is that the business can use these funds

effectively over a period of time and government can either make these loans free or ask

for a low rate of interest.

b) Critically discuss the link between the above financing decision

The above mentioned financing decisions are linked to the each other as these provide funds to

the business which can be utilized by the business over a long period of time. The main

advantage of these sources is that the business doesn't have to always depend on its profits to

grow its business, they can simply acquire the funds from the market and pay the necessary

interest to these lenders. The main disadvantage of this is that that it increases the cost of the

business for the time being until these loans and advances are paid off.

TASK C

a) Prepare a full variance analysis statement of the variable cost elements

Particular Standard

Price (per

unit)

Standard

quantity

Standard

cost

Standard

cost *

quantity

Actual

price

Actual

Quantity

Actual cost

Direct

Material- S

£ 3 10000 £ 3 £ 30000 £ 3.5 8500 £ 29750

Direct

Material - T

£ 1 20000 £ 2 £ 20000 £ 1 18000 £ 18000

businesses in regards to the funds provided the company needs to provide some

percentage of the ownership to these investors. The main advantage of this type of

funding is that these people gets the ownership of the business which means they will not

ask the business to pay back these funds in near future and K plc., can use these funds

efficiently.

Government grants and loans- The government can supply assets for a business in the

kind of a aid. A aid normally is planned to boost economic development or to stimulate

enquiry for a special manufacture. Options will vary depending on the business. K plc.,

can go for this source of funds if it is working in production of such an item which is a

necessary good. The main advantage of this is that the business can use these funds

effectively over a period of time and government can either make these loans free or ask

for a low rate of interest.

b) Critically discuss the link between the above financing decision

The above mentioned financing decisions are linked to the each other as these provide funds to

the business which can be utilized by the business over a long period of time. The main

advantage of these sources is that the business doesn't have to always depend on its profits to

grow its business, they can simply acquire the funds from the market and pay the necessary

interest to these lenders. The main disadvantage of this is that that it increases the cost of the

business for the time being until these loans and advances are paid off.

TASK C

a) Prepare a full variance analysis statement of the variable cost elements

Particular Standard

Price (per

unit)

Standard

quantity

Standard

cost

Standard

cost *

quantity

Actual

price

Actual

Quantity

Actual cost

Direct

Material- S

£ 3 10000 £ 3 £ 30000 £ 3.5 8500 £ 29750

Direct

Material - T

£ 1 20000 £ 2 £ 20000 £ 1 18000 £ 18000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

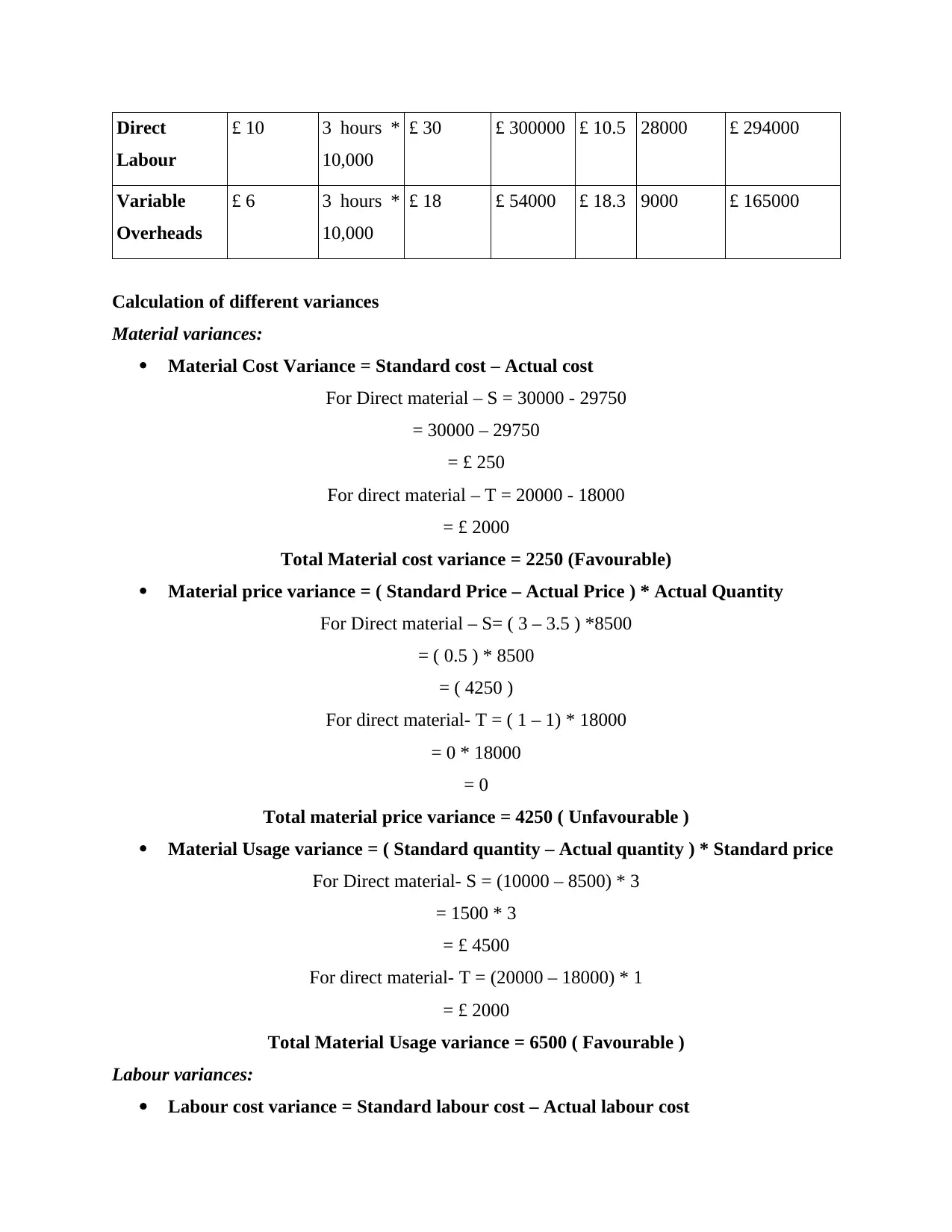

Direct

Labour

£ 10 3 hours *

10,000

£ 30 £ 300000 £ 10.5 28000 £ 294000

Variable

Overheads

£ 6 3 hours *

10,000

£ 18 £ 54000 £ 18.3 9000 £ 165000

Calculation of different variances

Material variances:

Material Cost Variance = Standard cost – Actual cost

For Direct material – S = 30000 - 29750

= 30000 – 29750

= £ 250

For direct material – T = 20000 - 18000

= £ 2000

Total Material cost variance = 2250 (Favourable)

Material price variance = ( Standard Price – Actual Price ) * Actual Quantity

For Direct material – S= ( 3 – 3.5 ) *8500

= ( 0.5 ) * 8500

= ( 4250 )

For direct material- T = ( 1 – 1) * 18000

= 0 * 18000

= 0

Total material price variance = 4250 ( Unfavourable )

Material Usage variance = ( Standard quantity – Actual quantity ) * Standard price

For Direct material- S = (10000 – 8500) * 3

= 1500 * 3

= £ 4500

For direct material- T = (20000 – 18000) * 1

= £ 2000

Total Material Usage variance = 6500 ( Favourable )

Labour variances:

Labour cost variance = Standard labour cost – Actual labour cost

Labour

£ 10 3 hours *

10,000

£ 30 £ 300000 £ 10.5 28000 £ 294000

Variable

Overheads

£ 6 3 hours *

10,000

£ 18 £ 54000 £ 18.3 9000 £ 165000

Calculation of different variances

Material variances:

Material Cost Variance = Standard cost – Actual cost

For Direct material – S = 30000 - 29750

= 30000 – 29750

= £ 250

For direct material – T = 20000 - 18000

= £ 2000

Total Material cost variance = 2250 (Favourable)

Material price variance = ( Standard Price – Actual Price ) * Actual Quantity

For Direct material – S= ( 3 – 3.5 ) *8500

= ( 0.5 ) * 8500

= ( 4250 )

For direct material- T = ( 1 – 1) * 18000

= 0 * 18000

= 0

Total material price variance = 4250 ( Unfavourable )

Material Usage variance = ( Standard quantity – Actual quantity ) * Standard price

For Direct material- S = (10000 – 8500) * 3

= 1500 * 3

= £ 4500

For direct material- T = (20000 – 18000) * 1

= £ 2000

Total Material Usage variance = 6500 ( Favourable )

Labour variances:

Labour cost variance = Standard labour cost – Actual labour cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=10 – 10.5

= 0.5

Labour rate variance = ( Standard rate – Actual rate ) * Actual hour

= ( 300000 – 294000 ) * 28000

= 6000 * 28000

=168000000

Labour efficiency variance = ( Standard hours – Actual Hours ) * standard rate

= ( 30000 – 28000 ) * 10

= 2000 * 10

= 20,000

Variable overhead variance = Standard variable overhead – Actual variable overhead

= 180000 – 165000

= 15000

b) From the available information suggest possible explanations for the variances identified.

Cost variances refers to the process of determining the financial performance of a production

project. The management calculates the variances in the basis of actual and budgeted costs of the

projects (Mukonza, and Swarts, 2020). The variances help the business decide how the business

is doing in the specified project. Cost variance is the difference between the actual and the

projected costs. It is critical for the management to ascertain the variance as it reveals the

important information regarding a project or a period. It shows how the company is lacking and

it gives them insight about how much the costs are variant from the projected ones. With this

information in hand the company can take necessary steps to reduce the costs and increase the

profits of the business. The above calculations are now being discussed.

Material variance is the difference between the actual cost incurred of direct materials and the

ones which were projected for the project. This variance determines the ability of the production

unit to incur the costs close to the levels which were planned for the project. The material cost

variance and material usage variance for the first quarter of K plc is favourable but material price

variance is unfavourable for the company. Labour variance determines the efficiency that the

labour is having in the production unit. It compares the cost of labour planned and what have

been incurred actually. The labour price variance of the company is favourable. Variable

= 0.5

Labour rate variance = ( Standard rate – Actual rate ) * Actual hour

= ( 300000 – 294000 ) * 28000

= 6000 * 28000

=168000000

Labour efficiency variance = ( Standard hours – Actual Hours ) * standard rate

= ( 30000 – 28000 ) * 10

= 2000 * 10

= 20,000

Variable overhead variance = Standard variable overhead – Actual variable overhead

= 180000 – 165000

= 15000

b) From the available information suggest possible explanations for the variances identified.

Cost variances refers to the process of determining the financial performance of a production

project. The management calculates the variances in the basis of actual and budgeted costs of the

projects (Mukonza, and Swarts, 2020). The variances help the business decide how the business

is doing in the specified project. Cost variance is the difference between the actual and the

projected costs. It is critical for the management to ascertain the variance as it reveals the

important information regarding a project or a period. It shows how the company is lacking and

it gives them insight about how much the costs are variant from the projected ones. With this

information in hand the company can take necessary steps to reduce the costs and increase the

profits of the business. The above calculations are now being discussed.

Material variance is the difference between the actual cost incurred of direct materials and the

ones which were projected for the project. This variance determines the ability of the production

unit to incur the costs close to the levels which were planned for the project. The material cost

variance and material usage variance for the first quarter of K plc is favourable but material price

variance is unfavourable for the company. Labour variance determines the efficiency that the

labour is having in the production unit. It compares the cost of labour planned and what have

been incurred actually. The labour price variance of the company is favourable. Variable

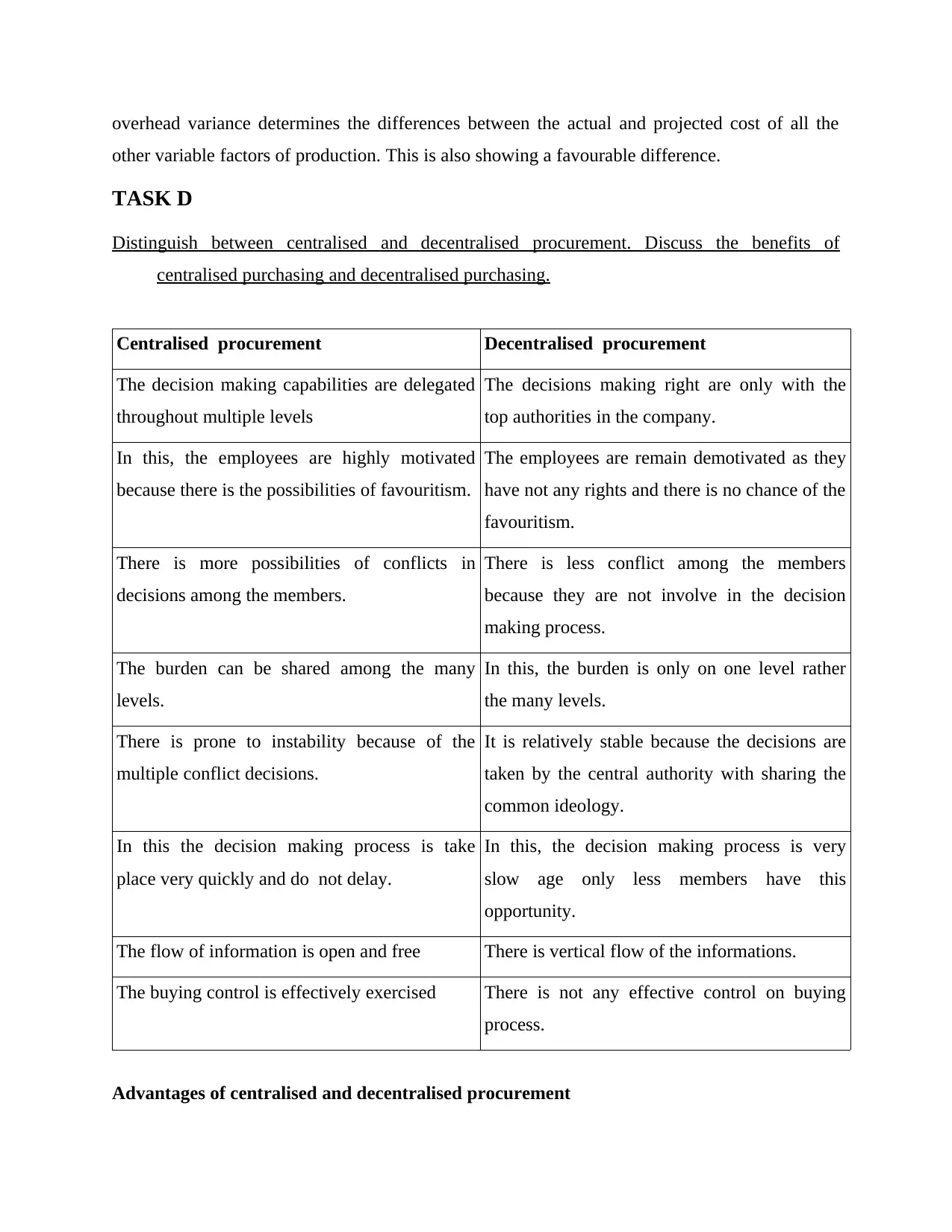

overhead variance determines the differences between the actual and projected cost of all the

other variable factors of production. This is also showing a favourable difference.

TASK D

Distinguish between centralised and decentralised procurement. Discuss the benefits of

centralised purchasing and decentralised purchasing.

Centralised procurement Decentralised procurement

The decision making capabilities are delegated

throughout multiple levels

The decisions making right are only with the

top authorities in the company.

In this, the employees are highly motivated

because there is the possibilities of favouritism.

The employees are remain demotivated as they

have not any rights and there is no chance of the

favouritism.

There is more possibilities of conflicts in

decisions among the members.

There is less conflict among the members

because they are not involve in the decision

making process.

The burden can be shared among the many

levels.

In this, the burden is only on one level rather

the many levels.

There is prone to instability because of the

multiple conflict decisions.

It is relatively stable because the decisions are

taken by the central authority with sharing the

common ideology.

In this the decision making process is take

place very quickly and do not delay.

In this, the decision making process is very

slow age only less members have this

opportunity.

The flow of information is open and free There is vertical flow of the informations.

The buying control is effectively exercised There is not any effective control on buying

process.

Advantages of centralised and decentralised procurement

other variable factors of production. This is also showing a favourable difference.

TASK D

Distinguish between centralised and decentralised procurement. Discuss the benefits of

centralised purchasing and decentralised purchasing.

Centralised procurement Decentralised procurement

The decision making capabilities are delegated

throughout multiple levels

The decisions making right are only with the

top authorities in the company.

In this, the employees are highly motivated

because there is the possibilities of favouritism.

The employees are remain demotivated as they

have not any rights and there is no chance of the

favouritism.

There is more possibilities of conflicts in

decisions among the members.

There is less conflict among the members

because they are not involve in the decision

making process.

The burden can be shared among the many

levels.

In this, the burden is only on one level rather

the many levels.

There is prone to instability because of the

multiple conflict decisions.

It is relatively stable because the decisions are

taken by the central authority with sharing the

common ideology.

In this the decision making process is take

place very quickly and do not delay.

In this, the decision making process is very

slow age only less members have this

opportunity.

The flow of information is open and free There is vertical flow of the informations.

The buying control is effectively exercised There is not any effective control on buying

process.

Advantages of centralised and decentralised procurement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.