Distinguishing Employment from Self Employment in Business Taxation

VerifiedAdded on 2022/12/29

|8

|1572

|23

AI Summary

This report discusses the criteria to distinguish between employment and self employment in business taxation. It also explores the six badges of trade and the VAT schemes available to VAT registered businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUSINESS TAXATION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

The criteria which can be used to distinguish employment from self employment....................3

Question 2........................................................................................................................................4

The six badges of trade................................................................................................................4

VAT scheme available to the VAT registered business..............................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

The criteria which can be used to distinguish employment from self employment....................3

Question 2........................................................................................................................................4

The six badges of trade................................................................................................................4

VAT scheme available to the VAT registered business..............................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................1

INTRODUCTION

Taxation is a means by which government levies tax on its citizens and different business

entities. It is divided into direct tax and indirect tax. In this report, we will discuss about the

criteria through which we can distinguish between employment and self employment. In this

report, we will also understand the six badges of trade along with different VAT scheme which is

available to the VAT registered business.

MAIN BODY

Question 1

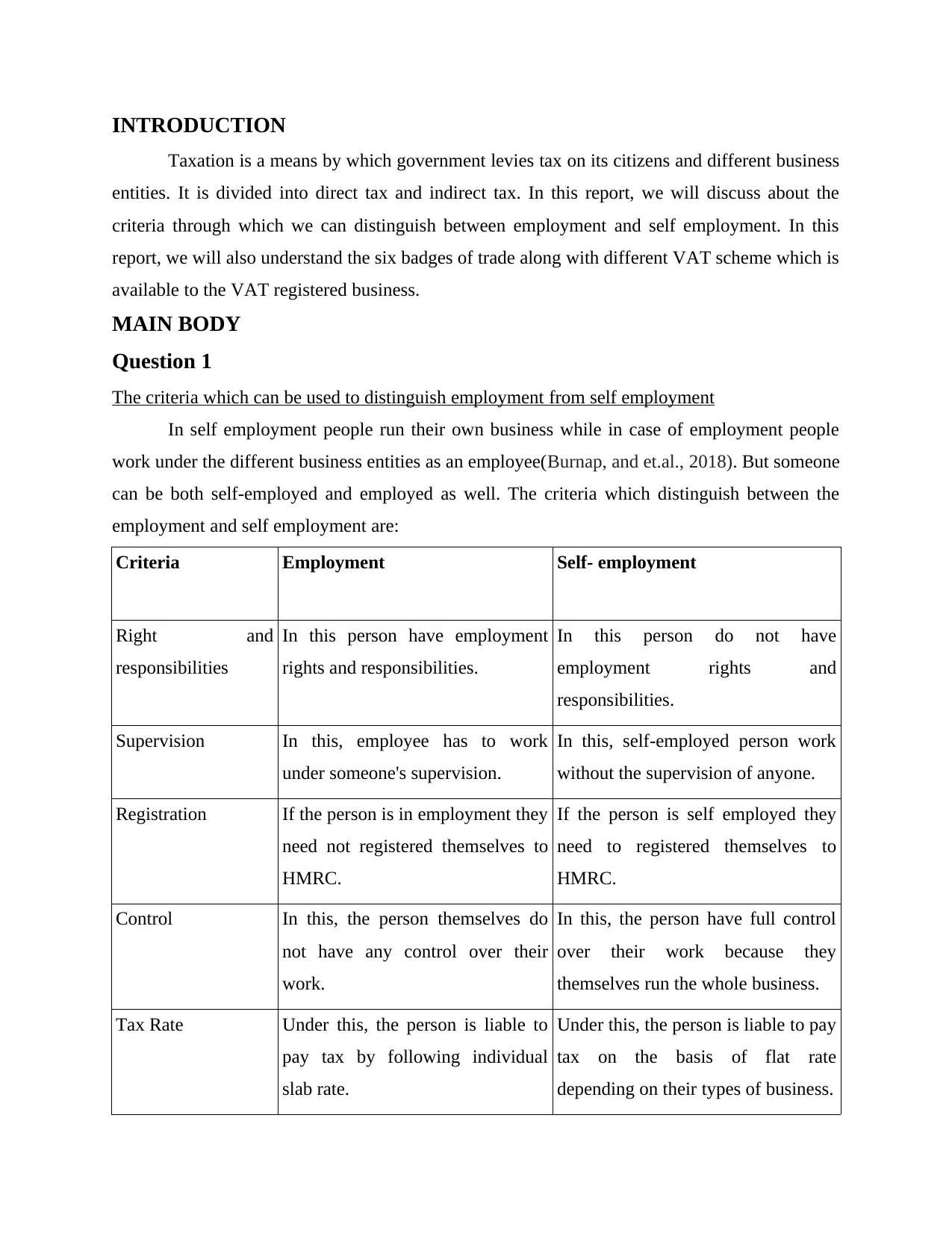

The criteria which can be used to distinguish employment from self employment

In self employment people run their own business while in case of employment people

work under the different business entities as an employee(Burnap, and et.al., 2018). But someone

can be both self-employed and employed as well. The criteria which distinguish between the

employment and self employment are:

Criteria Employment Self- employment

Right and

responsibilities

In this person have employment

rights and responsibilities.

In this person do not have

employment rights and

responsibilities.

Supervision In this, employee has to work

under someone's supervision.

In this, self-employed person work

without the supervision of anyone.

Registration If the person is in employment they

need not registered themselves to

HMRC.

If the person is self employed they

need to registered themselves to

HMRC.

Control In this, the person themselves do

not have any control over their

work.

In this, the person have full control

over their work because they

themselves run the whole business.

Tax Rate Under this, the person is liable to

pay tax by following individual

slab rate.

Under this, the person is liable to pay

tax on the basis of flat rate

depending on their types of business.

Taxation is a means by which government levies tax on its citizens and different business

entities. It is divided into direct tax and indirect tax. In this report, we will discuss about the

criteria through which we can distinguish between employment and self employment. In this

report, we will also understand the six badges of trade along with different VAT scheme which is

available to the VAT registered business.

MAIN BODY

Question 1

The criteria which can be used to distinguish employment from self employment

In self employment people run their own business while in case of employment people

work under the different business entities as an employee(Burnap, and et.al., 2018). But someone

can be both self-employed and employed as well. The criteria which distinguish between the

employment and self employment are:

Criteria Employment Self- employment

Right and

responsibilities

In this person have employment

rights and responsibilities.

In this person do not have

employment rights and

responsibilities.

Supervision In this, employee has to work

under someone's supervision.

In this, self-employed person work

without the supervision of anyone.

Registration If the person is in employment they

need not registered themselves to

HMRC.

If the person is self employed they

need to registered themselves to

HMRC.

Control In this, the person themselves do

not have any control over their

work.

In this, the person have full control

over their work because they

themselves run the whole business.

Tax Rate Under this, the person is liable to

pay tax by following individual

slab rate.

Under this, the person is liable to pay

tax on the basis of flat rate

depending on their types of business.

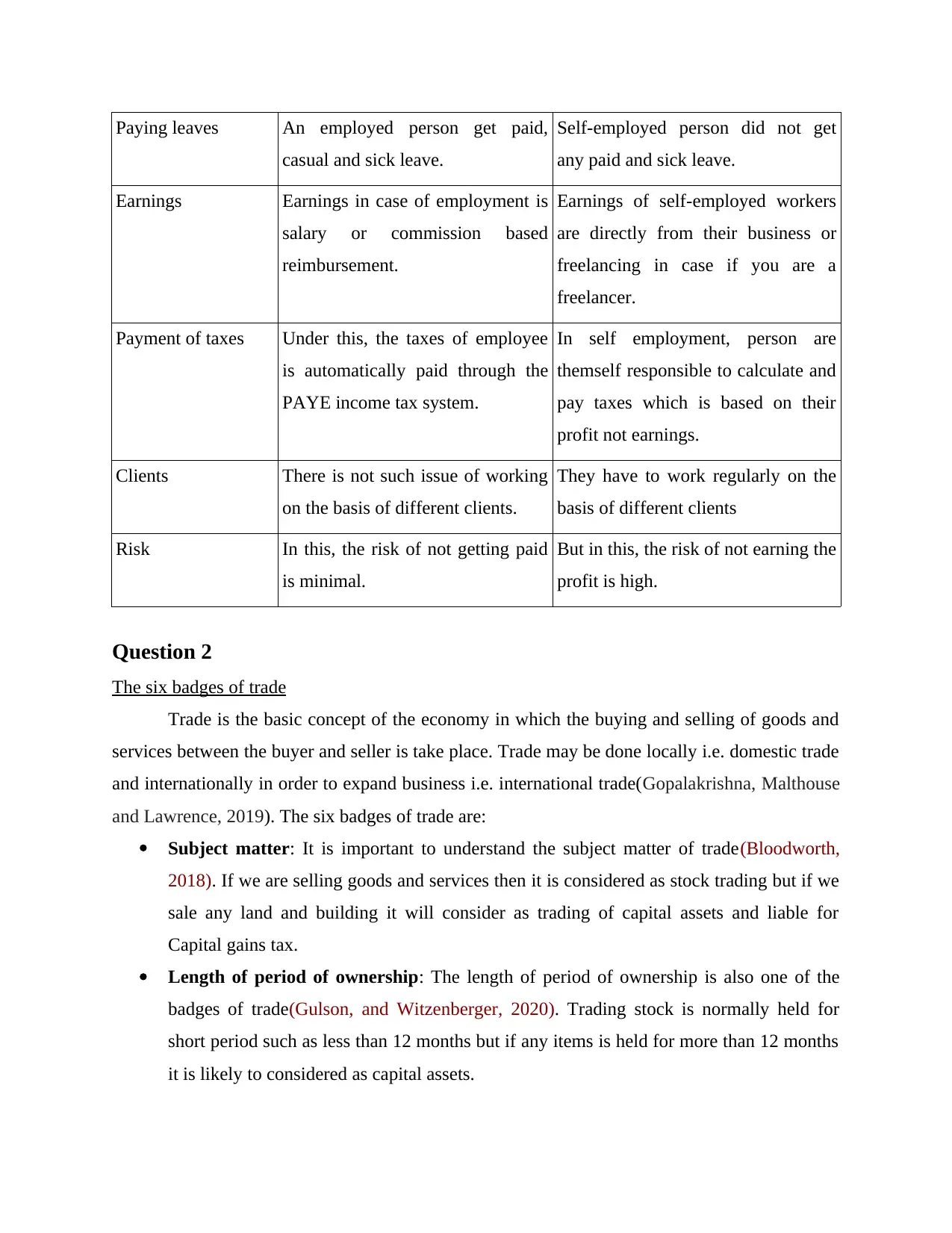

Paying leaves An employed person get paid,

casual and sick leave.

Self-employed person did not get

any paid and sick leave.

Earnings Earnings in case of employment is

salary or commission based

reimbursement.

Earnings of self-employed workers

are directly from their business or

freelancing in case if you are a

freelancer.

Payment of taxes Under this, the taxes of employee

is automatically paid through the

PAYE income tax system.

In self employment, person are

themself responsible to calculate and

pay taxes which is based on their

profit not earnings.

Clients There is not such issue of working

on the basis of different clients.

They have to work regularly on the

basis of different clients

Risk In this, the risk of not getting paid

is minimal.

But in this, the risk of not earning the

profit is high.

Question 2

The six badges of trade

Trade is the basic concept of the economy in which the buying and selling of goods and

services between the buyer and seller is take place. Trade may be done locally i.e. domestic trade

and internationally in order to expand business i.e. international trade(Gopalakrishna, Malthouse

and Lawrence, 2019). The six badges of trade are:

Subject matter: It is important to understand the subject matter of trade(Bloodworth,

2018). If we are selling goods and services then it is considered as stock trading but if we

sale any land and building it will consider as trading of capital assets and liable for

Capital gains tax.

Length of period of ownership: The length of period of ownership is also one of the

badges of trade(Gulson, and Witzenberger, 2020). Trading stock is normally held for

short period such as less than 12 months but if any items is held for more than 12 months

it is likely to considered as capital assets.

casual and sick leave.

Self-employed person did not get

any paid and sick leave.

Earnings Earnings in case of employment is

salary or commission based

reimbursement.

Earnings of self-employed workers

are directly from their business or

freelancing in case if you are a

freelancer.

Payment of taxes Under this, the taxes of employee

is automatically paid through the

PAYE income tax system.

In self employment, person are

themself responsible to calculate and

pay taxes which is based on their

profit not earnings.

Clients There is not such issue of working

on the basis of different clients.

They have to work regularly on the

basis of different clients

Risk In this, the risk of not getting paid

is minimal.

But in this, the risk of not earning the

profit is high.

Question 2

The six badges of trade

Trade is the basic concept of the economy in which the buying and selling of goods and

services between the buyer and seller is take place. Trade may be done locally i.e. domestic trade

and internationally in order to expand business i.e. international trade(Gopalakrishna, Malthouse

and Lawrence, 2019). The six badges of trade are:

Subject matter: It is important to understand the subject matter of trade(Bloodworth,

2018). If we are selling goods and services then it is considered as stock trading but if we

sale any land and building it will consider as trading of capital assets and liable for

Capital gains tax.

Length of period of ownership: The length of period of ownership is also one of the

badges of trade(Gulson, and Witzenberger, 2020). Trading stock is normally held for

short period such as less than 12 months but if any items is held for more than 12 months

it is likely to considered as capital assets.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

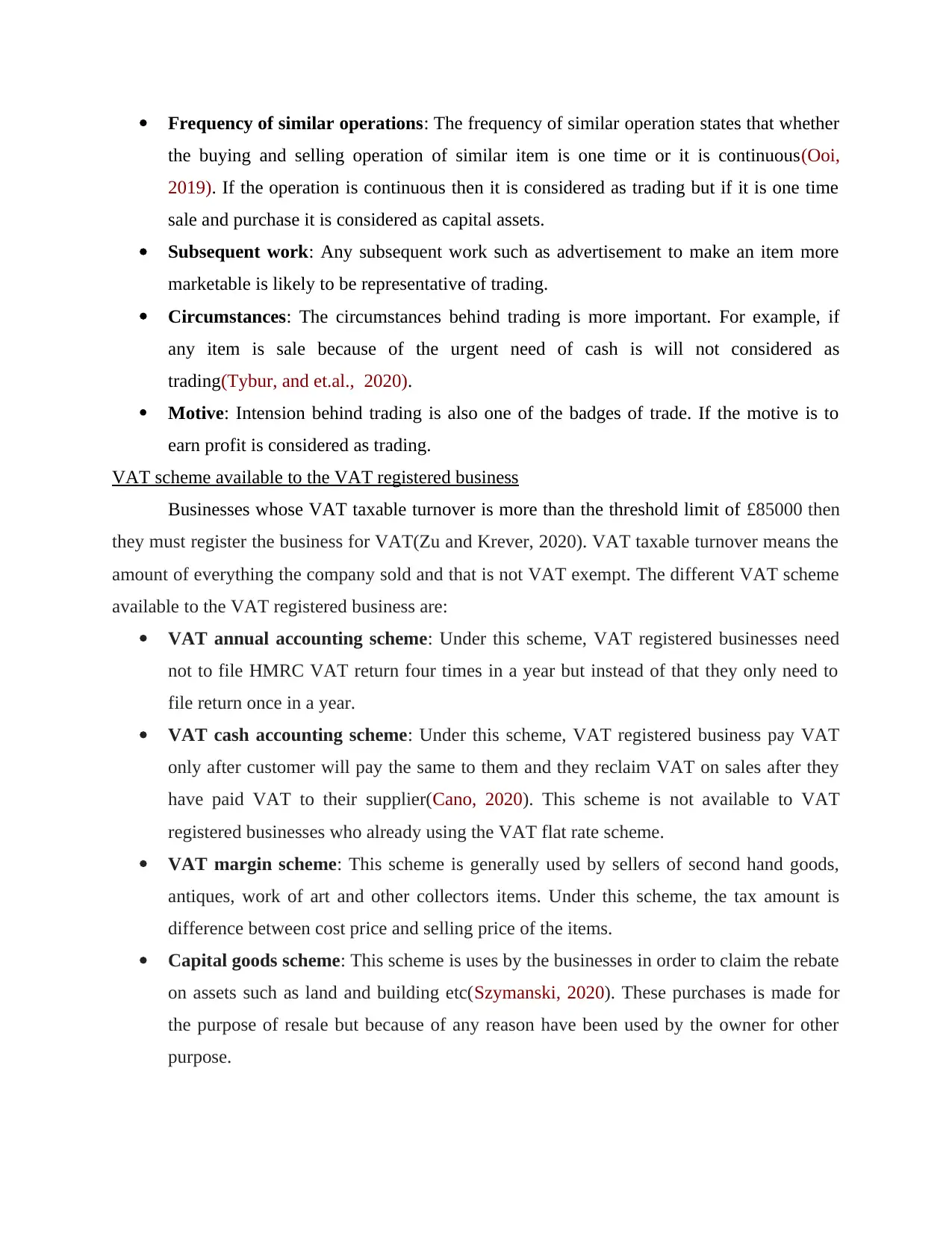

Frequency of similar operations: The frequency of similar operation states that whether

the buying and selling operation of similar item is one time or it is continuous(Ooi,

2019). If the operation is continuous then it is considered as trading but if it is one time

sale and purchase it is considered as capital assets.

Subsequent work: Any subsequent work such as advertisement to make an item more

marketable is likely to be representative of trading.

Circumstances: The circumstances behind trading is more important. For example, if

any item is sale because of the urgent need of cash is will not considered as

trading(Tybur, and et.al., 2020).

Motive: Intension behind trading is also one of the badges of trade. If the motive is to

earn profit is considered as trading.

VAT scheme available to the VAT registered business

Businesses whose VAT taxable turnover is more than the threshold limit of £85000 then

they must register the business for VAT(Zu and Krever, 2020). VAT taxable turnover means the

amount of everything the company sold and that is not VAT exempt. The different VAT scheme

available to the VAT registered business are:

VAT annual accounting scheme: Under this scheme, VAT registered businesses need

not to file HMRC VAT return four times in a year but instead of that they only need to

file return once in a year.

VAT cash accounting scheme: Under this scheme, VAT registered business pay VAT

only after customer will pay the same to them and they reclaim VAT on sales after they

have paid VAT to their supplier(Cano, 2020). This scheme is not available to VAT

registered businesses who already using the VAT flat rate scheme.

VAT margin scheme: This scheme is generally used by sellers of second hand goods,

antiques, work of art and other collectors items. Under this scheme, the tax amount is

difference between cost price and selling price of the items.

Capital goods scheme: This scheme is uses by the businesses in order to claim the rebate

on assets such as land and building etc(Szymanski, 2020). These purchases is made for

the purpose of resale but because of any reason have been used by the owner for other

purpose.

the buying and selling operation of similar item is one time or it is continuous(Ooi,

2019). If the operation is continuous then it is considered as trading but if it is one time

sale and purchase it is considered as capital assets.

Subsequent work: Any subsequent work such as advertisement to make an item more

marketable is likely to be representative of trading.

Circumstances: The circumstances behind trading is more important. For example, if

any item is sale because of the urgent need of cash is will not considered as

trading(Tybur, and et.al., 2020).

Motive: Intension behind trading is also one of the badges of trade. If the motive is to

earn profit is considered as trading.

VAT scheme available to the VAT registered business

Businesses whose VAT taxable turnover is more than the threshold limit of £85000 then

they must register the business for VAT(Zu and Krever, 2020). VAT taxable turnover means the

amount of everything the company sold and that is not VAT exempt. The different VAT scheme

available to the VAT registered business are:

VAT annual accounting scheme: Under this scheme, VAT registered businesses need

not to file HMRC VAT return four times in a year but instead of that they only need to

file return once in a year.

VAT cash accounting scheme: Under this scheme, VAT registered business pay VAT

only after customer will pay the same to them and they reclaim VAT on sales after they

have paid VAT to their supplier(Cano, 2020). This scheme is not available to VAT

registered businesses who already using the VAT flat rate scheme.

VAT margin scheme: This scheme is generally used by sellers of second hand goods,

antiques, work of art and other collectors items. Under this scheme, the tax amount is

difference between cost price and selling price of the items.

Capital goods scheme: This scheme is uses by the businesses in order to claim the rebate

on assets such as land and building etc(Szymanski, 2020). These purchases is made for

the purpose of resale but because of any reason have been used by the owner for other

purpose.

VAT retail scheme: This scheme is only used by the businesses that make retail sales

and have the annual VAT turnover is less than £130 million. The businesses who make

both retail and non retail sales also avail these scheme but for their non retail business

they must account it in the regular way.

CONCLUSION

In this report, we conclude the different criteria which can be used to distinguish between

employment and self employment. This report also state the six badges of trade and how this

badges help us to differentiate between trading stock and capital assets. In this report we also

conclude the different VAT scheme which VAT registered businesses can avail.

and have the annual VAT turnover is less than £130 million. The businesses who make

both retail and non retail sales also avail these scheme but for their non retail business

they must account it in the regular way.

CONCLUSION

In this report, we conclude the different criteria which can be used to distinguish between

employment and self employment. This report also state the six badges of trade and how this

badges help us to differentiate between trading stock and capital assets. In this report we also

conclude the different VAT scheme which VAT registered businesses can avail.

REFERENCES

Books and journals

Burnap, P. and et.al., 2018. Malware classification using self organising feature maps and

machine activity data. computers & security. 73. pp.399-410.

Bakhshi, H. and et.al., 2017. The future of skills: Employment in 2030. Pearson.

Bloodworth, J., 2018. Hired: Six months undercover in low-wage Britain. Atlantic books.

Gopalakrishna, S., Malthouse, E. C. and Lawrence, J. M., 2019. Managing customer

engagement at trade shows. Industrial Marketing Management. 81. pp.99-114.

Zu, Y. and Krever, R., 2020. The United Kingdom has spoken: The receding impact of

European jurisprudence on the UK interpretation of the common VAT

system. Common Law World Review. 49(1). pp.75-91.

Ooi, V., 2019. Taxing ‘all other income’in Singapore and Malaysia. Oxford University

Commonwealth Law Journal. 19(2). pp.204-226.

Tybur, J. M. and et.al., 2020. <? covid19?> Behavioral Immune Trade-Offs: Interpersonal

Value Relaxes Social Pathogen Avoidance. Psychological science. 31(10). pp.1211-

1221.

Gulson, K. N. and Witzenberger, K., 2020. Repackaging authority: artificial intelligence,

automated governance and education trade shows. Journal of Education Policy. pp.1-

16.

Cano, M. C., 2020. UK retailers anxious over withdrawal of VAT retail export

scheme. International Tax Review.

Szymanski, S., 2020. On the Incidence of an Ad Valorem Tax: The Adoption of VAT in the UK

and Cost Pass Through by English Football Clubs. De Economist. pp.1-25.

Online

Business Taxation Meaning: Everything You Need to Know. 2021 [Online]. Available

through:<https://www.upcounsel.com/business-taxation-meaning>

1

Books and journals

Burnap, P. and et.al., 2018. Malware classification using self organising feature maps and

machine activity data. computers & security. 73. pp.399-410.

Bakhshi, H. and et.al., 2017. The future of skills: Employment in 2030. Pearson.

Bloodworth, J., 2018. Hired: Six months undercover in low-wage Britain. Atlantic books.

Gopalakrishna, S., Malthouse, E. C. and Lawrence, J. M., 2019. Managing customer

engagement at trade shows. Industrial Marketing Management. 81. pp.99-114.

Zu, Y. and Krever, R., 2020. The United Kingdom has spoken: The receding impact of

European jurisprudence on the UK interpretation of the common VAT

system. Common Law World Review. 49(1). pp.75-91.

Ooi, V., 2019. Taxing ‘all other income’in Singapore and Malaysia. Oxford University

Commonwealth Law Journal. 19(2). pp.204-226.

Tybur, J. M. and et.al., 2020. <? covid19?> Behavioral Immune Trade-Offs: Interpersonal

Value Relaxes Social Pathogen Avoidance. Psychological science. 31(10). pp.1211-

1221.

Gulson, K. N. and Witzenberger, K., 2020. Repackaging authority: artificial intelligence,

automated governance and education trade shows. Journal of Education Policy. pp.1-

16.

Cano, M. C., 2020. UK retailers anxious over withdrawal of VAT retail export

scheme. International Tax Review.

Szymanski, S., 2020. On the Incidence of an Ad Valorem Tax: The Adoption of VAT in the UK

and Cost Pass Through by English Football Clubs. De Economist. pp.1-25.

Online

Business Taxation Meaning: Everything You Need to Know. 2021 [Online]. Available

through:<https://www.upcounsel.com/business-taxation-meaning>

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.