Business Taxation: Trading Profits, Employment vs Self Employment, VAT Schemes

VerifiedAdded on 2022/12/28

|13

|3442

|88

AI Summary

This document provides an overview of business taxation, covering topics such as trading profits, employment vs self employment, and different VAT schemes for VAT registered companies. It discusses the criteria to distinguish employment from self employment and explores why people prefer self employment. The document also delves into the six badges of trade and their significance. Additionally, it provides insights into different VAT schemes for small businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUSINESS TAXATION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Linda's trading profits for the year 31st march 2021..............................................................3

QUESTION 2...................................................................................................................................4

Criteria which can be used to distinguish employment from self employment. Why people

prefer self employment?.........................................................................................................4

Why prefer self employment rather than being employed, resulting in so many IR 35 cases5

QUESTION 3...................................................................................................................................5

Discussion of Six badges for trade.........................................................................................5

Different VAT schemes for various VAT registered companies...........................................7

QUESTION 4...................................................................................................................................8

Inheritance tax arising when the death...................................................................................8

Capital gain tax liability.........................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Linda's trading profits for the year 31st march 2021..............................................................3

QUESTION 2...................................................................................................................................4

Criteria which can be used to distinguish employment from self employment. Why people

prefer self employment?.........................................................................................................4

Why prefer self employment rather than being employed, resulting in so many IR 35 cases5

QUESTION 3...................................................................................................................................5

Discussion of Six badges for trade.........................................................................................5

Different VAT schemes for various VAT registered companies...........................................7

QUESTION 4...................................................................................................................................8

Inheritance tax arising when the death...................................................................................8

Capital gain tax liability.........................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Business taxation is defined as the taxes that businesses as a basic component of their

business operations must pay. Whether there is a sole businessman, mate, component of limited

liability firm or a corporation etc. every type of enterprise will have to follow tax regulations.

Each type of entity will face different type of tax consequences(Blakeley, 2018). The study

assessment describes the various aspects of business taxation. The report focuses on facets such

as practical sum on trading profits assessments, key 6 badges of trade, multiple VAT schemes in

context of registered VAT businesses etc. It also covers capital gain tax needs as well as practical

addition of inheritance tax.

QUESTION 1

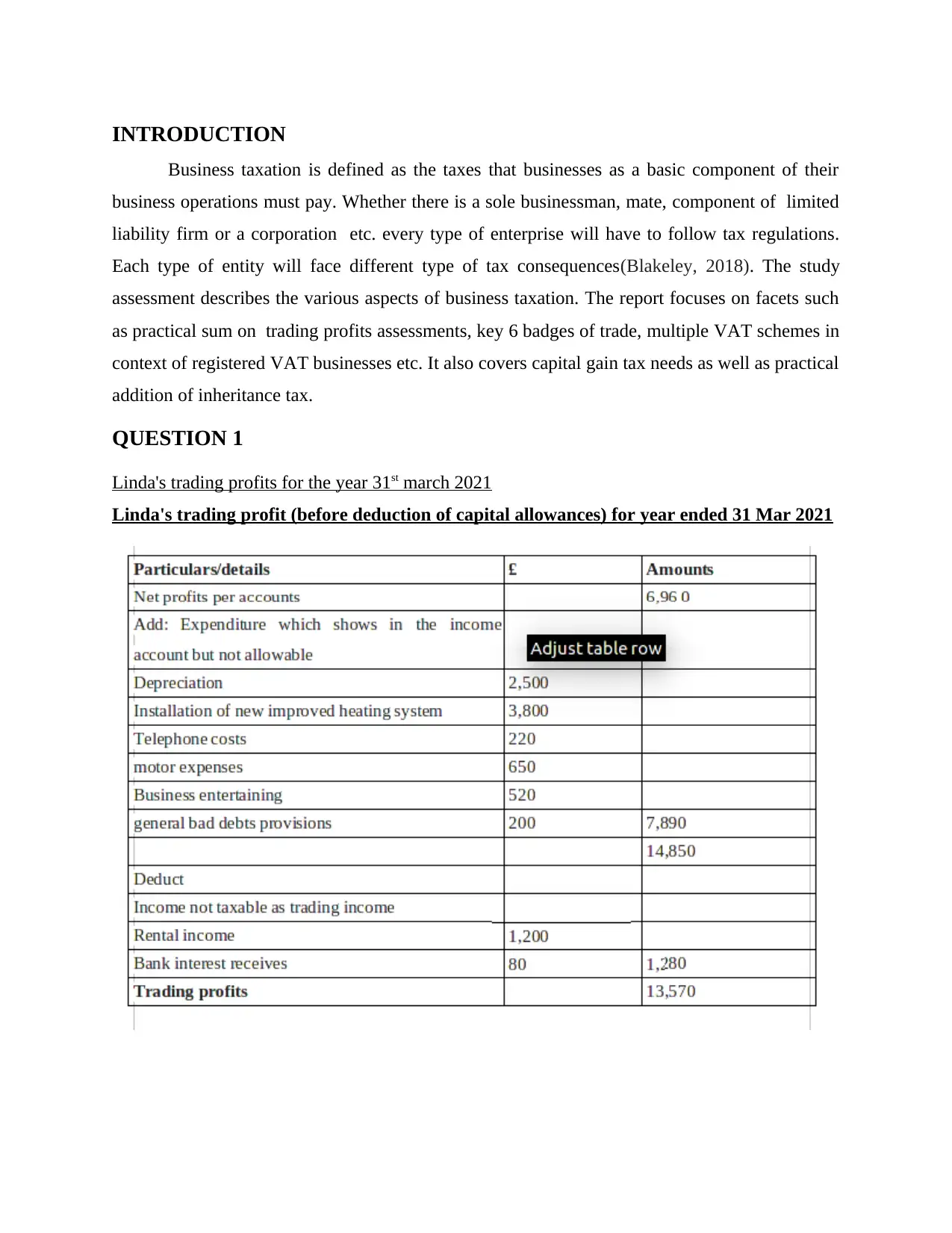

Linda's trading profits for the year 31st march 2021

Linda's trading profit (before deduction of capital allowances) for year ended 31 Mar 2021

Business taxation is defined as the taxes that businesses as a basic component of their

business operations must pay. Whether there is a sole businessman, mate, component of limited

liability firm or a corporation etc. every type of enterprise will have to follow tax regulations.

Each type of entity will face different type of tax consequences(Blakeley, 2018). The study

assessment describes the various aspects of business taxation. The report focuses on facets such

as practical sum on trading profits assessments, key 6 badges of trade, multiple VAT schemes in

context of registered VAT businesses etc. It also covers capital gain tax needs as well as practical

addition of inheritance tax.

QUESTION 1

Linda's trading profits for the year 31st march 2021

Linda's trading profit (before deduction of capital allowances) for year ended 31 Mar 2021

QUESTION 2

Criteria which can be used to distinguish employment from self employment. Why people prefer

self employment?

Employment refers as a bond between two parties basically based on written agreement

where work is paid for, here one party whether it is a corporation, profitable or non profitable

organisation or other type of entity act as employer and another party is employee. For salaries

employees work which can be either in form of hourly wages or annual salary totally depends on

type of work allotted to employee or their sector of working. In some fields employees receives

tips, bonuses etc. or in some fields they get benefits like health insurances, Disability and

housing insurances, or gym memberships etc. Employment is strictly governed under

employment laws or organisation contracts. Both employee and employer can cancel the contract

also (England, 2017). Employment contract with employees may need written correspondences,

letter of confirmation as well as verbal confrontation. The UK describes employment in terms of

'service contract'. This contract empowers employers as where they can appoint employees and

how they can get done their works.

Employment allows employees to decide or control various aspects of their job like

working place, infrastructure, hours, salaries and duty. Employer controls the feedback of

employee as well as trust on them. In private sector when employee have some issues with

employer then they have a wide range of options either they can take their problem to supervisor,

speak to senior authorities, go to HR etc. Employers are not permitted to discriminate on basis of

sex, colour, age, religion, nationality, personal liking, sexual liking, political positioning or

disabilities (Fritsch and Wyrwich, 2017). As employees possess the right to file a complaint on

the basis of discrimination they have faced to relevant authorities which obligates correct

regulations of employment. In UK employment contracts are classified by government into

different categories such as fixed time contract (it lasts for definite period of time), part time or

full time contract( it has no specific period of time), agency staffs, freelancers, contractors,

consultants and zero hour contracts.

The term self employment refers to 'setting up and operating a profitable company or

social welfare organisation'. A lot of successful firms were started when males and females

invented something innovative, set up their business and certified a trademark. In success of a

business an important role is played by outstanding business concept in market place while its

Criteria which can be used to distinguish employment from self employment. Why people prefer

self employment?

Employment refers as a bond between two parties basically based on written agreement

where work is paid for, here one party whether it is a corporation, profitable or non profitable

organisation or other type of entity act as employer and another party is employee. For salaries

employees work which can be either in form of hourly wages or annual salary totally depends on

type of work allotted to employee or their sector of working. In some fields employees receives

tips, bonuses etc. or in some fields they get benefits like health insurances, Disability and

housing insurances, or gym memberships etc. Employment is strictly governed under

employment laws or organisation contracts. Both employee and employer can cancel the contract

also (England, 2017). Employment contract with employees may need written correspondences,

letter of confirmation as well as verbal confrontation. The UK describes employment in terms of

'service contract'. This contract empowers employers as where they can appoint employees and

how they can get done their works.

Employment allows employees to decide or control various aspects of their job like

working place, infrastructure, hours, salaries and duty. Employer controls the feedback of

employee as well as trust on them. In private sector when employee have some issues with

employer then they have a wide range of options either they can take their problem to supervisor,

speak to senior authorities, go to HR etc. Employers are not permitted to discriminate on basis of

sex, colour, age, religion, nationality, personal liking, sexual liking, political positioning or

disabilities (Fritsch and Wyrwich, 2017). As employees possess the right to file a complaint on

the basis of discrimination they have faced to relevant authorities which obligates correct

regulations of employment. In UK employment contracts are classified by government into

different categories such as fixed time contract (it lasts for definite period of time), part time or

full time contract( it has no specific period of time), agency staffs, freelancers, contractors,

consultants and zero hour contracts.

The term self employment refers to 'setting up and operating a profitable company or

social welfare organisation'. A lot of successful firms were started when males and females

invented something innovative, set up their business and certified a trademark. In success of a

business an important role is played by outstanding business concept in market place while its

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

implementation determines its fate. If someone has particular choice of career in certain direction

then self employment can be chosen. Basically

journalism, law, medical, artists these type of fields in which self employment or self practice

can be chosen (Hessels and et. al., 2017). It evinces to state of practice by self rather than

employer. In self employment individual will have to submit tax on the basis of revenue they

generate and under the law of applicable jurisdiction as well as according to the tax slab category

in which they fall. Basically the taxation authorities will consider individuals applicable to pay

taxes if they are known or generates revenue so that they can pay tax according to law in

applicable jurisdiction. For taxation officials their job is to overlook whether individual is

trading, efficient or actually taxable. If individual is not making profit so it is looked by taxation

officials occasionally or on the basis of hobby enthusiastic practice of economy.

Self employed people usually opt employment of their own choice vs recruited by firms and

receive their incomes from commercialism or from the firms where they work. Law makers in

few countries have more faith in evaluation whether an individual is self employed or they might

have registered to distinct employment, which sometimes represented as assumption for

negotiating the deal of intra business to conceal what is actually this employee-employer

agreement. After this also some people's role is not that promptly manifest.

Why people prefer self employment rather than being employed, resulting in so many IR 35

cases

As analysed in recent times, various individual prefer to work for themselves rather then

being an employee of an organisation. The common reason which was been extracted by

performing various researches was the most of them feel if provided with full freedom they can

be more productive (Milovanoff, Posen and MacLean, 2020). Various controlling activities in an

organisation is the main reason behind an individual being self employee-employed. Being in

freedom stage not only refers to flexibility in working hours but also is related to respective

operational activities of the business firm. A sense of better motivation is been delivered to an

individual after realising on fact of fully owned profits. Being self-employed refers to being in

stage of carrying individual business activities with their own mind sets and preparation of

respective business policies as per an individual comfort.

According to Lea, 2020, in year 1999, UK's Inland Revenue presented a new measure

which was been dedicated for tax avoidance techniques. It is aimed at limiting ability of small

then self employment can be chosen. Basically

journalism, law, medical, artists these type of fields in which self employment or self practice

can be chosen (Hessels and et. al., 2017). It evinces to state of practice by self rather than

employer. In self employment individual will have to submit tax on the basis of revenue they

generate and under the law of applicable jurisdiction as well as according to the tax slab category

in which they fall. Basically the taxation authorities will consider individuals applicable to pay

taxes if they are known or generates revenue so that they can pay tax according to law in

applicable jurisdiction. For taxation officials their job is to overlook whether individual is

trading, efficient or actually taxable. If individual is not making profit so it is looked by taxation

officials occasionally or on the basis of hobby enthusiastic practice of economy.

Self employed people usually opt employment of their own choice vs recruited by firms and

receive their incomes from commercialism or from the firms where they work. Law makers in

few countries have more faith in evaluation whether an individual is self employed or they might

have registered to distinct employment, which sometimes represented as assumption for

negotiating the deal of intra business to conceal what is actually this employee-employer

agreement. After this also some people's role is not that promptly manifest.

Why people prefer self employment rather than being employed, resulting in so many IR 35

cases

As analysed in recent times, various individual prefer to work for themselves rather then

being an employee of an organisation. The common reason which was been extracted by

performing various researches was the most of them feel if provided with full freedom they can

be more productive (Milovanoff, Posen and MacLean, 2020). Various controlling activities in an

organisation is the main reason behind an individual being self employee-employed. Being in

freedom stage not only refers to flexibility in working hours but also is related to respective

operational activities of the business firm. A sense of better motivation is been delivered to an

individual after realising on fact of fully owned profits. Being self-employed refers to being in

stage of carrying individual business activities with their own mind sets and preparation of

respective business policies as per an individual comfort.

According to Lea, 2020, in year 1999, UK's Inland Revenue presented a new measure

which was been dedicated for tax avoidance techniques. It is aimed at limiting ability of small

business owners and employees working on contractual basis to limit amount of their respective

contribution towards income tax. This technique was been used by many business enterprise but

after introduction of IR-35, there were major changes been done in governing policies of the

nation. By using intermediate companies, various individual in past could take advantages of tax

liabilities, for instance, sharing up of ownership of their small business firm with a family

member or relative which provided them huge benefits in taxations. This also created a huge

factor in increasing cases of self employed individuals rather then being in job profile (How The

IR35 Changes Will Affect Rules On Self-Employment, 2020). Addition reasons of being in self

employed business rather than in working in a job profile are as follows:

Tax Benefits: Individuals with self employment can use benefits of exemption of cost

such as telephone bills and various network facilities (Modrego, Paredes and Romaní, 2017).

With light to the fact that respective government body of respective nation focuses more on

company structures for imposing taxations. Whereas individuals with self employment are been

benefited with these types of regulations.

Potential for Growth: As by analysing market trend, it can be said that potential for

growth of an individual firm is likely to be greater then being in specific job profile working. As

being self employed involves more individual efforts in various operational activities of the

business firm when compared to being employed in an organisation. Respective individual are

more explored to various business activities and it also includes conduction of activities outside

comfortable zones of respective individuals.

Customer interaction: In case of self employment, it is been analysed that there is greater

opportunity for interaction of business customers as compared to employed people (Moritz,

2017). In employment type profile, individuals are been expected to perform their respective job

tasks and their efforts are been concentrated towards completion of organisational objectives and

goals.

QUESTION 3

Discussion of Six badges for trade

The basic concept of six badges of trade refers to classification of various activities as

business or just a hobby. As per policies of trading allowances introduced in 2017, tax payers are

been given allowance of 1000 cents to spend their income on hobbies, which will be 100% tax

contribution towards income tax. This technique was been used by many business enterprise but

after introduction of IR-35, there were major changes been done in governing policies of the

nation. By using intermediate companies, various individual in past could take advantages of tax

liabilities, for instance, sharing up of ownership of their small business firm with a family

member or relative which provided them huge benefits in taxations. This also created a huge

factor in increasing cases of self employed individuals rather then being in job profile (How The

IR35 Changes Will Affect Rules On Self-Employment, 2020). Addition reasons of being in self

employed business rather than in working in a job profile are as follows:

Tax Benefits: Individuals with self employment can use benefits of exemption of cost

such as telephone bills and various network facilities (Modrego, Paredes and Romaní, 2017).

With light to the fact that respective government body of respective nation focuses more on

company structures for imposing taxations. Whereas individuals with self employment are been

benefited with these types of regulations.

Potential for Growth: As by analysing market trend, it can be said that potential for

growth of an individual firm is likely to be greater then being in specific job profile working. As

being self employed involves more individual efforts in various operational activities of the

business firm when compared to being employed in an organisation. Respective individual are

more explored to various business activities and it also includes conduction of activities outside

comfortable zones of respective individuals.

Customer interaction: In case of self employment, it is been analysed that there is greater

opportunity for interaction of business customers as compared to employed people (Moritz,

2017). In employment type profile, individuals are been expected to perform their respective job

tasks and their efforts are been concentrated towards completion of organisational objectives and

goals.

QUESTION 3

Discussion of Six badges for trade

The basic concept of six badges of trade refers to classification of various activities as

business or just a hobby. As per policies of trading allowances introduced in 2017, tax payers are

been given allowance of 1000 cents to spend their income on hobbies, which will be 100% tax

free. A report was been conducted by Royal Commission of Taxation of Profits and Incomes in

1955 and six badges of trades were been identified. It includes the following six badges of trade

which are as follows:

Profit Motive: For classifying various activities as business and non business activities,

ultimate objective or goals are been determined. In this heading of profit motive, it is being

determined if respective activity is been carried out with a motive to earn profits, then it will be

eligible for taxation policies. An individual should not be confused between two term which is

profits and gains respectively (Patel and Wolfe, 2019). The term profits refers to various

activities which are been performed by business enterprise on regular bases. For example;

production and selling tea is a main business of an enterprise, profits earned by such activities is

taxable. On the other hand, term gain refers to various activities which are irregular in nature and

includes selling of fixed assets of the company. For example; selling any machinery which is

used in production activity of the business firm is termed under capital gains and is taxable under

capital gains taxation policy.

Transaction Number: A single transaction should not be considered as trading activity.

However, transaction done on regular basis and extracting profits from them is to be covered in

trading profits of the business firm and is taxable under the law (Scarcella, 2020).

Changes to the Asset: It refers to any changes in value of asset caused due to internal and

external environment of business firm. For instance, a firm deals with production of masks and

by a sudden changes in the market trends, demand for mask arose. By taking example of current

pandemic situation, as per changes in political and legal environment of the business firm,

demand for respective product arises (Siebert, 2019). The respective firms engaged in production

of masks, noticed a huge boom in market demand of the product and increased value of asset to

the firm due to changes in market demand.

Finance source: Determination of various sources of finance to a business firm is an

important task for the business firm. Finance is treated as valuable resource to the company as

various activities of the firm is been directed towards availability of financial resources of

business firm (Sun, Zhan and Du, 2020). Respective decision making and strategies made in

planning structures of workforce includes availability of finance resource to the business firm.

Sound management of the company extract finance for the company effectively in order to shape

1955 and six badges of trades were been identified. It includes the following six badges of trade

which are as follows:

Profit Motive: For classifying various activities as business and non business activities,

ultimate objective or goals are been determined. In this heading of profit motive, it is being

determined if respective activity is been carried out with a motive to earn profits, then it will be

eligible for taxation policies. An individual should not be confused between two term which is

profits and gains respectively (Patel and Wolfe, 2019). The term profits refers to various

activities which are been performed by business enterprise on regular bases. For example;

production and selling tea is a main business of an enterprise, profits earned by such activities is

taxable. On the other hand, term gain refers to various activities which are irregular in nature and

includes selling of fixed assets of the company. For example; selling any machinery which is

used in production activity of the business firm is termed under capital gains and is taxable under

capital gains taxation policy.

Transaction Number: A single transaction should not be considered as trading activity.

However, transaction done on regular basis and extracting profits from them is to be covered in

trading profits of the business firm and is taxable under the law (Scarcella, 2020).

Changes to the Asset: It refers to any changes in value of asset caused due to internal and

external environment of business firm. For instance, a firm deals with production of masks and

by a sudden changes in the market trends, demand for mask arose. By taking example of current

pandemic situation, as per changes in political and legal environment of the business firm,

demand for respective product arises (Siebert, 2019). The respective firms engaged in production

of masks, noticed a huge boom in market demand of the product and increased value of asset to

the firm due to changes in market demand.

Finance source: Determination of various sources of finance to a business firm is an

important task for the business firm. Finance is treated as valuable resource to the company as

various activities of the firm is been directed towards availability of financial resources of

business firm (Sun, Zhan and Du, 2020). Respective decision making and strategies made in

planning structures of workforce includes availability of finance resource to the business firm.

Sound management of the company extract finance for the company effectively in order to shape

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

respective activities of an organisation towards completion of organisational goals and

objectives.

Time period between purchase and sales: The time of holding up of an asset is an

important indicator of trade. It changes the nature of the transaction of the time being help in

exchange. If longer time is been consumed in the process it would be considered as an

investment rather then a normal trade activity. It results in huge changes in planning of finance

for a business firm, as tax policies for investment and trade are different.

Method of Acquisition: In this badge of trade, it highlights the importance of processes

involved in acquisition of an asset. An asset of a business firm can be acquired in different ways,

Firstly an asset is been purchased from open market another would be that an asset is been gifted

to a business firm. An asset acquired by a firm is by purchasing involves trading activities and

therefore is eligible for taxation under law.

Different VAT schemes for various VAT registered companies

VAT is understated as a consumption tax which is been imposed on a product, whenever

certain value is been added in various stages i.e. from point of production to sales activities. As

analysed more then 160 countries across the world uses VAT system out of which most of them

are from EU. It proves to be an effective method that contributes to increased revenue of

government without hampering success or wealth of various companies. It is an indirect form of

taxation system which is been imposed on consumption products or services.

According to Money Donut, various VAT accounting schemes makes corporate life

easier by simplifying taxation systems of a the company and enables management of concerned

organisation to focus more effectively on their core business activities. An ideal standard is been

setted for various companies, if company's net turnover is below 1.35 million cents, then this

type of taxation policies proves to be best effective for conduction of their respective operational

activities (VAT accounting schemes, 2021). In UK origin various types of VAT schemes are

been followed which are mentioned below:

VAT annual accounting system scheme: In this type of VAT accounting scheme, a

company is been entitled to file VAT return once a year. This scheme is usually been used by

various business enterprise which deals in small scale scale operational activities. One of

eligibility criteria for this scheme is that a company must have VAT turnover less then or equal

to 1.35 million cents. Management of various small scale business organisation enjoys befits for

objectives.

Time period between purchase and sales: The time of holding up of an asset is an

important indicator of trade. It changes the nature of the transaction of the time being help in

exchange. If longer time is been consumed in the process it would be considered as an

investment rather then a normal trade activity. It results in huge changes in planning of finance

for a business firm, as tax policies for investment and trade are different.

Method of Acquisition: In this badge of trade, it highlights the importance of processes

involved in acquisition of an asset. An asset of a business firm can be acquired in different ways,

Firstly an asset is been purchased from open market another would be that an asset is been gifted

to a business firm. An asset acquired by a firm is by purchasing involves trading activities and

therefore is eligible for taxation under law.

Different VAT schemes for various VAT registered companies

VAT is understated as a consumption tax which is been imposed on a product, whenever

certain value is been added in various stages i.e. from point of production to sales activities. As

analysed more then 160 countries across the world uses VAT system out of which most of them

are from EU. It proves to be an effective method that contributes to increased revenue of

government without hampering success or wealth of various companies. It is an indirect form of

taxation system which is been imposed on consumption products or services.

According to Money Donut, various VAT accounting schemes makes corporate life

easier by simplifying taxation systems of a the company and enables management of concerned

organisation to focus more effectively on their core business activities. An ideal standard is been

setted for various companies, if company's net turnover is below 1.35 million cents, then this

type of taxation policies proves to be best effective for conduction of their respective operational

activities (VAT accounting schemes, 2021). In UK origin various types of VAT schemes are

been followed which are mentioned below:

VAT annual accounting system scheme: In this type of VAT accounting scheme, a

company is been entitled to file VAT return once a year. This scheme is usually been used by

various business enterprise which deals in small scale scale operational activities. One of

eligibility criteria for this scheme is that a company must have VAT turnover less then or equal

to 1.35 million cents. Management of various small scale business organisation enjoys befits for

filing of VAT return file once a year rather then 4 times a year. It proves great help to such

organisation as its management could focus more effectively on core operational activities and

provides better path towards objectives and goals of a business firm.

Flat rate scheme: In this type of scheme a business organisation have to pay percent of

their revenue to HM revenue and customs. The percentage which is been changed to a business

varies from business to business depending on operational activities conducted by them. The

customers of such business firms are been charged with an add on to MRP with name of VAT,

without giving any particular detail about purchase and sales activities of the business firm. For

being eligible for this taxation system, turnover of respective firms should be less the or equal to

1.50 million cents. Benefits of this scheme is that it saves up to time as a resource of the firm and

also helps in saving up of cost in compiling process of the firm, as less unproductive formalities

are been followed up in such schemes (Wood and Lehdonvirta, 2019). Disadvantage of this

scheme is that, if a business firm carries out more turnover, ultimately it have to pay more. As it

is the percent charged on net turnover of the firm charges increases with increment in turnover of

company and in long term it might affect profitability of the business firm.

VAT margin scheme: This type of scheme is been largely used by various business

which deals in antique products as well as goods which are already in use and up to the mark for

resale condition. It is the most flexible and clear scheme in various VAT schemes. The

calculation of tax is been determined by difference in amount of acquisition and selling of

respective product or services by a business firm. In this scheme, the manager or leader of the

business firm is entitled to present firm's daily transaction report.

organisation as its management could focus more effectively on core operational activities and

provides better path towards objectives and goals of a business firm.

Flat rate scheme: In this type of scheme a business organisation have to pay percent of

their revenue to HM revenue and customs. The percentage which is been changed to a business

varies from business to business depending on operational activities conducted by them. The

customers of such business firms are been charged with an add on to MRP with name of VAT,

without giving any particular detail about purchase and sales activities of the business firm. For

being eligible for this taxation system, turnover of respective firms should be less the or equal to

1.50 million cents. Benefits of this scheme is that it saves up to time as a resource of the firm and

also helps in saving up of cost in compiling process of the firm, as less unproductive formalities

are been followed up in such schemes (Wood and Lehdonvirta, 2019). Disadvantage of this

scheme is that, if a business firm carries out more turnover, ultimately it have to pay more. As it

is the percent charged on net turnover of the firm charges increases with increment in turnover of

company and in long term it might affect profitability of the business firm.

VAT margin scheme: This type of scheme is been largely used by various business

which deals in antique products as well as goods which are already in use and up to the mark for

resale condition. It is the most flexible and clear scheme in various VAT schemes. The

calculation of tax is been determined by difference in amount of acquisition and selling of

respective product or services by a business firm. In this scheme, the manager or leader of the

business firm is entitled to present firm's daily transaction report.

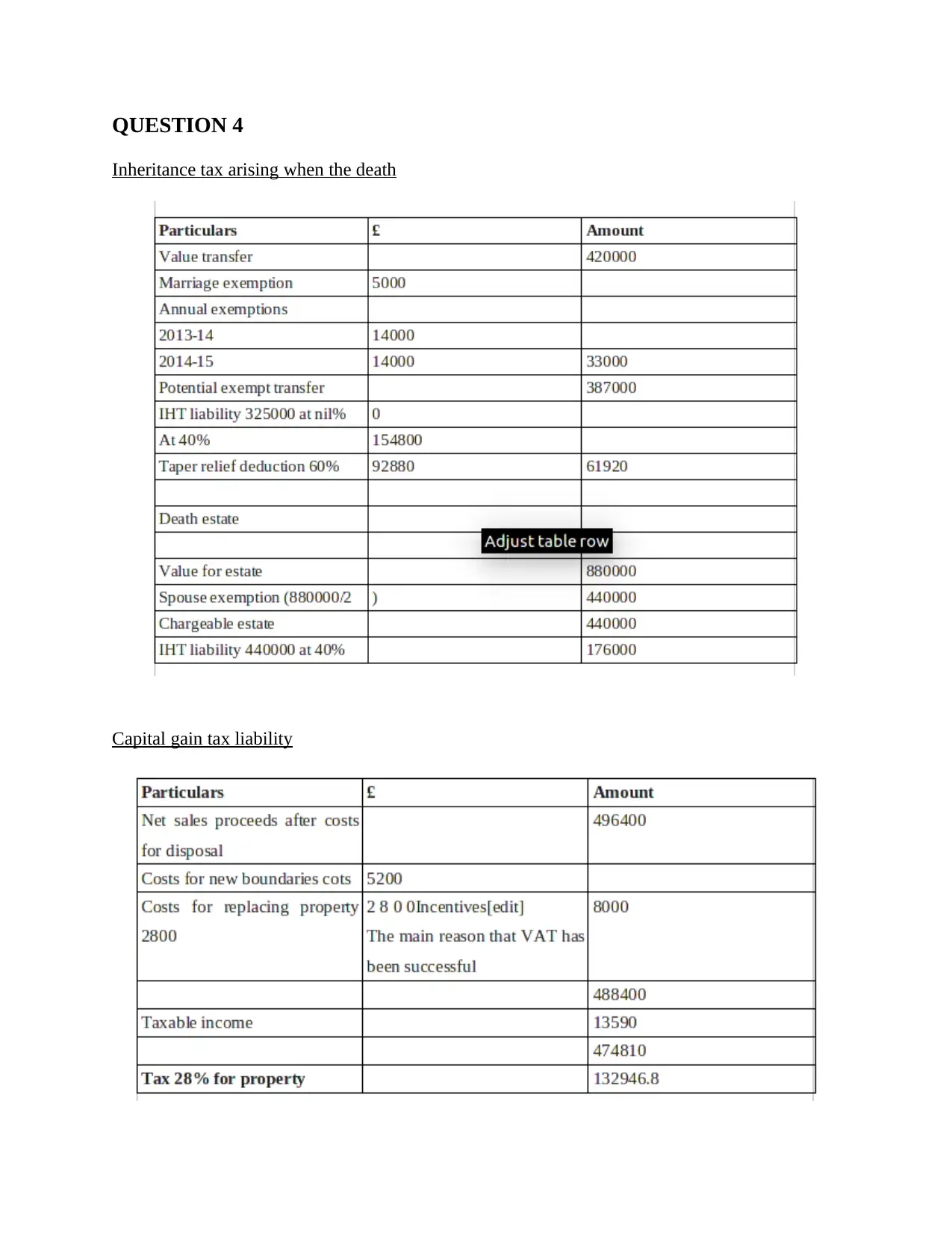

QUESTION 4

Inheritance tax arising when the death

Capital gain tax liability

Inheritance tax arising when the death

Capital gain tax liability

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

From the above report, it can be concluded that various types of business organisation

have its distinctive tax consequences. Various owners of business enterprises are been owed to

government of their respective nation for payment of taxes for conducting various activities of

the business firm. Focus on meaning of taxable income is been highlighted in this document with

company's trading profit statement. With addition to that, reason for individual being more

concerned about self employment rather then working in a company as a employee is being

analysed and this report is been supported with setting of standards of trade badges which

classify respective activities of the firm as trading taxable as well as non taxable income.

From the above report, it can be concluded that various types of business organisation

have its distinctive tax consequences. Various owners of business enterprises are been owed to

government of their respective nation for payment of taxes for conducting various activities of

the business firm. Focus on meaning of taxable income is been highlighted in this document with

company's trading profit statement. With addition to that, reason for individual being more

concerned about self employment rather then working in a company as a employee is being

analysed and this report is been supported with setting of standards of trade badges which

classify respective activities of the firm as trading taxable as well as non taxable income.

REFERENCES

Books and Journals

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

England, P., 2017. Households, employment, and gender: A social, economic, and demographic

view. Routledge.

Fritsch, M. and Wyrwich, M., 2017. The effect of entrepreneurship on economic development—

an empirical analysis using regional entrepreneurship culture. Journal of Economic

Geography, 17(1), pp.157-189.

Hessels, J. and et. al., 2017. Self-employment and work-related stress: The mediating role of job

control and job demand. Journal of Business Venturing, 32(2), pp.178-196.

Milovanoff, A., Posen, I.D. and MacLean, H.L., 2020. Quantifying environmental impacts of

primary aluminum ingot production and consumption: A trade‐linked multilevel life

cycle assessment. Journal of Industrial Ecology.

Modrego, F., Paredes, D. and Romaní, G., 2017. Individual and place-based drivers of self-

employment in Chile. Small Business Economics, 49(2), pp.469-492.

Moritz, S.C., 2017. Examination of badges to increase nursing student engagement: A quasi-

experimental study (Doctoral dissertation, Capella University).

Patel, P.C. and Wolfe, M.T., 2019. In the eye of the beholder? The returns to beauty and IQ for

the self‐employed. Strategic Entrepreneurship Journal.

Scarcella, L., 2020. E-commerce and effective VAT/GST enforcement: Can online platforms

play a valuable role?. Computer Law & Security Review, 36, p.105371.

Siebert, H., 2019. Reforming capital income taxation. Routledge.

Sun, C., Zhan, Y. and Du, G., 2020. Can value-added tax incentives of new energy industry

increase firm's profitability? Evidence from financial data of China's listed

companies. Energy Economics, 86, p.104654.

Wood, A. and Lehdonvirta, V., 2019. Platform labour and structured antagonism: Understanding

the origins of protest in the gig economy. Available at SSRN 3357804.

Online

VAT accounting schemes, 2021, [online], available

through<https://www.moneydonut.co.uk/tax/vat/vat-accounting-schemes>

How The IR35 Changes Will Affect Rules On Self-Employment, 2020, [online], available

through<https://www.jonathanlea.net/2019/how-the-ir35-changes-will-affect-rules-on-

self-employment/>

Books and Journals

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

England, P., 2017. Households, employment, and gender: A social, economic, and demographic

view. Routledge.

Fritsch, M. and Wyrwich, M., 2017. The effect of entrepreneurship on economic development—

an empirical analysis using regional entrepreneurship culture. Journal of Economic

Geography, 17(1), pp.157-189.

Hessels, J. and et. al., 2017. Self-employment and work-related stress: The mediating role of job

control and job demand. Journal of Business Venturing, 32(2), pp.178-196.

Milovanoff, A., Posen, I.D. and MacLean, H.L., 2020. Quantifying environmental impacts of

primary aluminum ingot production and consumption: A trade‐linked multilevel life

cycle assessment. Journal of Industrial Ecology.

Modrego, F., Paredes, D. and Romaní, G., 2017. Individual and place-based drivers of self-

employment in Chile. Small Business Economics, 49(2), pp.469-492.

Moritz, S.C., 2017. Examination of badges to increase nursing student engagement: A quasi-

experimental study (Doctoral dissertation, Capella University).

Patel, P.C. and Wolfe, M.T., 2019. In the eye of the beholder? The returns to beauty and IQ for

the self‐employed. Strategic Entrepreneurship Journal.

Scarcella, L., 2020. E-commerce and effective VAT/GST enforcement: Can online platforms

play a valuable role?. Computer Law & Security Review, 36, p.105371.

Siebert, H., 2019. Reforming capital income taxation. Routledge.

Sun, C., Zhan, Y. and Du, G., 2020. Can value-added tax incentives of new energy industry

increase firm's profitability? Evidence from financial data of China's listed

companies. Energy Economics, 86, p.104654.

Wood, A. and Lehdonvirta, V., 2019. Platform labour and structured antagonism: Understanding

the origins of protest in the gig economy. Available at SSRN 3357804.

Online

VAT accounting schemes, 2021, [online], available

through<https://www.moneydonut.co.uk/tax/vat/vat-accounting-schemes>

How The IR35 Changes Will Affect Rules On Self-Employment, 2020, [online], available

through<https://www.jonathanlea.net/2019/how-the-ir35-changes-will-affect-rules-on-

self-employment/>

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.