Business Taxation Law and Policy

VerifiedAdded on 2023/06/09

|11

|2723

|122

AI Summary

This article discusses the principles of business taxation law and policy in Australia. It covers topics such as input tax credits, GST-free exports, and taxable importations. The article also provides examples and references to relevant taxation rulings and legislation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS TAXATION LAW AND POLICY

Business Taxation Law and Policy

Name of the Student

Name of the University

Authors Note

Course ID

Business Taxation Law and Policy

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS TAXATION LAW AND POLICY

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................6

References..................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................6

References..................................................................................................................................9

2BUSINESS TAXATION LAW AND POLICY

Answer to question 1:

An individual entity registered or required to obtain the registration is held liable for

GST payable relating to the taxable supplies made by the entity1. The entity is also entitled to

obtain the input tax credit for the creditable acquisition that is made on carrying on the

enterprise. In order to make the acquisition creditable the entity is required to acquire or

import the goods entirely for the creditable purpose. When there is a circumstances of partly

creditable purpose the entity is not allowed to claim input tax credit unless and until

“Division 131” is applicable.

The taxation ruling of “Goods and Service Tax GSTR 2000/6” is associated with

the creditable purpose for the purpose of claiming input tax credits. The Australian taxation

office provides that an individual can claim credit for any amount of GST that is included in

the price of any goods and service that is bought by a person for the purpose of business2.

This is known as the GST credits or the input tax credits – a credit that forms the part of the

price of an entity’s business inputs. An important consideration of claiming GST credits is

that it is necessary to ensure that the suppliers are registered for GST.

As evident from the current situation of ABC Comp the company has only managed

to make sales of $6,000 throughout the year. The company incurs business and input tax

expenses of $5,100 for the year 2016. The “taxation ruling of GSTR 2000/6” lay down the

guidance of determining the degree to which an entity for creditable purpose while making

acquisition and importation enables in claiming the correct sum of input tax credits3. An

individual can only claim input tax credits for the acquisition which is creditable. To

1 Brokelind, Cécile. Principles Of Law 2014. Print

2 Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 Principles Of

Business Taxation. Print.

3 James, Simon. 2018 The Economics Of Taxation. Print.

Answer to question 1:

An individual entity registered or required to obtain the registration is held liable for

GST payable relating to the taxable supplies made by the entity1. The entity is also entitled to

obtain the input tax credit for the creditable acquisition that is made on carrying on the

enterprise. In order to make the acquisition creditable the entity is required to acquire or

import the goods entirely for the creditable purpose. When there is a circumstances of partly

creditable purpose the entity is not allowed to claim input tax credit unless and until

“Division 131” is applicable.

The taxation ruling of “Goods and Service Tax GSTR 2000/6” is associated with

the creditable purpose for the purpose of claiming input tax credits. The Australian taxation

office provides that an individual can claim credit for any amount of GST that is included in

the price of any goods and service that is bought by a person for the purpose of business2.

This is known as the GST credits or the input tax credits – a credit that forms the part of the

price of an entity’s business inputs. An important consideration of claiming GST credits is

that it is necessary to ensure that the suppliers are registered for GST.

As evident from the current situation of ABC Comp the company has only managed

to make sales of $6,000 throughout the year. The company incurs business and input tax

expenses of $5,100 for the year 2016. The “taxation ruling of GSTR 2000/6” lay down the

guidance of determining the degree to which an entity for creditable purpose while making

acquisition and importation enables in claiming the correct sum of input tax credits3. An

individual can only claim input tax credits for the acquisition which is creditable. To

1 Brokelind, Cécile. Principles Of Law 2014. Print

2 Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 Principles Of

Business Taxation. Print.

3 James, Simon. 2018 The Economics Of Taxation. Print.

3BUSINESS TAXATION LAW AND POLICY

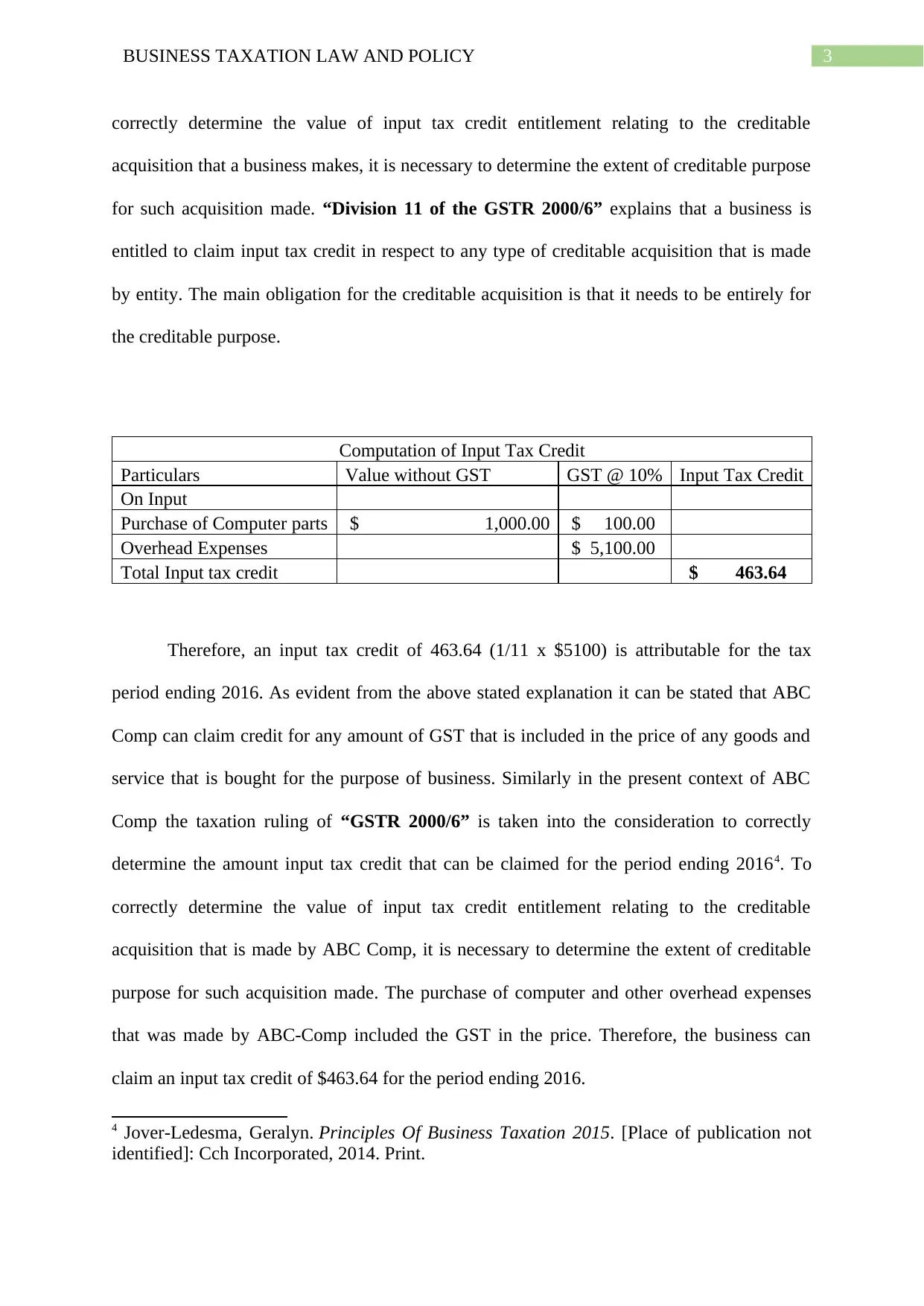

correctly determine the value of input tax credit entitlement relating to the creditable

acquisition that a business makes, it is necessary to determine the extent of creditable purpose

for such acquisition made. “Division 11 of the GSTR 2000/6” explains that a business is

entitled to claim input tax credit in respect to any type of creditable acquisition that is made

by entity. The main obligation for the creditable acquisition is that it needs to be entirely for

the creditable purpose.

Computation of Input Tax Credit

Particulars Value without GST GST @ 10% Input Tax Credit

On Input

Purchase of Computer parts $ 1,000.00 $ 100.00

Overhead Expenses $ 5,100.00

Total Input tax credit $ 463.64

Therefore, an input tax credit of 463.64 (1/11 x $5100) is attributable for the tax

period ending 2016. As evident from the above stated explanation it can be stated that ABC

Comp can claim credit for any amount of GST that is included in the price of any goods and

service that is bought for the purpose of business. Similarly in the present context of ABC

Comp the taxation ruling of “GSTR 2000/6” is taken into the consideration to correctly

determine the amount input tax credit that can be claimed for the period ending 20164. To

correctly determine the value of input tax credit entitlement relating to the creditable

acquisition that is made by ABC Comp, it is necessary to determine the extent of creditable

purpose for such acquisition made. The purchase of computer and other overhead expenses

that was made by ABC-Comp included the GST in the price. Therefore, the business can

claim an input tax credit of $463.64 for the period ending 2016.

4 Jover-Ledesma, Geralyn. Principles Of Business Taxation 2015. [Place of publication not

identified]: Cch Incorporated, 2014. Print.

correctly determine the value of input tax credit entitlement relating to the creditable

acquisition that a business makes, it is necessary to determine the extent of creditable purpose

for such acquisition made. “Division 11 of the GSTR 2000/6” explains that a business is

entitled to claim input tax credit in respect to any type of creditable acquisition that is made

by entity. The main obligation for the creditable acquisition is that it needs to be entirely for

the creditable purpose.

Computation of Input Tax Credit

Particulars Value without GST GST @ 10% Input Tax Credit

On Input

Purchase of Computer parts $ 1,000.00 $ 100.00

Overhead Expenses $ 5,100.00

Total Input tax credit $ 463.64

Therefore, an input tax credit of 463.64 (1/11 x $5100) is attributable for the tax

period ending 2016. As evident from the above stated explanation it can be stated that ABC

Comp can claim credit for any amount of GST that is included in the price of any goods and

service that is bought for the purpose of business. Similarly in the present context of ABC

Comp the taxation ruling of “GSTR 2000/6” is taken into the consideration to correctly

determine the amount input tax credit that can be claimed for the period ending 20164. To

correctly determine the value of input tax credit entitlement relating to the creditable

acquisition that is made by ABC Comp, it is necessary to determine the extent of creditable

purpose for such acquisition made. The purchase of computer and other overhead expenses

that was made by ABC-Comp included the GST in the price. Therefore, the business can

claim an input tax credit of $463.64 for the period ending 2016.

4 Jover-Ledesma, Geralyn. Principles Of Business Taxation 2015. [Place of publication not

identified]: Cch Incorporated, 2014. Print.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS TAXATION LAW AND POLICY

Answer to question 2:

According to the Australian taxation office GST is the wider based tax of 10 per cent

on majority of the goods, services and other types of items that are consumed or sold in

Australia. The exports of goods and services from Australia is considered as usually GST-

Free. An individual is able to claim GST only when it is registered for GST5. This implies

that the individual business concern is not required to include GST in the price of exports.

However, a business can claim GST credits in the price of purchases that is used to make the

export of goods and services.

Evidences from the case facts suggest that X-Corp receives a big order from ABC-Comp

and also makes a part payment for the same on 1st November. The size of order enabled the

ABC-Corp to delay in exporting the computers to X-Corp and order was finally exported in

May 2018. According to the Australian taxation office goods that are exported from Australia

within 60 days of the two below stated events;

a. Suppliers receiving any payment for the goods

b. The supplier issuing an invoice for the goods

The “taxation ruling of GSTR 2002/6” is associated with the application of “section 38-

185 of the GST Act 1999” that defines the supplies of goods are GST-free exports6.

“Section 38-185 of the GST Act 1999” is applicable only for the supplies of goods.

According to the legislative context of “section 9-5” a taxable supply is occurs if an

individual makes the supply for considerations or the supply is associated with Australia and

an individual is required to be registered or registered under GST. The supply of goods where

the goods are exported from Australia is considered as GST-free given the requirements of

5 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. Print.

6 McCouat, Philip. Australian Master GST Guide 2018. Print.

Answer to question 2:

According to the Australian taxation office GST is the wider based tax of 10 per cent

on majority of the goods, services and other types of items that are consumed or sold in

Australia. The exports of goods and services from Australia is considered as usually GST-

Free. An individual is able to claim GST only when it is registered for GST5. This implies

that the individual business concern is not required to include GST in the price of exports.

However, a business can claim GST credits in the price of purchases that is used to make the

export of goods and services.

Evidences from the case facts suggest that X-Corp receives a big order from ABC-Comp

and also makes a part payment for the same on 1st November. The size of order enabled the

ABC-Corp to delay in exporting the computers to X-Corp and order was finally exported in

May 2018. According to the Australian taxation office goods that are exported from Australia

within 60 days of the two below stated events;

a. Suppliers receiving any payment for the goods

b. The supplier issuing an invoice for the goods

The “taxation ruling of GSTR 2002/6” is associated with the application of “section 38-

185 of the GST Act 1999” that defines the supplies of goods are GST-free exports6.

“Section 38-185 of the GST Act 1999” is applicable only for the supplies of goods.

According to the legislative context of “section 9-5” a taxable supply is occurs if an

individual makes the supply for considerations or the supply is associated with Australia and

an individual is required to be registered or registered under GST. The supply of goods where

the goods are exported from Australia is considered as GST-free given the requirements of

5 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. Print.

6 McCouat, Philip. Australian Master GST Guide 2018. Print.

5BUSINESS TAXATION LAW AND POLICY

the “subsection 38-168 (1)” is met7. The supply of goods is considered as GST-free given

the suppliers exports the goods from Australia before or inside 60 days following the day on

which the suppliers receives any form of considerations for the supply or when the supplier

gives the invoice for the supply of goods.

The “subsection 38-168 (1)” also explains that a supply is GST-free when the supply

of goods for which considerations is paid in instalments based on contract that requires the

goods to be exported. The supplies are GST free when the day when the suppliers receives

any form of final instalment for the consideration of supply. Similarly, in the situation of X-

Corp “section 38-185” is applicable to the company as the supply of goods occurred from

Australia to overseas8. The supplier X-Corp was the entity and the supply of goods would be

considered as the GST-free under “section 38-185” since the supplier X-Corp has exported

the goods from Australia. the meaning that is provided in this ruling up to the phrase of the

supplier exports that particularly focuses on whether X-Corp sends computer outside

Australia in regard to the act makes sure that section 38-185 is applicable as intended9. The

supply of goods that was made by supplier X-Corp would be considered as the GST-free.

As the supply of goods is GST-free no amount of GST is payable on the supply.

However, X-Corp can claim the input tax credit for materials that was purchased.

7 Nethercott, Les, Ken Devos, and Livia Gonzaga. Australian Taxation Study Manual. 2015

Print.

8 Sadiq, Kerrie et al. Principles Of Taxation Law 2018. Print.

9 Sadiq, Kerrie. Australian Taxation Law Cases 2018. Pyrmont, NSW: Thomson Reuters,

2018. Print.

the “subsection 38-168 (1)” is met7. The supply of goods is considered as GST-free given

the suppliers exports the goods from Australia before or inside 60 days following the day on

which the suppliers receives any form of considerations for the supply or when the supplier

gives the invoice for the supply of goods.

The “subsection 38-168 (1)” also explains that a supply is GST-free when the supply

of goods for which considerations is paid in instalments based on contract that requires the

goods to be exported. The supplies are GST free when the day when the suppliers receives

any form of final instalment for the consideration of supply. Similarly, in the situation of X-

Corp “section 38-185” is applicable to the company as the supply of goods occurred from

Australia to overseas8. The supplier X-Corp was the entity and the supply of goods would be

considered as the GST-free under “section 38-185” since the supplier X-Corp has exported

the goods from Australia. the meaning that is provided in this ruling up to the phrase of the

supplier exports that particularly focuses on whether X-Corp sends computer outside

Australia in regard to the act makes sure that section 38-185 is applicable as intended9. The

supply of goods that was made by supplier X-Corp would be considered as the GST-free.

As the supply of goods is GST-free no amount of GST is payable on the supply.

However, X-Corp can claim the input tax credit for materials that was purchased.

7 Nethercott, Les, Ken Devos, and Livia Gonzaga. Australian Taxation Study Manual. 2015

Print.

8 Sadiq, Kerrie et al. Principles Of Taxation Law 2018. Print.

9 Sadiq, Kerrie. Australian Taxation Law Cases 2018. Pyrmont, NSW: Thomson Reuters,

2018. Print.

6BUSINESS TAXATION LAW AND POLICY

Answer to question 3:

The “Goods and Services Tax Ruling GSTR 2000/31” is related with the supplies

related with the Australia. The ruling identifies that the supply of goods that is associated

with Australia may result in the taxable supply and taxable importations. The supply of goods

is not considered to be GST-free given the supplier re-imports the goods to Australia.

The import of goods to Australia may be considered as the taxable importations and it

is subjected to GST. The ruling also explains that importations of things apart from goods

which is supplied from the overseas nations for the purpose of use in Australia is not

considered as the taxable importations10. Nevertheless, the import of goods apart from the

goods or the real property might be subjected to GST due to the application of operation of

Division 84.

The present case facts of ABC-Comp provide that the company bought and imported

internal hard-drives from the Canadian Hard-drives Ltd which is the Canadian based

company. During the month of July 2017, the hard-drives became defective which resulted

the ABC-Comp to ship back the drives back to Canadian Hard-drive for the purpose of repair.

Following the completion of repair, ABC-Comp reimported the repaired drives back into the

warehouse in Australia.

The “Goods and Service Taxation Ruling 2000/31” explains that if an individual

entity makes the import of goods into the Australia, that the individual entity may be required

to pay the GST on the importation given that importation is the assessable importation11. With

respect to “subsection 13-5(1) of the Goods and Service Taxation Ruling 2000/31” an

individual making an importation of goods would be considered as the taxable supply. Under

10 Taylor, C. J et al. Understanding Taxation Law 2018. Print.

11 Woellner, R. H et al. Australian Taxation Law 2018. Print.

Answer to question 3:

The “Goods and Services Tax Ruling GSTR 2000/31” is related with the supplies

related with the Australia. The ruling identifies that the supply of goods that is associated

with Australia may result in the taxable supply and taxable importations. The supply of goods

is not considered to be GST-free given the supplier re-imports the goods to Australia.

The import of goods to Australia may be considered as the taxable importations and it

is subjected to GST. The ruling also explains that importations of things apart from goods

which is supplied from the overseas nations for the purpose of use in Australia is not

considered as the taxable importations10. Nevertheless, the import of goods apart from the

goods or the real property might be subjected to GST due to the application of operation of

Division 84.

The present case facts of ABC-Comp provide that the company bought and imported

internal hard-drives from the Canadian Hard-drives Ltd which is the Canadian based

company. During the month of July 2017, the hard-drives became defective which resulted

the ABC-Comp to ship back the drives back to Canadian Hard-drive for the purpose of repair.

Following the completion of repair, ABC-Comp reimported the repaired drives back into the

warehouse in Australia.

The “Goods and Service Taxation Ruling 2000/31” explains that if an individual

entity makes the import of goods into the Australia, that the individual entity may be required

to pay the GST on the importation given that importation is the assessable importation11. With

respect to “subsection 13-5(1) of the Goods and Service Taxation Ruling 2000/31” an

individual making an importation of goods would be considered as the taxable supply. Under

10 Taylor, C. J et al. Understanding Taxation Law 2018. Print.

11 Woellner, R. H et al. Australian Taxation Law 2018. Print.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS TAXATION LAW AND POLICY

“section 15-5 of the Goods and Service Taxation Ruling 2000/31” an individual makes the

creditable importation if they import goods entirely or partially for the creditable purpose and

the importation is considered as the assessable importation12.

The entity that makes the assessable import of goods is required to pay the GST

payable on the assessable importations. The amount of tax that is levied on the assessable

import is 10% of the total value of the taxable import. “Subsection 13-20 (2)” offers that the

value of the assessable importation necessarily reflects the value of goods along with the cost

that is incurred in bringing the goods to Australia13.

An individual entity that makes the importation of goods for the creditable purpose up

to the extent that an entity import goods is generally for carrying on the enterprise. As evident

in the current situation of ABC-Comp the company has made the taxable importation that are

within the meaning of customs Act and importation of goods would be considered as taxable

importation. Certainly in case of ABC-Comp “Division 13 of GSTR 2003/15” is applicable

since the taxable importation that is entered into by the company is imported to Australia for

home consumption which is in accordance with the Customs Act14. The court of law in

“Wilson v Chambers (1923)” stated that goods that are imported to Australia when they are

bought to the port of destination for the purpose of being unloaded.

“Subsection 33-15 (1)” explains that GST on the taxable importations is payable by

the importer of goods to Customs at the same time and place and in the identical manner as

12 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

13 Woellner, Robin, Stephen Barkoczy, and Shirley Murphy. Australian Taxation Law 2018

Ebook 28E. Melbourne: OUPANZ, 2018. Print.

14 Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-

1762.

“section 15-5 of the Goods and Service Taxation Ruling 2000/31” an individual makes the

creditable importation if they import goods entirely or partially for the creditable purpose and

the importation is considered as the assessable importation12.

The entity that makes the assessable import of goods is required to pay the GST

payable on the assessable importations. The amount of tax that is levied on the assessable

import is 10% of the total value of the taxable import. “Subsection 13-20 (2)” offers that the

value of the assessable importation necessarily reflects the value of goods along with the cost

that is incurred in bringing the goods to Australia13.

An individual entity that makes the importation of goods for the creditable purpose up

to the extent that an entity import goods is generally for carrying on the enterprise. As evident

in the current situation of ABC-Comp the company has made the taxable importation that are

within the meaning of customs Act and importation of goods would be considered as taxable

importation. Certainly in case of ABC-Comp “Division 13 of GSTR 2003/15” is applicable

since the taxable importation that is entered into by the company is imported to Australia for

home consumption which is in accordance with the Customs Act14. The court of law in

“Wilson v Chambers (1923)” stated that goods that are imported to Australia when they are

bought to the port of destination for the purpose of being unloaded.

“Subsection 33-15 (1)” explains that GST on the taxable importations is payable by

the importer of goods to Customs at the same time and place and in the identical manner as

12 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

13 Woellner, Robin, Stephen Barkoczy, and Shirley Murphy. Australian Taxation Law 2018

Ebook 28E. Melbourne: OUPANZ, 2018. Print.

14 Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-

1762.

8BUSINESS TAXATION LAW AND POLICY

the custom duty is paid on the goods15. Similarly, for ABC-Comp the liability for the GST

falls on the company for making the taxable importation. Therefore, the sum of GST that is

payable on taxable importation made by ABC-Corp stands 10% of its total value.

Import tax credits are available for the creditable importations. An organization that

makes the creditable importation under the Division 15 given the entity imports the goods

entirely for the creditable purpose and the importation would be considered as the taxable

importation16. The primary requirement for the creditable importation is that the entity should

import the goods. In consistent with the scheme of the act the entity that makes the creditable

acquisition can also claim the input tax credit on the creditable acquisition or the creditable

importation. Similarly, for ABC-Corp it completes the custom formalities when the taxable

importation was made by entering into the import of goods for home consumptions. ABC-

Comp would be considered liable to pay the GST on the taxable importation and apart from

this it would also be considered entitled for input tax credits for the creditable importation.

15 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

16 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

the custom duty is paid on the goods15. Similarly, for ABC-Comp the liability for the GST

falls on the company for making the taxable importation. Therefore, the sum of GST that is

payable on taxable importation made by ABC-Corp stands 10% of its total value.

Import tax credits are available for the creditable importations. An organization that

makes the creditable importation under the Division 15 given the entity imports the goods

entirely for the creditable purpose and the importation would be considered as the taxable

importation16. The primary requirement for the creditable importation is that the entity should

import the goods. In consistent with the scheme of the act the entity that makes the creditable

acquisition can also claim the input tax credit on the creditable acquisition or the creditable

importation. Similarly, for ABC-Corp it completes the custom formalities when the taxable

importation was made by entering into the import of goods for home consumptions. ABC-

Comp would be considered liable to pay the GST on the taxable importation and apart from

this it would also be considered entitled for input tax credits for the creditable importation.

15 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

16 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

9BUSINESS TAXATION LAW AND POLICY

References

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Brokelind, Cécile. Principles Of Law 2014. Print.

Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 Principles Of Business

Taxation. Print.

James, Simon. 2018 The Economics Of Taxation. Print.

Jover-Ledesma, Geralyn. Principles Of Business Taxation 2015. [Place of publication not

identified]: Cch Incorporated, 2014. Print.

Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. Print.

McCouat, Philip. Australian Master GST Guide 2018. Print.

Nethercott, Les, Ken Devos, and Livia Gonzaga. Australian Taxation Study Manual. 2015

Print.

Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-

1762.

ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

Sadiq, Kerrie et al. Principles Of Taxation Law 2018. Print.

Sadiq, Kerrie. Australian Taxation Law Cases 2018. Pyrmont, NSW: Thomson Reuters,

2018. Print.

References

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Brokelind, Cécile. Principles Of Law 2014. Print.

Grange, Janet, Geralyn A Jover-Ledesma, and Gary L Maydew. 2014 Principles Of Business

Taxation. Print.

James, Simon. 2018 The Economics Of Taxation. Print.

Jover-Ledesma, Geralyn. Principles Of Business Taxation 2015. [Place of publication not

identified]: Cch Incorporated, 2014. Print.

Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. Print.

McCouat, Philip. Australian Master GST Guide 2018. Print.

Nethercott, Les, Ken Devos, and Livia Gonzaga. Australian Taxation Study Manual. 2015

Print.

Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-

1762.

ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

Sadiq, Kerrie et al. Principles Of Taxation Law 2018. Print.

Sadiq, Kerrie. Australian Taxation Law Cases 2018. Pyrmont, NSW: Thomson Reuters,

2018. Print.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS TAXATION LAW AND POLICY

Taylor, C. J et al. Understanding Taxation Law 2018. Print.

Woellner, R. H et al. Australian Taxation Law 2018. Print.

Woellner, Robin, Stephen Barkoczy, and Shirley Murphy. Australian Taxation Law 2018

Ebook 28E. Melbourne: OUPANZ, 2018. Print.

Taylor, C. J et al. Understanding Taxation Law 2018. Print.

Woellner, R. H et al. Australian Taxation Law 2018. Print.

Woellner, Robin, Stephen Barkoczy, and Shirley Murphy. Australian Taxation Law 2018

Ebook 28E. Melbourne: OUPANZ, 2018. Print.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.