Business Taxation: Trading Profit, Self Employment, VAT Schemes

VerifiedAdded on 2022/12/28

|12

|3510

|32

AI Summary

This document provides insights into business taxation, including trading profit, self employment criteria, and different VAT schemes for various companies. It discusses the importance of taxation, different types of taxes, and their impact on businesses. The document also covers Linda's trading profit, six badges of trade, and capital gain tax liability. It is a valuable resource for students studying business and taxation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business

Taxation

Taxation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

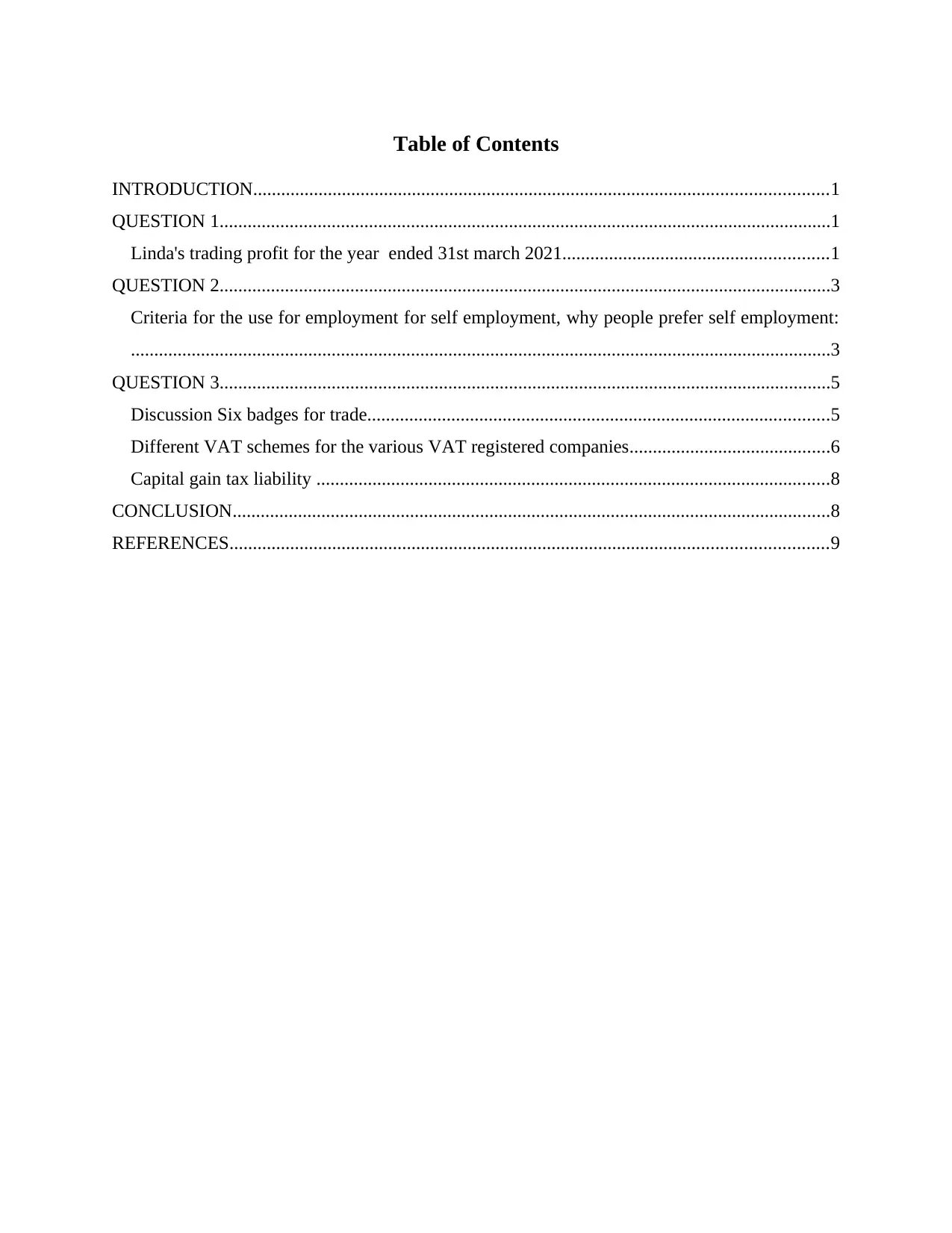

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Linda's trading profit for the year ended 31st march 2021.........................................................1

QUESTION 2...................................................................................................................................3

Criteria for the use for employment for self employment, why people prefer self employment:

......................................................................................................................................................3

QUESTION 3...................................................................................................................................5

Discussion Six badges for trade...................................................................................................5

Different VAT schemes for the various VAT registered companies...........................................6

Capital gain tax liability ..............................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Linda's trading profit for the year ended 31st march 2021.........................................................1

QUESTION 2...................................................................................................................................3

Criteria for the use for employment for self employment, why people prefer self employment:

......................................................................................................................................................3

QUESTION 3...................................................................................................................................5

Discussion Six badges for trade...................................................................................................5

Different VAT schemes for the various VAT registered companies...........................................6

Capital gain tax liability ..............................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Business taxation refers to the tax the business must have to pay when the normal

operations of the business arises. The tax regulations are to be followed by the company in an

proper manner and will not affect the organisation. It is an compulsory payment that every

organisation has to pay so that in future there will no issues arise (Arnold, Ault and Cooper,

2019). The taxation is classified into two parts direct tax and indirect tax. Different types of the

business have to pay different taxes which are charged by the business organisation. There are 5

types of the taxes that the business has to pay that are Gross receipt tax, corporate franchise tax,

employment withholding tax, Excise tax, value added tax. There are some companies which have

to pay the high taxes as they are restricted like the alcohol company. These taxes are collected by

the government and invest in the social programmes and the administration or building up of the

infrastructure in an organisation. There are various industries like mining, insurance they have to

pay the extra taxes as they are using the resources of an environment. The topic cover under this

report are the Linda's trading profit, six badges of trade, VAT schemes, inheritance tax arise and

capital gain tax liability.

QUESTION 1

Linda's trading profit for the year ended 31st march 2021

Trading profit account is equal to the activities from where there is proper earning. These

do not include expenses and the incomes arises from the assets. Trading account is prepared by

the company to identify the loss and the profit that the business is earning and have the growth.

This trading account mostly includes the buying and the selling of the activities so the decision

regarding the business are to be taken in the proper manner and will not affect the organisation. It

is an indicator the business must have to increase the probability so the decisions are to be taken

in an properly in an organisation. These profits are arise from the sales and the purchase of the

securities in an organisation so that the company may now about its position weather the

company is suffering from loss or profit. They help in identifying the risk which is involved in

the business while preparing the accounts. It also helps in accomplishing the objectives of the

business and have the future growth of the organisation. It helps the managers to take the

financial decision and have the growth in an organisation. Trading, income statement, balance

sheet are included in financial statements. The direct expense incurred by the company are

Business taxation refers to the tax the business must have to pay when the normal

operations of the business arises. The tax regulations are to be followed by the company in an

proper manner and will not affect the organisation. It is an compulsory payment that every

organisation has to pay so that in future there will no issues arise (Arnold, Ault and Cooper,

2019). The taxation is classified into two parts direct tax and indirect tax. Different types of the

business have to pay different taxes which are charged by the business organisation. There are 5

types of the taxes that the business has to pay that are Gross receipt tax, corporate franchise tax,

employment withholding tax, Excise tax, value added tax. There are some companies which have

to pay the high taxes as they are restricted like the alcohol company. These taxes are collected by

the government and invest in the social programmes and the administration or building up of the

infrastructure in an organisation. There are various industries like mining, insurance they have to

pay the extra taxes as they are using the resources of an environment. The topic cover under this

report are the Linda's trading profit, six badges of trade, VAT schemes, inheritance tax arise and

capital gain tax liability.

QUESTION 1

Linda's trading profit for the year ended 31st march 2021

Trading profit account is equal to the activities from where there is proper earning. These

do not include expenses and the incomes arises from the assets. Trading account is prepared by

the company to identify the loss and the profit that the business is earning and have the growth.

This trading account mostly includes the buying and the selling of the activities so the decision

regarding the business are to be taken in the proper manner and will not affect the organisation. It

is an indicator the business must have to increase the probability so the decisions are to be taken

in an properly in an organisation. These profits are arise from the sales and the purchase of the

securities in an organisation so that the company may now about its position weather the

company is suffering from loss or profit. They help in identifying the risk which is involved in

the business while preparing the accounts. It also helps in accomplishing the objectives of the

business and have the future growth of the organisation. It helps the managers to take the

financial decision and have the growth in an organisation. Trading, income statement, balance

sheet are included in financial statements. The direct expense incurred by the company are

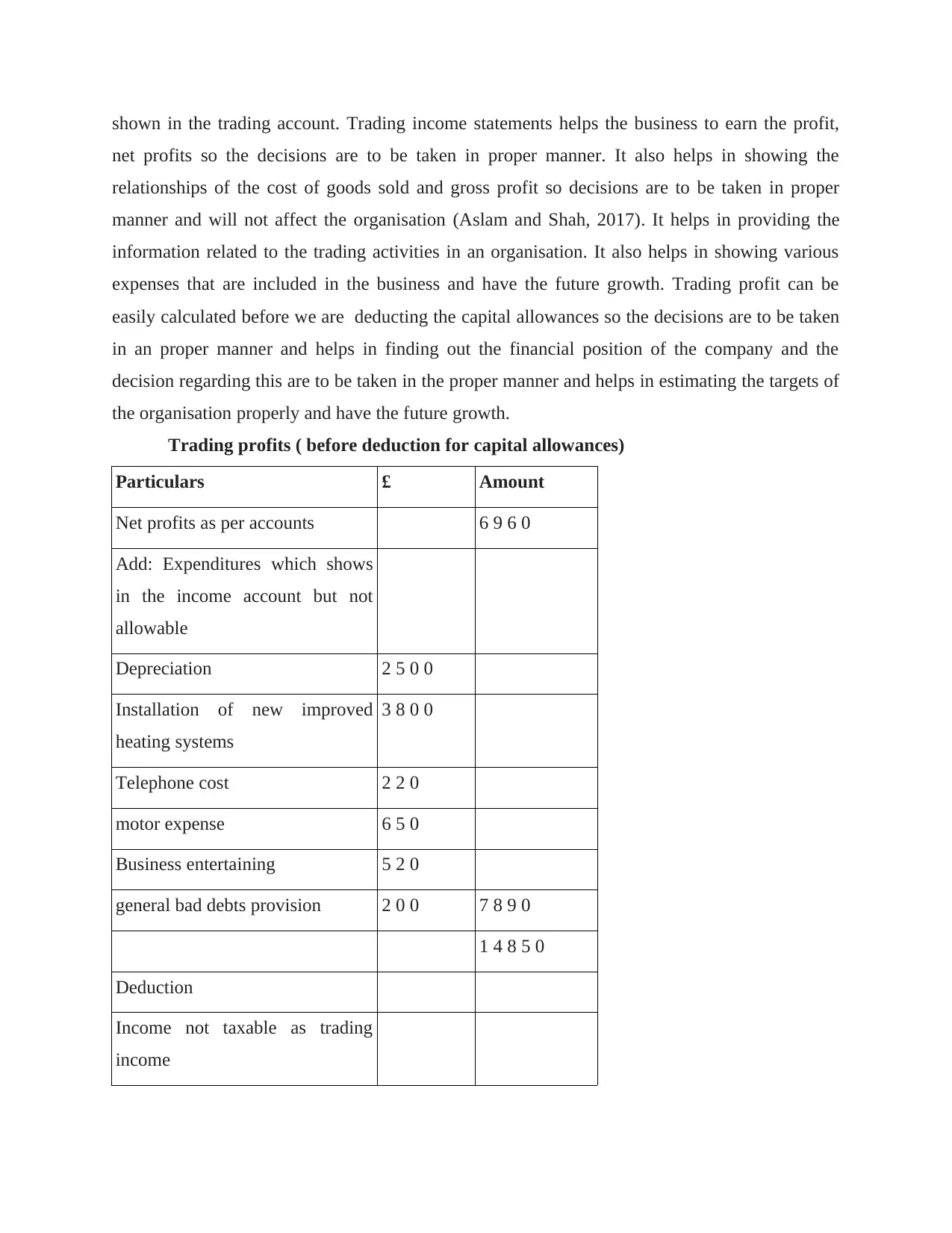

shown in the trading account. Trading income statements helps the business to earn the profit,

net profits so the decisions are to be taken in proper manner. It also helps in showing the

relationships of the cost of goods sold and gross profit so decisions are to be taken in proper

manner and will not affect the organisation (Aslam and Shah, 2017). It helps in providing the

information related to the trading activities in an organisation. It also helps in showing various

expenses that are included in the business and have the future growth. Trading profit can be

easily calculated before we are deducting the capital allowances so the decisions are to be taken

in an proper manner and helps in finding out the financial position of the company and the

decision regarding this are to be taken in the proper manner and helps in estimating the targets of

the organisation properly and have the future growth.

Trading profits ( before deduction for capital allowances)

Particulars £ Amount

Net profits as per accounts.... 6 9 6 0

Add: Expenditures which shows

in the income account but not

allowable

Depreciation 2 5 0 0

Installation of new improved

heating systems

3 8 0 0

Telephone cost 2 2 0

motor expense 6 5 0

Business entertaining 5 2 0

general bad debts provision 2 0 0 7 8 9 0

1 4 8 5 0

Deduction

Income not taxable as trading

income

net profits so the decisions are to be taken in proper manner. It also helps in showing the

relationships of the cost of goods sold and gross profit so decisions are to be taken in proper

manner and will not affect the organisation (Aslam and Shah, 2017). It helps in providing the

information related to the trading activities in an organisation. It also helps in showing various

expenses that are included in the business and have the future growth. Trading profit can be

easily calculated before we are deducting the capital allowances so the decisions are to be taken

in an proper manner and helps in finding out the financial position of the company and the

decision regarding this are to be taken in the proper manner and helps in estimating the targets of

the organisation properly and have the future growth.

Trading profits ( before deduction for capital allowances)

Particulars £ Amount

Net profits as per accounts.... 6 9 6 0

Add: Expenditures which shows

in the income account but not

allowable

Depreciation 2 5 0 0

Installation of new improved

heating systems

3 8 0 0

Telephone cost 2 2 0

motor expense 6 5 0

Business entertaining 5 2 0

general bad debts provision 2 0 0 7 8 9 0

1 4 8 5 0

Deduction

Income not taxable as trading

income

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

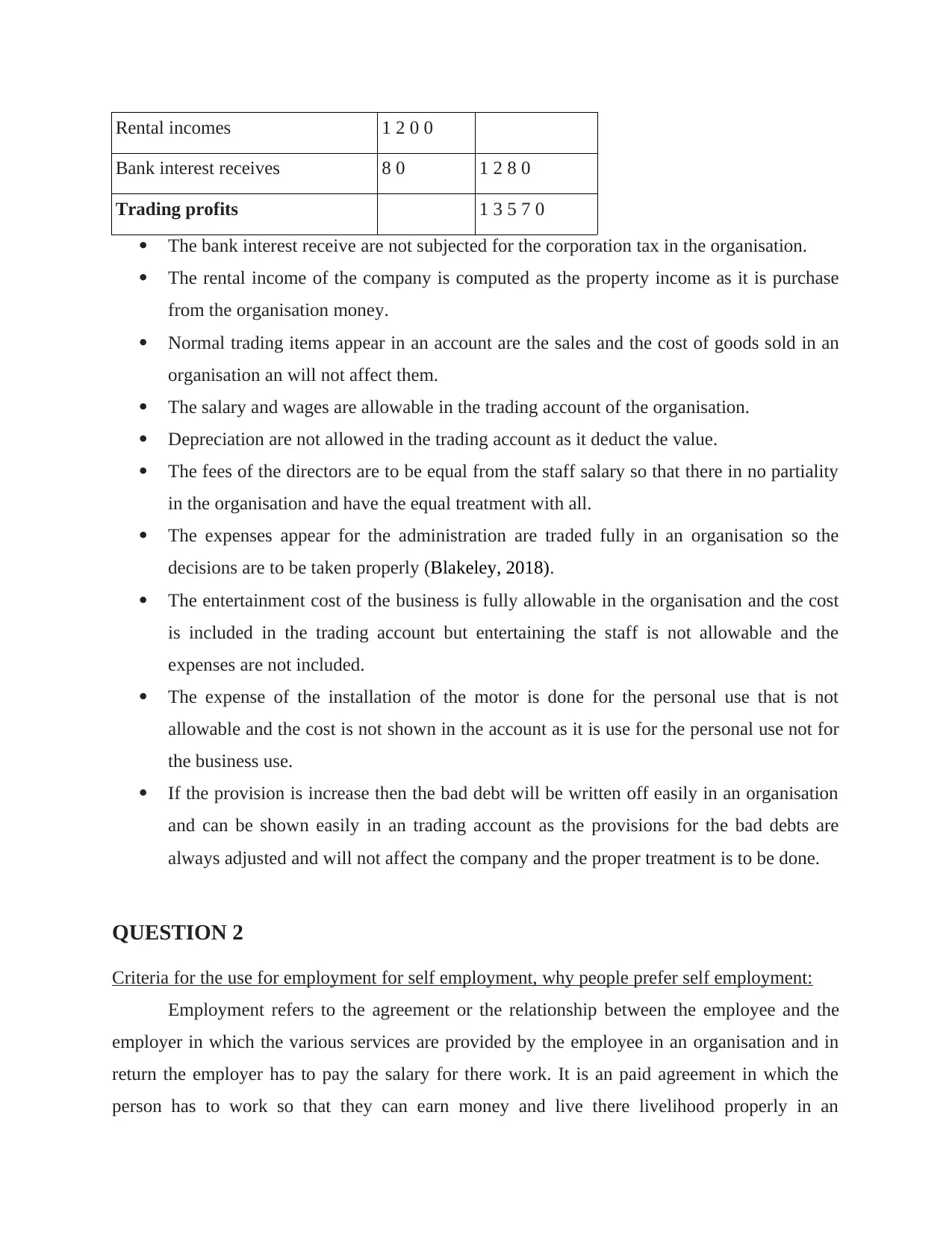

Rental incomes 1 2 0 0

Bank interest receives 8 0 1 2 8 0

Trading profits 1 3 5 7 0

The bank interest receive are not subjected for the corporation tax in the organisation.

The rental income of the company is computed as the property income as it is purchase

from the organisation money.

Normal trading items appear in an account are the sales and the cost of goods sold in an

organisation an will not affect them.

The salary and wages are allowable in the trading account of the organisation.

Depreciation are not allowed in the trading account as it deduct the value.

The fees of the directors are to be equal from the staff salary so that there in no partiality

in the organisation and have the equal treatment with all.

The expenses appear for the administration are traded fully in an organisation so the

decisions are to be taken properly (Blakeley, 2018).

The entertainment cost of the business is fully allowable in the organisation and the cost

is included in the trading account but entertaining the staff is not allowable and the

expenses are not included.

The expense of the installation of the motor is done for the personal use that is not

allowable and the cost is not shown in the account as it is use for the personal use not for

the business use.

If the provision is increase then the bad debt will be written off easily in an organisation

and can be shown easily in an trading account as the provisions for the bad debts are

always adjusted and will not affect the company and the proper treatment is to be done.

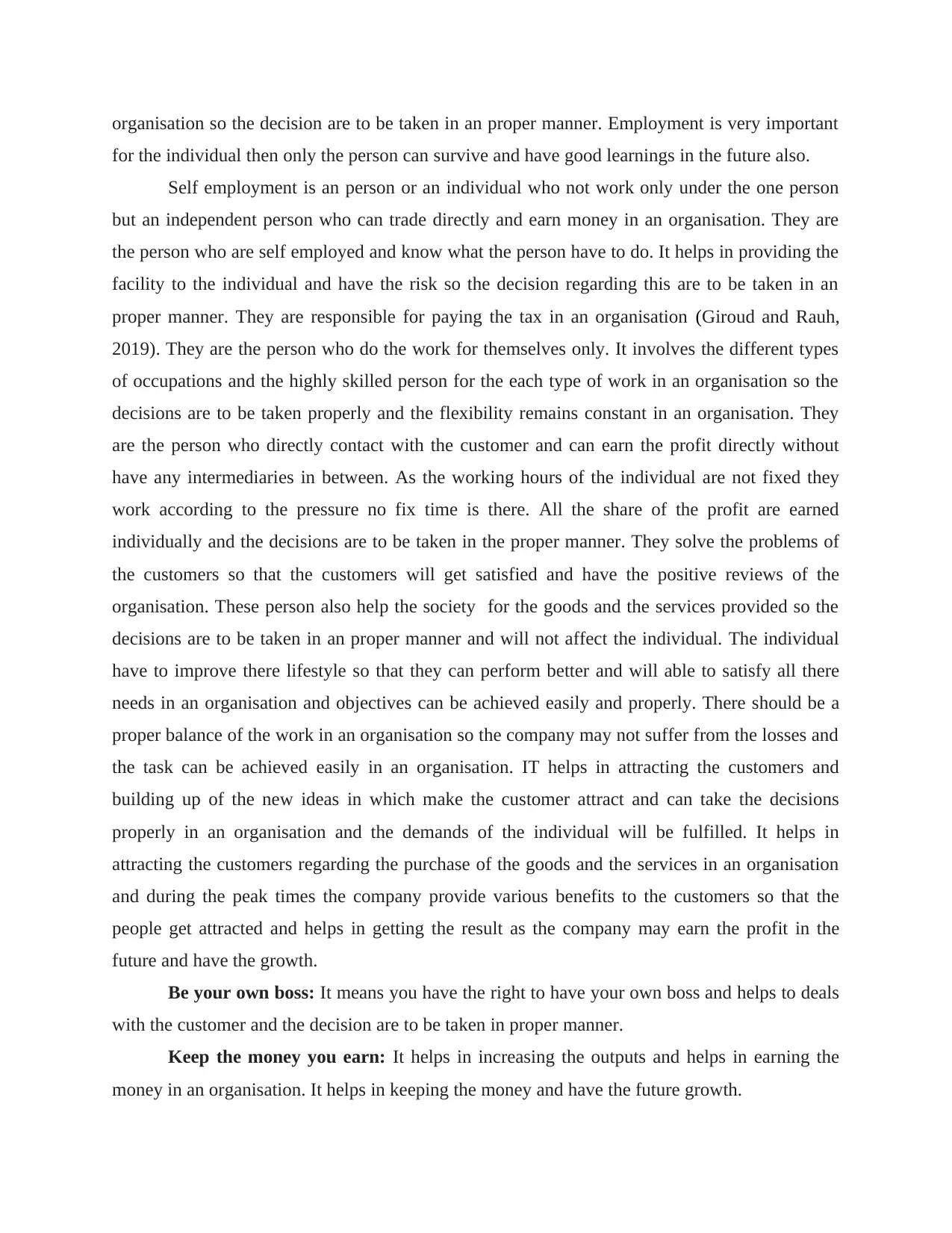

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment refers to the agreement or the relationship between the employee and the

employer in which the various services are provided by the employee in an organisation and in

return the employer has to pay the salary for there work. It is an paid agreement in which the

person has to work so that they can earn money and live there livelihood properly in an

Bank interest receives 8 0 1 2 8 0

Trading profits 1 3 5 7 0

The bank interest receive are not subjected for the corporation tax in the organisation.

The rental income of the company is computed as the property income as it is purchase

from the organisation money.

Normal trading items appear in an account are the sales and the cost of goods sold in an

organisation an will not affect them.

The salary and wages are allowable in the trading account of the organisation.

Depreciation are not allowed in the trading account as it deduct the value.

The fees of the directors are to be equal from the staff salary so that there in no partiality

in the organisation and have the equal treatment with all.

The expenses appear for the administration are traded fully in an organisation so the

decisions are to be taken properly (Blakeley, 2018).

The entertainment cost of the business is fully allowable in the organisation and the cost

is included in the trading account but entertaining the staff is not allowable and the

expenses are not included.

The expense of the installation of the motor is done for the personal use that is not

allowable and the cost is not shown in the account as it is use for the personal use not for

the business use.

If the provision is increase then the bad debt will be written off easily in an organisation

and can be shown easily in an trading account as the provisions for the bad debts are

always adjusted and will not affect the company and the proper treatment is to be done.

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment refers to the agreement or the relationship between the employee and the

employer in which the various services are provided by the employee in an organisation and in

return the employer has to pay the salary for there work. It is an paid agreement in which the

person has to work so that they can earn money and live there livelihood properly in an

organisation so the decision are to be taken in an proper manner. Employment is very important

for the individual then only the person can survive and have good learnings in the future also.

Self employment is an person or an individual who not work only under the one person

but an independent person who can trade directly and earn money in an organisation. They are

the person who are self employed and know what the person have to do. It helps in providing the

facility to the individual and have the risk so the decision regarding this are to be taken in an

proper manner. They are responsible for paying the tax in an organisation (Giroud and Rauh,

2019). They are the person who do the work for themselves only. It involves the different types

of occupations and the highly skilled person for the each type of work in an organisation so the

decisions are to be taken properly and the flexibility remains constant in an organisation. They

are the person who directly contact with the customer and can earn the profit directly without

have any intermediaries in between. As the working hours of the individual are not fixed they

work according to the pressure no fix time is there. All the share of the profit are earned

individually and the decisions are to be taken in the proper manner. They solve the problems of

the customers so that the customers will get satisfied and have the positive reviews of the

organisation. These person also help the society for the goods and the services provided so the

decisions are to be taken in an proper manner and will not affect the individual. The individual

have to improve there lifestyle so that they can perform better and will able to satisfy all there

needs in an organisation and objectives can be achieved easily and properly. There should be a

proper balance of the work in an organisation so the company may not suffer from the losses and

the task can be achieved easily in an organisation. IT helps in attracting the customers and

building up of the new ideas in which make the customer attract and can take the decisions

properly in an organisation and the demands of the individual will be fulfilled. It helps in

attracting the customers regarding the purchase of the goods and the services in an organisation

and during the peak times the company provide various benefits to the customers so that the

people get attracted and helps in getting the result as the company may earn the profit in the

future and have the growth.

Be your own boss: It means you have the right to have your own boss and helps to deals

with the customer and the decision are to be taken in proper manner.

Keep the money you earn: It helps in increasing the outputs and helps in earning the

money in an organisation. It helps in keeping the money and have the future growth.

for the individual then only the person can survive and have good learnings in the future also.

Self employment is an person or an individual who not work only under the one person

but an independent person who can trade directly and earn money in an organisation. They are

the person who are self employed and know what the person have to do. It helps in providing the

facility to the individual and have the risk so the decision regarding this are to be taken in an

proper manner. They are responsible for paying the tax in an organisation (Giroud and Rauh,

2019). They are the person who do the work for themselves only. It involves the different types

of occupations and the highly skilled person for the each type of work in an organisation so the

decisions are to be taken properly and the flexibility remains constant in an organisation. They

are the person who directly contact with the customer and can earn the profit directly without

have any intermediaries in between. As the working hours of the individual are not fixed they

work according to the pressure no fix time is there. All the share of the profit are earned

individually and the decisions are to be taken in the proper manner. They solve the problems of

the customers so that the customers will get satisfied and have the positive reviews of the

organisation. These person also help the society for the goods and the services provided so the

decisions are to be taken in an proper manner and will not affect the individual. The individual

have to improve there lifestyle so that they can perform better and will able to satisfy all there

needs in an organisation and objectives can be achieved easily and properly. There should be a

proper balance of the work in an organisation so the company may not suffer from the losses and

the task can be achieved easily in an organisation. IT helps in attracting the customers and

building up of the new ideas in which make the customer attract and can take the decisions

properly in an organisation and the demands of the individual will be fulfilled. It helps in

attracting the customers regarding the purchase of the goods and the services in an organisation

and during the peak times the company provide various benefits to the customers so that the

people get attracted and helps in getting the result as the company may earn the profit in the

future and have the growth.

Be your own boss: It means you have the right to have your own boss and helps to deals

with the customer and the decision are to be taken in proper manner.

Keep the money you earn: It helps in increasing the outputs and helps in earning the

money in an organisation. It helps in keeping the money and have the future growth.

Self own schedule: The self employ workers have to work in there own way and

according to there own schedule so the decisions are to be taken in an proper manner and will not

affect the organisation and have the future growth.

Enjoy career for creative freedom: They can work with there own as they are creative

enough and the work is to be done in an proper manner and will not affect the organisation so the

decisions regarding this are to be taken care and are not fixed at the one work they can change

the technologies according to the requirement so the decisions are to be taken care in an proper

manner and will not affect the organisation (Isabelle, 2016).

Self employ tax benefits: It helps in deducting the tax from the business and helps in

earning the revenues so the decision are to be taken properly in an organisation.

QUESTION 3

Discussion Six badges for trade

Badges of trade refers to the economic activity so that the money can be run properly by

an organisation. It is a profit motive and helps in earning the profit in the organisation so that

there is proper growth and the results will be achieved . It is utilised by the HMRC for proper

determination of the activity in the organisation. It helps in determining weather the hobby can

be transform into the taxable activity of not so the decisions are to be taken in an proper manner.

These badges includes the transaction. It helps in establishing the criteria and the badges are to

be identified which includes the matter of realisation, frequency of the similar transactions and

the supplement work. There are six badges where the transaction can be rise these are the profit

motive, frequency of number of transaction, nature of assets, modification of the underlying

assets, ownership length and the trade frequencies below are the six badges of trade are

described:

Profit motive: During the trade it is essential for the company that these activities pertain the

motive and helps in increasing the profit in the organisation so the decision are to be taken care

in the proper manner. The intentions in term of the profit is known as trading activities and the

main motive of the organisation is to earn profit only (Kaledin 2019). The quality of purchase

will be large which means that the company is earning the profit in the organisation and it is not

use for the personal use and is used when the investment is done for the businesses so the

decision should be taken carefully in the organisation.

according to there own schedule so the decisions are to be taken in an proper manner and will not

affect the organisation and have the future growth.

Enjoy career for creative freedom: They can work with there own as they are creative

enough and the work is to be done in an proper manner and will not affect the organisation so the

decisions regarding this are to be taken care and are not fixed at the one work they can change

the technologies according to the requirement so the decisions are to be taken care in an proper

manner and will not affect the organisation (Isabelle, 2016).

Self employ tax benefits: It helps in deducting the tax from the business and helps in

earning the revenues so the decision are to be taken properly in an organisation.

QUESTION 3

Discussion Six badges for trade

Badges of trade refers to the economic activity so that the money can be run properly by

an organisation. It is a profit motive and helps in earning the profit in the organisation so that

there is proper growth and the results will be achieved . It is utilised by the HMRC for proper

determination of the activity in the organisation. It helps in determining weather the hobby can

be transform into the taxable activity of not so the decisions are to be taken in an proper manner.

These badges includes the transaction. It helps in establishing the criteria and the badges are to

be identified which includes the matter of realisation, frequency of the similar transactions and

the supplement work. There are six badges where the transaction can be rise these are the profit

motive, frequency of number of transaction, nature of assets, modification of the underlying

assets, ownership length and the trade frequencies below are the six badges of trade are

described:

Profit motive: During the trade it is essential for the company that these activities pertain the

motive and helps in increasing the profit in the organisation so the decision are to be taken care

in the proper manner. The intentions in term of the profit is known as trading activities and the

main motive of the organisation is to earn profit only (Kaledin 2019). The quality of purchase

will be large which means that the company is earning the profit in the organisation and it is not

use for the personal use and is used when the investment is done for the businesses so the

decision should be taken carefully in the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Number of transactions: The transactions that occur in an organisation is in a repetitive

manner and helps in indicating how many times the transactions occur in an organisation and

will be not get affected in an proper manner. In this case study there is an proper study about the

trade and the transaction should be recorded on regular basis. An assets which are include are

related to the subject matter of the trade so the decisions are to be taken properly in organisation.

Nature of assets: The problem arises when the assets are bought as the investment and they have

the ability to increase the income in an organisation, personal assets and the assets they have the

trade of securities (Milanez, 2017). There is a situation where the land was purchased and have

done the investment and also have the permission still no income was generated and later on the

land was sold at low price. As the transaction is removed and has no similar investment and no

profit will arise in the future.

Existence for the similar trading transactions, interests: The case discussed was of CIR vs

FRASER in which the taxpayer shows that the woodcutter the person who has the consignment

for the whiskey for the bonds and can run activities in the business. So that the company may

earn the interest and may also have the future growth in the organisation.

Changes the assets: It is important to have the change of assets and can be marketable easily in

an organisation. The brandy is purchase from the South Africa and tax payers are arguing for the

sale and the investment in the business.

The way the sale makes: The guidance of the HMRC show the transactions which helps in

following the trades which are undisputed in an organisation. There are three unconnected

vessels which together bought the Cargo vessel (Wei, 2019). These vessels are sold for the profit.

These profits are helps in trading so the decisions are to be taken in an proper manner.

Source of finance: There are the various source of finance in an organisation where the trade

arises and carried out the businesses in an proper manner and will not affect organisation so the

decisions are to be taken properly.

Interval times for the purchase, sales: The highest indicator of the trade is the length of the

assets as they have the higher ownership in an organisation and the decisions are to be taken in

the timely manner.

Different VAT schemes for the various VAT registered companies

Value added tax is the consumption tax for the product where the values are added for

each supply and the sales of the customers so the decisions are to be taken in an proper manner

manner and helps in indicating how many times the transactions occur in an organisation and

will be not get affected in an proper manner. In this case study there is an proper study about the

trade and the transaction should be recorded on regular basis. An assets which are include are

related to the subject matter of the trade so the decisions are to be taken properly in organisation.

Nature of assets: The problem arises when the assets are bought as the investment and they have

the ability to increase the income in an organisation, personal assets and the assets they have the

trade of securities (Milanez, 2017). There is a situation where the land was purchased and have

done the investment and also have the permission still no income was generated and later on the

land was sold at low price. As the transaction is removed and has no similar investment and no

profit will arise in the future.

Existence for the similar trading transactions, interests: The case discussed was of CIR vs

FRASER in which the taxpayer shows that the woodcutter the person who has the consignment

for the whiskey for the bonds and can run activities in the business. So that the company may

earn the interest and may also have the future growth in the organisation.

Changes the assets: It is important to have the change of assets and can be marketable easily in

an organisation. The brandy is purchase from the South Africa and tax payers are arguing for the

sale and the investment in the business.

The way the sale makes: The guidance of the HMRC show the transactions which helps in

following the trades which are undisputed in an organisation. There are three unconnected

vessels which together bought the Cargo vessel (Wei, 2019). These vessels are sold for the profit.

These profits are helps in trading so the decisions are to be taken in an proper manner.

Source of finance: There are the various source of finance in an organisation where the trade

arises and carried out the businesses in an proper manner and will not affect organisation so the

decisions are to be taken properly.

Interval times for the purchase, sales: The highest indicator of the trade is the length of the

assets as they have the higher ownership in an organisation and the decisions are to be taken in

the timely manner.

Different VAT schemes for the various VAT registered companies

Value added tax is the consumption tax for the product where the values are added for

each supply and the sales of the customers so the decisions are to be taken in an proper manner

and will not affect the organisation. In the customers have to pay the tax for its products and the

material use as they have already tax included in it. The additional tax in an organisation helps in

achieving the objectives. The tax are paid by the individual according to the place and the

product. The various taxes are used which helps in earning the revenue in an organisation. There

are the various methods which helps in calculating the VAT includes the account based method

and the credit invoice (Nechaev and Antipina, 2016). The method used in Japan is the Flat tax

which helps in performing different proposals for the politician of US. Accrual basis accounting

helps in tracking the payable and the receivables in the organisation. It helps matching the

revenue and expenses and have the higher profitability.

VAT Annual Accounting Schemes: These scheme are for the HMRC and have the VAT

returns. The return for the small business become easier and the advance payments of the

company are based on the previous returns.

VAT Cash Accounting Schemes: The scheme regarding the sales of the customers

where the stock can be reclaim and will be pays to the suppliers so the decisions are to be taken

in proper manner.

Capital goods schemes: The goods of the business is the Claim done for the assets

which includes the land, property and the resale of goods and the assets. This helps the business

to have the value added tax for the assets.

VAT retail schemes: The schemes which are for the resale purpose and have the more

annual turnover of an organisation (Wasylenko, 2019). It helps the business to have the initial

value added tax for the assets.

Direct Calculation Scheme: There are the large amount of sales in the business and have

the various calculations so the decisions are to be taken in an proper manner and will not affect

the organisation and help in deriving the results.

Inheritance tax arising when the death

Particulars £ Amount

Value transfers 4 2 0 0 0 0

Marriage exemptions 5 0 0 0

Annual exemption

material use as they have already tax included in it. The additional tax in an organisation helps in

achieving the objectives. The tax are paid by the individual according to the place and the

product. The various taxes are used which helps in earning the revenue in an organisation. There

are the various methods which helps in calculating the VAT includes the account based method

and the credit invoice (Nechaev and Antipina, 2016). The method used in Japan is the Flat tax

which helps in performing different proposals for the politician of US. Accrual basis accounting

helps in tracking the payable and the receivables in the organisation. It helps matching the

revenue and expenses and have the higher profitability.

VAT Annual Accounting Schemes: These scheme are for the HMRC and have the VAT

returns. The return for the small business become easier and the advance payments of the

company are based on the previous returns.

VAT Cash Accounting Schemes: The scheme regarding the sales of the customers

where the stock can be reclaim and will be pays to the suppliers so the decisions are to be taken

in proper manner.

Capital goods schemes: The goods of the business is the Claim done for the assets

which includes the land, property and the resale of goods and the assets. This helps the business

to have the value added tax for the assets.

VAT retail schemes: The schemes which are for the resale purpose and have the more

annual turnover of an organisation (Wasylenko, 2019). It helps the business to have the initial

value added tax for the assets.

Direct Calculation Scheme: There are the large amount of sales in the business and have

the various calculations so the decisions are to be taken in an proper manner and will not affect

the organisation and help in deriving the results.

Inheritance tax arising when the death

Particulars £ Amount

Value transfers 4 2 0 0 0 0

Marriage exemptions 5 0 0 0

Annual exemption

2013-14 1 4 0 0 0

2014-15 1 4 0 0 0 3 3 0 0 0

Potential exempt transfer 3 8 7 0 0 0

IHT liabilities 325000 at nil% 0

At 40% 1 5 4 8 0 0

Taper reliefs deduction 60% 9 2 8 8 0 6 1 9 2 0

Death estates

Value for an estate 8 8 0 0 0 0

Spouse exemption (880000/2 ) 4 4 0 0 0 0

Chargeables estate 4 4 0 0 0 0

IHT liability 440000 at 40% 1 7 6 0 0 0

Capital gain tax liability

Particulars £ Amount

Net sales proceeds after the

costs for disposal

4 9 6 4 0 0

Costs for the new boundaries

cots

5 2 0 0

Costs for replacing the

property 2800

2 8 0 0Incentives[edit]

The main reason that VAT has

been successfull

8 0 0 0

4 8 8 4 0 0

Taxable income 1 3 5 9 0

4 7 4 8 1 0

2014-15 1 4 0 0 0 3 3 0 0 0

Potential exempt transfer 3 8 7 0 0 0

IHT liabilities 325000 at nil% 0

At 40% 1 5 4 8 0 0

Taper reliefs deduction 60% 9 2 8 8 0 6 1 9 2 0

Death estates

Value for an estate 8 8 0 0 0 0

Spouse exemption (880000/2 ) 4 4 0 0 0 0

Chargeables estate 4 4 0 0 0 0

IHT liability 440000 at 40% 1 7 6 0 0 0

Capital gain tax liability

Particulars £ Amount

Net sales proceeds after the

costs for disposal

4 9 6 4 0 0

Costs for the new boundaries

cots

5 2 0 0

Costs for replacing the

property 2800

2 8 0 0Incentives[edit]

The main reason that VAT has

been successfull

8 0 0 0

4 8 8 4 0 0

Taxable income 1 3 5 9 0

4 7 4 8 1 0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Tax 28% for property 1 3 2 9 4 6 . 8 1 3 2 9 4 6 . 8

CONCLUSION

From the above report it has been concluded that the business tax refers to the process in

which the company has to pay the tax related to the transaction in the business. These taxes are

paid by the company as per the government rules. In this report the trading profits are equal to

the earnings and not include the finance related incomes. Badges are utilized by the HMRC

which helps in determining the economic activity of an organisation and will have an hobby of

the person. It is a process in which the customer has to pay the tax which includes the goods and

services in organisation.

CONCLUSION

From the above report it has been concluded that the business tax refers to the process in

which the company has to pay the tax related to the transaction in the business. These taxes are

paid by the company as per the government rules. In this report the trading profits are equal to

the earnings and not include the finance related incomes. Badges are utilized by the HMRC

which helps in determining the economic activity of an organisation and will have an hobby of

the person. It is a process in which the customer has to pay the tax which includes the goods and

services in organisation.

REFERENCES

Books & Journals

Arnold, B. J., Ault, H. J. and Cooper, G. eds., 2019. Comparative income taxation: a structural

analysis. Kluwer Law International BV.

Aslam, A. and Shah, M. A., 2017. Taxation and the peer-to-peer economy. International

Monetary Fund.

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

Giroud, X. and Rauh, J., 2019. State taxation and the reallocation of business activity: Evidence

from establishment-level data. Journal of Political Economy. 127(3), pp.1262-1316.

Isabelle, R., 2016. State aid law and business taxation. Springer.

Kaledin, S.V. and et. al., 2019, January. Usage of Indicators of the Small Business Taxation in

USA and Modern Russia. In International Scientific Conference" Far East

Con"(ISCFEC 2018) (pp. 319-326). Atlantis Press.

Milanez, A., 2017. Legal tax liability, legal remittance responsibility and tax incidence: Three

dimensions of business taxation.

Nechaev, A. and Antipina, O., 2016. Analysis of the Impact of Taxation of Business Entities on

the Innovative Development of the Country.

Wasylenko, M., 2019. Taxation and economic development: The state of the economic

literature. In Handbook on Taxation(pp. 309-327). Taylor and Francis.

Wei, F., 2019. July. Three Essays on Business Taxation. Arts.

Books & Journals

Arnold, B. J., Ault, H. J. and Cooper, G. eds., 2019. Comparative income taxation: a structural

analysis. Kluwer Law International BV.

Aslam, A. and Shah, M. A., 2017. Taxation and the peer-to-peer economy. International

Monetary Fund.

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

Giroud, X. and Rauh, J., 2019. State taxation and the reallocation of business activity: Evidence

from establishment-level data. Journal of Political Economy. 127(3), pp.1262-1316.

Isabelle, R., 2016. State aid law and business taxation. Springer.

Kaledin, S.V. and et. al., 2019, January. Usage of Indicators of the Small Business Taxation in

USA and Modern Russia. In International Scientific Conference" Far East

Con"(ISCFEC 2018) (pp. 319-326). Atlantis Press.

Milanez, A., 2017. Legal tax liability, legal remittance responsibility and tax incidence: Three

dimensions of business taxation.

Nechaev, A. and Antipina, O., 2016. Analysis of the Impact of Taxation of Business Entities on

the Innovative Development of the Country.

Wasylenko, M., 2019. Taxation and economic development: The state of the economic

literature. In Handbook on Taxation(pp. 309-327). Taylor and Francis.

Wei, F., 2019. July. Three Essays on Business Taxation. Arts.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.