Business Valuation and Analysis

VerifiedAdded on 2023/03/21

|15

|2676

|60

AI Summary

Valuation of a company is a very complex task that requires substantial knowledge in the field of accounting. There are number of valuation techniques that are available to determine the value of a company. In case of acquisition of target companies as well as selling of a company the management uses the services of the experts to determine the value of these companies. It helps management to either acquire a target company at correct value or to get correct price for selling a company’s share. As mentioned that there are number of different valuation techniques which are used by management to ascertain the value of a company however, the discounted cash flow method and price earnings ratio method are two of the most popular methods used to ascertain value of a company. Valuation of ABC Company using these two methods show that there is significant difference in the values calculated between discounted cash flow method and price earning method.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS VALUATION AND ANALYSIS

Business Valuation and Analysis

Name of the Student:

Name of the University:

Authors Note:

Business Valuation and Analysis

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

BUSINESS VALUATION AND ANALYSIS

Executive summary:

Valuation of a company is a very complex task that requires substantial knowledge in the

field of accounting. There are number of valuation techniques that are available to determine the

value of a company. In case of acquisition of target companies as well as selling of a company

the management uses the services of the experts to determine the value of these companies. It

helps management to either acquire a target company at correct value or to get correct price for

selling a company’s share. As mentioned that there are number of different valuation techniques

which are used by management to ascertain the value of a company however, the discounted

cash flow method and price earnings ratio method are two of the most popular methods used to

ascertain value of a company. Valuation of ABC Company using these two methods show that

there is significant difference in the values calculated between discounted cash flow method and

price earning method.

BUSINESS VALUATION AND ANALYSIS

Executive summary:

Valuation of a company is a very complex task that requires substantial knowledge in the

field of accounting. There are number of valuation techniques that are available to determine the

value of a company. In case of acquisition of target companies as well as selling of a company

the management uses the services of the experts to determine the value of these companies. It

helps management to either acquire a target company at correct value or to get correct price for

selling a company’s share. As mentioned that there are number of different valuation techniques

which are used by management to ascertain the value of a company however, the discounted

cash flow method and price earnings ratio method are two of the most popular methods used to

ascertain value of a company. Valuation of ABC Company using these two methods show that

there is significant difference in the values calculated between discounted cash flow method and

price earning method.

2

BUSINESS VALUATION AND ANALYSIS

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Discounted cash flow method:.........................................................................................................3

Price earnings ratio model:..............................................................................................................7

Net asset method:...........................................................................................................................10

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

BUSINESS VALUATION AND ANALYSIS

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Discounted cash flow method:.........................................................................................................3

Price earnings ratio model:..............................................................................................................7

Net asset method:...........................................................................................................................10

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

3

BUSINESS VALUATION AND ANALYSIS

Introduction:

In discounted cash flow method the expected cash flows of a company in the future is

calculated and discounted by using appropriate discounting rate, i.e. generally the cost of capital

of the company. In price earnings ratio method the earnings per share of a company is calculated

for the latest ending financial year which is then multiplied by the PE ratio to get the market

value of each share. Once the market value of a share is calculated it would be easier to calculate

the value of the whole company, i.e. by multiplying the market value of each share with the

number of shares outstanding as on the last date of the latest ending financial year. Valuation of

ABC Limited using two alternative valuation techniques will show the difference in valuation of

the company due to the difference in valuation techniques (Cifuentes, 2016).

Discounted cash flow method:

As mentioned at the beginning of this document that there are number of valuation techniques

and method that are in use to calculate the value of a company however, only few techniques

have been universally accepted as effective techniques to ascertain proper value of a company.

Discounted cash flow method is one of the techniques which is accepted as an effective method

to value a company ("Discounted Cash Flow Method for Valuing International Chemical

Distributors", 2018).

However, it is important to understand how the valuation technique is used to calculate the value

of a company properly. There are number of assumptions which have to be made to ascertain the

value of a company using the discounted cash flow method. In case of ABC Limited firstly, it is

important to forecast the expected future cash flows to the company. In the document the

BUSINESS VALUATION AND ANALYSIS

Introduction:

In discounted cash flow method the expected cash flows of a company in the future is

calculated and discounted by using appropriate discounting rate, i.e. generally the cost of capital

of the company. In price earnings ratio method the earnings per share of a company is calculated

for the latest ending financial year which is then multiplied by the PE ratio to get the market

value of each share. Once the market value of a share is calculated it would be easier to calculate

the value of the whole company, i.e. by multiplying the market value of each share with the

number of shares outstanding as on the last date of the latest ending financial year. Valuation of

ABC Limited using two alternative valuation techniques will show the difference in valuation of

the company due to the difference in valuation techniques (Cifuentes, 2016).

Discounted cash flow method:

As mentioned at the beginning of this document that there are number of valuation techniques

and method that are in use to calculate the value of a company however, only few techniques

have been universally accepted as effective techniques to ascertain proper value of a company.

Discounted cash flow method is one of the techniques which is accepted as an effective method

to value a company ("Discounted Cash Flow Method for Valuing International Chemical

Distributors", 2018).

However, it is important to understand how the valuation technique is used to calculate the value

of a company properly. There are number of assumptions which have to be made to ascertain the

value of a company using the discounted cash flow method. In case of ABC Limited firstly, it is

important to forecast the expected future cash flows to the company. In the document the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

BUSINESS VALUATION AND ANALYSIS

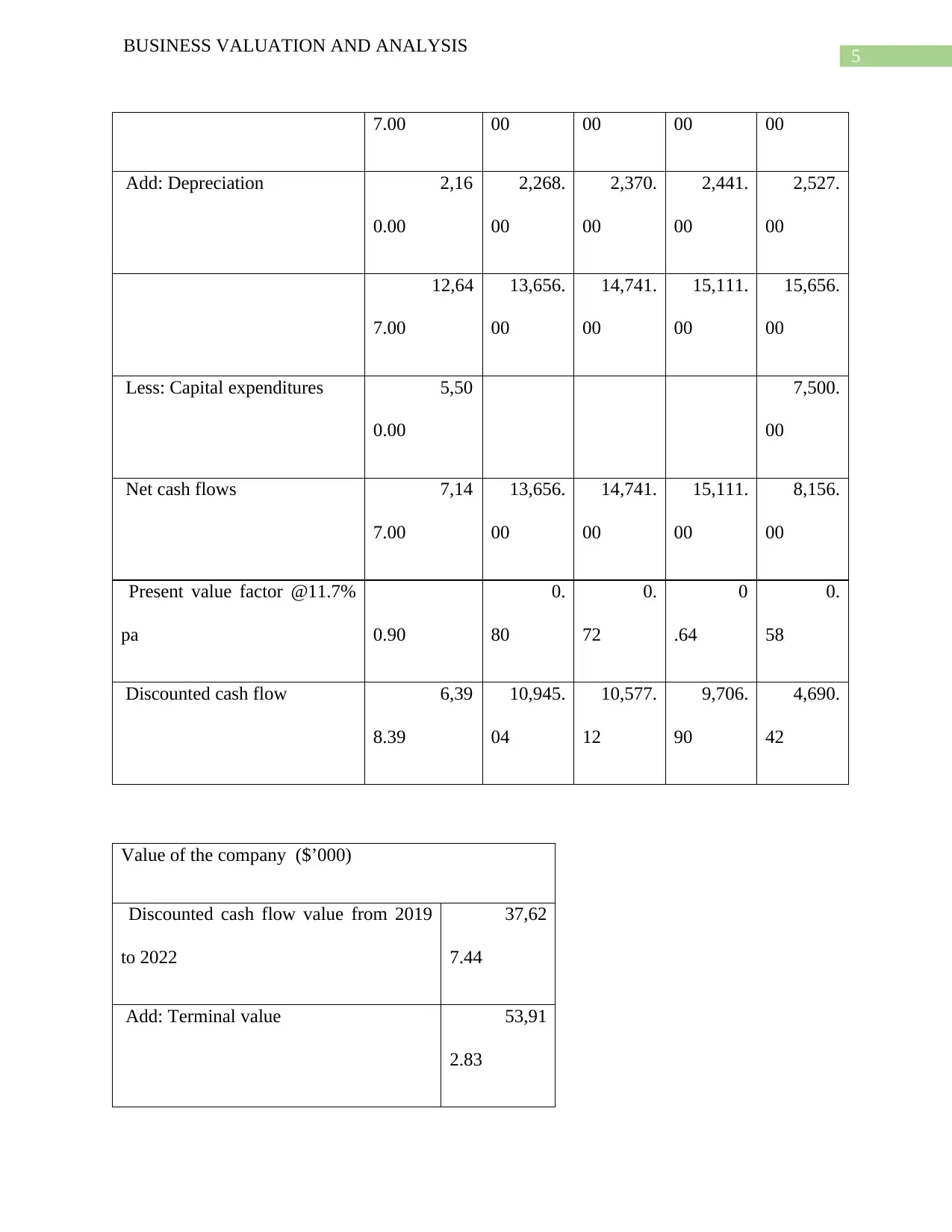

management has already forecasted the expected net profit after tax for the next five years i.e.

from 2019 to 2023. It has been mentioned that the company is expected incur certain capital

expenditure in the future, i.e. $5.5 million in 2019 and $7.5 million in 2023. These have been

considered in calculating the expected future cash flows to the company. Firstly, Net profit

before tax has been increased by adding the depreciation as it is a non-cash item. Then the

adjusted profit for 2019 and 2013 has been reduced by deducting the expected capital

expenditures of $5.5 million and $7.5 million respectively. The discounting factor is not given

hence, the cost of capital has been calculated by using capital asset pricing model (CAPM).

CAPM follows the following formula to calculate the cost of capital (Fernandez, 2013).

Cost of capital = Risk free rate of return + beta x market risk premium.

Accordingly, the cost of capital of ABC Limited has been calculated to discount the expected

future cash inflows of the company. It has been estimated that the company will grow at 3% in

the long run thus, using this as a growth rate the terminal value of the company has been

calculated. The detailed calculation is provided below to show the value of ABC Limited as per

the discounted cash flow method (Ghaeli, 2017).

Valuation of the company:

Discounted cash flow methods

Years (All amounts are in

$000)

2019 2020 2021 2022 2023

Net profit after tax 10,48 11,388. 12,371. 12,670. 13,129.

BUSINESS VALUATION AND ANALYSIS

management has already forecasted the expected net profit after tax for the next five years i.e.

from 2019 to 2023. It has been mentioned that the company is expected incur certain capital

expenditure in the future, i.e. $5.5 million in 2019 and $7.5 million in 2023. These have been

considered in calculating the expected future cash flows to the company. Firstly, Net profit

before tax has been increased by adding the depreciation as it is a non-cash item. Then the

adjusted profit for 2019 and 2013 has been reduced by deducting the expected capital

expenditures of $5.5 million and $7.5 million respectively. The discounting factor is not given

hence, the cost of capital has been calculated by using capital asset pricing model (CAPM).

CAPM follows the following formula to calculate the cost of capital (Fernandez, 2013).

Cost of capital = Risk free rate of return + beta x market risk premium.

Accordingly, the cost of capital of ABC Limited has been calculated to discount the expected

future cash inflows of the company. It has been estimated that the company will grow at 3% in

the long run thus, using this as a growth rate the terminal value of the company has been

calculated. The detailed calculation is provided below to show the value of ABC Limited as per

the discounted cash flow method (Ghaeli, 2017).

Valuation of the company:

Discounted cash flow methods

Years (All amounts are in

$000)

2019 2020 2021 2022 2023

Net profit after tax 10,48 11,388. 12,371. 12,670. 13,129.

5

BUSINESS VALUATION AND ANALYSIS

7.00 00 00 00 00

Add: Depreciation 2,16

0.00

2,268.

00

2,370.

00

2,441.

00

2,527.

00

12,64

7.00

13,656.

00

14,741.

00

15,111.

00

15,656.

00

Less: Capital expenditures 5,50

0.00

7,500.

00

Net cash flows 7,14

7.00

13,656.

00

14,741.

00

15,111.

00

8,156.

00

Present value factor @11.7%

pa 0.90

0.

80

0.

72

0

.64

0.

58

Discounted cash flow 6,39

8.39

10,945.

04

10,577.

12

9,706.

90

4,690.

42

Value of the company ($’000)

Discounted cash flow value from 2019

to 2022

37,62

7.44

Add: Terminal value 53,91

2.83

BUSINESS VALUATION AND ANALYSIS

7.00 00 00 00 00

Add: Depreciation 2,16

0.00

2,268.

00

2,370.

00

2,441.

00

2,527.

00

12,64

7.00

13,656.

00

14,741.

00

15,111.

00

15,656.

00

Less: Capital expenditures 5,50

0.00

7,500.

00

Net cash flows 7,14

7.00

13,656.

00

14,741.

00

15,111.

00

8,156.

00

Present value factor @11.7%

pa 0.90

0.

80

0.

72

0

.64

0.

58

Discounted cash flow 6,39

8.39

10,945.

04

10,577.

12

9,706.

90

4,690.

42

Value of the company ($’000)

Discounted cash flow value from 2019

to 2022

37,62

7.44

Add: Terminal value 53,91

2.83

6

BUSINESS VALUATION AND ANALYSIS

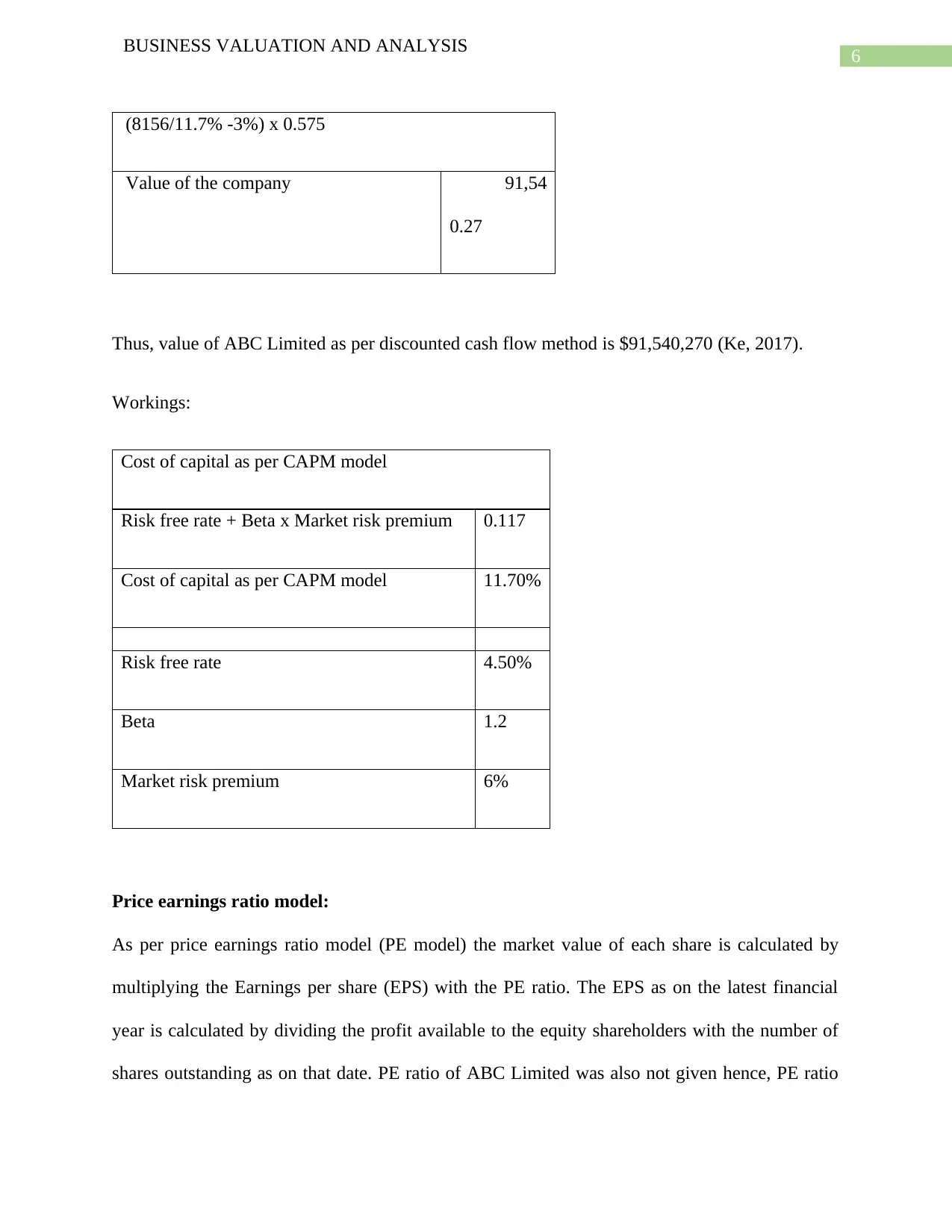

(8156/11.7% -3%) x 0.575

Value of the company 91,54

0.27

Thus, value of ABC Limited as per discounted cash flow method is $91,540,270 (Ke, 2017).

Workings:

Cost of capital as per CAPM model

Risk free rate + Beta x Market risk premium 0.117

Cost of capital as per CAPM model 11.70%

Risk free rate 4.50%

Beta 1.2

Market risk premium 6%

Price earnings ratio model:

As per price earnings ratio model (PE model) the market value of each share is calculated by

multiplying the Earnings per share (EPS) with the PE ratio. The EPS as on the latest financial

year is calculated by dividing the profit available to the equity shareholders with the number of

shares outstanding as on that date. PE ratio of ABC Limited was also not given hence, PE ratio

BUSINESS VALUATION AND ANALYSIS

(8156/11.7% -3%) x 0.575

Value of the company 91,54

0.27

Thus, value of ABC Limited as per discounted cash flow method is $91,540,270 (Ke, 2017).

Workings:

Cost of capital as per CAPM model

Risk free rate + Beta x Market risk premium 0.117

Cost of capital as per CAPM model 11.70%

Risk free rate 4.50%

Beta 1.2

Market risk premium 6%

Price earnings ratio model:

As per price earnings ratio model (PE model) the market value of each share is calculated by

multiplying the Earnings per share (EPS) with the PE ratio. The EPS as on the latest financial

year is calculated by dividing the profit available to the equity shareholders with the number of

shares outstanding as on that date. PE ratio of ABC Limited was also not given hence, PE ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BUSINESS VALUATION AND ANALYSIS

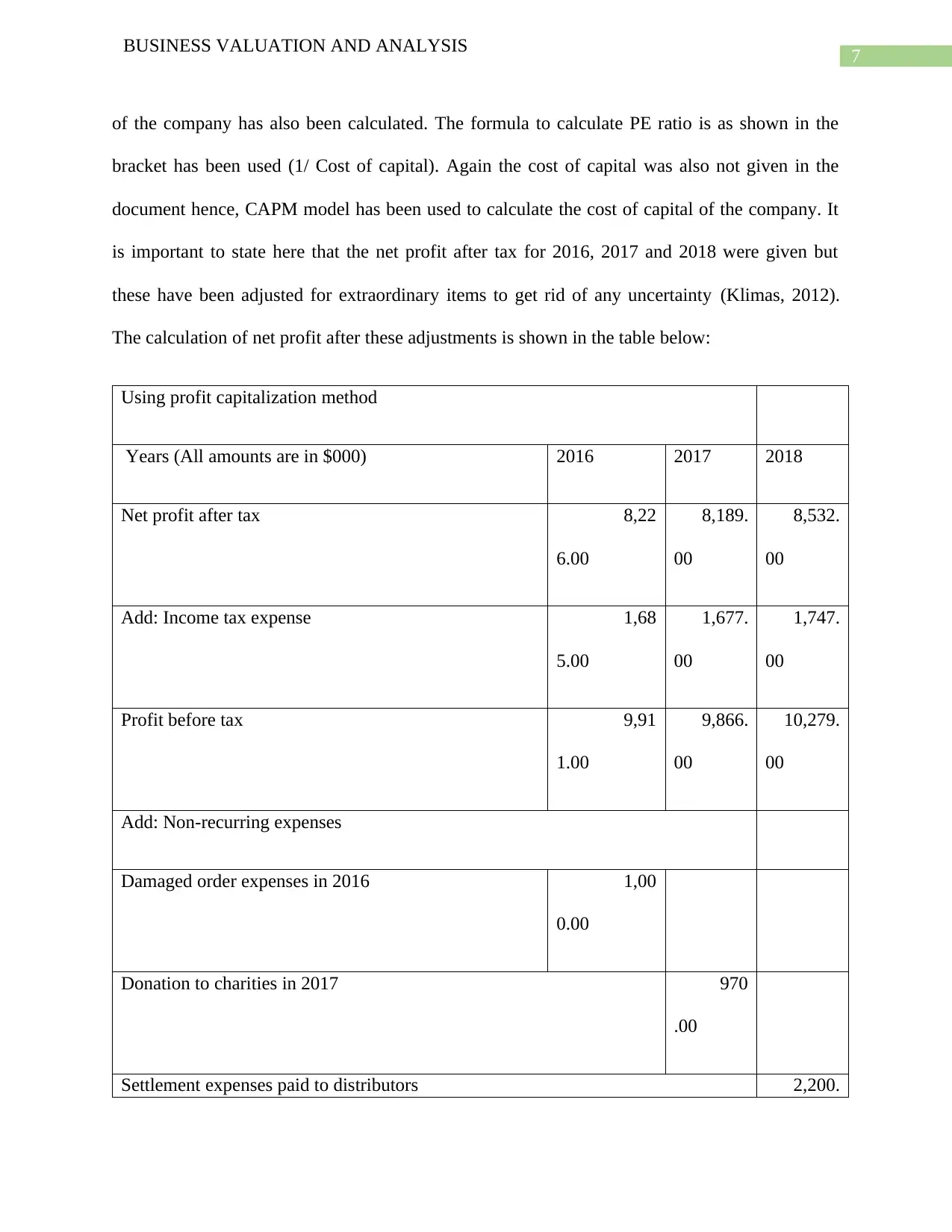

of the company has also been calculated. The formula to calculate PE ratio is as shown in the

bracket has been used (1/ Cost of capital). Again the cost of capital was also not given in the

document hence, CAPM model has been used to calculate the cost of capital of the company. It

is important to state here that the net profit after tax for 2016, 2017 and 2018 were given but

these have been adjusted for extraordinary items to get rid of any uncertainty (Klimas, 2012).

The calculation of net profit after these adjustments is shown in the table below:

Using profit capitalization method

Years (All amounts are in $000) 2016 2017 2018

Net profit after tax 8,22

6.00

8,189.

00

8,532.

00

Add: Income tax expense 1,68

5.00

1,677.

00

1,747.

00

Profit before tax 9,91

1.00

9,866.

00

10,279.

00

Add: Non-recurring expenses

Damaged order expenses in 2016 1,00

0.00

Donation to charities in 2017 970

.00

Settlement expenses paid to distributors 2,200.

BUSINESS VALUATION AND ANALYSIS

of the company has also been calculated. The formula to calculate PE ratio is as shown in the

bracket has been used (1/ Cost of capital). Again the cost of capital was also not given in the

document hence, CAPM model has been used to calculate the cost of capital of the company. It

is important to state here that the net profit after tax for 2016, 2017 and 2018 were given but

these have been adjusted for extraordinary items to get rid of any uncertainty (Klimas, 2012).

The calculation of net profit after these adjustments is shown in the table below:

Using profit capitalization method

Years (All amounts are in $000) 2016 2017 2018

Net profit after tax 8,22

6.00

8,189.

00

8,532.

00

Add: Income tax expense 1,68

5.00

1,677.

00

1,747.

00

Profit before tax 9,91

1.00

9,866.

00

10,279.

00

Add: Non-recurring expenses

Damaged order expenses in 2016 1,00

0.00

Donation to charities in 2017 970

.00

Settlement expenses paid to distributors 2,200.

8

BUSINESS VALUATION AND ANALYSIS

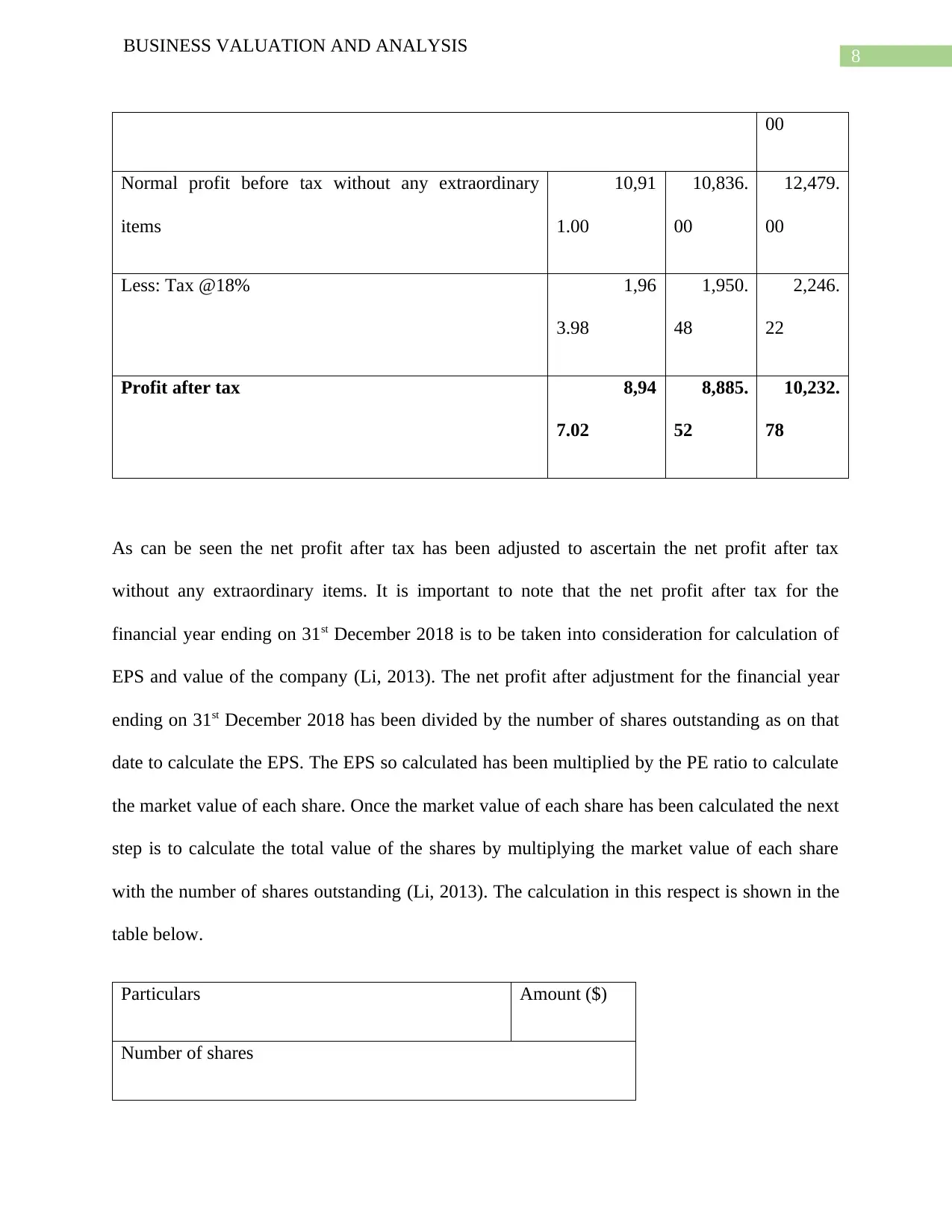

00

Normal profit before tax without any extraordinary

items

10,91

1.00

10,836.

00

12,479.

00

Less: Tax @18% 1,96

3.98

1,950.

48

2,246.

22

Profit after tax 8,94

7.02

8,885.

52

10,232.

78

As can be seen the net profit after tax has been adjusted to ascertain the net profit after tax

without any extraordinary items. It is important to note that the net profit after tax for the

financial year ending on 31st December 2018 is to be taken into consideration for calculation of

EPS and value of the company (Li, 2013). The net profit after adjustment for the financial year

ending on 31st December 2018 has been divided by the number of shares outstanding as on that

date to calculate the EPS. The EPS so calculated has been multiplied by the PE ratio to calculate

the market value of each share. Once the market value of each share has been calculated the next

step is to calculate the total value of the shares by multiplying the market value of each share

with the number of shares outstanding (Li, 2013). The calculation in this respect is shown in the

table below.

Particulars Amount ($)

Number of shares

BUSINESS VALUATION AND ANALYSIS

00

Normal profit before tax without any extraordinary

items

10,91

1.00

10,836.

00

12,479.

00

Less: Tax @18% 1,96

3.98

1,950.

48

2,246.

22

Profit after tax 8,94

7.02

8,885.

52

10,232.

78

As can be seen the net profit after tax has been adjusted to ascertain the net profit after tax

without any extraordinary items. It is important to note that the net profit after tax for the

financial year ending on 31st December 2018 is to be taken into consideration for calculation of

EPS and value of the company (Li, 2013). The net profit after adjustment for the financial year

ending on 31st December 2018 has been divided by the number of shares outstanding as on that

date to calculate the EPS. The EPS so calculated has been multiplied by the PE ratio to calculate

the market value of each share. Once the market value of each share has been calculated the next

step is to calculate the total value of the shares by multiplying the market value of each share

with the number of shares outstanding (Li, 2013). The calculation in this respect is shown in the

table below.

Particulars Amount ($)

Number of shares

9

BUSINESS VALUATION AND ANALYSIS

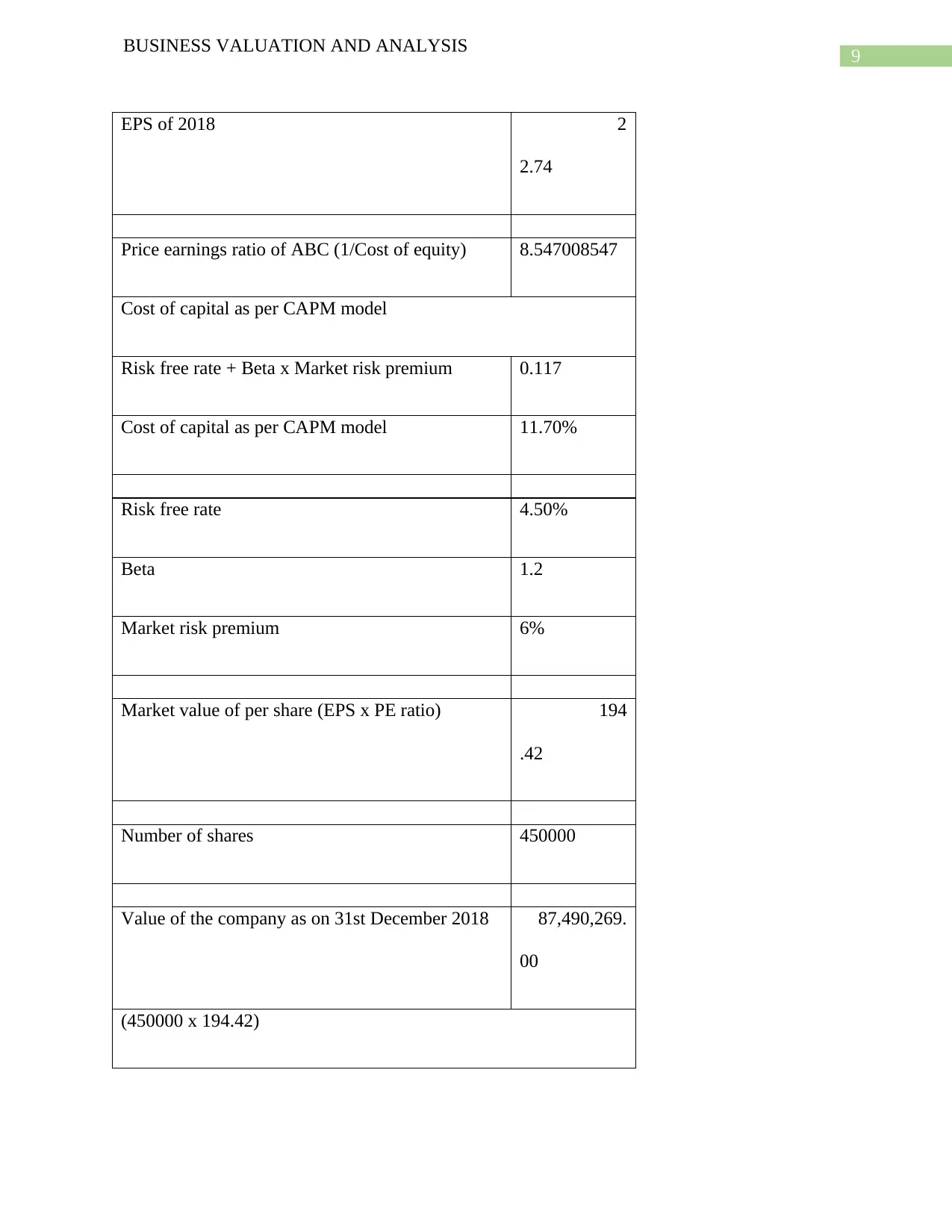

EPS of 2018 2

2.74

Price earnings ratio of ABC (1/Cost of equity) 8.547008547

Cost of capital as per CAPM model

Risk free rate + Beta x Market risk premium 0.117

Cost of capital as per CAPM model 11.70%

Risk free rate 4.50%

Beta 1.2

Market risk premium 6%

Market value of per share (EPS x PE ratio) 194

.42

Number of shares 450000

Value of the company as on 31st December 2018 87,490,269.

00

(450000 x 194.42)

BUSINESS VALUATION AND ANALYSIS

EPS of 2018 2

2.74

Price earnings ratio of ABC (1/Cost of equity) 8.547008547

Cost of capital as per CAPM model

Risk free rate + Beta x Market risk premium 0.117

Cost of capital as per CAPM model 11.70%

Risk free rate 4.50%

Beta 1.2

Market risk premium 6%

Market value of per share (EPS x PE ratio) 194

.42

Number of shares 450000

Value of the company as on 31st December 2018 87,490,269.

00

(450000 x 194.42)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

BUSINESS VALUATION AND ANALYSIS

Thus, the value of the company is $87,490,269 under PE ratio method. It is now clear that the

valuation techniques have significant influence on the resultant value of a company (Pohl, 2017).

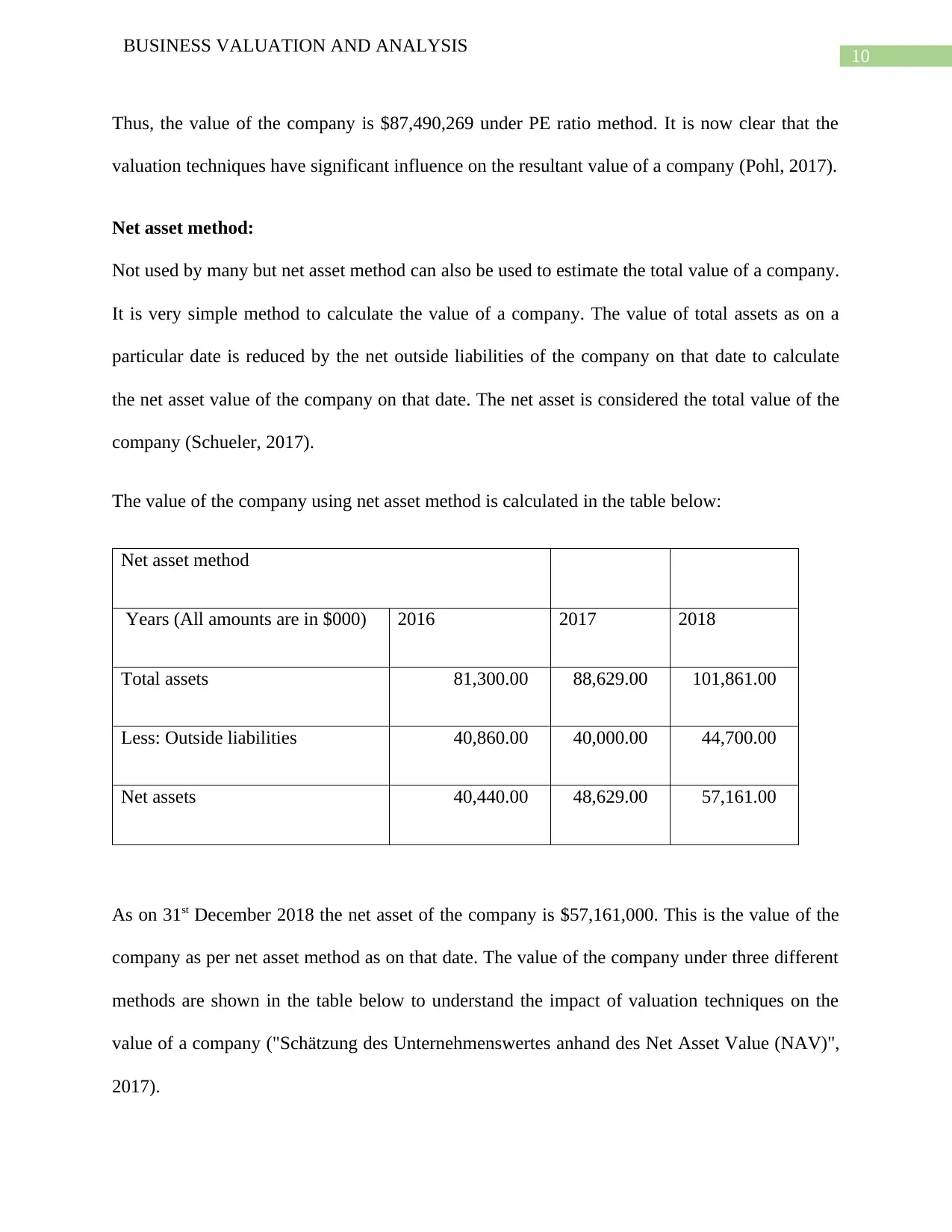

Net asset method:

Not used by many but net asset method can also be used to estimate the total value of a company.

It is very simple method to calculate the value of a company. The value of total assets as on a

particular date is reduced by the net outside liabilities of the company on that date to calculate

the net asset value of the company on that date. The net asset is considered the total value of the

company (Schueler, 2017).

The value of the company using net asset method is calculated in the table below:

Net asset method

Years (All amounts are in $000) 2016 2017 2018

Total assets 81,300.00 88,629.00 101,861.00

Less: Outside liabilities 40,860.00 40,000.00 44,700.00

Net assets 40,440.00 48,629.00 57,161.00

As on 31st December 2018 the net asset of the company is $57,161,000. This is the value of the

company as per net asset method as on that date. The value of the company under three different

methods are shown in the table below to understand the impact of valuation techniques on the

value of a company ("Schätzung des Unternehmenswertes anhand des Net Asset Value (NAV)",

2017).

BUSINESS VALUATION AND ANALYSIS

Thus, the value of the company is $87,490,269 under PE ratio method. It is now clear that the

valuation techniques have significant influence on the resultant value of a company (Pohl, 2017).

Net asset method:

Not used by many but net asset method can also be used to estimate the total value of a company.

It is very simple method to calculate the value of a company. The value of total assets as on a

particular date is reduced by the net outside liabilities of the company on that date to calculate

the net asset value of the company on that date. The net asset is considered the total value of the

company (Schueler, 2017).

The value of the company using net asset method is calculated in the table below:

Net asset method

Years (All amounts are in $000) 2016 2017 2018

Total assets 81,300.00 88,629.00 101,861.00

Less: Outside liabilities 40,860.00 40,000.00 44,700.00

Net assets 40,440.00 48,629.00 57,161.00

As on 31st December 2018 the net asset of the company is $57,161,000. This is the value of the

company as per net asset method as on that date. The value of the company under three different

methods are shown in the table below to understand the impact of valuation techniques on the

value of a company ("Schätzung des Unternehmenswertes anhand des Net Asset Value (NAV)",

2017).

11

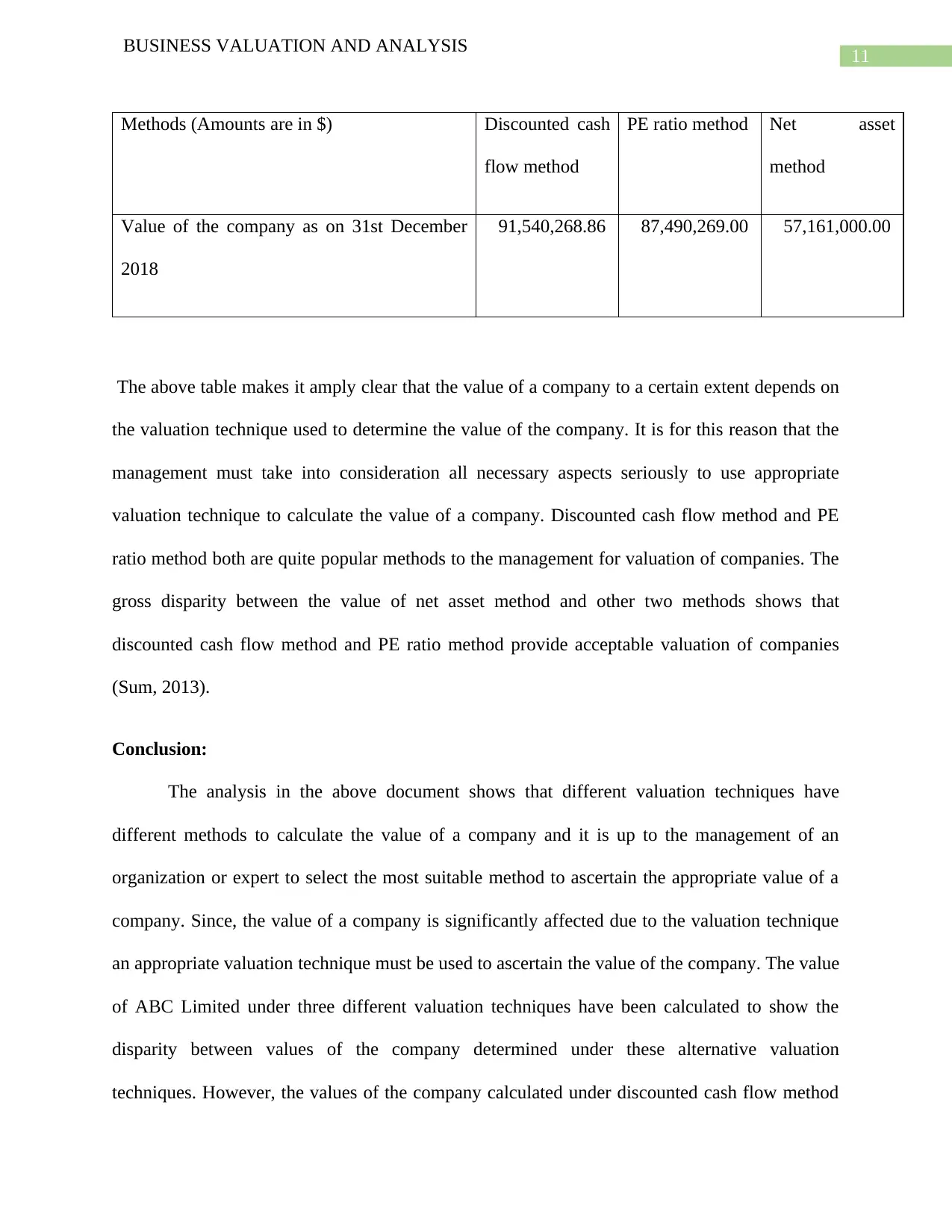

BUSINESS VALUATION AND ANALYSIS

Methods (Amounts are in $) Discounted cash

flow method

PE ratio method Net asset

method

Value of the company as on 31st December

2018

91,540,268.86 87,490,269.00 57,161,000.00

The above table makes it amply clear that the value of a company to a certain extent depends on

the valuation technique used to determine the value of the company. It is for this reason that the

management must take into consideration all necessary aspects seriously to use appropriate

valuation technique to calculate the value of a company. Discounted cash flow method and PE

ratio method both are quite popular methods to the management for valuation of companies. The

gross disparity between the value of net asset method and other two methods shows that

discounted cash flow method and PE ratio method provide acceptable valuation of companies

(Sum, 2013).

Conclusion:

The analysis in the above document shows that different valuation techniques have

different methods to calculate the value of a company and it is up to the management of an

organization or expert to select the most suitable method to ascertain the appropriate value of a

company. Since, the value of a company is significantly affected due to the valuation technique

an appropriate valuation technique must be used to ascertain the value of the company. The value

of ABC Limited under three different valuation techniques have been calculated to show the

disparity between values of the company determined under these alternative valuation

techniques. However, the values of the company calculated under discounted cash flow method

BUSINESS VALUATION AND ANALYSIS

Methods (Amounts are in $) Discounted cash

flow method

PE ratio method Net asset

method

Value of the company as on 31st December

2018

91,540,268.86 87,490,269.00 57,161,000.00

The above table makes it amply clear that the value of a company to a certain extent depends on

the valuation technique used to determine the value of the company. It is for this reason that the

management must take into consideration all necessary aspects seriously to use appropriate

valuation technique to calculate the value of a company. Discounted cash flow method and PE

ratio method both are quite popular methods to the management for valuation of companies. The

gross disparity between the value of net asset method and other two methods shows that

discounted cash flow method and PE ratio method provide acceptable valuation of companies

(Sum, 2013).

Conclusion:

The analysis in the above document shows that different valuation techniques have

different methods to calculate the value of a company and it is up to the management of an

organization or expert to select the most suitable method to ascertain the appropriate value of a

company. Since, the value of a company is significantly affected due to the valuation technique

an appropriate valuation technique must be used to ascertain the value of the company. The value

of ABC Limited under three different valuation techniques have been calculated to show the

disparity between values of the company determined under these alternative valuation

techniques. However, the values of the company calculated under discounted cash flow method

12

BUSINESS VALUATION AND ANALYSIS

and PE ratio method are quite close to each other hence, the value of the company will be closer

to the values determined under these two valuation techniques. The important thing to be

remembered is that the management should use the expert services to calculate the value of the

company as it is an extremely complex to correctly calculate value of a company.

BUSINESS VALUATION AND ANALYSIS

and PE ratio method are quite close to each other hence, the value of the company will be closer

to the values determined under these two valuation techniques. The important thing to be

remembered is that the management should use the expert services to calculate the value of the

company as it is an extremely complex to correctly calculate value of a company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

BUSINESS VALUATION AND ANALYSIS

References:

Cifuentes, A. (2016). The Discounted Cash Flow (DCF) Method Applied to Valuation: Too

Many Uncomfortable Truths. SSRN Electronic Journal, 2(3), 67. doi: 10.2139/ssrn.2845341

Discounted Cash Flow Method for Valuing International Chemical Distributors. (2018). The

Journal Of Private Equity, 1(2), 16-21. doi: 10.3905/jpe.2018.22.1.052

Fernandez, P. (2013). Price to Earnings Ratio, Value to Book Ratio and Growth. SSRN

Electronic Journal, 1(3), 26-39. doi: 10.2139/ssrn.2212373

Ghaeli, M. (2017). Price-to-earnings ratio: A state-of-art review. Accounting, 3(2), 131-136. doi:

10.5267/j.ac.2016.7.002

Ke, X. (2017). The Impacts of the CPS, Free Cash Flow, Tobin's Q, and Price-Earnings Ratio on

Investment Decisions. SSRN Electronic Journal, 1(9), 63-72. doi: 10.2139/ssrn.2957267

Klimas, T. (2012). Akcininkų susitarimai ir akcijų vertė (Shareholders' Agreements and

Company Valuation). SSRN Electronic Journal, 1(3), 16-394. doi: 10.2139/ssrn.2189297

Li, Y. (2013). How to Determine the Appropriate Discount Rate in Company Valuation?. SSRN

Electronic Journal, 2(4), 17-45. doi: 10.2139/ssrn.2340830

Li, Y. (2013). Improve the Target Price Performance by the Enhanced Company Valuation

Techniques. SSRN Electronic Journal, 2(5), 27-128. doi: 10.2139/ssrn.2344187

Pohl, P. (2017). Valuation of a Company using Time Series Analysis. Journal Of Business

Valuation And Economic Loss Analysis, 12(1), 1-39. doi: 10.1515/jbvela-2015-0004

BUSINESS VALUATION AND ANALYSIS

References:

Cifuentes, A. (2016). The Discounted Cash Flow (DCF) Method Applied to Valuation: Too

Many Uncomfortable Truths. SSRN Electronic Journal, 2(3), 67. doi: 10.2139/ssrn.2845341

Discounted Cash Flow Method for Valuing International Chemical Distributors. (2018). The

Journal Of Private Equity, 1(2), 16-21. doi: 10.3905/jpe.2018.22.1.052

Fernandez, P. (2013). Price to Earnings Ratio, Value to Book Ratio and Growth. SSRN

Electronic Journal, 1(3), 26-39. doi: 10.2139/ssrn.2212373

Ghaeli, M. (2017). Price-to-earnings ratio: A state-of-art review. Accounting, 3(2), 131-136. doi:

10.5267/j.ac.2016.7.002

Ke, X. (2017). The Impacts of the CPS, Free Cash Flow, Tobin's Q, and Price-Earnings Ratio on

Investment Decisions. SSRN Electronic Journal, 1(9), 63-72. doi: 10.2139/ssrn.2957267

Klimas, T. (2012). Akcininkų susitarimai ir akcijų vertė (Shareholders' Agreements and

Company Valuation). SSRN Electronic Journal, 1(3), 16-394. doi: 10.2139/ssrn.2189297

Li, Y. (2013). How to Determine the Appropriate Discount Rate in Company Valuation?. SSRN

Electronic Journal, 2(4), 17-45. doi: 10.2139/ssrn.2340830

Li, Y. (2013). Improve the Target Price Performance by the Enhanced Company Valuation

Techniques. SSRN Electronic Journal, 2(5), 27-128. doi: 10.2139/ssrn.2344187

Pohl, P. (2017). Valuation of a Company using Time Series Analysis. Journal Of Business

Valuation And Economic Loss Analysis, 12(1), 1-39. doi: 10.1515/jbvela-2015-0004

14

BUSINESS VALUATION AND ANALYSIS

Schätzung des Unternehmenswertes anhand des Net Asset Value (NAV). (2017). Die

Aktiengesellschaft, 62(15), 26-39. doi: 10.9785/ag-2017-1510

Schueler, A. (2017). A Tool Kit for Discounted Cash Flow Valuation: Consistent and

Inconsistent Ways to Value Risky Cash Flows. SSRN Electronic Journal, 7(9), 27-39. doi:

10.2139/ssrn.3132243

Sum, V. (2013). Dynamic Effect of Tobin's Q on Price-to-Earnings Ratio. SSRN Electronic

Journal, 3(6), 16-37. doi: 10.2139/ssrn.2292812

BUSINESS VALUATION AND ANALYSIS

Schätzung des Unternehmenswertes anhand des Net Asset Value (NAV). (2017). Die

Aktiengesellschaft, 62(15), 26-39. doi: 10.9785/ag-2017-1510

Schueler, A. (2017). A Tool Kit for Discounted Cash Flow Valuation: Consistent and

Inconsistent Ways to Value Risky Cash Flows. SSRN Electronic Journal, 7(9), 27-39. doi:

10.2139/ssrn.3132243

Sum, V. (2013). Dynamic Effect of Tobin's Q on Price-to-Earnings Ratio. SSRN Electronic

Journal, 3(6), 16-37. doi: 10.2139/ssrn.2292812

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.