Business Valuation and Analysis Report: Financial Analysis

VerifiedAdded on 2021/06/17

|13

|2859

|19

Report

AI Summary

This report presents a comprehensive business valuation and financial analysis, focusing on the financial performance of a company over a five-year period (2013-2017). The analysis encompasses a detailed examination of various financial ratios, including return on equity (ROE), return on net operating assets (RNOA), financial leverage, net borrowing cost, profitability margin, and asset turnover ratio. The report also delves into cash flow analysis, covering liquidity and solvency ratios, along with cash flow ratios like operating cash flow to sales and asset efficiency. The analysis highlights trends, fluctuations, and significant factors influencing the company's financial health, such as changes in finance costs, employee benefits, raw materials, and cash equivalents. The report provides insights into the company's stability, efficiency, and ability to manage its short-term and long-term obligations, offering a holistic view of its financial standing.

Running head: BUSINESS VALUATION AND ANALYSIS

Business valuation and analysis

Name of the student

Name of the university

Student ID

Author note

Business valuation and analysis

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS VALUATION AND ANALYSIS

Table of Contents

Reformatting..........................................................................................................................................2

Ratio analysis........................................................................................................................................2

Cash flow analysis.................................................................................................................................5

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

Table of Contents

Reformatting..........................................................................................................................................2

Ratio analysis........................................................................................................................................2

Cash flow analysis.................................................................................................................................5

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

2BUSINESS VALUATION AND ANALYSIS

Reformatting

Refer to appendix and Excel sheet

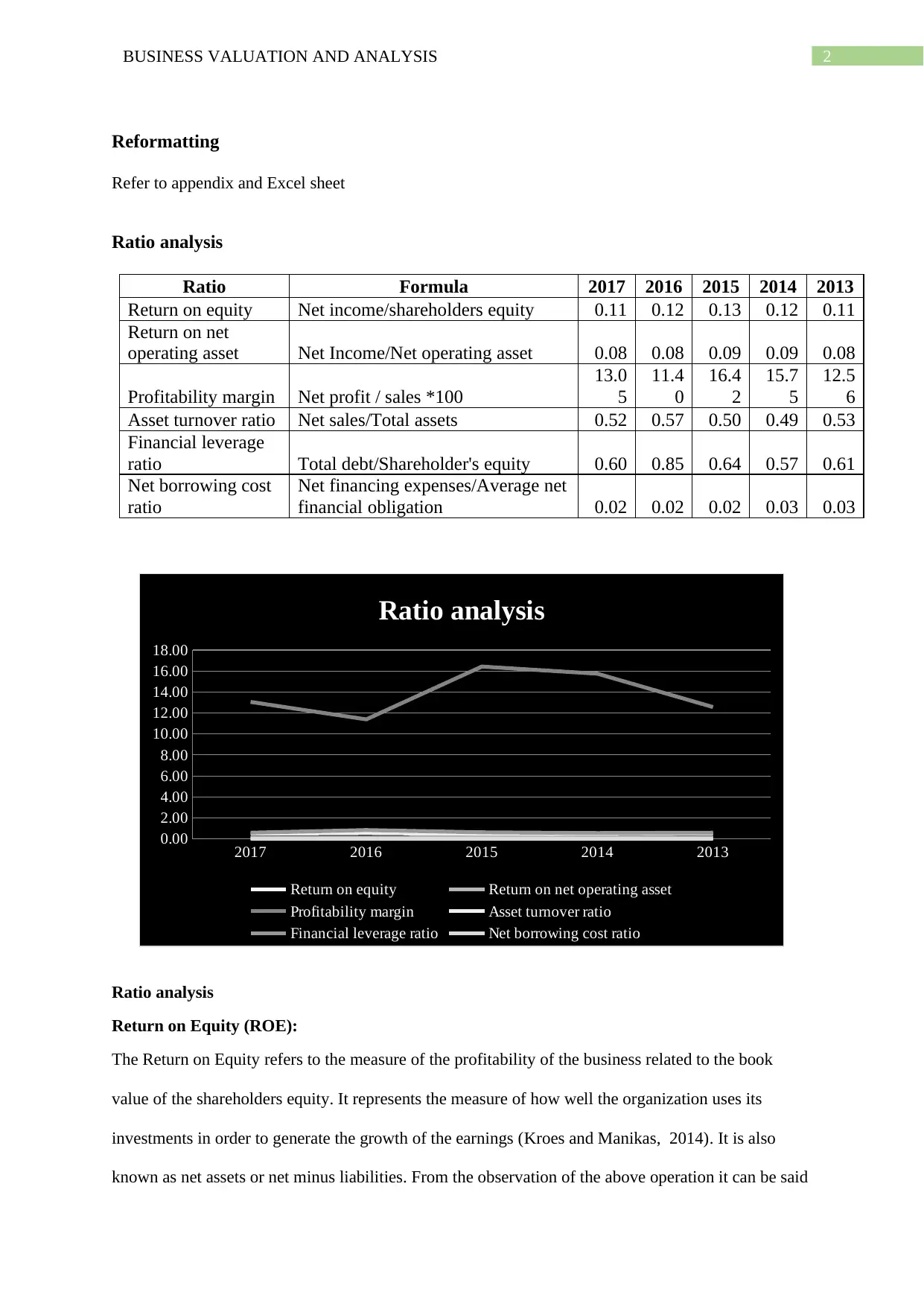

Ratio analysis

Ratio Formula 2017 2016 2015 2014 2013

Return on equity Net income/shareholders equity 0.11 0.12 0.13 0.12 0.11

Return on net

operating asset Net Income/Net operating asset 0.08 0.08 0.09 0.09 0.08

Profitability margin Net profit / sales *100

13.0

5

11.4

0

16.4

2

15.7

5

12.5

6

Asset turnover ratio Net sales/Total assets 0.52 0.57 0.50 0.49 0.53

Financial leverage

ratio Total debt/Shareholder's equity 0.60 0.85 0.64 0.57 0.61

Net borrowing cost

ratio

Net financing expenses/Average net

financial obligation 0.02 0.02 0.02 0.03 0.03

2017 2016 2015 2014 2013

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Ratio analysis

Return on equity Return on net operating asset

Profitability margin Asset turnover ratio

Financial leverage ratio Net borrowing cost ratio

Ratio analysis

Return on Equity (ROE):

The Return on Equity refers to the measure of the profitability of the business related to the book

value of the shareholders equity. It represents the measure of how well the organization uses its

investments in order to generate the growth of the earnings (Kroes and Manikas, 2014). It is also

known as net assets or net minus liabilities. From the observation of the above operation it can be said

Reformatting

Refer to appendix and Excel sheet

Ratio analysis

Ratio Formula 2017 2016 2015 2014 2013

Return on equity Net income/shareholders equity 0.11 0.12 0.13 0.12 0.11

Return on net

operating asset Net Income/Net operating asset 0.08 0.08 0.09 0.09 0.08

Profitability margin Net profit / sales *100

13.0

5

11.4

0

16.4

2

15.7

5

12.5

6

Asset turnover ratio Net sales/Total assets 0.52 0.57 0.50 0.49 0.53

Financial leverage

ratio Total debt/Shareholder's equity 0.60 0.85 0.64 0.57 0.61

Net borrowing cost

ratio

Net financing expenses/Average net

financial obligation 0.02 0.02 0.02 0.03 0.03

2017 2016 2015 2014 2013

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Ratio analysis

Return on equity Return on net operating asset

Profitability margin Asset turnover ratio

Financial leverage ratio Net borrowing cost ratio

Ratio analysis

Return on Equity (ROE):

The Return on Equity refers to the measure of the profitability of the business related to the book

value of the shareholders equity. It represents the measure of how well the organization uses its

investments in order to generate the growth of the earnings (Kroes and Manikas, 2014). It is also

known as net assets or net minus liabilities. From the observation of the above operation it can be said

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS VALUATION AND ANALYSIS

that the company maintained a stable rate of return on equity over the last 5 years. The rate also varied

between 0.11 and 0.13. Hence from the analysis it can be said that company is steady in providing the

shareholders return.

Return on net operating asset (RNOA):

The Return on Net assets is the mechanism that measures the financial performance that is calculated

by dividing the total income by the summation of the fixed assets and the net working capital. The

RNOA issued to compare the performance of a particular company with the other companies in the

same industry(Robinson and Sensoy 2016). It represents the management of the company by

deploying the economy value of the asset. If the ratio is high, it signifies that the company more

efficient. In the given case the RNOA is maintained at a stable rate over the recent 5 years that varied

from 0.89 and 0.09. Hence it has been identified that the present organisation is stable in providing the

operating asset return.

Financial leverage (FLEV): The financial leverage is the measure of the extent up to which the

business or the investor uses the money that is borrowed. If the leverage is high there is risk of

bankruptcy and in case the company is not being able to pay the debts, they might lead to problems in

getting new lenders in the times to come. The financial leverage can lead to increase in shareholders’

investment returns. It represents the reliability of an organisation on its debts in order to operate. In

the given case it has been observed that the organisation has a low financial leverage as the company

has used more equity as a source of finance for its assets as compared to the debts for the last 5 years

under considerations. The range varied from 0.57 and 0.85, which can be said to efficient enough to

maintain sustainability.

Net borrowing cost (NBC):

The Net borrowing cost is referred to as the interest and the other cost that are incurred by an

organisation related to the borrowing of the funds. In a more technical term it can be said that the

borrowing cost is the expense that is incurred in meeting the loan expenses. It includes the interest

payment made on issuing the loan. Moreover, the NBC also includes the amortization of the premium

that the company maintained a stable rate of return on equity over the last 5 years. The rate also varied

between 0.11 and 0.13. Hence from the analysis it can be said that company is steady in providing the

shareholders return.

Return on net operating asset (RNOA):

The Return on Net assets is the mechanism that measures the financial performance that is calculated

by dividing the total income by the summation of the fixed assets and the net working capital. The

RNOA issued to compare the performance of a particular company with the other companies in the

same industry(Robinson and Sensoy 2016). It represents the management of the company by

deploying the economy value of the asset. If the ratio is high, it signifies that the company more

efficient. In the given case the RNOA is maintained at a stable rate over the recent 5 years that varied

from 0.89 and 0.09. Hence it has been identified that the present organisation is stable in providing the

operating asset return.

Financial leverage (FLEV): The financial leverage is the measure of the extent up to which the

business or the investor uses the money that is borrowed. If the leverage is high there is risk of

bankruptcy and in case the company is not being able to pay the debts, they might lead to problems in

getting new lenders in the times to come. The financial leverage can lead to increase in shareholders’

investment returns. It represents the reliability of an organisation on its debts in order to operate. In

the given case it has been observed that the organisation has a low financial leverage as the company

has used more equity as a source of finance for its assets as compared to the debts for the last 5 years

under considerations. The range varied from 0.57 and 0.85, which can be said to efficient enough to

maintain sustainability.

Net borrowing cost (NBC):

The Net borrowing cost is referred to as the interest and the other cost that are incurred by an

organisation related to the borrowing of the funds. In a more technical term it can be said that the

borrowing cost is the expense that is incurred in meeting the loan expenses. It includes the interest

payment made on issuing the loan. Moreover, the NBC also includes the amortization of the premium

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS VALUATION AND ANALYSIS

or discount or debt. It has been observed in the given scenario that the net borrowing on the cost of

last 5 years that maintained more or less same ratio for the borrowing cost. The ratio of NBC of the

organisation in the year 2013 and 2014 is 0.3 and for 2015, 2016, 2017 it was constant at the rate of

0.02. Hence the organisation is stable in sustaining the ratio of borrowing cost.

Profitability margin (PM): The profitability margin is the ratio that measures the profitability of the

business by analysing the net profit of the company against the sales revenue(Prentice 2016). It helps

in the internal comparison of the business and indicates the company’s strategies of pricing and the

technique for controlling their cost. The variations in product mix and the competitive strategy may

cause the profit margin to vary among different organisations. In the given case the profitability

margin is fluctuating over the last 5 years there was no huge fluctuation noticed (Brooks 2015).

Beginning from the year 2013 till the time of 2015 the organization experienced expanding pattern for

PM and from 12.56% it expanded to 16.42%. Be that as it may, in 2016 the PM tumbled to 11.40%

however the organization could expand it to 13.05% in the year 2017. Three major expenses that

prompt diminishment in PM in the year 2016 when contrasted with 2015 are as per the following –

• Finance cost – finance cost expanded from $ 4,722 thousand to $ 7,374 thousand throughout

the years from 2015 to 2016.

• Employee benefits costs – Employee benefits costs fundamentally expanded from $ 58,631

thousand to $ 80.809 thousand throughout the years from 2015 to 2016.

Raw materials and consumables utilized – Raw materials and consumables utilized essentially

expanded from $ 164,452 thousand to $ 251,734 thousand throughout the years from 2015 to 2016.

All the over 3 costs prompted lessening of net benefit from $ 49,992 thousand to $ 48,493

thousand throughout the years from 2015 to 2016.

Assets turnover Ratio (ATO) – It is the productivity proportion that assesses the capacity of the

organization to generate sales from the assets through contrasting the deals and the aggregate

resources of the organization. To be more particular, it measures the effectiveness of the organization

or discount or debt. It has been observed in the given scenario that the net borrowing on the cost of

last 5 years that maintained more or less same ratio for the borrowing cost. The ratio of NBC of the

organisation in the year 2013 and 2014 is 0.3 and for 2015, 2016, 2017 it was constant at the rate of

0.02. Hence the organisation is stable in sustaining the ratio of borrowing cost.

Profitability margin (PM): The profitability margin is the ratio that measures the profitability of the

business by analysing the net profit of the company against the sales revenue(Prentice 2016). It helps

in the internal comparison of the business and indicates the company’s strategies of pricing and the

technique for controlling their cost. The variations in product mix and the competitive strategy may

cause the profit margin to vary among different organisations. In the given case the profitability

margin is fluctuating over the last 5 years there was no huge fluctuation noticed (Brooks 2015).

Beginning from the year 2013 till the time of 2015 the organization experienced expanding pattern for

PM and from 12.56% it expanded to 16.42%. Be that as it may, in 2016 the PM tumbled to 11.40%

however the organization could expand it to 13.05% in the year 2017. Three major expenses that

prompt diminishment in PM in the year 2016 when contrasted with 2015 are as per the following –

• Finance cost – finance cost expanded from $ 4,722 thousand to $ 7,374 thousand throughout

the years from 2015 to 2016.

• Employee benefits costs – Employee benefits costs fundamentally expanded from $ 58,631

thousand to $ 80.809 thousand throughout the years from 2015 to 2016.

Raw materials and consumables utilized – Raw materials and consumables utilized essentially

expanded from $ 164,452 thousand to $ 251,734 thousand throughout the years from 2015 to 2016.

All the over 3 costs prompted lessening of net benefit from $ 49,992 thousand to $ 48,493

thousand throughout the years from 2015 to 2016.

Assets turnover Ratio (ATO) – It is the productivity proportion that assesses the capacity of the

organization to generate sales from the assets through contrasting the deals and the aggregate

resources of the organization. To be more particular, it measures the effectiveness of the organization

5BUSINESS VALUATION AND ANALYSIS

with respect to utilization of the benefits for generating the sales(Grant 2016). It can be seen from the

yearly report and figuring introduced in the above table that there is not much changes in the ATO of

the organization in the course of the most recent 5 years that is from 2013 to 2017. The ATO of the

organization has a steady pattern it extended in the range of 0.49 and 0.57 during the year 2013 to

2017. Three major assets or liabilities that has effect on the benefit effectiveness ratio are as per the

following –

• Cash and cash equivalent – the cash and cash equivalent of the organization throughout the previous

5 years are fluctuating. There is no particular pattern for this thing under the present assets. It fell

altogether from $ 14,998 thousand to $ 7,656 thousand throughout the years and again expanded

significantly from $ 12,521 thousand to $ 30,561 throughout the years from 2016 to 2017(Qiu,

Shaukat and Tharyan 2016.).

• Trade and other receivables – it has no particular pattern in the course of the most recent 5 years.

Notwithstanding, it fell essentially from $ 13,349 thousand to $ 7,636 thousand throughout the years

and again expanded fundamentally from $ 14,034 thousand to $ 25,300 over the course of the years

from 2015 to 2016(Titman and Martin 2014).

• Biological asset – biological assets of the organization are in expanding pattern over the 5 years’

time frame from the year 2013 to 2017. It went up to $ 312,405 thousand from $ 159,935 thousand.

All the previously mentioned 3 things have added to the general changes of the assets efficiency

Tassal was the first salmon maker everywhere throughout the world that has 100% harvest

stock. The organization will probably keep up adjust among the budgetary, ecological, society, group

and operational value practices and standards (Yaplee and Chien 2015). It helped the organization to

keep up the stability concerning financial execution.

Cash flow analysis

Ratio Formula 2017 2016 2015 2014 2013

Liquidity ratio

with respect to utilization of the benefits for generating the sales(Grant 2016). It can be seen from the

yearly report and figuring introduced in the above table that there is not much changes in the ATO of

the organization in the course of the most recent 5 years that is from 2013 to 2017. The ATO of the

organization has a steady pattern it extended in the range of 0.49 and 0.57 during the year 2013 to

2017. Three major assets or liabilities that has effect on the benefit effectiveness ratio are as per the

following –

• Cash and cash equivalent – the cash and cash equivalent of the organization throughout the previous

5 years are fluctuating. There is no particular pattern for this thing under the present assets. It fell

altogether from $ 14,998 thousand to $ 7,656 thousand throughout the years and again expanded

significantly from $ 12,521 thousand to $ 30,561 throughout the years from 2016 to 2017(Qiu,

Shaukat and Tharyan 2016.).

• Trade and other receivables – it has no particular pattern in the course of the most recent 5 years.

Notwithstanding, it fell essentially from $ 13,349 thousand to $ 7,636 thousand throughout the years

and again expanded fundamentally from $ 14,034 thousand to $ 25,300 over the course of the years

from 2015 to 2016(Titman and Martin 2014).

• Biological asset – biological assets of the organization are in expanding pattern over the 5 years’

time frame from the year 2013 to 2017. It went up to $ 312,405 thousand from $ 159,935 thousand.

All the previously mentioned 3 things have added to the general changes of the assets efficiency

Tassal was the first salmon maker everywhere throughout the world that has 100% harvest

stock. The organization will probably keep up adjust among the budgetary, ecological, society, group

and operational value practices and standards (Yaplee and Chien 2015). It helped the organization to

keep up the stability concerning financial execution.

Cash flow analysis

Ratio Formula 2017 2016 2015 2014 2013

Liquidity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS VALUATION AND ANALYSIS

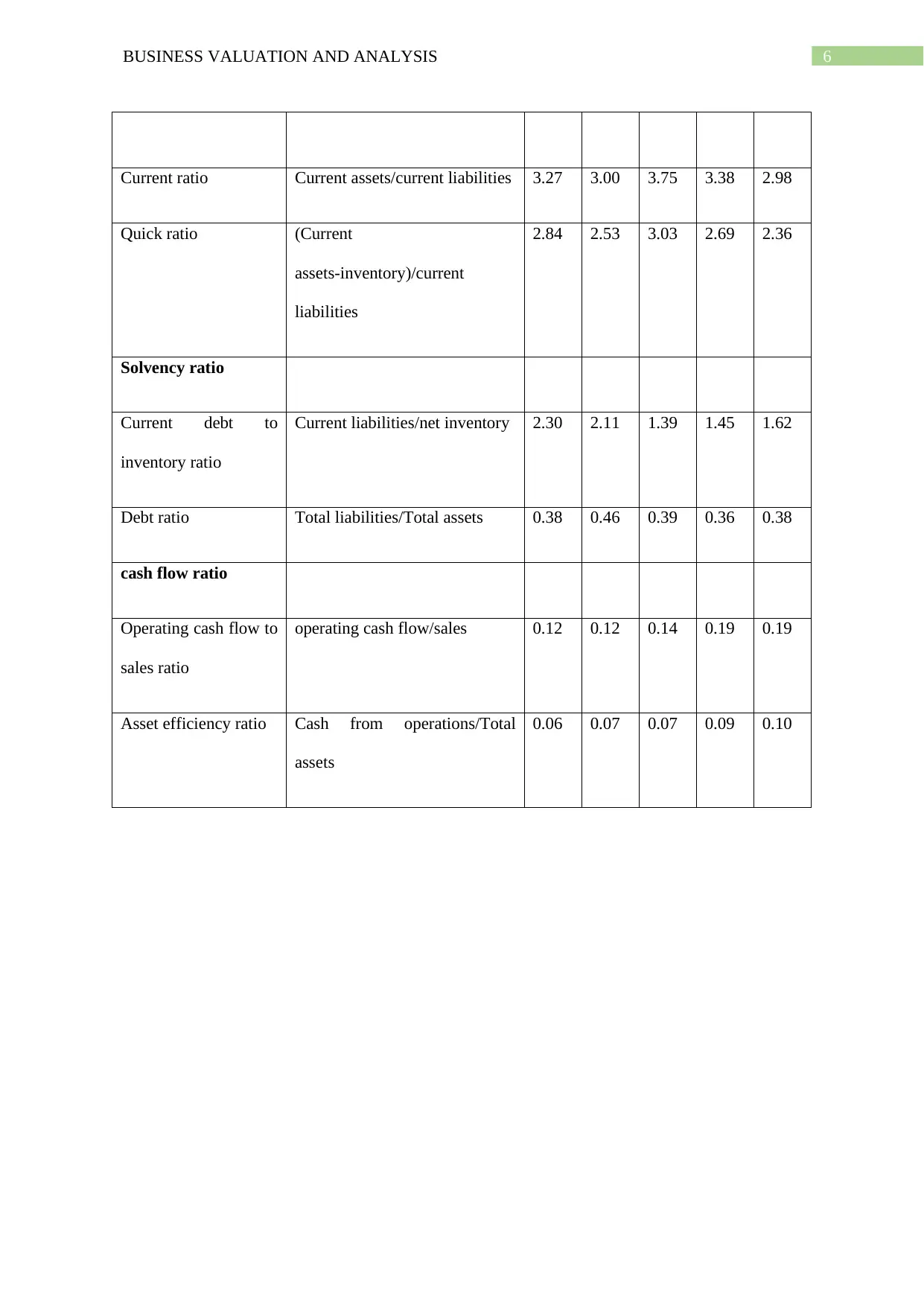

Current ratio Current assets/current liabilities 3.27 3.00 3.75 3.38 2.98

Quick ratio (Current

assets-inventory)/current

liabilities

2.84 2.53 3.03 2.69 2.36

Solvency ratio

Current debt to

inventory ratio

Current liabilities/net inventory 2.30 2.11 1.39 1.45 1.62

Debt ratio Total liabilities/Total assets 0.38 0.46 0.39 0.36 0.38

cash flow ratio

Operating cash flow to

sales ratio

operating cash flow/sales 0.12 0.12 0.14 0.19 0.19

Asset efficiency ratio Cash from operations/Total

assets

0.06 0.07 0.07 0.09 0.10

Current ratio Current assets/current liabilities 3.27 3.00 3.75 3.38 2.98

Quick ratio (Current

assets-inventory)/current

liabilities

2.84 2.53 3.03 2.69 2.36

Solvency ratio

Current debt to

inventory ratio

Current liabilities/net inventory 2.30 2.11 1.39 1.45 1.62

Debt ratio Total liabilities/Total assets 0.38 0.46 0.39 0.36 0.38

cash flow ratio

Operating cash flow to

sales ratio

operating cash flow/sales 0.12 0.12 0.14 0.19 0.19

Asset efficiency ratio Cash from operations/Total

assets

0.06 0.07 0.07 0.09 0.10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS VALUATION AND ANALYSIS

Current ratio Quick ratio Current debt

to inventory

ratio

Debt ratio Operating

cash flow to

sales ratio

Asset

efficiency

ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Cash flow analysis

2017

2016

2015

2014

2013

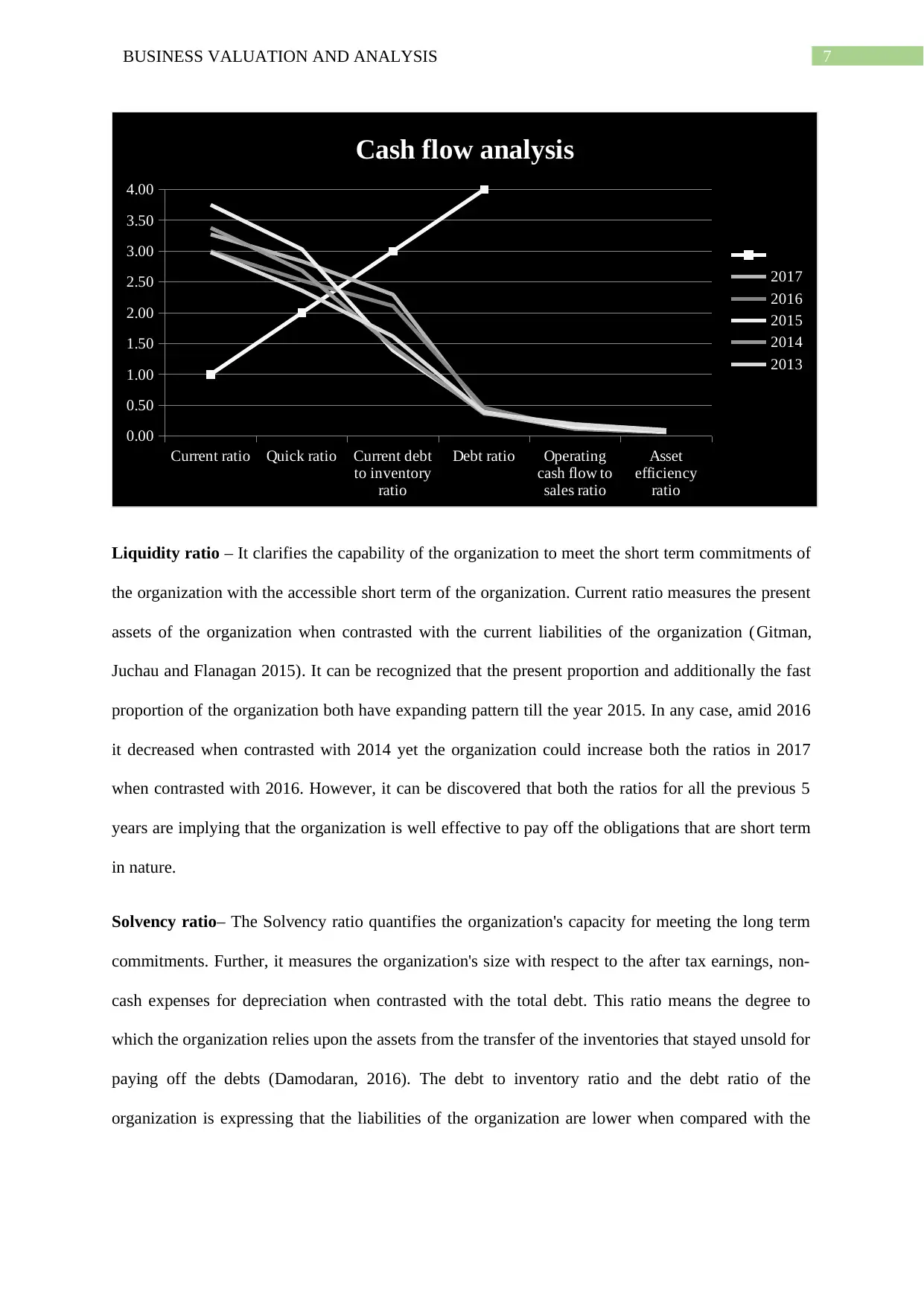

Liquidity ratio – It clarifies the capability of the organization to meet the short term commitments of

the organization with the accessible short term of the organization. Current ratio measures the present

assets of the organization when contrasted with the current liabilities of the organization (Gitman,

Juchau and Flanagan 2015). It can be recognized that the present proportion and additionally the fast

proportion of the organization both have expanding pattern till the year 2015. In any case, amid 2016

it decreased when contrasted with 2014 yet the organization could increase both the ratios in 2017

when contrasted with 2016. However, it can be discovered that both the ratios for all the previous 5

years are implying that the organization is well effective to pay off the obligations that are short term

in nature.

Solvency ratio– The Solvency ratio quantifies the organization's capacity for meeting the long term

commitments. Further, it measures the organization's size with respect to the after tax earnings, non-

cash expenses for depreciation when contrasted with the total debt. This ratio means the degree to

which the organization relies upon the assets from the transfer of the inventories that stayed unsold for

paying off the debts (Damodaran, 2016). The debt to inventory ratio and the debt ratio of the

organization is expressing that the liabilities of the organization are lower when compared with the

Current ratio Quick ratio Current debt

to inventory

ratio

Debt ratio Operating

cash flow to

sales ratio

Asset

efficiency

ratio

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Cash flow analysis

2017

2016

2015

2014

2013

Liquidity ratio – It clarifies the capability of the organization to meet the short term commitments of

the organization with the accessible short term of the organization. Current ratio measures the present

assets of the organization when contrasted with the current liabilities of the organization (Gitman,

Juchau and Flanagan 2015). It can be recognized that the present proportion and additionally the fast

proportion of the organization both have expanding pattern till the year 2015. In any case, amid 2016

it decreased when contrasted with 2014 yet the organization could increase both the ratios in 2017

when contrasted with 2016. However, it can be discovered that both the ratios for all the previous 5

years are implying that the organization is well effective to pay off the obligations that are short term

in nature.

Solvency ratio– The Solvency ratio quantifies the organization's capacity for meeting the long term

commitments. Further, it measures the organization's size with respect to the after tax earnings, non-

cash expenses for depreciation when contrasted with the total debt. This ratio means the degree to

which the organization relies upon the assets from the transfer of the inventories that stayed unsold for

paying off the debts (Damodaran, 2016). The debt to inventory ratio and the debt ratio of the

organization is expressing that the liabilities of the organization are lower when compared with the

8BUSINESS VALUATION AND ANALYSIS

assets of the organization. However, the organization is utilizing higher measure of debt for obtaining

the inventories.

Cash flow ratio – The cash flow ratio represents the ability of the organization to measure the

number of times the organization can pay the present commitments with the trade made out same

period under consideration(Olbrich, Quill and Rapp 2015) The operating cash flow to sales represents

the idea about the operating cash flow of the organization when contrasted with the net incomes or

sales that gives an idea to the financial investors regarding the capacity of transforming the sales into

cash. Both the income proportions that is the working income to deals and resource productivity

proportion are in diminishing pattern (Chen, Feldmann and Tang 2015). The operating cash flow

ratio has been lessened from 0.19 to 0.12 and the advantage efficiency ratio has been diminished from

0.10 to 0.06 over the previous years from 2013 to 2017. In this way, it can be expressed that the

capacity of the organization for transforming its deals into money are lessening over year to year.

References

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Trugman, 2016. Understanding business valuation: A practical guide to valuing small to medium

sized businesses. John Wiley & Sons.

Olbrich, M., Quill, T. and Rapp, D.J., 2015. Business valuation inspired by the Austrian

School. Journal of Business Valuation and Economic Loss Analysis, 10(1), pp.1-43.

Prentice, C.R., 2016. Why so many measures of nonprofit financial performance? Analyzing and

improving the use of financial measures in nonprofit research. Nonprofit and Voluntary Sector

Quarterly, 45(4), pp.715-740.

assets of the organization. However, the organization is utilizing higher measure of debt for obtaining

the inventories.

Cash flow ratio – The cash flow ratio represents the ability of the organization to measure the

number of times the organization can pay the present commitments with the trade made out same

period under consideration(Olbrich, Quill and Rapp 2015) The operating cash flow to sales represents

the idea about the operating cash flow of the organization when contrasted with the net incomes or

sales that gives an idea to the financial investors regarding the capacity of transforming the sales into

cash. Both the income proportions that is the working income to deals and resource productivity

proportion are in diminishing pattern (Chen, Feldmann and Tang 2015). The operating cash flow

ratio has been lessened from 0.19 to 0.12 and the advantage efficiency ratio has been diminished from

0.10 to 0.06 over the previous years from 2013 to 2017. In this way, it can be expressed that the

capacity of the organization for transforming its deals into money are lessening over year to year.

References

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Trugman, 2016. Understanding business valuation: A practical guide to valuing small to medium

sized businesses. John Wiley & Sons.

Olbrich, M., Quill, T. and Rapp, D.J., 2015. Business valuation inspired by the Austrian

School. Journal of Business Valuation and Economic Loss Analysis, 10(1), pp.1-43.

Prentice, C.R., 2016. Why so many measures of nonprofit financial performance? Analyzing and

improving the use of financial measures in nonprofit research. Nonprofit and Voluntary Sector

Quarterly, 45(4), pp.715-740.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS VALUATION AND ANALYSIS

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson Higher

Education AU.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Kroes, J.R. and Manikas, A.S., 2014. Cash flow management and manufacturing firm financial

performance: A longitudinal perspective. International Journal of Production Economics, 148, pp.37-

50.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-543.

Chen, L., Feldmann, A. and Tang, O., 2015. The relationship between disclosures of corporate social

performance and financial performance: Evidences from GRI reports in manufacturing

industry. International Journal of Production Economics, 170, pp.445-456.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review, 48(1), pp.102-116.

Yaplee, A. and Chien, S., eBay Inc, 2015. Cash flow management. U.S. Patent Application

14/091,161.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson Higher

Education AU.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Kroes, J.R. and Manikas, A.S., 2014. Cash flow management and manufacturing firm financial

performance: A longitudinal perspective. International Journal of Production Economics, 148, pp.37-

50.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-543.

Chen, L., Feldmann, A. and Tang, O., 2015. The relationship between disclosures of corporate social

performance and financial performance: Evidences from GRI reports in manufacturing

industry. International Journal of Production Economics, 170, pp.445-456.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review, 48(1), pp.102-116.

Yaplee, A. and Chien, S., eBay Inc, 2015. Cash flow management. U.S. Patent Application

14/091,161.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS VALUATION AND ANALYSIS

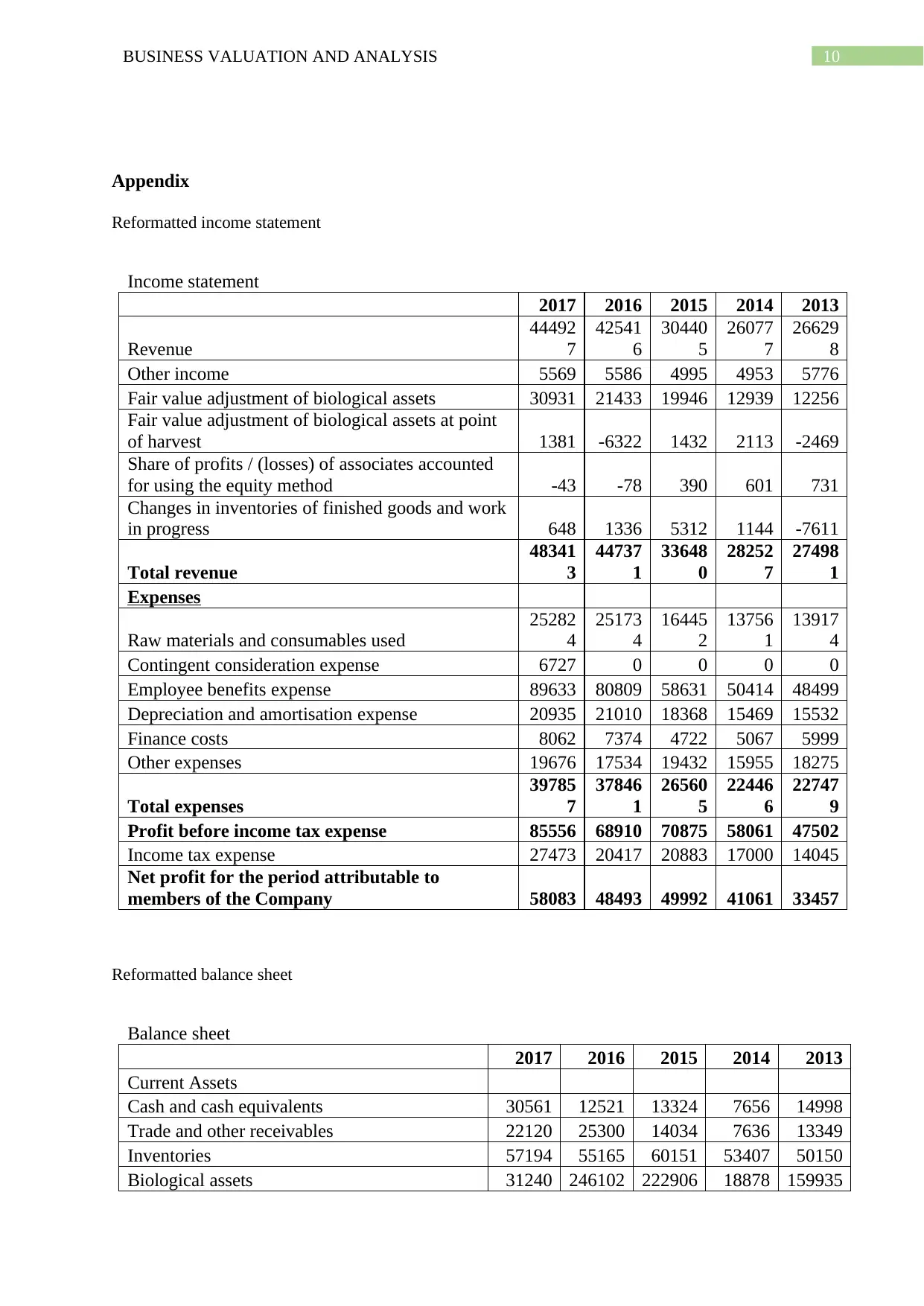

Appendix

Reformatted income statement

Income statement

2017 2016 2015 2014 2013

Revenue

44492

7

42541

6

30440

5

26077

7

26629

8

Other income 5569 5586 4995 4953 5776

Fair value adjustment of biological assets 30931 21433 19946 12939 12256

Fair value adjustment of biological assets at point

of harvest 1381 -6322 1432 2113 -2469

Share of profits / (losses) of associates accounted

for using the equity method -43 -78 390 601 731

Changes in inventories of finished goods and work

in progress 648 1336 5312 1144 -7611

Total revenue

48341

3

44737

1

33648

0

28252

7

27498

1

Expenses

Raw materials and consumables used

25282

4

25173

4

16445

2

13756

1

13917

4

Contingent consideration expense 6727 0 0 0 0

Employee benefits expense 89633 80809 58631 50414 48499

Depreciation and amortisation expense 20935 21010 18368 15469 15532

Finance costs 8062 7374 4722 5067 5999

Other expenses 19676 17534 19432 15955 18275

Total expenses

39785

7

37846

1

26560

5

22446

6

22747

9

Profit before income tax expense 85556 68910 70875 58061 47502

Income tax expense 27473 20417 20883 17000 14045

Net profit for the period attributable to

members of the Company 58083 48493 49992 41061 33457

Reformatted balance sheet

Balance sheet

2017 2016 2015 2014 2013

Current Assets

Cash and cash equivalents 30561 12521 13324 7656 14998

Trade and other receivables 22120 25300 14034 7636 13349

Inventories 57194 55165 60151 53407 50150

Biological assets 31240 246102 222906 18878 159935

Appendix

Reformatted income statement

Income statement

2017 2016 2015 2014 2013

Revenue

44492

7

42541

6

30440

5

26077

7

26629

8

Other income 5569 5586 4995 4953 5776

Fair value adjustment of biological assets 30931 21433 19946 12939 12256

Fair value adjustment of biological assets at point

of harvest 1381 -6322 1432 2113 -2469

Share of profits / (losses) of associates accounted

for using the equity method -43 -78 390 601 731

Changes in inventories of finished goods and work

in progress 648 1336 5312 1144 -7611

Total revenue

48341

3

44737

1

33648

0

28252

7

27498

1

Expenses

Raw materials and consumables used

25282

4

25173

4

16445

2

13756

1

13917

4

Contingent consideration expense 6727 0 0 0 0

Employee benefits expense 89633 80809 58631 50414 48499

Depreciation and amortisation expense 20935 21010 18368 15469 15532

Finance costs 8062 7374 4722 5067 5999

Other expenses 19676 17534 19432 15955 18275

Total expenses

39785

7

37846

1

26560

5

22446

6

22747

9

Profit before income tax expense 85556 68910 70875 58061 47502

Income tax expense 27473 20417 20883 17000 14045

Net profit for the period attributable to

members of the Company 58083 48493 49992 41061 33457

Reformatted balance sheet

Balance sheet

2017 2016 2015 2014 2013

Current Assets

Cash and cash equivalents 30561 12521 13324 7656 14998

Trade and other receivables 22120 25300 14034 7636 13349

Inventories 57194 55165 60151 53407 50150

Biological assets 31240 246102 222906 18878 159935

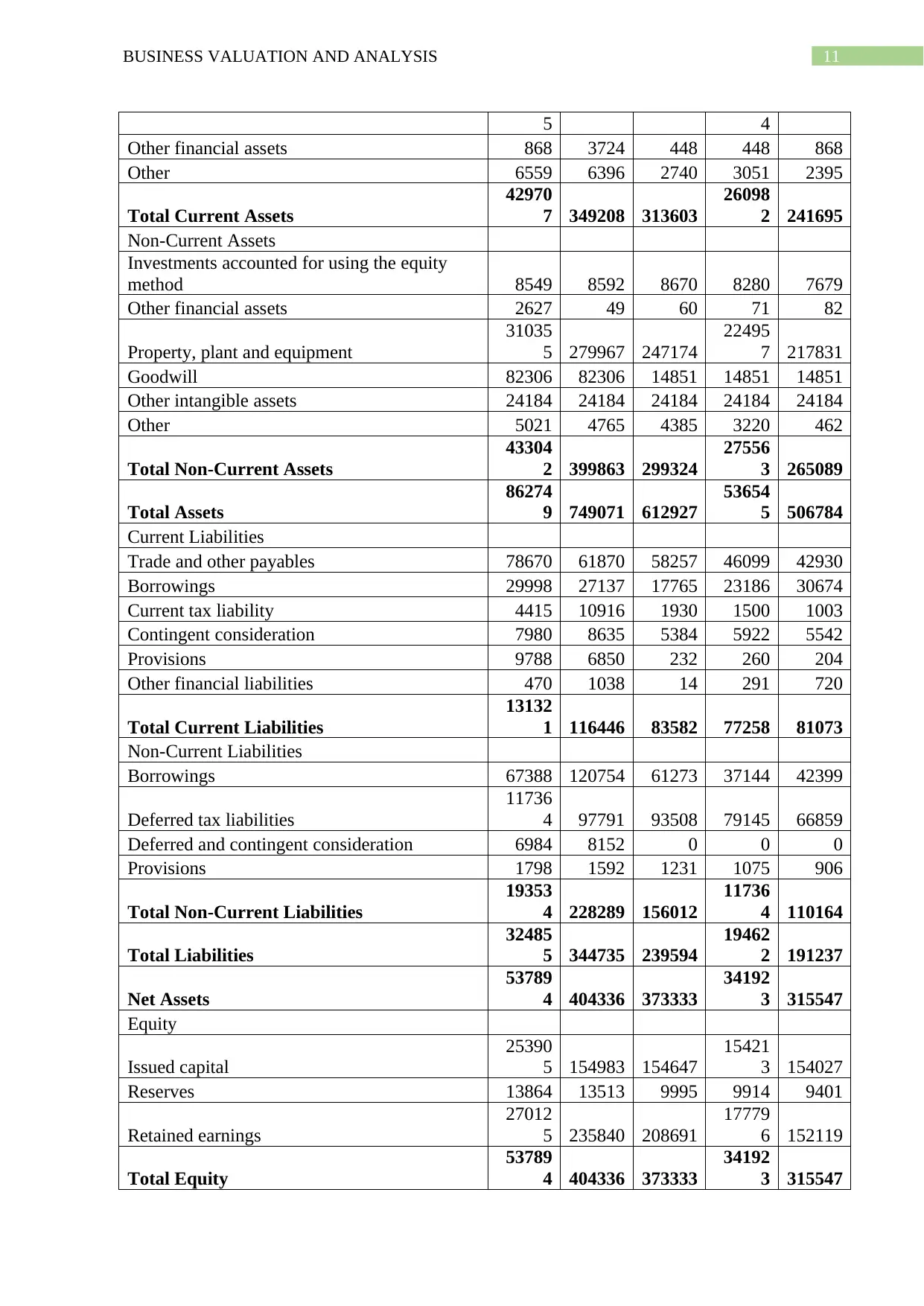

11BUSINESS VALUATION AND ANALYSIS

5 4

Other financial assets 868 3724 448 448 868

Other 6559 6396 2740 3051 2395

Total Current Assets

42970

7 349208 313603

26098

2 241695

Non-Current Assets

Investments accounted for using the equity

method 8549 8592 8670 8280 7679

Other financial assets 2627 49 60 71 82

Property, plant and equipment

31035

5 279967 247174

22495

7 217831

Goodwill 82306 82306 14851 14851 14851

Other intangible assets 24184 24184 24184 24184 24184

Other 5021 4765 4385 3220 462

Total Non-Current Assets

43304

2 399863 299324

27556

3 265089

Total Assets

86274

9 749071 612927

53654

5 506784

Current Liabilities

Trade and other payables 78670 61870 58257 46099 42930

Borrowings 29998 27137 17765 23186 30674

Current tax liability 4415 10916 1930 1500 1003

Contingent consideration 7980 8635 5384 5922 5542

Provisions 9788 6850 232 260 204

Other financial liabilities 470 1038 14 291 720

Total Current Liabilities

13132

1 116446 83582 77258 81073

Non-Current Liabilities

Borrowings 67388 120754 61273 37144 42399

Deferred tax liabilities

11736

4 97791 93508 79145 66859

Deferred and contingent consideration 6984 8152 0 0 0

Provisions 1798 1592 1231 1075 906

Total Non-Current Liabilities

19353

4 228289 156012

11736

4 110164

Total Liabilities

32485

5 344735 239594

19462

2 191237

Net Assets

53789

4 404336 373333

34192

3 315547

Equity

Issued capital

25390

5 154983 154647

15421

3 154027

Reserves 13864 13513 9995 9914 9401

Retained earnings

27012

5 235840 208691

17779

6 152119

Total Equity

53789

4 404336 373333

34192

3 315547

5 4

Other financial assets 868 3724 448 448 868

Other 6559 6396 2740 3051 2395

Total Current Assets

42970

7 349208 313603

26098

2 241695

Non-Current Assets

Investments accounted for using the equity

method 8549 8592 8670 8280 7679

Other financial assets 2627 49 60 71 82

Property, plant and equipment

31035

5 279967 247174

22495

7 217831

Goodwill 82306 82306 14851 14851 14851

Other intangible assets 24184 24184 24184 24184 24184

Other 5021 4765 4385 3220 462

Total Non-Current Assets

43304

2 399863 299324

27556

3 265089

Total Assets

86274

9 749071 612927

53654

5 506784

Current Liabilities

Trade and other payables 78670 61870 58257 46099 42930

Borrowings 29998 27137 17765 23186 30674

Current tax liability 4415 10916 1930 1500 1003

Contingent consideration 7980 8635 5384 5922 5542

Provisions 9788 6850 232 260 204

Other financial liabilities 470 1038 14 291 720

Total Current Liabilities

13132

1 116446 83582 77258 81073

Non-Current Liabilities

Borrowings 67388 120754 61273 37144 42399

Deferred tax liabilities

11736

4 97791 93508 79145 66859

Deferred and contingent consideration 6984 8152 0 0 0

Provisions 1798 1592 1231 1075 906

Total Non-Current Liabilities

19353

4 228289 156012

11736

4 110164

Total Liabilities

32485

5 344735 239594

19462

2 191237

Net Assets

53789

4 404336 373333

34192

3 315547

Equity

Issued capital

25390

5 154983 154647

15421

3 154027

Reserves 13864 13513 9995 9914 9401

Retained earnings

27012

5 235840 208691

17779

6 152119

Total Equity

53789

4 404336 373333

34192

3 315547

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.