Analysis of Share Buyback & Impairment Loss Accounting Practices

VerifiedAdded on 2023/06/05

|6

|1538

|184

Report

AI Summary

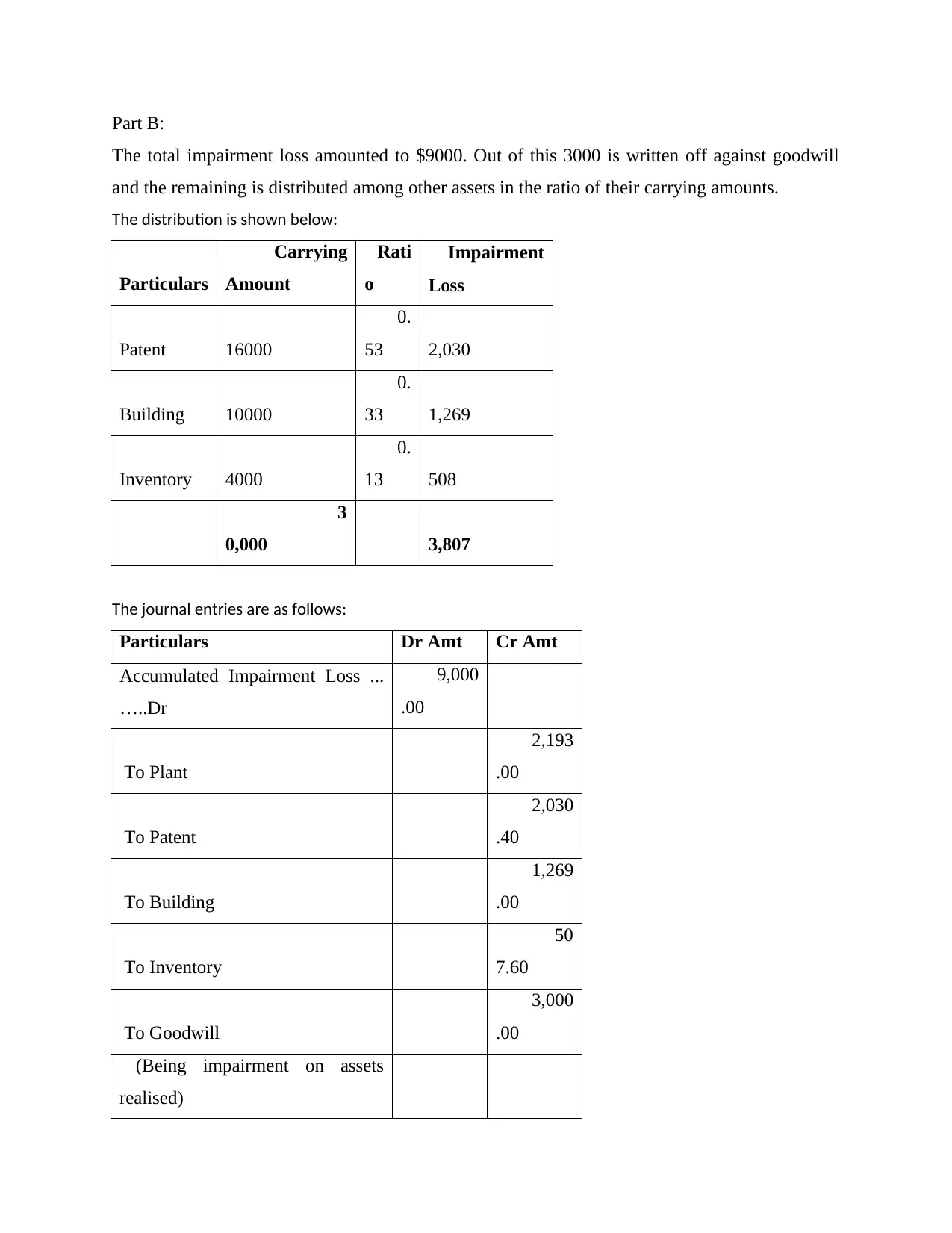

This report provides a detailed analysis of share buyback strategies and impairment loss accounting. It begins by explaining the concept of share buybacks, including the reasons why companies choose to repurchase their own shares, such as improving earnings per share, returning capital to shareholders, and optimizing capital structure. The report outlines the conditions for buybacks, including limitations on the amount, authorization requirements, and debt-equity ratio considerations. It also covers the accounting entries involved in share buybacks, including the treatment of premiums and the creation of a capital redemption reserve, and the disclosure requirements for financial reporting. Furthermore, the report discusses the implications of buybacks on a company's financial health and investor perception. The second part of the report deals with impairment loss accounting, providing a specific example of how an impairment loss is allocated across different assets, including goodwill, patents, buildings, and inventory, along with the corresponding journal entries. The report concludes by referencing relevant literature on financial statement analysis and corporate finance.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.