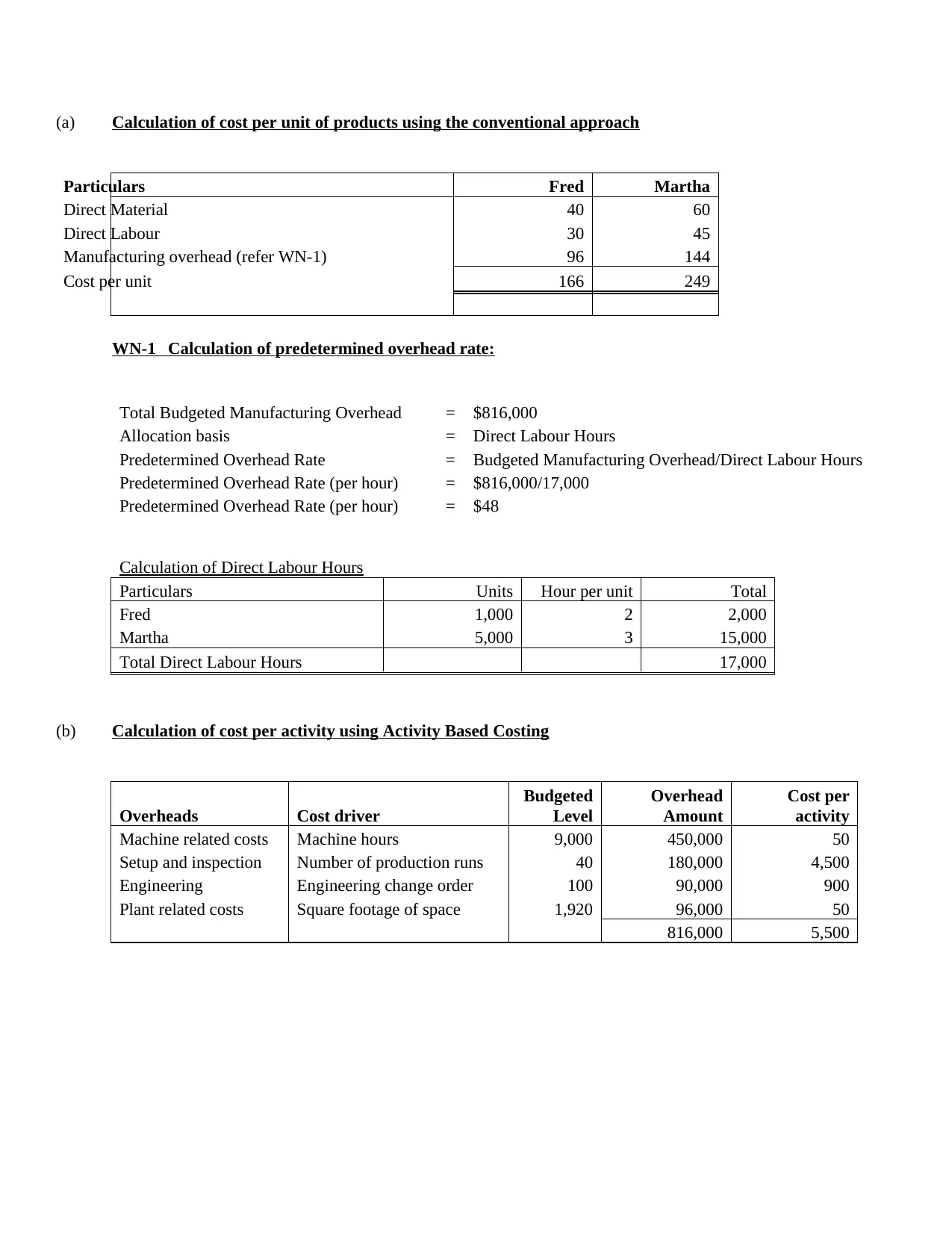

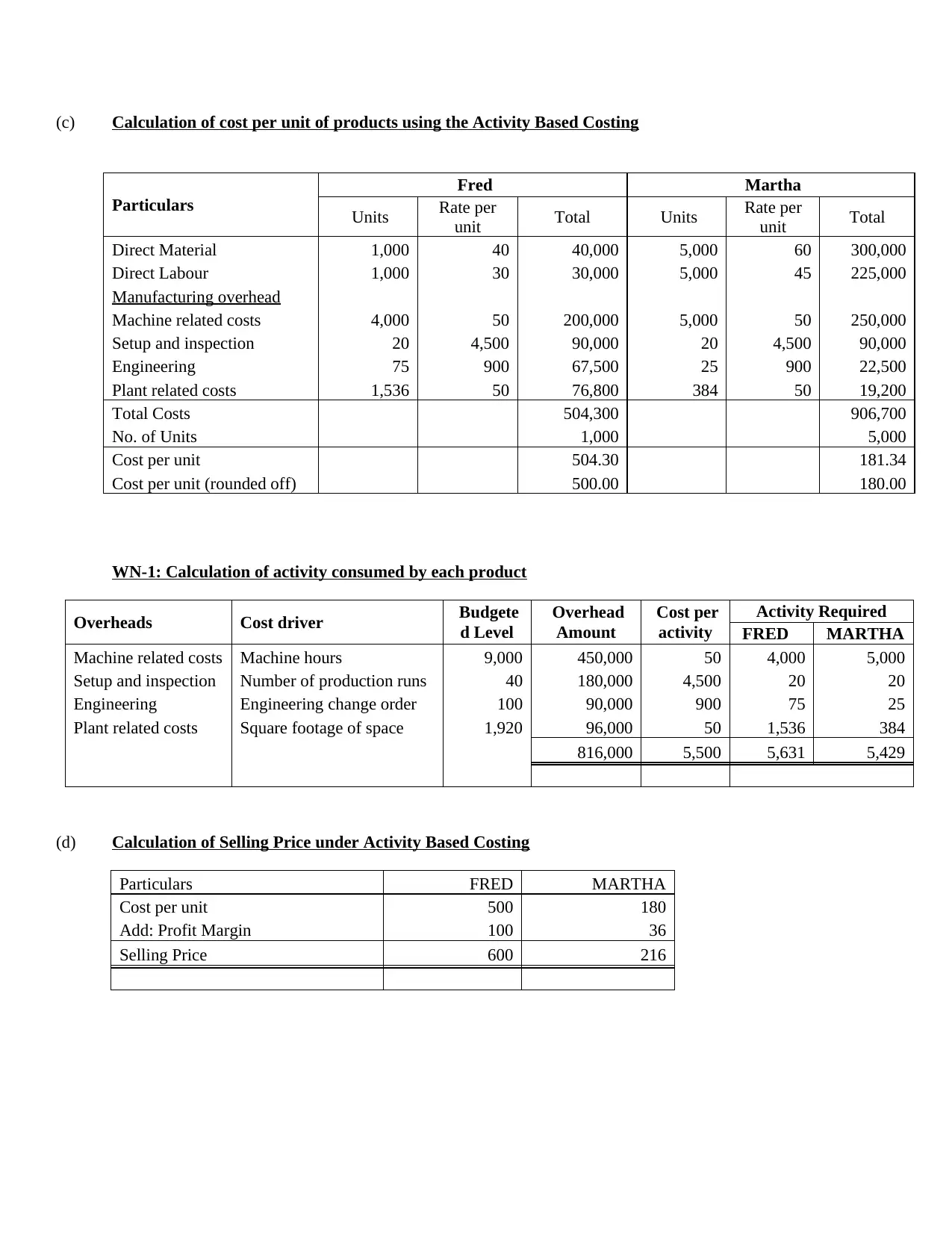

The assignment content discusses the difference between conventional and activity-based costing methods in determining the selling price of products. Under conventional approach, costs are allocated using a plant-wide allocation rate, which may not reflect actual resource consumption. Activity-based costing (ABC), on the other hand, allocates costs based on actual resources used in manufacturing, providing a more accurate picture of product costs. The example illustrates how ABC can lead to under-costing or over-costing of products compared to conventional approach. The advantages of ABC include improvement in process, scientific method of cost allocation, competitive pricing, and identification of costs at each level. However, the implementation costs, flaws in data, and lengthy process are some of the disadvantages of using ABC.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)