Financial Feasibility Analysis of Business Expansion Projects

VerifiedAdded on 2020/10/22

|9

|2154

|107

AI Summary

This assignment involves analyzing three different business expansion projects using financial feasibility analysis techniques. The existing business proposal, liquor proposal, and Rye Whisky project are evaluated based on their Net Present Value (NPV) and Internal Rate Of Return (IRR). The results show that the Rye Whisky project has the highest NPV and IRR, making it the most viable option for business expansion. The analysis is supported by references from academic journals and books in the field of finance and accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL FOR

BUSINESS DECISION

MAKING

BUSINESS DECISION

MAKING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

Calculation of NPV of projects...................................................................................................2

Outcomes form the analysis........................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Calculation of NPV of projects...................................................................................................2

Outcomes form the analysis........................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Financial information are considered important for financial decision making and

planning. It remain helpful for finance consultants and accountants to consolidate and correlate

the functions of business and functions of business with appropriate business decision making.

Lochside Liquors Limited (LLL) is a manufacturing organisation that sells premium Scotch

whisky under the brand name of “Highland Princess”. Management committee of this

organisation is seeking for business expansion plan for business which is to analyse with the

capital budgeting methods and streams. Overall case scenario is evaluated by implementing

investment appraisal techniques like NPV, IRR. Feasibility of investment projects evaluated with

peer comparison among available investment options.

Summary of the question

Chairman of Lochside Liquors Limited (LLL) is organised a meeting with its director

term members regarding proposed capital investment plan for expansion of business. The capital

expenditure budget is limited up to £500,000 which can not be exceed form the above limit.

Organisation has two business projects subject to expand Scotch Whisky Market in South Asia

and The Far East. One project is Whisky based liqueur to Drambuie and second project is a new

cheaper variety of Whisky made form rye.

Requirements for the projects

1. 50000 Sq. ft of space

2. An option of leasing out the section for £25000 a year to save the cost of building a new

shed.

3. Rend of the area will be £30000 (based upon 150000 sq. ft. for £90000 for a year)

4. Additional cost of renovating the section for a new project - £20000

5. Plant cost for Liqueur project as £140000 plus £20000 for shipping and installation

6. Plant cost for Rye project is £250000 plus £50000 of shipping and installation.

7. No salvage value for liqueur plant is Nil after five year whereas salvage value for

£40000 after five year.

8. Creditors will be increased by £10000, debtors will be increased by £5000 every year.

9. Contribution form Existing business is £4 contribution per bottle.

10. It is expected that the Highland princess sales will be reduced by 30000 bottles per

annum.

1

Financial information are considered important for financial decision making and

planning. It remain helpful for finance consultants and accountants to consolidate and correlate

the functions of business and functions of business with appropriate business decision making.

Lochside Liquors Limited (LLL) is a manufacturing organisation that sells premium Scotch

whisky under the brand name of “Highland Princess”. Management committee of this

organisation is seeking for business expansion plan for business which is to analyse with the

capital budgeting methods and streams. Overall case scenario is evaluated by implementing

investment appraisal techniques like NPV, IRR. Feasibility of investment projects evaluated with

peer comparison among available investment options.

Summary of the question

Chairman of Lochside Liquors Limited (LLL) is organised a meeting with its director

term members regarding proposed capital investment plan for expansion of business. The capital

expenditure budget is limited up to £500,000 which can not be exceed form the above limit.

Organisation has two business projects subject to expand Scotch Whisky Market in South Asia

and The Far East. One project is Whisky based liqueur to Drambuie and second project is a new

cheaper variety of Whisky made form rye.

Requirements for the projects

1. 50000 Sq. ft of space

2. An option of leasing out the section for £25000 a year to save the cost of building a new

shed.

3. Rend of the area will be £30000 (based upon 150000 sq. ft. for £90000 for a year)

4. Additional cost of renovating the section for a new project - £20000

5. Plant cost for Liqueur project as £140000 plus £20000 for shipping and installation

6. Plant cost for Rye project is £250000 plus £50000 of shipping and installation.

7. No salvage value for liqueur plant is Nil after five year whereas salvage value for

£40000 after five year.

8. Creditors will be increased by £10000, debtors will be increased by £5000 every year.

9. Contribution form Existing business is £4 contribution per bottle.

10. It is expected that the Highland princess sales will be reduced by 30000 bottles per

annum.

1

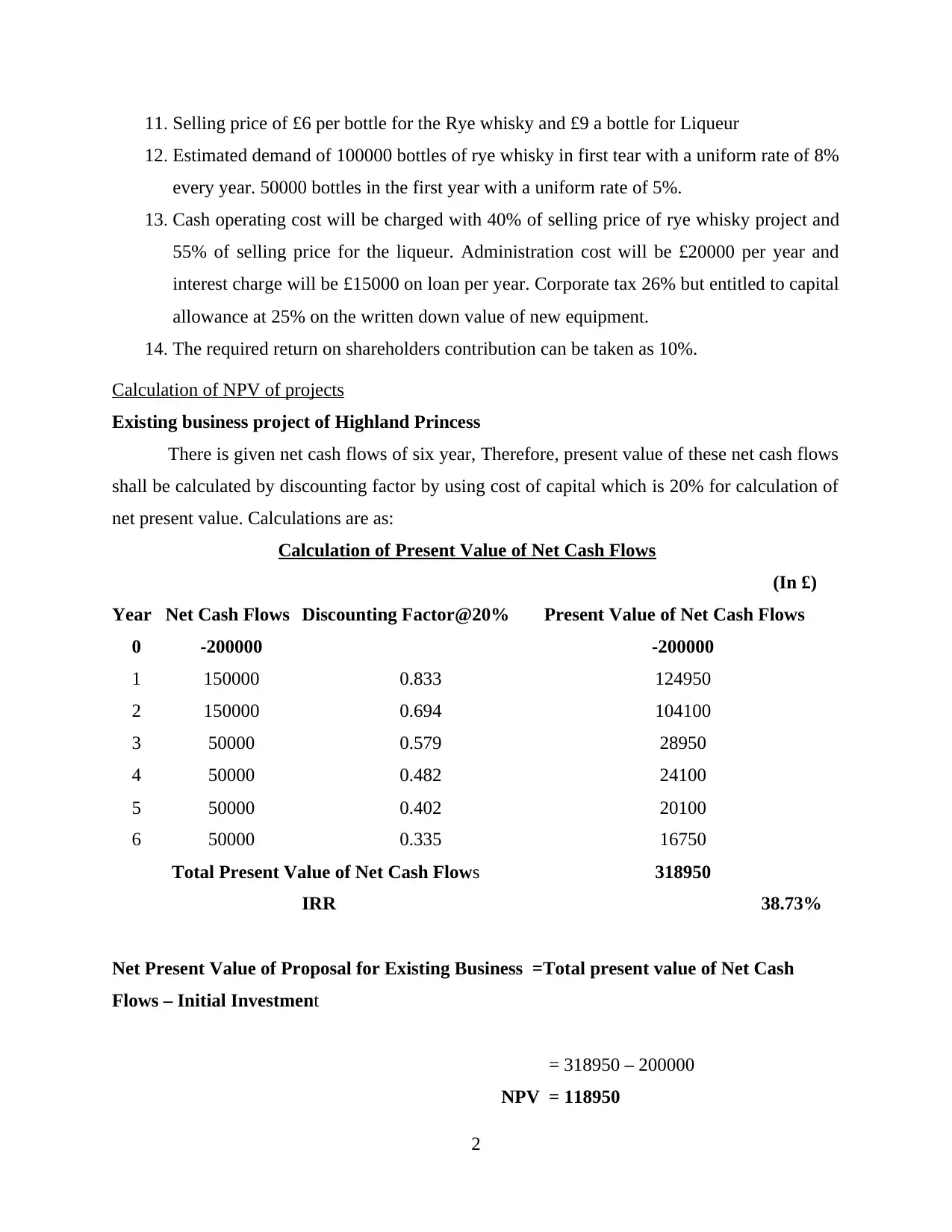

11. Selling price of £6 per bottle for the Rye whisky and £9 a bottle for Liqueur

12. Estimated demand of 100000 bottles of rye whisky in first tear with a uniform rate of 8%

every year. 50000 bottles in the first year with a uniform rate of 5%.

13. Cash operating cost will be charged with 40% of selling price of rye whisky project and

55% of selling price for the liqueur. Administration cost will be £20000 per year and

interest charge will be £15000 on loan per year. Corporate tax 26% but entitled to capital

allowance at 25% on the written down value of new equipment.

14. The required return on shareholders contribution can be taken as 10%.

Calculation of NPV of projects

Existing business project of Highland Princess

There is given net cash flows of six year, Therefore, present value of these net cash flows

shall be calculated by discounting factor by using cost of capital which is 20% for calculation of

net present value. Calculations are as:

Calculation of Present Value of Net Cash Flows

(In £)

Year Net Cash Flows Discounting Factor@20% Present Value of Net Cash Flows

0 -200000 -200000

1 150000 0.833 124950

2 150000 0.694 104100

3 50000 0.579 28950

4 50000 0.482 24100

5 50000 0.402 20100

6 50000 0.335 16750

Total Present Value of Net Cash Flows 318950

IRR 38.73%

Net Present Value of Proposal for Existing Business =Total present value of Net Cash

Flows – Initial Investment

= 318950 – 200000

NPV = 118950

2

12. Estimated demand of 100000 bottles of rye whisky in first tear with a uniform rate of 8%

every year. 50000 bottles in the first year with a uniform rate of 5%.

13. Cash operating cost will be charged with 40% of selling price of rye whisky project and

55% of selling price for the liqueur. Administration cost will be £20000 per year and

interest charge will be £15000 on loan per year. Corporate tax 26% but entitled to capital

allowance at 25% on the written down value of new equipment.

14. The required return on shareholders contribution can be taken as 10%.

Calculation of NPV of projects

Existing business project of Highland Princess

There is given net cash flows of six year, Therefore, present value of these net cash flows

shall be calculated by discounting factor by using cost of capital which is 20% for calculation of

net present value. Calculations are as:

Calculation of Present Value of Net Cash Flows

(In £)

Year Net Cash Flows Discounting Factor@20% Present Value of Net Cash Flows

0 -200000 -200000

1 150000 0.833 124950

2 150000 0.694 104100

3 50000 0.579 28950

4 50000 0.482 24100

5 50000 0.402 20100

6 50000 0.335 16750

Total Present Value of Net Cash Flows 318950

IRR 38.73%

Net Present Value of Proposal for Existing Business =Total present value of Net Cash

Flows – Initial Investment

= 318950 – 200000

NPV = 118950

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

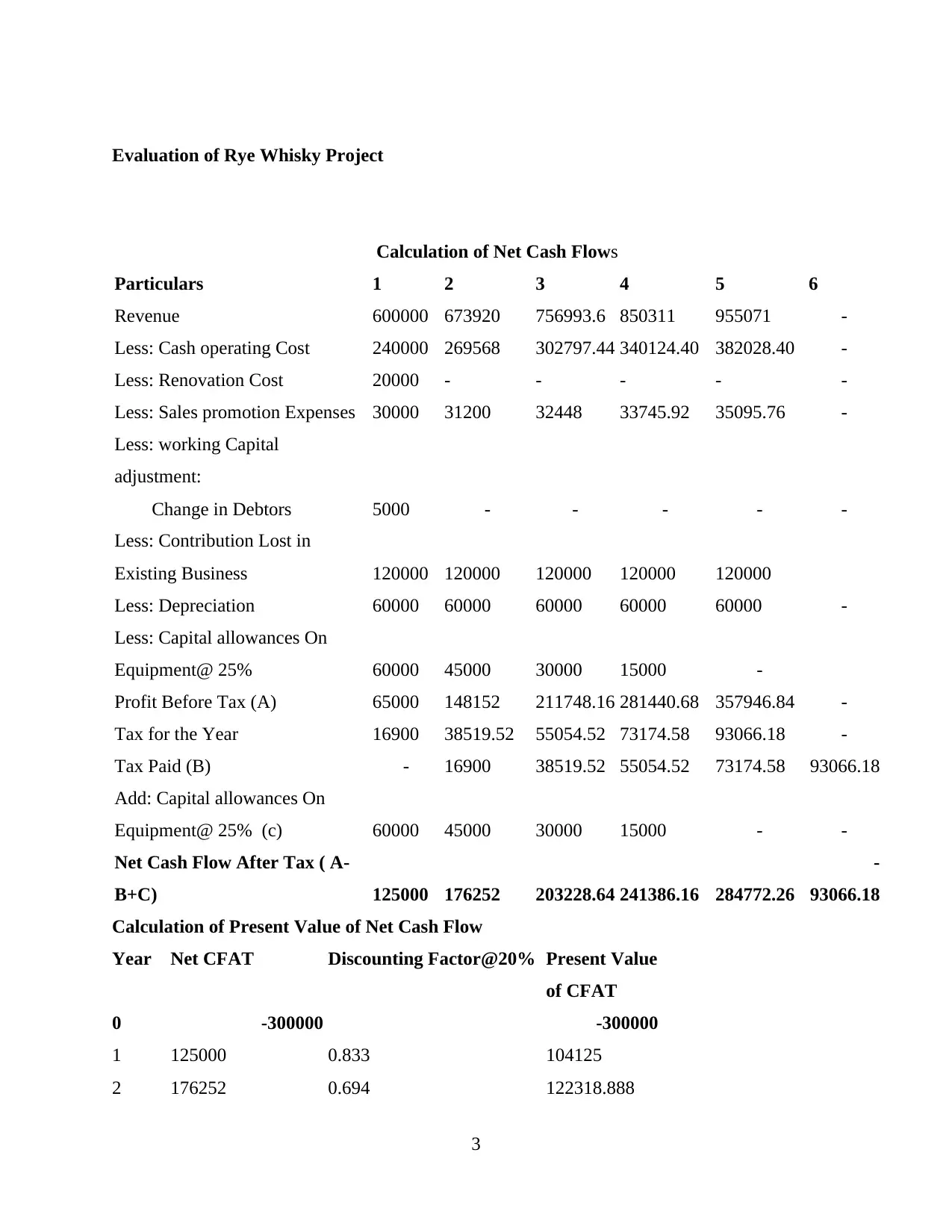

Evaluation of Rye Whisky Project

Calculation of Net Cash Flows

Particulars 1 2 3 4 5 6

Revenue 600000 673920 756993.6 850311 955071 -

Less: Cash operating Cost 240000 269568 302797.44 340124.40 382028.40 -

Less: Renovation Cost 20000 - - - - -

Less: Sales promotion Expenses 30000 31200 32448 33745.92 35095.76 -

Less: working Capital

adjustment:

Change in Debtors 5000 - - - - -

Less: Contribution Lost in

Existing Business 120000 120000 120000 120000 120000

Less: Depreciation 60000 60000 60000 60000 60000 -

Less: Capital allowances On

Equipment@ 25% 60000 45000 30000 15000 -

Profit Before Tax (A) 65000 148152 211748.16 281440.68 357946.84 -

Tax for the Year 16900 38519.52 55054.52 73174.58 93066.18 -

Tax Paid (B) - 16900 38519.52 55054.52 73174.58 93066.18

Add: Capital allowances On

Equipment@ 25% (c) 60000 45000 30000 15000 - -

Net Cash Flow After Tax ( A-

B+C) 125000 176252 203228.64 241386.16 284772.26

-

93066.18

Calculation of Present Value of Net Cash Flow

Year Net CFAT Discounting Factor@20% Present Value

of CFAT

0 -300000 -300000

1 125000 0.833 104125

2 176252 0.694 122318.888

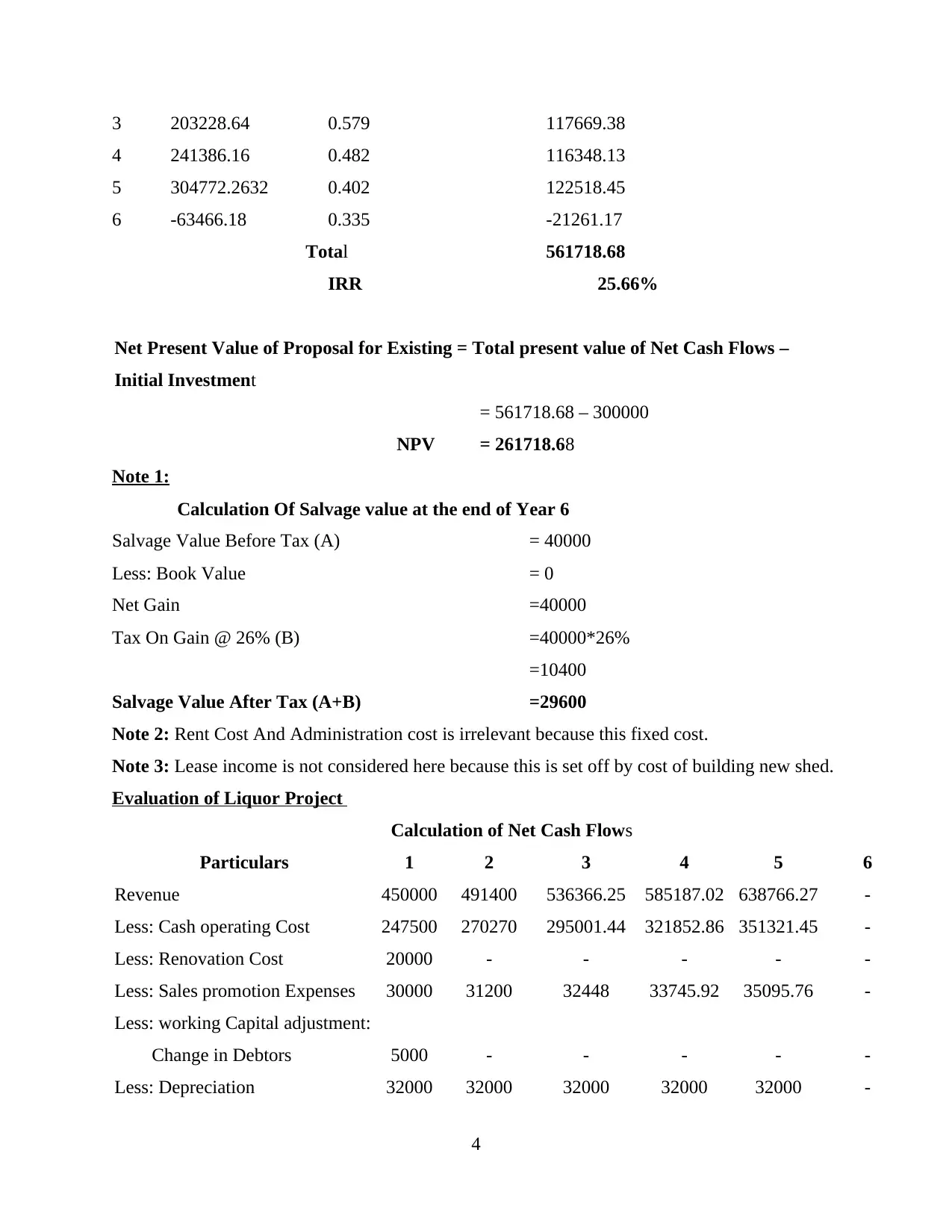

3

Calculation of Net Cash Flows

Particulars 1 2 3 4 5 6

Revenue 600000 673920 756993.6 850311 955071 -

Less: Cash operating Cost 240000 269568 302797.44 340124.40 382028.40 -

Less: Renovation Cost 20000 - - - - -

Less: Sales promotion Expenses 30000 31200 32448 33745.92 35095.76 -

Less: working Capital

adjustment:

Change in Debtors 5000 - - - - -

Less: Contribution Lost in

Existing Business 120000 120000 120000 120000 120000

Less: Depreciation 60000 60000 60000 60000 60000 -

Less: Capital allowances On

Equipment@ 25% 60000 45000 30000 15000 -

Profit Before Tax (A) 65000 148152 211748.16 281440.68 357946.84 -

Tax for the Year 16900 38519.52 55054.52 73174.58 93066.18 -

Tax Paid (B) - 16900 38519.52 55054.52 73174.58 93066.18

Add: Capital allowances On

Equipment@ 25% (c) 60000 45000 30000 15000 - -

Net Cash Flow After Tax ( A-

B+C) 125000 176252 203228.64 241386.16 284772.26

-

93066.18

Calculation of Present Value of Net Cash Flow

Year Net CFAT Discounting Factor@20% Present Value

of CFAT

0 -300000 -300000

1 125000 0.833 104125

2 176252 0.694 122318.888

3

3 203228.64 0.579 117669.38

4 241386.16 0.482 116348.13

5 304772.2632 0.402 122518.45

6 -63466.18 0.335 -21261.17

Total 561718.68

IRR 25.66%

Net Present Value of Proposal for Existing = Total present value of Net Cash Flows –

Initial Investment

= 561718.68 – 300000

NPV = 261718.68

Note 1:

Calculation Of Salvage value at the end of Year 6

Salvage Value Before Tax (A) = 40000

Less: Book Value = 0

Net Gain =40000

Tax On Gain @ 26% (B) =40000*26%

=10400

Salvage Value After Tax (A+B) =29600

Note 2: Rent Cost And Administration cost is irrelevant because this fixed cost.

Note 3: Lease income is not considered here because this is set off by cost of building new shed.

Evaluation of Liquor Project

Calculation of Net Cash Flows

Particulars 1 2 3 4 5 6

Revenue 450000 491400 536366.25 585187.02 638766.27 -

Less: Cash operating Cost 247500 270270 295001.44 321852.86 351321.45 -

Less: Renovation Cost 20000 - - - - -

Less: Sales promotion Expenses 30000 31200 32448 33745.92 35095.76 -

Less: working Capital adjustment:

Change in Debtors 5000 - - - - -

Less: Depreciation 32000 32000 32000 32000 32000 -

4

4 241386.16 0.482 116348.13

5 304772.2632 0.402 122518.45

6 -63466.18 0.335 -21261.17

Total 561718.68

IRR 25.66%

Net Present Value of Proposal for Existing = Total present value of Net Cash Flows –

Initial Investment

= 561718.68 – 300000

NPV = 261718.68

Note 1:

Calculation Of Salvage value at the end of Year 6

Salvage Value Before Tax (A) = 40000

Less: Book Value = 0

Net Gain =40000

Tax On Gain @ 26% (B) =40000*26%

=10400

Salvage Value After Tax (A+B) =29600

Note 2: Rent Cost And Administration cost is irrelevant because this fixed cost.

Note 3: Lease income is not considered here because this is set off by cost of building new shed.

Evaluation of Liquor Project

Calculation of Net Cash Flows

Particulars 1 2 3 4 5 6

Revenue 450000 491400 536366.25 585187.02 638766.27 -

Less: Cash operating Cost 247500 270270 295001.44 321852.86 351321.45 -

Less: Renovation Cost 20000 - - - - -

Less: Sales promotion Expenses 30000 31200 32448 33745.92 35095.76 -

Less: working Capital adjustment:

Change in Debtors 5000 - - - - -

Less: Depreciation 32000 32000 32000 32000 32000 -

4

Less: Capital allowances On

Equipment @ 25% 32000 24000 16000 8000 -

Profit Before Tax (A) 83500 133930 160916.81 189588.24 220349.06 -

Tax for the Year 21710 34821.8 41838.37 49292.94 57290.76 -

Tax Paid (B) - 21710 34821.8 41838.37 49292.94 57290.76

Add: Capital allowances On

Equipment @ 25% (c) 32000 24000 16000 8000 - -

Net Cash Flow After Tax ( A-

B+C) 115500 136220 142095.01 155749.87 171056.12 -57290.76

Calculation of Present Value of Net Cash Flow

Year Net CFAT Discounting

Factor@20%

Present Value

of CFAT

0 -160000 -160000

1 115500 0.833 96211.5

2 136220 0.694 94536.68

3 142095.01 0.579 82273.01

4 155749.87 0.482 75071.44

5 191056.12 0.402 76804.56

6 -57290.76 0.335 -19192.40

Total 405704.78

IRR 47.20%

Calculation of Present Value of Net Cash Flow

Year Net CFAT Discounting

Factor@20%

Present Value

of CFAT

0 -160000 -160000

1 115500 0.833 96211.5

2 136220 0.694 94536.68

3 142095.01 0.579 82273.01

4 155749.87 0.482 75071.44

5 191056.12 0.402 76804.56

5

Equipment @ 25% 32000 24000 16000 8000 -

Profit Before Tax (A) 83500 133930 160916.81 189588.24 220349.06 -

Tax for the Year 21710 34821.8 41838.37 49292.94 57290.76 -

Tax Paid (B) - 21710 34821.8 41838.37 49292.94 57290.76

Add: Capital allowances On

Equipment @ 25% (c) 32000 24000 16000 8000 - -

Net Cash Flow After Tax ( A-

B+C) 115500 136220 142095.01 155749.87 171056.12 -57290.76

Calculation of Present Value of Net Cash Flow

Year Net CFAT Discounting

Factor@20%

Present Value

of CFAT

0 -160000 -160000

1 115500 0.833 96211.5

2 136220 0.694 94536.68

3 142095.01 0.579 82273.01

4 155749.87 0.482 75071.44

5 191056.12 0.402 76804.56

6 -57290.76 0.335 -19192.40

Total 405704.78

IRR 47.20%

Calculation of Present Value of Net Cash Flow

Year Net CFAT Discounting

Factor@20%

Present Value

of CFAT

0 -160000 -160000

1 115500 0.833 96211.5

2 136220 0.694 94536.68

3 142095.01 0.579 82273.01

4 155749.87 0.482 75071.44

5 191056.12 0.402 76804.56

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

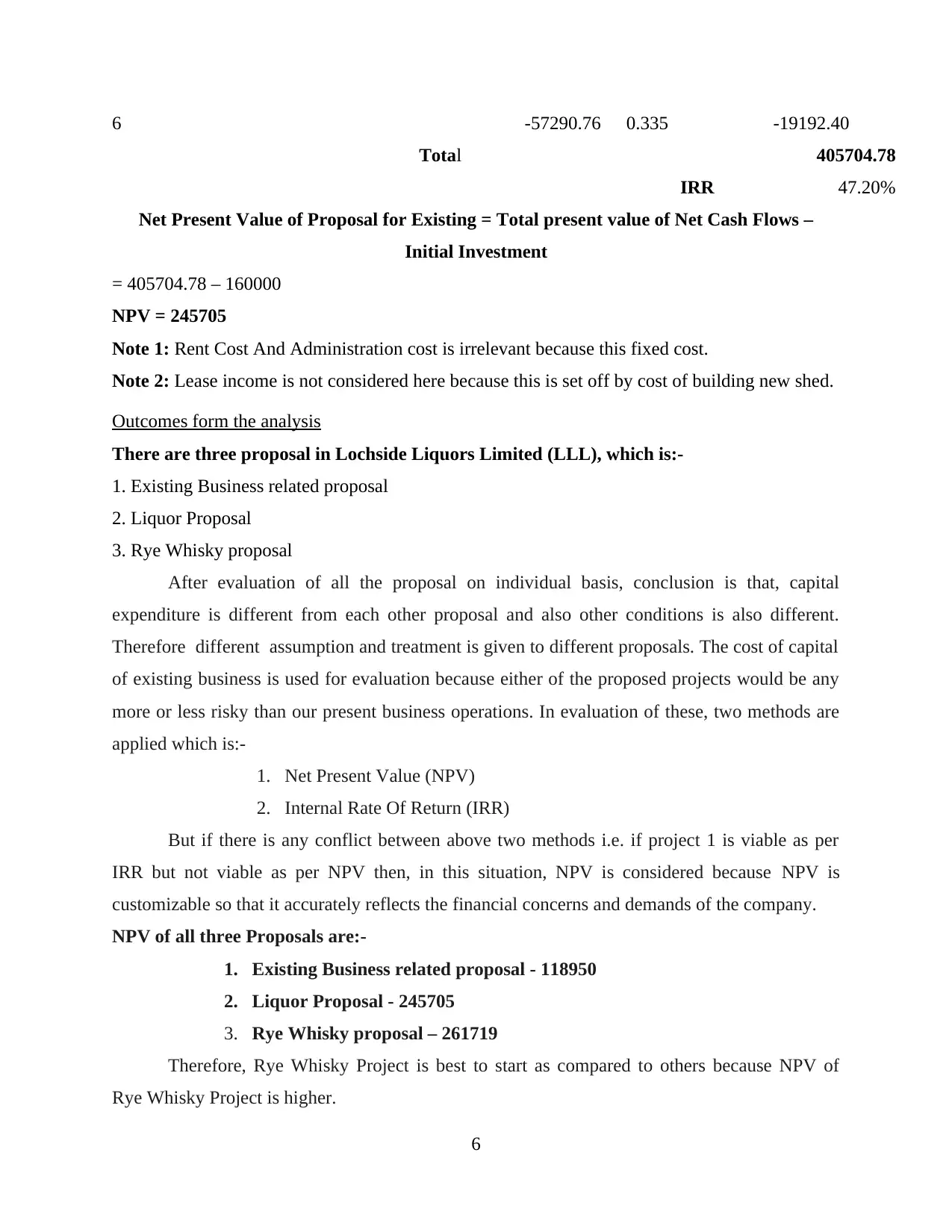

6 -57290.76 0.335 -19192.40

Total 405704.78

IRR 47.20%

Net Present Value of Proposal for Existing = Total present value of Net Cash Flows –

Initial Investment

= 405704.78 – 160000

NPV = 245705

Note 1: Rent Cost And Administration cost is irrelevant because this fixed cost.

Note 2: Lease income is not considered here because this is set off by cost of building new shed.

Outcomes form the analysis

There are three proposal in Lochside Liquors Limited (LLL), which is:-

1. Existing Business related proposal

2. Liquor Proposal

3. Rye Whisky proposal

After evaluation of all the proposal on individual basis, conclusion is that, capital

expenditure is different from each other proposal and also other conditions is also different.

Therefore different assumption and treatment is given to different proposals. The cost of capital

of existing business is used for evaluation because either of the proposed projects would be any

more or less risky than our present business operations. In evaluation of these, two methods are

applied which is:-

1. Net Present Value (NPV)

2. Internal Rate Of Return (IRR)

But if there is any conflict between above two methods i.e. if project 1 is viable as per

IRR but not viable as per NPV then, in this situation, NPV is considered because NPV is

customizable so that it accurately reflects the financial concerns and demands of the company.

NPV of all three Proposals are:-

1. Existing Business related proposal - 118950

2. Liquor Proposal - 245705

3. Rye Whisky proposal – 261719

Therefore, Rye Whisky Project is best to start as compared to others because NPV of

Rye Whisky Project is higher.

6

Total 405704.78

IRR 47.20%

Net Present Value of Proposal for Existing = Total present value of Net Cash Flows –

Initial Investment

= 405704.78 – 160000

NPV = 245705

Note 1: Rent Cost And Administration cost is irrelevant because this fixed cost.

Note 2: Lease income is not considered here because this is set off by cost of building new shed.

Outcomes form the analysis

There are three proposal in Lochside Liquors Limited (LLL), which is:-

1. Existing Business related proposal

2. Liquor Proposal

3. Rye Whisky proposal

After evaluation of all the proposal on individual basis, conclusion is that, capital

expenditure is different from each other proposal and also other conditions is also different.

Therefore different assumption and treatment is given to different proposals. The cost of capital

of existing business is used for evaluation because either of the proposed projects would be any

more or less risky than our present business operations. In evaluation of these, two methods are

applied which is:-

1. Net Present Value (NPV)

2. Internal Rate Of Return (IRR)

But if there is any conflict between above two methods i.e. if project 1 is viable as per

IRR but not viable as per NPV then, in this situation, NPV is considered because NPV is

customizable so that it accurately reflects the financial concerns and demands of the company.

NPV of all three Proposals are:-

1. Existing Business related proposal - 118950

2. Liquor Proposal - 245705

3. Rye Whisky proposal – 261719

Therefore, Rye Whisky Project is best to start as compared to others because NPV of

Rye Whisky Project is higher.

6

CONCLUSION

The above project is prepared to analyse the feasibility of projects and plans in order to

expand the business in near future. Business expansion project plans are evaluated with practical

based case scenario. With the analysis of investment appraisal technique such as NPV and IRR it

is analysed that organisation be able to analyse the potential cost of operations in more effective

style.

7

The above project is prepared to analyse the feasibility of projects and plans in order to

expand the business in near future. Business expansion project plans are evaluated with practical

based case scenario. With the analysis of investment appraisal technique such as NPV and IRR it

is analysed that organisation be able to analyse the potential cost of operations in more effective

style.

7

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.