An Analysis of the Capital Asset Pricing Model (CAPM)

VerifiedAdded on 2021/05/27

|15

|3664

|89

Report

AI Summary

This report provides a comprehensive analysis of the Capital Asset Pricing Model (CAPM), a financial model used to evaluate the relationship between expected returns and risks associated with investments. The report defines CAPM, explains its formula, and illustrates its application with a practical calculation example. It delves into the model's key assumptions, such as diversified portfolios and a perfect capital market, while also acknowledging their limitations in the real world. The report critically examines the criticisms and limitations of CAPM, including its unrealistic assumptions and statistical deficiencies. Furthermore, it explores alternative models like the Intertemporal Capital Asset Pricing Model (ICAPM) and the Consumption Capital Asset Pricing Model (CCAPM) to address CAPM's shortcomings. The report also discusses other asset pricing models, such as Arbitrage Pricing Theory (APT) and the Three-Factor Model, offering a broader perspective on investment analysis. Overall, the report offers valuable insights into the CAPM model, its applications, and its place in the financial world.

CAPM 1

Capital asset pricing model (CAPM)

by Student Name

The Name of the Class (Course)

Professor

The Name of the University

The City & State

Date

Capital asset pricing model (CAPM)

by Student Name

The Name of the Class (Course)

Professor

The Name of the University

The City & State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPM 2

Capital asset pricing model (CAPM)

Introduction

The Capital asset pricing model (CAPM) is a beneficial model, and it is used widely in the

industry even though it is based on extreme assumptions. In line with this statement, this

paper seeks to investigate on the issues surrounding CAPM as a financial/ investment concept

heavily relied upon by the investors in the economic and investment markets. Specifically,

the study seeks to address the specific issues surrounding CAPM such as its definition, key

assumptions, criticisms and limitations, other alternative financial models that can be used in

place of CAPM and the application of CAPM.

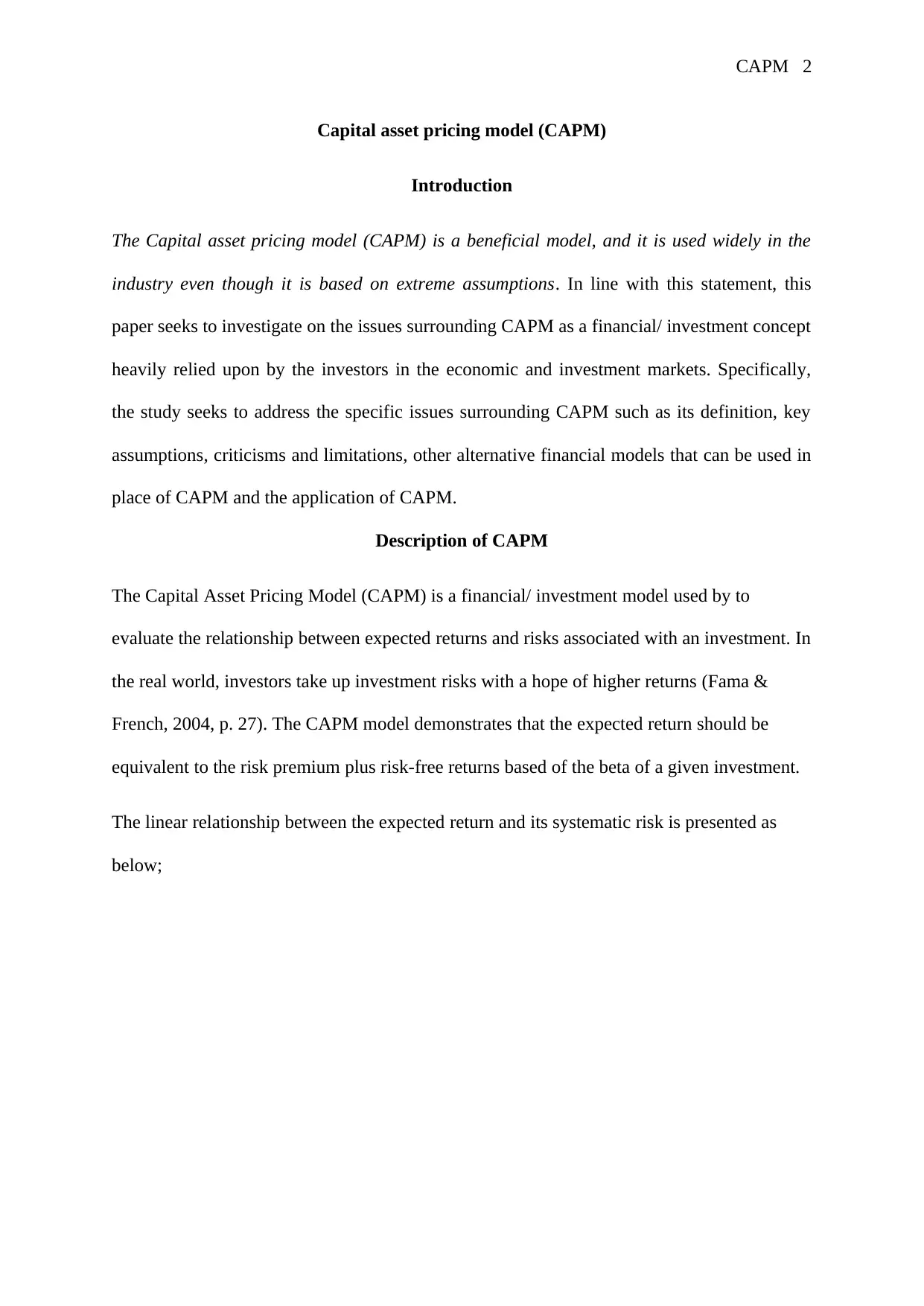

Description of CAPM

The Capital Asset Pricing Model (CAPM) is a financial/ investment model used by to

evaluate the relationship between expected returns and risks associated with an investment. In

the real world, investors take up investment risks with a hope of higher returns (Fama &

French, 2004, p. 27). The CAPM model demonstrates that the expected return should be

equivalent to the risk premium plus risk-free returns based of the beta of a given investment.

The linear relationship between the expected return and its systematic risk is presented as

below;

Capital asset pricing model (CAPM)

Introduction

The Capital asset pricing model (CAPM) is a beneficial model, and it is used widely in the

industry even though it is based on extreme assumptions. In line with this statement, this

paper seeks to investigate on the issues surrounding CAPM as a financial/ investment concept

heavily relied upon by the investors in the economic and investment markets. Specifically,

the study seeks to address the specific issues surrounding CAPM such as its definition, key

assumptions, criticisms and limitations, other alternative financial models that can be used in

place of CAPM and the application of CAPM.

Description of CAPM

The Capital Asset Pricing Model (CAPM) is a financial/ investment model used by to

evaluate the relationship between expected returns and risks associated with an investment. In

the real world, investors take up investment risks with a hope of higher returns (Fama &

French, 2004, p. 27). The CAPM model demonstrates that the expected return should be

equivalent to the risk premium plus risk-free returns based of the beta of a given investment.

The linear relationship between the expected return and its systematic risk is presented as

below;

CAPM 3

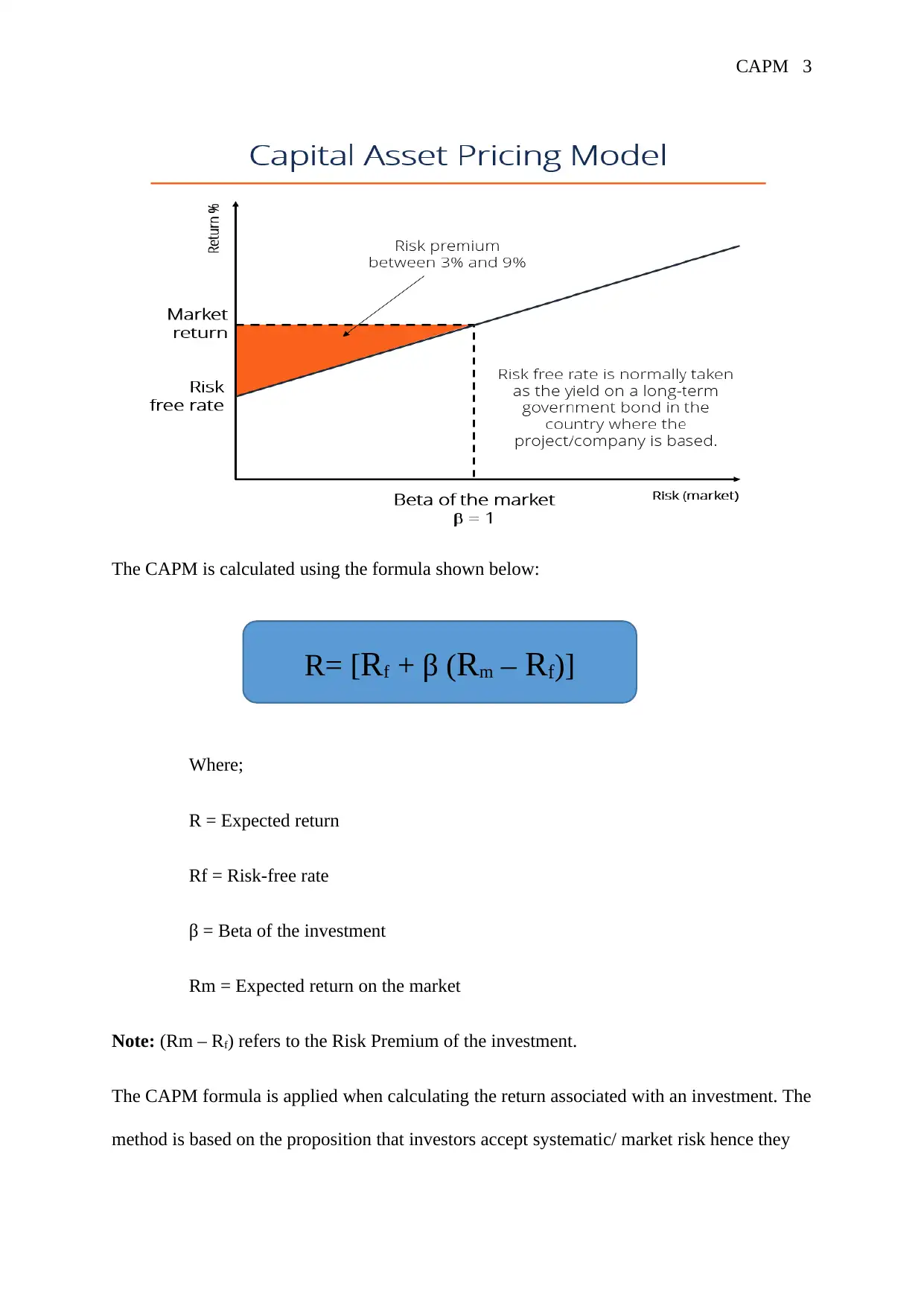

The CAPM is calculated using the formula shown below:

Where;

R = Expected return

Rf = Risk-free rate

β = Beta of the investment

Rm = Expected return on the market

Note: (Rm – Rf) refers to the Risk Premium of the investment.

The CAPM formula is applied when calculating the return associated with an investment. The

method is based on the proposition that investors accept systematic/ market risk hence they

R= [Rf + β (Rm – Rf)]

The CAPM is calculated using the formula shown below:

Where;

R = Expected return

Rf = Risk-free rate

β = Beta of the investment

Rm = Expected return on the market

Note: (Rm – Rf) refers to the Risk Premium of the investment.

The CAPM formula is applied when calculating the return associated with an investment. The

method is based on the proposition that investors accept systematic/ market risk hence they

R= [Rf + β (Rm – Rf)]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPM 4

should be compensated using risk premium. In simple terms, investors expect higher returns

for taking additional risks after investing in an asset (Graham & Harvey, 2001, p. 190).

The CAPM variables cab be defined as below:

a) Expected return (R): The notation "R" stands for the expected return from a capital

investment over time. The expected return is dependent on the other three variables.

According to the CAPM model, the expected return is measured using a long-term

period, for example, the entire life of the capital asset (Ang, et al., 2006, p. 261).

b) Risk-free rate (Rf): The notation "Rf" represent risk-free rate which is equivalent to

the return from a 10-year government bond. A 10-year bond is mostly used to

measure the risk-free rate associated with a capital investment because it is most

liquid and heavily quoted in the investment market (Lewellen & Nagel, 2006, p. 300).

c) Beta (β): The notation "β" represents beta which measures the degree of risks

associated with a stock. Beta can be obtained by establishing the degree at which the

price of a stock fluctuates relative to the market price. For example, if the beta of a

company is 1.5 relative to the market's 1, therefore the company has a volatility rate

of 150%. In other words, beta measures the sensitivity of an investment to the market

risks.

d) Premium market risk (Rm): The notation "Rm" represents the premium market risk

which is obtained by subtracting the risk-free rate from the expected return. The

variable represents the excess return that an investor would realize by accepting

additional investment risk (Banz, 1981, p. 12).

CAPM calculation

Suppose you have been provided with the following information:

A stock trades in the Singapore stock exchange market.

should be compensated using risk premium. In simple terms, investors expect higher returns

for taking additional risks after investing in an asset (Graham & Harvey, 2001, p. 190).

The CAPM variables cab be defined as below:

a) Expected return (R): The notation "R" stands for the expected return from a capital

investment over time. The expected return is dependent on the other three variables.

According to the CAPM model, the expected return is measured using a long-term

period, for example, the entire life of the capital asset (Ang, et al., 2006, p. 261).

b) Risk-free rate (Rf): The notation "Rf" represent risk-free rate which is equivalent to

the return from a 10-year government bond. A 10-year bond is mostly used to

measure the risk-free rate associated with a capital investment because it is most

liquid and heavily quoted in the investment market (Lewellen & Nagel, 2006, p. 300).

c) Beta (β): The notation "β" represents beta which measures the degree of risks

associated with a stock. Beta can be obtained by establishing the degree at which the

price of a stock fluctuates relative to the market price. For example, if the beta of a

company is 1.5 relative to the market's 1, therefore the company has a volatility rate

of 150%. In other words, beta measures the sensitivity of an investment to the market

risks.

d) Premium market risk (Rm): The notation "Rm" represents the premium market risk

which is obtained by subtracting the risk-free rate from the expected return. The

variable represents the excess return that an investor would realize by accepting

additional investment risk (Banz, 1981, p. 12).

CAPM calculation

Suppose you have been provided with the following information:

A stock trades in the Singapore stock exchange market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPM 5

Its current yield based on a ten year Singapore bond is 3.5%.

Historically the stock has an annual return of 6.5%.

The stock has a beta of 1.26.

Calculate the expected return on the investment using the CAPM formula.

Expected return = [Risk Free Rate + (Beta x Market Return Premium)]

R= [Rf + β (Rm – Rf)]

R= [Rf + β (Rm – Rf)]

R= 3.5% + [1.26 x 6.5%]

R= 11.69%

Therefore, the expected return on the investment is 11.9%.

CAPM Assumptions

The CAPM model has received criticism from different quarters because of its unrealistic

assumptions. This section discusses the four main assumptions of CAPM and their

applicability in the real world. The premises are:

First, Investors hold diversified portfolios. The assumption states that investors should rely on

systematic risk when choosing an investment portfolio. The unsystematic risk is ignored

because it is diversified (Sharpe, 1964, p. 427).

In the real world, it is impossible for investors to hold an entire market portfolio. However, it

is inexpensive and more manageable for investors to diversify unsystematic risk which offers

an opportunity for an expected return to relying entirely on the systematic risk. Therefore the

assumption is reasonable where investors only focus on acquiring systematic risk for

financial compensation (Kellerhals, 2013, p. 76).

Its current yield based on a ten year Singapore bond is 3.5%.

Historically the stock has an annual return of 6.5%.

The stock has a beta of 1.26.

Calculate the expected return on the investment using the CAPM formula.

Expected return = [Risk Free Rate + (Beta x Market Return Premium)]

R= [Rf + β (Rm – Rf)]

R= [Rf + β (Rm – Rf)]

R= 3.5% + [1.26 x 6.5%]

R= 11.69%

Therefore, the expected return on the investment is 11.9%.

CAPM Assumptions

The CAPM model has received criticism from different quarters because of its unrealistic

assumptions. This section discusses the four main assumptions of CAPM and their

applicability in the real world. The premises are:

First, Investors hold diversified portfolios. The assumption states that investors should rely on

systematic risk when choosing an investment portfolio. The unsystematic risk is ignored

because it is diversified (Sharpe, 1964, p. 427).

In the real world, it is impossible for investors to hold an entire market portfolio. However, it

is inexpensive and more manageable for investors to diversify unsystematic risk which offers

an opportunity for an expected return to relying entirely on the systematic risk. Therefore the

assumption is reasonable where investors only focus on acquiring systematic risk for

financial compensation (Kellerhals, 2013, p. 76).

CAPM 6

Second, single-period transaction horizon. CAPM model prefers to apply a standardized

period for different investments for comparability purposes. In other words, returns realized

from a six-month investment cannot be compared to returns realized from a twelve-month

investment. CAPM usually uses a one year as a universally acceptable holding period (Fama

& French, 2006, p. 2172).

In the real world, a single period transaction horizon is reasonable. Although investors hold

investment portfolio for at least one year, the returns are disclosed on an annual basis.

Therefore, using a one year horizon period realistic in the investment market.

Third, investors can borrow and lend at the risk-free rate of return. The assumption was

developed from the portfolio theory which was used to establish the CAPM model as well. In

other words, investors can borrow and lend freely without worrying about additional risk

(Bailey, 2005, p. 132).

However, the assumption cannot hold in the real world. In the investment market, the risk

associated with individual investments is higher compared to the risk associated with the

government investments. Therefore, in the real world, there is no possibility of borrowing and

lending at a risk-free rate. The inability to borrow and lend at a risk-free rate makes the

assumption unrealistic.

Fourth the capital market is perfect. The assumption means that investments in the market are

valued correctly. An ideal market is associated with the following attributes. First, there are

no transaction costs and taxes related to investments. Second, information can be freely

accessed by all investors at the same time. Third, all investors in the market are well informed

about the risk. Fourth, all investors are rational decision-makers and possess the desire to

maximize the return from their securities. And fifth, the market has many sellers and buyers

(Economou, et al., 2017).

Second, single-period transaction horizon. CAPM model prefers to apply a standardized

period for different investments for comparability purposes. In other words, returns realized

from a six-month investment cannot be compared to returns realized from a twelve-month

investment. CAPM usually uses a one year as a universally acceptable holding period (Fama

& French, 2006, p. 2172).

In the real world, a single period transaction horizon is reasonable. Although investors hold

investment portfolio for at least one year, the returns are disclosed on an annual basis.

Therefore, using a one year horizon period realistic in the investment market.

Third, investors can borrow and lend at the risk-free rate of return. The assumption was

developed from the portfolio theory which was used to establish the CAPM model as well. In

other words, investors can borrow and lend freely without worrying about additional risk

(Bailey, 2005, p. 132).

However, the assumption cannot hold in the real world. In the investment market, the risk

associated with individual investments is higher compared to the risk associated with the

government investments. Therefore, in the real world, there is no possibility of borrowing and

lending at a risk-free rate. The inability to borrow and lend at a risk-free rate makes the

assumption unrealistic.

Fourth the capital market is perfect. The assumption means that investments in the market are

valued correctly. An ideal market is associated with the following attributes. First, there are

no transaction costs and taxes related to investments. Second, information can be freely

accessed by all investors at the same time. Third, all investors in the market are well informed

about the risk. Fourth, all investors are rational decision-makers and possess the desire to

maximize the return from their securities. And fifth, the market has many sellers and buyers

(Economou, et al., 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPM 7

The perfect capital market assumption allows the CAPM model to present a relationship

between expected return and systematic risk. Although the assumption work in an idealized

world, it does not give the same results in the real world.

In the real-world capital markets are not perfect. In developed investment markets,

information is not freely available to the investment. Realistically, information is sold to the

highest buyers. Likewise, capital markets are characterized by transaction costs and taxes.

Lastly, the price of securities, as well as the revenues associated with such securities, cannot

be estimated accurately making it challenging to present a relationship between expected

return and systematic risk (Levy, 2012, p. 45).

Overall while some assumptions are unrealistic, some are realistic. Although most of the

assumptions make sense when applied in the idealized world, there is a possibility of

implementing them in the real world to obtain a linear relationship between expected return

and systematic risk (Kothari Et Al., 1995, p. 197).

Critique of CAPM

The CAPM's assumptions make the model unrealistic and difficult to apply in the real world.

The real capital market does not comprise of assumptions. For instance, free capital markets

do not exist; risk-free lending and borrowing is not realistic; different securities have

different taxes; not all investors are rational when it comes to decision making, and the

information is not free. The assumptions have been used as the basis for criticizing the

CAPM model.

According to Roll (1977), the CAPM is incorrect, and the model cannot be tested when the

real market portfolio is unknown. Roll used a proxy market (S&P 500) to justify the problems

associated with the CAPM model. First, when the S&P 500 proved to be efficient, the market

The perfect capital market assumption allows the CAPM model to present a relationship

between expected return and systematic risk. Although the assumption work in an idealized

world, it does not give the same results in the real world.

In the real-world capital markets are not perfect. In developed investment markets,

information is not freely available to the investment. Realistically, information is sold to the

highest buyers. Likewise, capital markets are characterized by transaction costs and taxes.

Lastly, the price of securities, as well as the revenues associated with such securities, cannot

be estimated accurately making it challenging to present a relationship between expected

return and systematic risk (Levy, 2012, p. 45).

Overall while some assumptions are unrealistic, some are realistic. Although most of the

assumptions make sense when applied in the idealized world, there is a possibility of

implementing them in the real world to obtain a linear relationship between expected return

and systematic risk (Kothari Et Al., 1995, p. 197).

Critique of CAPM

The CAPM's assumptions make the model unrealistic and difficult to apply in the real world.

The real capital market does not comprise of assumptions. For instance, free capital markets

do not exist; risk-free lending and borrowing is not realistic; different securities have

different taxes; not all investors are rational when it comes to decision making, and the

information is not free. The assumptions have been used as the basis for criticizing the

CAPM model.

According to Roll (1977), the CAPM is incorrect, and the model cannot be tested when the

real market portfolio is unknown. Roll used a proxy market (S&P 500) to justify the problems

associated with the CAPM model. First, when the S&P 500 proved to be efficient, the market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPM 8

portfolio was not. And second, there was no explanation for the market portfolio is efficient

when S&P 500 was inefficient.

The attempt by CAPM to measure the relationship between the expected revenue and beta

values as single equity is unrealistic. Market index (S&P 500) comprises of the index of all

securities and not a single entity. A market index should comprise of bonds, foreign assets,

tangible or intangible human capital and property. Unless the market portfolio is known, the

accuracy and efficiency of the CAPM model cannot be ascertained (Fama & French, 1993, p.

34).

According to Jeng (2018, p. 178), CAPM model is affected by the statistical deficiency. By

ignoring risks such as P/E ratio, book-to-market equity value and company size make it

difficult to prove the accuracy of the model.

The findings by Roll (1977) was also supported by Jagannathan and McGrattan (1995). The

study found out that the CAPM model is inappropriate as a result of its assumptions. A real

market should comprise of all factors in the economy. CAPM does not capture intangible

assets like human capital which profoundly influence the performance of an investment in a

capital market.

New directions to resolve challenges

Two models were developed to address the challenges experienced under CAPM. The

models are the Intertemporal Capital Asset Pricing Model (ICAPM) and the Consumption

Capital Asset Pricing Model (CCAPM).

a) Intertemporal Capital Asset Pricing Model (ICAPM)

Merton developed ICAPM in 1973 as an improved version of CAPM. ICPAM takes into

account the time-varying factors. The model assumes that investors take into account the

portfolio was not. And second, there was no explanation for the market portfolio is efficient

when S&P 500 was inefficient.

The attempt by CAPM to measure the relationship between the expected revenue and beta

values as single equity is unrealistic. Market index (S&P 500) comprises of the index of all

securities and not a single entity. A market index should comprise of bonds, foreign assets,

tangible or intangible human capital and property. Unless the market portfolio is known, the

accuracy and efficiency of the CAPM model cannot be ascertained (Fama & French, 1993, p.

34).

According to Jeng (2018, p. 178), CAPM model is affected by the statistical deficiency. By

ignoring risks such as P/E ratio, book-to-market equity value and company size make it

difficult to prove the accuracy of the model.

The findings by Roll (1977) was also supported by Jagannathan and McGrattan (1995). The

study found out that the CAPM model is inappropriate as a result of its assumptions. A real

market should comprise of all factors in the economy. CAPM does not capture intangible

assets like human capital which profoundly influence the performance of an investment in a

capital market.

New directions to resolve challenges

Two models were developed to address the challenges experienced under CAPM. The

models are the Intertemporal Capital Asset Pricing Model (ICAPM) and the Consumption

Capital Asset Pricing Model (CCAPM).

a) Intertemporal Capital Asset Pricing Model (ICAPM)

Merton developed ICAPM in 1973 as an improved version of CAPM. ICPAM takes into

account the time-varying factors. The model assumes that investors take into account the

CAPM 9

current and future risk factors like inflation, unemployment rate and future returns (Riley,

2009).

Considering that investors' appetite for risk varies, the ICAPM model a men variance analysis

to mitigate projected risk from one investor to another. The mean-variance analysis makes it

easier to arrive at a normal distribution of risk over time. Lastly, ICAPM formula comprises

of several beta coefficients representing different hedging portfolios (Berk, 1995, p. 281).

The ICAPM formula is:

Ri = Rf + β*(Rm-Rf) + βj*(Rn – Rf)

Where:

Ri = Expected return

Rf = Risk-free rate

Rm = Return on the market portfolio and

Rn = Expected return on the hedging

β = Measure of systematic risk concerning the market portfolio

βj= Represents the measure of volatility concerning the hedging security

b) Consumption Capital Asset Pricing Model (CCAPM)

Breeden created the CCAPM in 1979 as an improved version of the CAPM model. Unlike

CAPM that uses a market beta, CCAPM uses consumption beta to determine the expected

return premiums over the risk-free rate. According to CCAPM security premiums are

determined by consumption betas. CCAPM is useful because it allows measurement of risks

associated with stock based on the consumption growth. The higher the consumption beta,

the higher the expected return on a security.

current and future risk factors like inflation, unemployment rate and future returns (Riley,

2009).

Considering that investors' appetite for risk varies, the ICAPM model a men variance analysis

to mitigate projected risk from one investor to another. The mean-variance analysis makes it

easier to arrive at a normal distribution of risk over time. Lastly, ICAPM formula comprises

of several beta coefficients representing different hedging portfolios (Berk, 1995, p. 281).

The ICAPM formula is:

Ri = Rf + β*(Rm-Rf) + βj*(Rn – Rf)

Where:

Ri = Expected return

Rf = Risk-free rate

Rm = Return on the market portfolio and

Rn = Expected return on the hedging

β = Measure of systematic risk concerning the market portfolio

βj= Represents the measure of volatility concerning the hedging security

b) Consumption Capital Asset Pricing Model (CCAPM)

Breeden created the CCAPM in 1979 as an improved version of the CAPM model. Unlike

CAPM that uses a market beta, CCAPM uses consumption beta to determine the expected

return premiums over the risk-free rate. According to CCAPM security premiums are

determined by consumption betas. CCAPM is useful because it allows measurement of risks

associated with stock based on the consumption growth. The higher the consumption beta,

the higher the expected return on a security.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPM 10

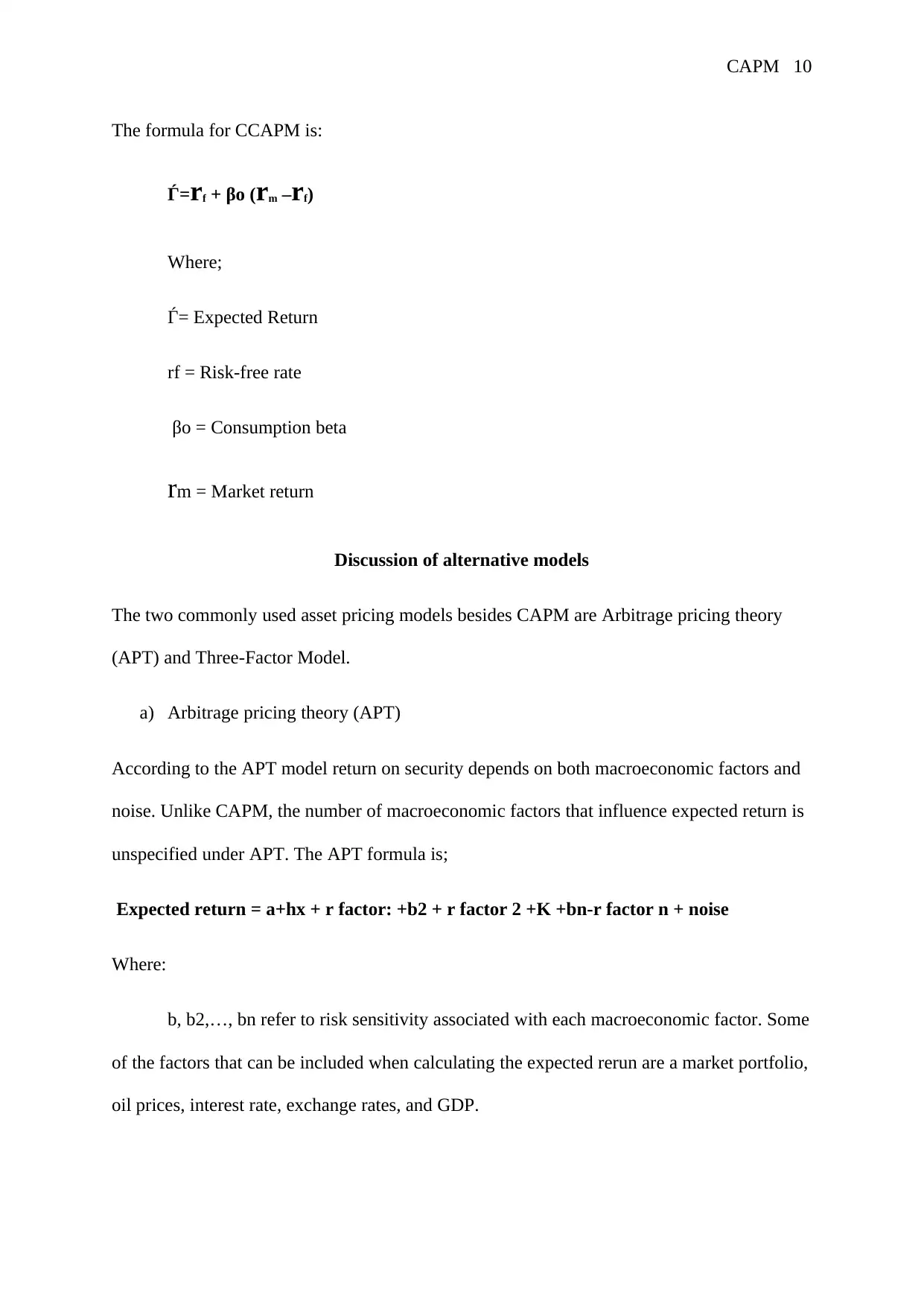

The formula for CCAPM is:

Ѓ=rf + βo (rm –rf)

Where;

Ѓ= Expected Return

rf = Risk-free rate

βo = Consumption beta

rm = Market return

Discussion of alternative models

The two commonly used asset pricing models besides CAPM are Arbitrage pricing theory

(APT) and Three-Factor Model.

a) Arbitrage pricing theory (APT)

According to the APT model return on security depends on both macroeconomic factors and

noise. Unlike CAPM, the number of macroeconomic factors that influence expected return is

unspecified under APT. The APT formula is;

Expected return = a+hx + r factor: +b2 + r factor 2 +K +bn-r factor n + noise

Where:

b, b2,…, bn refer to risk sensitivity associated with each macroeconomic factor. Some

of the factors that can be included when calculating the expected rerun are a market portfolio,

oil prices, interest rate, exchange rates, and GDP.

The formula for CCAPM is:

Ѓ=rf + βo (rm –rf)

Where;

Ѓ= Expected Return

rf = Risk-free rate

βo = Consumption beta

rm = Market return

Discussion of alternative models

The two commonly used asset pricing models besides CAPM are Arbitrage pricing theory

(APT) and Three-Factor Model.

a) Arbitrage pricing theory (APT)

According to the APT model return on security depends on both macroeconomic factors and

noise. Unlike CAPM, the number of macroeconomic factors that influence expected return is

unspecified under APT. The APT formula is;

Expected return = a+hx + r factor: +b2 + r factor 2 +K +bn-r factor n + noise

Where:

b, b2,…, bn refer to risk sensitivity associated with each macroeconomic factor. Some

of the factors that can be included when calculating the expected rerun are a market portfolio,

oil prices, interest rate, exchange rates, and GDP.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPM 11

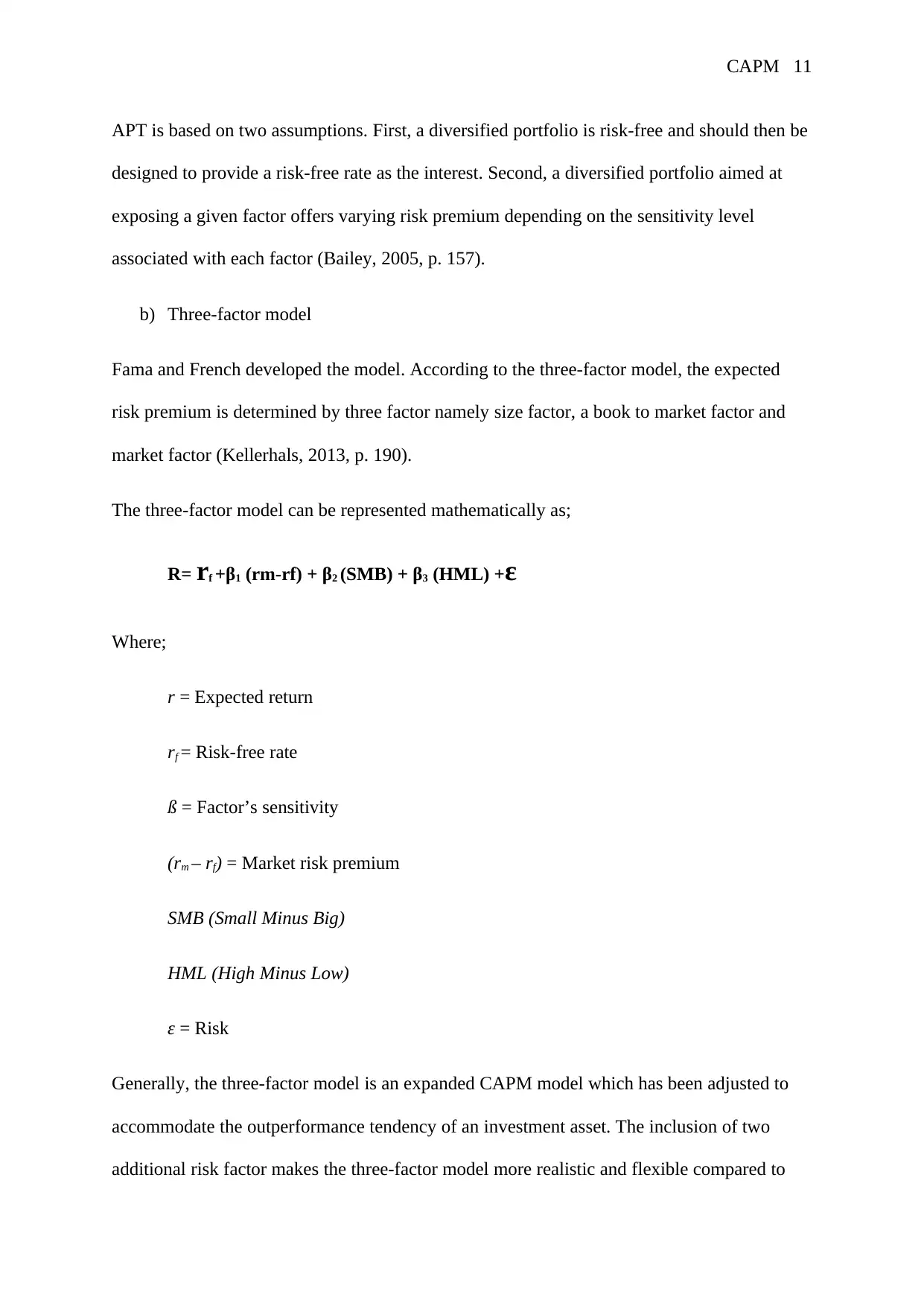

APT is based on two assumptions. First, a diversified portfolio is risk-free and should then be

designed to provide a risk-free rate as the interest. Second, a diversified portfolio aimed at

exposing a given factor offers varying risk premium depending on the sensitivity level

associated with each factor (Bailey, 2005, p. 157).

b) Three-factor model

Fama and French developed the model. According to the three-factor model, the expected

risk premium is determined by three factor namely size factor, a book to market factor and

market factor (Kellerhals, 2013, p. 190).

The three-factor model can be represented mathematically as;

R= rf +β1 (rm-rf) + β2 (SMB) + β3 (HML) +ε

Where;

r = Expected return

rf = Risk-free rate

ß = Factor’s sensitivity

(rm – rf) = Market risk premium

SMB (Small Minus Big)

HML (High Minus Low)

ε = Risk

Generally, the three-factor model is an expanded CAPM model which has been adjusted to

accommodate the outperformance tendency of an investment asset. The inclusion of two

additional risk factor makes the three-factor model more realistic and flexible compared to

APT is based on two assumptions. First, a diversified portfolio is risk-free and should then be

designed to provide a risk-free rate as the interest. Second, a diversified portfolio aimed at

exposing a given factor offers varying risk premium depending on the sensitivity level

associated with each factor (Bailey, 2005, p. 157).

b) Three-factor model

Fama and French developed the model. According to the three-factor model, the expected

risk premium is determined by three factor namely size factor, a book to market factor and

market factor (Kellerhals, 2013, p. 190).

The three-factor model can be represented mathematically as;

R= rf +β1 (rm-rf) + β2 (SMB) + β3 (HML) +ε

Where;

r = Expected return

rf = Risk-free rate

ß = Factor’s sensitivity

(rm – rf) = Market risk premium

SMB (Small Minus Big)

HML (High Minus Low)

ε = Risk

Generally, the three-factor model is an expanded CAPM model which has been adjusted to

accommodate the outperformance tendency of an investment asset. The inclusion of two

additional risk factor makes the three-factor model more realistic and flexible compared to

CAPM 12

CAPM. Currently, the three-factor model has been expanded further to include the four-factor

model and the five-factor model.

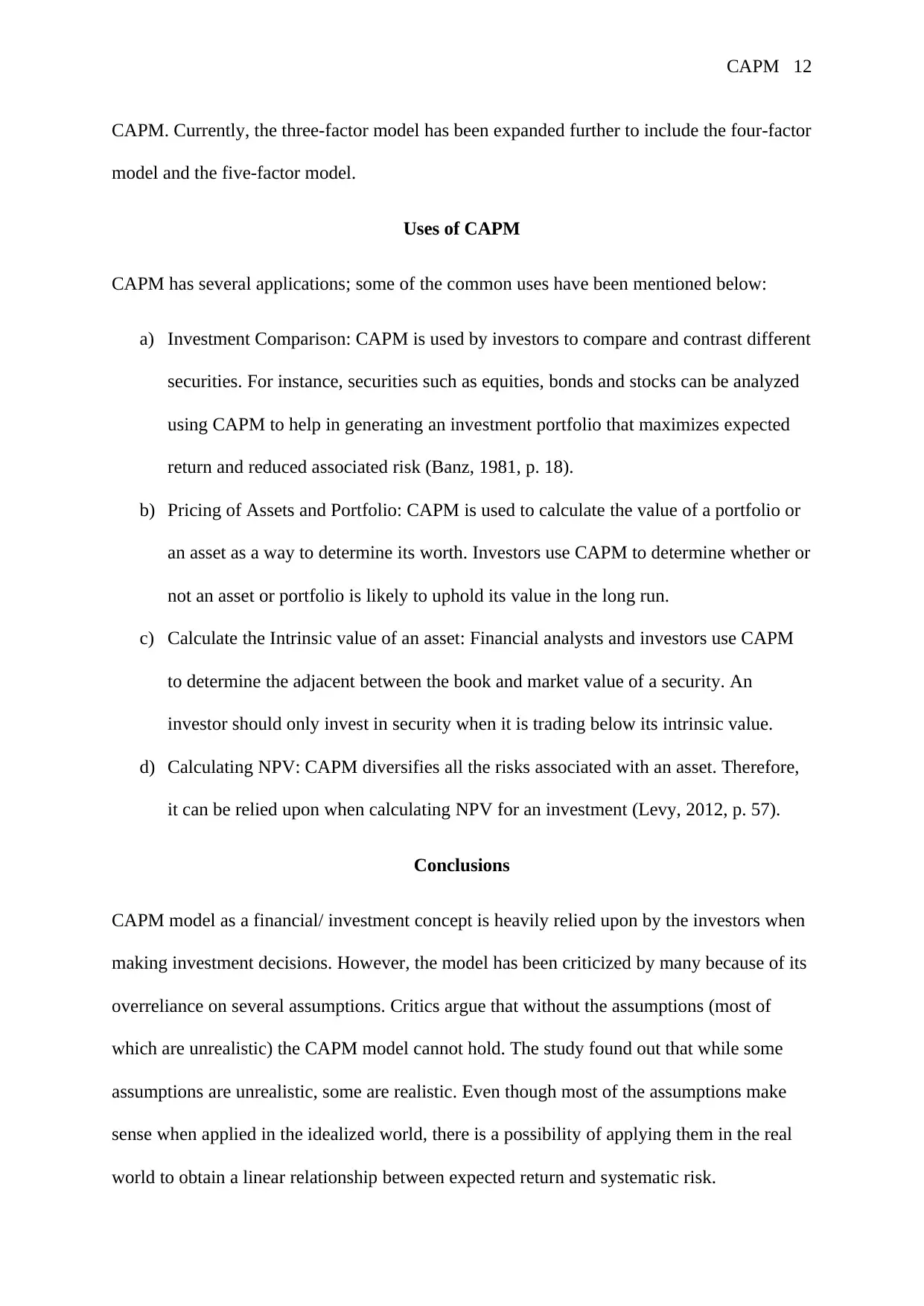

Uses of CAPM

CAPM has several applications; some of the common uses have been mentioned below:

a) Investment Comparison: CAPM is used by investors to compare and contrast different

securities. For instance, securities such as equities, bonds and stocks can be analyzed

using CAPM to help in generating an investment portfolio that maximizes expected

return and reduced associated risk (Banz, 1981, p. 18).

b) Pricing of Assets and Portfolio: CAPM is used to calculate the value of a portfolio or

an asset as a way to determine its worth. Investors use CAPM to determine whether or

not an asset or portfolio is likely to uphold its value in the long run.

c) Calculate the Intrinsic value of an asset: Financial analysts and investors use CAPM

to determine the adjacent between the book and market value of a security. An

investor should only invest in security when it is trading below its intrinsic value.

d) Calculating NPV: CAPM diversifies all the risks associated with an asset. Therefore,

it can be relied upon when calculating NPV for an investment (Levy, 2012, p. 57).

Conclusions

CAPM model as a financial/ investment concept is heavily relied upon by the investors when

making investment decisions. However, the model has been criticized by many because of its

overreliance on several assumptions. Critics argue that without the assumptions (most of

which are unrealistic) the CAPM model cannot hold. The study found out that while some

assumptions are unrealistic, some are realistic. Even though most of the assumptions make

sense when applied in the idealized world, there is a possibility of applying them in the real

world to obtain a linear relationship between expected return and systematic risk.

CAPM. Currently, the three-factor model has been expanded further to include the four-factor

model and the five-factor model.

Uses of CAPM

CAPM has several applications; some of the common uses have been mentioned below:

a) Investment Comparison: CAPM is used by investors to compare and contrast different

securities. For instance, securities such as equities, bonds and stocks can be analyzed

using CAPM to help in generating an investment portfolio that maximizes expected

return and reduced associated risk (Banz, 1981, p. 18).

b) Pricing of Assets and Portfolio: CAPM is used to calculate the value of a portfolio or

an asset as a way to determine its worth. Investors use CAPM to determine whether or

not an asset or portfolio is likely to uphold its value in the long run.

c) Calculate the Intrinsic value of an asset: Financial analysts and investors use CAPM

to determine the adjacent between the book and market value of a security. An

investor should only invest in security when it is trading below its intrinsic value.

d) Calculating NPV: CAPM diversifies all the risks associated with an asset. Therefore,

it can be relied upon when calculating NPV for an investment (Levy, 2012, p. 57).

Conclusions

CAPM model as a financial/ investment concept is heavily relied upon by the investors when

making investment decisions. However, the model has been criticized by many because of its

overreliance on several assumptions. Critics argue that without the assumptions (most of

which are unrealistic) the CAPM model cannot hold. The study found out that while some

assumptions are unrealistic, some are realistic. Even though most of the assumptions make

sense when applied in the idealized world, there is a possibility of applying them in the real

world to obtain a linear relationship between expected return and systematic risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.