Royal Holloway: MN3365 Strategic Finance - CAPM Recent Developments

VerifiedAdded on 2023/06/04

|10

|2873

|59

Essay

AI Summary

This essay provides a comprehensive analysis of the Capital Asset Pricing Model (CAPM), exploring its usefulness and recent developments within the field of strategic finance. It discusses the model's underlying assumptions and critiques, highlighting the challenges in attaining a real market portfolio and the potential inappropriateness of empirical model testing. The essay also examines the advantages of CAPM implementation, such as its ease of calculation and consideration of systematic risk, while acknowledging its limitations and the emergence of alternative models. Ultimately, the essay concludes that while CAPM has its critics, it remains a widely used technique in the industry for anticipating returns and evaluating investment portfolios.

Running head: STRATEGIC FINANCE

Strategic Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Strategic Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1STRATEGIC FINANCE

Introduction:

The Capital Asset Pricing Model (CAPM) serve as an important tool and is employed

broadly within the international industry as it is relied in extremely strong estimations. In

light of recent developments in this topic a detailed development within the area. Whether

this model is credible model for analysing risks along with anticipated return has attained

high academic and professional elaboration. Aggarwal (2017) explained CAPM to be a

theory of relationship between risk and return which indicates that the anticipated risk

premium on certain security is identical to its beta times the market risk premium. The

CAPM serves as a highly renowned technique employee because of its capability to account

for systematic uncertainty in comparison to the unsystematic ones in order to decrease the

diversification impacts on anticipated returns. This is for aa particular shareholder after being

added to an investor’s well-developed portfolio.

The CAPM employs beta in order to signify the “sensitivity of a stock’s return to the

market portfolio return. The CAPM also indicates that the cost of equity capital of the

investor’s is determined by the beta (Akpo, Hassan and Esuike 2015). Such beta is also

multiplied by the market risk premium that is the difference between treasury bill returns and

anticipated market return. This facilitates in computing the asset’s risk premium, decreasing

the impacts of diversification on the expected return of assets that facilitates in computing the

systematic risk through adding a particular asset to an established well-developed portfolio.

The risk premium is then added within the risk-free rate or the return rate related with

treasury bills. The security market line explains the association among the beta and expected

return.

Introduction:

The Capital Asset Pricing Model (CAPM) serve as an important tool and is employed

broadly within the international industry as it is relied in extremely strong estimations. In

light of recent developments in this topic a detailed development within the area. Whether

this model is credible model for analysing risks along with anticipated return has attained

high academic and professional elaboration. Aggarwal (2017) explained CAPM to be a

theory of relationship between risk and return which indicates that the anticipated risk

premium on certain security is identical to its beta times the market risk premium. The

CAPM serves as a highly renowned technique employee because of its capability to account

for systematic uncertainty in comparison to the unsystematic ones in order to decrease the

diversification impacts on anticipated returns. This is for aa particular shareholder after being

added to an investor’s well-developed portfolio.

The CAPM employs beta in order to signify the “sensitivity of a stock’s return to the

market portfolio return. The CAPM also indicates that the cost of equity capital of the

investor’s is determined by the beta (Akpo, Hassan and Esuike 2015). Such beta is also

multiplied by the market risk premium that is the difference between treasury bill returns and

anticipated market return. This facilitates in computing the asset’s risk premium, decreasing

the impacts of diversification on the expected return of assets that facilitates in computing the

systematic risk through adding a particular asset to an established well-developed portfolio.

The risk premium is then added within the risk-free rate or the return rate related with

treasury bills. The security market line explains the association among the beta and expected

return.

2STRATEGIC FINANCE

Concepts behind the problem and discussion:

Baker and Wurgler (2015) revealed that CAPM is implemented by the portfolio

manager in supporting the investors to decide their portfolio through carrying out equity

capital computation of the organization. For this reason, it can be said that this technique

facilitates expected decay quantification and this facilitates conversion of likely uncetainities

related with anticipated return on equity. The CPAM theory is observed to have several

assumptions that is considered at the time of computing anticipated risk returns that is

attained by securities. One of such assumption is that the financial market includes numerous

investors those are well-informed, educated as well as prudent sellers and buyers. Another

assumption is that that the investors are highly concerned regarding their money and

anticipated to attain a premium or additional uncetainities they assume at the time of

investment (Barberis, Greenwood, Jin and Shleifer 2015). Third assumption considers that

investors deemed to be moving ahead towards a same duration for investment planning.

Fourth assumption is that less taxes and concessions along with commissions are applicable

and it is also assumed that there is a single tax-free rate and investors lend or borrow in a

particular rate.

Barillas and Shanken (2018) revealed certain criticism as is present over the validity

of CAPM in ensuring a needed return rate that is used commonly and the work of

“JohnLintner, Jack Treynor, William Sharpe and Jan Mossinis” are considered as among the

most vital financial theories prepared. Nobel prize was awarded to William Sharpe in

Economics in the year 1990 for his work accomplished with CAPM. There have been several

extensions to the CAPM as it was initially developed that has made the model that is highly

complex and this is slightly highly accurate. Most of the criticism related with the original

CAPM exist in the basic anticipations. Several critiques have also argued that there are

several assumptions and numerous assumptions among them are observed to be highly

Concepts behind the problem and discussion:

Baker and Wurgler (2015) revealed that CAPM is implemented by the portfolio

manager in supporting the investors to decide their portfolio through carrying out equity

capital computation of the organization. For this reason, it can be said that this technique

facilitates expected decay quantification and this facilitates conversion of likely uncetainities

related with anticipated return on equity. The CPAM theory is observed to have several

assumptions that is considered at the time of computing anticipated risk returns that is

attained by securities. One of such assumption is that the financial market includes numerous

investors those are well-informed, educated as well as prudent sellers and buyers. Another

assumption is that that the investors are highly concerned regarding their money and

anticipated to attain a premium or additional uncetainities they assume at the time of

investment (Barberis, Greenwood, Jin and Shleifer 2015). Third assumption considers that

investors deemed to be moving ahead towards a same duration for investment planning.

Fourth assumption is that less taxes and concessions along with commissions are applicable

and it is also assumed that there is a single tax-free rate and investors lend or borrow in a

particular rate.

Barillas and Shanken (2018) revealed certain criticism as is present over the validity

of CAPM in ensuring a needed return rate that is used commonly and the work of

“JohnLintner, Jack Treynor, William Sharpe and Jan Mossinis” are considered as among the

most vital financial theories prepared. Nobel prize was awarded to William Sharpe in

Economics in the year 1990 for his work accomplished with CAPM. There have been several

extensions to the CAPM as it was initially developed that has made the model that is highly

complex and this is slightly highly accurate. Most of the criticism related with the original

CAPM exist in the basic anticipations. Several critiques have also argued that there are

several assumptions and numerous assumptions among them are observed to be highly

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3STRATEGIC FINANCE

presumptuous. Among the most renowned CAPM critiques such as Berk and Van Binsbergen

(2016) which argues that it is virtually impossible to attain a real market portfolio along with

the past and current empirical model testing is inappropriate. These reasechers also argued

that the CAPM can be considered identical to testing of an asset’s mean variance

effectiveness.

In contrast, Fama (2014) stated that it is not possible to test aa market’s mean-

variance effectiveness in case of an unobservable market. The reasechers have also

considered that for maintaining aa genuinely diversified portfolio it can also consider all the

investments in all the assets in all the industries internationally. For this reason, the empirical

tests employed for the CAPM are not enough for they employ “insufficient market proxies”

that includes DAX and FTSE 100 which do not consider all the financial asset types into

account for this might be unobservable. It was evidenced by Jarrow (2018) that ineffective

marketing proxies are employed in CAPM in which a manager with “suitable capability”

might be deemed as inferior for a manager with less than perfect capability in case they

employ an ineffective market proxy focussed on mean-variance.

Kristoufek and Ferreira (2018) recognised that the CAPM model implementation has

several advantages that facilitates the investors in deciding the securities to acquire and in

developing an efficient and profitable portfolio. One of these advantages includes that the

calculations provided by this model is easier and stress tested that offered a broad range of

results. This further facilitates in developing confidence among the investors in investing

within an effective portfolio. Moreover, existence of a diversified portfolio facilitates in

decreasing the unsystematic uncertainty. Another advantage that is offered by

implementation of CAPM model is that it considers the systematic risk (Akpo, Hassan and

Esuike 2015). In such condition it is vital to consider that the identified risk is unforeseen that

must not be neglected and can form a part of risk evaluation theory. For this reason, this

presumptuous. Among the most renowned CAPM critiques such as Berk and Van Binsbergen

(2016) which argues that it is virtually impossible to attain a real market portfolio along with

the past and current empirical model testing is inappropriate. These reasechers also argued

that the CAPM can be considered identical to testing of an asset’s mean variance

effectiveness.

In contrast, Fama (2014) stated that it is not possible to test aa market’s mean-

variance effectiveness in case of an unobservable market. The reasechers have also

considered that for maintaining aa genuinely diversified portfolio it can also consider all the

investments in all the assets in all the industries internationally. For this reason, the empirical

tests employed for the CAPM are not enough for they employ “insufficient market proxies”

that includes DAX and FTSE 100 which do not consider all the financial asset types into

account for this might be unobservable. It was evidenced by Jarrow (2018) that ineffective

marketing proxies are employed in CAPM in which a manager with “suitable capability”

might be deemed as inferior for a manager with less than perfect capability in case they

employ an ineffective market proxy focussed on mean-variance.

Kristoufek and Ferreira (2018) recognised that the CAPM model implementation has

several advantages that facilitates the investors in deciding the securities to acquire and in

developing an efficient and profitable portfolio. One of these advantages includes that the

calculations provided by this model is easier and stress tested that offered a broad range of

results. This further facilitates in developing confidence among the investors in investing

within an effective portfolio. Moreover, existence of a diversified portfolio facilitates in

decreasing the unsystematic uncertainty. Another advantage that is offered by

implementation of CAPM model is that it considers the systematic risk (Akpo, Hassan and

Esuike 2015). In such condition it is vital to consider that the identified risk is unforeseen that

must not be neglected and can form a part of risk evaluation theory. For this reason, this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4STRATEGIC FINANCE

technique is deemed to be highly reliable that ensures comparison of organizational

performance with account for market performance. Kuehn, Simutin and Wang (2017) also

indicated that CAPM is also advantageous for investment portfolio appraisal as the offered

discount rate is higher than those provided by other models. For this reason, it maintains a

good link between expected investor returns from his investment and systematic risks of the

same.

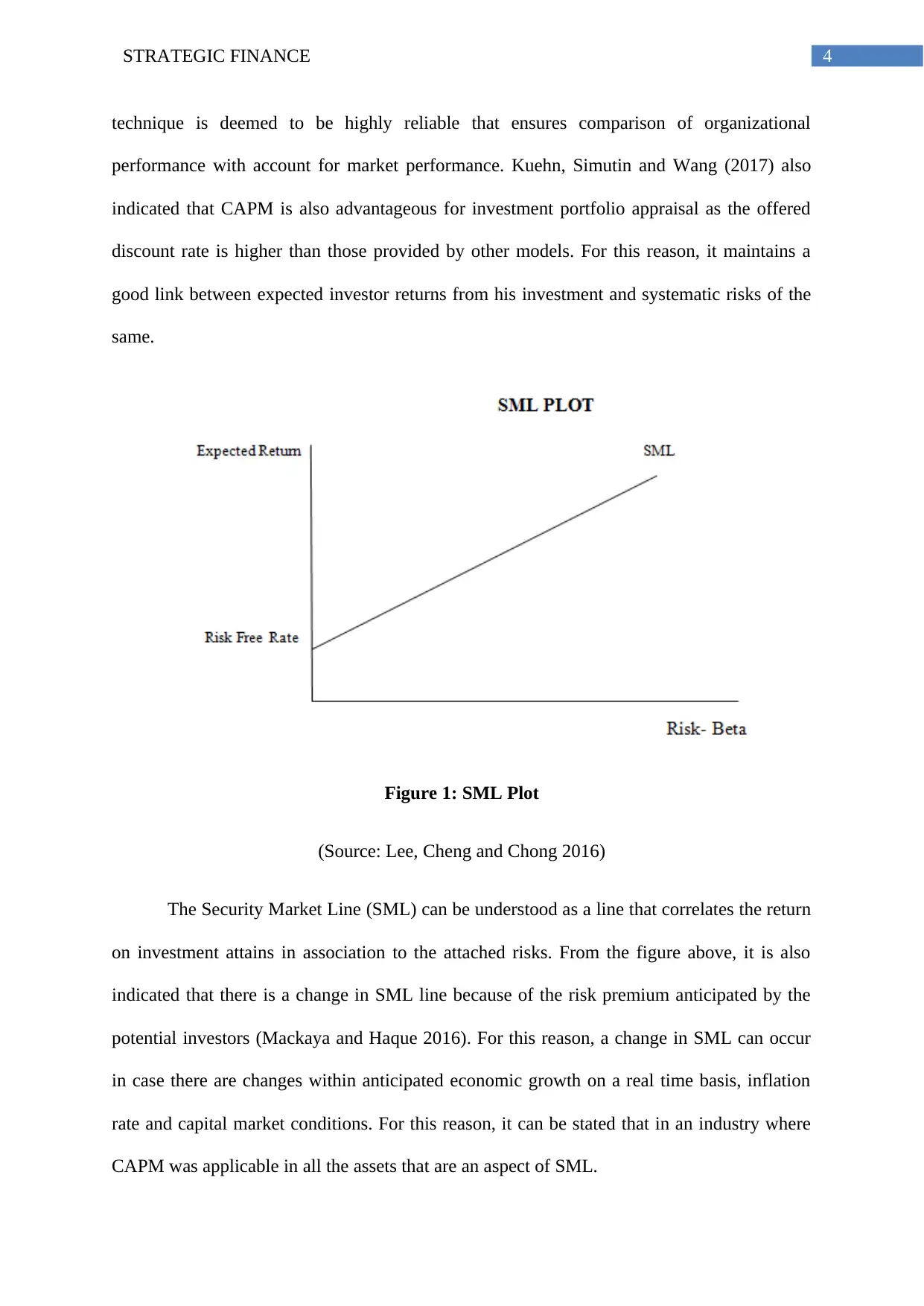

Figure 1: SML Plot

(Source: Lee, Cheng and Chong 2016)

The Security Market Line (SML) can be understood as a line that correlates the return

on investment attains in association to the attached risks. From the figure above, it is also

indicated that there is a change in SML line because of the risk premium anticipated by the

potential investors (Mackaya and Haque 2016). For this reason, a change in SML can occur

in case there are changes within anticipated economic growth on a real time basis, inflation

rate and capital market conditions. For this reason, it can be stated that in an industry where

CAPM was applicable in all the assets that are an aspect of SML.

technique is deemed to be highly reliable that ensures comparison of organizational

performance with account for market performance. Kuehn, Simutin and Wang (2017) also

indicated that CAPM is also advantageous for investment portfolio appraisal as the offered

discount rate is higher than those provided by other models. For this reason, it maintains a

good link between expected investor returns from his investment and systematic risks of the

same.

Figure 1: SML Plot

(Source: Lee, Cheng and Chong 2016)

The Security Market Line (SML) can be understood as a line that correlates the return

on investment attains in association to the attached risks. From the figure above, it is also

indicated that there is a change in SML line because of the risk premium anticipated by the

potential investors (Mackaya and Haque 2016). For this reason, a change in SML can occur

in case there are changes within anticipated economic growth on a real time basis, inflation

rate and capital market conditions. For this reason, it can be stated that in an industry where

CAPM was applicable in all the assets that are an aspect of SML.

5STRATEGIC FINANCE

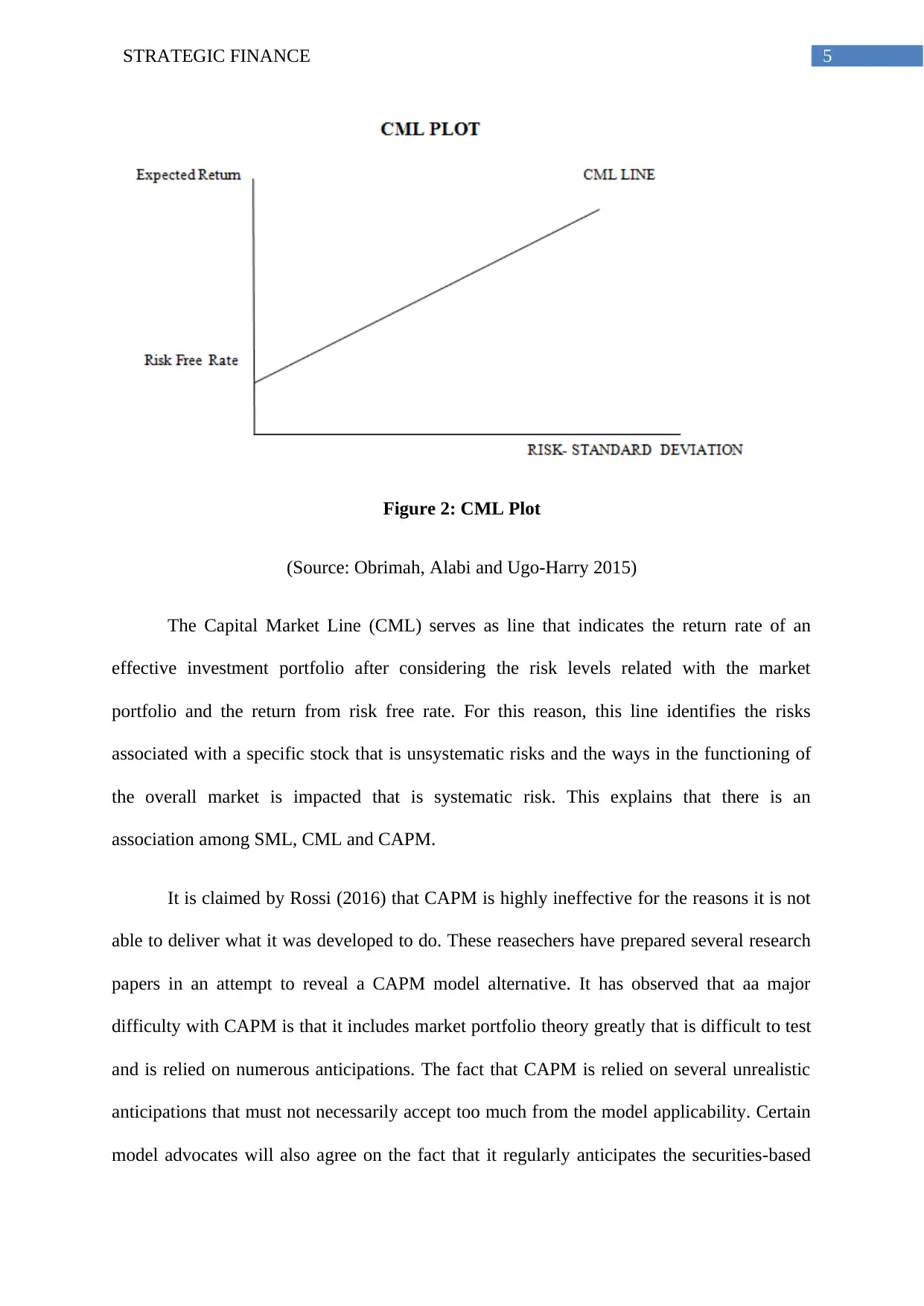

Figure 2: CML Plot

(Source: Obrimah, Alabi and Ugo‐Harry 2015)

The Capital Market Line (CML) serves as line that indicates the return rate of an

effective investment portfolio after considering the risk levels related with the market

portfolio and the return from risk free rate. For this reason, this line identifies the risks

associated with a specific stock that is unsystematic risks and the ways in the functioning of

the overall market is impacted that is systematic risk. This explains that there is an

association among SML, CML and CAPM.

It is claimed by Rossi (2016) that CAPM is highly ineffective for the reasons it is not

able to deliver what it was developed to do. These reasechers have prepared several research

papers in an attempt to reveal a CAPM model alternative. It has observed that aa major

difficulty with CAPM is that it includes market portfolio theory greatly that is difficult to test

and is relied on numerous anticipations. The fact that CAPM is relied on several unrealistic

anticipations that must not necessarily accept too much from the model applicability. Certain

model advocates will also agree on the fact that it regularly anticipates the securities-based

Figure 2: CML Plot

(Source: Obrimah, Alabi and Ugo‐Harry 2015)

The Capital Market Line (CML) serves as line that indicates the return rate of an

effective investment portfolio after considering the risk levels related with the market

portfolio and the return from risk free rate. For this reason, this line identifies the risks

associated with a specific stock that is unsystematic risks and the ways in the functioning of

the overall market is impacted that is systematic risk. This explains that there is an

association among SML, CML and CAPM.

It is claimed by Rossi (2016) that CAPM is highly ineffective for the reasons it is not

able to deliver what it was developed to do. These reasechers have prepared several research

papers in an attempt to reveal a CAPM model alternative. It has observed that aa major

difficulty with CAPM is that it includes market portfolio theory greatly that is difficult to test

and is relied on numerous anticipations. The fact that CAPM is relied on several unrealistic

anticipations that must not necessarily accept too much from the model applicability. Certain

model advocates will also agree on the fact that it regularly anticipates the securities-based

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6STRATEGIC FINANCE

cost of capital in a fair manner and for this reason its recent regular use in several institutions

and for this reason its unrealistic anticipations must not matter. A three-factor model

developed by Tsuji (2017) through employing three major variables as different from the one

implemented in CAPM are used in explaining the stock returns. Their model also explained

that nit just beta serves as aa variable in anticipating a stock’s anticipated return, the book-to-

market ratio and market capitalization were also important in anticipating stock returns. It

was also revealed by these reasechers that small cap stocks tend to attain an increased book-

to-market ratio (value stocks) that have increased returns in comparison to the ones with

decreased book-to-market ratios or growth stocks. Incorporating these variables facilitate in

adjusting the tend of outperformance. This also concluded that beta was considered being less

vital in anticipating stock returns in comparison to other two variables.

According to the views presented by Zabarankin, Pavlikov and Uryasev (2014) it is

revealed that addition of two variables within the original CAPM computation is possible in

order to reveal that their computation was capable in justifying 90% of diversified portfolio

returns. On the other hand, CAPM was just capable to identify 70% of the returns. The

arguments of these reasechers are deemed effective and resulted in further debate from the

time their research was published. It was also elaborated by Zabarankin, Pavlikov and

Uryasev (2014) that evidence on CAPM is also relied on the data impacted by basis of

survivorship on COMPUSTAT. These reasechers also argued that they recognised no

increased returns with any of the identified three factors. However, the CAPM might appear

to be ineffective but still it is observed to be a renowned technique of anticipating the returns.

It is evidenced that “The theory and corporate finance practice: evidence from the field”

article elaborated that CAPM is a widely used technique that is used in percentage of 77.49%

within the industries. It was also revealed that CAPM or implementation of this model was

cost of capital in a fair manner and for this reason its recent regular use in several institutions

and for this reason its unrealistic anticipations must not matter. A three-factor model

developed by Tsuji (2017) through employing three major variables as different from the one

implemented in CAPM are used in explaining the stock returns. Their model also explained

that nit just beta serves as aa variable in anticipating a stock’s anticipated return, the book-to-

market ratio and market capitalization were also important in anticipating stock returns. It

was also revealed by these reasechers that small cap stocks tend to attain an increased book-

to-market ratio (value stocks) that have increased returns in comparison to the ones with

decreased book-to-market ratios or growth stocks. Incorporating these variables facilitate in

adjusting the tend of outperformance. This also concluded that beta was considered being less

vital in anticipating stock returns in comparison to other two variables.

According to the views presented by Zabarankin, Pavlikov and Uryasev (2014) it is

revealed that addition of two variables within the original CAPM computation is possible in

order to reveal that their computation was capable in justifying 90% of diversified portfolio

returns. On the other hand, CAPM was just capable to identify 70% of the returns. The

arguments of these reasechers are deemed effective and resulted in further debate from the

time their research was published. It was also elaborated by Zabarankin, Pavlikov and

Uryasev (2014) that evidence on CAPM is also relied on the data impacted by basis of

survivorship on COMPUSTAT. These reasechers also argued that they recognised no

increased returns with any of the identified three factors. However, the CAPM might appear

to be ineffective but still it is observed to be a renowned technique of anticipating the returns.

It is evidenced that “The theory and corporate finance practice: evidence from the field”

article elaborated that CAPM is a widely used technique that is used in percentage of 77.49%

within the industries. It was also revealed that CAPM or implementation of this model was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STRATEGIC FINANCE

employed by 85% of the companies those follow “best-practice” (Berk and Van Binsbergen

2016).

Tsuji (2017) revealed that CAPM model implication has numerous critics in the

industry that indicates a positive attitude towards CAPM that was deemed as a new model.

The major concern detected by the “The Harvard Business Review” that CAPM have

numerous critics and major concern was considered regarding the beta values that is subject

to variations over time for the reason that organization’s capital structure change even

through beta values are computed from the historical data. Moreover, several anticipations

like the anticipated turn on the market that are subject to error. Conversely, it was also

indicated that the CAPM model is employed in alignment with several other financial models

in anticipating the equity cost that is considered as “Weighted Average Cost of Capital

(WACC)” along with “Dividend Growth Model” that admits that CAPM is not that better in

comparison to financial model for anticipating equity cost.

Conclusion:

The objective of the essay is to analyse the recent developments in Capital Asset

Pricing Model (CAPM) to serve as an important tool and to explain a detailed development

within the area. It is gathered from the essay that most of the criticism related with the

original CAPM exist in the basic anticipations. Several critiques have also argued that there

are several assumptions and numerous assumptions among them are observed to be highly

presumptuous. Moreover, the researchers have also considered that for maintaining aa

genuinely diversified portfolio it can also consider all the investments in all the assets in all

the industries internationally. The essay also clarified that it is virtually impossible to attain a

real market portfolio along with the past and current empirical model testing is inappropriate.

These reasechers also argued that the CAPM can be considered identical to testing of an

employed by 85% of the companies those follow “best-practice” (Berk and Van Binsbergen

2016).

Tsuji (2017) revealed that CAPM model implication has numerous critics in the

industry that indicates a positive attitude towards CAPM that was deemed as a new model.

The major concern detected by the “The Harvard Business Review” that CAPM have

numerous critics and major concern was considered regarding the beta values that is subject

to variations over time for the reason that organization’s capital structure change even

through beta values are computed from the historical data. Moreover, several anticipations

like the anticipated turn on the market that are subject to error. Conversely, it was also

indicated that the CAPM model is employed in alignment with several other financial models

in anticipating the equity cost that is considered as “Weighted Average Cost of Capital

(WACC)” along with “Dividend Growth Model” that admits that CAPM is not that better in

comparison to financial model for anticipating equity cost.

Conclusion:

The objective of the essay is to analyse the recent developments in Capital Asset

Pricing Model (CAPM) to serve as an important tool and to explain a detailed development

within the area. It is gathered from the essay that most of the criticism related with the

original CAPM exist in the basic anticipations. Several critiques have also argued that there

are several assumptions and numerous assumptions among them are observed to be highly

presumptuous. Moreover, the researchers have also considered that for maintaining aa

genuinely diversified portfolio it can also consider all the investments in all the assets in all

the industries internationally. The essay also clarified that it is virtually impossible to attain a

real market portfolio along with the past and current empirical model testing is inappropriate.

These reasechers also argued that the CAPM can be considered identical to testing of an

8STRATEGIC FINANCE

asset’s mean variance effectiveness. It has also been gathered that managers might be native

to employ the CAPM on their own and along with that there are numerous extensions of the

model that must be considered for use along with CAPM along with other traditional

techniques.

References:

Aggarwal, R., 2017. The Fama-French Three Factor Model and the Capital Asset Pricing

Model: Evidence from the Indian Stock Market. Indian Journal of Research in Capital

Markets, 4(2), pp.36-47.

Akpo, E.S., Hassan, S. and Esuike, B.U., 2015. Reconciling the arbitrage pricing theory

(APT) and the capital asset pricing model (CAPM) institutional and theoretical

framework. International Journal of Development and Economic Sustainability, 3(6), pp.17-

23.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Barillas, F. and Shanken, J., 2018. Comparing asset pricing models. The Journal of

Finance, 73(2), pp.715-754.

Berk, J.B. and Van Binsbergen, J.H., 2016. Assessing asset pricing models using revealed

preference. Journal of Financial Economics, 119(1), pp.1-23.

Fama, E.F., 2014. Two pillars of asset pricing. American Economic Review, 104(6), pp.1467-

1485.

asset’s mean variance effectiveness. It has also been gathered that managers might be native

to employ the CAPM on their own and along with that there are numerous extensions of the

model that must be considered for use along with CAPM along with other traditional

techniques.

References:

Aggarwal, R., 2017. The Fama-French Three Factor Model and the Capital Asset Pricing

Model: Evidence from the Indian Stock Market. Indian Journal of Research in Capital

Markets, 4(2), pp.36-47.

Akpo, E.S., Hassan, S. and Esuike, B.U., 2015. Reconciling the arbitrage pricing theory

(APT) and the capital asset pricing model (CAPM) institutional and theoretical

framework. International Journal of Development and Economic Sustainability, 3(6), pp.17-

23.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Barillas, F. and Shanken, J., 2018. Comparing asset pricing models. The Journal of

Finance, 73(2), pp.715-754.

Berk, J.B. and Van Binsbergen, J.H., 2016. Assessing asset pricing models using revealed

preference. Journal of Financial Economics, 119(1), pp.1-23.

Fama, E.F., 2014. Two pillars of asset pricing. American Economic Review, 104(6), pp.1467-

1485.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9STRATEGIC FINANCE

Jarrow, R., 2018. An equilibrium capital asset pricing model in markets with price jumps and

price bubbles. Quarterly Journal of Finance, 8(02), p.18-23.

Kristoufek, L. and Ferreira, P., 2018. Capital asset pricing model in Portugal: Evidence from

fractal regressions. Portuguese Economic Journal, 17(9), pp.1-11.

Kuehn, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Lee, H.S., Cheng, F.F. and Chong, S.C., 2016. Markowitz portfolio theory and capital asset

pricing model for Kuala Lumpur stock exchange: A case revisited. International Journal of

Economics and Financial Issues, 6(3), pp.59-65.

Mackaya, W. and Haque, T., 2016. A study of industry cost of equity in Australia using the

Fama and French 5 Factor model and the Capital Asset Pricing Model (CAPM): A

pitch. Accounting and Management Information Systems, 15(3), p.618.

Obrimah, O.A., Alabi, J. and Ugo‐Harry, B., 2015. How relevant is the Capital Asset Pricing

Model (CAPM) for tests of market efficiency on the Nigerian stock exchange?. African

Development Review, 27(3), pp.262-273.

Rossi, M., 2016. The capital asset pricing model: a critical literature review. Global Business

and Economics Review, 18(5), pp.604-617.

Tsuji, C., 2017. An exploration of the time-varying beta of the international capital asset

pricing model: The case of the Japanese and the other Asia-Pacific stock markets. Accounting

and Finance Research, 6(2), pp.86-95.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM)

with drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

Jarrow, R., 2018. An equilibrium capital asset pricing model in markets with price jumps and

price bubbles. Quarterly Journal of Finance, 8(02), p.18-23.

Kristoufek, L. and Ferreira, P., 2018. Capital asset pricing model in Portugal: Evidence from

fractal regressions. Portuguese Economic Journal, 17(9), pp.1-11.

Kuehn, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Lee, H.S., Cheng, F.F. and Chong, S.C., 2016. Markowitz portfolio theory and capital asset

pricing model for Kuala Lumpur stock exchange: A case revisited. International Journal of

Economics and Financial Issues, 6(3), pp.59-65.

Mackaya, W. and Haque, T., 2016. A study of industry cost of equity in Australia using the

Fama and French 5 Factor model and the Capital Asset Pricing Model (CAPM): A

pitch. Accounting and Management Information Systems, 15(3), p.618.

Obrimah, O.A., Alabi, J. and Ugo‐Harry, B., 2015. How relevant is the Capital Asset Pricing

Model (CAPM) for tests of market efficiency on the Nigerian stock exchange?. African

Development Review, 27(3), pp.262-273.

Rossi, M., 2016. The capital asset pricing model: a critical literature review. Global Business

and Economics Review, 18(5), pp.604-617.

Tsuji, C., 2017. An exploration of the time-varying beta of the international capital asset

pricing model: The case of the Japanese and the other Asia-Pacific stock markets. Accounting

and Finance Research, 6(2), pp.86-95.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM)

with drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.