Corporate Finance: Project Evaluation and Capital Budgeting Analysis

VerifiedAdded on 2023/06/05

|7

|1151

|393

Homework Assignment

AI Summary

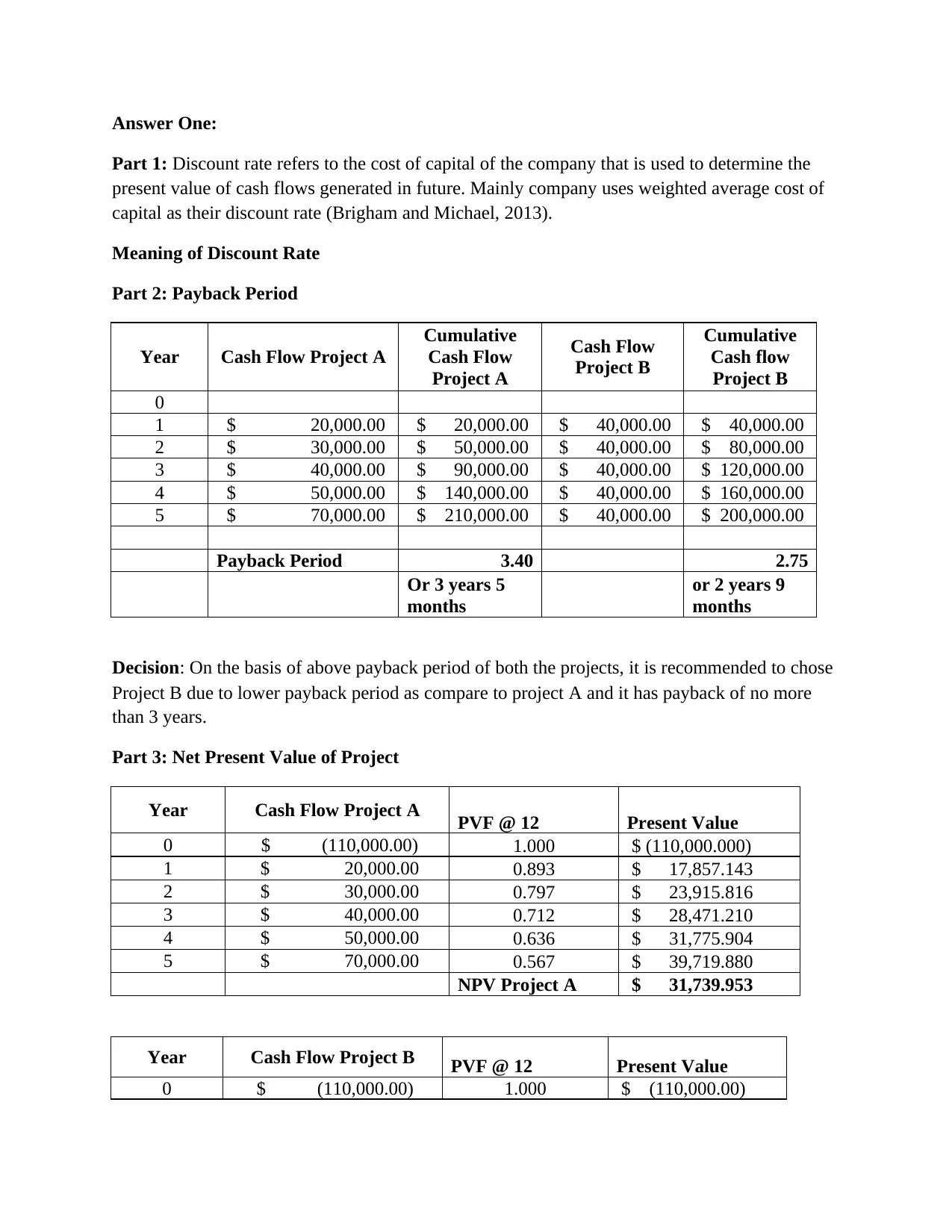

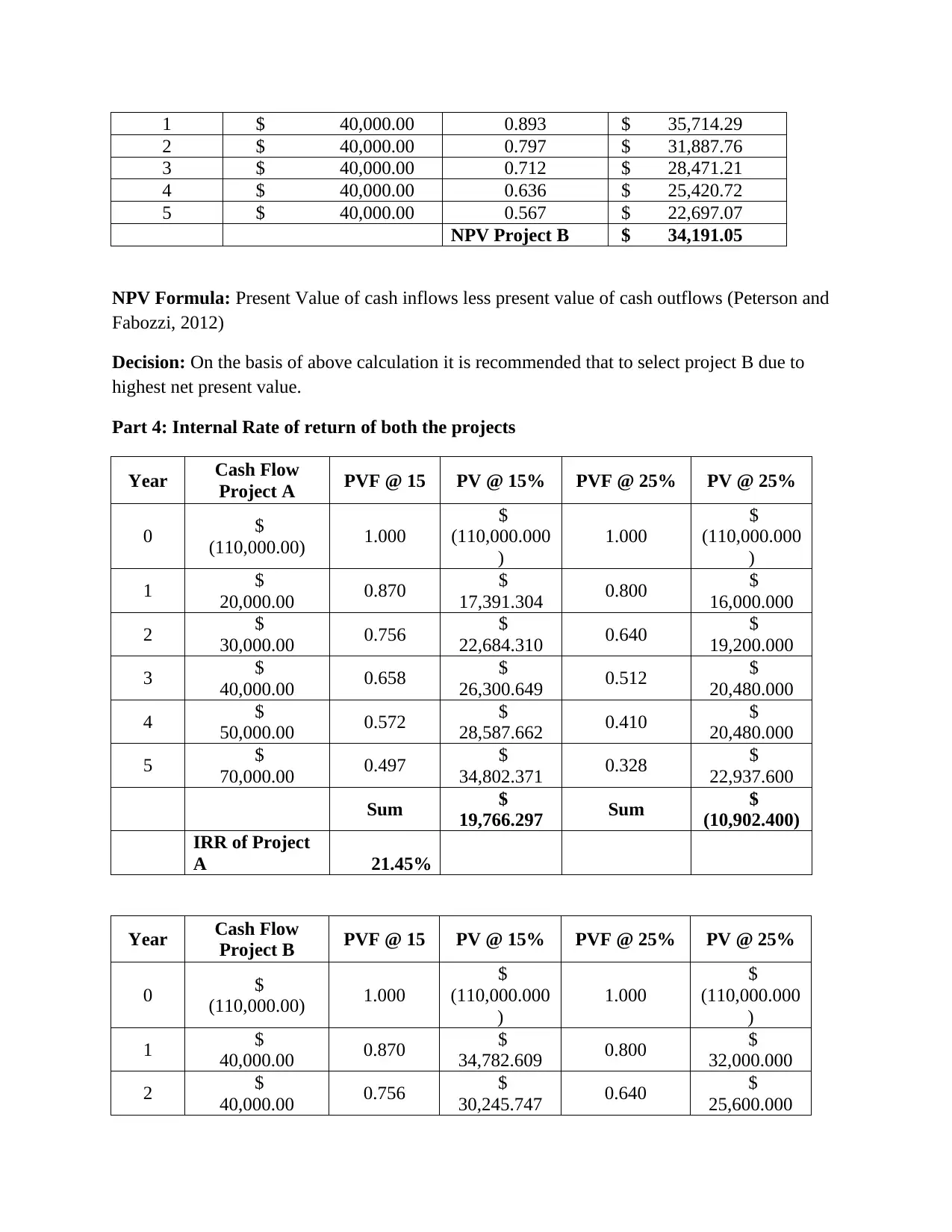

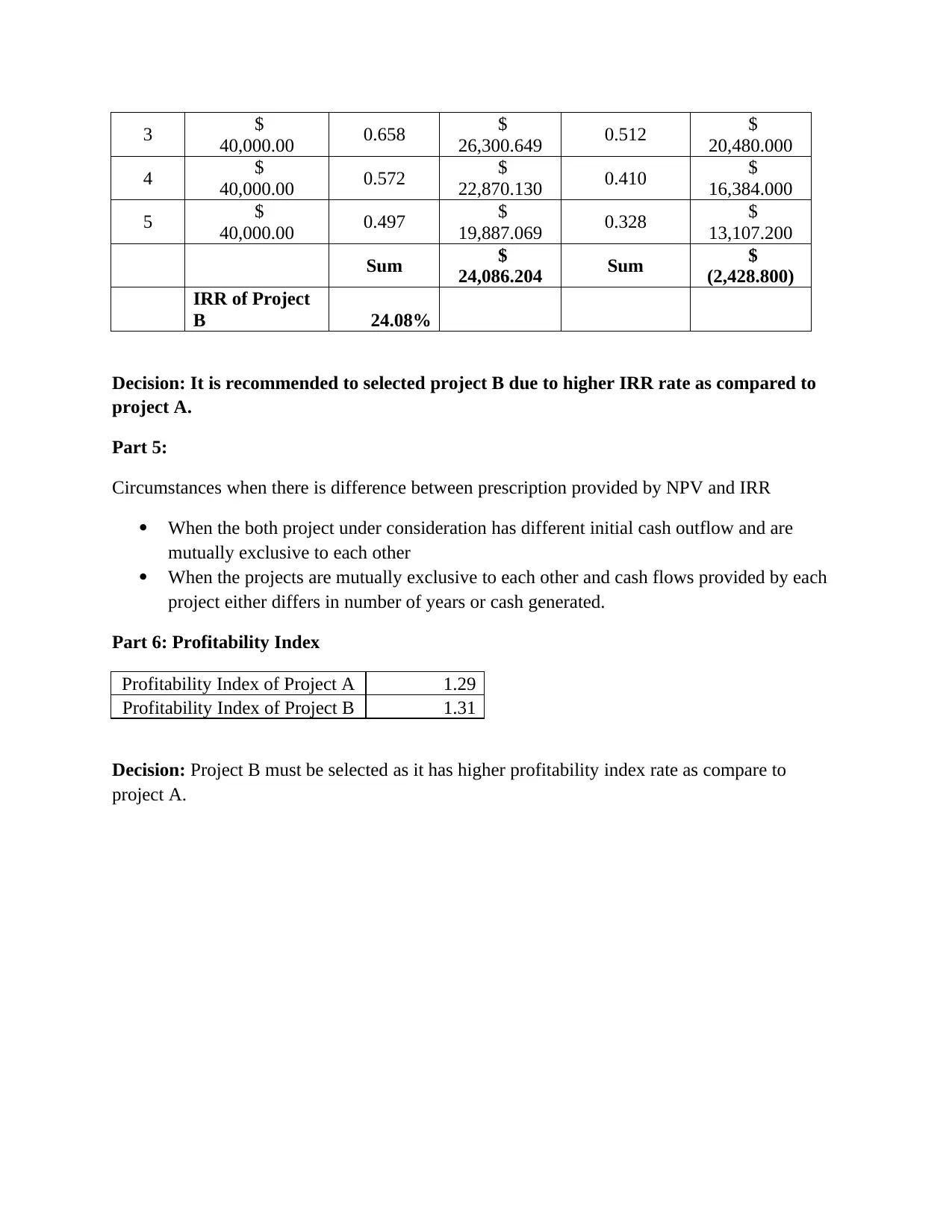

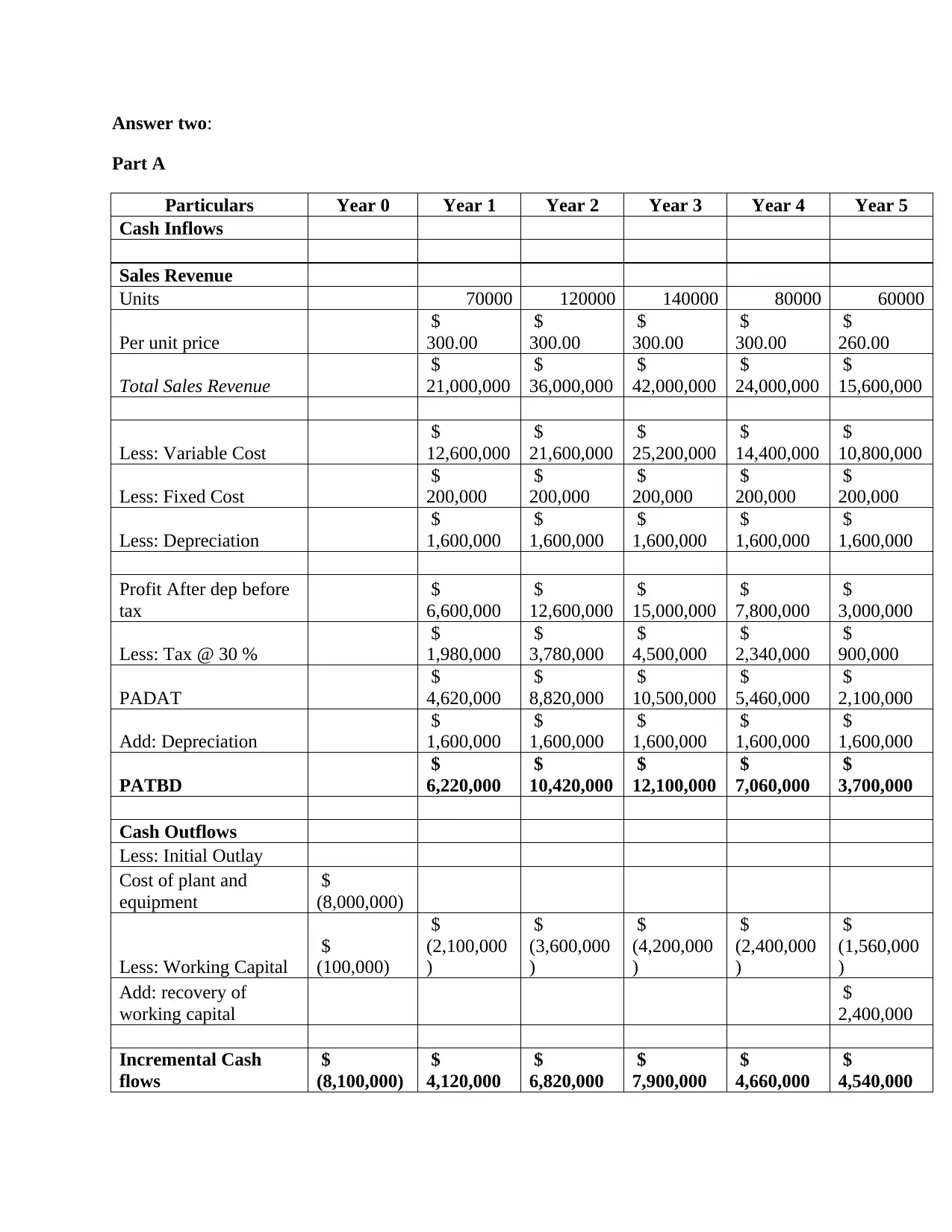

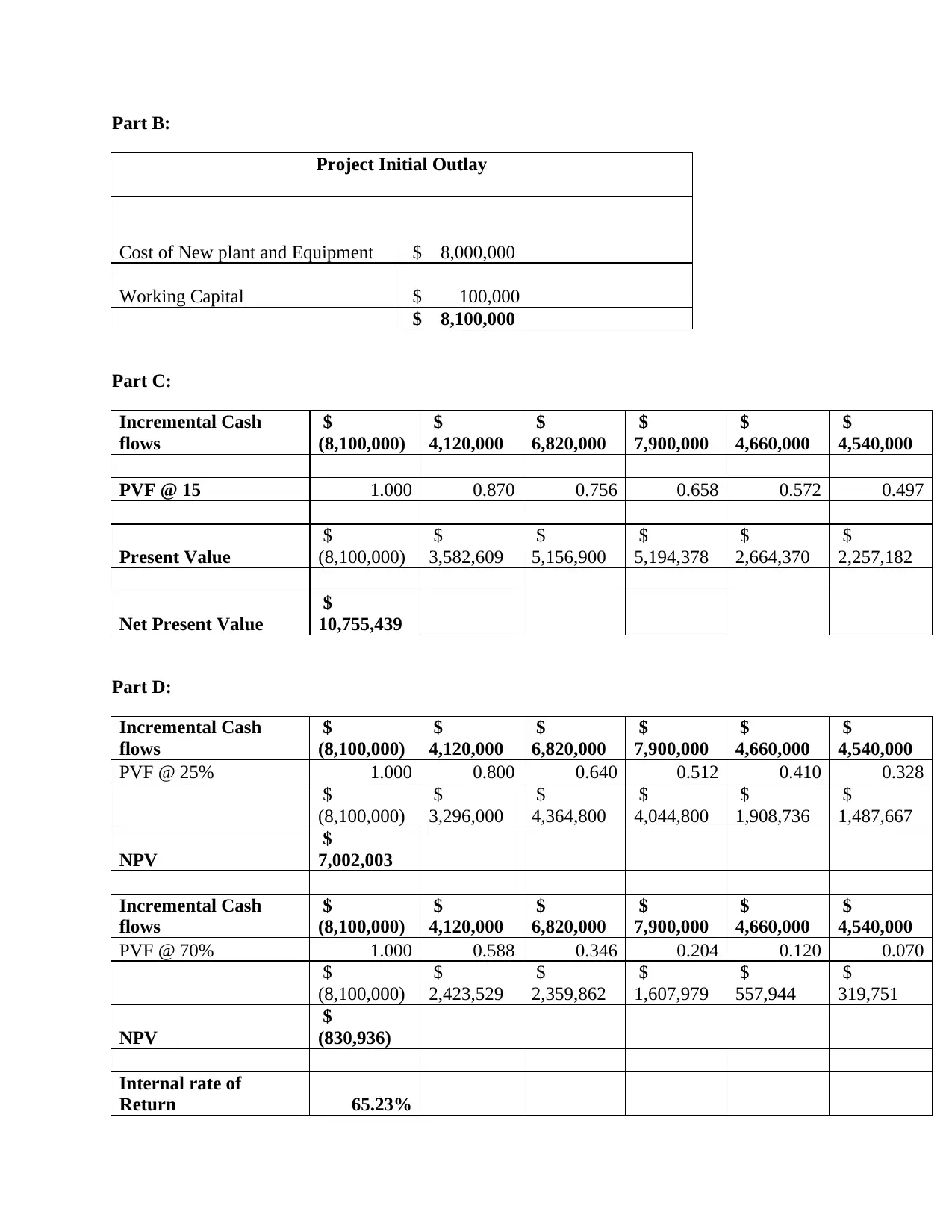

This finance assignment solution delves into project evaluation techniques, providing a comprehensive analysis of two projects using various financial metrics. The assignment starts by defining and explaining the significance of discount rates, including the weighted average cost of capital. It then proceeds to evaluate projects using the payback period method, recommending a project based on its shorter payback time. The core of the assignment focuses on net present value (NPV) and internal rate of return (IRR) calculations, comparing the profitability of two projects and recommending the selection of the project with the higher NPV and IRR. The assignment also discusses circumstances where NPV and IRR prescriptions differ. Furthermore, the solution calculates and interprets the profitability index (PI) to aid in project selection. The second part of the assignment involves a detailed cash flow analysis for a new project, including incremental cash flow calculations, NPV, and IRR under different discount rates, culminating in a recommendation on whether to accept the project based on the financial analysis. References to academic sources are included to support the analysis.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.