Capital Budgeting: Calculation of Payback Period, NPV, IRR and Profitability Index

Added on 2023-06-05

7 Pages1151 Words393 Views

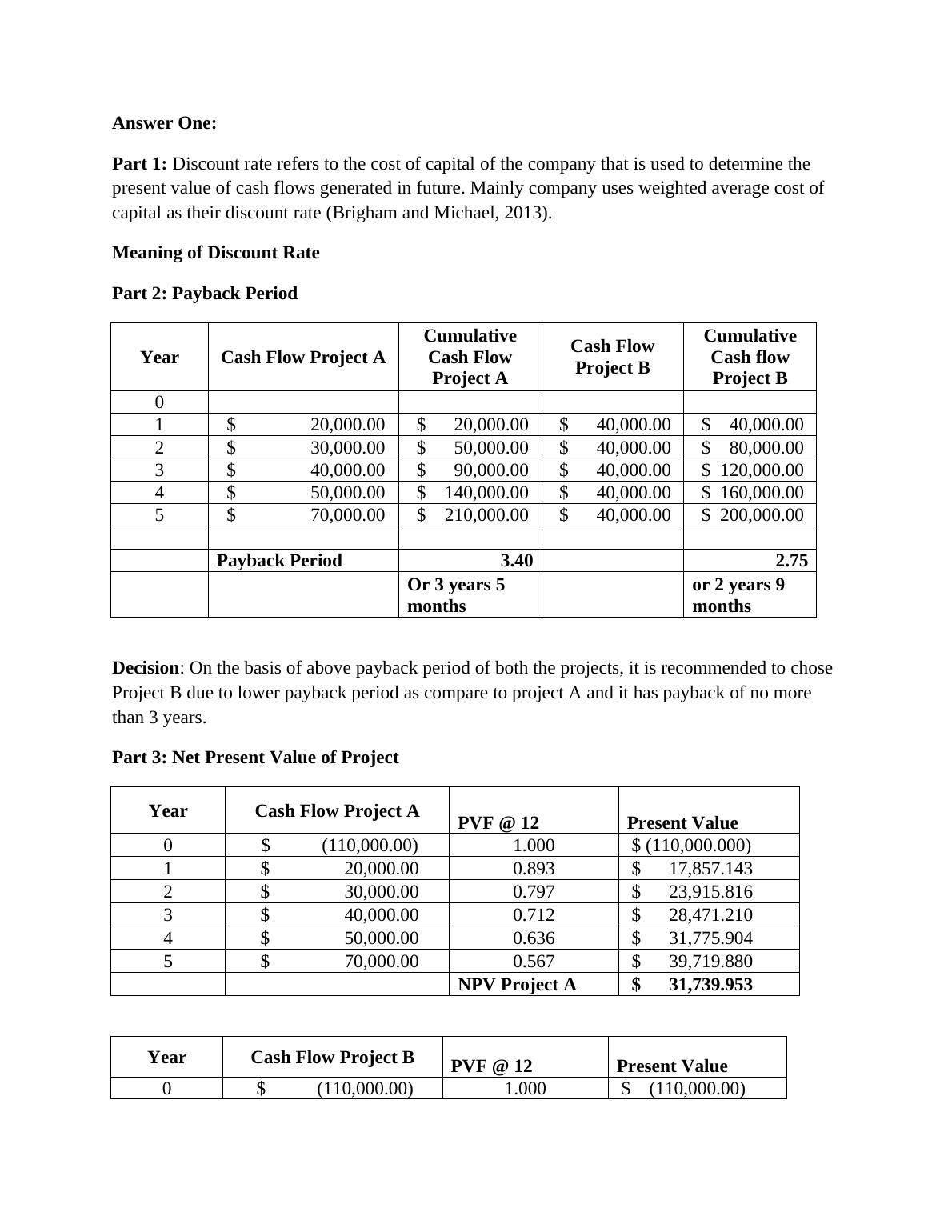

Answer One:

Part 1: Discount rate refers to the cost of capital of the company that is used to determine the

present value of cash flows generated in future. Mainly company uses weighted average cost of

capital as their discount rate (Brigham and Michael, 2013).

Meaning of Discount Rate

Part 2: Payback Period

Year Cash Flow Project A

Cumulative

Cash Flow

Project A

Cash Flow

Project B

Cumulative

Cash flow

Project B

0

1 $ 20,000.00 $ 20,000.00 $ 40,000.00 $ 40,000.00

2 $ 30,000.00 $ 50,000.00 $ 40,000.00 $ 80,000.00

3 $ 40,000.00 $ 90,000.00 $ 40,000.00 $ 120,000.00

4 $ 50,000.00 $ 140,000.00 $ 40,000.00 $ 160,000.00

5 $ 70,000.00 $ 210,000.00 $ 40,000.00 $ 200,000.00

Payback Period 3.40 2.75

Or 3 years 5

months

or 2 years 9

months

Decision: On the basis of above payback period of both the projects, it is recommended to chose

Project B due to lower payback period as compare to project A and it has payback of no more

than 3 years.

Part 3: Net Present Value of Project

Year Cash Flow Project A PVF @ 12 Present Value

0 $ (110,000.00) 1.000 $ (110,000.000)

1 $ 20,000.00 0.893 $ 17,857.143

2 $ 30,000.00 0.797 $ 23,915.816

3 $ 40,000.00 0.712 $ 28,471.210

4 $ 50,000.00 0.636 $ 31,775.904

5 $ 70,000.00 0.567 $ 39,719.880

NPV Project A $ 31,739.953

Year Cash Flow Project B PVF @ 12 Present Value

0 $ (110,000.00) 1.000 $ (110,000.00)

Part 1: Discount rate refers to the cost of capital of the company that is used to determine the

present value of cash flows generated in future. Mainly company uses weighted average cost of

capital as their discount rate (Brigham and Michael, 2013).

Meaning of Discount Rate

Part 2: Payback Period

Year Cash Flow Project A

Cumulative

Cash Flow

Project A

Cash Flow

Project B

Cumulative

Cash flow

Project B

0

1 $ 20,000.00 $ 20,000.00 $ 40,000.00 $ 40,000.00

2 $ 30,000.00 $ 50,000.00 $ 40,000.00 $ 80,000.00

3 $ 40,000.00 $ 90,000.00 $ 40,000.00 $ 120,000.00

4 $ 50,000.00 $ 140,000.00 $ 40,000.00 $ 160,000.00

5 $ 70,000.00 $ 210,000.00 $ 40,000.00 $ 200,000.00

Payback Period 3.40 2.75

Or 3 years 5

months

or 2 years 9

months

Decision: On the basis of above payback period of both the projects, it is recommended to chose

Project B due to lower payback period as compare to project A and it has payback of no more

than 3 years.

Part 3: Net Present Value of Project

Year Cash Flow Project A PVF @ 12 Present Value

0 $ (110,000.00) 1.000 $ (110,000.000)

1 $ 20,000.00 0.893 $ 17,857.143

2 $ 30,000.00 0.797 $ 23,915.816

3 $ 40,000.00 0.712 $ 28,471.210

4 $ 50,000.00 0.636 $ 31,775.904

5 $ 70,000.00 0.567 $ 39,719.880

NPV Project A $ 31,739.953

Year Cash Flow Project B PVF @ 12 Present Value

0 $ (110,000.00) 1.000 $ (110,000.00)

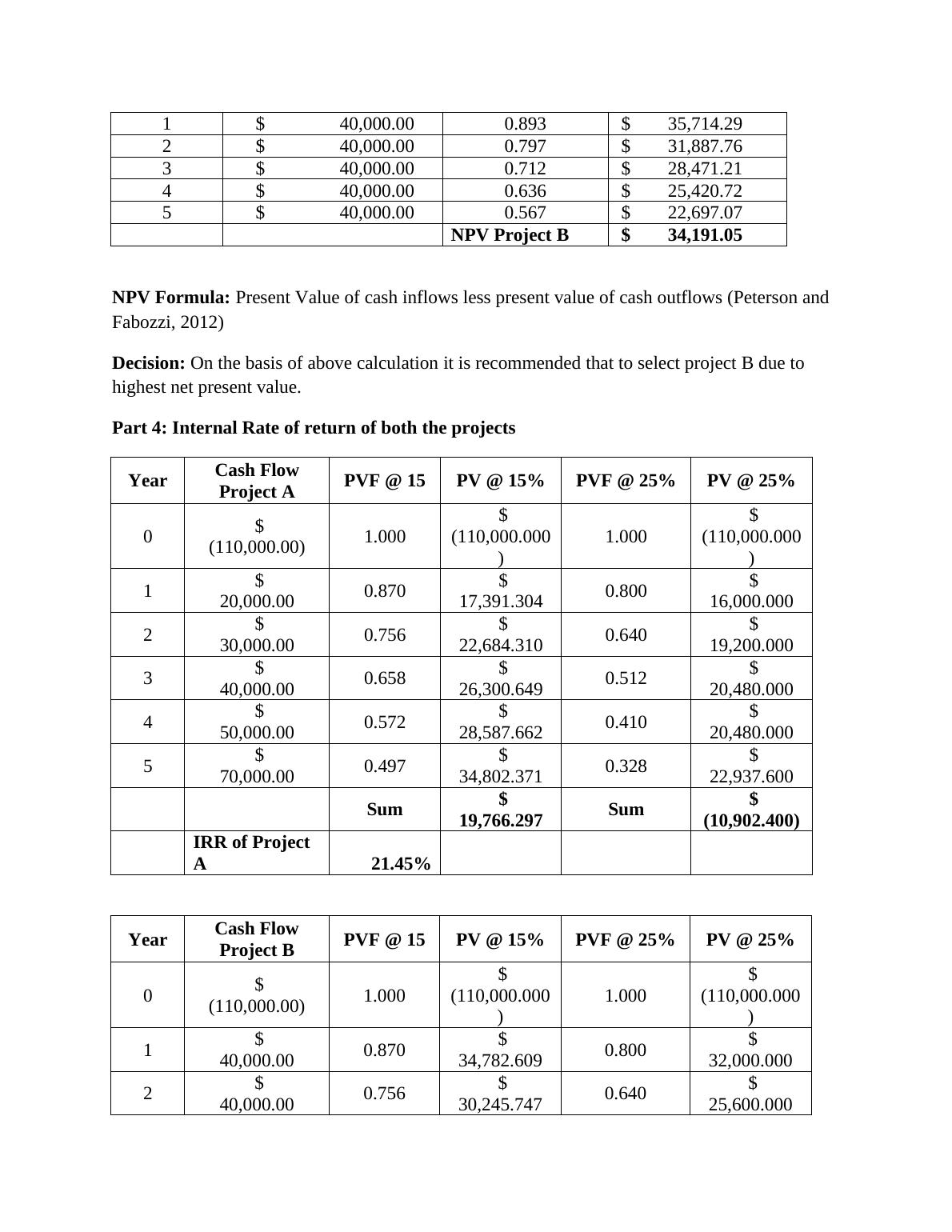

1 $ 40,000.00 0.893 $ 35,714.29

2 $ 40,000.00 0.797 $ 31,887.76

3 $ 40,000.00 0.712 $ 28,471.21

4 $ 40,000.00 0.636 $ 25,420.72

5 $ 40,000.00 0.567 $ 22,697.07

NPV Project B $ 34,191.05

NPV Formula: Present Value of cash inflows less present value of cash outflows (Peterson and

Fabozzi, 2012)

Decision: On the basis of above calculation it is recommended that to select project B due to

highest net present value.

Part 4: Internal Rate of return of both the projects

Year Cash Flow

Project A PVF @ 15 PV @ 15% PVF @ 25% PV @ 25%

0 $

(110,000.00) 1.000

$

(110,000.000

)

1.000

$

(110,000.000

)

1 $

20,000.00 0.870 $

17,391.304 0.800 $

16,000.000

2 $

30,000.00 0.756 $

22,684.310 0.640 $

19,200.000

3 $

40,000.00 0.658 $

26,300.649 0.512 $

20,480.000

4 $

50,000.00 0.572 $

28,587.662 0.410 $

20,480.000

5 $

70,000.00 0.497 $

34,802.371 0.328 $

22,937.600

Sum $

19,766.297 Sum $

(10,902.400)

IRR of Project

A 21.45%

Year Cash Flow

Project B PVF @ 15 PV @ 15% PVF @ 25% PV @ 25%

0 $

(110,000.00) 1.000

$

(110,000.000

)

1.000

$

(110,000.000

)

1 $

40,000.00 0.870 $

34,782.609 0.800 $

32,000.000

2 $

40,000.00 0.756 $

30,245.747 0.640 $

25,600.000

2 $ 40,000.00 0.797 $ 31,887.76

3 $ 40,000.00 0.712 $ 28,471.21

4 $ 40,000.00 0.636 $ 25,420.72

5 $ 40,000.00 0.567 $ 22,697.07

NPV Project B $ 34,191.05

NPV Formula: Present Value of cash inflows less present value of cash outflows (Peterson and

Fabozzi, 2012)

Decision: On the basis of above calculation it is recommended that to select project B due to

highest net present value.

Part 4: Internal Rate of return of both the projects

Year Cash Flow

Project A PVF @ 15 PV @ 15% PVF @ 25% PV @ 25%

0 $

(110,000.00) 1.000

$

(110,000.000

)

1.000

$

(110,000.000

)

1 $

20,000.00 0.870 $

17,391.304 0.800 $

16,000.000

2 $

30,000.00 0.756 $

22,684.310 0.640 $

19,200.000

3 $

40,000.00 0.658 $

26,300.649 0.512 $

20,480.000

4 $

50,000.00 0.572 $

28,587.662 0.410 $

20,480.000

5 $

70,000.00 0.497 $

34,802.371 0.328 $

22,937.600

Sum $

19,766.297 Sum $

(10,902.400)

IRR of Project

A 21.45%

Year Cash Flow

Project B PVF @ 15 PV @ 15% PVF @ 25% PV @ 25%

0 $

(110,000.00) 1.000

$

(110,000.000

)

1.000

$

(110,000.000

)

1 $

40,000.00 0.870 $

34,782.609 0.800 $

32,000.000

2 $

40,000.00 0.756 $

30,245.747 0.640 $

25,600.000

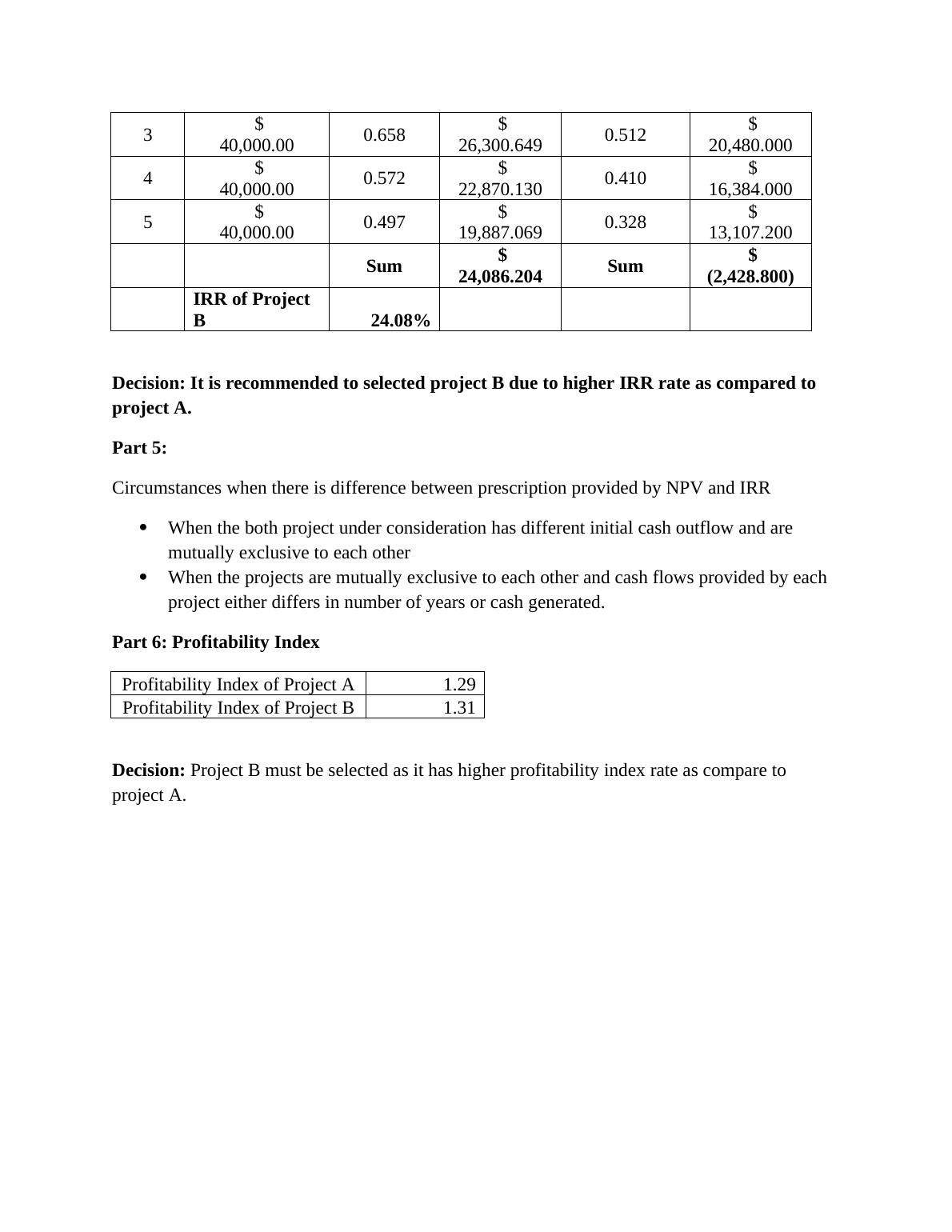

3 $

40,000.00 0.658 $

26,300.649 0.512 $

20,480.000

4 $

40,000.00 0.572 $

22,870.130 0.410 $

16,384.000

5 $

40,000.00 0.497 $

19,887.069 0.328 $

13,107.200

Sum $

24,086.204 Sum $

(2,428.800)

IRR of Project

B 24.08%

Decision: It is recommended to selected project B due to higher IRR rate as compared to

project A.

Part 5:

Circumstances when there is difference between prescription provided by NPV and IRR

When the both project under consideration has different initial cash outflow and are

mutually exclusive to each other

When the projects are mutually exclusive to each other and cash flows provided by each

project either differs in number of years or cash generated.

Part 6: Profitability Index

Profitability Index of Project A 1.29

Profitability Index of Project B 1.31

Decision: Project B must be selected as it has higher profitability index rate as compare to

project A.

40,000.00 0.658 $

26,300.649 0.512 $

20,480.000

4 $

40,000.00 0.572 $

22,870.130 0.410 $

16,384.000

5 $

40,000.00 0.497 $

19,887.069 0.328 $

13,107.200

Sum $

24,086.204 Sum $

(2,428.800)

IRR of Project

B 24.08%

Decision: It is recommended to selected project B due to higher IRR rate as compared to

project A.

Part 5:

Circumstances when there is difference between prescription provided by NPV and IRR

When the both project under consideration has different initial cash outflow and are

mutually exclusive to each other

When the projects are mutually exclusive to each other and cash flows provided by each

project either differs in number of years or cash generated.

Part 6: Profitability Index

Profitability Index of Project A 1.29

Profitability Index of Project B 1.31

Decision: Project B must be selected as it has higher profitability index rate as compare to

project A.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Management: Concepts and Techniqueslg...

|12

|2012

|441

Capital Budgeting and Business Valuation: FIN 505 – FALL 2018lg...

|8

|1607

|81

Capital Budgeting | Assignment-1lg...

|9

|1291

|22