ACC701 - Capital Budgeting Techniques for Investment Appraisal

VerifiedAdded on 2023/06/15

|11

|2353

|295

Homework Assignment

AI Summary

This assignment provides a detailed appraisal of capital investments using various techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, and Annual Rate of Return (ARR). It analyzes two investment options for Noothercompany Limited, evaluating their financial viability and recommending the most suitable choice based on the calculated metrics. The assignment also discusses the importance of sensitivity analysis in capital budgeting, highlighting key variables that should be sensitized due to the fluctuating cash flows. Furthermore, it examines the Return on Investment (ROI) and Residual Income (RI) of two divisions, Queensland (QLD) and New South Wales (NSW), providing a comparative analysis of their performance and discussing the strengths and weaknesses of each measure. Finally, the assignment includes a profit and loss budget for Last Chance Group Limited over five years, applying discounted cash flow techniques to determine the project's NPV and IRR, and concludes with a discussion of the advantages and disadvantages of budgeting.

Running Head: Appraisal of Capital Investments

Capital Budgeting Techniques

Capital Budgeting Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 1

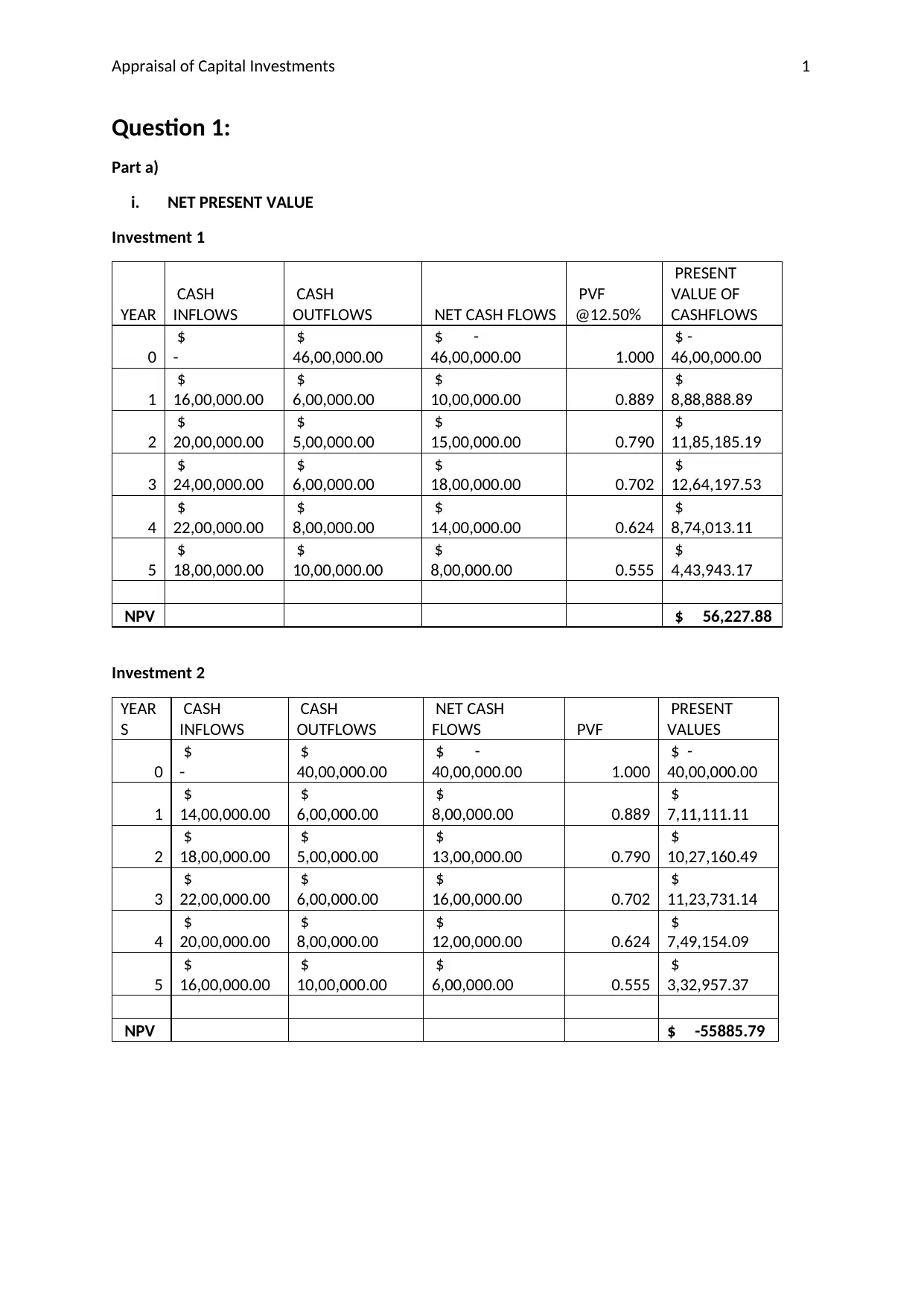

Question 1:

Part a)

i. NET PRESENT VALUE

Investment 1

YEAR

CASH

INFLOWS

CASH

OUTFLOWS NET CASH FLOWS

PVF

@12.50%

PRESENT

VALUE OF

CASHFLOWS

0

$

-

$

46,00,000.00

$ -

46,00,000.00 1.000

$ -

46,00,000.00

1

$

16,00,000.00

$

6,00,000.00

$

10,00,000.00 0.889

$

8,88,888.89

2

$

20,00,000.00

$

5,00,000.00

$

15,00,000.00 0.790

$

11,85,185.19

3

$

24,00,000.00

$

6,00,000.00

$

18,00,000.00 0.702

$

12,64,197.53

4

$

22,00,000.00

$

8,00,000.00

$

14,00,000.00 0.624

$

8,74,013.11

5

$

18,00,000.00

$

10,00,000.00

$

8,00,000.00 0.555

$

4,43,943.17

NPV $ 56,227.88

Investment 2

YEAR

S

CASH

INFLOWS

CASH

OUTFLOWS

NET CASH

FLOWS PVF

PRESENT

VALUES

0

$

-

$

40,00,000.00

$ -

40,00,000.00 1.000

$ -

40,00,000.00

1

$

14,00,000.00

$

6,00,000.00

$

8,00,000.00 0.889

$

7,11,111.11

2

$

18,00,000.00

$

5,00,000.00

$

13,00,000.00 0.790

$

10,27,160.49

3

$

22,00,000.00

$

6,00,000.00

$

16,00,000.00 0.702

$

11,23,731.14

4

$

20,00,000.00

$

8,00,000.00

$

12,00,000.00 0.624

$

7,49,154.09

5

$

16,00,000.00

$

10,00,000.00

$

6,00,000.00 0.555

$

3,32,957.37

NPV $ -55885.79

Question 1:

Part a)

i. NET PRESENT VALUE

Investment 1

YEAR

CASH

INFLOWS

CASH

OUTFLOWS NET CASH FLOWS

PVF

@12.50%

PRESENT

VALUE OF

CASHFLOWS

0

$

-

$

46,00,000.00

$ -

46,00,000.00 1.000

$ -

46,00,000.00

1

$

16,00,000.00

$

6,00,000.00

$

10,00,000.00 0.889

$

8,88,888.89

2

$

20,00,000.00

$

5,00,000.00

$

15,00,000.00 0.790

$

11,85,185.19

3

$

24,00,000.00

$

6,00,000.00

$

18,00,000.00 0.702

$

12,64,197.53

4

$

22,00,000.00

$

8,00,000.00

$

14,00,000.00 0.624

$

8,74,013.11

5

$

18,00,000.00

$

10,00,000.00

$

8,00,000.00 0.555

$

4,43,943.17

NPV $ 56,227.88

Investment 2

YEAR

S

CASH

INFLOWS

CASH

OUTFLOWS

NET CASH

FLOWS PVF

PRESENT

VALUES

0

$

-

$

40,00,000.00

$ -

40,00,000.00 1.000

$ -

40,00,000.00

1

$

14,00,000.00

$

6,00,000.00

$

8,00,000.00 0.889

$

7,11,111.11

2

$

18,00,000.00

$

5,00,000.00

$

13,00,000.00 0.790

$

10,27,160.49

3

$

22,00,000.00

$

6,00,000.00

$

16,00,000.00 0.702

$

11,23,731.14

4

$

20,00,000.00

$

8,00,000.00

$

12,00,000.00 0.624

$

7,49,154.09

5

$

16,00,000.00

$

10,00,000.00

$

6,00,000.00 0.555

$

3,32,957.37

NPV $ -55885.79

Appraisal of Capital Investments 2

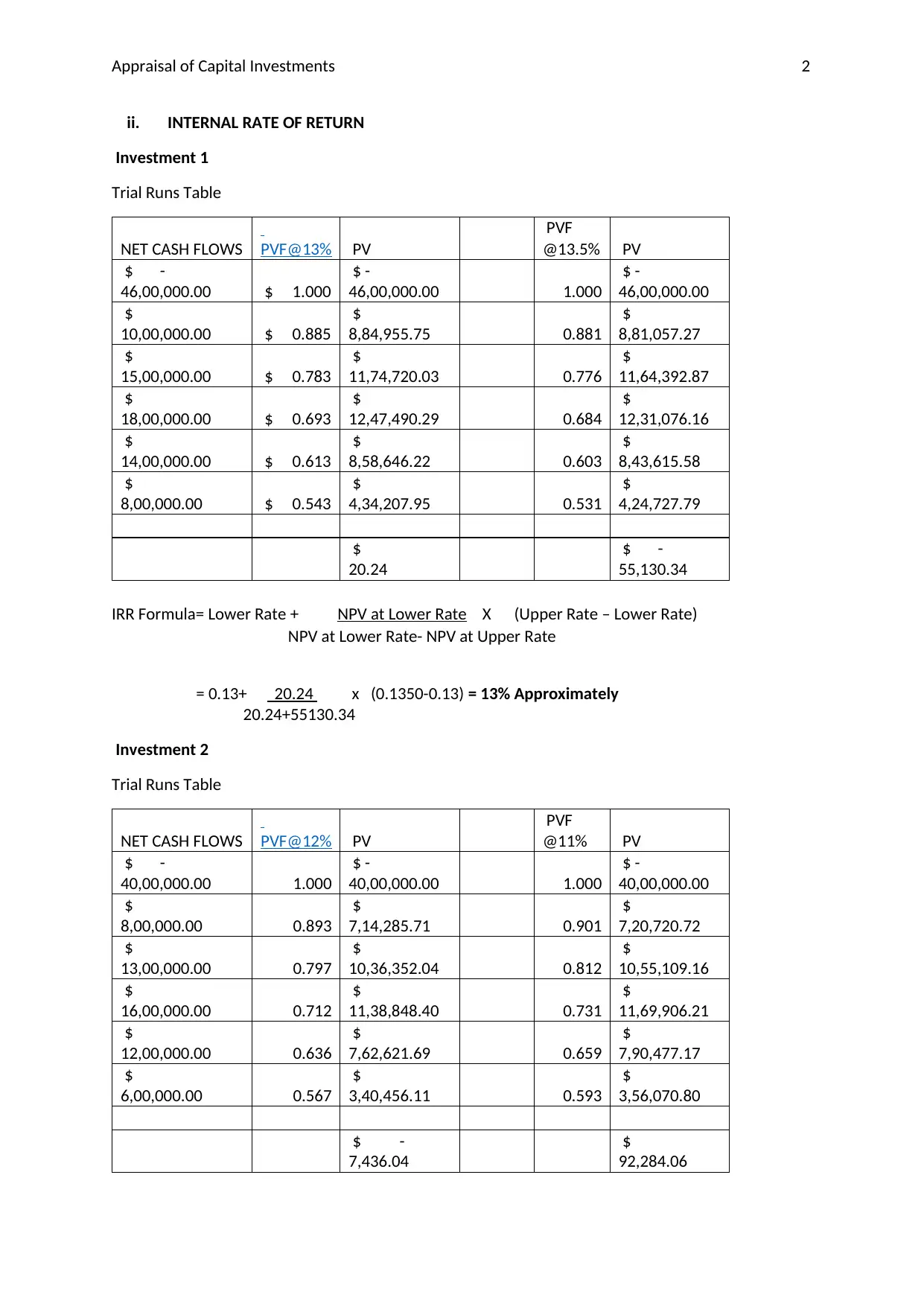

ii. INTERNAL RATE OF RETURN

Investment 1

Trial Runs Table

NET CASH FLOWS PVF@13% PV

PVF

@13.5% PV

$ -

46,00,000.00 $ 1.000

$ -

46,00,000.00 1.000

$ -

46,00,000.00

$

10,00,000.00 $ 0.885

$

8,84,955.75 0.881

$

8,81,057.27

$

15,00,000.00 $ 0.783

$

11,74,720.03 0.776

$

11,64,392.87

$

18,00,000.00 $ 0.693

$

12,47,490.29 0.684

$

12,31,076.16

$

14,00,000.00 $ 0.613

$

8,58,646.22 0.603

$

8,43,615.58

$

8,00,000.00 $ 0.543

$

4,34,207.95 0.531

$

4,24,727.79

$

20.24

$ -

55,130.34

IRR Formula= Lower Rate + NPV at Lower Rate X (Upper Rate – Lower Rate)

NPV at Lower Rate- NPV at Upper Rate

= 0.13+ 20.24 x (0.1350-0.13) = 13% Approximately

20.24+55130.34

Investment 2

Trial Runs Table

NET CASH FLOWS PVF@12% PV

PVF

@11% PV

$ -

40,00,000.00 1.000

$ -

40,00,000.00 1.000

$ -

40,00,000.00

$

8,00,000.00 0.893

$

7,14,285.71 0.901

$

7,20,720.72

$

13,00,000.00 0.797

$

10,36,352.04 0.812

$

10,55,109.16

$

16,00,000.00 0.712

$

11,38,848.40 0.731

$

11,69,906.21

$

12,00,000.00 0.636

$

7,62,621.69 0.659

$

7,90,477.17

$

6,00,000.00 0.567

$

3,40,456.11 0.593

$

3,56,070.80

$ -

7,436.04

$

92,284.06

ii. INTERNAL RATE OF RETURN

Investment 1

Trial Runs Table

NET CASH FLOWS PVF@13% PV

PVF

@13.5% PV

$ -

46,00,000.00 $ 1.000

$ -

46,00,000.00 1.000

$ -

46,00,000.00

$

10,00,000.00 $ 0.885

$

8,84,955.75 0.881

$

8,81,057.27

$

15,00,000.00 $ 0.783

$

11,74,720.03 0.776

$

11,64,392.87

$

18,00,000.00 $ 0.693

$

12,47,490.29 0.684

$

12,31,076.16

$

14,00,000.00 $ 0.613

$

8,58,646.22 0.603

$

8,43,615.58

$

8,00,000.00 $ 0.543

$

4,34,207.95 0.531

$

4,24,727.79

$

20.24

$ -

55,130.34

IRR Formula= Lower Rate + NPV at Lower Rate X (Upper Rate – Lower Rate)

NPV at Lower Rate- NPV at Upper Rate

= 0.13+ 20.24 x (0.1350-0.13) = 13% Approximately

20.24+55130.34

Investment 2

Trial Runs Table

NET CASH FLOWS PVF@12% PV

PVF

@11% PV

$ -

40,00,000.00 1.000

$ -

40,00,000.00 1.000

$ -

40,00,000.00

$

8,00,000.00 0.893

$

7,14,285.71 0.901

$

7,20,720.72

$

13,00,000.00 0.797

$

10,36,352.04 0.812

$

10,55,109.16

$

16,00,000.00 0.712

$

11,38,848.40 0.731

$

11,69,906.21

$

12,00,000.00 0.636

$

7,62,621.69 0.659

$

7,90,477.17

$

6,00,000.00 0.567

$

3,40,456.11 0.593

$

3,56,070.80

$ -

7,436.04

$

92,284.06

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appraisal of Capital Investments 3

IRR FORMULA= 0.13+ 7436.04 x (0.12-0.11) = 11.92% Approximately

92284.06+7436.04

iii. PAYBACK PERIOD

Investment 1

Table for discounted payback period

YEARS NET CASH FLOWS PVF

PRESENT

VALUE OF

CASHFLOWS

CUMULATIVE

PV OF

CASHFLOWS

0

$ -

46,00,000.00 1.000

$ -

46,00,000.00

$ -

46,00,000.00

1

$

10,00,000.00 0.889

$

8,88,888.89

$ -

37,11,111.11

2

$

15,00,000.00 0.790

$

11,85,185.19

$ -

25,25,925.93

3

$

18,00,000.00 0.702

$

12,64,197.53

$ -

12,61,728.40

4

$

14,00,000.00 0.624

$

8,74,013.11

$ -

3,87,715.29

5

$

8,00,000.00 0.555

$

4,43,943.17

$

56,227.88

PAYBACK

PERIOD 4.87 years

Payback period =4 + -3, 87,715.29

4, 43,943.17

=4.87 Years

Investment 2

Note: As the NPV of the Investment 2 is negative, it would not have any Payback period as the cost

of the initial investment would not be recovered during the entire project life.

iv. ANNUAL RATE OF RETURN

ARR = Average net income after depreciation and taxes

Initial investment

IRR FORMULA= 0.13+ 7436.04 x (0.12-0.11) = 11.92% Approximately

92284.06+7436.04

iii. PAYBACK PERIOD

Investment 1

Table for discounted payback period

YEARS NET CASH FLOWS PVF

PRESENT

VALUE OF

CASHFLOWS

CUMULATIVE

PV OF

CASHFLOWS

0

$ -

46,00,000.00 1.000

$ -

46,00,000.00

$ -

46,00,000.00

1

$

10,00,000.00 0.889

$

8,88,888.89

$ -

37,11,111.11

2

$

15,00,000.00 0.790

$

11,85,185.19

$ -

25,25,925.93

3

$

18,00,000.00 0.702

$

12,64,197.53

$ -

12,61,728.40

4

$

14,00,000.00 0.624

$

8,74,013.11

$ -

3,87,715.29

5

$

8,00,000.00 0.555

$

4,43,943.17

$

56,227.88

PAYBACK

PERIOD 4.87 years

Payback period =4 + -3, 87,715.29

4, 43,943.17

=4.87 Years

Investment 2

Note: As the NPV of the Investment 2 is negative, it would not have any Payback period as the cost

of the initial investment would not be recovered during the entire project life.

iv. ANNUAL RATE OF RETURN

ARR = Average net income after depreciation and taxes

Initial investment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 4

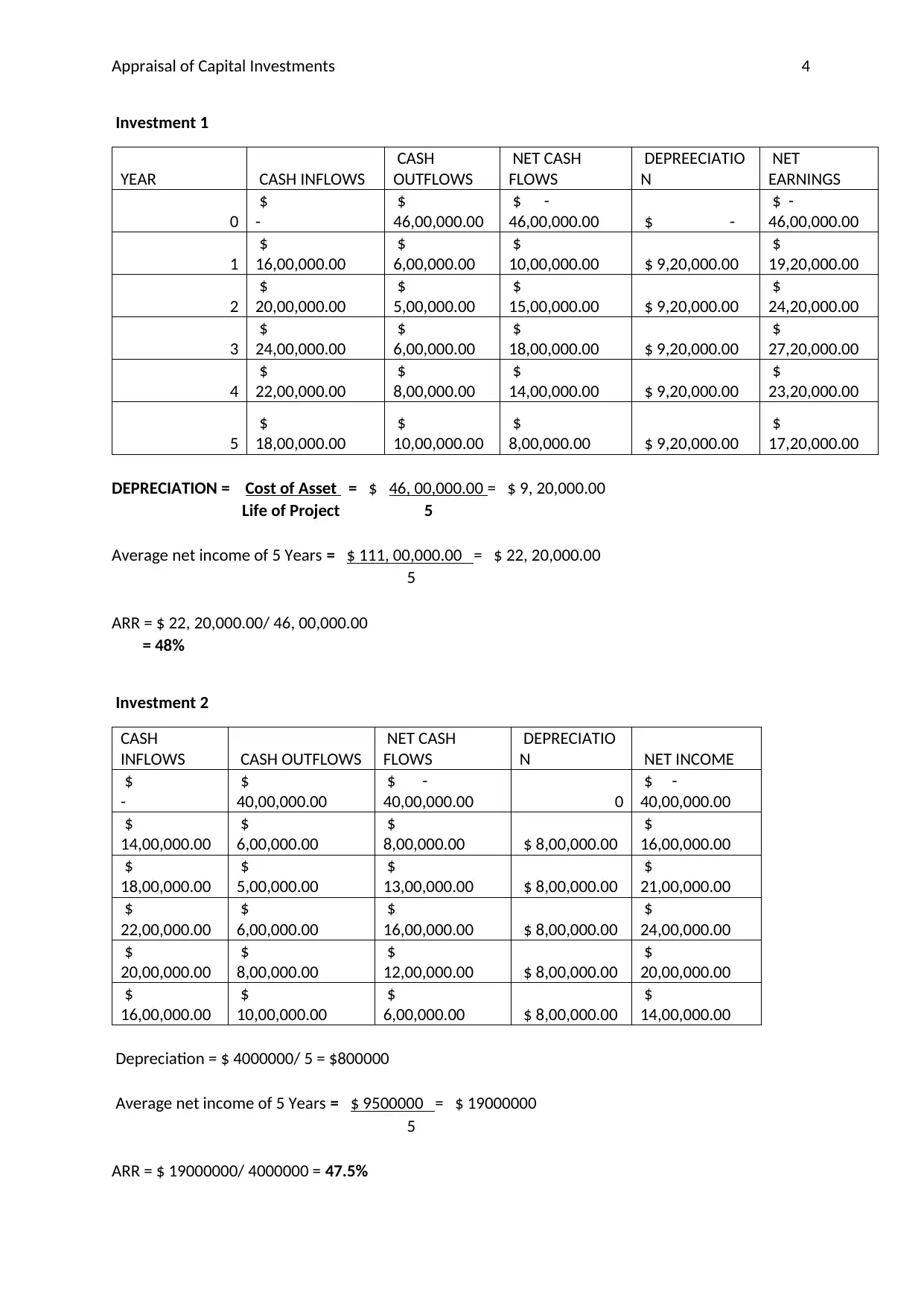

Investment 1

YEAR CASH INFLOWS

CASH

OUTFLOWS

NET CASH

FLOWS

DEPREECIATIO

N

NET

EARNINGS

0

$

-

$

46,00,000.00

$ -

46,00,000.00 $ -

$ -

46,00,000.00

1

$

16,00,000.00

$

6,00,000.00

$

10,00,000.00 $ 9,20,000.00

$

19,20,000.00

2

$

20,00,000.00

$

5,00,000.00

$

15,00,000.00 $ 9,20,000.00

$

24,20,000.00

3

$

24,00,000.00

$

6,00,000.00

$

18,00,000.00 $ 9,20,000.00

$

27,20,000.00

4

$

22,00,000.00

$

8,00,000.00

$

14,00,000.00 $ 9,20,000.00

$

23,20,000.00

5

$

18,00,000.00

$

10,00,000.00

$

8,00,000.00 $ 9,20,000.00

$

17,20,000.00

DEPRECIATION = Cost of Asset = $ 46, 00,000.00 = $ 9, 20,000.00

Life of Project 5

Average net income of 5 Years = $ 111, 00,000.00 = $ 22, 20,000.00

5

ARR = $ 22, 20,000.00/ 46, 00,000.00

= 48%

Investment 2

CASH

INFLOWS CASH OUTFLOWS

NET CASH

FLOWS

DEPRECIATIO

N NET INCOME

$

-

$

40,00,000.00

$ -

40,00,000.00 0

$ -

40,00,000.00

$

14,00,000.00

$

6,00,000.00

$

8,00,000.00 $ 8,00,000.00

$

16,00,000.00

$

18,00,000.00

$

5,00,000.00

$

13,00,000.00 $ 8,00,000.00

$

21,00,000.00

$

22,00,000.00

$

6,00,000.00

$

16,00,000.00 $ 8,00,000.00

$

24,00,000.00

$

20,00,000.00

$

8,00,000.00

$

12,00,000.00 $ 8,00,000.00

$

20,00,000.00

$

16,00,000.00

$

10,00,000.00

$

6,00,000.00 $ 8,00,000.00

$

14,00,000.00

Depreciation = $ 4000000/ 5 = $800000

Average net income of 5 Years = $ 9500000 = $ 19000000

5

ARR = $ 19000000/ 4000000 = 47.5%

Investment 1

YEAR CASH INFLOWS

CASH

OUTFLOWS

NET CASH

FLOWS

DEPREECIATIO

N

NET

EARNINGS

0

$

-

$

46,00,000.00

$ -

46,00,000.00 $ -

$ -

46,00,000.00

1

$

16,00,000.00

$

6,00,000.00

$

10,00,000.00 $ 9,20,000.00

$

19,20,000.00

2

$

20,00,000.00

$

5,00,000.00

$

15,00,000.00 $ 9,20,000.00

$

24,20,000.00

3

$

24,00,000.00

$

6,00,000.00

$

18,00,000.00 $ 9,20,000.00

$

27,20,000.00

4

$

22,00,000.00

$

8,00,000.00

$

14,00,000.00 $ 9,20,000.00

$

23,20,000.00

5

$

18,00,000.00

$

10,00,000.00

$

8,00,000.00 $ 9,20,000.00

$

17,20,000.00

DEPRECIATION = Cost of Asset = $ 46, 00,000.00 = $ 9, 20,000.00

Life of Project 5

Average net income of 5 Years = $ 111, 00,000.00 = $ 22, 20,000.00

5

ARR = $ 22, 20,000.00/ 46, 00,000.00

= 48%

Investment 2

CASH

INFLOWS CASH OUTFLOWS

NET CASH

FLOWS

DEPRECIATIO

N NET INCOME

$

-

$

40,00,000.00

$ -

40,00,000.00 0

$ -

40,00,000.00

$

14,00,000.00

$

6,00,000.00

$

8,00,000.00 $ 8,00,000.00

$

16,00,000.00

$

18,00,000.00

$

5,00,000.00

$

13,00,000.00 $ 8,00,000.00

$

21,00,000.00

$

22,00,000.00

$

6,00,000.00

$

16,00,000.00 $ 8,00,000.00

$

24,00,000.00

$

20,00,000.00

$

8,00,000.00

$

12,00,000.00 $ 8,00,000.00

$

20,00,000.00

$

16,00,000.00

$

10,00,000.00

$

6,00,000.00 $ 8,00,000.00

$

14,00,000.00

Depreciation = $ 4000000/ 5 = $800000

Average net income of 5 Years = $ 9500000 = $ 19000000

5

ARR = $ 19000000/ 4000000 = 47.5%

Appraisal of Capital Investments 5

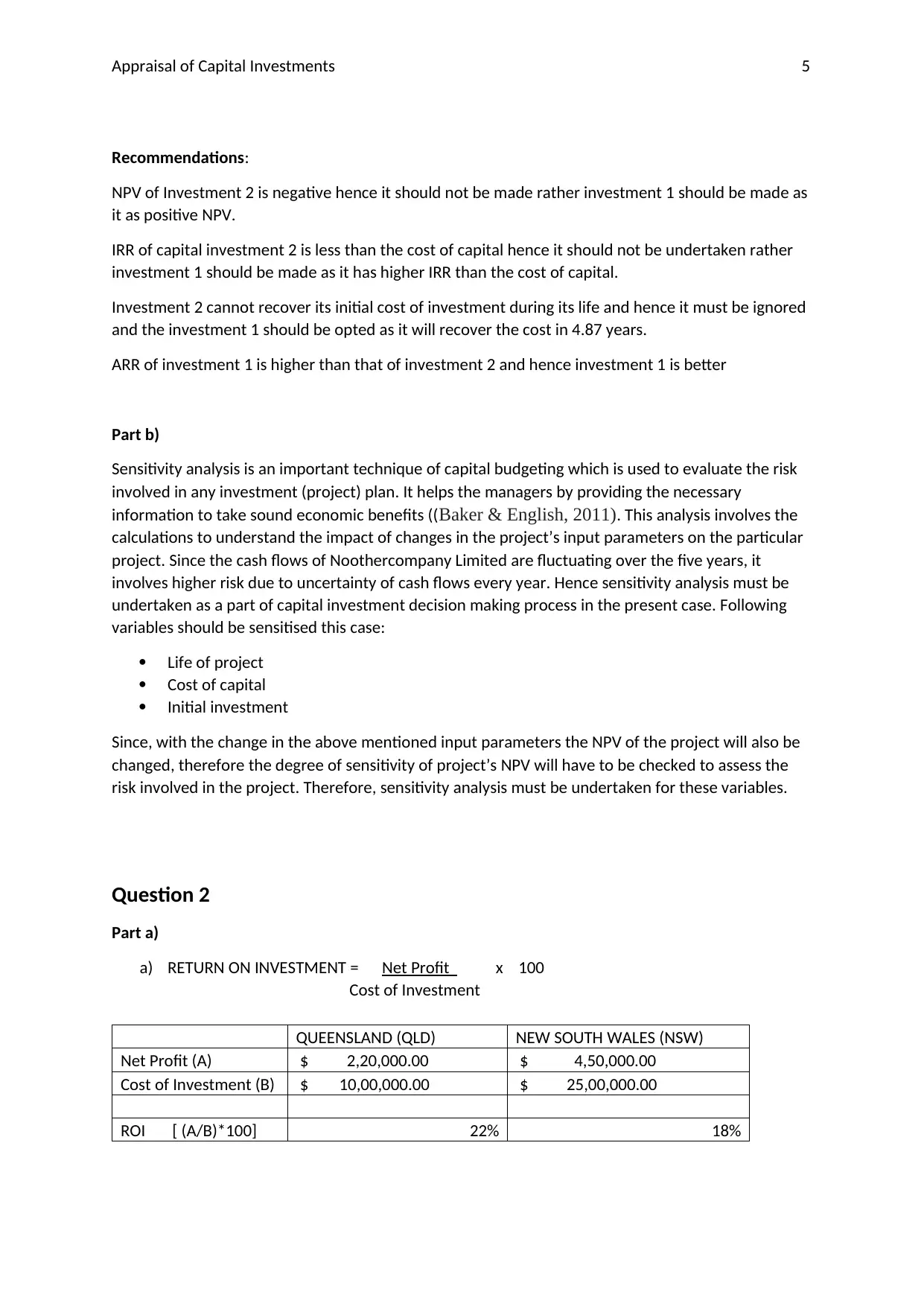

Recommendations:

NPV of Investment 2 is negative hence it should not be made rather investment 1 should be made as

it as positive NPV.

IRR of capital investment 2 is less than the cost of capital hence it should not be undertaken rather

investment 1 should be made as it has higher IRR than the cost of capital.

Investment 2 cannot recover its initial cost of investment during its life and hence it must be ignored

and the investment 1 should be opted as it will recover the cost in 4.87 years.

ARR of investment 1 is higher than that of investment 2 and hence investment 1 is better

Part b)

Sensitivity analysis is an important technique of capital budgeting which is used to evaluate the risk

involved in any investment (project) plan. It helps the managers by providing the necessary

information to take sound economic benefits ((Baker & English, 2011). This analysis involves the

calculations to understand the impact of changes in the project’s input parameters on the particular

project. Since the cash flows of Noothercompany Limited are fluctuating over the five years, it

involves higher risk due to uncertainty of cash flows every year. Hence sensitivity analysis must be

undertaken as a part of capital investment decision making process in the present case. Following

variables should be sensitised this case:

Life of project

Cost of capital

Initial investment

Since, with the change in the above mentioned input parameters the NPV of the project will also be

changed, therefore the degree of sensitivity of project’s NPV will have to be checked to assess the

risk involved in the project. Therefore, sensitivity analysis must be undertaken for these variables.

Question 2

Part a)

a) RETURN ON INVESTMENT = Net Profit x 100

Cost of Investment

QUEENSLAND (QLD) NEW SOUTH WALES (NSW)

Net Profit (A) $ 2,20,000.00 $ 4,50,000.00

Cost of Investment (B) $ 10,00,000.00 $ 25,00,000.00

ROI [ (A/B)*100] 22% 18%

Recommendations:

NPV of Investment 2 is negative hence it should not be made rather investment 1 should be made as

it as positive NPV.

IRR of capital investment 2 is less than the cost of capital hence it should not be undertaken rather

investment 1 should be made as it has higher IRR than the cost of capital.

Investment 2 cannot recover its initial cost of investment during its life and hence it must be ignored

and the investment 1 should be opted as it will recover the cost in 4.87 years.

ARR of investment 1 is higher than that of investment 2 and hence investment 1 is better

Part b)

Sensitivity analysis is an important technique of capital budgeting which is used to evaluate the risk

involved in any investment (project) plan. It helps the managers by providing the necessary

information to take sound economic benefits ((Baker & English, 2011). This analysis involves the

calculations to understand the impact of changes in the project’s input parameters on the particular

project. Since the cash flows of Noothercompany Limited are fluctuating over the five years, it

involves higher risk due to uncertainty of cash flows every year. Hence sensitivity analysis must be

undertaken as a part of capital investment decision making process in the present case. Following

variables should be sensitised this case:

Life of project

Cost of capital

Initial investment

Since, with the change in the above mentioned input parameters the NPV of the project will also be

changed, therefore the degree of sensitivity of project’s NPV will have to be checked to assess the

risk involved in the project. Therefore, sensitivity analysis must be undertaken for these variables.

Question 2

Part a)

a) RETURN ON INVESTMENT = Net Profit x 100

Cost of Investment

QUEENSLAND (QLD) NEW SOUTH WALES (NSW)

Net Profit (A) $ 2,20,000.00 $ 4,50,000.00

Cost of Investment (B) $ 10,00,000.00 $ 25,00,000.00

ROI [ (A/B)*100] 22% 18%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appraisal of Capital Investments 6

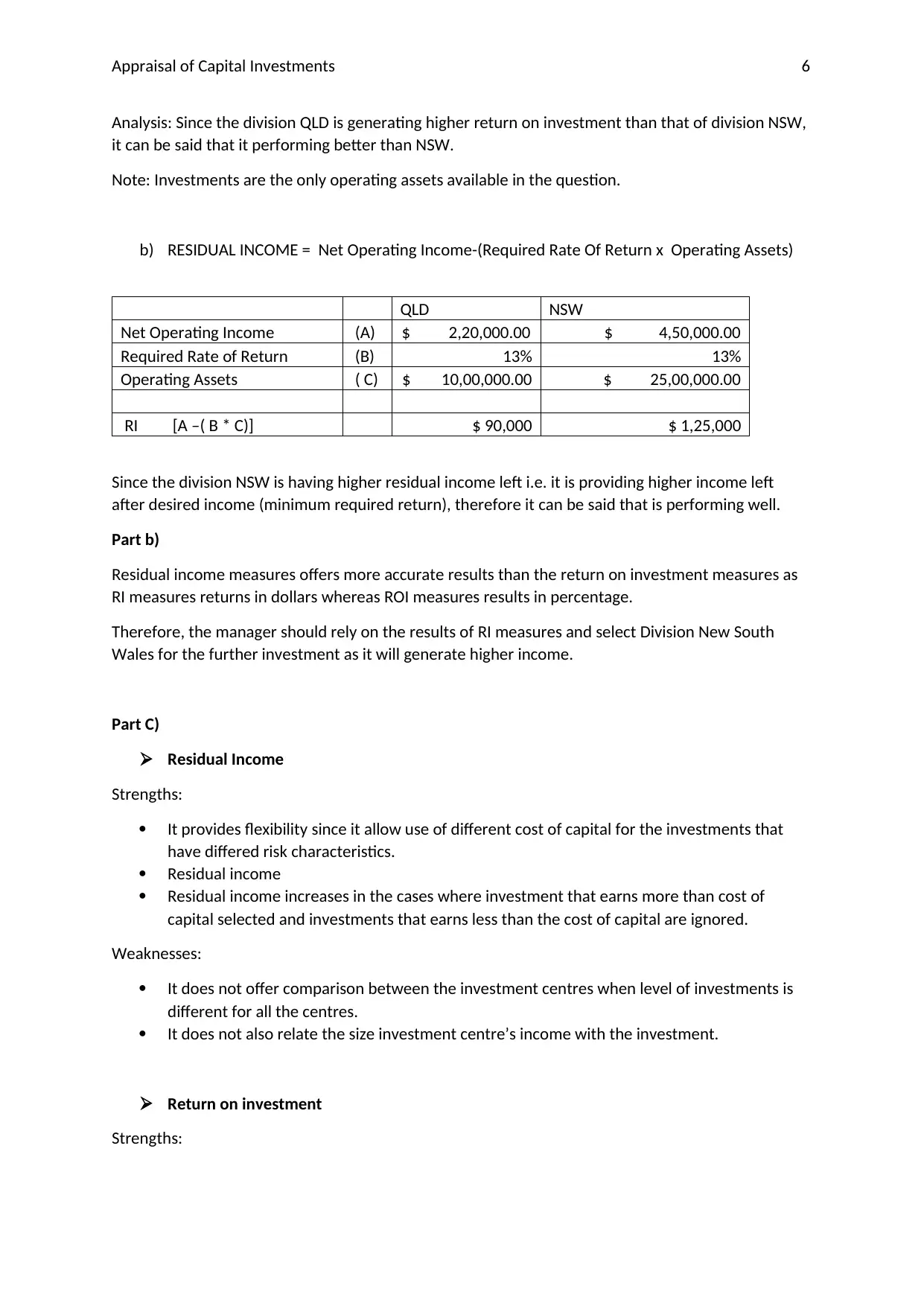

Analysis: Since the division QLD is generating higher return on investment than that of division NSW,

it can be said that it performing better than NSW.

Note: Investments are the only operating assets available in the question.

b) RESIDUAL INCOME = Net Operating Income-(Required Rate Of Return x Operating Assets)

QLD NSW

Net Operating Income (A) $ 2,20,000.00 $ 4,50,000.00

Required Rate of Return (B) 13% 13%

Operating Assets ( C) $ 10,00,000.00 $ 25,00,000.00

RI [A –( B * C)] $ 90,000 $ 1,25,000

Since the division NSW is having higher residual income left i.e. it is providing higher income left

after desired income (minimum required return), therefore it can be said that is performing well.

Part b)

Residual income measures offers more accurate results than the return on investment measures as

RI measures returns in dollars whereas ROI measures results in percentage.

Therefore, the manager should rely on the results of RI measures and select Division New South

Wales for the further investment as it will generate higher income.

Part C)

Residual Income

Strengths:

It provides flexibility since it allow use of different cost of capital for the investments that

have differed risk characteristics.

Residual income

Residual income increases in the cases where investment that earns more than cost of

capital selected and investments that earns less than the cost of capital are ignored.

Weaknesses:

It does not offer comparison between the investment centres when level of investments is

different for all the centres.

It does not also relate the size investment centre’s income with the investment.

Return on investment

Strengths:

Analysis: Since the division QLD is generating higher return on investment than that of division NSW,

it can be said that it performing better than NSW.

Note: Investments are the only operating assets available in the question.

b) RESIDUAL INCOME = Net Operating Income-(Required Rate Of Return x Operating Assets)

QLD NSW

Net Operating Income (A) $ 2,20,000.00 $ 4,50,000.00

Required Rate of Return (B) 13% 13%

Operating Assets ( C) $ 10,00,000.00 $ 25,00,000.00

RI [A –( B * C)] $ 90,000 $ 1,25,000

Since the division NSW is having higher residual income left i.e. it is providing higher income left

after desired income (minimum required return), therefore it can be said that is performing well.

Part b)

Residual income measures offers more accurate results than the return on investment measures as

RI measures returns in dollars whereas ROI measures results in percentage.

Therefore, the manager should rely on the results of RI measures and select Division New South

Wales for the further investment as it will generate higher income.

Part C)

Residual Income

Strengths:

It provides flexibility since it allow use of different cost of capital for the investments that

have differed risk characteristics.

Residual income

Residual income increases in the cases where investment that earns more than cost of

capital selected and investments that earns less than the cost of capital are ignored.

Weaknesses:

It does not offer comparison between the investment centres when level of investments is

different for all the centres.

It does not also relate the size investment centre’s income with the investment.

Return on investment

Strengths:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 7

It serves as benchmark to measure the efficiency of investment or operating assets and

enables the business managers to understand and emphasise on the relationship between

sales, expenses an investments.

It aids managers in making comparison of several business divisions in profitability and asset

utilisation terms (Bierman & Smidt, 2012).

Weaknesses:

It can lead to making dysfunctional decisions that impacts the efficient asset allocation.

The information of sales, costs, assets etc. is difficult to be obtained at times.

Economic value added is the measure used to evaluate the financial performance of the

company on the basis of its residual wealth. It is calculated by deducting firm’s cost of capital

from its net operating profits after taxes.

There is no benefit of using EVA in place of RI in this case as they are similar measures with the

difference that the EVA measure considers operating profits after taxation effect. In this question

there is no tax rate given so use of EVA would not make any difference.

Question 3

Part a)

I. Profit & Loss Budget of Last Chance Group Limited

year 1 year 2 year 3 year 4 year 5

Sales (A) $ 45,00,000.00 $ 65,00,000.00 $85,00,000.00 $ 65,00,000.00 $45,00,000.00

Cost Of Sales (B) $ 15,75,000.00 $ 22,75,000.00 $29,75,000.00 $ 22,75,000.00 $15,75,000.00

Gross Profit C= (A)-(B) $ 29,25,000.00 $ 42,25,000.00 $55,25,000.00 $ 42,25,000.00 $29,25,000.00

Less: Admin & Selling

Expenses:

Rent (D) $ 3,00,000.00 $ 3,00,000.00 $ 3,00,000.00 $ 3,00,000.00 $ 3,00,000.00

Repairs & Maintenance

(E) $ 1,00,000.00 $ 1,00,000.00 $ 2,00,000.00 $ 2,00,000.00 $ 3,00,000.00

S & A Salaries (F) $ 4,00,000.00 $ 4,20,000.00 $ 4,41,000.00 $ 4,63,050.00 $ 4,86,202.50

Profit Before

Depreciation (C-D-E-F) $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00 $18,38,797.50

Less: Depreciation $ 27,50,000.00 $ 20,62,500.00 $15,46,875.00 $ 11,60,156.25 $ 8,70,117.19

Profit Before Interest

And Tax/Operating Profit $ -6,25,000.00 $ 13,42,500.00 $30,37,125.00 $ 21,01,793.75 $ 9,68,680.31

II. Cash flows for Five Years

year 1 year 2 year 3 year 4 year 5

Operating Profit (from

above table) $ -6,25,000.00 $ 13,42,500.00 $30,37,125.00 $ 21,01,793.75 $ 9,68,680.31

Add: Depreciation $ 27,50,000.00 $ 20,62,500.00 $15,46,875.00 $ 11,60,156.25 $ 8,70,117.19

It serves as benchmark to measure the efficiency of investment or operating assets and

enables the business managers to understand and emphasise on the relationship between

sales, expenses an investments.

It aids managers in making comparison of several business divisions in profitability and asset

utilisation terms (Bierman & Smidt, 2012).

Weaknesses:

It can lead to making dysfunctional decisions that impacts the efficient asset allocation.

The information of sales, costs, assets etc. is difficult to be obtained at times.

Economic value added is the measure used to evaluate the financial performance of the

company on the basis of its residual wealth. It is calculated by deducting firm’s cost of capital

from its net operating profits after taxes.

There is no benefit of using EVA in place of RI in this case as they are similar measures with the

difference that the EVA measure considers operating profits after taxation effect. In this question

there is no tax rate given so use of EVA would not make any difference.

Question 3

Part a)

I. Profit & Loss Budget of Last Chance Group Limited

year 1 year 2 year 3 year 4 year 5

Sales (A) $ 45,00,000.00 $ 65,00,000.00 $85,00,000.00 $ 65,00,000.00 $45,00,000.00

Cost Of Sales (B) $ 15,75,000.00 $ 22,75,000.00 $29,75,000.00 $ 22,75,000.00 $15,75,000.00

Gross Profit C= (A)-(B) $ 29,25,000.00 $ 42,25,000.00 $55,25,000.00 $ 42,25,000.00 $29,25,000.00

Less: Admin & Selling

Expenses:

Rent (D) $ 3,00,000.00 $ 3,00,000.00 $ 3,00,000.00 $ 3,00,000.00 $ 3,00,000.00

Repairs & Maintenance

(E) $ 1,00,000.00 $ 1,00,000.00 $ 2,00,000.00 $ 2,00,000.00 $ 3,00,000.00

S & A Salaries (F) $ 4,00,000.00 $ 4,20,000.00 $ 4,41,000.00 $ 4,63,050.00 $ 4,86,202.50

Profit Before

Depreciation (C-D-E-F) $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00 $18,38,797.50

Less: Depreciation $ 27,50,000.00 $ 20,62,500.00 $15,46,875.00 $ 11,60,156.25 $ 8,70,117.19

Profit Before Interest

And Tax/Operating Profit $ -6,25,000.00 $ 13,42,500.00 $30,37,125.00 $ 21,01,793.75 $ 9,68,680.31

II. Cash flows for Five Years

year 1 year 2 year 3 year 4 year 5

Operating Profit (from

above table) $ -6,25,000.00 $ 13,42,500.00 $30,37,125.00 $ 21,01,793.75 $ 9,68,680.31

Add: Depreciation $ 27,50,000.00 $ 20,62,500.00 $15,46,875.00 $ 11,60,156.25 $ 8,70,117.19

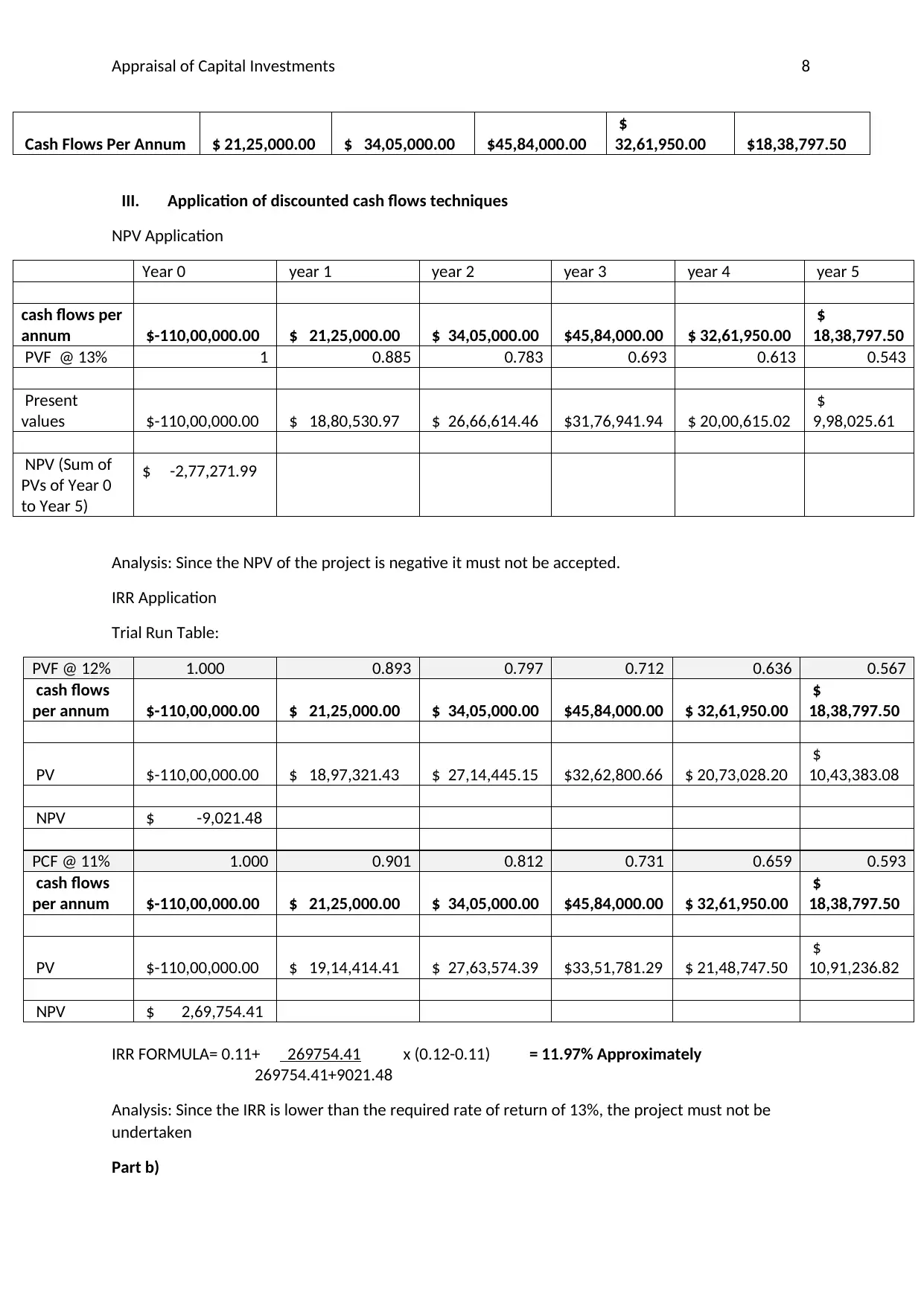

Appraisal of Capital Investments 8

Cash Flows Per Annum $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00

$

32,61,950.00 $18,38,797.50

III. Application of discounted cash flows techniques

NPV Application

Year 0 year 1 year 2 year 3 year 4 year 5

cash flows per

annum $-110,00,000.00 $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00

$

18,38,797.50

PVF @ 13% 1 0.885 0.783 0.693 0.613 0.543

Present

values $-110,00,000.00 $ 18,80,530.97 $ 26,66,614.46 $31,76,941.94 $ 20,00,615.02

$

9,98,025.61

NPV (Sum of

PVs of Year 0

to Year 5)

$ -2,77,271.99

Analysis: Since the NPV of the project is negative it must not be accepted.

IRR Application

Trial Run Table:

PVF @ 12% 1.000 0.893 0.797 0.712 0.636 0.567

cash flows

per annum $-110,00,000.00 $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00

$

18,38,797.50

PV $-110,00,000.00 $ 18,97,321.43 $ 27,14,445.15 $32,62,800.66 $ 20,73,028.20

$

10,43,383.08

NPV $ -9,021.48

PCF @ 11% 1.000 0.901 0.812 0.731 0.659 0.593

cash flows

per annum $-110,00,000.00 $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00

$

18,38,797.50

PV $-110,00,000.00 $ 19,14,414.41 $ 27,63,574.39 $33,51,781.29 $ 21,48,747.50

$

10,91,236.82

NPV $ 2,69,754.41

IRR FORMULA= 0.11+ 269754.41 x (0.12-0.11) = 11.97% Approximately

269754.41+9021.48

Analysis: Since the IRR is lower than the required rate of return of 13%, the project must not be

undertaken

Part b)

Cash Flows Per Annum $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00

$

32,61,950.00 $18,38,797.50

III. Application of discounted cash flows techniques

NPV Application

Year 0 year 1 year 2 year 3 year 4 year 5

cash flows per

annum $-110,00,000.00 $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00

$

18,38,797.50

PVF @ 13% 1 0.885 0.783 0.693 0.613 0.543

Present

values $-110,00,000.00 $ 18,80,530.97 $ 26,66,614.46 $31,76,941.94 $ 20,00,615.02

$

9,98,025.61

NPV (Sum of

PVs of Year 0

to Year 5)

$ -2,77,271.99

Analysis: Since the NPV of the project is negative it must not be accepted.

IRR Application

Trial Run Table:

PVF @ 12% 1.000 0.893 0.797 0.712 0.636 0.567

cash flows

per annum $-110,00,000.00 $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00

$

18,38,797.50

PV $-110,00,000.00 $ 18,97,321.43 $ 27,14,445.15 $32,62,800.66 $ 20,73,028.20

$

10,43,383.08

NPV $ -9,021.48

PCF @ 11% 1.000 0.901 0.812 0.731 0.659 0.593

cash flows

per annum $-110,00,000.00 $ 21,25,000.00 $ 34,05,000.00 $45,84,000.00 $ 32,61,950.00

$

18,38,797.50

PV $-110,00,000.00 $ 19,14,414.41 $ 27,63,574.39 $33,51,781.29 $ 21,48,747.50

$

10,91,236.82

NPV $ 2,69,754.41

IRR FORMULA= 0.11+ 269754.41 x (0.12-0.11) = 11.97% Approximately

269754.41+9021.48

Analysis: Since the IRR is lower than the required rate of return of 13%, the project must not be

undertaken

Part b)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appraisal of Capital Investments 9

Budgeting is the integral part of future planning. It has its own advantages and advantages that are

given below:

Advantages:

It provides businesses with the ‘’plan of spending ’’ and thereby helps the managers in

decision making.

It provides the tool to evaluate the performance of company by offering the basis to make

comparisons of actual and planned results.

It aids the distribution and appropriate allocation of resources of the business to the key

areas (DRURY, 2013).

Disadvantages:

Budgeting process is featured by rigidity of Budgeted plans which do not work in the

changing environment of business (Wampler, 2010).

It is also very time consuming process.

Budgeting is the integral part of future planning. It has its own advantages and advantages that are

given below:

Advantages:

It provides businesses with the ‘’plan of spending ’’ and thereby helps the managers in

decision making.

It provides the tool to evaluate the performance of company by offering the basis to make

comparisons of actual and planned results.

It aids the distribution and appropriate allocation of resources of the business to the key

areas (DRURY, 2013).

Disadvantages:

Budgeting process is featured by rigidity of Budgeted plans which do not work in the

changing environment of business (Wampler, 2010).

It is also very time consuming process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments

10

References:

Baker, H. K., & English, P. (2011). Capital budgeting valuation: Financial analysis for today's

investment projects (Vol. 13). John Wiley & Sons.

Bierman Jr, H., & Smidt, S. (2012). The capital budgeting decision: economic analysis of investment

projects. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Wampler, B. (2010). Participatory budgeting in Brazil: Contestation, cooperation, and accountability.

Penn State Press.

10

References:

Baker, H. K., & English, P. (2011). Capital budgeting valuation: Financial analysis for today's

investment projects (Vol. 13). John Wiley & Sons.

Bierman Jr, H., & Smidt, S. (2012). The capital budgeting decision: economic analysis of investment

projects. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Wampler, B. (2010). Participatory budgeting in Brazil: Contestation, cooperation, and accountability.

Penn State Press.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.