Capital Gain Tax | Taxation Law | Assignment

VerifiedAdded on 2022/08/25

|7

|1164

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................3

References:.................................................................................................................................6

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................3

References:.................................................................................................................................6

2TAXATION LAW

Answer to Part 1:

A capital gain tax can be defined as the set of rules which is mainly designed to

compute the gains which will would be taxed under the laws of income tax because of one of

53 CGT events. A capital gain happens when the proceeds following the disposal of asset

exceeds the costs of purchasing the asset (Lam and Whitney 2016). A capital gains or loss

happens under “sec 100-20 (1)” when the CGT events happens. A “CGT event A1” takes

place when the disposal of CGT asset happens under sec 104-10. The sale of CGT event

would usually happen when a contract is entered into by the taxpayer for sale.

According to the “sec 104-10(3) ITAA 1997” the time of CGT event upon the transfer

of CGT asset happens when the taxpayer forms an agreement or if there is no agreement, then

it involves when the change of ownership happened upon the settlement (Phan 2016).

Reference to “FCT v Sara Lee Household & Body Care P/L (2000)” can be made to

understand the time of CGT event. The factors include;

1. The applicable contract amounts to a source of obligation in performing the transfer

of assets that results in relevant sale.

2. If there is more than two contracts which forms the sources of obligation to execute

the transfer, there is need for judgement as which contracts is property to be viewed as

the source of obligation to create an impact on the disposal.

3. It is not possible to recognize the single agreement based on which the sale happened,

then the time represents when the change of ownership took place.

4. The date of purchase and sale of same CGT asset might not be same and does not

requires to be contemporaneous (Armstrong 2016).

5. The relevant time is when the contact is made and not when it became unconditional

or enforceable specifically.

Answer to Part 1:

A capital gain tax can be defined as the set of rules which is mainly designed to

compute the gains which will would be taxed under the laws of income tax because of one of

53 CGT events. A capital gain happens when the proceeds following the disposal of asset

exceeds the costs of purchasing the asset (Lam and Whitney 2016). A capital gains or loss

happens under “sec 100-20 (1)” when the CGT events happens. A “CGT event A1” takes

place when the disposal of CGT asset happens under sec 104-10. The sale of CGT event

would usually happen when a contract is entered into by the taxpayer for sale.

According to the “sec 104-10(3) ITAA 1997” the time of CGT event upon the transfer

of CGT asset happens when the taxpayer forms an agreement or if there is no agreement, then

it involves when the change of ownership happened upon the settlement (Phan 2016).

Reference to “FCT v Sara Lee Household & Body Care P/L (2000)” can be made to

understand the time of CGT event. The factors include;

1. The applicable contract amounts to a source of obligation in performing the transfer

of assets that results in relevant sale.

2. If there is more than two contracts which forms the sources of obligation to execute

the transfer, there is need for judgement as which contracts is property to be viewed as

the source of obligation to create an impact on the disposal.

3. It is not possible to recognize the single agreement based on which the sale happened,

then the time represents when the change of ownership took place.

4. The date of purchase and sale of same CGT asset might not be same and does not

requires to be contemporaneous (Armstrong 2016).

5. The relevant time is when the contact is made and not when it became unconditional

or enforceable specifically.

3TAXATION LAW

When it is noticed that the relevant contract is signed prior to 30 June, the CGT event along

with the liability of paying the CGT will be for the year ended 30 June.

Answer to Part 2:

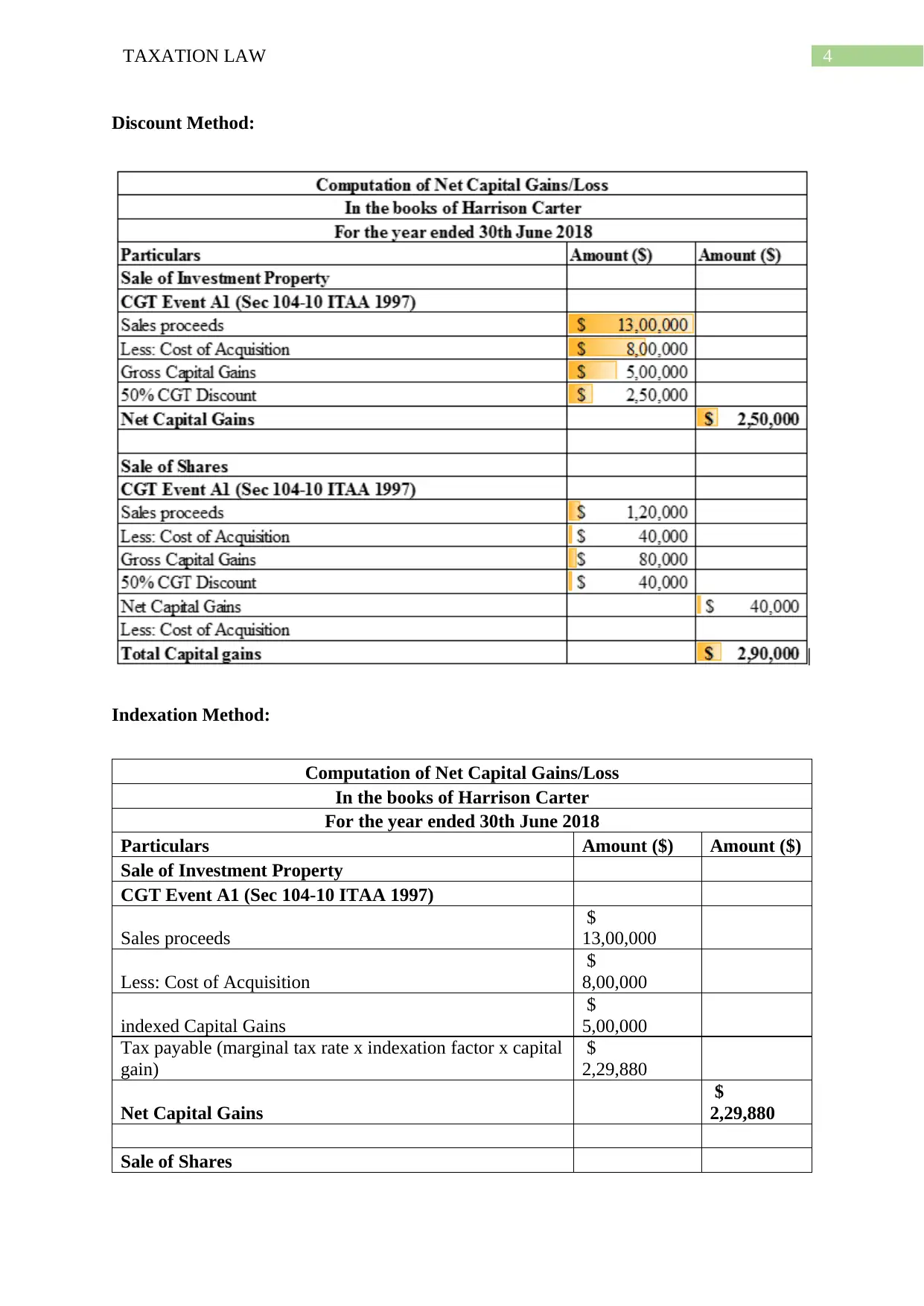

During the year 2001 Harrison purchased an investment property for $80,000. Citing

“section 108-5 ITAA 1997” the property is a CGT asset. In the year 2018 the property was

sold by Harrison for $1.3 million. When the property was sold by Harrison a “CGT event

A1” happened under “section 104-10 (1)” happened. Citing the case of “FCT v Sara Lee

Household (2002)” a “CGT event A1” took place when Harrison arrived in the contract of

selling the investment property (Villios 2014). There was a change in ownership when

property was eventually sold by Harrison. As a result under “section 102-5 ITAA 1997” the

net amount of capital gains made by Harrison from selling the property will be included in his

taxable income.

Apart from selling the property, Harrison also sold $10,000 shares that he purchased

in October 1985 for $4 per share. On 20th June 2018 all the shares were sold for $12 per

share. Referring to “FCT v Sara Lee Household (2002)” the contract for transferring the

shares was entered into by Harrison on 20th June 2018 (Friend 2015). Referring to “sec 104-

10 (3) ITAA 1997” the timing of CGT event will be the income year 2017-18 since it

represent the year in which the agreement actually took place.

As explained by ATO when a capital loss happens on disposing the CGT asset, the

loss should be used to reduce the capital gains in the same financial year (Mark and James

2016). When it is found that no gains are reported by taxpayer, the losses is carried forward

to subsequent year. Similarly, Harrison did not reported any capital gain in 2018-19 but

reported a capital loss of $65,000. So these losses needs to be carried forward by Harrison to

subsequent years.

When it is noticed that the relevant contract is signed prior to 30 June, the CGT event along

with the liability of paying the CGT will be for the year ended 30 June.

Answer to Part 2:

During the year 2001 Harrison purchased an investment property for $80,000. Citing

“section 108-5 ITAA 1997” the property is a CGT asset. In the year 2018 the property was

sold by Harrison for $1.3 million. When the property was sold by Harrison a “CGT event

A1” happened under “section 104-10 (1)” happened. Citing the case of “FCT v Sara Lee

Household (2002)” a “CGT event A1” took place when Harrison arrived in the contract of

selling the investment property (Villios 2014). There was a change in ownership when

property was eventually sold by Harrison. As a result under “section 102-5 ITAA 1997” the

net amount of capital gains made by Harrison from selling the property will be included in his

taxable income.

Apart from selling the property, Harrison also sold $10,000 shares that he purchased

in October 1985 for $4 per share. On 20th June 2018 all the shares were sold for $12 per

share. Referring to “FCT v Sara Lee Household (2002)” the contract for transferring the

shares was entered into by Harrison on 20th June 2018 (Friend 2015). Referring to “sec 104-

10 (3) ITAA 1997” the timing of CGT event will be the income year 2017-18 since it

represent the year in which the agreement actually took place.

As explained by ATO when a capital loss happens on disposing the CGT asset, the

loss should be used to reduce the capital gains in the same financial year (Mark and James

2016). When it is found that no gains are reported by taxpayer, the losses is carried forward

to subsequent year. Similarly, Harrison did not reported any capital gain in 2018-19 but

reported a capital loss of $65,000. So these losses needs to be carried forward by Harrison to

subsequent years.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Discount Method:

Indexation Method:

Computation of Net Capital Gains/Loss

In the books of Harrison Carter

For the year ended 30th June 2018

Particulars Amount ($) Amount ($)

Sale of Investment Property

CGT Event A1 (Sec 104-10 ITAA 1997)

Sales proceeds

$

13,00,000

Less: Cost of Acquisition

$

8,00,000

indexed Capital Gains

$

5,00,000

Tax payable (marginal tax rate x indexation factor x capital

gain)

$

2,29,880

Net Capital Gains

$

2,29,880

Sale of Shares

Discount Method:

Indexation Method:

Computation of Net Capital Gains/Loss

In the books of Harrison Carter

For the year ended 30th June 2018

Particulars Amount ($) Amount ($)

Sale of Investment Property

CGT Event A1 (Sec 104-10 ITAA 1997)

Sales proceeds

$

13,00,000

Less: Cost of Acquisition

$

8,00,000

indexed Capital Gains

$

5,00,000

Tax payable (marginal tax rate x indexation factor x capital

gain)

$

2,29,880

Net Capital Gains

$

2,29,880

Sale of Shares

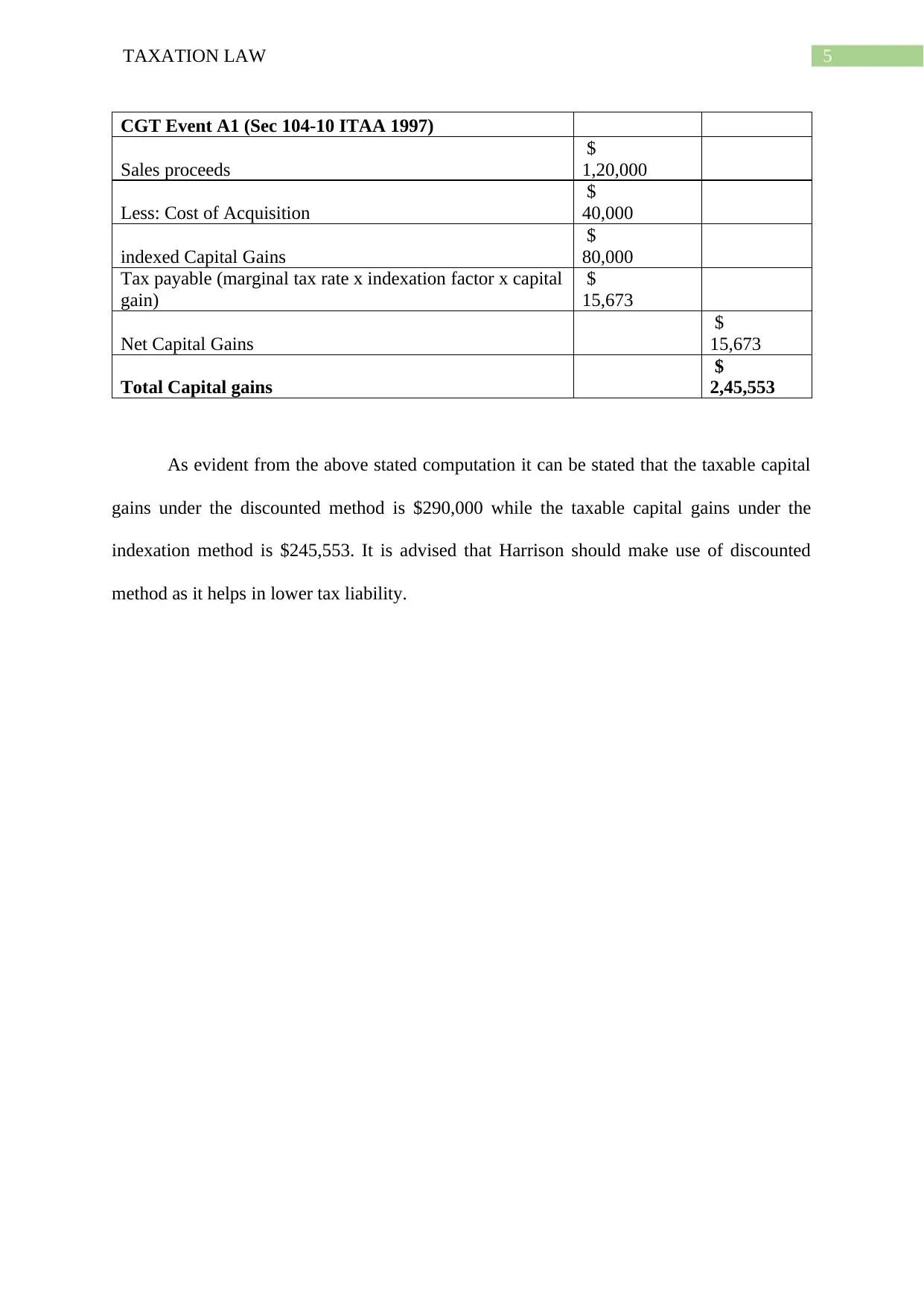

5TAXATION LAW

CGT Event A1 (Sec 104-10 ITAA 1997)

Sales proceeds

$

1,20,000

Less: Cost of Acquisition

$

40,000

indexed Capital Gains

$

80,000

Tax payable (marginal tax rate x indexation factor x capital

gain)

$

15,673

Net Capital Gains

$

15,673

Total Capital gains

$

2,45,553

As evident from the above stated computation it can be stated that the taxable capital

gains under the discounted method is $290,000 while the taxable capital gains under the

indexation method is $245,553. It is advised that Harrison should make use of discounted

method as it helps in lower tax liability.

CGT Event A1 (Sec 104-10 ITAA 1997)

Sales proceeds

$

1,20,000

Less: Cost of Acquisition

$

40,000

indexed Capital Gains

$

80,000

Tax payable (marginal tax rate x indexation factor x capital

gain)

$

15,673

Net Capital Gains

$

15,673

Total Capital gains

$

2,45,553

As evident from the above stated computation it can be stated that the taxable capital

gains under the discounted method is $290,000 while the taxable capital gains under the

indexation method is $245,553. It is advised that Harrison should make use of discounted

method as it helps in lower tax liability.

6TAXATION LAW

References:

Armstrong, M., 2016. CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, pp.Mondaq Business Briefing, March 11, 2016.

Friend, R., 2015. The CGT small business concessions: issues, anomalies and opportunities.

(capital gains tax) (Australia). Australian Tax Review, 40(2), pp.108–137.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Mark, K., and James, M., 2016. PM weighs higher capital gains tax. The Age (Melbourne,

Australia), p.4.

Phan, L., 2016. Australia's Foreign Resident Capital Gains Tax Withholding Regime.

Mondaq Business Briefing, pp.Mondaq Business Briefing, Sept 29, 2016.

Villios, S., et al., 2014. The capital gains tax implications of buy-sell agreements.(Australia).

Australian Tax Review, 41(2), pp.100–112.

References:

Armstrong, M., 2016. CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, pp.Mondaq Business Briefing, March 11, 2016.

Friend, R., 2015. The CGT small business concessions: issues, anomalies and opportunities.

(capital gains tax) (Australia). Australian Tax Review, 40(2), pp.108–137.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Mark, K., and James, M., 2016. PM weighs higher capital gains tax. The Age (Melbourne,

Australia), p.4.

Phan, L., 2016. Australia's Foreign Resident Capital Gains Tax Withholding Regime.

Mondaq Business Briefing, pp.Mondaq Business Briefing, Sept 29, 2016.

Villios, S., et al., 2014. The capital gains tax implications of buy-sell agreements.(Australia).

Australian Tax Review, 41(2), pp.100–112.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.