Taxation Theory, Practice & Law: CGT and FBT Analysis

VerifiedAdded on 2023/06/04

|12

|2573

|102

Homework Assignment

AI Summary

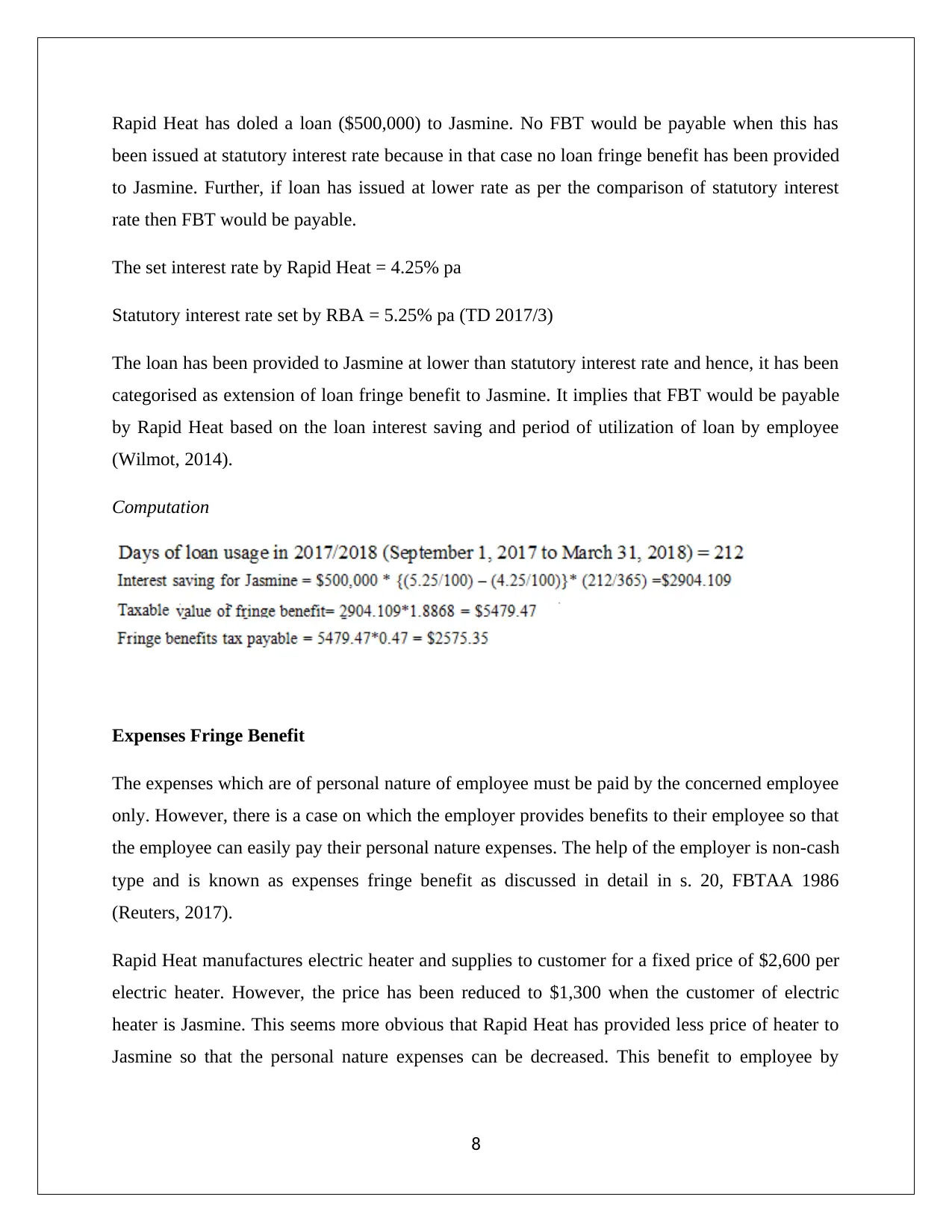

This assignment solution addresses key aspects of Australian taxation law, focusing on Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT). Question 1 delves into CGT implications for asset disposal, including pre-CGT assets, CGT events, cost base calculations, and the application of the 50% discount method for long-term capital gains. It analyzes the tax consequences of disposing various assets like vacant land, an antique bed, a painting, shares, and a violin, considering acquisition dates, and specific tax rules for each asset type. Question 2 examines Fringe Benefit Tax (FBT), specifically car, loan and expenses fringe benefits. It covers the computation of FBT for car fringe benefits, considering the car's capital value and usage duration. Furthermore, it assesses loan fringe benefits, comparing the interest rate on a loan provided to an employee with the statutory interest rate. Lastly, it explores expenses fringe benefits, particularly when an employer reduces prices on goods or services for an employee. The assignment provides detailed calculations and explanations based on relevant tax legislation and case law.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.