HI6028 Taxation: Capital Gains Tax & Fringe Benefits Tax Analysis

VerifiedAdded on 2023/06/04

|13

|3090

|227

Report

AI Summary

This report provides a detailed analysis of capital gains tax (CGT) and fringe benefits tax (FBT) implications for an investor client. It examines the tax treatment of various asset disposals, including vacant land, antiques, paintings, and shares, considering pre-CGT status, holding periods, and applicable discounts. The report also addresses FBT liabilities related to car fringe benefits and loan fringe benefits, offering calculations and explanations based on relevant legislation and tax rulings. The final capital gains are calculated after considering previous losses and applicable rebates. The analysis incorporates provisions from the Income Tax Assessment Act 1997 and the Fringe Benefits Assessment Act 1986 to provide comprehensive tax advice.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The present circumstances would be analysed and the tax advice would be provided to the client

on the account of the received capital gains/losses from the disposal of the assets. The imperative

aspect is that taxpayer is not running a business involving trading of asset or engagement in

selling or buying the assets to generate revenue receipts and hence, the only available scenario

for the sale proceeds is capital receipts. Further, the tax treatment for the capital receipts would

not be done based on the assessable income taxation concepts and hence, the applicable tax

treatment would be Capital Gains Tax (CGT) on the account of the capital gains or capital losses

that have resulted from the capital proceeds. The basic terms which are essential to understand

the context of CGT are highlighted below.

(1) Pre-CGT Asset: Capital Gains Tax (CGT) has come into existence on September 20, 1985.

The assets which have been acquired before this date are categorised as pre-CGT asset. The

relevant provisions are highlighted in s. 140-10 Income Tax Assessment Act 1997 (ITAA

1997) (Krever, 2017). As the pre-CGT assets belong to the period which is prior to the

enforceability of CGT and hence, CGT liability is not applicable on those assets. The

taxpayer would not be held accountable for the CGT implication on the capital gains or

losses which are obtained due to the disposal of the pre-CGT asset (Woellner, 2017).

(2) CGT Event: Capital gains or losses would be computed when there is a CGT event

occurrence. The provision of s. 104-5 ITAA 1997 defines the list of CGT events for different

categories of the transactions. According to the current information, it would be concluded

that the incurred transactions of the taxpayers for the selling of the assets are CGT event and

the associated category is A1 (Krever, 2017). This indicates that income from disposal and

cost base of asset are the two main variables which need to be calculated to determine the

incurred capital gains/losses.

(3) Cost Base: This is combination of the various costs which are associated with the asset and

are paid by the taxpayer as defined in s. 110-25 ITAA 1997. The major components of cost

base are five which are shown below (Coleman, 2016).

Component 1 of cost base: Cost for the procuring the asset at the time of purchase

1

The present circumstances would be analysed and the tax advice would be provided to the client

on the account of the received capital gains/losses from the disposal of the assets. The imperative

aspect is that taxpayer is not running a business involving trading of asset or engagement in

selling or buying the assets to generate revenue receipts and hence, the only available scenario

for the sale proceeds is capital receipts. Further, the tax treatment for the capital receipts would

not be done based on the assessable income taxation concepts and hence, the applicable tax

treatment would be Capital Gains Tax (CGT) on the account of the capital gains or capital losses

that have resulted from the capital proceeds. The basic terms which are essential to understand

the context of CGT are highlighted below.

(1) Pre-CGT Asset: Capital Gains Tax (CGT) has come into existence on September 20, 1985.

The assets which have been acquired before this date are categorised as pre-CGT asset. The

relevant provisions are highlighted in s. 140-10 Income Tax Assessment Act 1997 (ITAA

1997) (Krever, 2017). As the pre-CGT assets belong to the period which is prior to the

enforceability of CGT and hence, CGT liability is not applicable on those assets. The

taxpayer would not be held accountable for the CGT implication on the capital gains or

losses which are obtained due to the disposal of the pre-CGT asset (Woellner, 2017).

(2) CGT Event: Capital gains or losses would be computed when there is a CGT event

occurrence. The provision of s. 104-5 ITAA 1997 defines the list of CGT events for different

categories of the transactions. According to the current information, it would be concluded

that the incurred transactions of the taxpayers for the selling of the assets are CGT event and

the associated category is A1 (Krever, 2017). This indicates that income from disposal and

cost base of asset are the two main variables which need to be calculated to determine the

incurred capital gains/losses.

(3) Cost Base: This is combination of the various costs which are associated with the asset and

are paid by the taxpayer as defined in s. 110-25 ITAA 1997. The major components of cost

base are five which are shown below (Coleman, 2016).

Component 1 of cost base: Cost for the procuring the asset at the time of purchase

1

Component 2 of cost base: Incidental costs which are associated with selling and buying

Component 3 of cost base: Capital expenses invested by taxpayer to improve the worth of asset

so that high sale proceeds can be derived

Component 4 of cost base: Capital expenses invested by taxpayer to keep the asset title

Component 5 of cost base: Cost related to the action which has been done so as to retain the

ownership of asset

(4) Capital Loss: There is a possibility that disposal of the asset would generate capital losses to

taxpayer and hence, in such cases the capital losses will be adjusted with the capital gains

received as per the understanding highlighted in s.102 -5 ITAA 1997. Moreover, if no capital

gains are generated to adjust the capital losses then these losses would be rolled over to the

next financial year (Barkoczy, 2017).

(5) Discount Method for Capital Gains: Assets that are deriving long term capital gains will be

liable for 50% discount on the capital gains for CGT implication as per s. 115-25 (Woellner,

2017). Long term capital gains are derived when there is holding period of asset of more than

12 months. Further, short term capital gains (holding period of asset less than 12 months) are

derived, then 50% discount will not be valid.

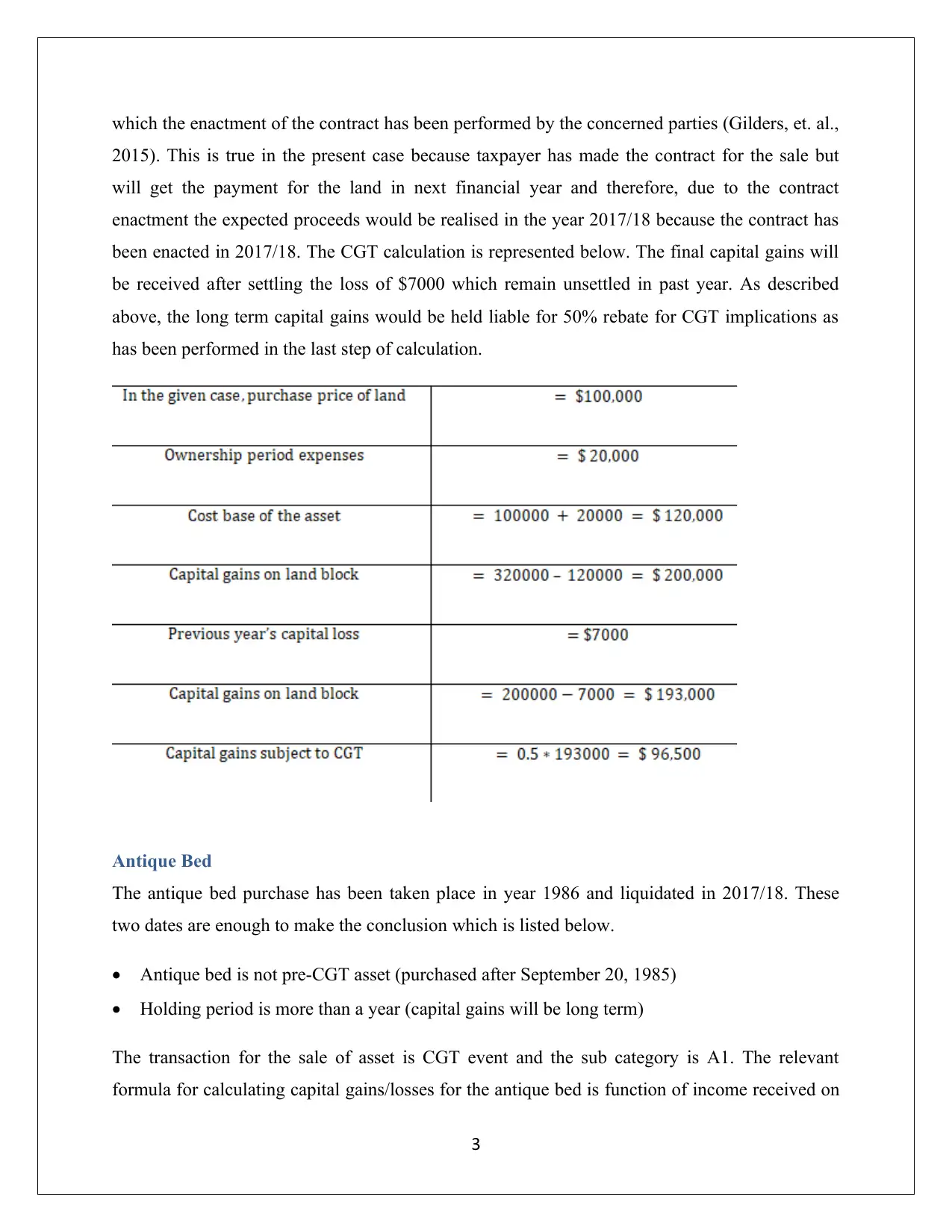

Block of vacant land

The land purchase has been taken place in year 2001 and liquidated in 2017/18. . These two

dates are enough to make the conclusion which is listed below.

Land block is not pre-CGT asset (purchased after September 20, 1985)

Holding period is more than a year (capital gains will be long term)

The transaction for the sale of asset is CGT event and the sub category is A1. The relevant

formula for calculating capital gains/losses for the block of vacant land is function of income

received on the account of selling of the asset and the cost base. Further, the relevant factor

related to the sell proceeds realisation is that taxpayer did not get the payment of land from the

respective buyer and only signed the contract for selling. As per the understanding highlighted in

TR 94/29, the expected proceeds of the sale will be realised in the very same income year in

2

Component 3 of cost base: Capital expenses invested by taxpayer to improve the worth of asset

so that high sale proceeds can be derived

Component 4 of cost base: Capital expenses invested by taxpayer to keep the asset title

Component 5 of cost base: Cost related to the action which has been done so as to retain the

ownership of asset

(4) Capital Loss: There is a possibility that disposal of the asset would generate capital losses to

taxpayer and hence, in such cases the capital losses will be adjusted with the capital gains

received as per the understanding highlighted in s.102 -5 ITAA 1997. Moreover, if no capital

gains are generated to adjust the capital losses then these losses would be rolled over to the

next financial year (Barkoczy, 2017).

(5) Discount Method for Capital Gains: Assets that are deriving long term capital gains will be

liable for 50% discount on the capital gains for CGT implication as per s. 115-25 (Woellner,

2017). Long term capital gains are derived when there is holding period of asset of more than

12 months. Further, short term capital gains (holding period of asset less than 12 months) are

derived, then 50% discount will not be valid.

Block of vacant land

The land purchase has been taken place in year 2001 and liquidated in 2017/18. . These two

dates are enough to make the conclusion which is listed below.

Land block is not pre-CGT asset (purchased after September 20, 1985)

Holding period is more than a year (capital gains will be long term)

The transaction for the sale of asset is CGT event and the sub category is A1. The relevant

formula for calculating capital gains/losses for the block of vacant land is function of income

received on the account of selling of the asset and the cost base. Further, the relevant factor

related to the sell proceeds realisation is that taxpayer did not get the payment of land from the

respective buyer and only signed the contract for selling. As per the understanding highlighted in

TR 94/29, the expected proceeds of the sale will be realised in the very same income year in

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which the enactment of the contract has been performed by the concerned parties (Gilders, et. al.,

2015). This is true in the present case because taxpayer has made the contract for the sale but

will get the payment for the land in next financial year and therefore, due to the contract

enactment the expected proceeds would be realised in the year 2017/18 because the contract has

been enacted in 2017/18. The CGT calculation is represented below. The final capital gains will

be received after settling the loss of $7000 which remain unsettled in past year. As described

above, the long term capital gains would be held liable for 50% rebate for CGT implications as

has been performed in the last step of calculation.

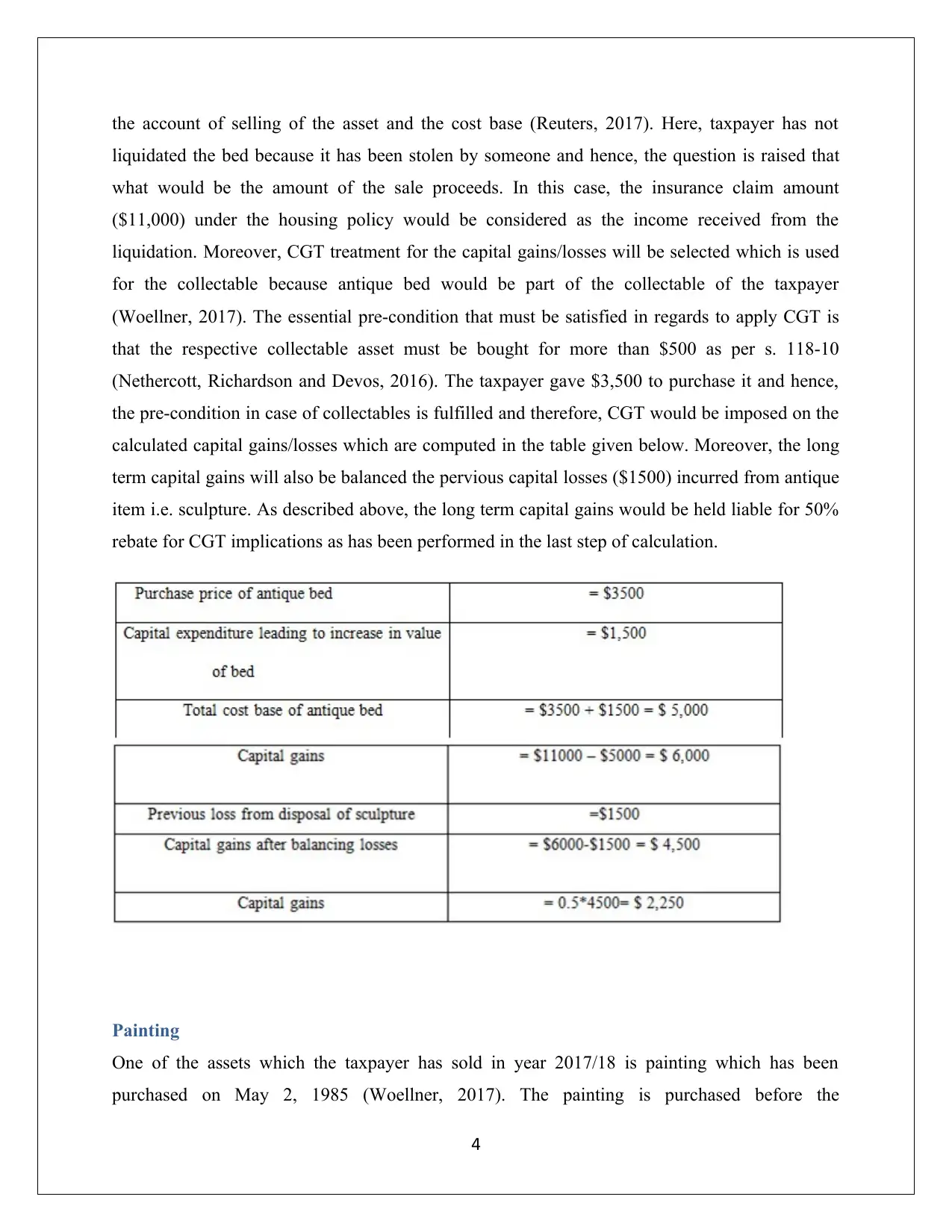

Antique Bed

The antique bed purchase has been taken place in year 1986 and liquidated in 2017/18. These

two dates are enough to make the conclusion which is listed below.

Antique bed is not pre-CGT asset (purchased after September 20, 1985)

Holding period is more than a year (capital gains will be long term)

The transaction for the sale of asset is CGT event and the sub category is A1. The relevant

formula for calculating capital gains/losses for the antique bed is function of income received on

3

2015). This is true in the present case because taxpayer has made the contract for the sale but

will get the payment for the land in next financial year and therefore, due to the contract

enactment the expected proceeds would be realised in the year 2017/18 because the contract has

been enacted in 2017/18. The CGT calculation is represented below. The final capital gains will

be received after settling the loss of $7000 which remain unsettled in past year. As described

above, the long term capital gains would be held liable for 50% rebate for CGT implications as

has been performed in the last step of calculation.

Antique Bed

The antique bed purchase has been taken place in year 1986 and liquidated in 2017/18. These

two dates are enough to make the conclusion which is listed below.

Antique bed is not pre-CGT asset (purchased after September 20, 1985)

Holding period is more than a year (capital gains will be long term)

The transaction for the sale of asset is CGT event and the sub category is A1. The relevant

formula for calculating capital gains/losses for the antique bed is function of income received on

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the account of selling of the asset and the cost base (Reuters, 2017). Here, taxpayer has not

liquidated the bed because it has been stolen by someone and hence, the question is raised that

what would be the amount of the sale proceeds. In this case, the insurance claim amount

($11,000) under the housing policy would be considered as the income received from the

liquidation. Moreover, CGT treatment for the capital gains/losses will be selected which is used

for the collectable because antique bed would be part of the collectable of the taxpayer

(Woellner, 2017). The essential pre-condition that must be satisfied in regards to apply CGT is

that the respective collectable asset must be bought for more than $500 as per s. 118-10

(Nethercott, Richardson and Devos, 2016). The taxpayer gave $3,500 to purchase it and hence,

the pre-condition in case of collectables is fulfilled and therefore, CGT would be imposed on the

calculated capital gains/losses which are computed in the table given below. Moreover, the long

term capital gains will also be balanced the pervious capital losses ($1500) incurred from antique

item i.e. sculpture. As described above, the long term capital gains would be held liable for 50%

rebate for CGT implications as has been performed in the last step of calculation.

Painting

One of the assets which the taxpayer has sold in year 2017/18 is painting which has been

purchased on May 2, 1985 (Woellner, 2017). The painting is purchased before the

4

liquidated the bed because it has been stolen by someone and hence, the question is raised that

what would be the amount of the sale proceeds. In this case, the insurance claim amount

($11,000) under the housing policy would be considered as the income received from the

liquidation. Moreover, CGT treatment for the capital gains/losses will be selected which is used

for the collectable because antique bed would be part of the collectable of the taxpayer

(Woellner, 2017). The essential pre-condition that must be satisfied in regards to apply CGT is

that the respective collectable asset must be bought for more than $500 as per s. 118-10

(Nethercott, Richardson and Devos, 2016). The taxpayer gave $3,500 to purchase it and hence,

the pre-condition in case of collectables is fulfilled and therefore, CGT would be imposed on the

calculated capital gains/losses which are computed in the table given below. Moreover, the long

term capital gains will also be balanced the pervious capital losses ($1500) incurred from antique

item i.e. sculpture. As described above, the long term capital gains would be held liable for 50%

rebate for CGT implications as has been performed in the last step of calculation.

Painting

One of the assets which the taxpayer has sold in year 2017/18 is painting which has been

purchased on May 2, 1985 (Woellner, 2017). The painting is purchased before the

4

commencement of CGT regime which is September 20, 1985 and therefore, the asset of taxpayer

is clearly a pre-CGT asset which is free from CGT implication as per the clauses of s. 149(10)

ITAA 1997 (Hodgson,Mortimer and Butler, 2016). Therefore, the capital gains or losses derived

from the sale of painting do not extend any CGT liability on her.

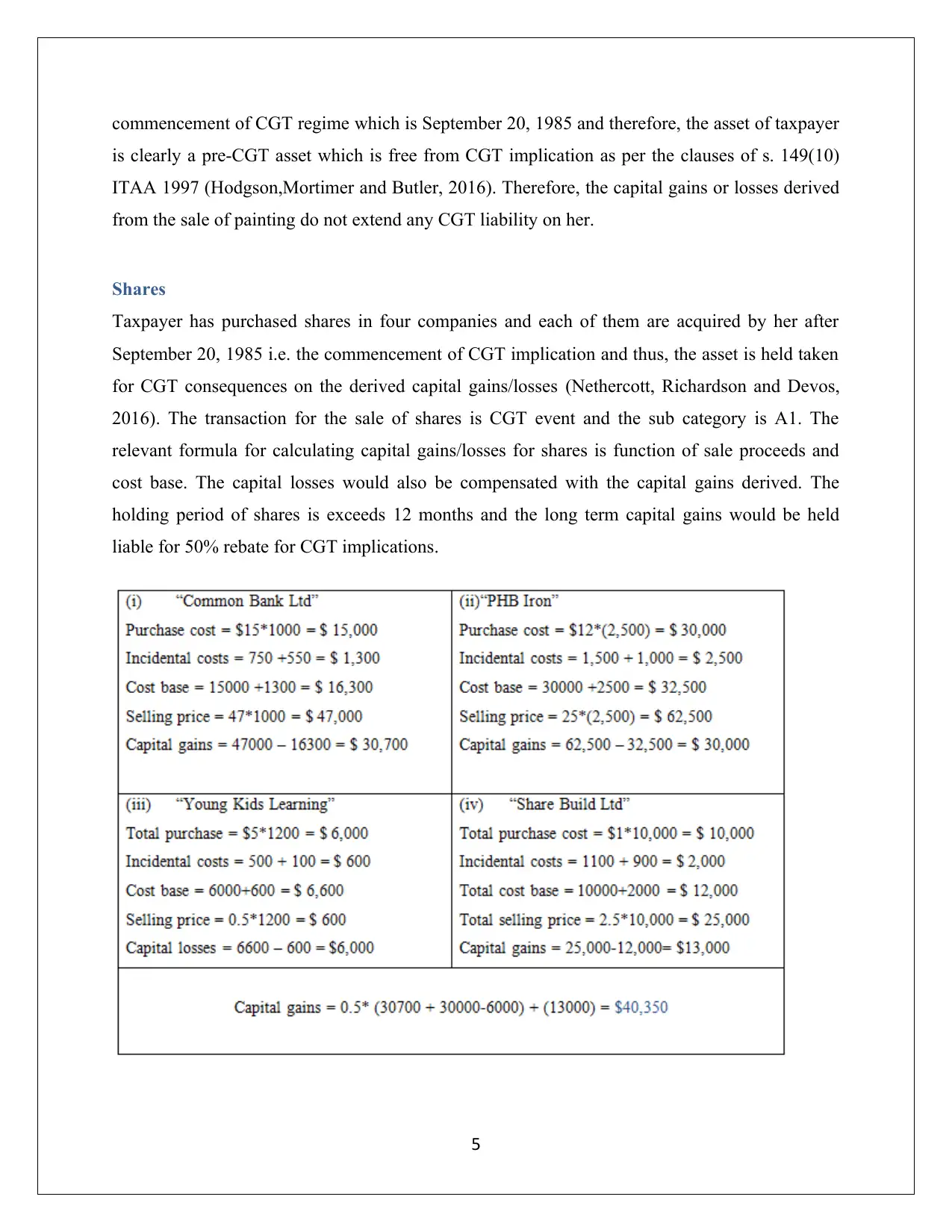

Shares

Taxpayer has purchased shares in four companies and each of them are acquired by her after

September 20, 1985 i.e. the commencement of CGT implication and thus, the asset is held taken

for CGT consequences on the derived capital gains/losses (Nethercott, Richardson and Devos,

2016). The transaction for the sale of shares is CGT event and the sub category is A1. The

relevant formula for calculating capital gains/losses for shares is function of sale proceeds and

cost base. The capital losses would also be compensated with the capital gains derived. The

holding period of shares is exceeds 12 months and the long term capital gains would be held

liable for 50% rebate for CGT implications.

5

is clearly a pre-CGT asset which is free from CGT implication as per the clauses of s. 149(10)

ITAA 1997 (Hodgson,Mortimer and Butler, 2016). Therefore, the capital gains or losses derived

from the sale of painting do not extend any CGT liability on her.

Shares

Taxpayer has purchased shares in four companies and each of them are acquired by her after

September 20, 1985 i.e. the commencement of CGT implication and thus, the asset is held taken

for CGT consequences on the derived capital gains/losses (Nethercott, Richardson and Devos,

2016). The transaction for the sale of shares is CGT event and the sub category is A1. The

relevant formula for calculating capital gains/losses for shares is function of sale proceeds and

cost base. The capital losses would also be compensated with the capital gains derived. The

holding period of shares is exceeds 12 months and the long term capital gains would be held

liable for 50% rebate for CGT implications.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Violin

Violin of the taxpayer would not fall under the collectable asset category because she does not

purchase the respective violin for her collection and rather purchases for personal enjoyment. It

is evident from information that she frequently played violin for her personal enjoyment not for

deriving the income or other reason. Hence, it can be said that sale of the violin is disposal of

personal use asset. It is essential for the CGT applicable on the capital gains or losses that the

buying price must exceed $10,000 as per s. 108-20(1) (Nethercott, Richardson and Devos, 2016).

Taxpayer purchased violin only for $5,500 and therefore, the essential condition is not satisfied

and hence, the CGT will be exempted on the capital gains/loss.

Cumulative Capital Gains

The taxpayer client has total $139,100 as capital gains raised from the transactions of the

disposal of the assets during 2017/18. CGT would be applied on this.

Question 2

(a) Fringe Benefits Tax (FBT) liability will be discussed for each benefit in the given case for

the employer Rapid Heat and employee Jasmine for FY 2017/18.

Car fringe benefits

As per the clauses of s.7 Fringe Benefits Assessment Act 1986, when car has been issued to

employee on the part of employer so that the respective employee will travel through car for

his/her own work, then it is termed as car fringe benefit (Woellner, 2017). In such cases, the

employer would be held responsible for FBT liability when the employer extends car fringe

benefit to employee. Further, the employee is the concerned recipient of the benefit but will not

liable to pay and FBT on the benefit (Hodgson,Mortimer and Butler, 2016). Car is subjected to

6

Violin of the taxpayer would not fall under the collectable asset category because she does not

purchase the respective violin for her collection and rather purchases for personal enjoyment. It

is evident from information that she frequently played violin for her personal enjoyment not for

deriving the income or other reason. Hence, it can be said that sale of the violin is disposal of

personal use asset. It is essential for the CGT applicable on the capital gains or losses that the

buying price must exceed $10,000 as per s. 108-20(1) (Nethercott, Richardson and Devos, 2016).

Taxpayer purchased violin only for $5,500 and therefore, the essential condition is not satisfied

and hence, the CGT will be exempted on the capital gains/loss.

Cumulative Capital Gains

The taxpayer client has total $139,100 as capital gains raised from the transactions of the

disposal of the assets during 2017/18. CGT would be applied on this.

Question 2

(a) Fringe Benefits Tax (FBT) liability will be discussed for each benefit in the given case for

the employer Rapid Heat and employee Jasmine for FY 2017/18.

Car fringe benefits

As per the clauses of s.7 Fringe Benefits Assessment Act 1986, when car has been issued to

employee on the part of employer so that the respective employee will travel through car for

his/her own work, then it is termed as car fringe benefit (Woellner, 2017). In such cases, the

employer would be held responsible for FBT liability when the employer extends car fringe

benefit to employee. Further, the employee is the concerned recipient of the benefit but will not

liable to pay and FBT on the benefit (Hodgson,Mortimer and Butler, 2016). Car is subjected to

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

GST and belongs to type I goods as referred from GST act 1999. Moreover, GST input credits

will also be available for employer to claim on the deduction (Sadiq, et.al., 2015).

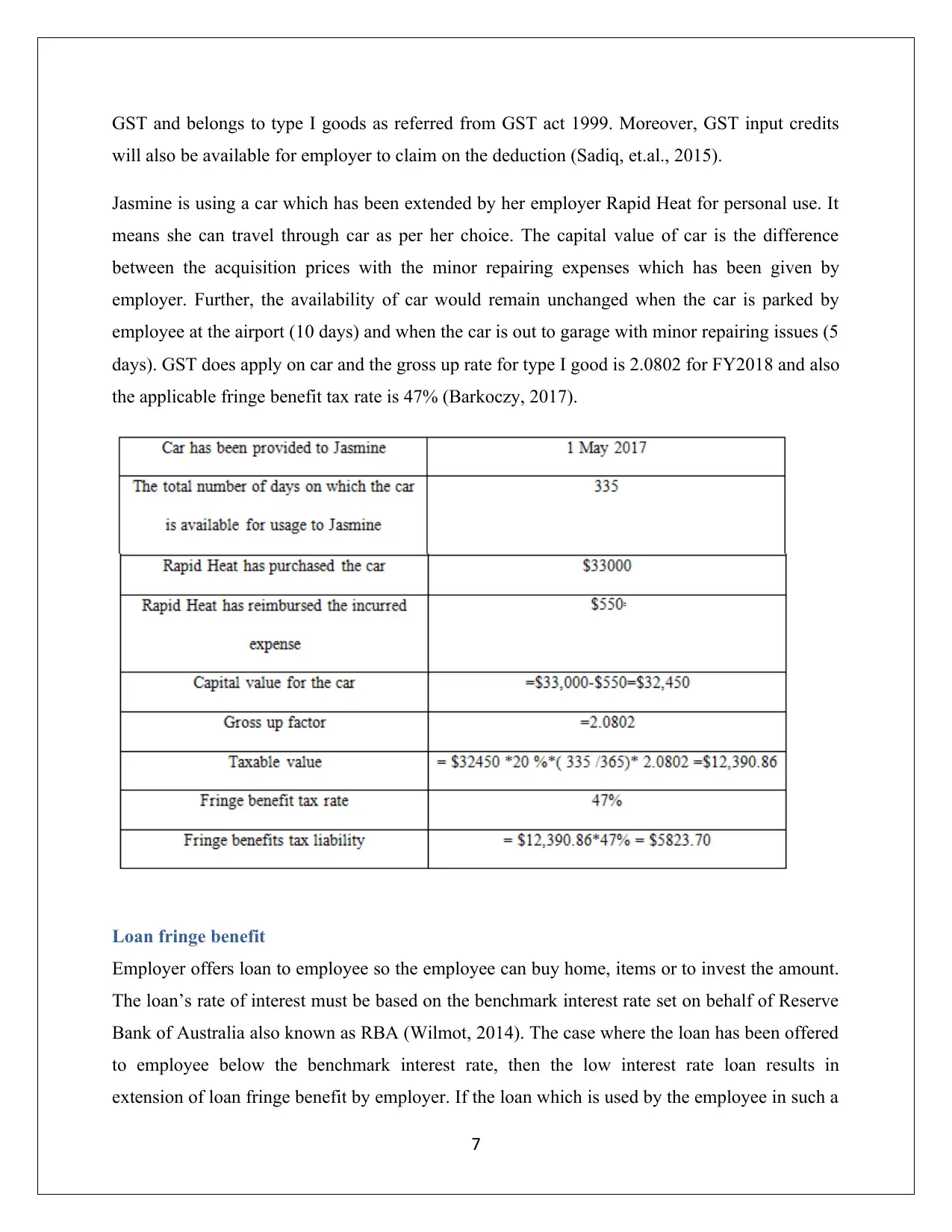

Jasmine is using a car which has been extended by her employer Rapid Heat for personal use. It

means she can travel through car as per her choice. The capital value of car is the difference

between the acquisition prices with the minor repairing expenses which has been given by

employer. Further, the availability of car would remain unchanged when the car is parked by

employee at the airport (10 days) and when the car is out to garage with minor repairing issues (5

days). GST does apply on car and the gross up rate for type I good is 2.0802 for FY2018 and also

the applicable fringe benefit tax rate is 47% (Barkoczy, 2017).

Loan fringe benefit

Employer offers loan to employee so the employee can buy home, items or to invest the amount.

The loan’s rate of interest must be based on the benchmark interest rate set on behalf of Reserve

Bank of Australia also known as RBA (Wilmot, 2014). The case where the loan has been offered

to employee below the benchmark interest rate, then the low interest rate loan results in

extension of loan fringe benefit by employer. If the loan which is used by the employee in such a

7

will also be available for employer to claim on the deduction (Sadiq, et.al., 2015).

Jasmine is using a car which has been extended by her employer Rapid Heat for personal use. It

means she can travel through car as per her choice. The capital value of car is the difference

between the acquisition prices with the minor repairing expenses which has been given by

employer. Further, the availability of car would remain unchanged when the car is parked by

employee at the airport (10 days) and when the car is out to garage with minor repairing issues (5

days). GST does apply on car and the gross up rate for type I good is 2.0802 for FY2018 and also

the applicable fringe benefit tax rate is 47% (Barkoczy, 2017).

Loan fringe benefit

Employer offers loan to employee so the employee can buy home, items or to invest the amount.

The loan’s rate of interest must be based on the benchmark interest rate set on behalf of Reserve

Bank of Australia also known as RBA (Wilmot, 2014). The case where the loan has been offered

to employee below the benchmark interest rate, then the low interest rate loan results in

extension of loan fringe benefit by employer. If the loan which is used by the employee in such a

7

manner that the amount of loan become the source of assessable income, then the interest savings

on loan will be considered for the tax deduction for employer (Sadiq, et.al., 2015).

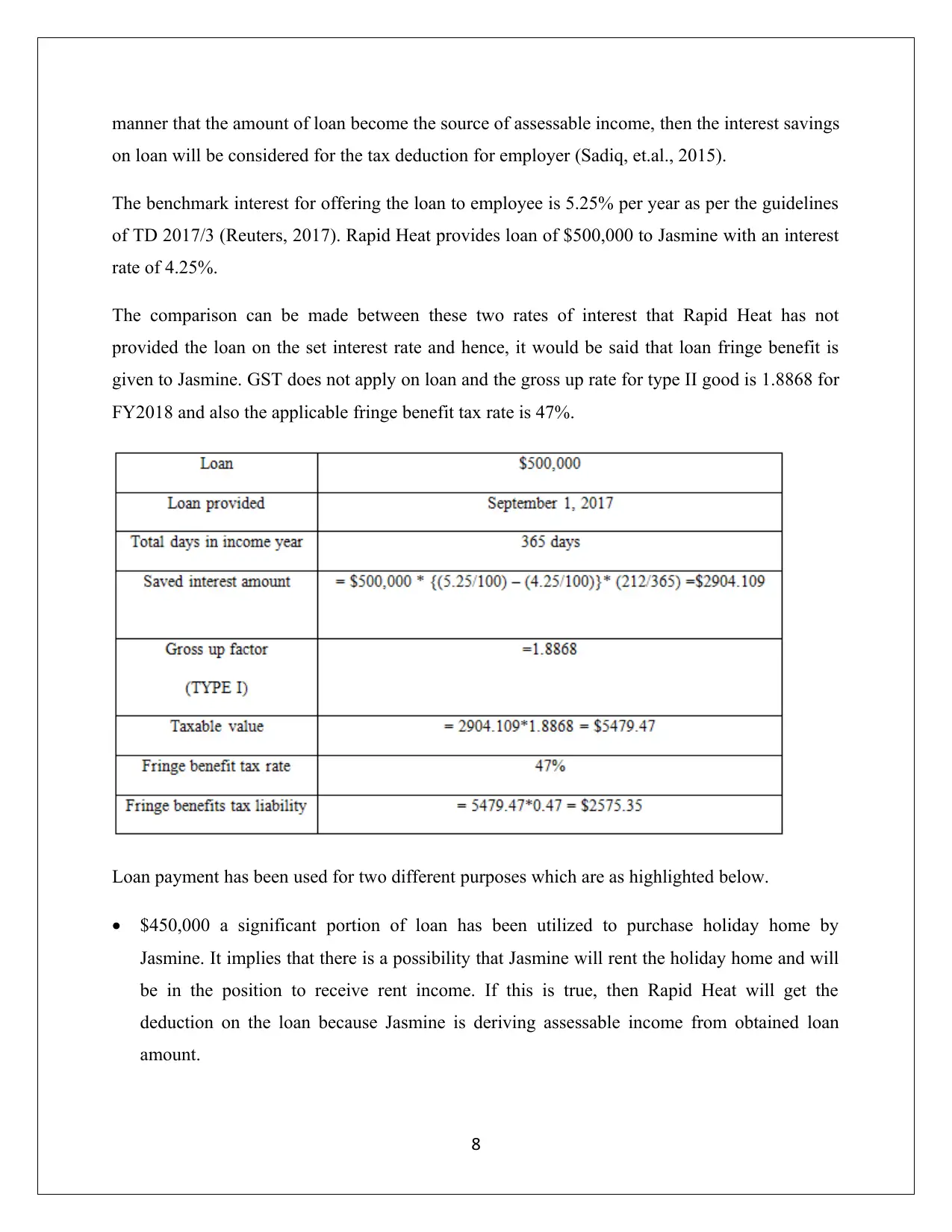

The benchmark interest for offering the loan to employee is 5.25% per year as per the guidelines

of TD 2017/3 (Reuters, 2017). Rapid Heat provides loan of $500,000 to Jasmine with an interest

rate of 4.25%.

The comparison can be made between these two rates of interest that Rapid Heat has not

provided the loan on the set interest rate and hence, it would be said that loan fringe benefit is

given to Jasmine. GST does not apply on loan and the gross up rate for type II good is 1.8868 for

FY2018 and also the applicable fringe benefit tax rate is 47%.

Loan payment has been used for two different purposes which are as highlighted below.

$450,000 a significant portion of loan has been utilized to purchase holiday home by

Jasmine. It implies that there is a possibility that Jasmine will rent the holiday home and will

be in the position to receive rent income. If this is true, then Rapid Heat will get the

deduction on the loan because Jasmine is deriving assessable income from obtained loan

amount.

8

on loan will be considered for the tax deduction for employer (Sadiq, et.al., 2015).

The benchmark interest for offering the loan to employee is 5.25% per year as per the guidelines

of TD 2017/3 (Reuters, 2017). Rapid Heat provides loan of $500,000 to Jasmine with an interest

rate of 4.25%.

The comparison can be made between these two rates of interest that Rapid Heat has not

provided the loan on the set interest rate and hence, it would be said that loan fringe benefit is

given to Jasmine. GST does not apply on loan and the gross up rate for type II good is 1.8868 for

FY2018 and also the applicable fringe benefit tax rate is 47%.

Loan payment has been used for two different purposes which are as highlighted below.

$450,000 a significant portion of loan has been utilized to purchase holiday home by

Jasmine. It implies that there is a possibility that Jasmine will rent the holiday home and will

be in the position to receive rent income. If this is true, then Rapid Heat will get the

deduction on the loan because Jasmine is deriving assessable income from obtained loan

amount.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

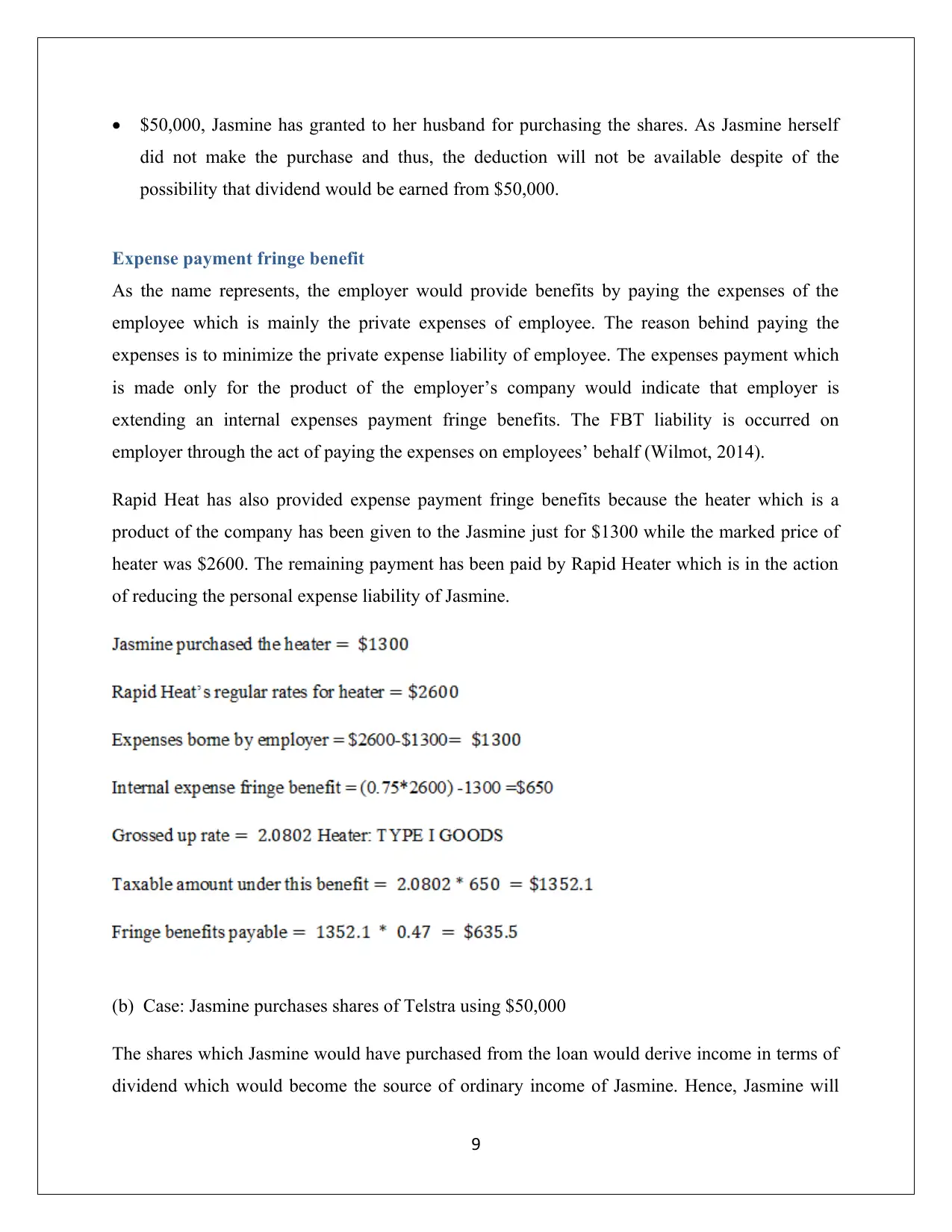

$50,000, Jasmine has granted to her husband for purchasing the shares. As Jasmine herself

did not make the purchase and thus, the deduction will not be available despite of the

possibility that dividend would be earned from $50,000.

Expense payment fringe benefit

As the name represents, the employer would provide benefits by paying the expenses of the

employee which is mainly the private expenses of employee. The reason behind paying the

expenses is to minimize the private expense liability of employee. The expenses payment which

is made only for the product of the employer’s company would indicate that employer is

extending an internal expenses payment fringe benefits. The FBT liability is occurred on

employer through the act of paying the expenses on employees’ behalf (Wilmot, 2014).

Rapid Heat has also provided expense payment fringe benefits because the heater which is a

product of the company has been given to the Jasmine just for $1300 while the marked price of

heater was $2600. The remaining payment has been paid by Rapid Heater which is in the action

of reducing the personal expense liability of Jasmine.

(b) Case: Jasmine purchases shares of Telstra using $50,000

The shares which Jasmine would have purchased from the loan would derive income in terms of

dividend which would become the source of ordinary income of Jasmine. Hence, Jasmine will

9

did not make the purchase and thus, the deduction will not be available despite of the

possibility that dividend would be earned from $50,000.

Expense payment fringe benefit

As the name represents, the employer would provide benefits by paying the expenses of the

employee which is mainly the private expenses of employee. The reason behind paying the

expenses is to minimize the private expense liability of employee. The expenses payment which

is made only for the product of the employer’s company would indicate that employer is

extending an internal expenses payment fringe benefits. The FBT liability is occurred on

employer through the act of paying the expenses on employees’ behalf (Wilmot, 2014).

Rapid Heat has also provided expense payment fringe benefits because the heater which is a

product of the company has been given to the Jasmine just for $1300 while the marked price of

heater was $2600. The remaining payment has been paid by Rapid Heater which is in the action

of reducing the personal expense liability of Jasmine.

(b) Case: Jasmine purchases shares of Telstra using $50,000

The shares which Jasmine would have purchased from the loan would derive income in terms of

dividend which would become the source of ordinary income of Jasmine. Hence, Jasmine will

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

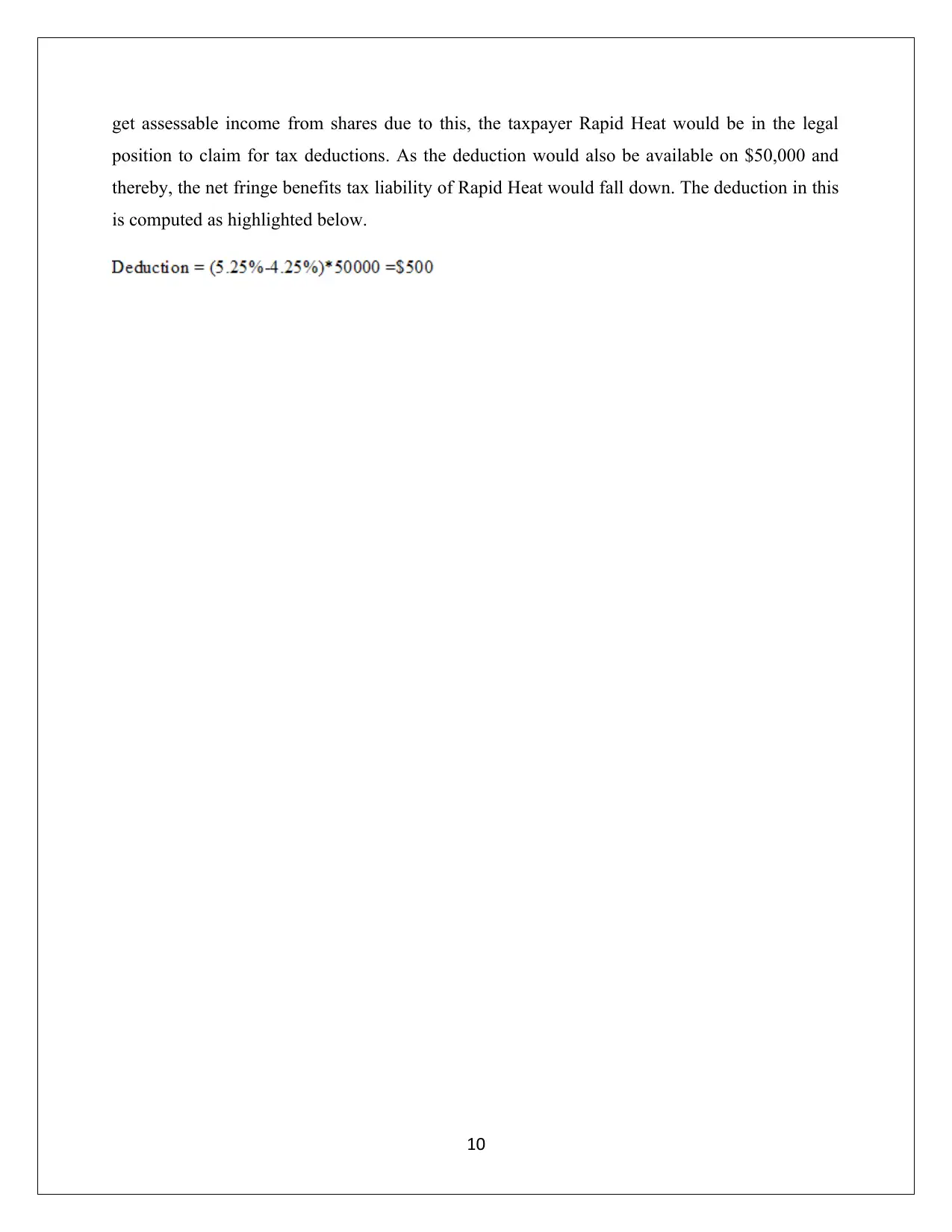

get assessable income from shares due to this, the taxpayer Rapid Heat would be in the legal

position to claim for tax deductions. As the deduction would also be available on $50,000 and

thereby, the net fringe benefits tax liability of Rapid Heat would fall down. The deduction in this

is computed as highlighted below.

10

position to claim for tax deductions. As the deduction would also be available on $50,000 and

thereby, the net fringe benefits tax liability of Rapid Heat would fall down. The deduction in this

is computed as highlighted below.

10

References

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F, Taylor, J, Walpole, M, Burton, M. and Ciro, T (2014) Understanding taxation law

2013. 6th ed. Sydney: LexisNexis/Butterworths

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F, Taylor, J, Walpole, M, Burton, M. and Ciro, T (2014) Understanding taxation law

2013. 6th ed. Sydney: LexisNexis/Butterworths

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.