HI6028 Taxation Theory: Capital Gains Tax, Practice & Fringe Benefits

VerifiedAdded on 2023/06/04

|11

|3112

|220

Report

AI Summary

This assignment provides a detailed analysis of Capital Gains Tax (CGT) implications arising from the disposal of various capital assets, including land, antiques, paintings, and shares, while considering relevant CGT events, cost base calculations, and discount methods. It also assesses Fringe Benefits Tax (FBT) liabilities for car and loan fringe benefits, calculating taxable values and FBT rates according to the Fringe Benefits Tax Assessment Act 1986. The report thoroughly examines relevant sections of the ITAA 1997 and FBTAA 1986, along with tax rulings, to provide comprehensive advice on taxation matters. Desklib offers a wide range of solved assignments and past papers to assist students in their studies.

Taxation Theory, Practice & Law

HI6028

Student Name

[Pick the date]

HI6028

Student Name

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The facts in the given situation indicate that a client needs to be offered advice with regards to

the implications related to Capital Gains Tax (CGT) that would arise from the transactions

enacted by the taxpayer which involve a host of capital assets. For each of the asset category, the

relevant CGT related computations are carried out below.

Asset - Vacant Land

At the outset it is noteworthy that liability related to CGT is only applicable on assets which are

termed as post CGT i.e. they have been purchased on or after September 20, 1985. As a result,

the capital assets which have been acquired before the above mentioned threshold date would be

termed as pre-CGT assets and no CGT liability would arise as highlighted in s. 149(10) ITAA

1997 (Nethercott, Richardson and Devos, 2016).

The various type of events which can potentially lead to creation of capital gains or loss are

known as capital events and outlined in s. 104-5 ITAA 1997 (Barkoczy, 2017) . The capital

event needs to be clearly identified as the underlying capital gains computation method is also

slightly different for the various events. In the given case, the relevant event that would apply is

A1 since it related to disposal of a capital asset and the concerned capital asset is land (Gilders,

et. al., 2016). The resultant capital gains with regards to this event can be obtained by subtracting

the underlying asset cost base from the proceeds derived from sale of asset.

Thus, the next imperative task is to compute the given assets’ cost base which needs to be carried

in manner consistent with s.110-25 ITAA 1997. The various key elements that have been

highlighted in accordance with this approach are mentioned as follows (Nethercott, Richardson

and Devos, 2016).

Element 1: The purchase cost linked to the underlying asset.

Element 2: Incidents costs that are spent by the taxpayer during purchase or sale of asset.

Element 3: Costs related to tax, interest cost which are incurred by the asset owner as ownership

costs.

The facts in the given situation indicate that a client needs to be offered advice with regards to

the implications related to Capital Gains Tax (CGT) that would arise from the transactions

enacted by the taxpayer which involve a host of capital assets. For each of the asset category, the

relevant CGT related computations are carried out below.

Asset - Vacant Land

At the outset it is noteworthy that liability related to CGT is only applicable on assets which are

termed as post CGT i.e. they have been purchased on or after September 20, 1985. As a result,

the capital assets which have been acquired before the above mentioned threshold date would be

termed as pre-CGT assets and no CGT liability would arise as highlighted in s. 149(10) ITAA

1997 (Nethercott, Richardson and Devos, 2016).

The various type of events which can potentially lead to creation of capital gains or loss are

known as capital events and outlined in s. 104-5 ITAA 1997 (Barkoczy, 2017) . The capital

event needs to be clearly identified as the underlying capital gains computation method is also

slightly different for the various events. In the given case, the relevant event that would apply is

A1 since it related to disposal of a capital asset and the concerned capital asset is land (Gilders,

et. al., 2016). The resultant capital gains with regards to this event can be obtained by subtracting

the underlying asset cost base from the proceeds derived from sale of asset.

Thus, the next imperative task is to compute the given assets’ cost base which needs to be carried

in manner consistent with s.110-25 ITAA 1997. The various key elements that have been

highlighted in accordance with this approach are mentioned as follows (Nethercott, Richardson

and Devos, 2016).

Element 1: The purchase cost linked to the underlying asset.

Element 2: Incidents costs that are spent by the taxpayer during purchase or sale of asset.

Element 3: Costs related to tax, interest cost which are incurred by the asset owner as ownership

costs.

Element 4: For the preservation of value or appreciation of same, capital expenditure may be

incurred which is included as part of cost base.

Element 5: Title preservations related capital costs

In accordance with the above discussion, the cost base of the given asset (land) needs

computation.

Element 1: Purchase Price = $ 100,000

Element 3: Ownership costs = $ 20,000

Cost base of given asset as per s. 110-25 = $ 120,000

In the sale of capital assets, a pertinent issue that may arise is due to timing difference between

the signing of sale contract and closure of the deal which typically happens with the receipt of

the sale proceeds. A critical question therefore arises in relation to CGT liability as to whether it

must be levied in the year the asset is sold or when the final payment is received. Assistance in

this regards is provided by analysing tax ruling TR 94/29 which opines that the CGT would be

levied in the year when the agreement for sale is enacted irrespective of the payment being

settled in the same year or next (Hodgson, Mortimer and Butler, 2016). Taking a cue from the

above, it is appropriate to conclude that even in case of given land also, CGT would be levied in

the current year only.

There is a capital loss to the tune of $ 7,000 which is being brought forward from previous year

and would be adjusted against the capital gains. Therefore the capital gains would reduce to $

193,000.

Section 115-25 allows discount method of taxable capital gains computation whereby 50%

rebate on long term capital gains is allowed (Kreyer, 2016). The land has been held by the client

for more than a year owing to which the underlying capital gains on land would be long term.

incurred which is included as part of cost base.

Element 5: Title preservations related capital costs

In accordance with the above discussion, the cost base of the given asset (land) needs

computation.

Element 1: Purchase Price = $ 100,000

Element 3: Ownership costs = $ 20,000

Cost base of given asset as per s. 110-25 = $ 120,000

In the sale of capital assets, a pertinent issue that may arise is due to timing difference between

the signing of sale contract and closure of the deal which typically happens with the receipt of

the sale proceeds. A critical question therefore arises in relation to CGT liability as to whether it

must be levied in the year the asset is sold or when the final payment is received. Assistance in

this regards is provided by analysing tax ruling TR 94/29 which opines that the CGT would be

levied in the year when the agreement for sale is enacted irrespective of the payment being

settled in the same year or next (Hodgson, Mortimer and Butler, 2016). Taking a cue from the

above, it is appropriate to conclude that even in case of given land also, CGT would be levied in

the current year only.

There is a capital loss to the tune of $ 7,000 which is being brought forward from previous year

and would be adjusted against the capital gains. Therefore the capital gains would reduce to $

193,000.

Section 115-25 allows discount method of taxable capital gains computation whereby 50%

rebate on long term capital gains is allowed (Kreyer, 2016). The land has been held by the client

for more than a year owing to which the underlying capital gains on land would be long term.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Asset: Antique Bed

In the given case, the relevant event that would apply is A1 since it related to disposal of a

capital asset and the concerned capital asset is land. The resultant capital gains with regards to

this event can be obtained by subtracting the underlying asset cost base from the proceeds

derived from sale of asset (Coleman, 2016).

Considering the date of purchase, it is apparent that the concerned asset is not a pre-CGT asset.

Also, the acquisition price is higher than $500, the minimum threshold for application of CGT

and therefore the capital gains ought to be computed in the manner highlighted below.

Element 1: Purchase price of asset = $ 3,500

Element 4: Capital expenditure for value appreciation = $ 1,500

Cost base of given asset as per s. 110-25 = $ 5,000

The market value would not be taken as sales proceeds since the antique has been stolen and the

insurance has only provided $ 11,000 for the same which would be used for computation of

capital gains.

Consideration needs to be given to the carry forward loss of $ 1,500 in relation to a sculpture

which also needs to be deducted from the capital gains derived above reducing the capital gains

to 4,500.

Section 115-25 allows discount method of taxable capital gains computation whereby 50%

rebate on long term capital gains is allowed (Gilders, et. al., 2016). The land has been held by the

client for more than a year owing to which the underlying capital gains on land would be long

term.

Asset : Painting

In the given case, the relevant event that would apply is A1 since it related to disposal of a

capital asset and the concerned capital asset is land. The resultant capital gains with regards to

this event can be obtained by subtracting the underlying asset cost base from the proceeds

derived from sale of asset (Coleman, 2016).

Considering the date of purchase, it is apparent that the concerned asset is not a pre-CGT asset.

Also, the acquisition price is higher than $500, the minimum threshold for application of CGT

and therefore the capital gains ought to be computed in the manner highlighted below.

Element 1: Purchase price of asset = $ 3,500

Element 4: Capital expenditure for value appreciation = $ 1,500

Cost base of given asset as per s. 110-25 = $ 5,000

The market value would not be taken as sales proceeds since the antique has been stolen and the

insurance has only provided $ 11,000 for the same which would be used for computation of

capital gains.

Consideration needs to be given to the carry forward loss of $ 1,500 in relation to a sculpture

which also needs to be deducted from the capital gains derived above reducing the capital gains

to 4,500.

Section 115-25 allows discount method of taxable capital gains computation whereby 50%

rebate on long term capital gains is allowed (Gilders, et. al., 2016). The land has been held by the

client for more than a year owing to which the underlying capital gains on land would be long

term.

Asset : Painting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section 149(1) ITAA 1997 clearly states that assets that have been acquired prior to September

20, 1985 would be categorised as pre-CGT assets and such assets would not give rise to any

liability or asset related to CGT as it would not be applicable (Nethercott, Richardson and Devos,

2016). The given asset i.e. painting on account of the date of purchase would be a pre-CGT asset

and therefore exempt from any CGT.

Asset: Shares

In the given case, the relevant event that would apply is A1 since it related to disposal of a

capital asset and the concerned capital asset is share (Hodgson, Mortimer and Butler, 2016). The

resultant capital gains with regards to this event can be obtained by subtracting the underlying

asset cost base from the proceeds derived from sale of asset.

(i) Element 1: Purchase cost= $15*1000 = $ 15,000

Element 2: Related costs of buying and selling (stamp duty and brokerage)= $ 1,300

Cost base of given asset as per s. 110-25 = 15000 +1300 = $ 16,300

Cash proceeds generated from sale of asset = 47*1000 = $ 47,000

Long term capital gains from shares = 47000 – 16300 = $ 30,700

(ii) Element 1: Purchase cost= $12*2500 = $ 30,000

Element 2: Related costs of buying and selling (stamp duty and brokerage) = $ 2,500

Cost base of given asset as per s. 110-25 = 30000 +2500 = $ 32,500

Cash proceeds generated from sale of asset = 25*2500 = $ 62,500

Long term capital gains from shares = 62500 - 32500 = $ 30,000

20, 1985 would be categorised as pre-CGT assets and such assets would not give rise to any

liability or asset related to CGT as it would not be applicable (Nethercott, Richardson and Devos,

2016). The given asset i.e. painting on account of the date of purchase would be a pre-CGT asset

and therefore exempt from any CGT.

Asset: Shares

In the given case, the relevant event that would apply is A1 since it related to disposal of a

capital asset and the concerned capital asset is share (Hodgson, Mortimer and Butler, 2016). The

resultant capital gains with regards to this event can be obtained by subtracting the underlying

asset cost base from the proceeds derived from sale of asset.

(i) Element 1: Purchase cost= $15*1000 = $ 15,000

Element 2: Related costs of buying and selling (stamp duty and brokerage)= $ 1,300

Cost base of given asset as per s. 110-25 = 15000 +1300 = $ 16,300

Cash proceeds generated from sale of asset = 47*1000 = $ 47,000

Long term capital gains from shares = 47000 – 16300 = $ 30,700

(ii) Element 1: Purchase cost= $12*2500 = $ 30,000

Element 2: Related costs of buying and selling (stamp duty and brokerage) = $ 2,500

Cost base of given asset as per s. 110-25 = 30000 +2500 = $ 32,500

Cash proceeds generated from sale of asset = 25*2500 = $ 62,500

Long term capital gains from shares = 62500 - 32500 = $ 30,000

(iii) Element 1: Purchase cost = $5*1200 = $ 6,000

Element 2: Related costs of buying and selling (stamp duty and brokerage) = $ 600

Cost base of given asset as per s. 110-25 = 6000+600 = $ 6,600

Cash proceeds generated from sale of asset = 0.5*1200 = $ 600

Long term capital losses from shares = 6600 – 600 = $6,000

(iv) Element 1: Purchase Cost= $1*10000 = $ 10,000

Element 2: Related costs of buying and selling (stamp duty and brokerage) = $ 2,000

Cost base of given asset as per s. 110-25 = 10000+2000 = $ 12,000

Cash proceeds generated from sale of asset = 2.5*10000 = $ 25,000

Short term capital gains from shares = 25000-12000= $13,000

Asset: Violin

The key asset is violin in this case which is often used by the client for her entertainment as she

is an avid player and collector of violins (Wollner, 2014). As the usage of violin is carried for

personal entertainment and that too regular basis, thus it would be labelled as an personal use

item. In relation to these items, CGT implications are only considered if the buying price exceeds

$ 10,000 which is not true for the violin in question whose acquisition price is $ 5,500 and hence

no taxable capital gains would arise.

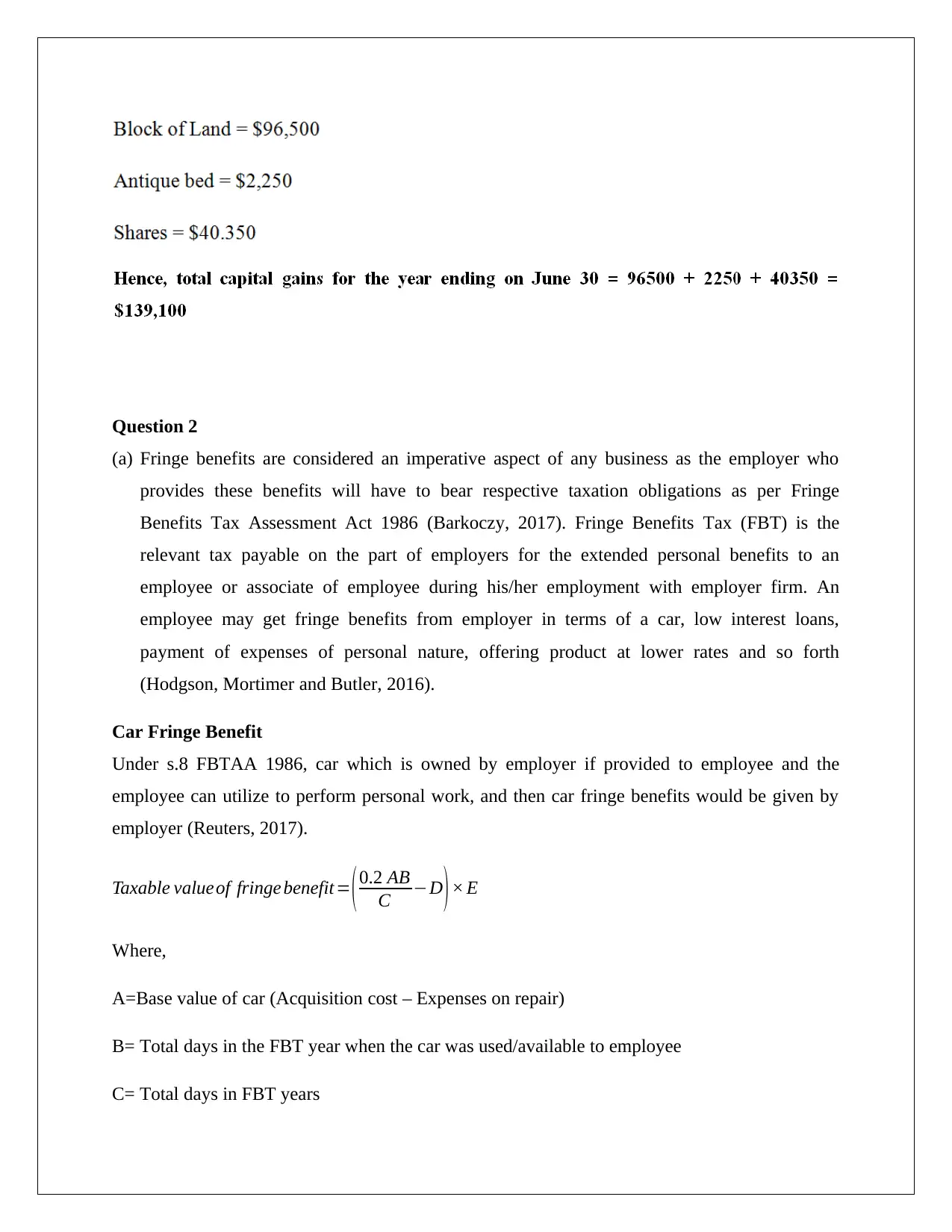

Net capital gains

Element 2: Related costs of buying and selling (stamp duty and brokerage) = $ 600

Cost base of given asset as per s. 110-25 = 6000+600 = $ 6,600

Cash proceeds generated from sale of asset = 0.5*1200 = $ 600

Long term capital losses from shares = 6600 – 600 = $6,000

(iv) Element 1: Purchase Cost= $1*10000 = $ 10,000

Element 2: Related costs of buying and selling (stamp duty and brokerage) = $ 2,000

Cost base of given asset as per s. 110-25 = 10000+2000 = $ 12,000

Cash proceeds generated from sale of asset = 2.5*10000 = $ 25,000

Short term capital gains from shares = 25000-12000= $13,000

Asset: Violin

The key asset is violin in this case which is often used by the client for her entertainment as she

is an avid player and collector of violins (Wollner, 2014). As the usage of violin is carried for

personal entertainment and that too regular basis, thus it would be labelled as an personal use

item. In relation to these items, CGT implications are only considered if the buying price exceeds

$ 10,000 which is not true for the violin in question whose acquisition price is $ 5,500 and hence

no taxable capital gains would arise.

Net capital gains

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

(a) Fringe benefits are considered an imperative aspect of any business as the employer who

provides these benefits will have to bear respective taxation obligations as per Fringe

Benefits Tax Assessment Act 1986 (Barkoczy, 2017). Fringe Benefits Tax (FBT) is the

relevant tax payable on the part of employers for the extended personal benefits to an

employee or associate of employee during his/her employment with employer firm. An

employee may get fringe benefits from employer in terms of a car, low interest loans,

payment of expenses of personal nature, offering product at lower rates and so forth

(Hodgson, Mortimer and Butler, 2016).

Car Fringe Benefit

Under s.8 FBTAA 1986, car which is owned by employer if provided to employee and the

employee can utilize to perform personal work, and then car fringe benefits would be given by

employer (Reuters, 2017).

Taxable valueof fringe benefit= (0.2 AB

C −D )× E

Where,

A=Base value of car (Acquisition cost – Expenses on repair)

B= Total days in the FBT year when the car was used/available to employee

C= Total days in FBT years

(a) Fringe benefits are considered an imperative aspect of any business as the employer who

provides these benefits will have to bear respective taxation obligations as per Fringe

Benefits Tax Assessment Act 1986 (Barkoczy, 2017). Fringe Benefits Tax (FBT) is the

relevant tax payable on the part of employers for the extended personal benefits to an

employee or associate of employee during his/her employment with employer firm. An

employee may get fringe benefits from employer in terms of a car, low interest loans,

payment of expenses of personal nature, offering product at lower rates and so forth

(Hodgson, Mortimer and Butler, 2016).

Car Fringe Benefit

Under s.8 FBTAA 1986, car which is owned by employer if provided to employee and the

employee can utilize to perform personal work, and then car fringe benefits would be given by

employer (Reuters, 2017).

Taxable valueof fringe benefit= (0.2 AB

C −D )× E

Where,

A=Base value of car (Acquisition cost – Expenses on repair)

B= Total days in the FBT year when the car was used/available to employee

C= Total days in FBT years

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D = Contribution by recipient employee

E = Gross up rate with respect to type of goods

It is evident that Rapid Heat Ltd (Rapid Heat) provides a car to its employee Jasmine on May 1,

2017 that she can use it for personal work. Therefore, car fringe benefit has been issued to

Jasmine which means FBT liability would have to be borne by Rapid Heat. Rapid Heat has paid

$33,000 to purchase the car also made the payment of expenses occurred due to minor repairs on

car.

Base value = 33000-550= $32,450

Total days in FBT year when the car was available to use for employee will be the time between

May 1, 2017 and March 31, 2018 which comes out to be 335 days. Five days when car was at the

garage for minor repairs will not be decreased from 335. Similarly, ten days when car was at

airport and Jasmine was not in the city will not be detracted from 334 days as car was available

for her to use. Also, the FBT year 2017 comprises 365 days. Jasmine has not made any payment

for car and hence, her contribution will become zero. Gross up rate with respect to car is 2.0802

(March 31, 2018) because it comes into the category of type I good as defined in GST 1999

(Deutsch, et. al., 2015).

Taxable valueof fringe benefit= (0.2 ×32450 × 335

365 −0.00 )× 2.0802=$ 12,390.85

The taxable value of car fringe benefits will be used to find the net FBT liability for employer by

multiplying with FBT rate. The FBT rate is 47% would be taken from Australian Taxation Office

for 31 March 2018.

FBT liability levied on Rapid Heat=Taxable value of fringe benefit × FBT rate=$ 12390.85× 47 %=$ 5823.7

Loan Fringe Benefit

It is a common practice for the employer to provide loan to employee at minimal interest rate or

no interest which would lead to loan fringe benefits only if the interest rate is less than the

E = Gross up rate with respect to type of goods

It is evident that Rapid Heat Ltd (Rapid Heat) provides a car to its employee Jasmine on May 1,

2017 that she can use it for personal work. Therefore, car fringe benefit has been issued to

Jasmine which means FBT liability would have to be borne by Rapid Heat. Rapid Heat has paid

$33,000 to purchase the car also made the payment of expenses occurred due to minor repairs on

car.

Base value = 33000-550= $32,450

Total days in FBT year when the car was available to use for employee will be the time between

May 1, 2017 and March 31, 2018 which comes out to be 335 days. Five days when car was at the

garage for minor repairs will not be decreased from 335. Similarly, ten days when car was at

airport and Jasmine was not in the city will not be detracted from 334 days as car was available

for her to use. Also, the FBT year 2017 comprises 365 days. Jasmine has not made any payment

for car and hence, her contribution will become zero. Gross up rate with respect to car is 2.0802

(March 31, 2018) because it comes into the category of type I good as defined in GST 1999

(Deutsch, et. al., 2015).

Taxable valueof fringe benefit= (0.2 ×32450 × 335

365 −0.00 )× 2.0802=$ 12,390.85

The taxable value of car fringe benefits will be used to find the net FBT liability for employer by

multiplying with FBT rate. The FBT rate is 47% would be taken from Australian Taxation Office

for 31 March 2018.

FBT liability levied on Rapid Heat=Taxable value of fringe benefit × FBT rate=$ 12390.85× 47 %=$ 5823.7

Loan Fringe Benefit

It is a common practice for the employer to provide loan to employee at minimal interest rate or

no interest which would lead to loan fringe benefits only if the interest rate is less than the

statutory interest rate. The statutory interest rate is the one which is announced by Reserve Bank

of Australia (RBA) for loans for the respective FBT year (Wilmot, 2014).

Taxable valueof loan= { A ( B−C ) E

D }× F

Where,

A= Total loan given to employee

B= Statutory interest rate selected by RBA

C = Interest rate selected by employer for the loan

D = Total days in FBT years

E = Total days in the FBT year when the loan was used/available to employee

F = Gross up rate with respect to type of goods

Rapid Heat Ltd has issued loan of $500,000 to Jasmine with an interest rate of 4.25% p.a. The

interest rate selected by RBA is 5.25% p.a. It can be seen that Rapid Heat has issued loan at 1%

lower rate (5.25% -4.25% =1%). Hence, Rapid Heat has issued loan fringe benefit to Jasmine.

Total days in FBT year when loan was available to Jasmine will be the time between September

1, 2017 and March 31, 2018 which is 212 days. Also, the FBT year 2017 comprises 365 days.

Gross up rate with respect to loan is 1.8868 (March 31, 2018) because it comes into the category

of type II good in GST 1999.

Taxable valueof loan= { 500000∗1 %∗212

365 } ×1.8868=$ 5479.5

FBT liability levied on Rapid Heat=Taxable value of fringe benefit × FBT rate=$ 5479.5∗47 %=$ 2575.35

It is noteworthy that deduction will be available for Rapid Heat Ltd only if the loan payment has

been used by Jasmine for assessable income production. Here, Jasmine herself used $450,000 to

own holiday home and provided rest $50,000 to husband to purchase the shares. The deduction

will be available on $450,000 when the holiday home would have been used for earning

assessable income. Further, as the $50,000 has not been used by her to purchase shares and

of Australia (RBA) for loans for the respective FBT year (Wilmot, 2014).

Taxable valueof loan= { A ( B−C ) E

D }× F

Where,

A= Total loan given to employee

B= Statutory interest rate selected by RBA

C = Interest rate selected by employer for the loan

D = Total days in FBT years

E = Total days in the FBT year when the loan was used/available to employee

F = Gross up rate with respect to type of goods

Rapid Heat Ltd has issued loan of $500,000 to Jasmine with an interest rate of 4.25% p.a. The

interest rate selected by RBA is 5.25% p.a. It can be seen that Rapid Heat has issued loan at 1%

lower rate (5.25% -4.25% =1%). Hence, Rapid Heat has issued loan fringe benefit to Jasmine.

Total days in FBT year when loan was available to Jasmine will be the time between September

1, 2017 and March 31, 2018 which is 212 days. Also, the FBT year 2017 comprises 365 days.

Gross up rate with respect to loan is 1.8868 (March 31, 2018) because it comes into the category

of type II good in GST 1999.

Taxable valueof loan= { 500000∗1 %∗212

365 } ×1.8868=$ 5479.5

FBT liability levied on Rapid Heat=Taxable value of fringe benefit × FBT rate=$ 5479.5∗47 %=$ 2575.35

It is noteworthy that deduction will be available for Rapid Heat Ltd only if the loan payment has

been used by Jasmine for assessable income production. Here, Jasmine herself used $450,000 to

own holiday home and provided rest $50,000 to husband to purchase the shares. The deduction

will be available on $450,000 when the holiday home would have been used for earning

assessable income. Further, as the $50,000 has not been used by her to purchase shares and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

therefore, this amount will not be deductible irrespective of the fact that shares is deriving

assessable income for her husband or not (Sadiq, et. al., 2015).

Expense payment fringe benefits

Benefits provided to employees or their family members by providing expense benefits such as

product of company at low prices will be termed as expense payment fringe benefits (Wollner,

2014). The FBT will be payable by employer on the account of this benefit.

Jasmine wanted to purchase a heater from Rapid Heater and therefore, they have provided the

heater to her for a price of $1300. However, the regular price of heater is $2600 for the

customers. Hence, it can be said that Rapid Heat is providing expense payment fringe benefits to

Jasmine.

Discount in price = 2600-1300 = $1300

Saving amount = (0.75*2600) -1300 =$650

Gross up rate with respect to heater is 2.0802 (March 31, 2018) because it comes into the

category of type I good in GST 1999.

Taxable value of benefit = 650 *2.0802 = $1352.1

FBT liability levied on Rapid Heat=Taxable value of fringe benefit × FBT rate=$ 1352.1∗47 %=$ 635.5

(b) Extra deduction will be available for Rapid Heat Ltd only if the $50,000 has been used by

Jasmine for purchasing the share. Therefore, the extra deduction will be calculated as

highlighted below.

Extra deduction due to $50,000 = 50000 *1 % = $500

This extra deduction will be used by Rapid Heat to lower the total FBT liability.

References

assessable income for her husband or not (Sadiq, et. al., 2015).

Expense payment fringe benefits

Benefits provided to employees or their family members by providing expense benefits such as

product of company at low prices will be termed as expense payment fringe benefits (Wollner,

2014). The FBT will be payable by employer on the account of this benefit.

Jasmine wanted to purchase a heater from Rapid Heater and therefore, they have provided the

heater to her for a price of $1300. However, the regular price of heater is $2600 for the

customers. Hence, it can be said that Rapid Heat is providing expense payment fringe benefits to

Jasmine.

Discount in price = 2600-1300 = $1300

Saving amount = (0.75*2600) -1300 =$650

Gross up rate with respect to heater is 2.0802 (March 31, 2018) because it comes into the

category of type I good in GST 1999.

Taxable value of benefit = 650 *2.0802 = $1352.1

FBT liability levied on Rapid Heat=Taxable value of fringe benefit × FBT rate=$ 1352.1∗47 %=$ 635.5

(b) Extra deduction will be available for Rapid Heat Ltd only if the $50,000 has been used by

Jasmine for purchasing the share. Therefore, the extra deduction will be calculated as

highlighted below.

Extra deduction due to $50,000 = 50000 *1 % = $500

This extra deduction will be used by Rapid Heat to lower the total FBT liability.

References

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R. (2014) Australian taxation law 2014. 8th ed. North Ryde: CCH Australia.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R. (2014) Australian taxation law 2014. 8th ed. North Ryde: CCH Australia.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.