HI6028 Taxation Theory, Practice & Law: Capital Gains & FBT Analysis

VerifiedAdded on 2023/06/03

|14

|2906

|126

Homework Assignment

AI Summary

This assignment provides a detailed analysis of Australian taxation law, specifically focusing on Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT). The first question involves calculating long-term and short-term capital gains from the sale of various assets, including land, antiques, paintings, and shares, while considering applicable discounts and losses. The second question delves into FBT, calculating the tax payable on benefits such as low-interest loans, car usage, and electronic heaters provided to employees, utilizing statutory formulas and relevant tax rates. The assignment meticulously outlines the applicable provisions, working notes, and calculations involved in determining the taxable amounts for both CGT and FBT, offering a comprehensive understanding of these aspects of Australian taxation.

Taxation Theory, Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1.......................................................................................................................................3

Applicable Provisions..................................................................................................................3

Calculation of long-term capital gain...........................................................................................4

Calculation of the short-term capital gain...............................................................................5

Calculation of the net capital gain...........................................................................................5

Working notes..........................................................................................................................5

Question 2.......................................................................................................................................7

Applicable Provisions..................................................................................................................7

Calculations of fringe benefit tax.................................................................................................9

Calculations of fringe benefit tax...............................................................................................11

References.....................................................................................................................................14

Question 1.......................................................................................................................................3

Applicable Provisions..................................................................................................................3

Calculation of long-term capital gain...........................................................................................4

Calculation of the short-term capital gain...............................................................................5

Calculation of the net capital gain...........................................................................................5

Working notes..........................................................................................................................5

Question 2.......................................................................................................................................7

Applicable Provisions..................................................................................................................7

Calculations of fringe benefit tax.................................................................................................9

Calculations of fringe benefit tax...............................................................................................11

References.....................................................................................................................................14

Question 1

Applicable Provisions

Capital Gains Tax (CGT) in relation to the Australian Taxation System, refers to a tax levied on

the capital gain made subsequent to sale/disposal of an asset, with a series of particular

exemptions, the most considerable being the family home. Rollover provisions are applicable to

certain disposals, one of the most notable of which is a transfer made to beneficiaries on death

(Littlewood & Elliffe, 2017).

CGT works by regarding net capital gains as taxable income in the tax year in which the asset is

disposed or sold. If an asset is kept for a minimum of one year, then any gain will first be

discounted by 50% for an individual taxpayer, or by 33.3% for superannuation funds. Capital

losses could be offset against CG. The net capital loss in one tax year cannot be balanced against

regular income but could be carried forward any number of times.

Capital gain/loss needs to be determined for every CGT event that happens to an asset during the

taxable year. Plus, if a person/entity has earned both capital gain and loss, then they have to

determine net capital gain/loss for that year (Edmonds, Holle & Hartanti, 2015). There are three

techniques of calculating capital gain. The assessee may select any method which best suits

him/her.

CGT Discount method – The assessee may use the discount method for computing the capital

gain on the majority of the assets they have owned for a year or more. The eligibility for this

method is that the assessee must be an individual, complying superannuation fund or trust. Plus,

the CGT event occurred to their asset after 11:45am on 21 September 1999. Moreover, they

acquired the asset in question at least a year before the CGT event. Lastly, they did not select to

use the indexation method. This method usually is not applicable to companies, though it may

apply to some capital gains made by life insurance firms. The discount percentage is the

proportion by which the assessee will reduce their capital gain (Jacob, 2018). They can reduce

the capital gain only once they have applied every capital loss for the tax year and any unapplied

net loss from previous years. The discount percentage is 50% for trusts and individuals, and

33.33% for complying superannuation funds and qualified life insurance firms. For foreign

residents, the 50% discount has been eliminated or decreased on gains made after 8 May 2012.

Applicable Provisions

Capital Gains Tax (CGT) in relation to the Australian Taxation System, refers to a tax levied on

the capital gain made subsequent to sale/disposal of an asset, with a series of particular

exemptions, the most considerable being the family home. Rollover provisions are applicable to

certain disposals, one of the most notable of which is a transfer made to beneficiaries on death

(Littlewood & Elliffe, 2017).

CGT works by regarding net capital gains as taxable income in the tax year in which the asset is

disposed or sold. If an asset is kept for a minimum of one year, then any gain will first be

discounted by 50% for an individual taxpayer, or by 33.3% for superannuation funds. Capital

losses could be offset against CG. The net capital loss in one tax year cannot be balanced against

regular income but could be carried forward any number of times.

Capital gain/loss needs to be determined for every CGT event that happens to an asset during the

taxable year. Plus, if a person/entity has earned both capital gain and loss, then they have to

determine net capital gain/loss for that year (Edmonds, Holle & Hartanti, 2015). There are three

techniques of calculating capital gain. The assessee may select any method which best suits

him/her.

CGT Discount method – The assessee may use the discount method for computing the capital

gain on the majority of the assets they have owned for a year or more. The eligibility for this

method is that the assessee must be an individual, complying superannuation fund or trust. Plus,

the CGT event occurred to their asset after 11:45am on 21 September 1999. Moreover, they

acquired the asset in question at least a year before the CGT event. Lastly, they did not select to

use the indexation method. This method usually is not applicable to companies, though it may

apply to some capital gains made by life insurance firms. The discount percentage is the

proportion by which the assessee will reduce their capital gain (Jacob, 2018). They can reduce

the capital gain only once they have applied every capital loss for the tax year and any unapplied

net loss from previous years. The discount percentage is 50% for trusts and individuals, and

33.33% for complying superannuation funds and qualified life insurance firms. For foreign

residents, the 50% discount has been eliminated or decreased on gains made after 8 May 2012.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Indexation method – The assessee can utilize the indexation technique to compute CGT if a) a

CGT even occurred to an asset they obtained before 11:45 am on 21 September 1999, and b)

they owned the asset for a year or more. If the assessee is not a company but satisfies the two

criteria, and they want to employ indexation, they may do so. Otherwise the discount technique

will apply by default. If the assessee is a company and the and the gain satisfies the two criteria,

they must employ the indexation technique to compute the CGT (Evans, Minas & Lim, 2015).

Under this method, the assessee will increase every amount covered in a component of the cost

base by an indexation factor. This indexation factor is determined by to utilize the consumer

price index (CPI).

Other method – As per the research performed by Woellner and et al., (2016), this method is

used for assets that have been acquired for less than a year before the occurrence of the CGT

event. Under this case, the basic technique of reducing cost base from the sale amount is applied

for ascertaining capital gain/loss.

Davidson, & Evans (2015) claimed that setting the timing of CGT is also crucial as the reason

behind this is that it informs the assessee that in which year the gain or loss is to be reported and

perhaps has an impact on how a person calculates the tax liability. If an individual is disposing of

a CGT asset, then the event normally happens at the time when the person enters into the

contract of disposal. For example, in the case of real estate, CGT event normally occurs at the

time when a person enters into the control and not when a person settles.

Calculation of long-term capital gain

Particulars Working note Capital gain or loss

Amount (in $)

Block of vacant land 1 200000

Antique Bed 2 6000

Painting 3 123000

Profit/loss from shares 4

Common bank shares 29500

PHB Iron Ore Ltd 30000

Young Kids Learning (6000)

Violin 5 6500

CGT even occurred to an asset they obtained before 11:45 am on 21 September 1999, and b)

they owned the asset for a year or more. If the assessee is not a company but satisfies the two

criteria, and they want to employ indexation, they may do so. Otherwise the discount technique

will apply by default. If the assessee is a company and the and the gain satisfies the two criteria,

they must employ the indexation technique to compute the CGT (Evans, Minas & Lim, 2015).

Under this method, the assessee will increase every amount covered in a component of the cost

base by an indexation factor. This indexation factor is determined by to utilize the consumer

price index (CPI).

Other method – As per the research performed by Woellner and et al., (2016), this method is

used for assets that have been acquired for less than a year before the occurrence of the CGT

event. Under this case, the basic technique of reducing cost base from the sale amount is applied

for ascertaining capital gain/loss.

Davidson, & Evans (2015) claimed that setting the timing of CGT is also crucial as the reason

behind this is that it informs the assessee that in which year the gain or loss is to be reported and

perhaps has an impact on how a person calculates the tax liability. If an individual is disposing of

a CGT asset, then the event normally happens at the time when the person enters into the

contract of disposal. For example, in the case of real estate, CGT event normally occurs at the

time when a person enters into the control and not when a person settles.

Calculation of long-term capital gain

Particulars Working note Capital gain or loss

Amount (in $)

Block of vacant land 1 200000

Antique Bed 2 6000

Painting 3 123000

Profit/loss from shares 4

Common bank shares 29500

PHB Iron Ore Ltd 30000

Young Kids Learning (6000)

Violin 5 6500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

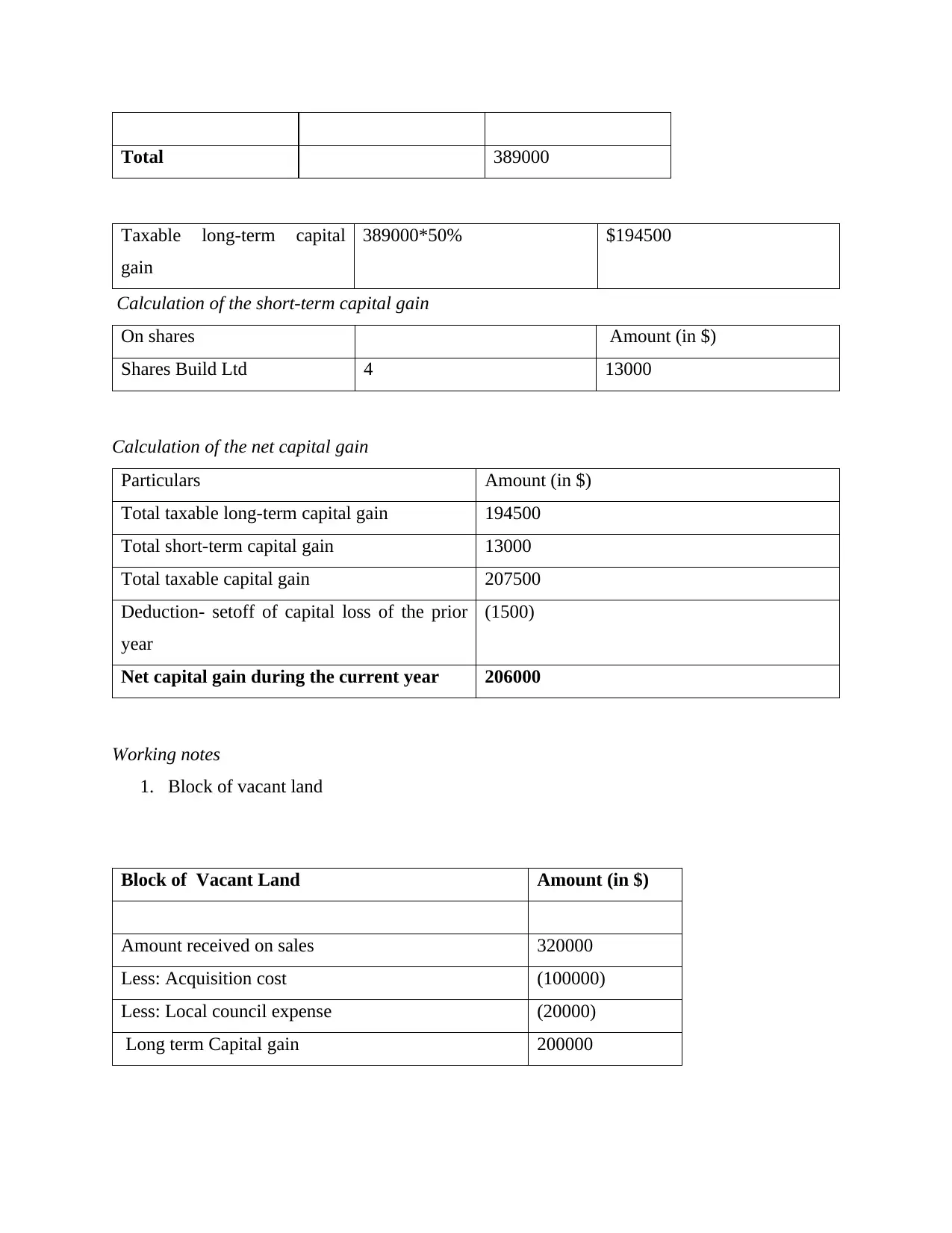

Total 389000

Taxable long-term capital

gain

389000*50% $194500

Calculation of the short-term capital gain

On shares Amount (in $)

Shares Build Ltd 4 13000

Calculation of the net capital gain

Particulars Amount (in $)

Total taxable long-term capital gain 194500

Total short-term capital gain 13000

Total taxable capital gain 207500

Deduction- setoff of capital loss of the prior

year

(1500)

Net capital gain during the current year 206000

Working notes

1. Block of vacant land

Block of Vacant Land Amount (in $)

Amount received on sales 320000

Less: Acquisition cost (100000)

Less: Local council expense (20000)

Long term Capital gain 200000

Taxable long-term capital

gain

389000*50% $194500

Calculation of the short-term capital gain

On shares Amount (in $)

Shares Build Ltd 4 13000

Calculation of the net capital gain

Particulars Amount (in $)

Total taxable long-term capital gain 194500

Total short-term capital gain 13000

Total taxable capital gain 207500

Deduction- setoff of capital loss of the prior

year

(1500)

Net capital gain during the current year 206000

Working notes

1. Block of vacant land

Block of Vacant Land Amount (in $)

Amount received on sales 320000

Less: Acquisition cost (100000)

Less: Local council expense (20000)

Long term Capital gain 200000

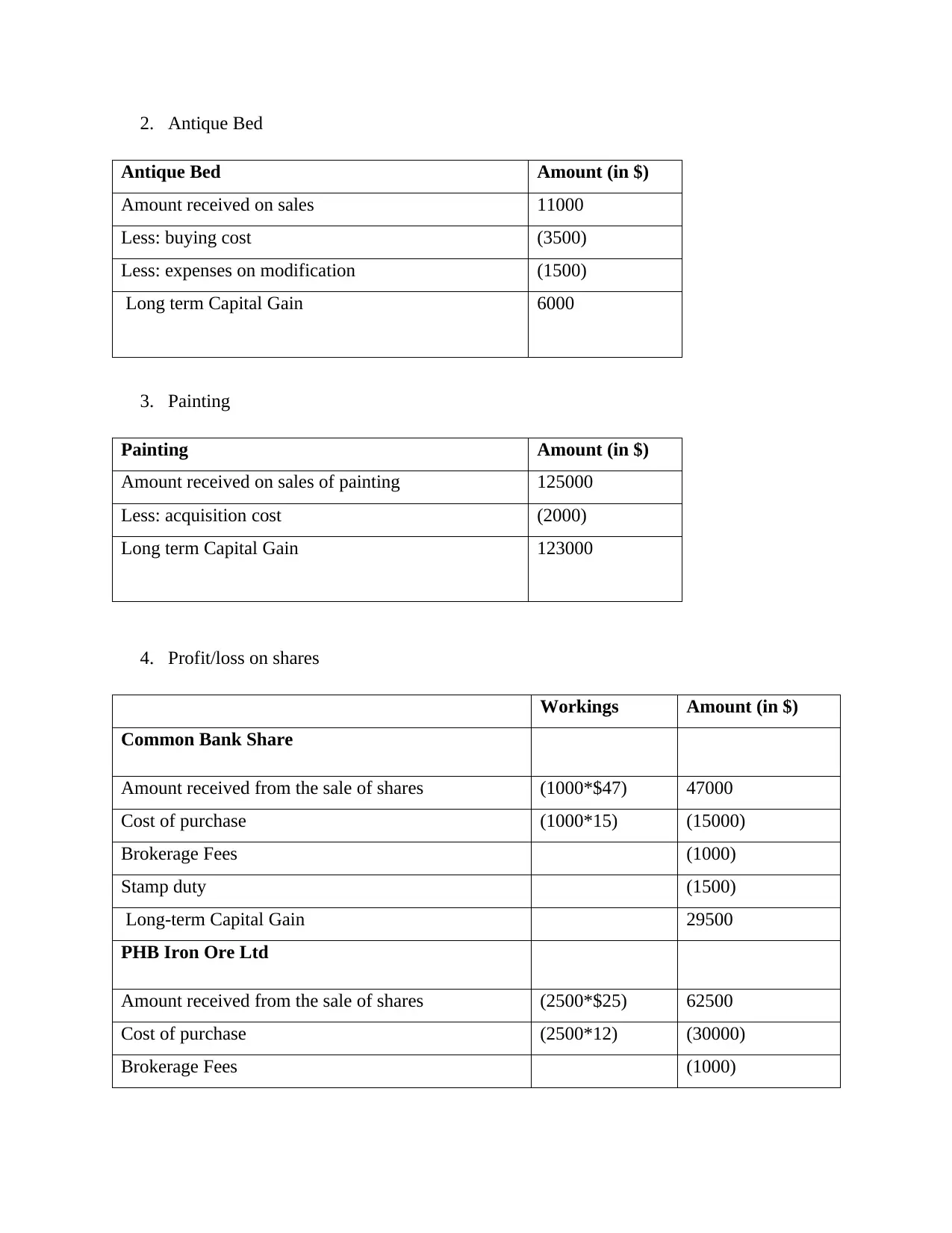

2. Antique Bed

Antique Bed Amount (in $)

Amount received on sales 11000

Less: buying cost (3500)

Less: expenses on modification (1500)

Long term Capital Gain 6000

3. Painting

Painting Amount (in $)

Amount received on sales of painting 125000

Less: acquisition cost (2000)

Long term Capital Gain 123000

4. Profit/loss on shares

Workings Amount (in $)

Common Bank Share

Amount received from the sale of shares (1000*$47) 47000

Cost of purchase (1000*15) (15000)

Brokerage Fees (1000)

Stamp duty (1500)

Long-term Capital Gain 29500

PHB Iron Ore Ltd

Amount received from the sale of shares (2500*$25) 62500

Cost of purchase (2500*12) (30000)

Brokerage Fees (1000)

Antique Bed Amount (in $)

Amount received on sales 11000

Less: buying cost (3500)

Less: expenses on modification (1500)

Long term Capital Gain 6000

3. Painting

Painting Amount (in $)

Amount received on sales of painting 125000

Less: acquisition cost (2000)

Long term Capital Gain 123000

4. Profit/loss on shares

Workings Amount (in $)

Common Bank Share

Amount received from the sale of shares (1000*$47) 47000

Cost of purchase (1000*15) (15000)

Brokerage Fees (1000)

Stamp duty (1500)

Long-term Capital Gain 29500

PHB Iron Ore Ltd

Amount received from the sale of shares (2500*$25) 62500

Cost of purchase (2500*12) (30000)

Brokerage Fees (1000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

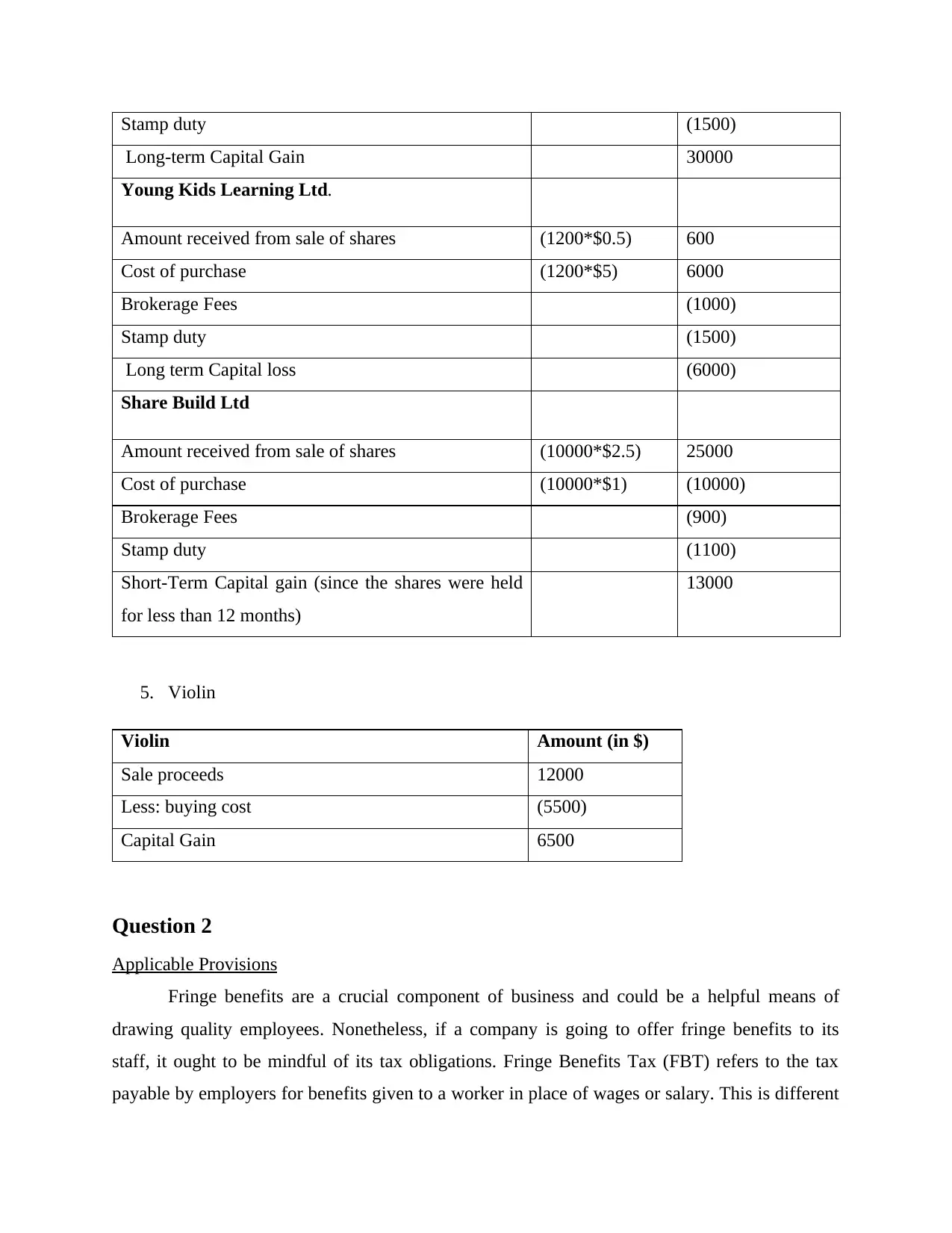

Stamp duty (1500)

Long-term Capital Gain 30000

Young Kids Learning Ltd.

Amount received from sale of shares (1200*$0.5) 600

Cost of purchase (1200*$5) 6000

Brokerage Fees (1000)

Stamp duty (1500)

Long term Capital loss (6000)

Share Build Ltd

Amount received from sale of shares (10000*$2.5) 25000

Cost of purchase (10000*$1) (10000)

Brokerage Fees (900)

Stamp duty (1100)

Short-Term Capital gain (since the shares were held

for less than 12 months)

13000

5. Violin

Violin Amount (in $)

Sale proceeds 12000

Less: buying cost (5500)

Capital Gain 6500

Question 2

Applicable Provisions

Fringe benefits are a crucial component of business and could be a helpful means of

drawing quality employees. Nonetheless, if a company is going to offer fringe benefits to its

staff, it ought to be mindful of its tax obligations. Fringe Benefits Tax (FBT) refers to the tax

payable by employers for benefits given to a worker in place of wages or salary. This is different

Long-term Capital Gain 30000

Young Kids Learning Ltd.

Amount received from sale of shares (1200*$0.5) 600

Cost of purchase (1200*$5) 6000

Brokerage Fees (1000)

Stamp duty (1500)

Long term Capital loss (6000)

Share Build Ltd

Amount received from sale of shares (10000*$2.5) 25000

Cost of purchase (10000*$1) (10000)

Brokerage Fees (900)

Stamp duty (1100)

Short-Term Capital gain (since the shares were held

for less than 12 months)

13000

5. Violin

Violin Amount (in $)

Sale proceeds 12000

Less: buying cost (5500)

Capital Gain 6500

Question 2

Applicable Provisions

Fringe benefits are a crucial component of business and could be a helpful means of

drawing quality employees. Nonetheless, if a company is going to offer fringe benefits to its

staff, it ought to be mindful of its tax obligations. Fringe Benefits Tax (FBT) refers to the tax

payable by employers for benefits given to a worker in place of wages or salary. This is different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

than income tax and is computed on the taxable amount of the benefits given. To obtain the best

employees, employers often have to appeal to them with non-income related benefits (Barkoczy,

2018). A worker can get fringe benefits in the form of:

Low-interest loans,

A car,

Free car parking,

Entertainment

Living away from home allowance

Payment of personal expenses

FBT on car

Car fringe benefit emerges in the situation when the company gives the car for private use to a

worker. Hence, if an employer makes a car it owns or leases available for the personal use of its

staff, then it is said to be provided as a fringe benefit. For the purpose of FBT, a car is any of the

below mentioned:

A station wagon or sedan

Any other vehicle which carries goods with a carrying capacity of not more than one ton.

Any other carrying vehicle built to carry less than 9 passengers (CCH Australia Ltd.

2011).

To compute fringe benefit on the car, the employer should determine the taxable value of the

benefit utilizing either:

The legal formula technique based on the cost price of the car; or

The operating cost technique based on the cost of using the car

The employer can pick whichever technique produces the lowest taxable value, irrespective of

which technique was utilized in the preceding year. However, if the employer has not maintained

needed documentation for the operating cost technique, then it must employ the legal formula.

Under the statutory formula, a single rate, i.e. 20% is used irrespective of the distance travelled.

This rate is applicable in all cases except in the case where a pre-established commitment is

present to give the car for private use (CCH Australia Ltd. 2011). Under the operating cost

formula, a fringe benefit is determined as the percentage of total cost of using the car during the

employees, employers often have to appeal to them with non-income related benefits (Barkoczy,

2018). A worker can get fringe benefits in the form of:

Low-interest loans,

A car,

Free car parking,

Entertainment

Living away from home allowance

Payment of personal expenses

FBT on car

Car fringe benefit emerges in the situation when the company gives the car for private use to a

worker. Hence, if an employer makes a car it owns or leases available for the personal use of its

staff, then it is said to be provided as a fringe benefit. For the purpose of FBT, a car is any of the

below mentioned:

A station wagon or sedan

Any other vehicle which carries goods with a carrying capacity of not more than one ton.

Any other carrying vehicle built to carry less than 9 passengers (CCH Australia Ltd.

2011).

To compute fringe benefit on the car, the employer should determine the taxable value of the

benefit utilizing either:

The legal formula technique based on the cost price of the car; or

The operating cost technique based on the cost of using the car

The employer can pick whichever technique produces the lowest taxable value, irrespective of

which technique was utilized in the preceding year. However, if the employer has not maintained

needed documentation for the operating cost technique, then it must employ the legal formula.

Under the statutory formula, a single rate, i.e. 20% is used irrespective of the distance travelled.

This rate is applicable in all cases except in the case where a pre-established commitment is

present to give the car for private use (CCH Australia Ltd. 2011). Under the operating cost

formula, a fringe benefit is determined as the percentage of total cost of using the car during the

taxable year. Plus, the percentage is assessed based on the degree to which car has been utilized

for personal use. The greater the actual personal use, the higher the taxable value.

FBT on loan

Fringe benefit pertaining to loan arises in the event where a loan is given to an employee, and the

interest rate is less than the normal industry rate. Plus, the loan must not be exempt for taxation

purposes. Fringe benefit pertaining to loan is available every year in which the employee is

obligated to pay either complete or part of the loan. Plus, the interest rate is less than the industry

standard. The statutory interest rate is worked out as per the standard variable rate pertaining to

owner-occupied housing loans of major banking institutions. This is also published the Reserve

Bank of Australia before the beginning of the new financial year (Wilmot, 2012).

FBT on other benefits

The provision of FBT is applicable if fringe benefit during the taxable year is above $2,000.

Hence, a worker is obligated to report the gross value of taxable fringe benefit given to him/her

in the way of a summary for the relevant income year. The rate at which FBT is taxable for the

financial year ending 31 March 2015 is 47%. A further tax on the same is paid by the employer.

Taxation rate of 47% includes 45% of marginal IT and 2% of the medical charge (Deutsch et al.,

2017). This rate is applicable to grossed-up value of all benefits that are obtained by the

employee reduced to the degree of contribution given by the employer.

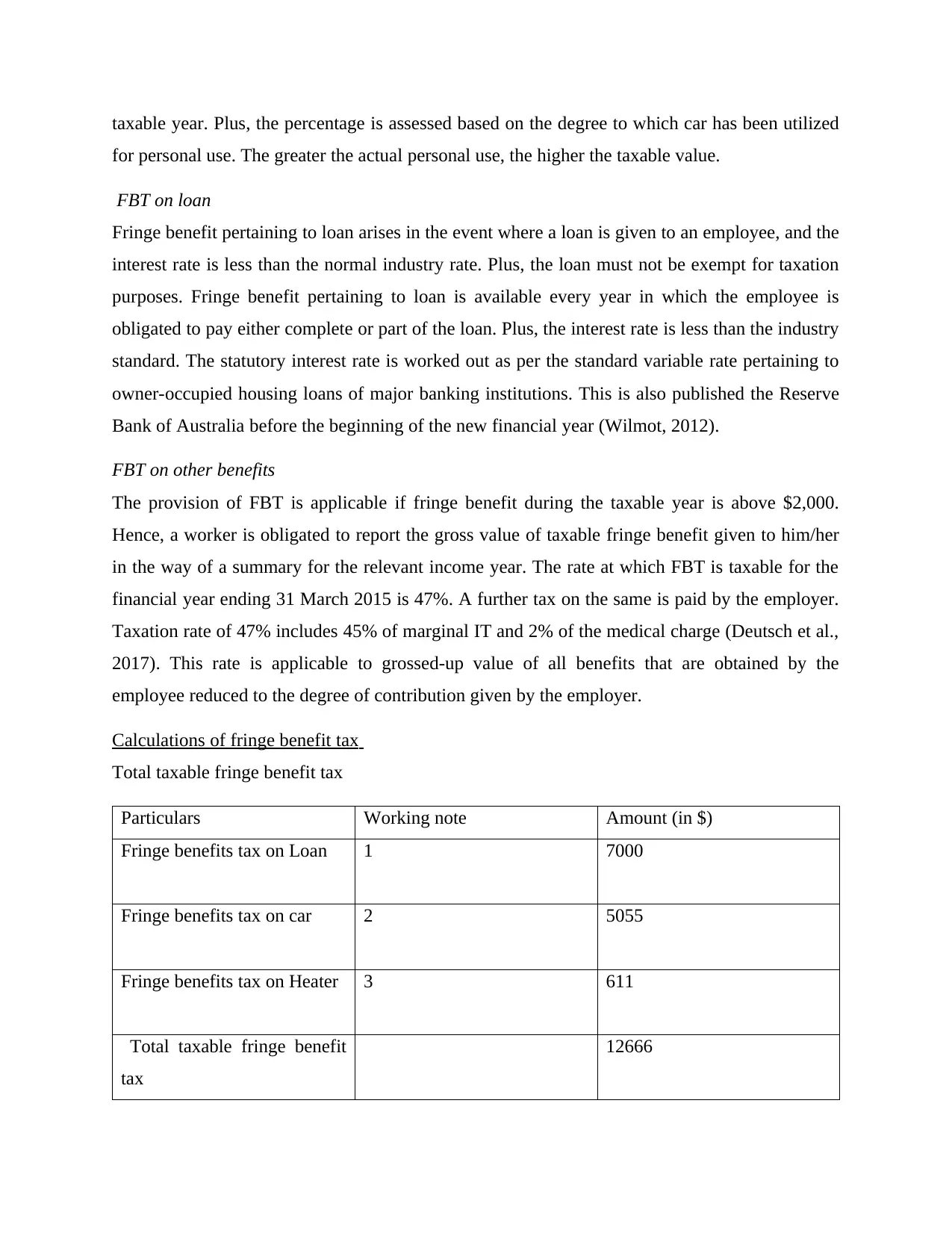

Calculations of fringe benefit tax

Total taxable fringe benefit tax

Particulars Working note Amount (in $)

Fringe benefits tax on Loan 1 7000

Fringe benefits tax on car 2 5055

Fringe benefits tax on Heater 3 611

Total taxable fringe benefit

tax

12666

for personal use. The greater the actual personal use, the higher the taxable value.

FBT on loan

Fringe benefit pertaining to loan arises in the event where a loan is given to an employee, and the

interest rate is less than the normal industry rate. Plus, the loan must not be exempt for taxation

purposes. Fringe benefit pertaining to loan is available every year in which the employee is

obligated to pay either complete or part of the loan. Plus, the interest rate is less than the industry

standard. The statutory interest rate is worked out as per the standard variable rate pertaining to

owner-occupied housing loans of major banking institutions. This is also published the Reserve

Bank of Australia before the beginning of the new financial year (Wilmot, 2012).

FBT on other benefits

The provision of FBT is applicable if fringe benefit during the taxable year is above $2,000.

Hence, a worker is obligated to report the gross value of taxable fringe benefit given to him/her

in the way of a summary for the relevant income year. The rate at which FBT is taxable for the

financial year ending 31 March 2015 is 47%. A further tax on the same is paid by the employer.

Taxation rate of 47% includes 45% of marginal IT and 2% of the medical charge (Deutsch et al.,

2017). This rate is applicable to grossed-up value of all benefits that are obtained by the

employee reduced to the degree of contribution given by the employer.

Calculations of fringe benefit tax

Total taxable fringe benefit tax

Particulars Working note Amount (in $)

Fringe benefits tax on Loan 1 7000

Fringe benefits tax on car 2 5055

Fringe benefits tax on Heater 3 611

Total taxable fringe benefit

tax

12666

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

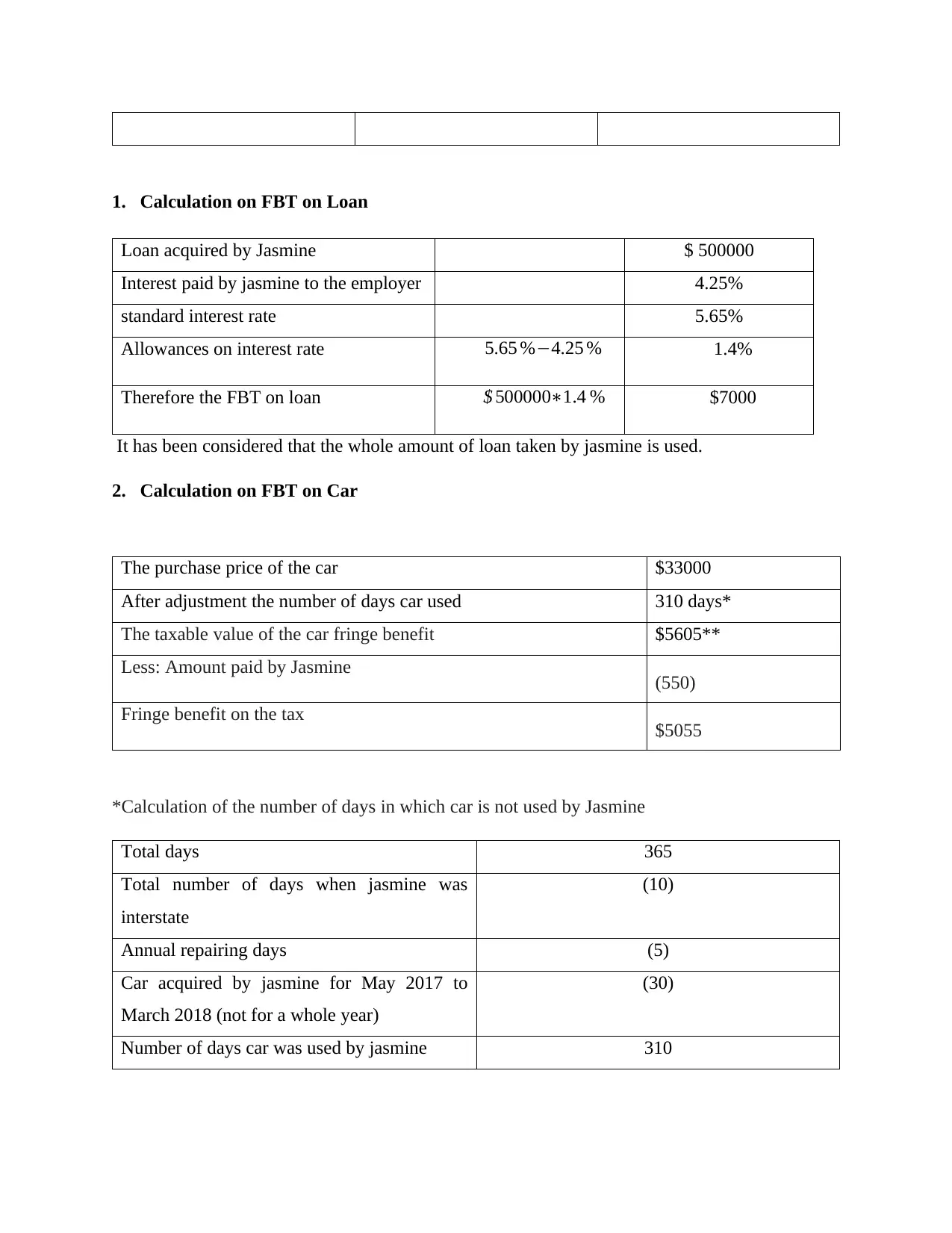

1. Calculation on FBT on Loan

Loan acquired by Jasmine $ 500000

Interest paid by jasmine to the employer 4.25%

standard interest rate 5.65%

Allowances on interest rate 5.65 %−4.25 % 1.4%

Therefore the FBT on loan $ 500000∗1.4 % $7000

It has been considered that the whole amount of loan taken by jasmine is used.

2. Calculation on FBT on Car

The purchase price of the car $33000

After adjustment the number of days car used 310 days*

The taxable value of the car fringe benefit $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

*Calculation of the number of days in which car is not used by Jasmine

Total days 365

Total number of days when jasmine was

interstate

(10)

Annual repairing days (5)

Car acquired by jasmine for May 2017 to

March 2018 (not for a whole year)

(30)

Number of days car was used by jasmine 310

Loan acquired by Jasmine $ 500000

Interest paid by jasmine to the employer 4.25%

standard interest rate 5.65%

Allowances on interest rate 5.65 %−4.25 % 1.4%

Therefore the FBT on loan $ 500000∗1.4 % $7000

It has been considered that the whole amount of loan taken by jasmine is used.

2. Calculation on FBT on Car

The purchase price of the car $33000

After adjustment the number of days car used 310 days*

The taxable value of the car fringe benefit $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

*Calculation of the number of days in which car is not used by Jasmine

Total days 365

Total number of days when jasmine was

interstate

(10)

Annual repairing days (5)

Car acquired by jasmine for May 2017 to

March 2018 (not for a whole year)

(30)

Number of days car was used by jasmine 310

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

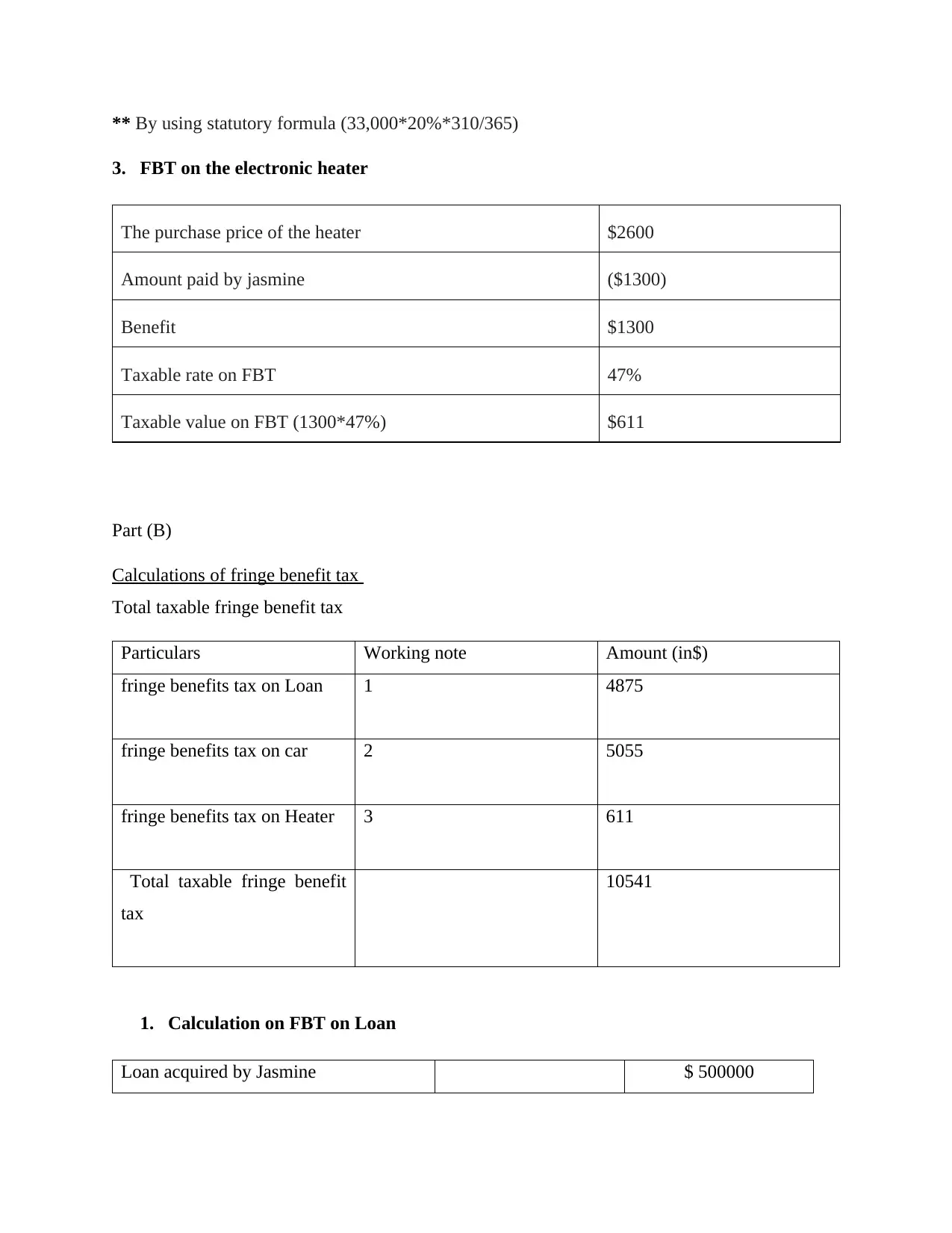

** By using statutory formula (33,000*20%*310/365)

3. FBT on the electronic heater

The purchase price of the heater $2600

Amount paid by jasmine ($1300)

Benefit $1300

Taxable rate on FBT 47%

Taxable value on FBT (1300*47%) $611

Part (B)

Calculations of fringe benefit tax

Total taxable fringe benefit tax

Particulars Working note Amount (in$)

fringe benefits tax on Loan 1 4875

fringe benefits tax on car 2 5055

fringe benefits tax on Heater 3 611

Total taxable fringe benefit

tax

10541

1. Calculation on FBT on Loan

Loan acquired by Jasmine $ 500000

3. FBT on the electronic heater

The purchase price of the heater $2600

Amount paid by jasmine ($1300)

Benefit $1300

Taxable rate on FBT 47%

Taxable value on FBT (1300*47%) $611

Part (B)

Calculations of fringe benefit tax

Total taxable fringe benefit tax

Particulars Working note Amount (in$)

fringe benefits tax on Loan 1 4875

fringe benefits tax on car 2 5055

fringe benefits tax on Heater 3 611

Total taxable fringe benefit

tax

10541

1. Calculation on FBT on Loan

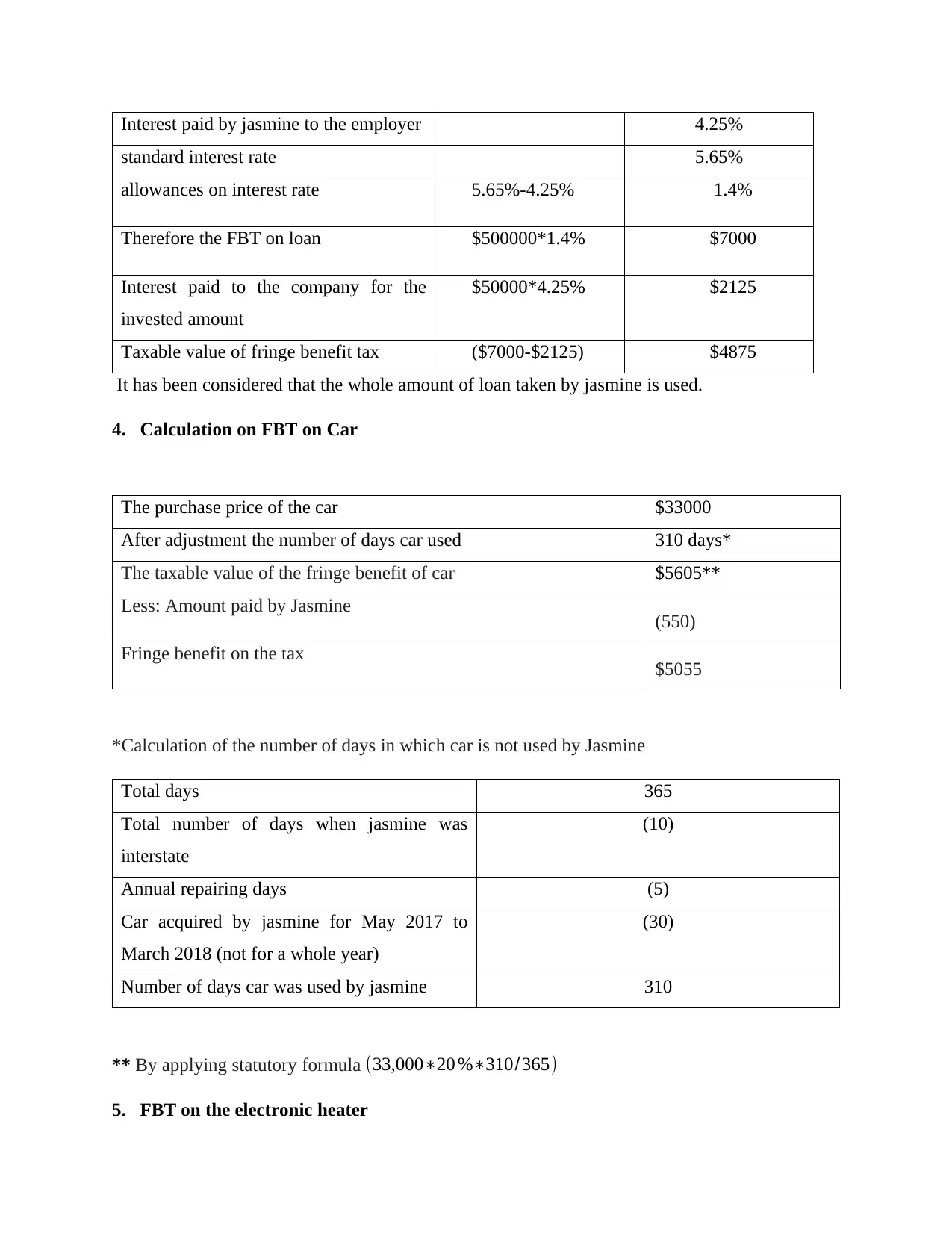

Loan acquired by Jasmine $ 500000

Interest paid by jasmine to the employer 4.25%

standard interest rate 5.65%

allowances on interest rate 5.65%-4.25% 1.4%

Therefore the FBT on loan $500000*1.4% $7000

Interest paid to the company for the

invested amount

$50000*4.25% $2125

Taxable value of fringe benefit tax ($7000-$2125) $4875

It has been considered that the whole amount of loan taken by jasmine is used.

4. Calculation on FBT on Car

The purchase price of the car $33000

After adjustment the number of days car used 310 days*

The taxable value of the fringe benefit of car $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

*Calculation of the number of days in which car is not used by Jasmine

Total days 365

Total number of days when jasmine was

interstate

(10)

Annual repairing days (5)

Car acquired by jasmine for May 2017 to

March 2018 (not for a whole year)

(30)

Number of days car was used by jasmine 310

** By applying statutory formula (33,000∗20 %∗310/365)

5. FBT on the electronic heater

standard interest rate 5.65%

allowances on interest rate 5.65%-4.25% 1.4%

Therefore the FBT on loan $500000*1.4% $7000

Interest paid to the company for the

invested amount

$50000*4.25% $2125

Taxable value of fringe benefit tax ($7000-$2125) $4875

It has been considered that the whole amount of loan taken by jasmine is used.

4. Calculation on FBT on Car

The purchase price of the car $33000

After adjustment the number of days car used 310 days*

The taxable value of the fringe benefit of car $5605**

Less: Amount paid by Jasmine (550)

Fringe benefit on the tax $5055

*Calculation of the number of days in which car is not used by Jasmine

Total days 365

Total number of days when jasmine was

interstate

(10)

Annual repairing days (5)

Car acquired by jasmine for May 2017 to

March 2018 (not for a whole year)

(30)

Number of days car was used by jasmine 310

** By applying statutory formula (33,000∗20 %∗310/365)

5. FBT on the electronic heater

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.