Taxation Law: Capital Gains Tax & Fringe Benefits Tax - T2 2018

VerifiedAdded on 2023/06/04

|12

|2636

|371

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT) based on a hypothetical scenario. It involves calculating capital gains and losses from the disposal of various assets, considering pre-CGT assets, CGT event A1, sale proceeds, and cost base. The assignment also addresses long-term capital gains and the applicability of discounts. Furthermore, it examines Fringe Benefits Tax (FBT) implications for an employer providing car fringe benefits, loan fringe benefits, and expense fringe benefits to an employee, considering relevant legislation such as the Fringe Benefits Assessment Act 1986. The analysis includes calculations of FBT liability and deductions based on provided scenarios, concluding with a determination of net capital gains and FBT obligations.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

CAPITAL GAINS TAX

Issue

The task is to do computation for the capital gains/losses which would be resulted from the

disposal of the capital assets of the taxpayers for FY 2018.

Law

For given scenario, the taxpayer does not carry a business of trading the assets and hence, the

implication of ordinary income generation would not be applied here and thus, the disposal of

capital assets is deriving capital proceeds only (Nethercott, Richardson and Devos, 2016).

The key elements required for calculating the capital gains/losses are discussed below based on

the relevant provisions.

It is essential to take note of the fact that Capital Gains Tax (CGT) will not be valid or apply

for the capital gains which are resulted from the liquidations of a pre-CGT asset. Thus, only

those assets which do not fall under the category of pre-CGT asset would be considered for

CGT liability. It can be easily be determined based on the date of buying of the capital assets

as any capital asset which has bought before September 20, 1985 is termed as pre-CGT asset

and capital gains from such type of assets will not be considered for CGT liability (Krever,

2017).

Capital gains produced from the transaction made for capital asset’s disposal is termed as

CGT event A1 (s. 104-5, ITAA 1997) (Sadiq, et.al., 2015). The main procedure of

determining the capital gain from the capital asset’s disposal would involve two main

parameters which are sale proceeds and cost base.

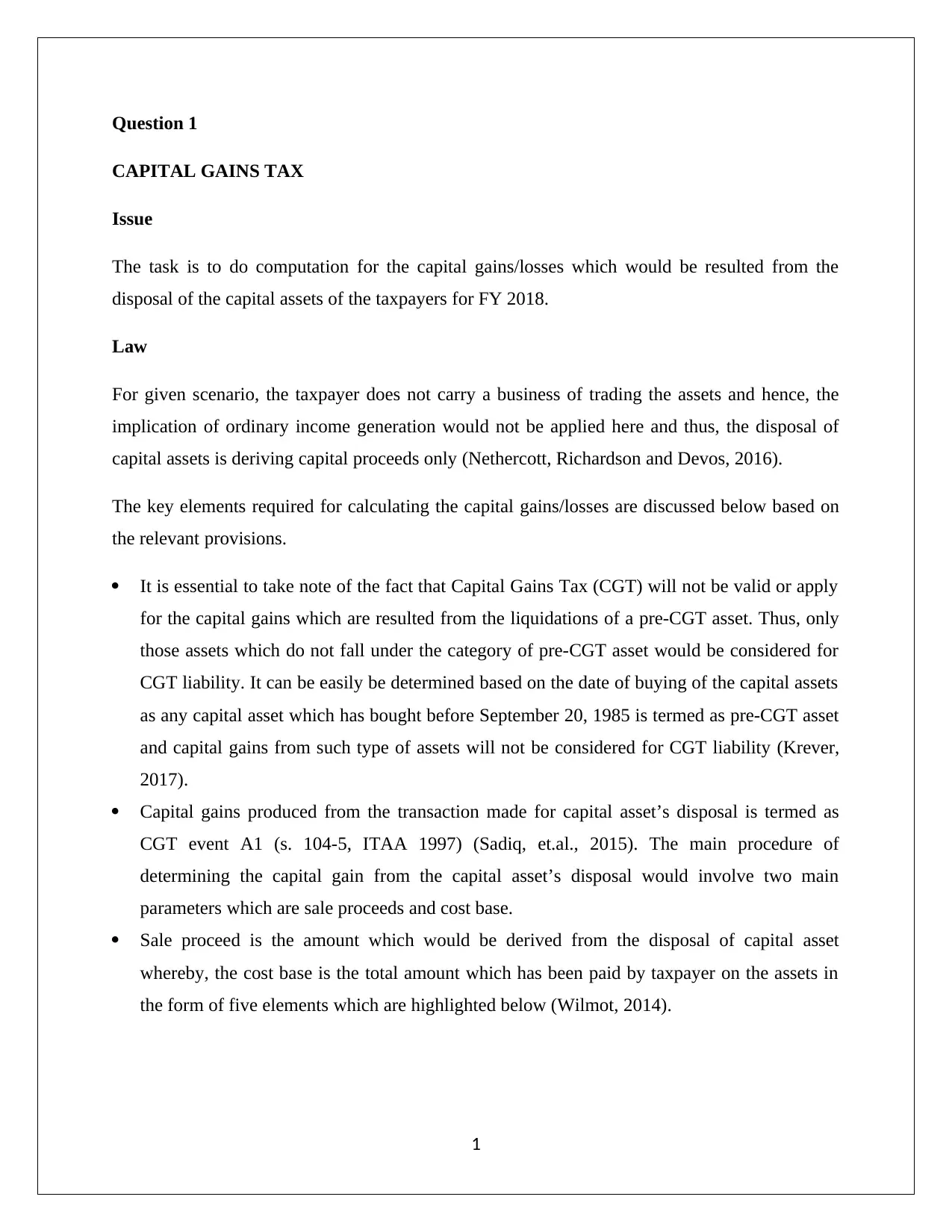

Sale proceed is the amount which would be derived from the disposal of capital asset

whereby, the cost base is the total amount which has been paid by taxpayer on the assets in

the form of five elements which are highlighted below (Wilmot, 2014).

1

CAPITAL GAINS TAX

Issue

The task is to do computation for the capital gains/losses which would be resulted from the

disposal of the capital assets of the taxpayers for FY 2018.

Law

For given scenario, the taxpayer does not carry a business of trading the assets and hence, the

implication of ordinary income generation would not be applied here and thus, the disposal of

capital assets is deriving capital proceeds only (Nethercott, Richardson and Devos, 2016).

The key elements required for calculating the capital gains/losses are discussed below based on

the relevant provisions.

It is essential to take note of the fact that Capital Gains Tax (CGT) will not be valid or apply

for the capital gains which are resulted from the liquidations of a pre-CGT asset. Thus, only

those assets which do not fall under the category of pre-CGT asset would be considered for

CGT liability. It can be easily be determined based on the date of buying of the capital assets

as any capital asset which has bought before September 20, 1985 is termed as pre-CGT asset

and capital gains from such type of assets will not be considered for CGT liability (Krever,

2017).

Capital gains produced from the transaction made for capital asset’s disposal is termed as

CGT event A1 (s. 104-5, ITAA 1997) (Sadiq, et.al., 2015). The main procedure of

determining the capital gain from the capital asset’s disposal would involve two main

parameters which are sale proceeds and cost base.

Sale proceed is the amount which would be derived from the disposal of capital asset

whereby, the cost base is the total amount which has been paid by taxpayer on the assets in

the form of five elements which are highlighted below (Wilmot, 2014).

1

Income from the sale would be part of the capital gains in the year in which the sale contract

has been signed between the parties (taxpayer and buyer) irrespective of the underlying

factor that income proceeds would not be received in the same income year (TR 97/29)

(Reuters, 2017).

According to TD 1997/40, any antique item will be known as collectable. Further, the CGT

liability will only be applicable when the purchasing amount of the antique item paid by

taxpayer is more than a benchmark amount which is $500 in case of collectables (Woellner,

2017).

The items which are known as the personal use asset of taxpayer will only be taken for CGT

liability after disposal when the purchasing amount paid by taxpayer is more than a set

amount which is $10,000 (Gilders, et. al., 2015).

For both collectables and personal use asset the benchmark buying cost paid by taxpayer is

essential condition because the CGT applicability will be valid only when the amount would

be more than $500 and $10,000 respectively (Sadiq, et.al., 2015).

Long term capital gains are those which are produced through capital assets which are held

by taxpayer for more a year (s. 11525(1), ITAA 1997. It is imperative aspect to differentiate

between long term and short terms capital gains because when there is a long term capital

gains, then the taxpayer will receive the discount to halve the total amount of capital gains

subject to CGT liability as per s. 115-25 ITAA 1997 (Hodgson,Mortimer and Butler, 2016).

Application

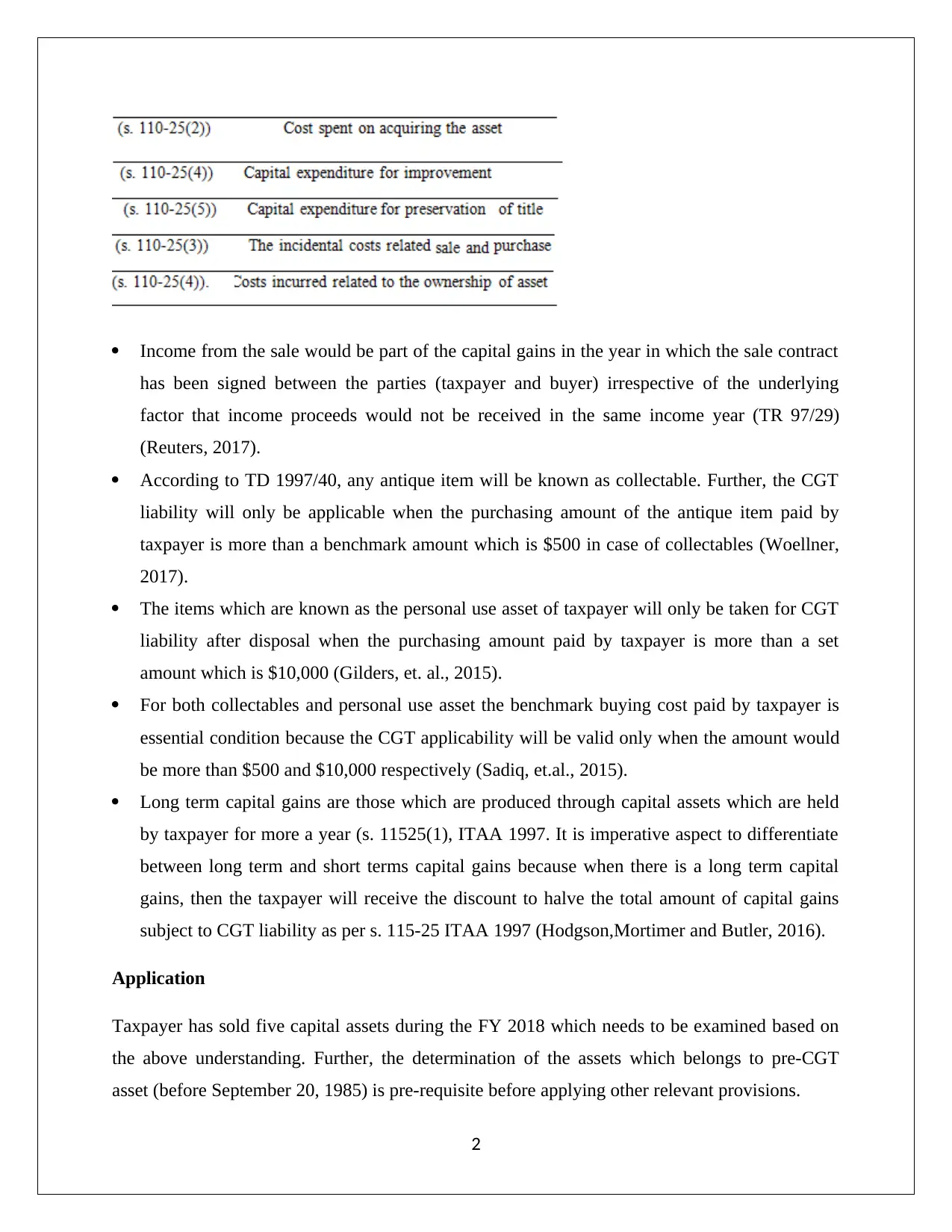

Taxpayer has sold five capital assets during the FY 2018 which needs to be examined based on

the above understanding. Further, the determination of the assets which belongs to pre-CGT

asset (before September 20, 1985) is pre-requisite before applying other relevant provisions.

2

has been signed between the parties (taxpayer and buyer) irrespective of the underlying

factor that income proceeds would not be received in the same income year (TR 97/29)

(Reuters, 2017).

According to TD 1997/40, any antique item will be known as collectable. Further, the CGT

liability will only be applicable when the purchasing amount of the antique item paid by

taxpayer is more than a benchmark amount which is $500 in case of collectables (Woellner,

2017).

The items which are known as the personal use asset of taxpayer will only be taken for CGT

liability after disposal when the purchasing amount paid by taxpayer is more than a set

amount which is $10,000 (Gilders, et. al., 2015).

For both collectables and personal use asset the benchmark buying cost paid by taxpayer is

essential condition because the CGT applicability will be valid only when the amount would

be more than $500 and $10,000 respectively (Sadiq, et.al., 2015).

Long term capital gains are those which are produced through capital assets which are held

by taxpayer for more a year (s. 11525(1), ITAA 1997. It is imperative aspect to differentiate

between long term and short terms capital gains because when there is a long term capital

gains, then the taxpayer will receive the discount to halve the total amount of capital gains

subject to CGT liability as per s. 115-25 ITAA 1997 (Hodgson,Mortimer and Butler, 2016).

Application

Taxpayer has sold five capital assets during the FY 2018 which needs to be examined based on

the above understanding. Further, the determination of the assets which belongs to pre-CGT

asset (before September 20, 1985) is pre-requisite before applying other relevant provisions.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is apparent from the above table that Painting is a pre-CGT asset and as per above

understanding the CGT liability will not be imposed on the capital gains/losses produced from

the disposal of paining. However, all the other four assets are not pre-CGT asset and the

respective transaction for capital asset sale is capital A1 event and therefore, the CGT liability

will bed impose and capital gains/losses are furnished as given below.

Block of vacant land

Purchase cost paid on January 2001=$ 100,000 ,

Signed contractual sale income that would receive in next year ¿ $ 320,000

Ownership payment would be incidental cost ¿ $ 20,000

Cost base ¿ 100,000+20,000=$ 120,000

Hence,

Capital gains ¿ 320,000 – 120,000=$ 200,000 (deducting cost base)

Capital losses = $7,000 (Previous years)

Net capital gains,

Capital gains ¿ 200,000−7,000=$ 193,000(Balancing capital losses)

Capital gains for CGT ¿ 0.5∗(193,000)=$ 96,500(long term capital gains because 50% rebate

will be applicable)

3

understanding the CGT liability will not be imposed on the capital gains/losses produced from

the disposal of paining. However, all the other four assets are not pre-CGT asset and the

respective transaction for capital asset sale is capital A1 event and therefore, the CGT liability

will bed impose and capital gains/losses are furnished as given below.

Block of vacant land

Purchase cost paid on January 2001=$ 100,000 ,

Signed contractual sale income that would receive in next year ¿ $ 320,000

Ownership payment would be incidental cost ¿ $ 20,000

Cost base ¿ 100,000+20,000=$ 120,000

Hence,

Capital gains ¿ 320,000 – 120,000=$ 200,000 (deducting cost base)

Capital losses = $7,000 (Previous years)

Net capital gains,

Capital gains ¿ 200,000−7,000=$ 193,000(Balancing capital losses)

Capital gains for CGT ¿ 0.5∗(193,000)=$ 96,500(long term capital gains because 50% rebate

will be applicable)

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Antique bed

According to TD 1997/40, antique bed will be known as collectable (Reuters, 2017). Further, the

CGT liability will be applicable because purchasing amount of the antique bed paid by taxpayer

($3,500) is more than a benchmark amount which is $500.

Purchase cost paid on July 21, 1986 ¿ $ 3,500

Capital expenditure for improvement of bed condition ¿ $ 1,500

Cost base ¿ 3500+1500=$ 5,000

Insurance income will be taken as sale income from disposal ¿ $ 11,000

Capital gains ¿ 11,000 – 5,000=$ 6,000

Capital losses ¿ $ 1500 ((Previous years) from sale of Sculpture)

Hence,

Capital gains ¿ 6000−1500=$ 4,500 (Balancing capital losses)

Capital gains ¿ 0.5∗( 4500)=$ 2,250 (long term capital gains because 50% rebate will be

applicable)

Painting

Capital gain tax liability will not impose on taxpayer as it belongs to pre-CGT asset.

Shares

Capital gain tax liability will be imposed on taxpayer as they do not belong to pre-CGT asset.

Also, transaction for the capital asset (share) sale is an A1 event.

4

According to TD 1997/40, antique bed will be known as collectable (Reuters, 2017). Further, the

CGT liability will be applicable because purchasing amount of the antique bed paid by taxpayer

($3,500) is more than a benchmark amount which is $500.

Purchase cost paid on July 21, 1986 ¿ $ 3,500

Capital expenditure for improvement of bed condition ¿ $ 1,500

Cost base ¿ 3500+1500=$ 5,000

Insurance income will be taken as sale income from disposal ¿ $ 11,000

Capital gains ¿ 11,000 – 5,000=$ 6,000

Capital losses ¿ $ 1500 ((Previous years) from sale of Sculpture)

Hence,

Capital gains ¿ 6000−1500=$ 4,500 (Balancing capital losses)

Capital gains ¿ 0.5∗( 4500)=$ 2,250 (long term capital gains because 50% rebate will be

applicable)

Painting

Capital gain tax liability will not impose on taxpayer as it belongs to pre-CGT asset.

Shares

Capital gain tax liability will be imposed on taxpayer as they do not belong to pre-CGT asset.

Also, transaction for the capital asset (share) sale is an A1 event.

4

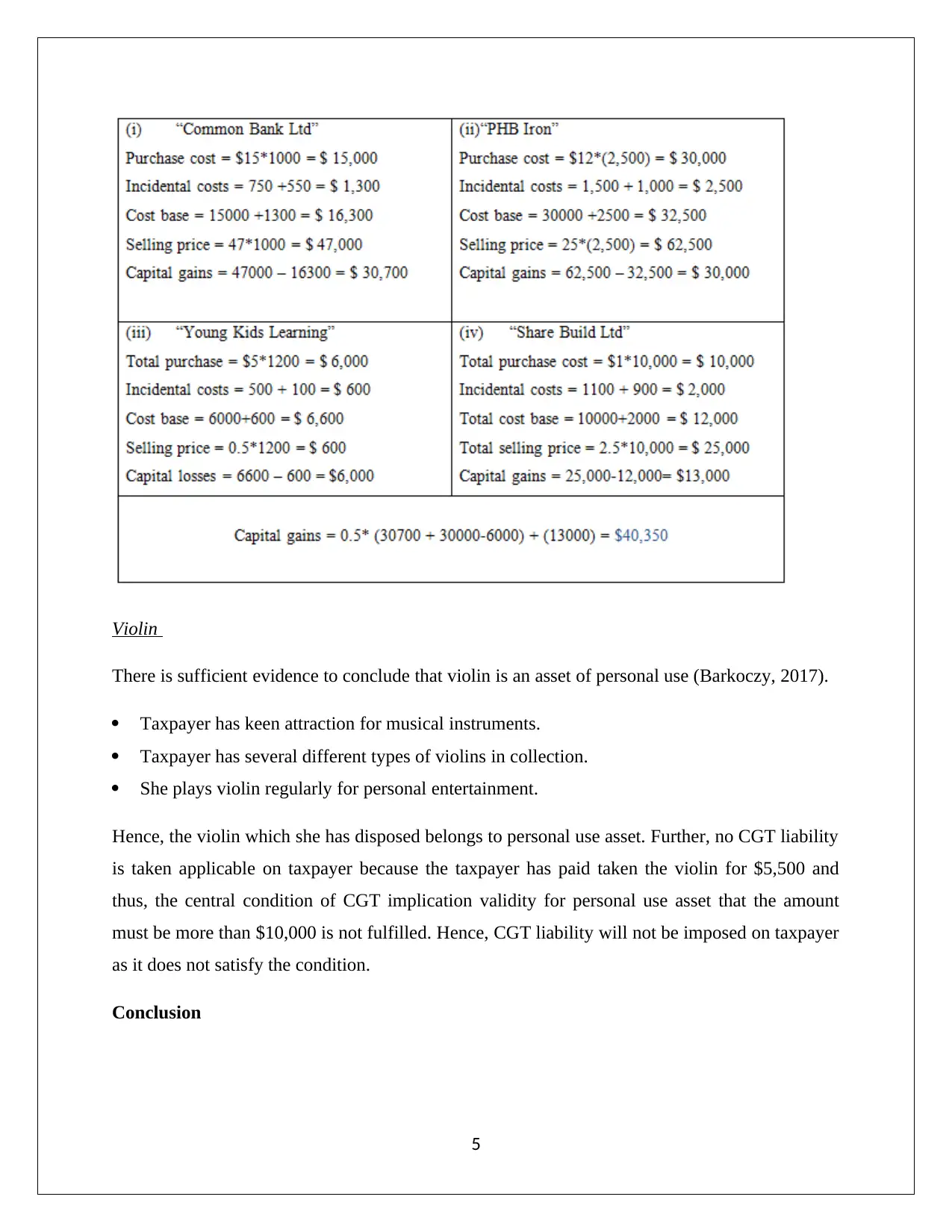

Violin

There is sufficient evidence to conclude that violin is an asset of personal use (Barkoczy, 2017).

Taxpayer has keen attraction for musical instruments.

Taxpayer has several different types of violins in collection.

She plays violin regularly for personal entertainment.

Hence, the violin which she has disposed belongs to personal use asset. Further, no CGT liability

is taken applicable on taxpayer because the taxpayer has paid taken the violin for $5,500 and

thus, the central condition of CGT implication validity for personal use asset that the amount

must be more than $10,000 is not fulfilled. Hence, CGT liability will not be imposed on taxpayer

as it does not satisfy the condition.

Conclusion

5

There is sufficient evidence to conclude that violin is an asset of personal use (Barkoczy, 2017).

Taxpayer has keen attraction for musical instruments.

Taxpayer has several different types of violins in collection.

She plays violin regularly for personal entertainment.

Hence, the violin which she has disposed belongs to personal use asset. Further, no CGT liability

is taken applicable on taxpayer because the taxpayer has paid taken the violin for $5,500 and

thus, the central condition of CGT implication validity for personal use asset that the amount

must be more than $10,000 is not fulfilled. Hence, CGT liability will not be imposed on taxpayer

as it does not satisfy the condition.

Conclusion

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxpayer has net capital gains of $139,100 as on June 30, 2018 after adjusting previous capital

losses and applying discount on long term capital gains. Thus, the CGT liability will be

considered on the net capital gains of $139,100.

Question 2

FRINGE BENEFIT TAX

Issue

The issue is to extend advice to Rapid Heat regarding their Fringe Benefits Tax payable (FBT

payable) for the consideration of offered fringe benefits in income year.

Law and Application

The relevant fringe benefits and its tax consequences are outlined in Fringe Benefits Assessment

Act 1986. The main understanding has been drawn from the act and it includes that fringe

benefits are for personal interest of employee provided by the respective employer, utilized by

the employee and taxed on behalf of the employer. No personal fringe benefit liability is attached

on employee or associates of employee for the utilization of the fringe benefits (Barkoczy, 2017).

Car fringe benefit

The employer may issue car as in the process of providing personal benefits to employee because

giving car for private use of employees is known as the car fringe benefits (s. 7, FBTAA 1986).

The capital value of car comprises purchasing cost along with the potential deduction for paid

minor expenses of the employer (Coleman, 2016). Further, the car availability defines the total

duration for which the car held present to employee for private utilization. The deduction would

not be available from the total duration for which the car is held present for personal usages

when the car is shifted to the garage in order to do some minor repairing and also when the car is

parked by the taxpayer at certain parking and taxpayer is away. Similarly, the car which is being

available for use when the employee is going out for work will not deducted from total duration

of car availability (Deutsch, et.al., 2015).

6

losses and applying discount on long term capital gains. Thus, the CGT liability will be

considered on the net capital gains of $139,100.

Question 2

FRINGE BENEFIT TAX

Issue

The issue is to extend advice to Rapid Heat regarding their Fringe Benefits Tax payable (FBT

payable) for the consideration of offered fringe benefits in income year.

Law and Application

The relevant fringe benefits and its tax consequences are outlined in Fringe Benefits Assessment

Act 1986. The main understanding has been drawn from the act and it includes that fringe

benefits are for personal interest of employee provided by the respective employer, utilized by

the employee and taxed on behalf of the employer. No personal fringe benefit liability is attached

on employee or associates of employee for the utilization of the fringe benefits (Barkoczy, 2017).

Car fringe benefit

The employer may issue car as in the process of providing personal benefits to employee because

giving car for private use of employees is known as the car fringe benefits (s. 7, FBTAA 1986).

The capital value of car comprises purchasing cost along with the potential deduction for paid

minor expenses of the employer (Coleman, 2016). Further, the car availability defines the total

duration for which the car held present to employee for private utilization. The deduction would

not be available from the total duration for which the car is held present for personal usages

when the car is shifted to the garage in order to do some minor repairing and also when the car is

parked by the taxpayer at certain parking and taxpayer is away. Similarly, the car which is being

available for use when the employee is going out for work will not deducted from total duration

of car availability (Deutsch, et.al., 2015).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Moreover, GST is also held imposed on car and hence, the gross up factor for type I goods is

also taken into account which is 2.0802. Likewise, the fringe benefits tax rate (FBT rate) for

March 31, 2018 is flat 47% on the derived taxable value of the fringe benefit (Hodgson,Mortimer

and Butler, 2016).

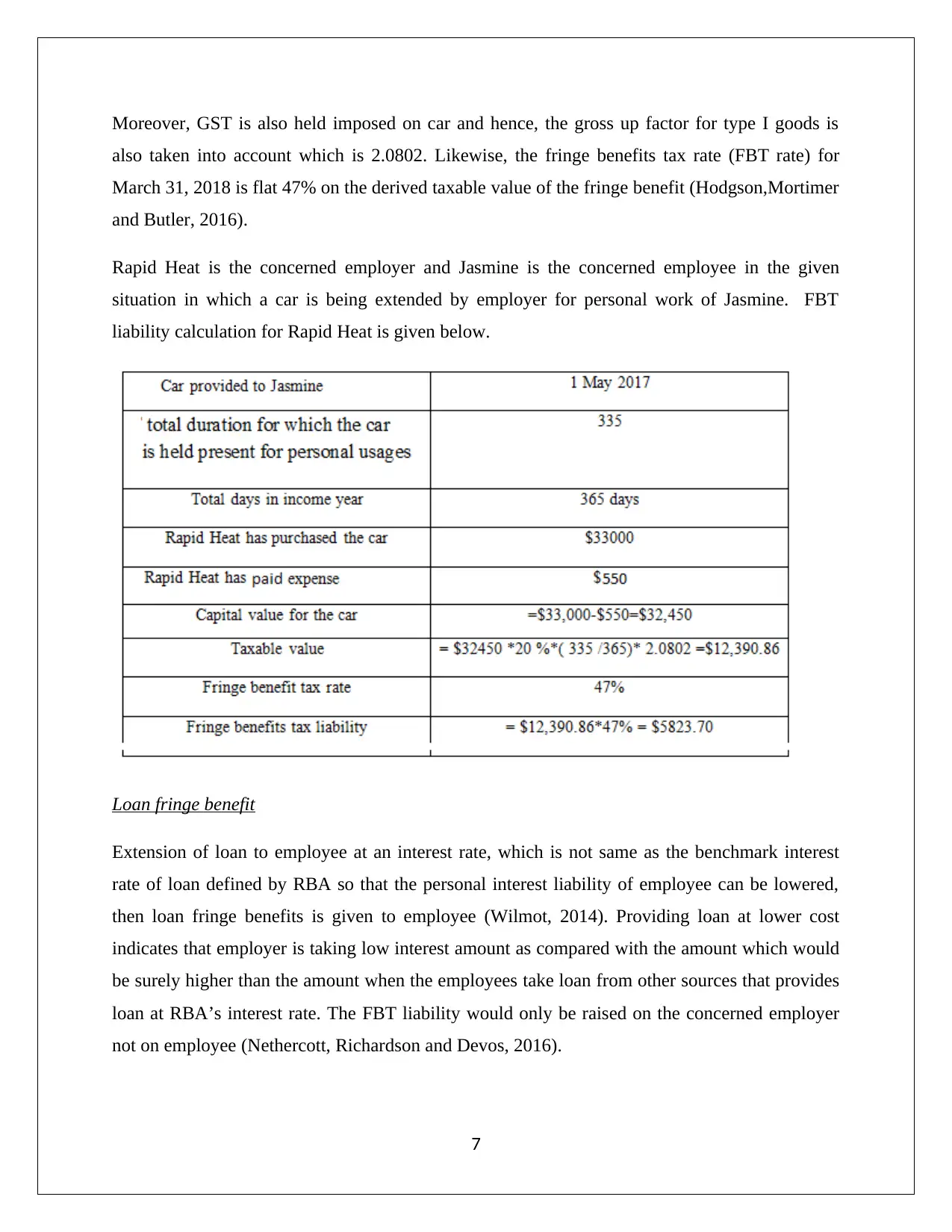

Rapid Heat is the concerned employer and Jasmine is the concerned employee in the given

situation in which a car is being extended by employer for personal work of Jasmine. FBT

liability calculation for Rapid Heat is given below.

Loan fringe benefit

Extension of loan to employee at an interest rate, which is not same as the benchmark interest

rate of loan defined by RBA so that the personal interest liability of employee can be lowered,

then loan fringe benefits is given to employee (Wilmot, 2014). Providing loan at lower cost

indicates that employer is taking low interest amount as compared with the amount which would

be surely higher than the amount when the employees take loan from other sources that provides

loan at RBA’s interest rate. The FBT liability would only be raised on the concerned employer

not on employee (Nethercott, Richardson and Devos, 2016).

7

also taken into account which is 2.0802. Likewise, the fringe benefits tax rate (FBT rate) for

March 31, 2018 is flat 47% on the derived taxable value of the fringe benefit (Hodgson,Mortimer

and Butler, 2016).

Rapid Heat is the concerned employer and Jasmine is the concerned employee in the given

situation in which a car is being extended by employer for personal work of Jasmine. FBT

liability calculation for Rapid Heat is given below.

Loan fringe benefit

Extension of loan to employee at an interest rate, which is not same as the benchmark interest

rate of loan defined by RBA so that the personal interest liability of employee can be lowered,

then loan fringe benefits is given to employee (Wilmot, 2014). Providing loan at lower cost

indicates that employer is taking low interest amount as compared with the amount which would

be surely higher than the amount when the employees take loan from other sources that provides

loan at RBA’s interest rate. The FBT liability would only be raised on the concerned employer

not on employee (Nethercott, Richardson and Devos, 2016).

7

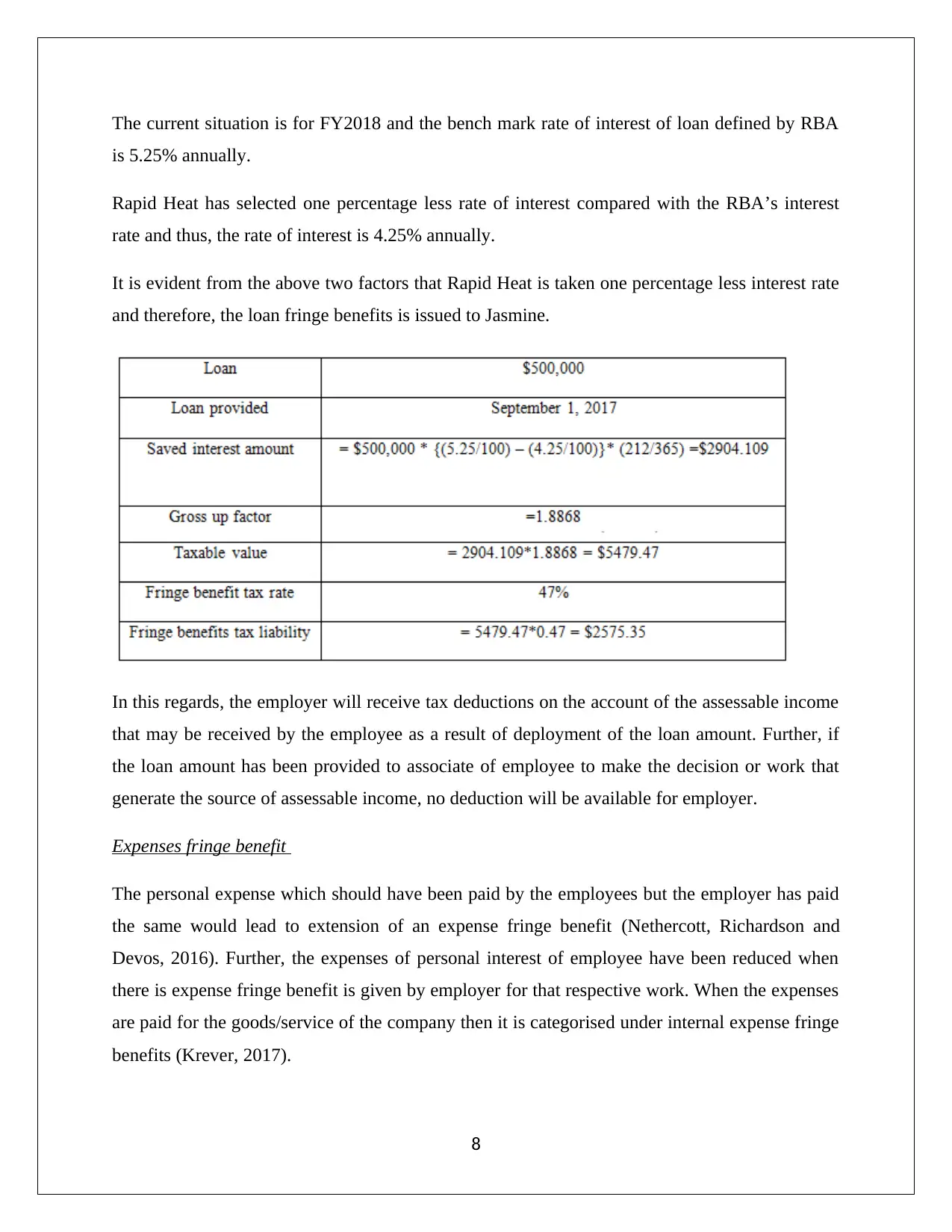

The current situation is for FY2018 and the bench mark rate of interest of loan defined by RBA

is 5.25% annually.

Rapid Heat has selected one percentage less rate of interest compared with the RBA’s interest

rate and thus, the rate of interest is 4.25% annually.

It is evident from the above two factors that Rapid Heat is taken one percentage less interest rate

and therefore, the loan fringe benefits is issued to Jasmine.

In this regards, the employer will receive tax deductions on the account of the assessable income

that may be received by the employee as a result of deployment of the loan amount. Further, if

the loan amount has been provided to associate of employee to make the decision or work that

generate the source of assessable income, no deduction will be available for employer.

Expenses fringe benefit

The personal expense which should have been paid by the employees but the employer has paid

the same would lead to extension of an expense fringe benefit (Nethercott, Richardson and

Devos, 2016). Further, the expenses of personal interest of employee have been reduced when

there is expense fringe benefit is given by employer for that respective work. When the expenses

are paid for the goods/service of the company then it is categorised under internal expense fringe

benefits (Krever, 2017).

8

is 5.25% annually.

Rapid Heat has selected one percentage less rate of interest compared with the RBA’s interest

rate and thus, the rate of interest is 4.25% annually.

It is evident from the above two factors that Rapid Heat is taken one percentage less interest rate

and therefore, the loan fringe benefits is issued to Jasmine.

In this regards, the employer will receive tax deductions on the account of the assessable income

that may be received by the employee as a result of deployment of the loan amount. Further, if

the loan amount has been provided to associate of employee to make the decision or work that

generate the source of assessable income, no deduction will be available for employer.

Expenses fringe benefit

The personal expense which should have been paid by the employees but the employer has paid

the same would lead to extension of an expense fringe benefit (Nethercott, Richardson and

Devos, 2016). Further, the expenses of personal interest of employee have been reduced when

there is expense fringe benefit is given by employer for that respective work. When the expenses

are paid for the goods/service of the company then it is categorised under internal expense fringe

benefits (Krever, 2017).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

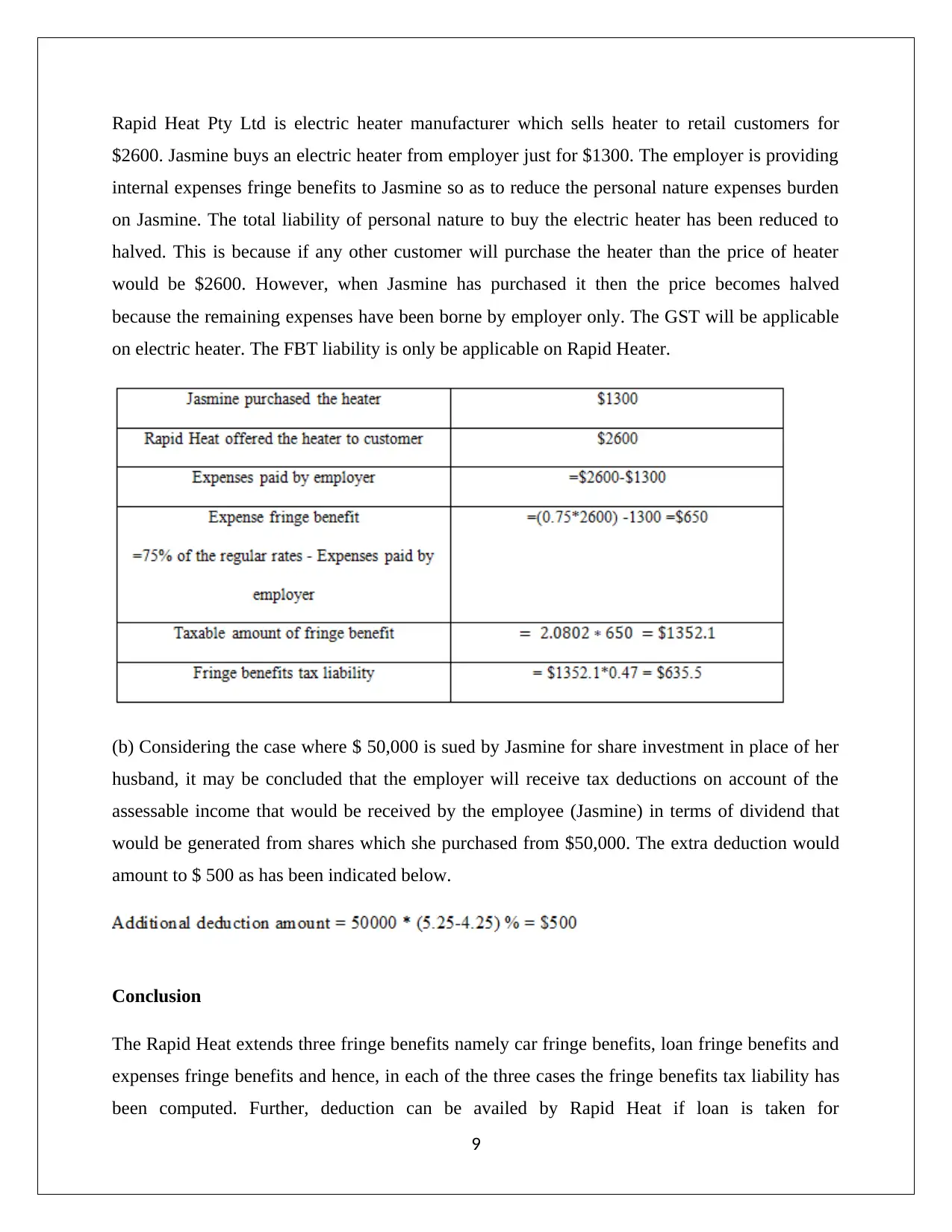

Rapid Heat Pty Ltd is electric heater manufacturer which sells heater to retail customers for

$2600. Jasmine buys an electric heater from employer just for $1300. The employer is providing

internal expenses fringe benefits to Jasmine so as to reduce the personal nature expenses burden

on Jasmine. The total liability of personal nature to buy the electric heater has been reduced to

halved. This is because if any other customer will purchase the heater than the price of heater

would be $2600. However, when Jasmine has purchased it then the price becomes halved

because the remaining expenses have been borne by employer only. The GST will be applicable

on electric heater. The FBT liability is only be applicable on Rapid Heater.

(b) Considering the case where $ 50,000 is sued by Jasmine for share investment in place of her

husband, it may be concluded that the employer will receive tax deductions on account of the

assessable income that would be received by the employee (Jasmine) in terms of dividend that

would be generated from shares which she purchased from $50,000. The extra deduction would

amount to $ 500 as has been indicated below.

Conclusion

The Rapid Heat extends three fringe benefits namely car fringe benefits, loan fringe benefits and

expenses fringe benefits and hence, in each of the three cases the fringe benefits tax liability has

been computed. Further, deduction can be availed by Rapid Heat if loan is taken for

9

$2600. Jasmine buys an electric heater from employer just for $1300. The employer is providing

internal expenses fringe benefits to Jasmine so as to reduce the personal nature expenses burden

on Jasmine. The total liability of personal nature to buy the electric heater has been reduced to

halved. This is because if any other customer will purchase the heater than the price of heater

would be $2600. However, when Jasmine has purchased it then the price becomes halved

because the remaining expenses have been borne by employer only. The GST will be applicable

on electric heater. The FBT liability is only be applicable on Rapid Heater.

(b) Considering the case where $ 50,000 is sued by Jasmine for share investment in place of her

husband, it may be concluded that the employer will receive tax deductions on account of the

assessable income that would be received by the employee (Jasmine) in terms of dividend that

would be generated from shares which she purchased from $50,000. The extra deduction would

amount to $ 500 as has been indicated below.

Conclusion

The Rapid Heat extends three fringe benefits namely car fringe benefits, loan fringe benefits and

expenses fringe benefits and hence, in each of the three cases the fringe benefits tax liability has

been computed. Further, deduction can be availed by Rapid Heat if loan is taken for

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consideration of assessable income generation but the same has to be done by Jasmine and not by

her husband.

10

her husband.

10

References

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017) Australian Taxation Law 2017 27th

ed. Sydney: Oxford University Press Australia.

11

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study Manual 2016. 8th

ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017) Australian Taxation Law 2017 27th

ed. Sydney: Oxford University Press Australia.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.