capital gains tax car or motorcycle Assignment 2022

Added on 2022-10-09

17 Pages3319 Words20 Views

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

TAXATION LAW1

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................2

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................3

Answer G:..............................................................................................................................3

Answer H:..............................................................................................................................3

Answer I:................................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................6

References:...............................................................................................................................15

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................2

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................3

Answer G:..............................................................................................................................3

Answer H:..............................................................................................................................3

Answer I:................................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................6

References:...............................................................................................................................15

TAXATION LAW2

Answer to question 1:

Answer A:

As states in “Taxation Ruling of TR 2009/1” it gives the view of official of tax about

when an organization do the business as per the term of SBE under “Sec-23 of the Income

Tax Rates Act 1986” that are relevant for the year 2015-16 and 2016-17 or within “sec-328-

110, ITAA 1997”1.

Answer B:

Gifts or payment for a fund is deductible from tax under the “Division 30, ITAA

1997”2.

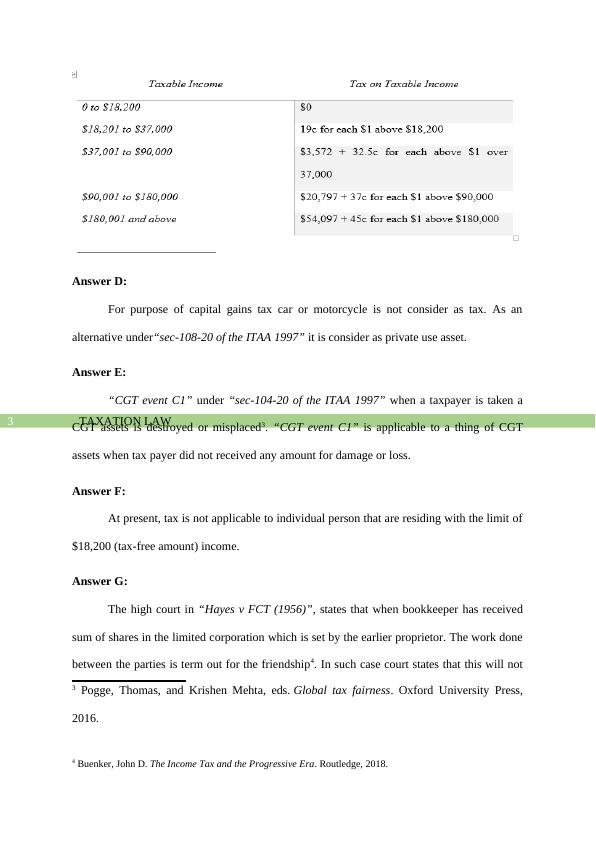

Answer C:

The maximum sum of marginal tax which is consider in Australian Resident Stands

45%.

1 Thuronyi, Victor, and Kim Brooks. Comparative tax law. Kluwer Law International BV,

2016.

2 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

Answer to question 1:

Answer A:

As states in “Taxation Ruling of TR 2009/1” it gives the view of official of tax about

when an organization do the business as per the term of SBE under “Sec-23 of the Income

Tax Rates Act 1986” that are relevant for the year 2015-16 and 2016-17 or within “sec-328-

110, ITAA 1997”1.

Answer B:

Gifts or payment for a fund is deductible from tax under the “Division 30, ITAA

1997”2.

Answer C:

The maximum sum of marginal tax which is consider in Australian Resident Stands

45%.

1 Thuronyi, Victor, and Kim Brooks. Comparative tax law. Kluwer Law International BV,

2016.

2 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

TAXATION LAW3

Answer D:

For purpose of capital gains tax car or motorcycle is not consider as tax. As an

alternative under“sec-108-20 of the ITAA 1997” it is consider as private use asset.

Answer E:

“CGT event C1” under “sec-104-20 of the ITAA 1997” when a taxpayer is taken a

CGT assets is destroyed or misplaced3. “CGT event C1” is applicable to a thing of CGT

assets when tax payer did not received any amount for damage or loss.

Answer F:

At present, tax is not applicable to individual person that are residing with the limit of

$18,200 (tax-free amount) income.

Answer G:

The high court in “Hayes v FCT (1956)”, states that when bookkeeper has received

sum of shares in the limited corporation which is set by the earlier proprietor. The work done

between the parties is term out for the friendship4. In such case court states that this will not

3 Pogge, Thomas, and Krishen Mehta, eds. Global tax fairness. Oxford University Press,

2016.

4 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

Answer D:

For purpose of capital gains tax car or motorcycle is not consider as tax. As an

alternative under“sec-108-20 of the ITAA 1997” it is consider as private use asset.

Answer E:

“CGT event C1” under “sec-104-20 of the ITAA 1997” when a taxpayer is taken a

CGT assets is destroyed or misplaced3. “CGT event C1” is applicable to a thing of CGT

assets when tax payer did not received any amount for damage or loss.

Answer F:

At present, tax is not applicable to individual person that are residing with the limit of

$18,200 (tax-free amount) income.

Answer G:

The high court in “Hayes v FCT (1956)”, states that when bookkeeper has received

sum of shares in the limited corporation which is set by the earlier proprietor. The work done

between the parties is term out for the friendship4. In such case court states that this will not

3 Pogge, Thomas, and Krishen Mehta, eds. Global tax fairness. Oxford University Press,

2016.

4 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation Law of Australialg...

|16

|3895

|77

Taxation Lawlg...

|18

|3675

|50

Taxation Law of Australia: Assignment Summarylg...

|20

|4401

|68

Answer to question 1: Taxation Law Name of the University Authors' Namelg...

|17

|3562

|242

Taxation Lawlg...

|21

|4006

|65

Assignment on Taxation Law - sec 6-5 ITAA 1997lg...

|12

|2873

|27