Capital Gains | Taxation Law | Assignment

VerifiedAdded on 2022/08/31

|6

|1132

|29

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................3

References:.................................................................................................................................5

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................3

References:.................................................................................................................................5

2TAXATION LAW

Answer to Part 1:

According to the explanation given in “sec 108-5 ITAA 1997” CGT asset represent

any form of property or lawful or equal rights that cannot be regarded as property. Important

examples of the CGT asset is the land, building, shares, debts which is owned by an

individual tax payer, right to enter in an agreement and foreign currency (McCluskey and

Franzsen 2017). On identifying the capital gains tax event relating to a specific CGT asset, it

becomes vital to calculate the capital gains or loss which happens from that event. As noted,

“CGT event A1” takes place under “sec 104-10 (1) ITAA 1997” when the sale of CGT asset

happens.

The law court in “FC of T v Sara Lee Household (2002)” held that the time of CGT

event is regarded as important, this comprises of the time when the taxpayer forms a contract

or given there is no contract, then it is important to determine when the change of ownership

happened. In another instance of “McDonald v FC of T (1998)” an oral agreement associated

to the acquisition involves, whether the contract is enforceable or not is to be determined on

the basis of date of purchase (O’Connell 2017). On noticing that the contract is preliminary

and not real contract for purchase, the latter date of contact is recognized.

When the taxpayer sells the CGT asset, the CGT event normally happens when the

taxpayer enters in the contract for selling the asset. Where assets involve the real estate, CGT

event takes place when the taxpayer forms a contract. This involves the date when the

taxpayer enters into the contract and not when the settlement happens (Jones 2016). As per

the ATO, shares which is held by the taxpayer in company or units in trust are taken into

account for determining CGT just like any other asset. A CGT event happens for an investor

when capital gains are made from disposal of share. Most importantly, it is important to

ascertain the time when the CGT event happened since the obligations falls on the taxpayer to

Answer to Part 1:

According to the explanation given in “sec 108-5 ITAA 1997” CGT asset represent

any form of property or lawful or equal rights that cannot be regarded as property. Important

examples of the CGT asset is the land, building, shares, debts which is owned by an

individual tax payer, right to enter in an agreement and foreign currency (McCluskey and

Franzsen 2017). On identifying the capital gains tax event relating to a specific CGT asset, it

becomes vital to calculate the capital gains or loss which happens from that event. As noted,

“CGT event A1” takes place under “sec 104-10 (1) ITAA 1997” when the sale of CGT asset

happens.

The law court in “FC of T v Sara Lee Household (2002)” held that the time of CGT

event is regarded as important, this comprises of the time when the taxpayer forms a contract

or given there is no contract, then it is important to determine when the change of ownership

happened. In another instance of “McDonald v FC of T (1998)” an oral agreement associated

to the acquisition involves, whether the contract is enforceable or not is to be determined on

the basis of date of purchase (O’Connell 2017). On noticing that the contract is preliminary

and not real contract for purchase, the latter date of contact is recognized.

When the taxpayer sells the CGT asset, the CGT event normally happens when the

taxpayer enters in the contract for selling the asset. Where assets involve the real estate, CGT

event takes place when the taxpayer forms a contract. This involves the date when the

taxpayer enters into the contract and not when the settlement happens (Jones 2016). As per

the ATO, shares which is held by the taxpayer in company or units in trust are taken into

account for determining CGT just like any other asset. A CGT event happens for an investor

when capital gains are made from disposal of share. Most importantly, it is important to

ascertain the time when the CGT event happened since the obligations falls on the taxpayer to

3TAXATION LAW

report the capital gains or loss that might affect the position of tax while determining the tax

liability.

Answer to Part 2:

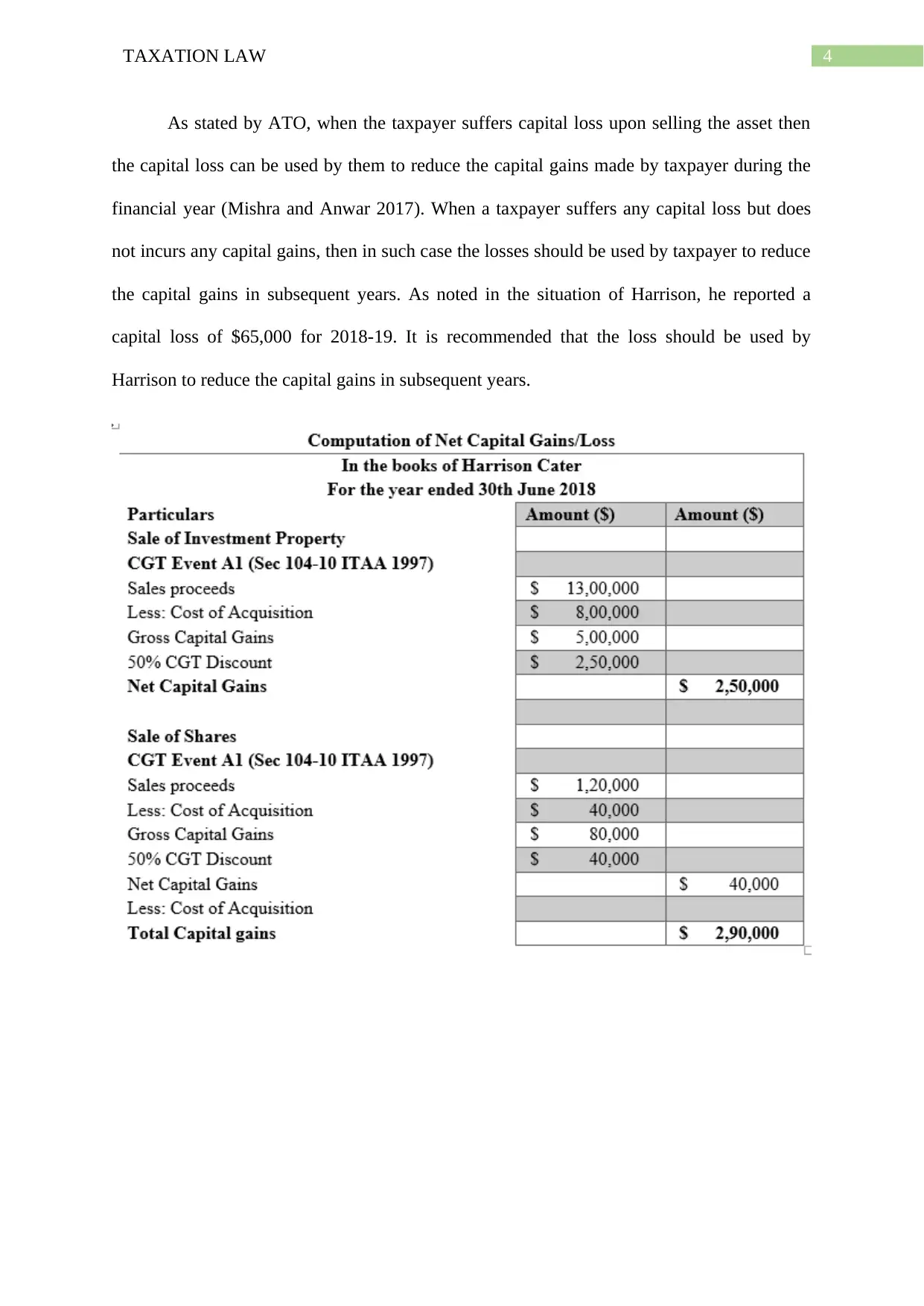

The circumstances obtained from the situation of Harrison suggest that he purchased

an investment property in 2001 at an acquisition cost of $800,000. Referring to “sec 108-5

ITAA 1997” the property will be treated as CGT asset (Freebairn 2016). During the year

2018, Harrison finally disposed the investment property for $1.3 million. The disposal of

investment property has given rise to “CGT event A1” under “sec 104-10 (1)”. Citing the

verdict made in “FC of T v Sara Lee Household (2002)” a “CGT event A1” happened when

Harrison formed a contract of selling the investment property (Bentley 2019). When Harrison

disposed the investment property, a change in ownership occurred. Referring to the “sec 116-

20 ITAA 1997” the amount of $1.3 million was received by Harrison when he sold the

property. The amount received represents the capital proceeds on the basis of market value

for the CGT event. Referring to “sec 102-5 ITAA 1997” the net value of capital gains earned

by Harrison on selling the property will be included in his taxable earnings for tax purpose.

Harrison also reports acquisition of shares in October 1985 by paying a sum of $4 per

share. Harrison ultimately sold the shares at $12 per share on 20th June 2018. As per “sec

108-5 ITAA 1997” the shares must be categorized as CGT asset. As Harrison acquired the

shares in October 1985, the shares will be treated as post-CGT asset and therefore the capital

gains regimes will be applicable (Mishra and Anwar 2017). Harrison entered into the contract

of sale on 20th June 2018. The sale of shares has given rise to “CGT event A1” within “sect

104-10 (1)”. Citing the judgement made in “FC of T v Sara Lee Household (2002)”

Harrison entered into the contract of selling the shares on 20th June, therefore the capital gains

is derived during the year of 2017-18. The time of CGT event is the year when a contract was

entered into by Harrison and not 2018-19 when the settlement happened.

report the capital gains or loss that might affect the position of tax while determining the tax

liability.

Answer to Part 2:

The circumstances obtained from the situation of Harrison suggest that he purchased

an investment property in 2001 at an acquisition cost of $800,000. Referring to “sec 108-5

ITAA 1997” the property will be treated as CGT asset (Freebairn 2016). During the year

2018, Harrison finally disposed the investment property for $1.3 million. The disposal of

investment property has given rise to “CGT event A1” under “sec 104-10 (1)”. Citing the

verdict made in “FC of T v Sara Lee Household (2002)” a “CGT event A1” happened when

Harrison formed a contract of selling the investment property (Bentley 2019). When Harrison

disposed the investment property, a change in ownership occurred. Referring to the “sec 116-

20 ITAA 1997” the amount of $1.3 million was received by Harrison when he sold the

property. The amount received represents the capital proceeds on the basis of market value

for the CGT event. Referring to “sec 102-5 ITAA 1997” the net value of capital gains earned

by Harrison on selling the property will be included in his taxable earnings for tax purpose.

Harrison also reports acquisition of shares in October 1985 by paying a sum of $4 per

share. Harrison ultimately sold the shares at $12 per share on 20th June 2018. As per “sec

108-5 ITAA 1997” the shares must be categorized as CGT asset. As Harrison acquired the

shares in October 1985, the shares will be treated as post-CGT asset and therefore the capital

gains regimes will be applicable (Mishra and Anwar 2017). Harrison entered into the contract

of sale on 20th June 2018. The sale of shares has given rise to “CGT event A1” within “sect

104-10 (1)”. Citing the judgement made in “FC of T v Sara Lee Household (2002)”

Harrison entered into the contract of selling the shares on 20th June, therefore the capital gains

is derived during the year of 2017-18. The time of CGT event is the year when a contract was

entered into by Harrison and not 2018-19 when the settlement happened.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

As stated by ATO, when the taxpayer suffers capital loss upon selling the asset then

the capital loss can be used by them to reduce the capital gains made by taxpayer during the

financial year (Mishra and Anwar 2017). When a taxpayer suffers any capital loss but does

not incurs any capital gains, then in such case the losses should be used by taxpayer to reduce

the capital gains in subsequent years. As noted in the situation of Harrison, he reported a

capital loss of $65,000 for 2018-19. It is recommended that the loss should be used by

Harrison to reduce the capital gains in subsequent years.

As stated by ATO, when the taxpayer suffers capital loss upon selling the asset then

the capital loss can be used by them to reduce the capital gains made by taxpayer during the

financial year (Mishra and Anwar 2017). When a taxpayer suffers any capital loss but does

not incurs any capital gains, then in such case the losses should be used by taxpayer to reduce

the capital gains in subsequent years. As noted in the situation of Harrison, he reported a

capital loss of $65,000 for 2018-19. It is recommended that the loss should be used by

Harrison to reduce the capital gains in subsequent years.

5TAXATION LAW

References:

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in Australia, 51(2),

p.67.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Mishra, A.V. and Anwar, S., 2017. Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54-68.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

References:

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in Australia, 51(2),

p.67.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Mishra, A.V. and Anwar, S., 2017. Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54-68.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.