Taxation Theory, Practice and Law: Capital Gains and FBT Analysis

VerifiedAdded on 2023/06/07

|11

|2113

|313

Homework Assignment

AI Summary

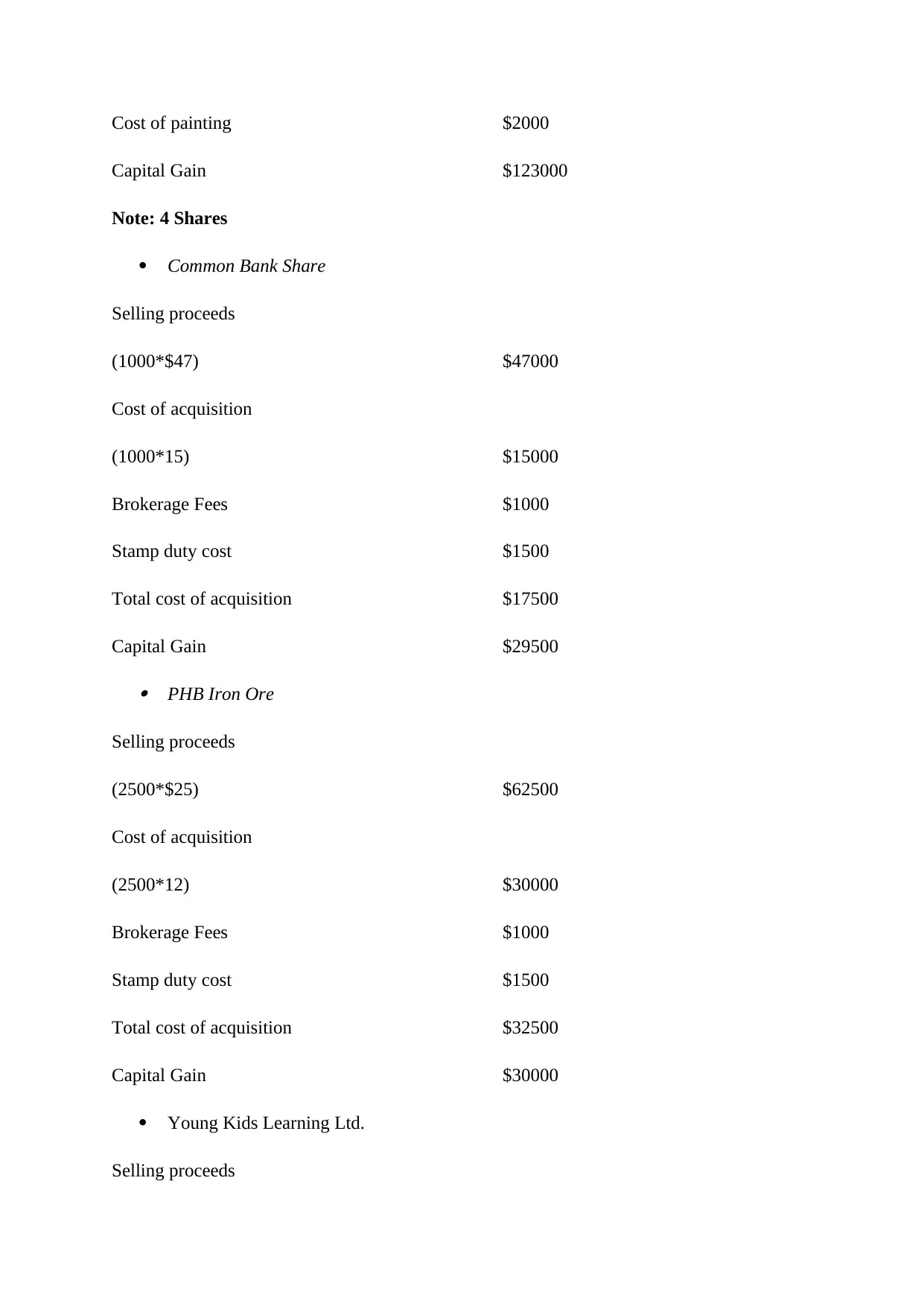

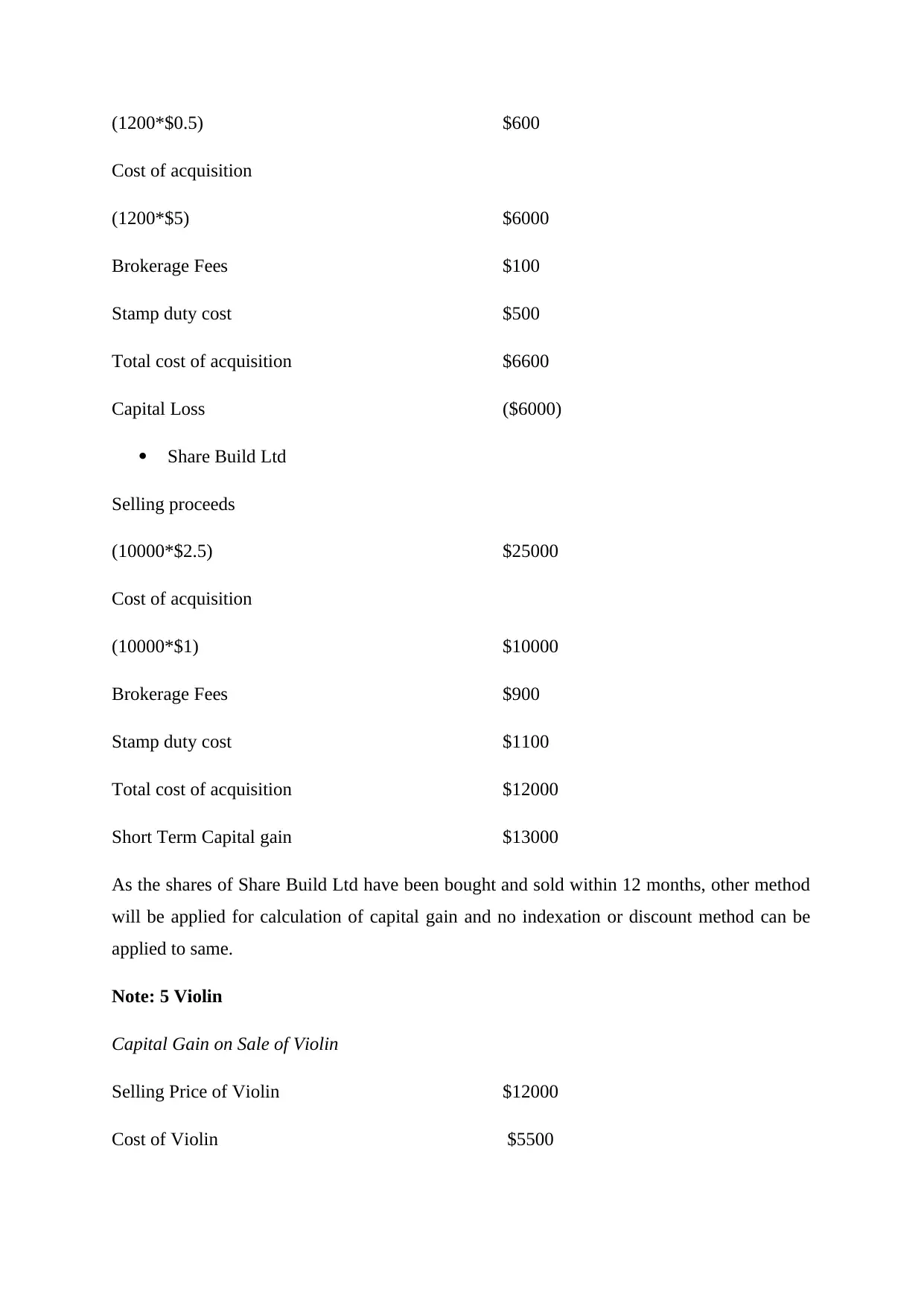

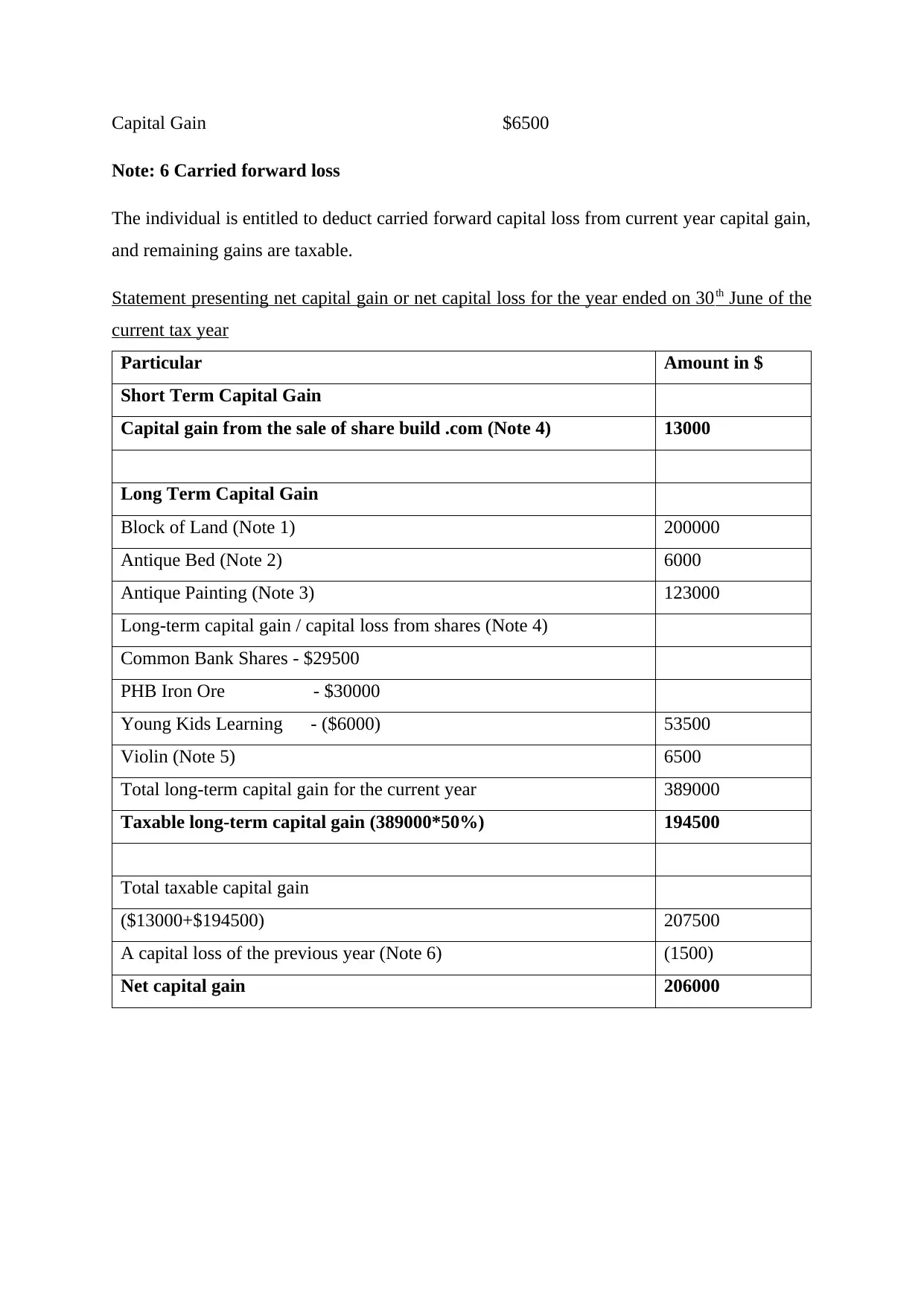

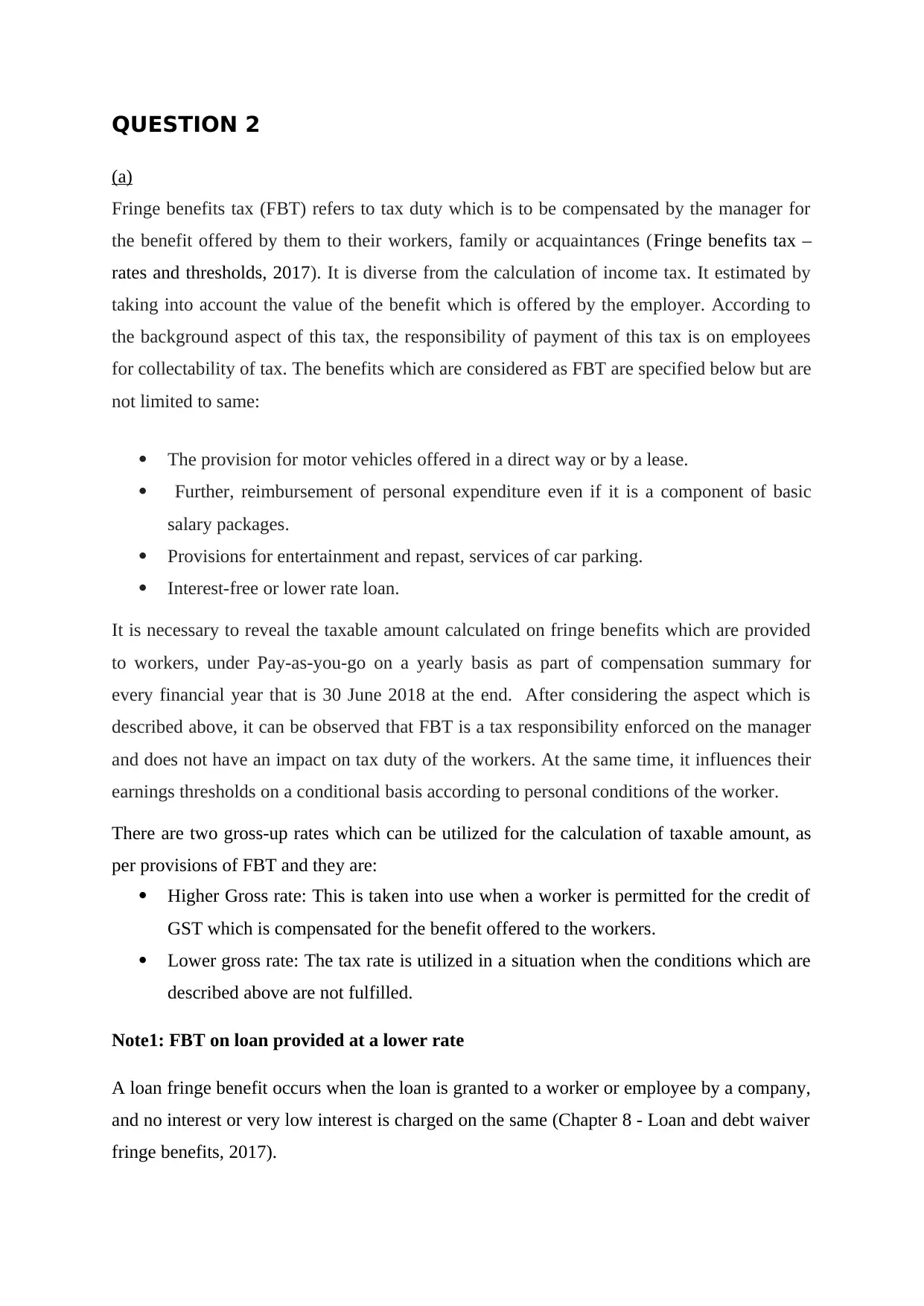

This assignment analyzes taxation principles, focusing on capital gains tax (CGT) and fringe benefits tax (FBT). It begins by outlining CGT provisions according to ITAA97, detailing how capital gains and losses are calculated, and providing examples for various assets including land, antiques, paintings, and shares. The assignment then presents a statement of net capital gain or loss for the tax year. The second part of the assignment addresses FBT, explaining its application and calculation for different scenarios, such as loans, cars, and electric heaters. It details the calculation of FBT on loans, considering benchmark interest rates, and on car fringe benefits using the statutory formula. The assignment concludes with a statement of total taxable FBT, providing a comprehensive overview of tax liabilities and calculations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.