Capital Budgeting Analysis for Curtis Industries Ltd.

VerifiedAdded on 2020/05/16

|12

|1693

|204

AI Summary

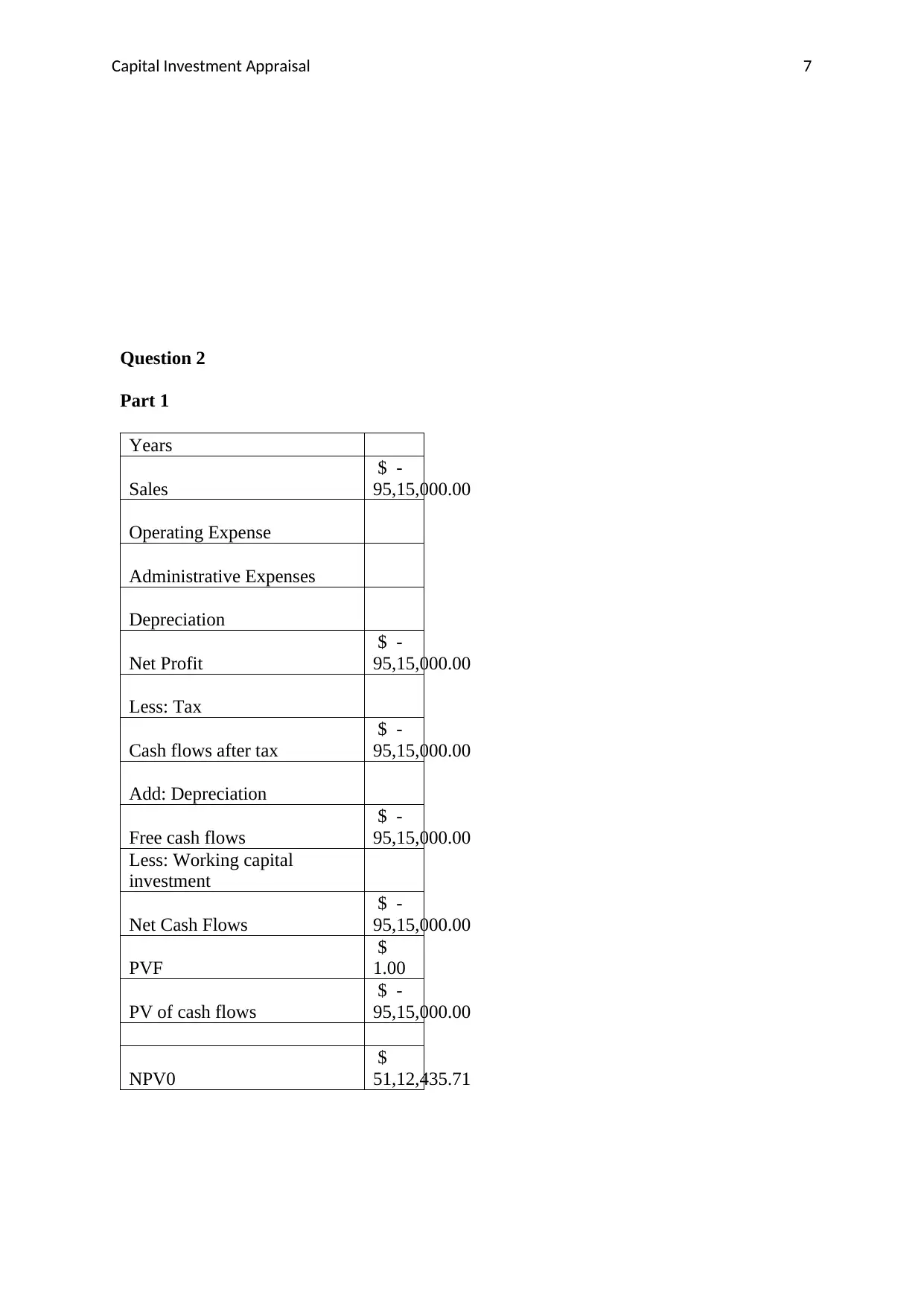

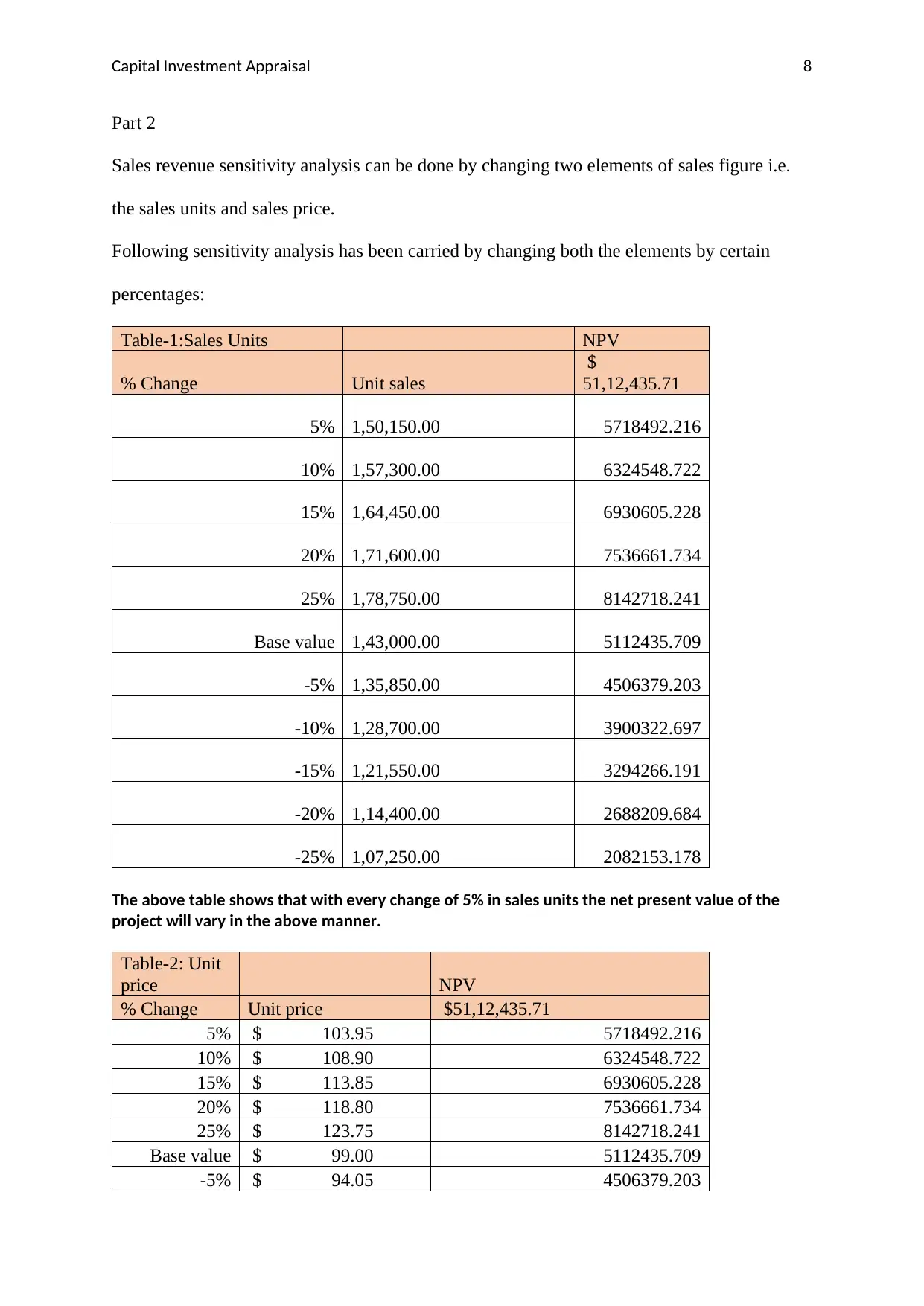

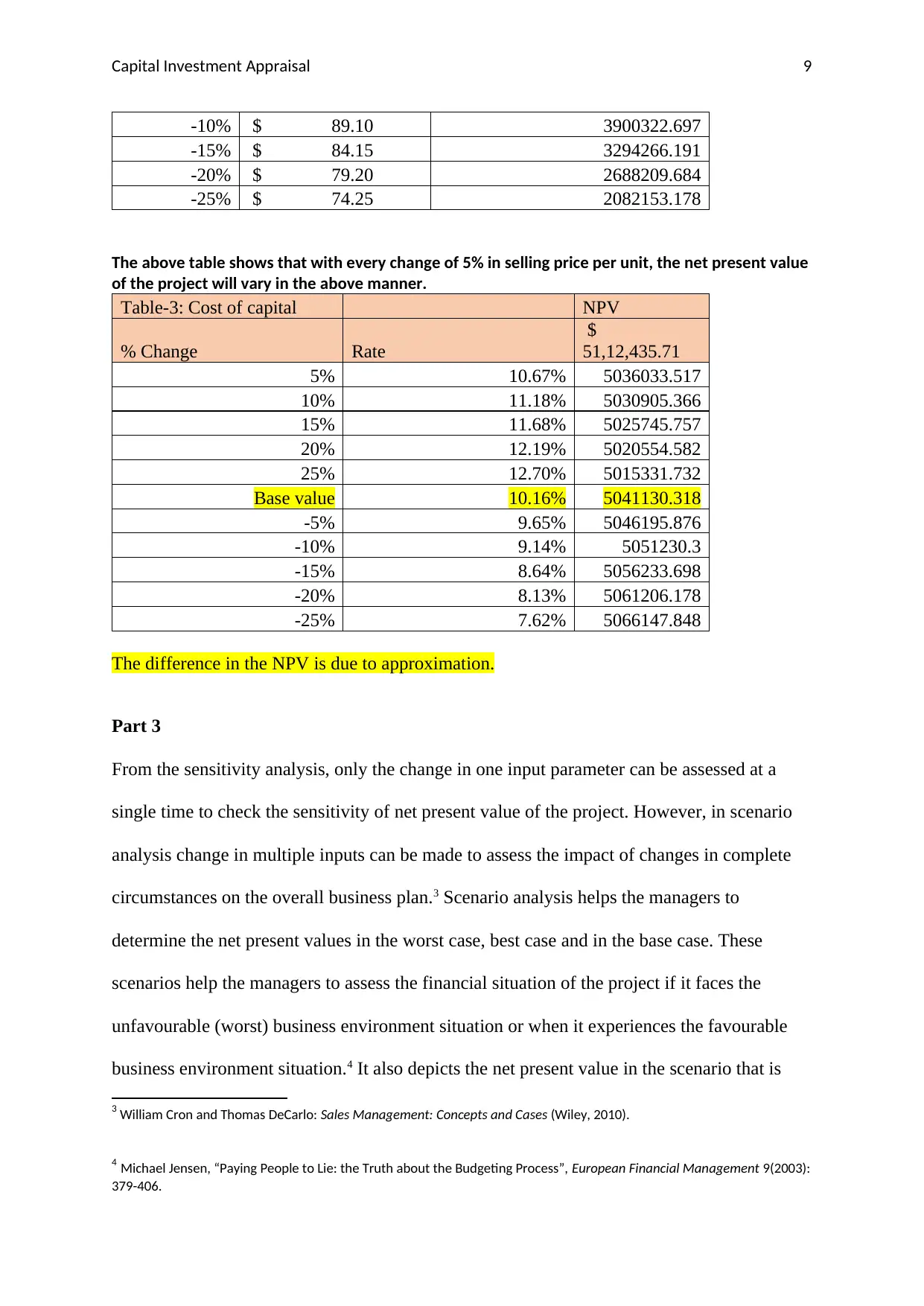

The document presents a comprehensive capital budgeting analysis for Curtis Industries Ltd., detailing cash flows from 2016 to 2020. The net present value (NPV) calculation, using a cost of capital of 10.16%, yields a positive NPV of $5,122,435, indicating project viability. Sensitivity analysis is employed to evaluate how changes in sales volume and selling price per unit affect the NPV, highlighting potential risks. Scenario analysis further assesses best, worst, and base case scenarios, providing insights into financial outcomes under varying conditions. The overall positive NPV suggests that projected cash inflows surpass outflows, aligning with acceptable risk levels for investment.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.