Accounting for Business: Capital Investment Appraisal and IRR

VerifiedAdded on 2023/06/13

|6

|1368

|266

Report

AI Summary

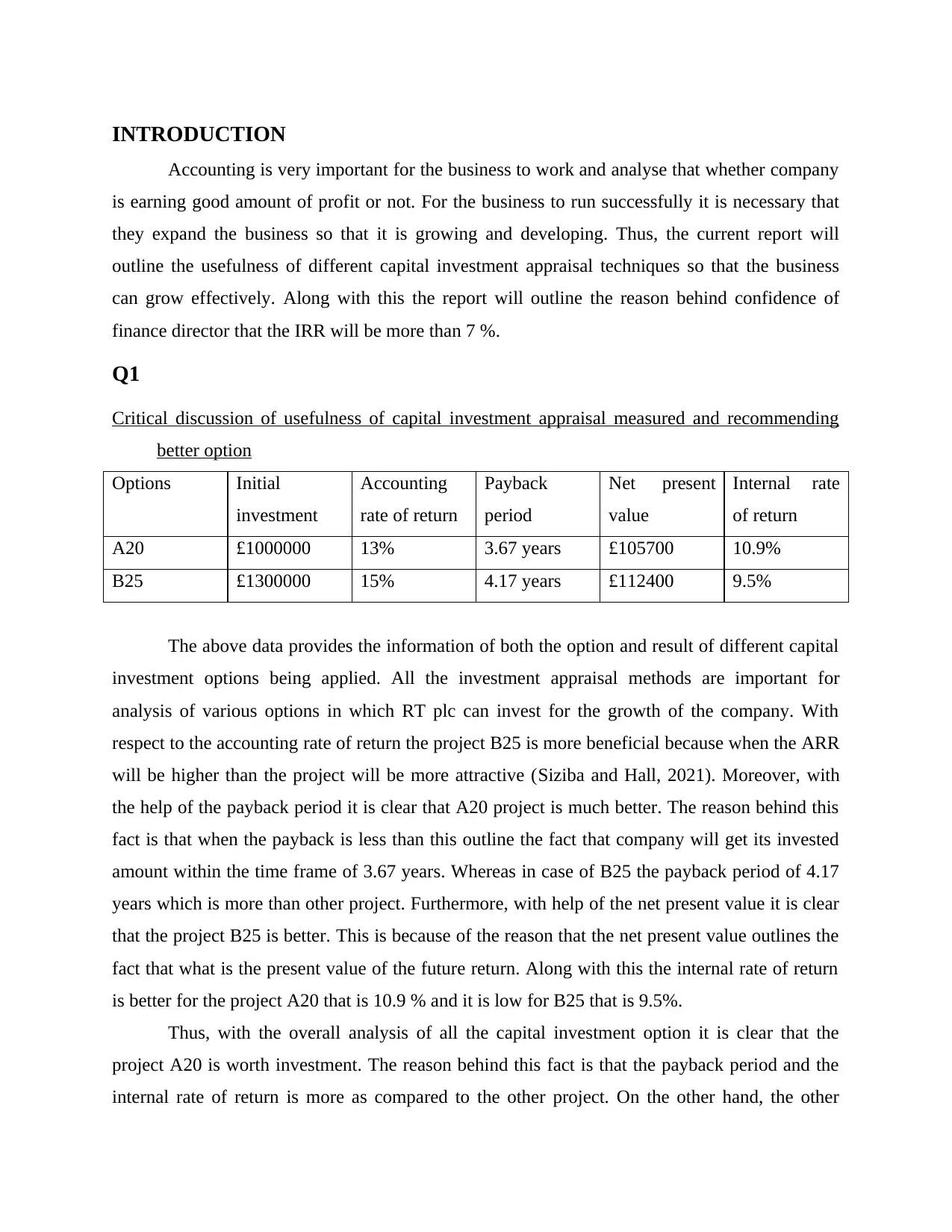

This report critically evaluates capital investment appraisal methods, focusing on their usefulness in business accounting. It analyzes different investment options for RT plc using metrics like accounting rate of return, payback period, net present value, and internal rate of return (IRR). The report recommends investment in option A20 based on its favorable payback period and IRR. It also explains the finance director's confidence in IRR exceeding 7%, linking it to the cost of capital. The discussion emphasizes the importance of these appraisal methods in making informed investment decisions and highlights the benefits and drawbacks of each approach. The report concludes that understanding and applying these accounting principles are crucial for business growth and profitability. Desklib provides additional solved assignments and resources for students studying finance and accounting.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.