Capital Investment Decision - Techniques, Merits, Demerits and Evaluation Methods

VerifiedAdded on 2023/06/03

|17

|3309

|334

AI Summary

The report covers the different aspects of capital investment technique its uses, merits and demerits. The report is designed to suggest Ang Thong Pty Ltd to avail the best option among the four for its investment and appraisal return from the investment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CAPITAL INVESTMENT DECISION

Capital Investment Decision

Name of the Student:

Name of the University:

Author Note:

Capital Investment Decision

Name of the Student:

Name of the University:

Author Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CAPITAL INVESTMENT DECISION

Executive Summary:

The report is formed to give a depth overview about the capital investment decision. The report

covers the different aspects of capital investment technique its uses, merits and demerits. Even

the best out result of the investment through using the technique on various options available for

investment is evaluated. The report is designed to suggest Ang Thong Pty Ltd to avail the best

option among the four for its investment and appraisal return from the investment.

Executive Summary:

The report is formed to give a depth overview about the capital investment decision. The report

covers the different aspects of capital investment technique its uses, merits and demerits. Even

the best out result of the investment through using the technique on various options available for

investment is evaluated. The report is designed to suggest Ang Thong Pty Ltd to avail the best

option among the four for its investment and appraisal return from the investment.

2CAPITAL INVESTMENT DECISION

Introduction:

Investment decision is based on rule where that decision is implemented upon certain

applicable situations. The base of the rule depends upon the three elements that is Cash flows,

life of the project and discounting factor. The decision is how much effective is relied upon the

assessment of these elements. In depth, understanding of the project is the basic requirement of

the project for estimating the cash flows specifically in macro and micro view of the economy.

Foremost thing is project life to be closely assessed before making an investment decision. Long

term investment decision is quite crucial because of some cause. The role of key management of

the entity is involved in the decision making in respect to the investments for long term. The key

feature for taking long term decision for investment are

Risk and uncertainty involved,

Longevity of time that is 5 years or more than 5 years,

Large amount of resources,

Initial investment involved a higher cash investment and the return of the initial investment is

identified over the period

Risk of reserve without losing of substantial capitals.

Introduction:

Investment decision is based on rule where that decision is implemented upon certain

applicable situations. The base of the rule depends upon the three elements that is Cash flows,

life of the project and discounting factor. The decision is how much effective is relied upon the

assessment of these elements. In depth, understanding of the project is the basic requirement of

the project for estimating the cash flows specifically in macro and micro view of the economy.

Foremost thing is project life to be closely assessed before making an investment decision. Long

term investment decision is quite crucial because of some cause. The role of key management of

the entity is involved in the decision making in respect to the investments for long term. The key

feature for taking long term decision for investment are

Risk and uncertainty involved,

Longevity of time that is 5 years or more than 5 years,

Large amount of resources,

Initial investment involved a higher cash investment and the return of the initial investment is

identified over the period

Risk of reserve without losing of substantial capitals.

3CAPITAL INVESTMENT DECISION

Discussion

Capital investment choice are important at two levels one is for the upcoming operability

of the company building the investment and for the economy of a country as a whole. Direction

of vital resources towards specific area of economic action. So all together, the economic

position of a county in a near future is being impacted by the capital investment decision of an

individual company. At an entity stage, the commitment of resources to long-term capital assets

has inferences for many phases of processes. Concern involved in capital investment is about the

purchase and change of plant and machinery so that the range, cost, innovation, quality and

leadership of the products are all pretentious by Capital Investment decision. (Baños-Caballero,

García-Teruel and Martínez-Solano 2014).

Capital investment generally involves:

Existing asset needed to be replaced.

Requirement of expansion of the existing assets.

Marketing or manufacturing of production technologies.

Non-monetary motivated expenditures.

Capital investment is done through a process that is involved in the decision-making. The

process is involved in the certain steps as identifying the potentiality of investment,

defining and screening of project, evaluating and accepting the project, implementing the

findings of the project. (DAILY, KIEFF and WILMARTH JR 2014).

Relevant Information for Capital Investment Decision Making

The information that helps in changing the decision for capital investment is consider to

be relevant for assessing the feasibility of that investment. That is, principal investment decision

Discussion

Capital investment choice are important at two levels one is for the upcoming operability

of the company building the investment and for the economy of a country as a whole. Direction

of vital resources towards specific area of economic action. So all together, the economic

position of a county in a near future is being impacted by the capital investment decision of an

individual company. At an entity stage, the commitment of resources to long-term capital assets

has inferences for many phases of processes. Concern involved in capital investment is about the

purchase and change of plant and machinery so that the range, cost, innovation, quality and

leadership of the products are all pretentious by Capital Investment decision. (Baños-Caballero,

García-Teruel and Martínez-Solano 2014).

Capital investment generally involves:

Existing asset needed to be replaced.

Requirement of expansion of the existing assets.

Marketing or manufacturing of production technologies.

Non-monetary motivated expenditures.

Capital investment is done through a process that is involved in the decision-making. The

process is involved in the certain steps as identifying the potentiality of investment,

defining and screening of project, evaluating and accepting the project, implementing the

findings of the project. (DAILY, KIEFF and WILMARTH JR 2014).

Relevant Information for Capital Investment Decision Making

The information that helps in changing the decision for capital investment is consider to

be relevant for assessing the feasibility of that investment. That is, principal investment decision

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CAPITAL INVESTMENT DECISION

taker must recognize relationships between either the assessments made, costs or reimbursements

that accrue from it instantaneously or in the upcoming time. Common examples of the

information is cost of installation and purchase of capital asset, requirement of increased working

capital and changes in charges or proceeds.

Financial Analysis of Capital Investments Options

Financial analysis is the foremost thing to be done before investing capital in several

options. There are certain views to measure the performance of investment and they are

considered as the technique of concluding the decision of investing at which options. The

techniques are either termed as monetary or economy concepts or accounting concepts. These

technique are named as traditional method.

In term of accounting concept if the options are relevant for long-term investment success

is measured at profitability. For this computation of profitability index can help in decision-

making. If the options are chosen for short-term investment decision-making should be based on

the liquidity terms of the investment. Where as in economic terms it is seen that fiscal

achievement is concerned based on maximization of stockholders wealth as well as considering

the risk. Capital investment decision is effected by allocating resources. As, it follows that the

success available options of capital investment are those that increases the worth of the company.

If this is considered as the base of decision-making then those options are accepted for capital

investment whose predictable cash returns outstrips its predictable cash outlays, to decrease the

importance of liquidity and profitability of such investments.

The grouping of assumed wealth expansion objectives a risk considered has led to the

progress of capital investment evaluation methods are quite dissimilar in comparison to the

taker must recognize relationships between either the assessments made, costs or reimbursements

that accrue from it instantaneously or in the upcoming time. Common examples of the

information is cost of installation and purchase of capital asset, requirement of increased working

capital and changes in charges or proceeds.

Financial Analysis of Capital Investments Options

Financial analysis is the foremost thing to be done before investing capital in several

options. There are certain views to measure the performance of investment and they are

considered as the technique of concluding the decision of investing at which options. The

techniques are either termed as monetary or economy concepts or accounting concepts. These

technique are named as traditional method.

In term of accounting concept if the options are relevant for long-term investment success

is measured at profitability. For this computation of profitability index can help in decision-

making. If the options are chosen for short-term investment decision-making should be based on

the liquidity terms of the investment. Where as in economic terms it is seen that fiscal

achievement is concerned based on maximization of stockholders wealth as well as considering

the risk. Capital investment decision is effected by allocating resources. As, it follows that the

success available options of capital investment are those that increases the worth of the company.

If this is considered as the base of decision-making then those options are accepted for capital

investment whose predictable cash returns outstrips its predictable cash outlays, to decrease the

importance of liquidity and profitability of such investments.

The grouping of assumed wealth expansion objectives a risk considered has led to the

progress of capital investment evaluation methods are quite dissimilar in comparison to the

5CAPITAL INVESTMENT DECISION

traditional method. Those methods are net present value, internal rate of return, profitability

index and discounted payback period.

Different Methodologies of Capital Investment

The methodologies have been divided into two groups:

Investment method under certainty

Investment method under Uncertainty

Investment Method under certainty:

This is also divided into groups

Pay Back Period (PBP)

Accounting Rate of Return (ARR)

Investment Method under Uncertainty

Net Present Value (NPV)

Internal Rate of Return (IRR)

Profitability Index (PI)

The above-mentioned methods are discussed below:

Pay Back Period

The payback period (PBP) is the outmoded manner of capital investment. It is the

modest and conceivably, the utmost extensively used measureable method for assessing capital

costs decision. (Graham, Harvey and Puri 2015).

traditional method. Those methods are net present value, internal rate of return, profitability

index and discounted payback period.

Different Methodologies of Capital Investment

The methodologies have been divided into two groups:

Investment method under certainty

Investment method under Uncertainty

Investment Method under certainty:

This is also divided into groups

Pay Back Period (PBP)

Accounting Rate of Return (ARR)

Investment Method under Uncertainty

Net Present Value (NPV)

Internal Rate of Return (IRR)

Profitability Index (PI)

The above-mentioned methods are discussed below:

Pay Back Period

The payback period (PBP) is the outmoded manner of capital investment. It is the

modest and conceivably, the utmost extensively used measureable method for assessing capital

costs decision. (Graham, Harvey and Puri 2015).

6CAPITAL INVESTMENT DECISION

Decision Rule:

Pay Back Period less than the maximum acceptable payback period = Accept.

Pay Back Period greater than the maximum acceptable payback period = Reject.

This method is used to do the comparison between the actual and standard payback

period that is decided by the management of the company to recover the initial investment. This

method is also used to rank the project. Ranking is done according to the duration of payback

period.

Merits

It is cost effective.

Helps in dealing with the risk.

Selection of the option available for early recovery of the investment.

Demerits

In this method time value of money is not considered.

Cash flow beyond the PBP is ignored for a reason the sustainability inflows of the

projected is rejected.

Recovery of the invested amount is measured not profitability. This is the sole reason

that this method is not used in the concluding the decision of accepting or rejecting

the project.

It is an idiosyncratic decision as no logic base of concluding the decision for the

options.

Decision Rule:

Pay Back Period less than the maximum acceptable payback period = Accept.

Pay Back Period greater than the maximum acceptable payback period = Reject.

This method is used to do the comparison between the actual and standard payback

period that is decided by the management of the company to recover the initial investment. This

method is also used to rank the project. Ranking is done according to the duration of payback

period.

Merits

It is cost effective.

Helps in dealing with the risk.

Selection of the option available for early recovery of the investment.

Demerits

In this method time value of money is not considered.

Cash flow beyond the PBP is ignored for a reason the sustainability inflows of the

projected is rejected.

Recovery of the invested amount is measured not profitability. This is the sole reason

that this method is not used in the concluding the decision of accepting or rejecting

the project.

It is an idiosyncratic decision as no logic base of concluding the decision for the

options.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CAPITAL INVESTMENT DECISION

Uses:

The PB method might be valuable for the firms going from a liquidity crunch.

It is very beneficial for those firms that accentuates on petite run receiving recital

rather than its long-term evolution.

The communal of PBP is a decent guesstimate of IRR that else requires

experimental and blunder method.

Accounting Rate of Return (ARR)

The other name of this method is return on investment and capital employed (ROI,

ROCE).

Decision Rule:

For selecting the investment proposal ARR can be used.

ARR higher than the minimum rate= Accept

ARR less than the minimum rate = Reject

Merits:

It is constructed on accounting information that is willingly accessible and acquainted to

business man.

It contemplates advantage over whole life of the options.

Demerits:

Time value is not taken into consideration so the advantages cannot be valued at par both

in earlier as well as later years.

Uses:

The PB method might be valuable for the firms going from a liquidity crunch.

It is very beneficial for those firms that accentuates on petite run receiving recital

rather than its long-term evolution.

The communal of PBP is a decent guesstimate of IRR that else requires

experimental and blunder method.

Accounting Rate of Return (ARR)

The other name of this method is return on investment and capital employed (ROI,

ROCE).

Decision Rule:

For selecting the investment proposal ARR can be used.

ARR higher than the minimum rate= Accept

ARR less than the minimum rate = Reject

Merits:

It is constructed on accounting information that is willingly accessible and acquainted to

business man.

It contemplates advantage over whole life of the options.

Demerits:

Time value is not taken into consideration so the advantages cannot be valued at par both

in earlier as well as later years.

8CAPITAL INVESTMENT DECISION

Use:

The ARR can be improved and used as recital appraisal quantity and switch devise but it is not

desirable to use as a verdict making condition for capital disbursements of the firm, as it is not

using cash flow data.

Discounted Cash Flow Criteria:

Net Present Value (NPV):

The Net Present Value is an individual of the cut-rate cash flow before period-

accustomed practice. It distinguishes that cash flow rivulets at unlike time old-fashioned varies in

worth and can be calculated single when they are uttered in rapports of communal denominator

that is present value.

Decision Rule:

If the

NPV is greater than 0= accept

NPV is less than zero= reject.

This method is used in selecting the options where mutually exclusive projects are available for

investment. The firm’s market value rises up if the available option with positive NPV is

accepted for investing. (Hartman and Schafrick 2014).

Merits:

It clearly identifies the time value of money.

Takings into justification all the years cash flows rising out of the project concluded its

convenient life.

Use:

The ARR can be improved and used as recital appraisal quantity and switch devise but it is not

desirable to use as a verdict making condition for capital disbursements of the firm, as it is not

using cash flow data.

Discounted Cash Flow Criteria:

Net Present Value (NPV):

The Net Present Value is an individual of the cut-rate cash flow before period-

accustomed practice. It distinguishes that cash flow rivulets at unlike time old-fashioned varies in

worth and can be calculated single when they are uttered in rapports of communal denominator

that is present value.

Decision Rule:

If the

NPV is greater than 0= accept

NPV is less than zero= reject.

This method is used in selecting the options where mutually exclusive projects are available for

investment. The firm’s market value rises up if the available option with positive NPV is

accepted for investing. (Hartman and Schafrick 2014).

Merits:

It clearly identifies the time value of money.

Takings into justification all the years cash flows rising out of the project concluded its

convenient life.

9CAPITAL INVESTMENT DECISION

It is a complete degree of productivity.

It is continuously reliable through the firm’s objective of stockholders treasure growth.

Demerits:

This technique involves assessment of cash flows that is very grim owing to suspicions

existing in corporate creation owing to so many uncontainable ecological influences.

When schemes under deliberation are equally special, it may not elasticity accountable

results if the schemes are having unacceptable lives, dissimilar cash flow outline, unlike

cash expenditure.

It does not clearly deal with indecision when appreciating the project and the degree of

organization’s suppleness toward reply to doubt over the lifetime of the scheme.

Uses:

NPV is very considerable in capital investment decision practice actuality a true effectiveness

degree.

Profitability Index (PI):

Profitability Index processes the present value of revenues per rupee capitalized. It is

observed in inadequacy of NPV that, actuality a complete measure; it is not a dependable method

to gauge schemes necessitating unlike early investments. It is a qualified measure and can be

distinct as the ratio that is attained by dividing the present value of upcoming cash inflows by the

present value of cash expenditures.

Decision Rule:

Accept the project when PI>1

It is a complete degree of productivity.

It is continuously reliable through the firm’s objective of stockholders treasure growth.

Demerits:

This technique involves assessment of cash flows that is very grim owing to suspicions

existing in corporate creation owing to so many uncontainable ecological influences.

When schemes under deliberation are equally special, it may not elasticity accountable

results if the schemes are having unacceptable lives, dissimilar cash flow outline, unlike

cash expenditure.

It does not clearly deal with indecision when appreciating the project and the degree of

organization’s suppleness toward reply to doubt over the lifetime of the scheme.

Uses:

NPV is very considerable in capital investment decision practice actuality a true effectiveness

degree.

Profitability Index (PI):

Profitability Index processes the present value of revenues per rupee capitalized. It is

observed in inadequacy of NPV that, actuality a complete measure; it is not a dependable method

to gauge schemes necessitating unlike early investments. It is a qualified measure and can be

distinct as the ratio that is attained by dividing the present value of upcoming cash inflows by the

present value of cash expenditures.

Decision Rule:

Accept the project when PI>1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CAPITAL INVESTMENT DECISION

Reject the project when PI<1

May or may not accept when PI=1 , the firm is indifferent to the project.

Merits:

PI contemplates the time value of money and entire cash flows created by the scheme.

It is reliable with the stockholders’ prosperity expansion.

Demerits:

When cash outflow ensues beyond the existing period, the PI is inappropriate as a

collection standard.

It necessitates approximation of cash flows with accuracy that is very tough under ever

altering sphere. (Ivanets 2017).

Use:

It is beneficial in appraising capital disbursements schemes being a comparative amount.

Internal Rate of Return (IRR):

The internal rate of return (IRR) is the reduction rate that compares the NPV of an

investment chance with Rs.0 since the present value of cash inflows contemporaries the initial

investment. It is the multifaceted annual rate of return that the firm will receive if it devotes in

the scheme and accepts the given cash inflows. (Islam, Xayavong, and Kingwell 2014).

Decision Rule:

If the

IRR is greater than the cost of capital= accept the scheme.

Reject the project when PI<1

May or may not accept when PI=1 , the firm is indifferent to the project.

Merits:

PI contemplates the time value of money and entire cash flows created by the scheme.

It is reliable with the stockholders’ prosperity expansion.

Demerits:

When cash outflow ensues beyond the existing period, the PI is inappropriate as a

collection standard.

It necessitates approximation of cash flows with accuracy that is very tough under ever

altering sphere. (Ivanets 2017).

Use:

It is beneficial in appraising capital disbursements schemes being a comparative amount.

Internal Rate of Return (IRR):

The internal rate of return (IRR) is the reduction rate that compares the NPV of an

investment chance with Rs.0 since the present value of cash inflows contemporaries the initial

investment. It is the multifaceted annual rate of return that the firm will receive if it devotes in

the scheme and accepts the given cash inflows. (Islam, Xayavong, and Kingwell 2014).

Decision Rule:

If the

IRR is greater than the cost of capital= accept the scheme.

11CAPITAL INVESTMENT DECISION

IRR is less than the cost of capital=reject the scheme.

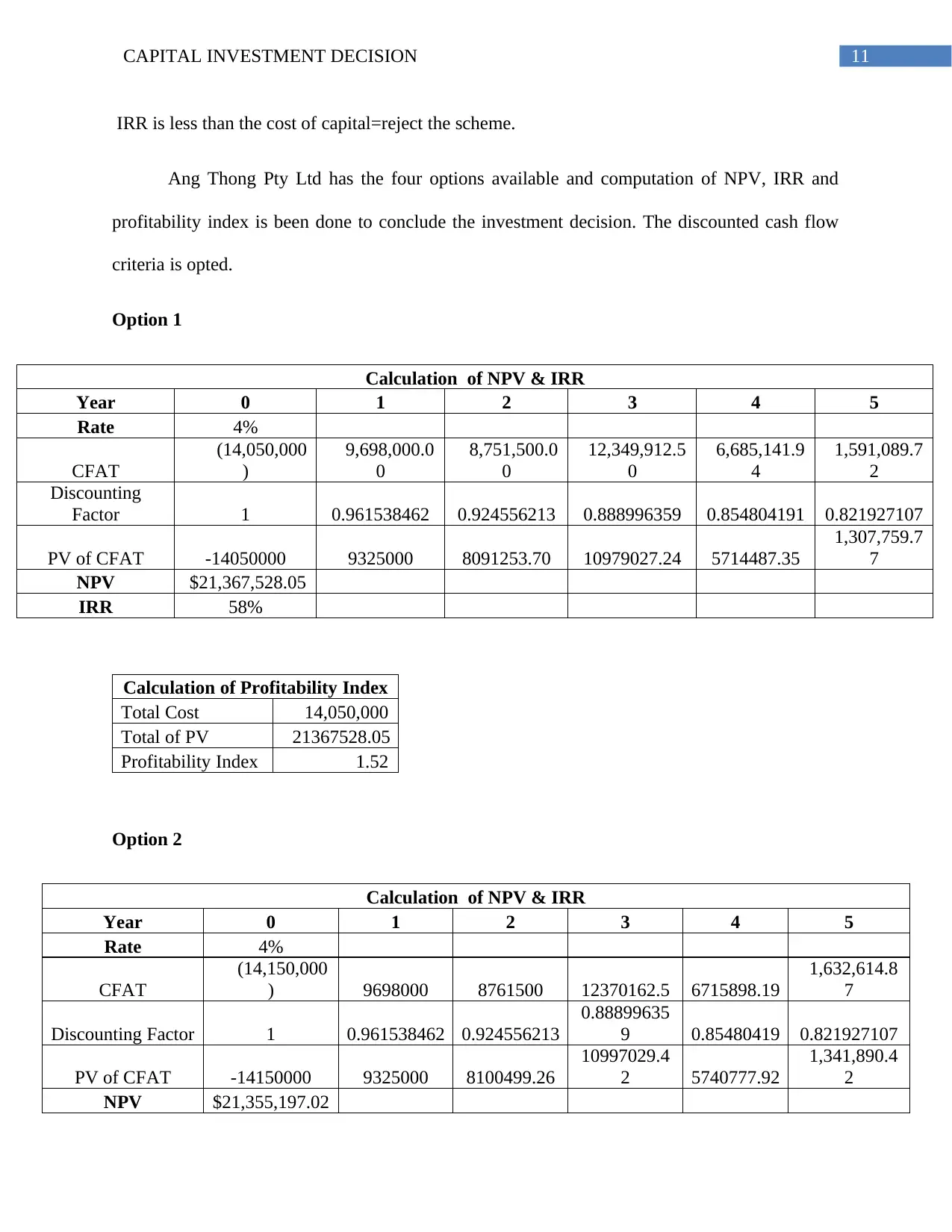

Ang Thong Pty Ltd has the four options available and computation of NPV, IRR and

profitability index is been done to conclude the investment decision. The discounted cash flow

criteria is opted.

Option 1

Calculation of NPV & IRR

Year 0 1 2 3 4 5

Rate 4%

CFAT

(14,050,000

)

9,698,000.0

0

8,751,500.0

0

12,349,912.5

0

6,685,141.9

4

1,591,089.7

2

Discounting

Factor 1 0.961538462 0.924556213 0.888996359 0.854804191 0.821927107

PV of CFAT -14050000 9325000 8091253.70 10979027.24 5714487.35

1,307,759.7

7

NPV $21,367,528.05

IRR 58%

Calculation of Profitability Index

Total Cost 14,050,000

Total of PV 21367528.05

Profitability Index 1.52

Option 2

Calculation of NPV & IRR

Year 0 1 2 3 4 5

Rate 4%

CFAT

(14,150,000

) 9698000 8761500 12370162.5 6715898.19

1,632,614.8

7

Discounting Factor 1 0.961538462 0.924556213

0.88899635

9 0.85480419 0.821927107

PV of CFAT -14150000 9325000 8100499.26

10997029.4

2 5740777.92

1,341,890.4

2

NPV $21,355,197.02

IRR is less than the cost of capital=reject the scheme.

Ang Thong Pty Ltd has the four options available and computation of NPV, IRR and

profitability index is been done to conclude the investment decision. The discounted cash flow

criteria is opted.

Option 1

Calculation of NPV & IRR

Year 0 1 2 3 4 5

Rate 4%

CFAT

(14,050,000

)

9,698,000.0

0

8,751,500.0

0

12,349,912.5

0

6,685,141.9

4

1,591,089.7

2

Discounting

Factor 1 0.961538462 0.924556213 0.888996359 0.854804191 0.821927107

PV of CFAT -14050000 9325000 8091253.70 10979027.24 5714487.35

1,307,759.7

7

NPV $21,367,528.05

IRR 58%

Calculation of Profitability Index

Total Cost 14,050,000

Total of PV 21367528.05

Profitability Index 1.52

Option 2

Calculation of NPV & IRR

Year 0 1 2 3 4 5

Rate 4%

CFAT

(14,150,000

) 9698000 8761500 12370162.5 6715898.19

1,632,614.8

7

Discounting Factor 1 0.961538462 0.924556213

0.88899635

9 0.85480419 0.821927107

PV of CFAT -14150000 9325000 8100499.26

10997029.4

2 5740777.92

1,341,890.4

2

NPV $21,355,197.02

12CAPITAL INVESTMENT DECISION

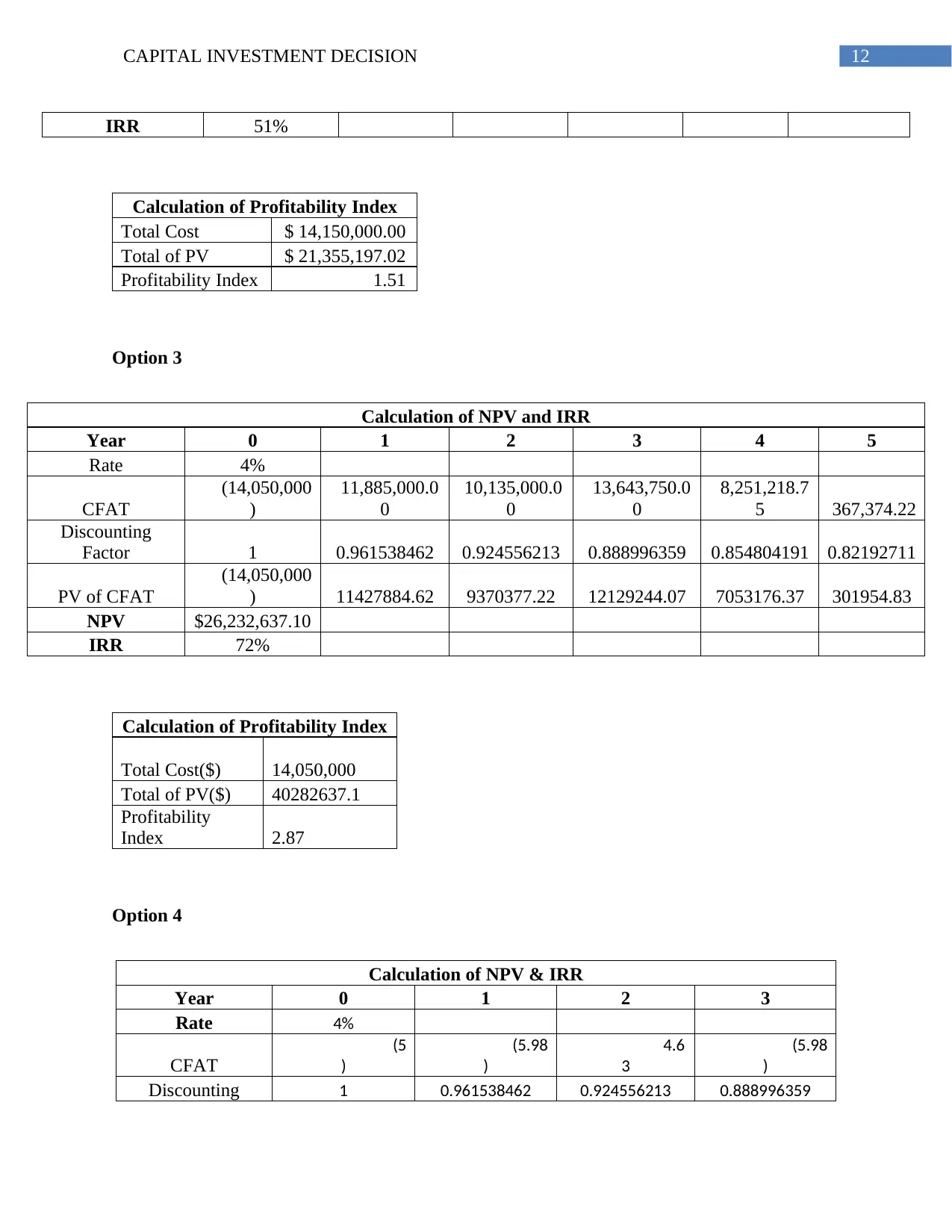

IRR 51%

Calculation of Profitability Index

Total Cost $ 14,150,000.00

Total of PV $ 21,355,197.02

Profitability Index 1.51

Option 3

Calculation of NPV and IRR

Year 0 1 2 3 4 5

Rate 4%

CFAT

(14,050,000

)

11,885,000.0

0

10,135,000.0

0

13,643,750.0

0

8,251,218.7

5 367,374.22

Discounting

Factor 1 0.961538462 0.924556213 0.888996359 0.854804191 0.82192711

PV of CFAT

(14,050,000

) 11427884.62 9370377.22 12129244.07 7053176.37 301954.83

NPV $26,232,637.10

IRR 72%

Calculation of Profitability Index

Total Cost($) 14,050,000

Total of PV($) 40282637.1

Profitability

Index 2.87

Option 4

Calculation of NPV & IRR

Year 0 1 2 3

Rate 4%

CFAT

(5

)

(5.98

)

4.6

3

(5.98

)

Discounting 1 0.961538462 0.924556213 0.888996359

IRR 51%

Calculation of Profitability Index

Total Cost $ 14,150,000.00

Total of PV $ 21,355,197.02

Profitability Index 1.51

Option 3

Calculation of NPV and IRR

Year 0 1 2 3 4 5

Rate 4%

CFAT

(14,050,000

)

11,885,000.0

0

10,135,000.0

0

13,643,750.0

0

8,251,218.7

5 367,374.22

Discounting

Factor 1 0.961538462 0.924556213 0.888996359 0.854804191 0.82192711

PV of CFAT

(14,050,000

) 11427884.62 9370377.22 12129244.07 7053176.37 301954.83

NPV $26,232,637.10

IRR 72%

Calculation of Profitability Index

Total Cost($) 14,050,000

Total of PV($) 40282637.1

Profitability

Index 2.87

Option 4

Calculation of NPV & IRR

Year 0 1 2 3

Rate 4%

CFAT

(5

)

(5.98

)

4.6

3

(5.98

)

Discounting 1 0.961538462 0.924556213 0.888996359

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CAPITAL INVESTMENT DECISION

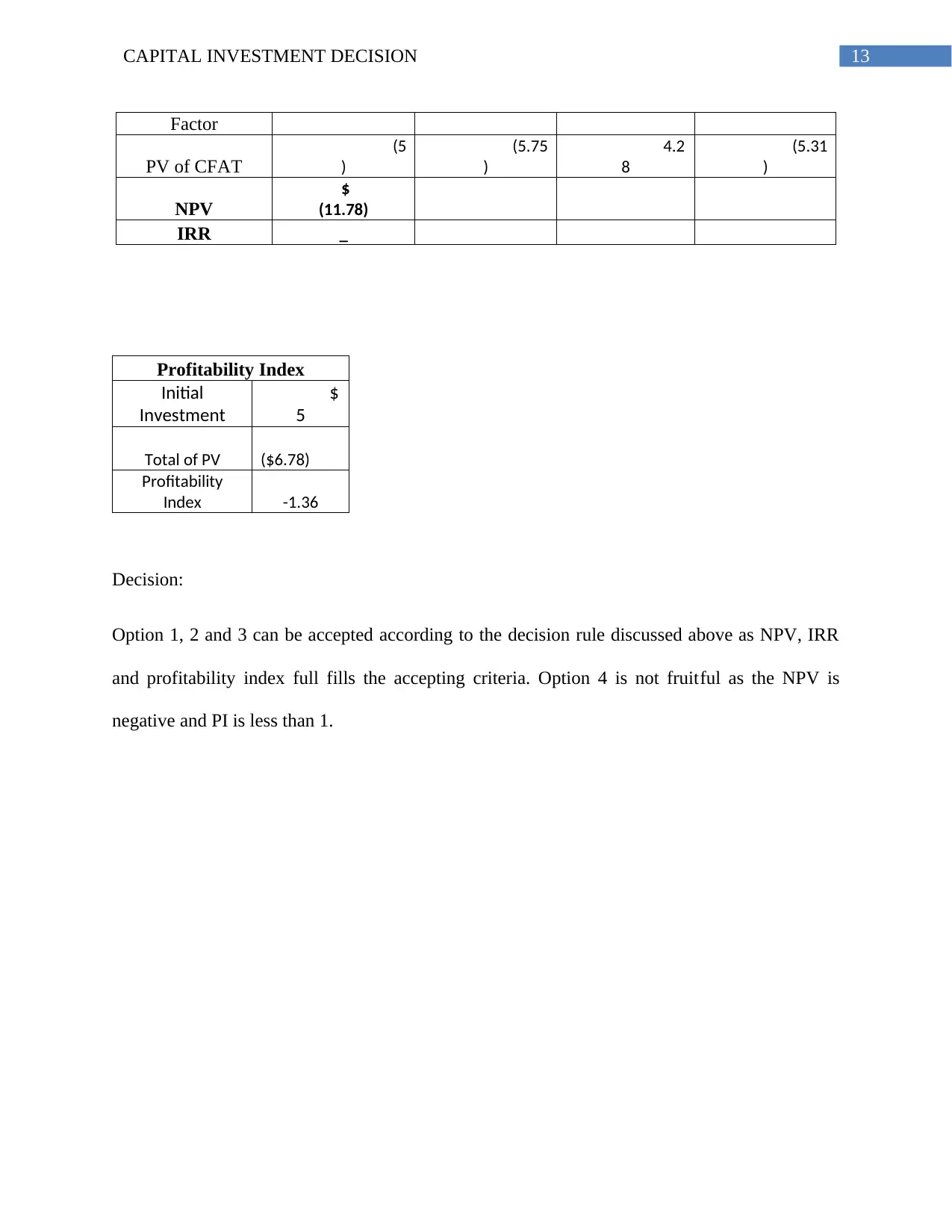

Factor

PV of CFAT

(5

)

(5.75

)

4.2

8

(5.31

)

NPV

$

(11.78)

IRR _

Profitability Index

Initial

Investment

$

5

Total of PV ($6.78)

Profitability

Index -1.36

Decision:

Option 1, 2 and 3 can be accepted according to the decision rule discussed above as NPV, IRR

and profitability index full fills the accepting criteria. Option 4 is not fruitful as the NPV is

negative and PI is less than 1.

Factor

PV of CFAT

(5

)

(5.75

)

4.2

8

(5.31

)

NPV

$

(11.78)

IRR _

Profitability Index

Initial

Investment

$

5

Total of PV ($6.78)

Profitability

Index -1.36

Decision:

Option 1, 2 and 3 can be accepted according to the decision rule discussed above as NPV, IRR

and profitability index full fills the accepting criteria. Option 4 is not fruitful as the NPV is

negative and PI is less than 1.

14CAPITAL INVESTMENT DECISION

Conclusion:

In this report, numerous techniques of capital investment under the supposition of

certainty as well as uncertainty have been conversed, emphasizing their virtual fortes and

faintness. The investment verdict made by directors will regulate a numeral of momentous

subjects like the cash flows created by the corporation, the dividends remunerated out by the

business, the market value of the business, the existence of the business etc. Many managers talk

about the superior skilled expertise that allows them to suggest a scheme should be commenced

even though it does not seem to have a positive NPV. It is tough to enumerate their worth, so the

“instinctive feel” method is often just to “estimate” that the scheme is commercial and then to go

gaining with it. In fact, the use of capital investment techniques permit for much more

conversant decisions with the attention that their submission does convert more challenging in a

period of rapid technical and fiscal change. In such a state, some form of processer based

imitation approach may well turn out to be of countless applied use. However, methods as if RO

plunders suppleness but it cannot substitute the standard capital investment practices (example

NPV) rather it increases on and progresses the insights of strategic assessment. However,

computer analyzes practically all capital investing methods, so it is informal to compute and list

all the choice events, because each one delivers decision makers with a slightly dissimilar piece

of applicable material.

Conclusion:

In this report, numerous techniques of capital investment under the supposition of

certainty as well as uncertainty have been conversed, emphasizing their virtual fortes and

faintness. The investment verdict made by directors will regulate a numeral of momentous

subjects like the cash flows created by the corporation, the dividends remunerated out by the

business, the market value of the business, the existence of the business etc. Many managers talk

about the superior skilled expertise that allows them to suggest a scheme should be commenced

even though it does not seem to have a positive NPV. It is tough to enumerate their worth, so the

“instinctive feel” method is often just to “estimate” that the scheme is commercial and then to go

gaining with it. In fact, the use of capital investment techniques permit for much more

conversant decisions with the attention that their submission does convert more challenging in a

period of rapid technical and fiscal change. In such a state, some form of processer based

imitation approach may well turn out to be of countless applied use. However, methods as if RO

plunders suppleness but it cannot substitute the standard capital investment practices (example

NPV) rather it increases on and progresses the insights of strategic assessment. However,

computer analyzes practically all capital investing methods, so it is informal to compute and list

all the choice events, because each one delivers decision makers with a slightly dissimilar piece

of applicable material.

15CAPITAL INVESTMENT DECISION

Reference:

Agrawal, A., Catalini, C. and Goldfarb, A., 2015. Crowdfunding: Geography, social networks,

and the timing of investment decisions. Journal of Economics & Management Strategy, 24(2),

pp.253-274.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Chiaroni, D., Chiesa, V., Colasanti, L., Cucchiella, F., D’Adamo, I. and Frattini, F., 2014.

Evaluating solar energy profitability: A focus on the role of self-consumption. Energy

Conversion and Management, 88, pp.317-331.

DAILY, J.E., KIEFF, F.S. and WILMARTH JR, A.E., 2014. Introduction. In Perspectives on

Financing Innovation (pp. 13-16). Routledge.

Genakoplos, J., Mitchell, O.S. and Zeldes, S.P., 2000. Would a privatized social security system

really pay a higher rate of return (No. w6713). National bureau of economic research.

Goodman, T.H., Neamtiu, M., Shroff, N. and White, H.D., 2013. Management forecast quality

and capital investment decisions. The Accounting Review, 89(1), pp.331-365.

Graham, J.R., Harvey, C.R. and Puri, M., 2015. Capital allocation and delegation of decision-

making authority within firms. Journal of Financial Economics, 115(3), pp.449-470.

Hartman, J.C. and Schafrick, I.C., 2014. The relevant internal rate of return. The Engineering

Economist, 49(2), pp.139-158.

Reference:

Agrawal, A., Catalini, C. and Goldfarb, A., 2015. Crowdfunding: Geography, social networks,

and the timing of investment decisions. Journal of Economics & Management Strategy, 24(2),

pp.253-274.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Chiaroni, D., Chiesa, V., Colasanti, L., Cucchiella, F., D’Adamo, I. and Frattini, F., 2014.

Evaluating solar energy profitability: A focus on the role of self-consumption. Energy

Conversion and Management, 88, pp.317-331.

DAILY, J.E., KIEFF, F.S. and WILMARTH JR, A.E., 2014. Introduction. In Perspectives on

Financing Innovation (pp. 13-16). Routledge.

Genakoplos, J., Mitchell, O.S. and Zeldes, S.P., 2000. Would a privatized social security system

really pay a higher rate of return (No. w6713). National bureau of economic research.

Goodman, T.H., Neamtiu, M., Shroff, N. and White, H.D., 2013. Management forecast quality

and capital investment decisions. The Accounting Review, 89(1), pp.331-365.

Graham, J.R., Harvey, C.R. and Puri, M., 2015. Capital allocation and delegation of decision-

making authority within firms. Journal of Financial Economics, 115(3), pp.449-470.

Hartman, J.C. and Schafrick, I.C., 2014. The relevant internal rate of return. The Engineering

Economist, 49(2), pp.139-158.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16CAPITAL INVESTMENT DECISION

Heckman, J.J., Moon, S.H., Pinto, R., Savelyev, P. and Yavitz, A., 2010. A new cost-benefit and

rate of return analysis for the Perry Preschool Program: A summary (No. w16180). National

Bureau of Economic Research.

Islam, N., Xayavong, V. and Kingwell, R., 2014. Broadacre farm productivity and profitability in

south‐western australia. Australian Journal of Agricultural and Resource Economics, 58(2),

pp.147-170.

Inanest, I., 2017. Capital Investment Decisions.

Kahlo, K.M. and Stutz, R.M., 2013. Access to capital, investment, and the financial

crisis. Journal of Financial Economics, 110(2), pp.280-299.

Kelleher, J.C. and McCormack, J.J., 2004. Internal rate of return: A cautionary tale. The

McKinsey Quarterly, 20, p.2004.

Settergren, O. and Mikula, B.D., 2005. The rate of return of pay-as-you-go pension systems: a

more exact consumption-loan model of interest. Journal of Pension Economics & Finance, 4(2),

pp.115-138.

Warscher, M., Strasser, U., Kraller, G., Marke, T., Franz, H. and Kunstmann, H., 2013.

Performance of complex snow cover descriptions in a distributed hydrological model system: A

case study for the high Alpine terrain of the Berchtesgaden Alps. Water resources

research, 49(5), pp.2619-2637.

Weber, T.A., 2014. On the (non-) equivalence of IRR and NPV. Journal of Mathematical

Economics, 52, pp.25-39.

Heckman, J.J., Moon, S.H., Pinto, R., Savelyev, P. and Yavitz, A., 2010. A new cost-benefit and

rate of return analysis for the Perry Preschool Program: A summary (No. w16180). National

Bureau of Economic Research.

Islam, N., Xayavong, V. and Kingwell, R., 2014. Broadacre farm productivity and profitability in

south‐western australia. Australian Journal of Agricultural and Resource Economics, 58(2),

pp.147-170.

Inanest, I., 2017. Capital Investment Decisions.

Kahlo, K.M. and Stutz, R.M., 2013. Access to capital, investment, and the financial

crisis. Journal of Financial Economics, 110(2), pp.280-299.

Kelleher, J.C. and McCormack, J.J., 2004. Internal rate of return: A cautionary tale. The

McKinsey Quarterly, 20, p.2004.

Settergren, O. and Mikula, B.D., 2005. The rate of return of pay-as-you-go pension systems: a

more exact consumption-loan model of interest. Journal of Pension Economics & Finance, 4(2),

pp.115-138.

Warscher, M., Strasser, U., Kraller, G., Marke, T., Franz, H. and Kunstmann, H., 2013.

Performance of complex snow cover descriptions in a distributed hydrological model system: A

case study for the high Alpine terrain of the Berchtesgaden Alps. Water resources

research, 49(5), pp.2619-2637.

Weber, T.A., 2014. On the (non-) equivalence of IRR and NPV. Journal of Mathematical

Economics, 52, pp.25-39.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.