Analyzing Stock Returns: CAPM Modeling, Risk, and Regression

VerifiedAdded on 2023/06/12

Student Name: Student ID:

Unit Name: Unit ID:

Date Due: Professor Name:

12

Paraphrase This Document

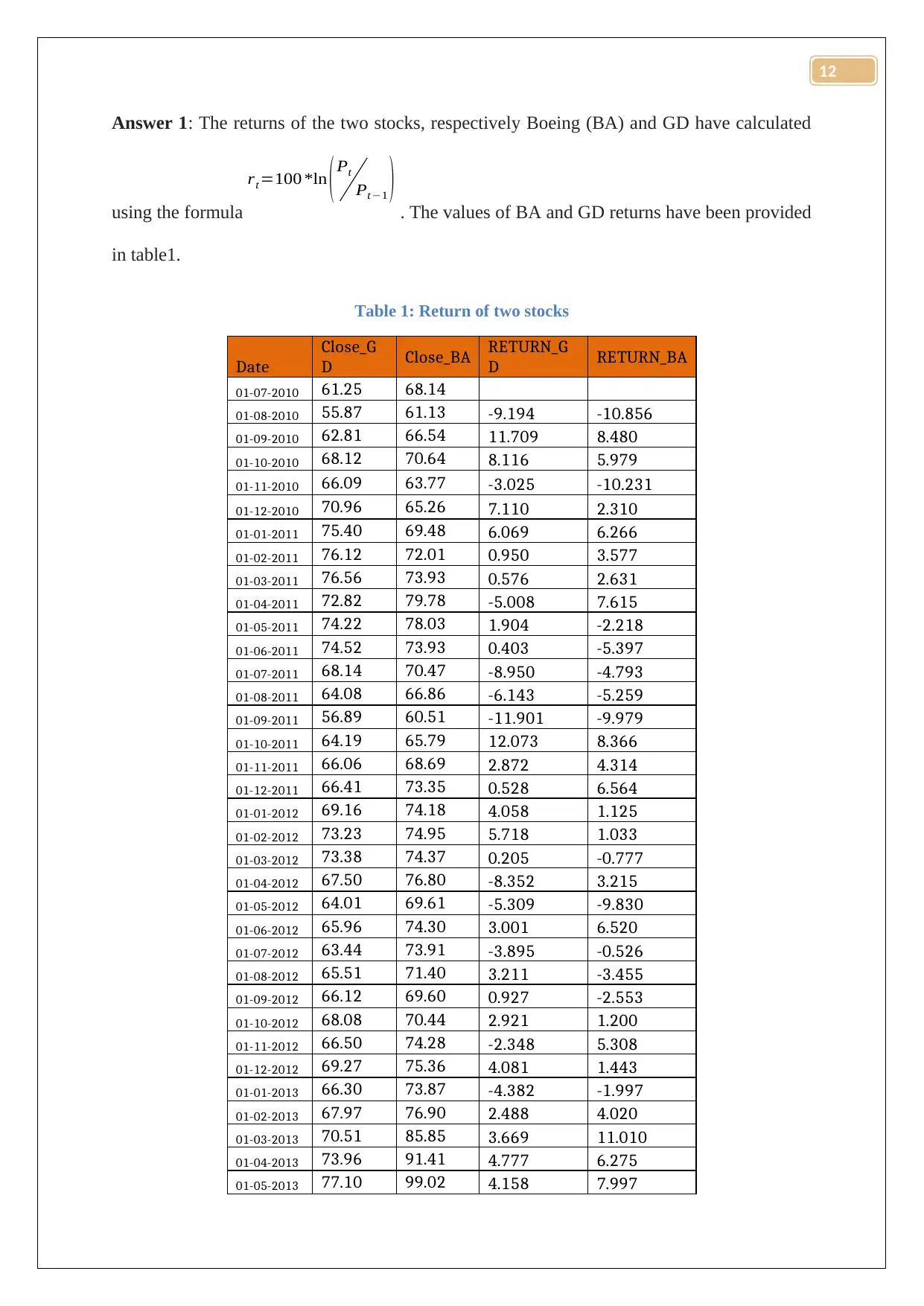

using the formula

rt=100 *ln ( Pt

Pt −1 ) . The values of BA and GD returns have been provided

in table1.

Table 1: Return of two stocks

Date

Close_G

D Close_BA RETURN_G

D RETURN_BA

01-07-2010 61.25 68.14

01-08-2010 55.87 61.13 -9.194 -10.856

01-09-2010 62.81 66.54 11.709 8.480

01-10-2010 68.12 70.64 8.116 5.979

01-11-2010 66.09 63.77 -3.025 -10.231

01-12-2010 70.96 65.26 7.110 2.310

01-01-2011 75.40 69.48 6.069 6.266

01-02-2011 76.12 72.01 0.950 3.577

01-03-2011 76.56 73.93 0.576 2.631

01-04-2011 72.82 79.78 -5.008 7.615

01-05-2011 74.22 78.03 1.904 -2.218

01-06-2011 74.52 73.93 0.403 -5.397

01-07-2011 68.14 70.47 -8.950 -4.793

01-08-2011 64.08 66.86 -6.143 -5.259

01-09-2011 56.89 60.51 -11.901 -9.979

01-10-2011 64.19 65.79 12.073 8.366

01-11-2011 66.06 68.69 2.872 4.314

01-12-2011 66.41 73.35 0.528 6.564

01-01-2012 69.16 74.18 4.058 1.125

01-02-2012 73.23 74.95 5.718 1.033

01-03-2012 73.38 74.37 0.205 -0.777

01-04-2012 67.50 76.80 -8.352 3.215

01-05-2012 64.01 69.61 -5.309 -9.830

01-06-2012 65.96 74.30 3.001 6.520

01-07-2012 63.44 73.91 -3.895 -0.526

01-08-2012 65.51 71.40 3.211 -3.455

01-09-2012 66.12 69.60 0.927 -2.553

01-10-2012 68.08 70.44 2.921 1.200

01-11-2012 66.50 74.28 -2.348 5.308

01-12-2012 69.27 75.36 4.081 1.443

01-01-2013 66.30 73.87 -4.382 -1.997

01-02-2013 67.97 76.90 2.488 4.020

01-03-2013 70.51 85.85 3.669 11.010

01-04-2013 73.96 91.41 4.777 6.275

01-05-2013 77.10 99.02 4.158 7.997

12

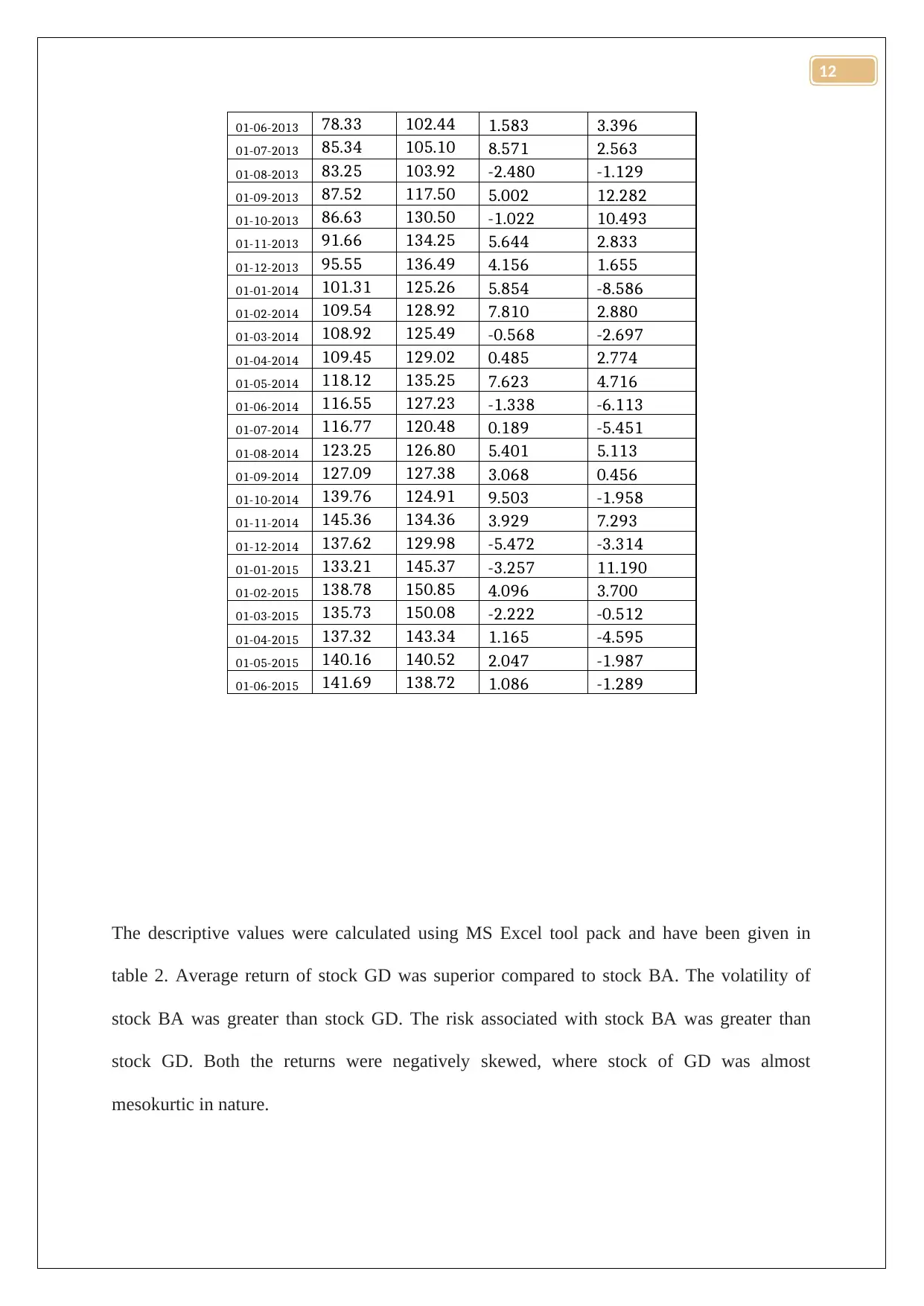

01-07-2013 85.34 105.10 8.571 2.563

01-08-2013 83.25 103.92 -2.480 -1.129

01-09-2013 87.52 117.50 5.002 12.282

01-10-2013 86.63 130.50 -1.022 10.493

01-11-2013 91.66 134.25 5.644 2.833

01-12-2013 95.55 136.49 4.156 1.655

01-01-2014 101.31 125.26 5.854 -8.586

01-02-2014 109.54 128.92 7.810 2.880

01-03-2014 108.92 125.49 -0.568 -2.697

01-04-2014 109.45 129.02 0.485 2.774

01-05-2014 118.12 135.25 7.623 4.716

01-06-2014 116.55 127.23 -1.338 -6.113

01-07-2014 116.77 120.48 0.189 -5.451

01-08-2014 123.25 126.80 5.401 5.113

01-09-2014 127.09 127.38 3.068 0.456

01-10-2014 139.76 124.91 9.503 -1.958

01-11-2014 145.36 134.36 3.929 7.293

01-12-2014 137.62 129.98 -5.472 -3.314

01-01-2015 133.21 145.37 -3.257 11.190

01-02-2015 138.78 150.85 4.096 3.700

01-03-2015 135.73 150.08 -2.222 -0.512

01-04-2015 137.32 143.34 1.165 -4.595

01-05-2015 140.16 140.52 2.047 -1.987

01-06-2015 141.69 138.72 1.086 -1.289

The descriptive values were calculated using MS Excel tool pack and have been given in

table 2. Average return of stock GD was superior compared to stock BA. The volatility of

stock BA was greater than stock GD. The risk associated with stock BA was greater than

stock GD. Both the returns were negatively skewed, where stock of GD was almost

mesokurtic in nature.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RETURN_GD Values RETURN_BA Values

Mean 1.421 Mean 1.205

Standard Error 0.668 Standard Error 0.739

Median 1.904 Median 1.655

Standard Deviation 5.131 Standard Deviation 5.675

Sample Variance 26.332 Sample Variance 32.206

Kurtosis 0.073 Kurtosis -0.444

Skewness -0.380 Skewness -0.240

Range 23.974 Range 23.138

Minimum -11.901 Minimum -10.856

Maximum 12.073 Maximum 12.282

Sum 83.868 Sum 71.089

Count 59.000 Count 59.000

Largest(1) 12.073 Largest(1) 12.282

Smallest(1) -11.901 Smallest(1) -10.856

Confidence Level

(95.0%) 1.337

Confidence Level

(95.0%) 1.479

Jarque-Berra test was performed for both the stocks to check normality. The statistical

work was performed in MS Excel. For the Jarque-Berra test, skewness and excess

kurtosis were evaluated. Using the test statistic

JB= n

6 ( S1

2

+

K1

2

4 ) where n is the

sample size, S1 denotes the skewness and K1denotes the excess kurtosis of the return of

the two stocks. The significance value was found by using the chi-square distribution

with 2 degrees of freedom. The Jarque-Berra test revealed that both the samples of the

stocks were not normal, as the JB values were insignificant (p value > 0.05).

Table 3: Jarque-Berra test results

SKEWNES

S KURTOSIS n

RETURN_GD -0.380 0.073 59

RETURN_BA -0.240 -0.444 59

JB-

Value p-value

Jarque-

Berra_GD 9.833 0.146 1.436 0.488

12

Paraphrase This Document

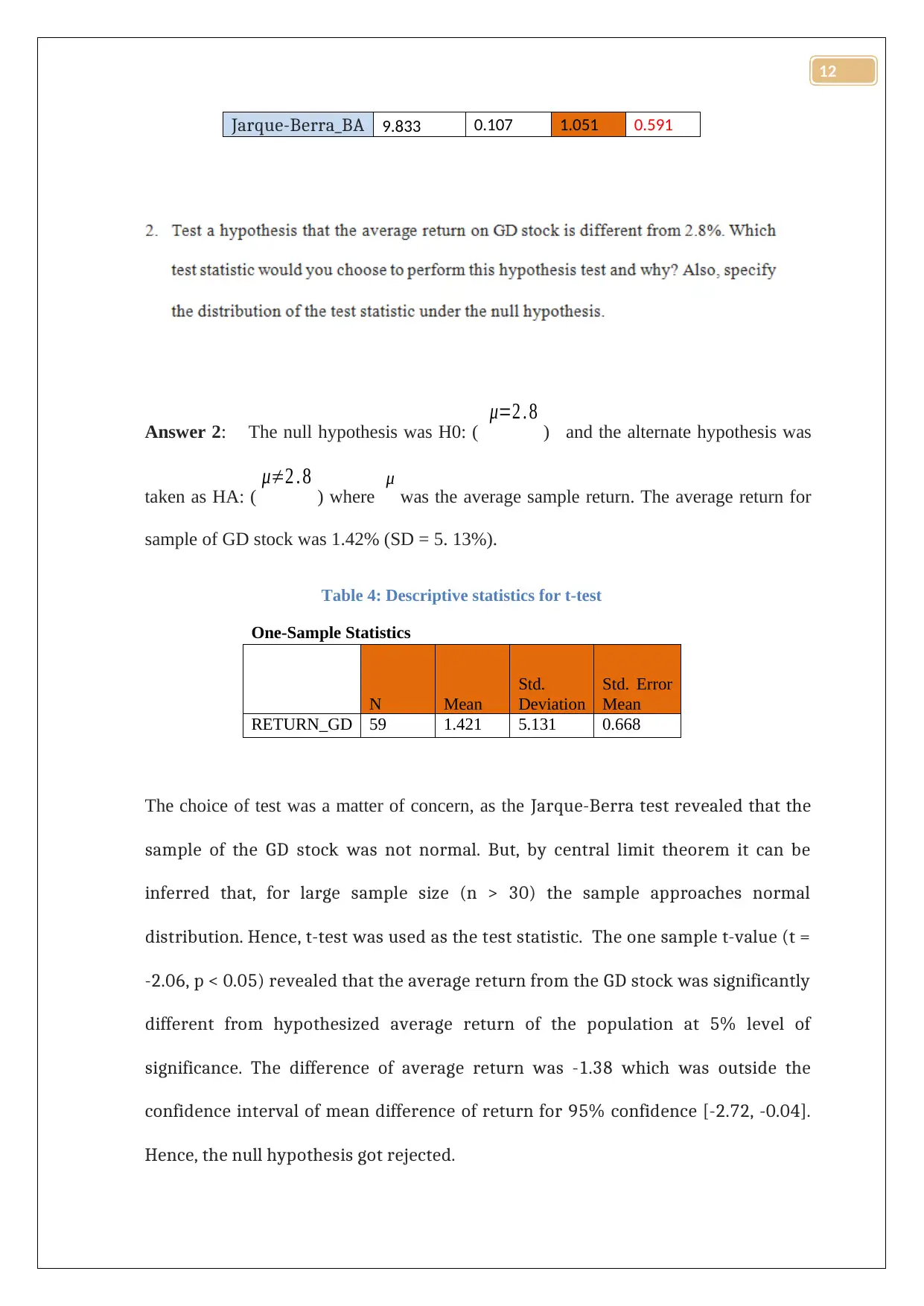

Answer 2: The null hypothesis was H0: (

μ=2 . 8 ) and the alternate hypothesis was

taken as HA: (

μ≠2 . 8 ) where μ

was the average sample return. The average return for

sample of GD stock was 1.42% (SD = 5. 13%).

Table 4: Descriptive statistics for t-test

One-Sample Statistics

N Mean

Std.

Deviation

Std. Error

Mean

RETURN_GD 59 1.421 5.131 0.668

The choice of test was a matter of concern, as the Jarque-Berra test revealed that the

sample of the GD stock was not normal. But, by central limit theorem it can be

inferred that, for large sample size (n > 30) the sample approaches normal

distribution. Hence, t-test was used as the test statistic. The one sample t-value (t =

-2.06, p < 0.05) revealed that the average return from the GD stock was significantly

different from hypothesized average return of the population at 5% level of

significance. The difference of average return was -1.38 which was outside the

confidence interval of mean difference of return for 95% confidence [-2.72, -0.04].

Hence, the null hypothesis got rejected.

12

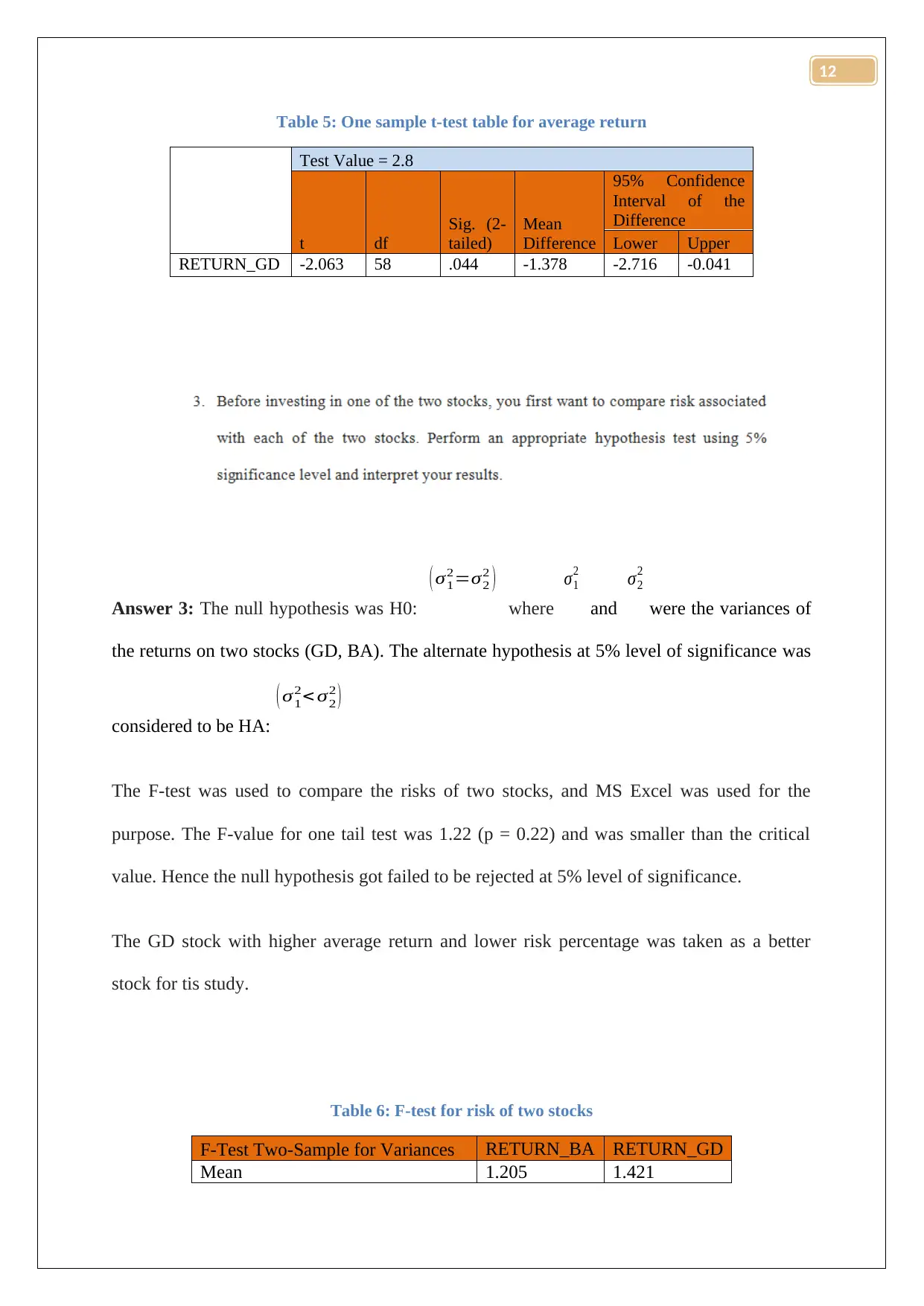

Test Value = 2.8

t df

Sig. (2-

tailed)

Mean

Difference

95% Confidence

Interval of the

Difference

Lower Upper

RETURN_GD -2.063 58 .044 -1.378 -2.716 -0.041

Answer 3: The null hypothesis was H0:

( σ1

2=σ2

2 )

where

σ1

2

and

σ2

2

were the variances of

the returns on two stocks (GD, BA). The alternate hypothesis at 5% level of significance was

considered to be HA:

( σ1

2< σ2

2 )

The F-test was used to compare the risks of two stocks, and MS Excel was used for the

purpose. The F-value for one tail test was 1.22 (p = 0.22) and was smaller than the critical

value. Hence the null hypothesis got failed to be rejected at 5% level of significance.

The GD stock with higher average return and lower risk percentage was taken as a better

stock for tis study.

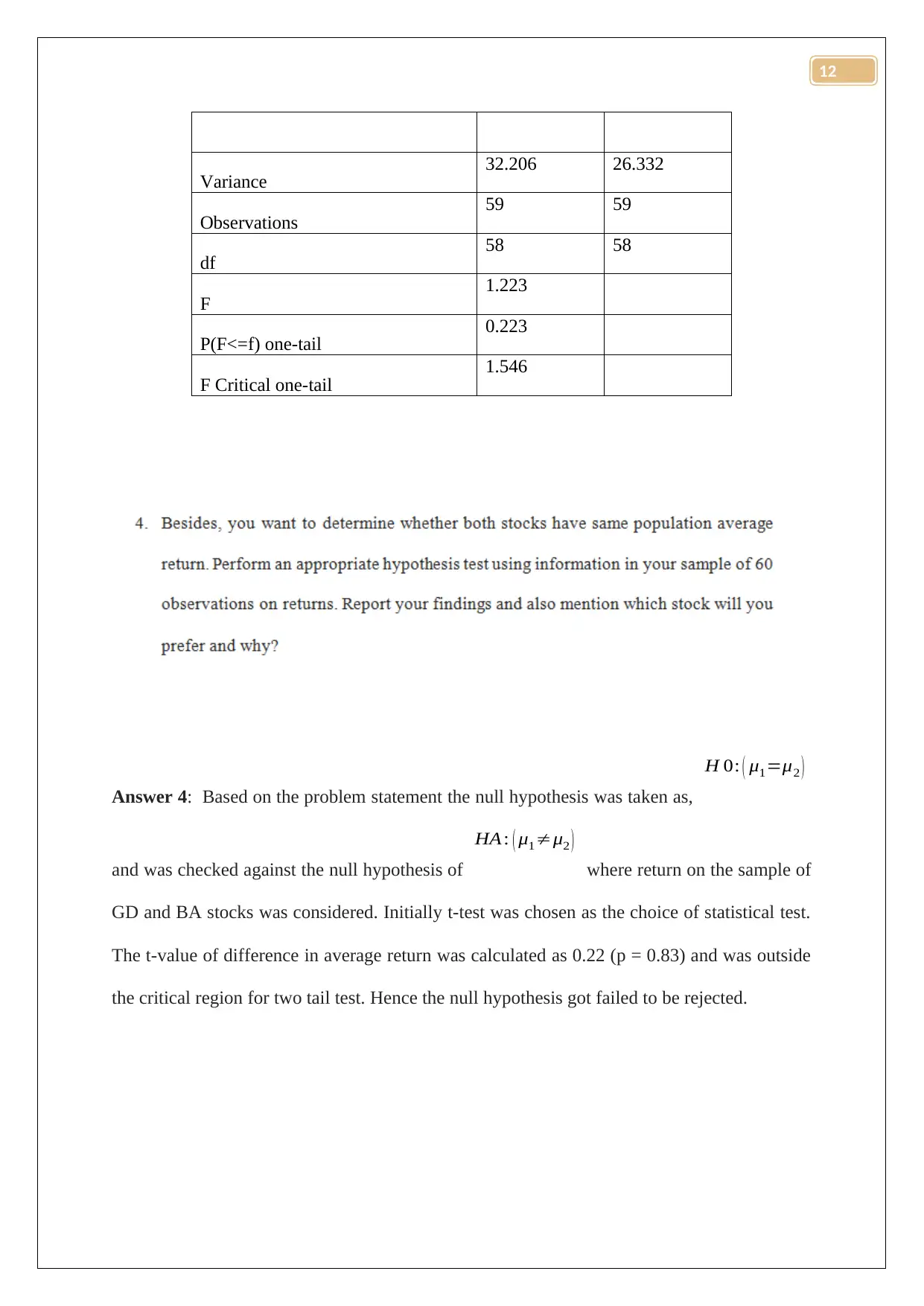

Table 6: F-test for risk of two stocks

F-Test Two-Sample for Variances RETURN_BA RETURN_GD

Mean 1.205 1.421

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Observations 59 59

df 58 58

F 1.223

P(F<=f) one-tail 0.223

F Critical one-tail 1.546

Answer 4: Based on the problem statement the null hypothesis was taken as,

H 0: ( μ1=μ2 )

and was checked against the null hypothesis of

HA : ( μ1≠μ2 )

where return on the sample of

GD and BA stocks was considered. Initially t-test was chosen as the choice of statistical test.

The t-value of difference in average return was calculated as 0.22 (p = 0.83) and was outside

the critical region for two tail test. Hence the null hypothesis got failed to be rejected.

12

Paraphrase This Document

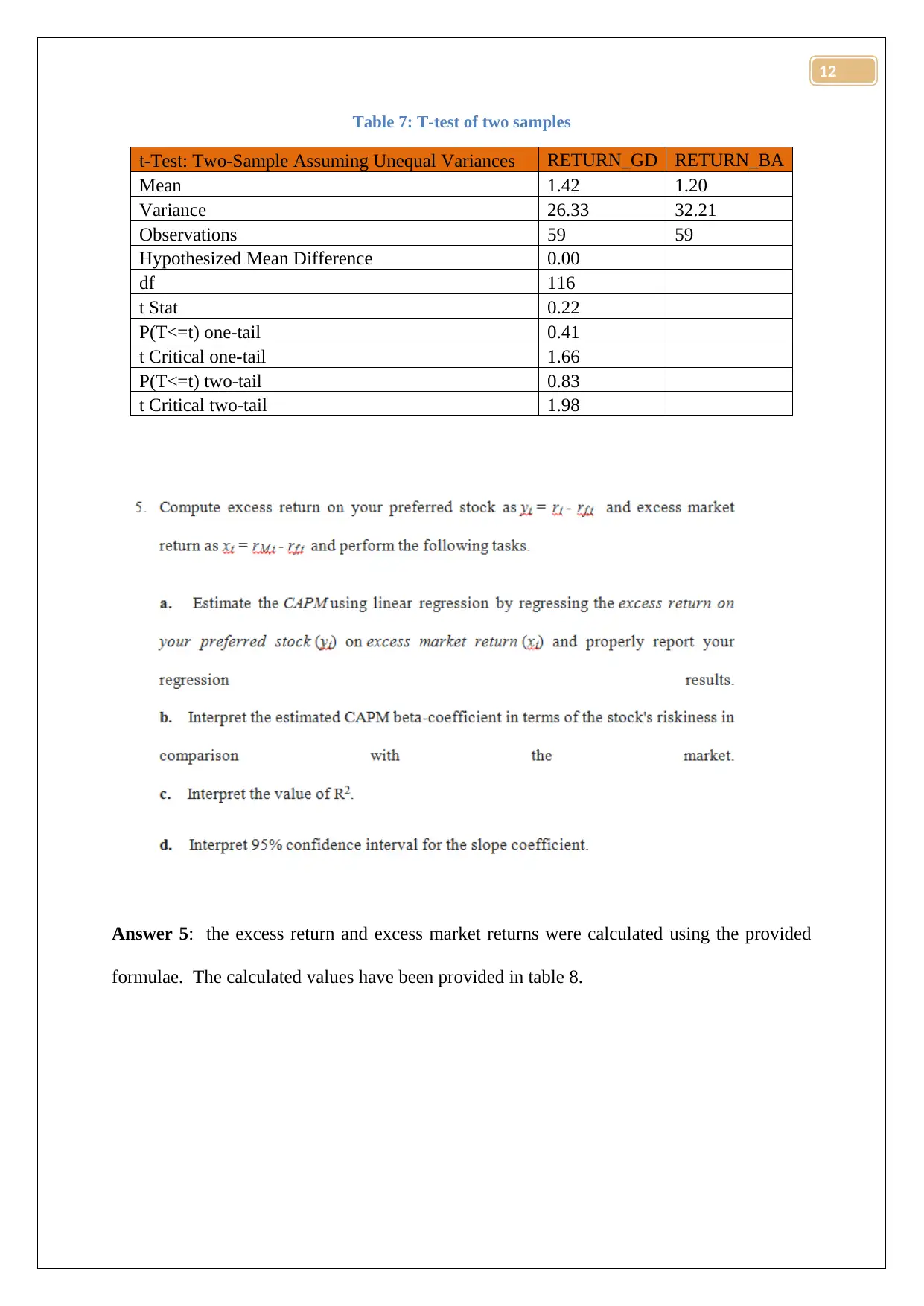

t-Test: Two-Sample Assuming Unequal Variances RETURN_GD RETURN_BA

Mean 1.42 1.20

Variance 26.33 32.21

Observations 59 59

Hypothesized Mean Difference 0.00

df 116

t Stat 0.22

P(T<=t) one-tail 0.41

t Critical one-tail 1.66

P(T<=t) two-tail 0.83

t Critical two-tail 1.98

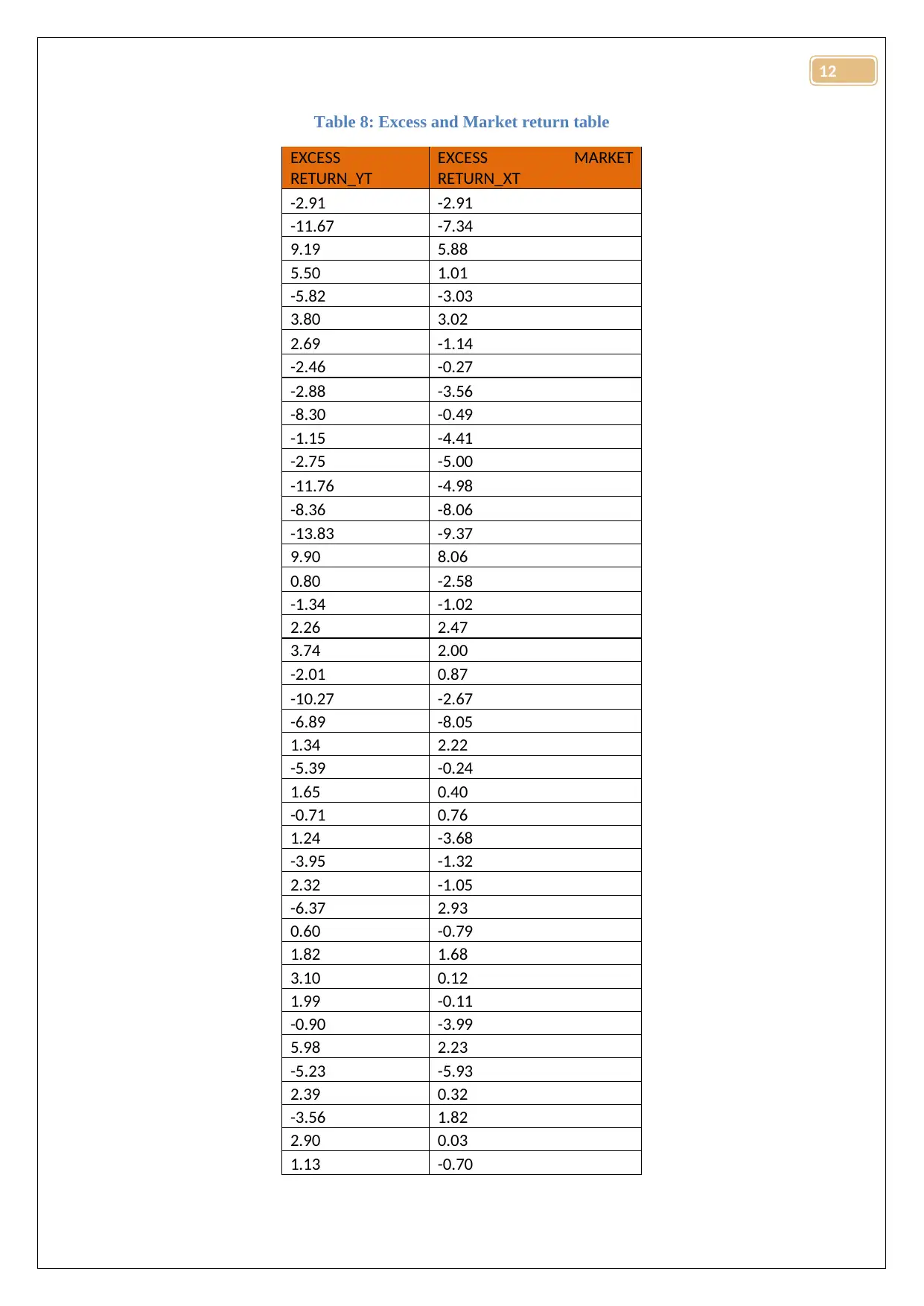

Answer 5: the excess return and excess market returns were calculated using the provided

formulae. The calculated values have been provided in table 8.

12

EXCESS

RETURN_YT

EXCESS MARKET

RETURN_XT

-2.91 -2.91

-11.67 -7.34

9.19 5.88

5.50 1.01

-5.82 -3.03

3.80 3.02

2.69 -1.14

-2.46 -0.27

-2.88 -3.56

-8.30 -0.49

-1.15 -4.41

-2.75 -5.00

-11.76 -4.98

-8.36 -8.06

-13.83 -9.37

9.90 8.06

0.80 -2.58

-1.34 -1.02

2.26 2.47

3.74 2.00

-2.01 0.87

-10.27 -2.67

-6.89 -8.05

1.34 2.22

-5.39 -0.24

1.65 0.40

-0.71 0.76

1.24 -3.68

-3.95 -1.32

2.32 -1.05

-6.37 2.93

0.60 -0.79

1.82 1.68

3.10 0.12

1.99 -0.11

-0.90 -3.99

5.98 2.23

-5.23 -5.93

2.39 0.32

-3.56 1.82

2.90 0.03

1.13 -0.70

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

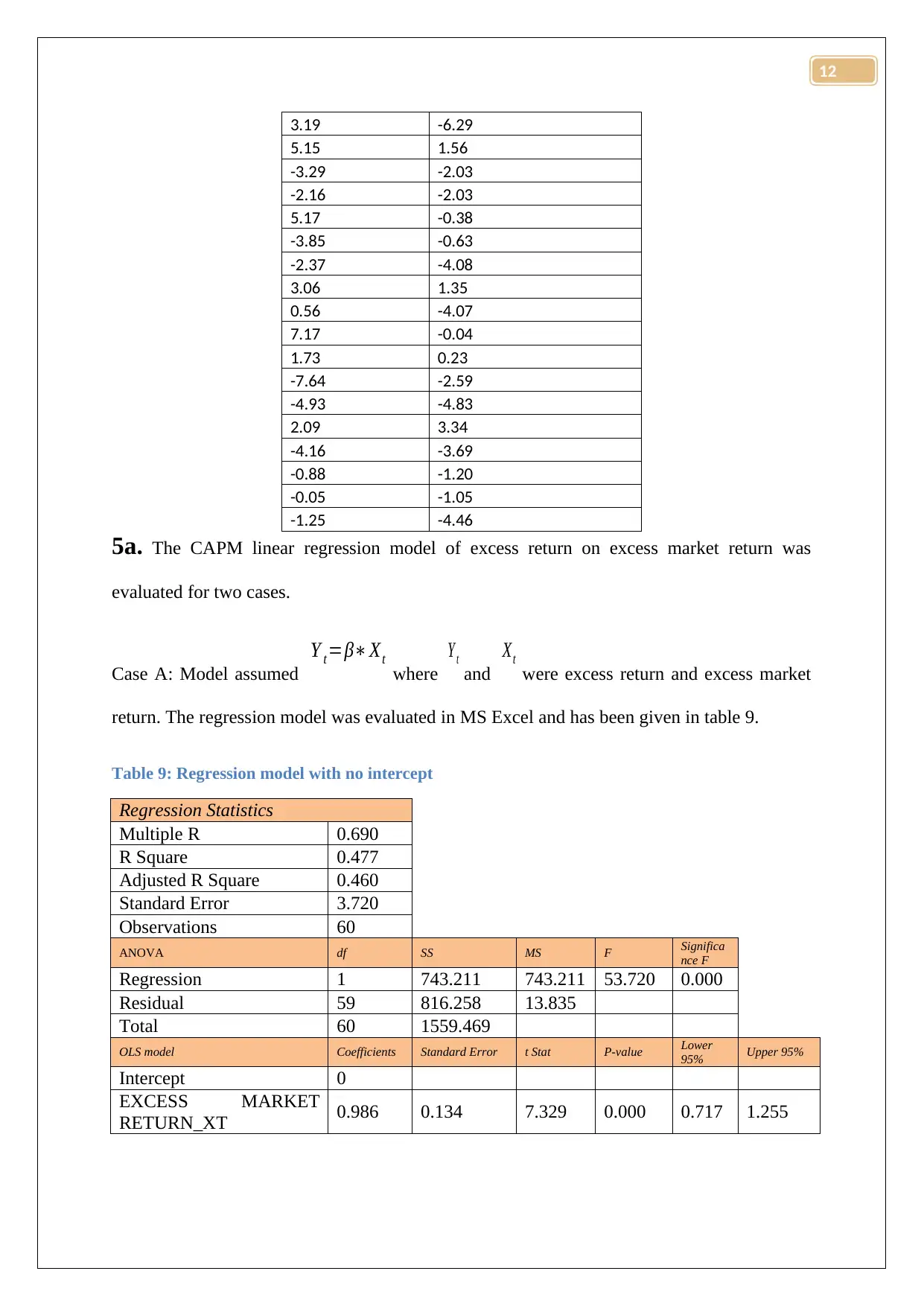

5.15 1.56

-3.29 -2.03

-2.16 -2.03

5.17 -0.38

-3.85 -0.63

-2.37 -4.08

3.06 1.35

0.56 -4.07

7.17 -0.04

1.73 0.23

-7.64 -2.59

-4.93 -4.83

2.09 3.34

-4.16 -3.69

-0.88 -1.20

-0.05 -1.05

-1.25 -4.46

5a. The CAPM linear regression model of excess return on excess market return was

evaluated for two cases.

Case A: Model assumed

Y t=β∗Xt

where

Y t

and

Xt

were excess return and excess market

return. The regression model was evaluated in MS Excel and has been given in table 9.

Table 9: Regression model with no intercept

Regression Statistics

Multiple R 0.690

R Square 0.477

Adjusted R Square 0.460

Standard Error 3.720

Observations 60

ANOVA df SS MS F Significa

nce F

Regression 1 743.211 743.211 53.720 0.000

Residual 59 816.258 13.835

Total 60 1559.469

OLS model Coefficients Standard Error t Stat P-value Lower

95% Upper 95%

Intercept 0

EXCESS MARKET

RETURN_XT 0.986 0.134 7.329 0.000 0.717 1.255

12

Paraphrase This Document

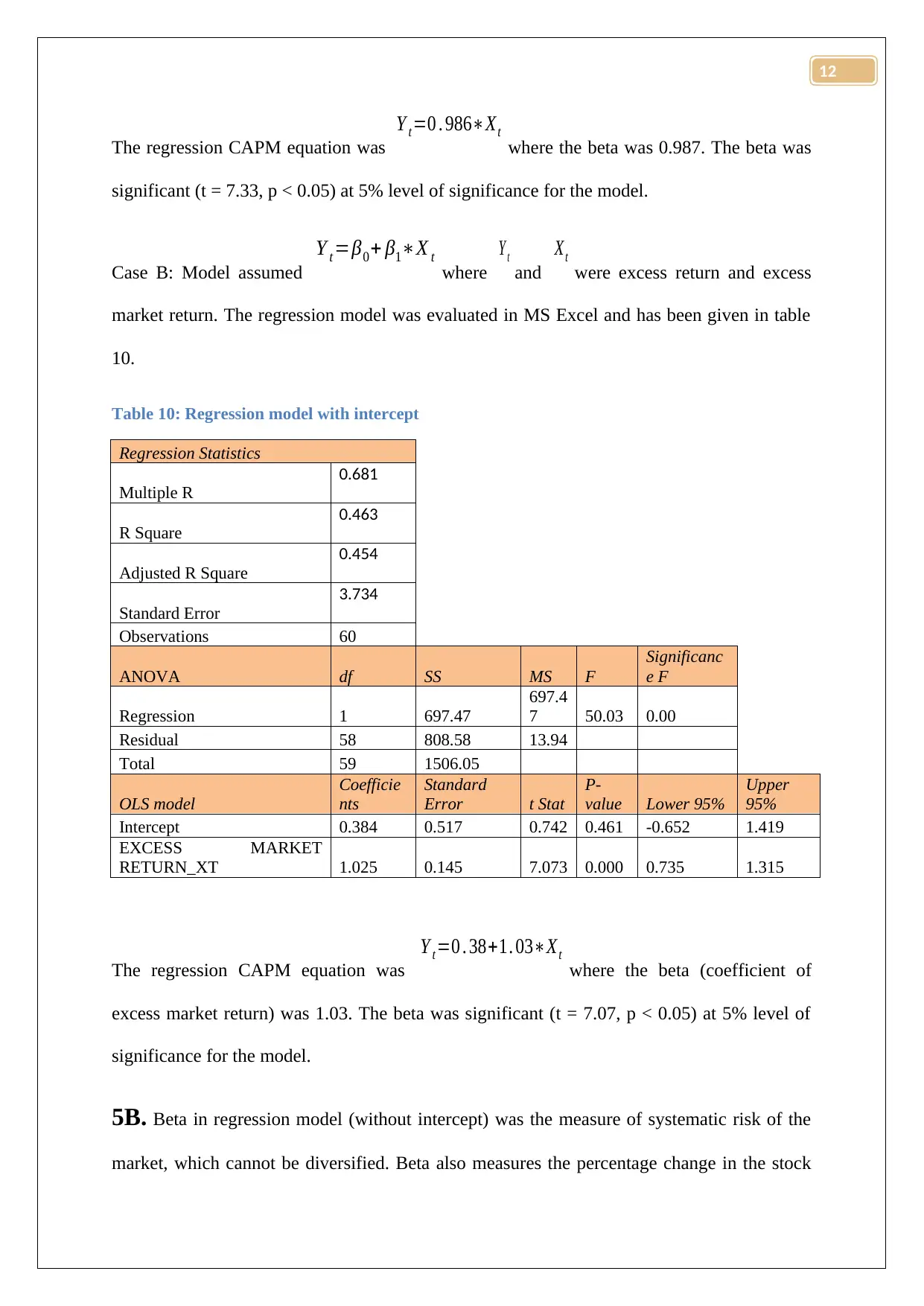

Y t =0 . 986∗Xt

where the beta was 0.987. The beta was

significant (t = 7.33, p < 0.05) at 5% level of significance for the model.

Case B: Model assumed

Y t=β0+ β1∗X t

where

Y t

and

Xt

were excess return and excess

market return. The regression model was evaluated in MS Excel and has been given in table

10.

Table 10: Regression model with intercept

Regression Statistics

Multiple R

0.681

R Square

0.463

Adjusted R Square

0.454

Standard Error

3.734

Observations 60

ANOVA df SS MS F

Significanc

e F

Regression 1 697.47

697.4

7 50.03 0.00

Residual 58 808.58 13.94

Total 59 1506.05

OLS model

Coefficie

nts

Standard

Error t Stat

P-

value Lower 95%

Upper

95%

Intercept 0.384 0.517 0.742 0.461 -0.652 1.419

EXCESS MARKET

RETURN_XT 1.025 0.145 7.073 0.000 0.735 1.315

The regression CAPM equation was

Y t =0 . 38+1. 03∗Xt

where the beta (coefficient of

excess market return) was 1.03. The beta was significant (t = 7.07, p < 0.05) at 5% level of

significance for the model.

5B. Beta in regression model (without intercept) was the measure of systematic risk of the

market, which cannot be diversified. Beta also measures the percentage change in the stock

12

hence the fund was a neutral stock. For 1% change in market folio, the GD stock will change

by almost 1%. The systematic risk for this model was less, sine the value of beta was less

than one.

Beta in regression model (with intercept) was the measure of systematic risk of the market,

which cannot be diversified. Beta also measures the percentage change in the stock return for

1% change in the market portfolio. The GD stock beta was greater than one; hence it was an

aggressive stock. For 1% change in market folio, the GD stock will change by almost 1.03%.

The systematic risk for this model was greater, sine the value of beta was slightly greater than

one.

5C. The coefficient of determination for model A was 0.48 and for model B, it was 0.46.

Therefore, in model A, the excess return on market was able to explain 48% variance of

excess return, whereas in model B, the excess return on market was able to explain 46%

variance of excess return.

5D. Case A: The 95% confidence interval not present.

Case B: The 95% confidence interval was [-0.65, 1.42], which signified that the slope of the

model (0.38) was within the acceptance region with t-value = 0.74 (p-value = 0.46). Hence

the null hypothesis that the slope was almost negligible and equal to zero did not get rejected

at 5% level of significance. The insignificance of the slope was evident and the model A was

the appropriation of that (Barberis et al., 2015).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The null hypothesis was

H 0: ( β1=1 ) and was tested at 5% level of significance against the

alternate hypothesis

Ha: ( β1≠1 ) . The appropriate choice of test was taken as t-test where

t = statistic−parameter

S . E of parameter .

Now, for model A, the test statistic was

t= 0. 986−1

0 . 134 =−0 . 1045

with 58 degrees of freedom.

The p value for t statistic with 58 degrees of freedom was p = 0.458 (Excel used). Hence the

null hypothesis failed to get rejected. It was concluded that the stock was almost a neutral

stock (Fard & Falah, 2015). The confidence interval was calculated as [0.986-0.134,

0.986+0.134] = [0.852, 1.12]. Hence the parameter was well within the confidence interval at

5% level of significance.

For model B, the test statistic was

t=1 . 025−1

0 . 145 =0 . 172

with 58 degrees of freedom. The p

value for t statistic with 58 degrees of freedom was p = 0.57 (Excel used). Hence the null

hypothesis failed to get rejected. It was concluded that the stock was almost a neutral stock.

The confidence interval was calculated as [1.025-0.145, 1.025+0.145] = [0.88, 1.17]. Hence

the parameter was well within the confidence interval at 5% level of significance.

12

Paraphrase This Document

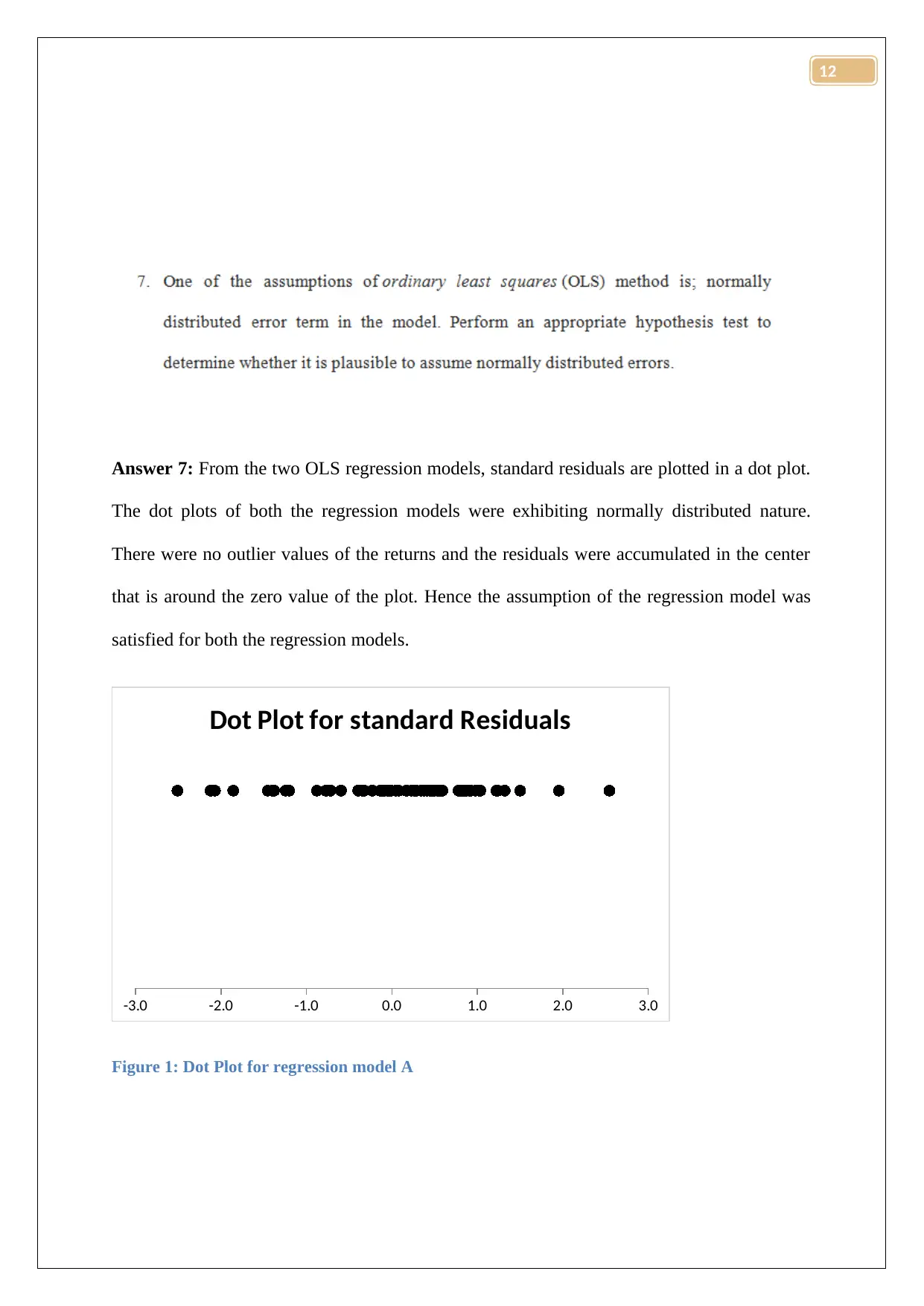

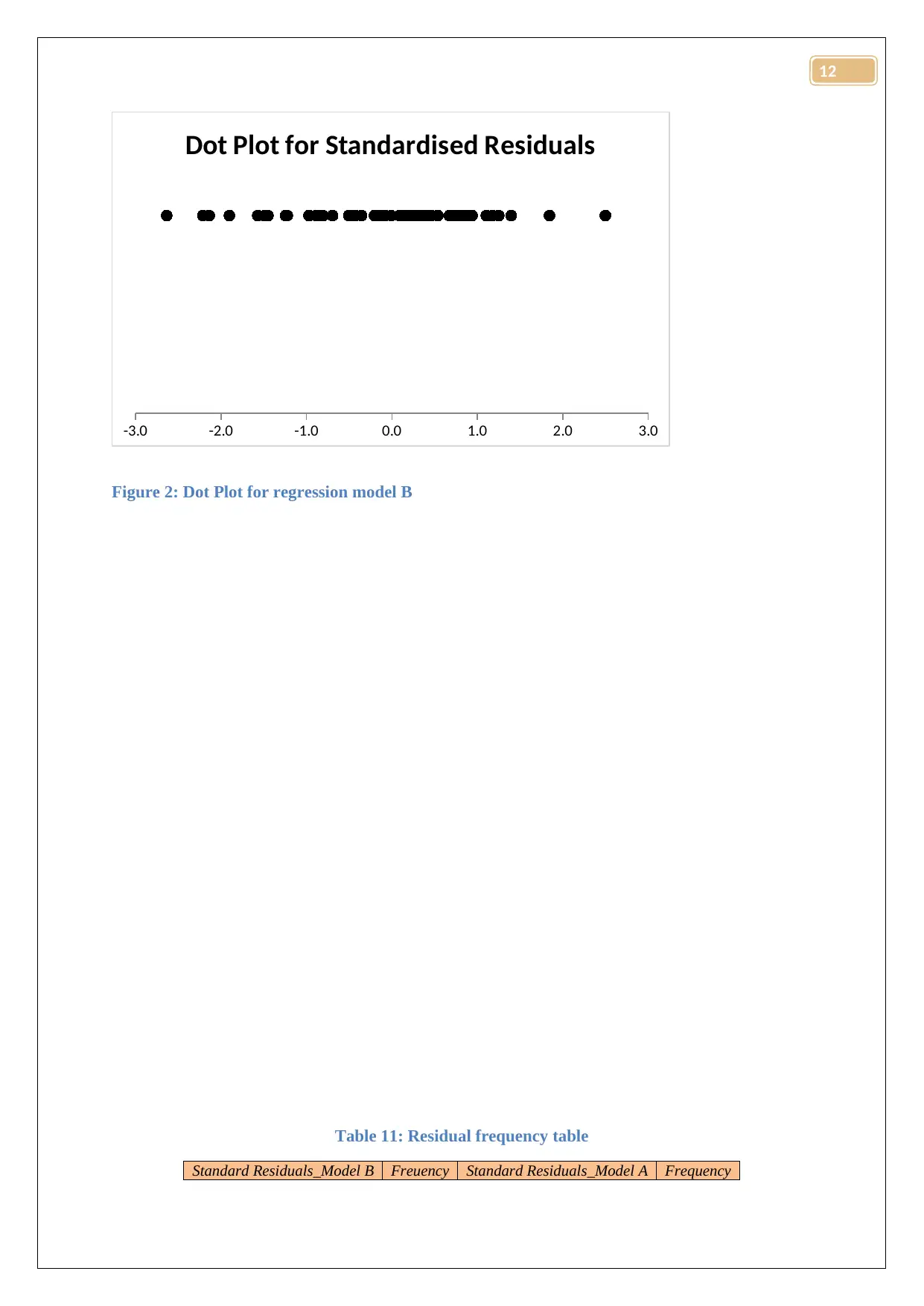

The dot plots of both the regression models were exhibiting normally distributed nature.

There were no outlier values of the returns and the residuals were accumulated in the center

that is around the zero value of the plot. Hence the assumption of the regression model was

satisfied for both the regression models.

-3.0 -2.0 -1.0 0.0 1.0 2.0 3.0

Dot Plot for standard Residuals

Figure 1: Dot Plot for regression model A

12

Dot Plot for Standardised Residuals

Figure 2: Dot Plot for regression model B

Table 11: Residual frequency table

Standard Residuals_Model B Freuency Standard Residuals_Model A Frequency

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0.0 1

-1.2 1

-1.2 1

0.8 1

0.9 1

1.1 1

1.2 1

-0.8 1

-0.8 1

0.1 1

0.2 1

0.9 1

1.0 1

-0.7 1

-0.6 1

0.1 1

0.2 1

-2.2 1

-2.1 1

0.8 1

0.9 1

0.5 1

0.6 1

-1.9 1

-1.9 1

-0.1 1

-0.1 1

-1.2 1

-1.2 1

0.3 1

0.5 1

0.8 1

0.9 1

-0.2 1

-0.1 1

-0.2 1

0.0 1

0.4 1

0.5 1

-0.9 1

-0.8 1

-2.1 1

-2.1 1

0.3 1

0.3 1

-0.4 1

-0.2 1

-1.5 1

-1.4 1

0.2 1

0.3 1

12

Paraphrase This Document

-0.4 1

1.2 1

1.3 1

-0.8 1

-0.7 1

0.8 1

0.9 1

-2.6 1

-2.5 1

0.3 1

0.4 1

-0.1 1

0.0 1

0.7 1

0.8 1

0.5 1

0.6 1

0.8 1

0.8 1

0.9 1

1.0 1

0.1 1

0.2 1

0.5 1

0.6 1

-1.6 1

-1.5 1

0.7 1

0.8 1

0.4 1

0.5 1

2.5 1

2.5 1

0.9 1

1.0 1

-0.4 1

-0.3 1

-0.1 1

0.0 1

1.4 1

1.5 1

-1.0 1

-0.9 1

0.4 1

0.4 1

0.3 1

0.5 1

1.2 1

1.2 1

1.8 1

2.0 1

0.3 1

0.4 1

12

-1.4 1

-0.1 1

0.0 1

-0.5 1

-0.3 1

-0.2 1

-0.1 1

0.0 1

0.1 1

0.2 1

0.3 1

0.8 1

0.9 1

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Barberis, N., Greenwood, R., Jin, L., & Shleifer, A. (2015). X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), 1-24.

Fard, H. V., & Falah, A. B. (2015). A New Modified CAPM Model: The Two Beta

CAPM. Jurnal UMP Social Sciences and Technology Management Vol, 3(1).

12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.