Carbon Disclosure in Australian Companies: Legitimacy Theory Analysis

VerifiedAdded on 2023/04/20

|14

|2553

|333

Report

AI Summary

This research report investigates carbon disclosure practices in Australian companies, framed by legitimacy theory to predict corporate responses to heightened societal environmental concerns. The report begins with an introduction outlining the research's focus on carbon disclosure and its relevance in the context of ecological imbalances and stakeholder pressures. It then presents practical motivations, highlighting the importance of carbon disclosure for both businesses and the community in achieving transparency regarding carbon emissions. A literature review synthesizes empirical research from three journal articles, using the annotated bibliography format to analyze and critique the findings, and it also discusses how companies respond to legitimacy threats. The report then proposes a methodology for future research, suggesting the automobile sector as a relevant case study and suggesting both survey and descriptive methodological approaches. The report concludes that carbon disclosure ensures corporate social responsibility and transparency and contributes significantly to corporate sustainability goals. The appendix provides a detailed summary of each of the articles reviewed, including their methodologies and findings.

CARBON DISCLOSURE IN THE LIGHT OF LEGITIMACY THEORY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1.0 Introduction................................................................................................................................3

2.0 Practical Motivation...................................................................................................................4

3.0 Literature Review......................................................................................................................5

4.0 Proposition and Possible Methodology.....................................................................................8

5.0 Conclusion.................................................................................................................................9

References:....................................................................................................................................10

Appendix:......................................................................................................................................12

Page 2 of 14

1.0 Introduction................................................................................................................................3

2.0 Practical Motivation...................................................................................................................4

3.0 Literature Review......................................................................................................................5

4.0 Proposition and Possible Methodology.....................................................................................8

5.0 Conclusion.................................................................................................................................9

References:....................................................................................................................................10

Appendix:......................................................................................................................................12

Page 2 of 14

1.0 Introduction

The research study has been an individual assignment focusing to underscore the usage of

legitimacy theory in predicting the manner in which the companies in the Australian market

would respond to the significant enhancement in the social concern related to the environment.

The project aims to highlight carbon disclosure as the primary issue and tends to evaluate it with

the support legitimacy theory. In the consideration of Michelon et al. (2018), it can be noted that

legitimacy theory tends to highlight the degree to which corporate social and environmental

revelations are controlled by the periphery developed by a community with the purpose of

appreciating and avoiding being penalized by society in which businesses operate. The literature

review section of the project aims to conduct empirical research of three different journals

containing the context “Carbon Disclosure in the light of Legitimacy Theory” in annotated

bibliography format. The journals would be discussed following argumentative format and

statements would be critiqued by other references. Depending on the entire discussions, a

suitable conclusion would be derived following strategic recommendations to overcome the

identified gaps.

Page 3 of 14

The research study has been an individual assignment focusing to underscore the usage of

legitimacy theory in predicting the manner in which the companies in the Australian market

would respond to the significant enhancement in the social concern related to the environment.

The project aims to highlight carbon disclosure as the primary issue and tends to evaluate it with

the support legitimacy theory. In the consideration of Michelon et al. (2018), it can be noted that

legitimacy theory tends to highlight the degree to which corporate social and environmental

revelations are controlled by the periphery developed by a community with the purpose of

appreciating and avoiding being penalized by society in which businesses operate. The literature

review section of the project aims to conduct empirical research of three different journals

containing the context “Carbon Disclosure in the light of Legitimacy Theory” in annotated

bibliography format. The journals would be discussed following argumentative format and

statements would be critiqued by other references. Depending on the entire discussions, a

suitable conclusion would be derived following strategic recommendations to overcome the

identified gaps.

Page 3 of 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.0 Practical Motivation

In the statement of Matthews et al. (2018), carbon emission has become one of the major factors

that are considered responsible behind the ecological imbalances. Moreover, companies are also

receiving several threats from the environmental agencies in terms of restricting their operations

that can lead devote to high carbon emission. Therefore, the organizations are required to have

an apparent idea regarding the carbon emission they are allowed to release in the environment to

maintain ecological stability (Jiang et al. 2018). Hence, carbon disclosure project has been a

relevant criterion that can help both businesses and community to gain transparent information

regarding the carbon emission an organization is causing in the environment (Fawcett and Parag,

2017). Based on which further actions can be taken. And legitimacy framework focus on

corporate and environmental wellbeing, thus, following legitimacy approach would help the

study to gain a better inference with logic.

Page 4 of 14

In the statement of Matthews et al. (2018), carbon emission has become one of the major factors

that are considered responsible behind the ecological imbalances. Moreover, companies are also

receiving several threats from the environmental agencies in terms of restricting their operations

that can lead devote to high carbon emission. Therefore, the organizations are required to have

an apparent idea regarding the carbon emission they are allowed to release in the environment to

maintain ecological stability (Jiang et al. 2018). Hence, carbon disclosure project has been a

relevant criterion that can help both businesses and community to gain transparent information

regarding the carbon emission an organization is causing in the environment (Fawcett and Parag,

2017). Based on which further actions can be taken. And legitimacy framework focus on

corporate and environmental wellbeing, thus, following legitimacy approach would help the

study to gain a better inference with logic.

Page 4 of 14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.0 Literature Review

Andrew, J. and Cortese, C. L. (2011) Carbon disclosures: comparability, the Carbon

Disclosure Project and the Greenhouse Gas Protocol, Australian Accounting Business and

Finance Journal, Vol 5(4) pp. 5-18

The specific journals emphasise on the fact that corporate carbon disclosure is increasingly

becoming a common curriculum that is frequently executed as the deliberate mechanism for both

the external and internal decision-making process. The author in this journal also claimed that

the generation of data produced is maintained to assist the corporate positioning strategically in

relation to opportunities and carbon risks they might face in the near future. Considering the

external aspects, it can be noted that carbon disclosures are used in retaining the promise of

helping in deciding the capital allocation. On the contrary, Fawcett and Parag (2017) denoted

that although organisations are emphasising more on carbon disclosure projects to help society in

gaining ecological balance. However, the businesses are seemed to be getting more inclined

towards their individual profit margin and attaining their bottom lines (Ben-Amar et al. 2017).

The capitals are not extensively used to develop a firm carbon disclosure projects, rather, it had

been used till minimal range that can derive goodwill to the brand in the community (Schiemann

and Sakhel, 2018). On the divergence, Andrew and Cortese (2011) in the chosen article defined

the fact that even though carbon disclosure is presented as equivalent, even essential to economic

exposure, deriving from the regulatory and legitimacy mandate, the designing of the data

generated is quite less accurate than equivalent fiscal exposures. As it is considered helpful at

least for the decisions concerning resource allocation, it required being evaluated alongside the

qualitative traits.

Page 5 of 14

Andrew, J. and Cortese, C. L. (2011) Carbon disclosures: comparability, the Carbon

Disclosure Project and the Greenhouse Gas Protocol, Australian Accounting Business and

Finance Journal, Vol 5(4) pp. 5-18

The specific journals emphasise on the fact that corporate carbon disclosure is increasingly

becoming a common curriculum that is frequently executed as the deliberate mechanism for both

the external and internal decision-making process. The author in this journal also claimed that

the generation of data produced is maintained to assist the corporate positioning strategically in

relation to opportunities and carbon risks they might face in the near future. Considering the

external aspects, it can be noted that carbon disclosures are used in retaining the promise of

helping in deciding the capital allocation. On the contrary, Fawcett and Parag (2017) denoted

that although organisations are emphasising more on carbon disclosure projects to help society in

gaining ecological balance. However, the businesses are seemed to be getting more inclined

towards their individual profit margin and attaining their bottom lines (Ben-Amar et al. 2017).

The capitals are not extensively used to develop a firm carbon disclosure projects, rather, it had

been used till minimal range that can derive goodwill to the brand in the community (Schiemann

and Sakhel, 2018). On the divergence, Andrew and Cortese (2011) in the chosen article defined

the fact that even though carbon disclosure is presented as equivalent, even essential to economic

exposure, deriving from the regulatory and legitimacy mandate, the designing of the data

generated is quite less accurate than equivalent fiscal exposures. As it is considered helpful at

least for the decisions concerning resource allocation, it required being evaluated alongside the

qualitative traits.

Page 5 of 14

Dawkins, C and Fraas, J.W. (2011). Coming Clean: The Impact of Environmental

Performance and Visibility on Corporate Climate Change Disclosure. Journal of Business

Ethics, 100, pp. 303–322

It has been identified from the concerned journals that the increasing degree of stakeholders’ and

institutional pressures are enforcing the global logistics businesses to enhance their carbon

disclosure related information in the market. Dawkins and Fraas (2011) in this article had

highlighted different carbon exposure strategies and responses depending on both the internal

and external pressures. On the other hand, Niehues and Dutzi (2018) determined that the current

research is found limited in terms of categorizing the pressures and its impact on corporate

carbon disclosure policies. Luo (2017) further pointed out that the literature to date has not been

distinguished in this journal between the carbon disclosure policies and the ways it had changed

over time. Nevertheless, the journal has been successful in underlining the fact that the degree of

useful peripheral carbon management functions can be tallied to the extent to which supervisors

provide precedence to contending stakeholders’ statements. It is indicating the notion of

stakeholder salience in the context of stakeholder framework. In the environment amend context,

the extent of salience relies on top of the degree that stakeholders can seize organizations’

responsible for carbon-concerning performances. Moreover, stakeholder salience remains on the

upper side when organizations incorporated an apparent policy with intend of complete

revelation, and it is found on the lower side when stakeholder stress is inept without severe

propositions for businesses legitimacy.

Herold, D., (2018). Has carbon disclosure become more transparent in the global logistics

industry? An investigation of corporate carbon disclosure strategies between 2010 and

2015. Logistics, 2(3), p.13

Page 6 of 14

Performance and Visibility on Corporate Climate Change Disclosure. Journal of Business

Ethics, 100, pp. 303–322

It has been identified from the concerned journals that the increasing degree of stakeholders’ and

institutional pressures are enforcing the global logistics businesses to enhance their carbon

disclosure related information in the market. Dawkins and Fraas (2011) in this article had

highlighted different carbon exposure strategies and responses depending on both the internal

and external pressures. On the other hand, Niehues and Dutzi (2018) determined that the current

research is found limited in terms of categorizing the pressures and its impact on corporate

carbon disclosure policies. Luo (2017) further pointed out that the literature to date has not been

distinguished in this journal between the carbon disclosure policies and the ways it had changed

over time. Nevertheless, the journal has been successful in underlining the fact that the degree of

useful peripheral carbon management functions can be tallied to the extent to which supervisors

provide precedence to contending stakeholders’ statements. It is indicating the notion of

stakeholder salience in the context of stakeholder framework. In the environment amend context,

the extent of salience relies on top of the degree that stakeholders can seize organizations’

responsible for carbon-concerning performances. Moreover, stakeholder salience remains on the

upper side when organizations incorporated an apparent policy with intend of complete

revelation, and it is found on the lower side when stakeholder stress is inept without severe

propositions for businesses legitimacy.

Herold, D., (2018). Has carbon disclosure become more transparent in the global logistics

industry? An investigation of corporate carbon disclosure strategies between 2010 and

2015. Logistics, 2(3), p.13

Page 6 of 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Herold (2018) in this journal aims to evaluate the literature on the context of environmental

policies and exposures by developing businesses visibility an issue. It also focused on conducting

effective interactions with the stakeholders to discuss the environmental performances aimed at

influencing the degree of voluntary climatic change exposures. The literature section of the

article emphasizes that stakeholders had extended argument on the fact that ecological directive

is necessary to impact enhanced ecological functions and majority of the large organizations

presently dedicate a substantial amount of time and resources to weather-related change concerns

and deliberate ecological exposures. On the other hand, Callery and Perkins (2017) determined

that the factor that is often overlooked by the majority of the journals including this one is the

voluntary disclosure and the impact of media visibility. Every year carbon disclosure projects

offer CEO's of MNCs to report their carbon emissions degree and the opportunities and risks

imposed on the company as a result of the climatic change. Following legitimacy approach,

Herold (2018) has been able to highlight the pros and cons management of companies had to

face with their carbon disclosure project reports.

Page 7 of 14

policies and exposures by developing businesses visibility an issue. It also focused on conducting

effective interactions with the stakeholders to discuss the environmental performances aimed at

influencing the degree of voluntary climatic change exposures. The literature section of the

article emphasizes that stakeholders had extended argument on the fact that ecological directive

is necessary to impact enhanced ecological functions and majority of the large organizations

presently dedicate a substantial amount of time and resources to weather-related change concerns

and deliberate ecological exposures. On the other hand, Callery and Perkins (2017) determined

that the factor that is often overlooked by the majority of the journals including this one is the

voluntary disclosure and the impact of media visibility. Every year carbon disclosure projects

offer CEO's of MNCs to report their carbon emissions degree and the opportunities and risks

imposed on the company as a result of the climatic change. Following legitimacy approach,

Herold (2018) has been able to highlight the pros and cons management of companies had to

face with their carbon disclosure project reports.

Page 7 of 14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.0 Proposition and Possible Methodology

It is evident that organizations are practising carbon disclosure functions; however, they are

conducting the effort due to the stakeholders’ and institutional pressures. Hence, the level of

efficacy and dedication on the performances are not relatively apparent.

In the claim of Niehues and Dutzi (2018), the rate of carbon emission is always found high in the

automobile sector. Therefore, in future research, the author would consider the automobile sector

to continue the research work following a similar context. Both survey and descriptive

methodological approach would be followed to determine the carbon disclosure aspect in the

automobile sector and efforts taken by businesses to control it. Hence, with both quantitative and

qualitative approach, the research would be conducted in the future project.

Page 8 of 14

It is evident that organizations are practising carbon disclosure functions; however, they are

conducting the effort due to the stakeholders’ and institutional pressures. Hence, the level of

efficacy and dedication on the performances are not relatively apparent.

In the claim of Niehues and Dutzi (2018), the rate of carbon emission is always found high in the

automobile sector. Therefore, in future research, the author would consider the automobile sector

to continue the research work following a similar context. Both survey and descriptive

methodological approach would be followed to determine the carbon disclosure aspect in the

automobile sector and efforts taken by businesses to control it. Hence, with both quantitative and

qualitative approach, the research would be conducted in the future project.

Page 8 of 14

5.0 Conclusion

Based on the discussion and analysis performed in the preceding sections of the paper, it may be

construed that the environmental legitimacy theory provides a broader base for the corporate

houses to comply with the regulations and directives issued by the rule makers and standard

setters in relation to the environmental safety and security. Usage of carbon and consequent

emission has been a burning issue in the present business scenario especially in the backdrop of

industrialization and globalization (Callery and Perkins, 2017). The carbon disclosure, therefore,

becomes the compliance requirement in the corporate reporting. Therefore, it may be stated that

carbon disclosure ensures the social responsibility of the business as well as transparency in the

corporate reporting framework of the business. Lastly, it may be concluded that a well-designed

corporate reporting with special emphasis on carbon disclosure will significantly contribute

towards the corporate goal of achievement of sustainability on the long-term in most cost and

time efficient manner.

Page 9 of 14

Based on the discussion and analysis performed in the preceding sections of the paper, it may be

construed that the environmental legitimacy theory provides a broader base for the corporate

houses to comply with the regulations and directives issued by the rule makers and standard

setters in relation to the environmental safety and security. Usage of carbon and consequent

emission has been a burning issue in the present business scenario especially in the backdrop of

industrialization and globalization (Callery and Perkins, 2017). The carbon disclosure, therefore,

becomes the compliance requirement in the corporate reporting. Therefore, it may be stated that

carbon disclosure ensures the social responsibility of the business as well as transparency in the

corporate reporting framework of the business. Lastly, it may be concluded that a well-designed

corporate reporting with special emphasis on carbon disclosure will significantly contribute

towards the corporate goal of achievement of sustainability on the long-term in most cost and

time efficient manner.

Page 9 of 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References:

Andrew, J. and Cortese, C. L. (2011) Carbon disclosures: comparability, the Carbon Disclosure

Project and the Greenhouse Gas Protocol, Australian Accounting Business and Finance Journal,

Vol 5(4) pp. 5-18.

Ben-Amar, W., Chang, M. and McIlkenny, P., (2017). Board gender diversity and corporate

response to sustainability initiatives: Evidence from the carbon disclosure project. Journal of

Business Ethics, 142(2), pp.369-383.

Callery, P.J. and Perkins, J., (2017). Unmasking Strategic Disclosure: Evidence from Voluntary

Corporate Carbon Disclosures. In Academy of Management Proceedings (Vol. (2017), No. 1, p.

11436). Briarcliff Manor, NY 10510: Academy of Management.

Dawkins, C and Fraas, J.W. (2011). Coming Clean: The Impact of Environmental Performance

and Visibility on Corporate Climate Change Disclosure. Journal of Business Ethics, 100, pp.

303–322

Fawcett, T. and Parag, Y., (2017). An introduction to personal carbon trading. In Personal

Carbon Trading (pp. 329-338). Routledge.

Herold, D., 2018. Has carbon disclosure become more transparent in the global logistics

industry? An investigation of corporate carbon disclosure strategies between 2010 and

2015. Logistics, 2(3), p.13.

Jiang, M., Zhu, B., Wei, Y.M., Chevallier, J. and He, K., (2018). An intertemporal carbon

emissions trading system with cap adjustment and path control. Energy policy, 122, pp.152-161.

Page 10 of 14

Andrew, J. and Cortese, C. L. (2011) Carbon disclosures: comparability, the Carbon Disclosure

Project and the Greenhouse Gas Protocol, Australian Accounting Business and Finance Journal,

Vol 5(4) pp. 5-18.

Ben-Amar, W., Chang, M. and McIlkenny, P., (2017). Board gender diversity and corporate

response to sustainability initiatives: Evidence from the carbon disclosure project. Journal of

Business Ethics, 142(2), pp.369-383.

Callery, P.J. and Perkins, J., (2017). Unmasking Strategic Disclosure: Evidence from Voluntary

Corporate Carbon Disclosures. In Academy of Management Proceedings (Vol. (2017), No. 1, p.

11436). Briarcliff Manor, NY 10510: Academy of Management.

Dawkins, C and Fraas, J.W. (2011). Coming Clean: The Impact of Environmental Performance

and Visibility on Corporate Climate Change Disclosure. Journal of Business Ethics, 100, pp.

303–322

Fawcett, T. and Parag, Y., (2017). An introduction to personal carbon trading. In Personal

Carbon Trading (pp. 329-338). Routledge.

Herold, D., 2018. Has carbon disclosure become more transparent in the global logistics

industry? An investigation of corporate carbon disclosure strategies between 2010 and

2015. Logistics, 2(3), p.13.

Jiang, M., Zhu, B., Wei, Y.M., Chevallier, J. and He, K., (2018). An intertemporal carbon

emissions trading system with cap adjustment and path control. Energy policy, 122, pp.152-161.

Page 10 of 14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Luo, L., (2017). The influence of institutional contexts on the relationship between voluntary

carbon disclosure and carbon emission performance. Accounting & Finance.

Matthews, H.D., Zickfeld, K., Knutti, R. and Allen, M.R., (2018). Focus on cumulative

emissions, global carbon budgets and the implications for climate mitigation

targets. Environmental Research Letters, 13(1), p.010201.

Michelon, G., Patten, D.M. and Romi, A.M., (2018). Creating Legitimacy for Sustainability

Assurance Practices: Evidence from Sustainability Restatements. European Accounting Review,

pp.1-28.

Niehues, N. and Dutzi, A., (2018). Disclosing the invisible: Measurement and disclosure pitfalls

of carbon dioxide emissions. In Measuring and Controlling Sustainability (pp. 166-178).

Routledge.

Schiemann, F. and Sakhel, A., (2018). Carbon Disclosure, Contextual Factors, and Information

Asymmetry: The Case of Physical Risk Reporting. European Accounting Review, pp.1-28.

Page 11 of 14

carbon disclosure and carbon emission performance. Accounting & Finance.

Matthews, H.D., Zickfeld, K., Knutti, R. and Allen, M.R., (2018). Focus on cumulative

emissions, global carbon budgets and the implications for climate mitigation

targets. Environmental Research Letters, 13(1), p.010201.

Michelon, G., Patten, D.M. and Romi, A.M., (2018). Creating Legitimacy for Sustainability

Assurance Practices: Evidence from Sustainability Restatements. European Accounting Review,

pp.1-28.

Niehues, N. and Dutzi, A., (2018). Disclosing the invisible: Measurement and disclosure pitfalls

of carbon dioxide emissions. In Measuring and Controlling Sustainability (pp. 166-178).

Routledge.

Schiemann, F. and Sakhel, A., (2018). Carbon Disclosure, Contextual Factors, and Information

Asymmetry: The Case of Physical Risk Reporting. European Accounting Review, pp.1-28.

Page 11 of 14

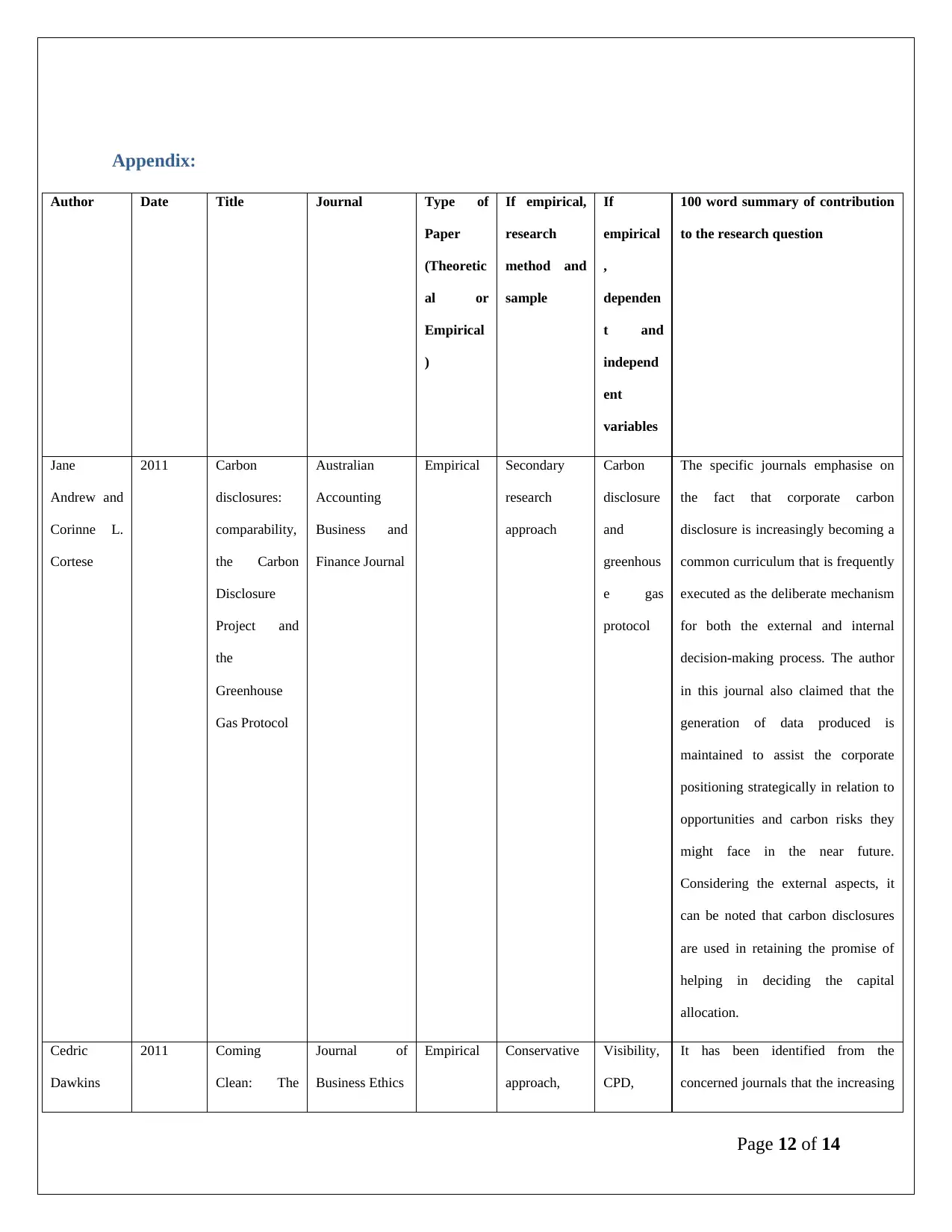

Appendix:

Author Date Title Journal Type of

Paper

(Theoretic

al or

Empirical

)

If empirical,

research

method and

sample

If

empirical

,

dependen

t and

independ

ent

variables

100 word summary of contribution

to the research question

Jane

Andrew and

Corinne L.

Cortese

2011 Carbon

disclosures:

comparability,

the Carbon

Disclosure

Project and

the

Greenhouse

Gas Protocol

Australian

Accounting

Business and

Finance Journal

Empirical Secondary

research

approach

Carbon

disclosure

and

greenhous

e gas

protocol

The specific journals emphasise on

the fact that corporate carbon

disclosure is increasingly becoming a

common curriculum that is frequently

executed as the deliberate mechanism

for both the external and internal

decision-making process. The author

in this journal also claimed that the

generation of data produced is

maintained to assist the corporate

positioning strategically in relation to

opportunities and carbon risks they

might face in the near future.

Considering the external aspects, it

can be noted that carbon disclosures

are used in retaining the promise of

helping in deciding the capital

allocation.

Cedric

Dawkins

2011 Coming

Clean: The

Journal of

Business Ethics

Empirical Conservative

approach,

Visibility,

CPD,

It has been identified from the

concerned journals that the increasing

Page 12 of 14

Author Date Title Journal Type of

Paper

(Theoretic

al or

Empirical

)

If empirical,

research

method and

sample

If

empirical

,

dependen

t and

independ

ent

variables

100 word summary of contribution

to the research question

Jane

Andrew and

Corinne L.

Cortese

2011 Carbon

disclosures:

comparability,

the Carbon

Disclosure

Project and

the

Greenhouse

Gas Protocol

Australian

Accounting

Business and

Finance Journal

Empirical Secondary

research

approach

Carbon

disclosure

and

greenhous

e gas

protocol

The specific journals emphasise on

the fact that corporate carbon

disclosure is increasingly becoming a

common curriculum that is frequently

executed as the deliberate mechanism

for both the external and internal

decision-making process. The author

in this journal also claimed that the

generation of data produced is

maintained to assist the corporate

positioning strategically in relation to

opportunities and carbon risks they

might face in the near future.

Considering the external aspects, it

can be noted that carbon disclosures

are used in retaining the promise of

helping in deciding the capital

allocation.

Cedric

Dawkins

2011 Coming

Clean: The

Journal of

Business Ethics

Empirical Conservative

approach,

Visibility,

CPD,

It has been identified from the

concerned journals that the increasing

Page 12 of 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.