Carbon Emission Reduction: Management Responsibility and Stakeholder Theory

VerifiedAdded on 2023/06/03

|21

|4957

|461

AI Summary

This paper investigates the relationship between management responsibility and stakeholder theory in reducing carbon emissions. The study uses ANOVA to test the hypothesis that higher influence of Board Responsibility for climate change in an organization leads to higher carbon emission reduction. The paper also includes a literature review, conceptual model, data collection, and descriptive and inferential analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MGT723 Research Project

Assessment Task 2: Data Collection

Student Name: Diksha Gautam

Title: Carbon Emission Reduction

Submission Date: 14/09/2018

Assessment Task 2: Data Collection

Student Name: Diksha Gautam

Title: Carbon Emission Reduction

Submission Date: 14/09/2018

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I

understand that the source of ideas must be referenced and that quotation marks and a

reference are required when directly quoting anyone else’s words.

Note that you are permitted to change your research question and hypothesis as your

research project develops over the semester. If you make changes you should note,

however, that you will need to update your conceptual model, hypothesis, theoretical

constructs and proxy measures accordingly. Although these not assessed directly, your

submission in Task 2 and Task 3 will be evaluated in the context of your stated conceptual

model etc.

2 | P a g e

I certify that I have carefully reviewed the university’s academic misconduct policy. I

understand that the source of ideas must be referenced and that quotation marks and a

reference are required when directly quoting anyone else’s words.

Note that you are permitted to change your research question and hypothesis as your

research project develops over the semester. If you make changes you should note,

however, that you will need to update your conceptual model, hypothesis, theoretical

constructs and proxy measures accordingly. Although these not assessed directly, your

submission in Task 2 and Task 3 will be evaluated in the context of your stated conceptual

model etc.

2 | P a g e

Introduction

This paper talks about does higher influence of Management’s Responsibility for climate

change within an Organization helps to reduce carbon emission. Management are ones who

handle organizations. Managers and Board of Director (BOD) are expected to reduce

emission in the organization and provide awareness of the physical, political and social risks

originate from the impacts of climate change (Wittneben and Kiyar, 2018)

Literature Review – Summary

Carbon emissions are increasing rapidly in developing countries because of the international

climate change mitigation treaty of Kyoto Protocol. There is increase from 33% to 40% in

1990 and 1997 respectively. Kyoto Protocol is negotiated in 1997 and it commits signatories

to achieve specific greenhouse gas (GHG) or carbon emission reduction targets (Kalu, Buang

and Aliagha, 2016). The four-determinant factor such as Social factor, economic factor, the

financial market factor and the institutional factor are included for carbon emissions

reduction. Because of the attendant implication of climate disasters developing countries

like India, China, Colombia, Malaysia and others must face increasing rate of carbon

emissions which can be move up to 70%. Due to this, developing country should make

contribution in any form of mitigation program for the achievement of success (Kalu, Buang

and Aliagha, 2016).

Management responsibilities are one due to which there will be reduction in carbon

emission. Due to the proper management actions it helps to reduce carbon emission and

helps to observe how company can respond pressures in a global organization (Lane, 2010).

If there will be explore of management actions by the Board of Director or by the manager

of the organization related with air travel of employees, by drawing how managerial

practice can affect organization’s environmental impact (Fraser, 2012). In London,

management introduce an internal EMCS to reduce carbon emission for Beta’s Company. In

that analysis they also compare that whether management incentives influence travellers or

not due to which there will be reduction in carbon emission. When management actions

were taken in the Beta’s company by following the steps like understanding the significant

clients, identifying travellers in terms of carbon impact, producing carbon impact statement

3 | P a g e

This paper talks about does higher influence of Management’s Responsibility for climate

change within an Organization helps to reduce carbon emission. Management are ones who

handle organizations. Managers and Board of Director (BOD) are expected to reduce

emission in the organization and provide awareness of the physical, political and social risks

originate from the impacts of climate change (Wittneben and Kiyar, 2018)

Literature Review – Summary

Carbon emissions are increasing rapidly in developing countries because of the international

climate change mitigation treaty of Kyoto Protocol. There is increase from 33% to 40% in

1990 and 1997 respectively. Kyoto Protocol is negotiated in 1997 and it commits signatories

to achieve specific greenhouse gas (GHG) or carbon emission reduction targets (Kalu, Buang

and Aliagha, 2016). The four-determinant factor such as Social factor, economic factor, the

financial market factor and the institutional factor are included for carbon emissions

reduction. Because of the attendant implication of climate disasters developing countries

like India, China, Colombia, Malaysia and others must face increasing rate of carbon

emissions which can be move up to 70%. Due to this, developing country should make

contribution in any form of mitigation program for the achievement of success (Kalu, Buang

and Aliagha, 2016).

Management responsibilities are one due to which there will be reduction in carbon

emission. Due to the proper management actions it helps to reduce carbon emission and

helps to observe how company can respond pressures in a global organization (Lane, 2010).

If there will be explore of management actions by the Board of Director or by the manager

of the organization related with air travel of employees, by drawing how managerial

practice can affect organization’s environmental impact (Fraser, 2012). In London,

management introduce an internal EMCS to reduce carbon emission for Beta’s Company. In

that analysis they also compare that whether management incentives influence travellers or

not due to which there will be reduction in carbon emission. When management actions

were taken in the Beta’s company by following the steps like understanding the significant

clients, identifying travellers in terms of carbon impact, producing carbon impact statement

3 | P a g e

with individual traveller, identifying significant travel routes in terms of carbon impact, to

reduce journey work with top travellers, by introducing incentive scheme to encourage

travellers, increasing the awareness as well as use of technology and lastly improving use of

communication channels there was reduction in carbon emission. Therefore, due to

management responsibility in an organization by following management incentive there will

be reduction in carbon emission (Giacomo, Guthrie and Farneti, 2017).

Stakeholders are the individuals who can affect the firm or who the actions of the

corporation can affect. Stakeholders comprise the workers, clients, competitors, and

creditors. The stakeholder theory posits that the corporations are responsible to not only

shareholders but to a group of stakeholders, which is broad (Bridoux and Stoelhorst, 2014).

According to Bridoux and Stoelhorst (2014), Edward Freeman is the one who proposed the

stakeholder theory. Edward Freeman acknowledged the theory as an essential component

of Corporate Social Responsibility. Corporate social responsibility (CSR) identifies the

companies’ responsibilities, which are philanthropic, ethical, and economic. The stakeholder

theory posits that the managers of the companies are supposed to take care of all the

stakeholders of the firm when making governance decisions. The managers should reduce

conflict that exists between the interests of the stakeholders (Kuo, Yah and Yu, 2012)

Therefore, from this review we can conclude that there is relation between management

responsibilities for climate change in an organization, relation with stakeholder to reduce

carbon emission.

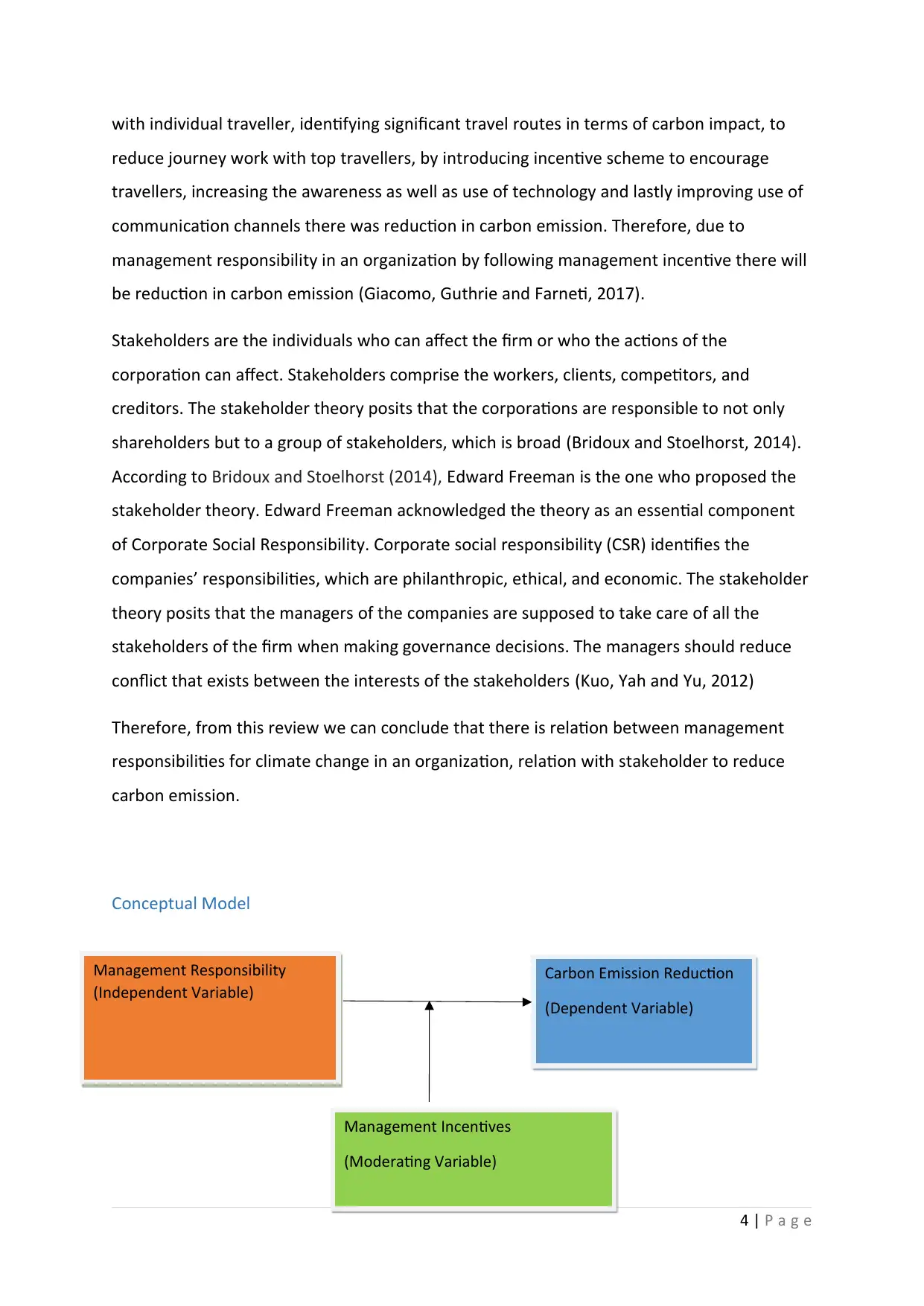

Conceptual Model

4 | P a g e

Management Responsibility

(Independent Variable)

Carbon Emission Reduction

(Dependent Variable)

Management Incentives

(Moderating Variable)

reduce journey work with top travellers, by introducing incentive scheme to encourage

travellers, increasing the awareness as well as use of technology and lastly improving use of

communication channels there was reduction in carbon emission. Therefore, due to

management responsibility in an organization by following management incentive there will

be reduction in carbon emission (Giacomo, Guthrie and Farneti, 2017).

Stakeholders are the individuals who can affect the firm or who the actions of the

corporation can affect. Stakeholders comprise the workers, clients, competitors, and

creditors. The stakeholder theory posits that the corporations are responsible to not only

shareholders but to a group of stakeholders, which is broad (Bridoux and Stoelhorst, 2014).

According to Bridoux and Stoelhorst (2014), Edward Freeman is the one who proposed the

stakeholder theory. Edward Freeman acknowledged the theory as an essential component

of Corporate Social Responsibility. Corporate social responsibility (CSR) identifies the

companies’ responsibilities, which are philanthropic, ethical, and economic. The stakeholder

theory posits that the managers of the companies are supposed to take care of all the

stakeholders of the firm when making governance decisions. The managers should reduce

conflict that exists between the interests of the stakeholders (Kuo, Yah and Yu, 2012)

Therefore, from this review we can conclude that there is relation between management

responsibilities for climate change in an organization, relation with stakeholder to reduce

carbon emission.

Conceptual Model

4 | P a g e

Management Responsibility

(Independent Variable)

Carbon Emission Reduction

(Dependent Variable)

Management Incentives

(Moderating Variable)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hypotheses

Higher the influence of Board Responsibility for the climate change in an organization higher

will be carbon emission reduction.

Data Collection

This paper uses descriptive and inferential statistics to investigate the relationship between

dependent and independent variables. The dependent variable is Carbon Emission

Reduction and independent variable is Board Responsible. Management Incentive is

moderating variable.

For the propose of this paper, only 5 most polluter’s countries China, India, Japan, Russia

and USA are included and rest are excluded from the data. Among 55 countries only 5

countries are taken in this paper. From 2011-2017 data are eliminated from 2294 samples

to 847. Data are selected from Carbon emission reduction for the year 2012. All the missing

data, unappropriated data are also deleted from the excel sheet.

5 | P a g e

Higher the influence of Board Responsibility for the climate change in an organization higher

will be carbon emission reduction.

Data Collection

This paper uses descriptive and inferential statistics to investigate the relationship between

dependent and independent variables. The dependent variable is Carbon Emission

Reduction and independent variable is Board Responsible. Management Incentive is

moderating variable.

For the propose of this paper, only 5 most polluter’s countries China, India, Japan, Russia

and USA are included and rest are excluded from the data. Among 55 countries only 5

countries are taken in this paper. From 2011-2017 data are eliminated from 2294 samples

to 847. Data are selected from Carbon emission reduction for the year 2012. All the missing

data, unappropriated data are also deleted from the excel sheet.

5 | P a g e

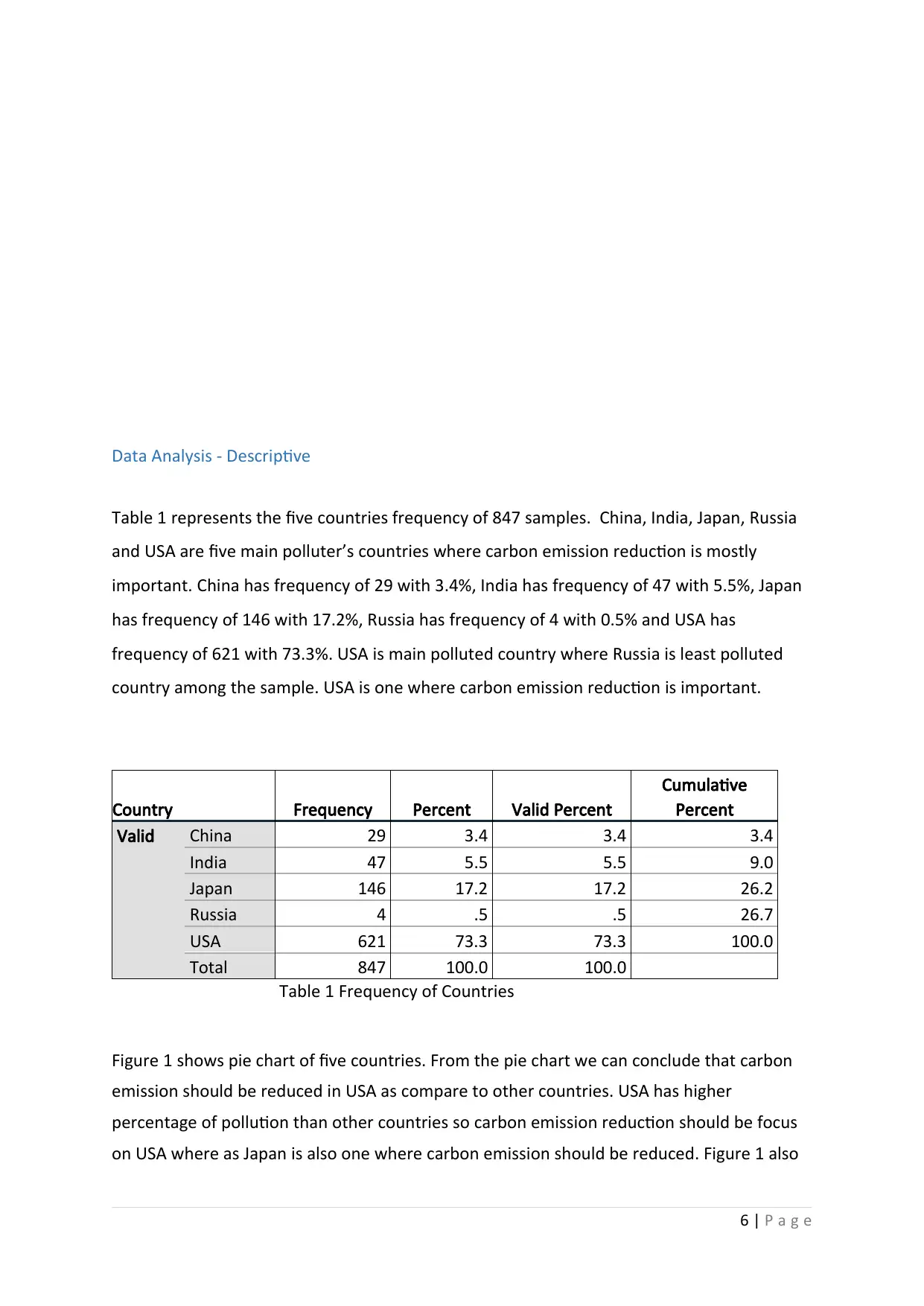

Data Analysis - Descriptive

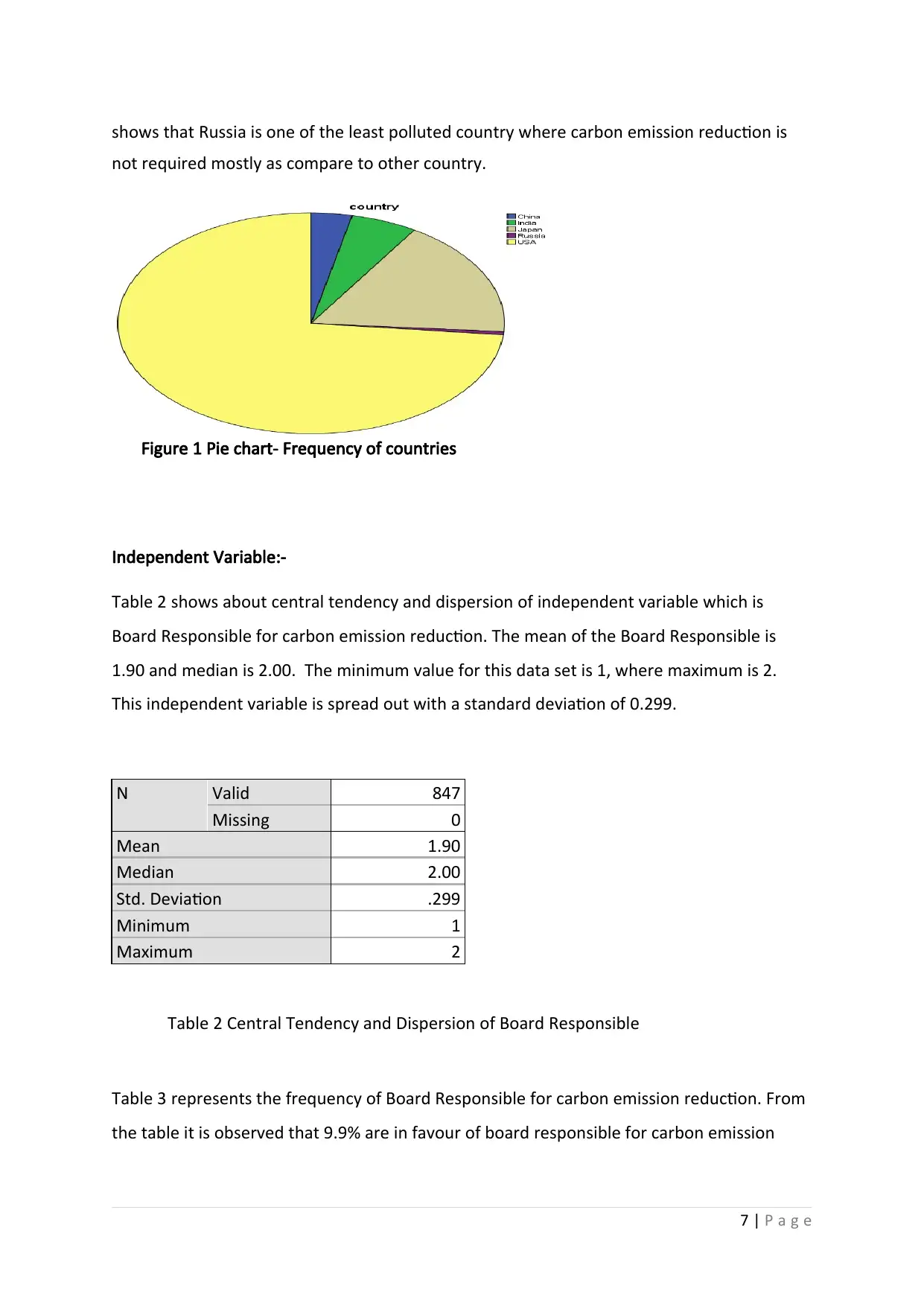

Table 1 represents the five countries frequency of 847 samples. China, India, Japan, Russia

and USA are five main polluter’s countries where carbon emission reduction is mostly

important. China has frequency of 29 with 3.4%, India has frequency of 47 with 5.5%, Japan

has frequency of 146 with 17.2%, Russia has frequency of 4 with 0.5% and USA has

frequency of 621 with 73.3%. USA is main polluted country where Russia is least polluted

country among the sample. USA is one where carbon emission reduction is important.

Country Frequency Percent Valid Percent

Cumulative

Percent

Valid China 29 3.4 3.4 3.4

India 47 5.5 5.5 9.0

Japan 146 17.2 17.2 26.2

Russia 4 .5 .5 26.7

USA 621 73.3 73.3 100.0

Total 847 100.0 100.0

Table 1 Frequency of Countries

Figure 1 shows pie chart of five countries. From the pie chart we can conclude that carbon

emission should be reduced in USA as compare to other countries. USA has higher

percentage of pollution than other countries so carbon emission reduction should be focus

on USA where as Japan is also one where carbon emission should be reduced. Figure 1 also

6 | P a g e

Table 1 represents the five countries frequency of 847 samples. China, India, Japan, Russia

and USA are five main polluter’s countries where carbon emission reduction is mostly

important. China has frequency of 29 with 3.4%, India has frequency of 47 with 5.5%, Japan

has frequency of 146 with 17.2%, Russia has frequency of 4 with 0.5% and USA has

frequency of 621 with 73.3%. USA is main polluted country where Russia is least polluted

country among the sample. USA is one where carbon emission reduction is important.

Country Frequency Percent Valid Percent

Cumulative

Percent

Valid China 29 3.4 3.4 3.4

India 47 5.5 5.5 9.0

Japan 146 17.2 17.2 26.2

Russia 4 .5 .5 26.7

USA 621 73.3 73.3 100.0

Total 847 100.0 100.0

Table 1 Frequency of Countries

Figure 1 shows pie chart of five countries. From the pie chart we can conclude that carbon

emission should be reduced in USA as compare to other countries. USA has higher

percentage of pollution than other countries so carbon emission reduction should be focus

on USA where as Japan is also one where carbon emission should be reduced. Figure 1 also

6 | P a g e

shows that Russia is one of the least polluted country where carbon emission reduction is

not required mostly as compare to other country.

Figure 1 Pie chart- Frequency of countries

Independent Variable:-

Table 2 shows about central tendency and dispersion of independent variable which is

Board Responsible for carbon emission reduction. The mean of the Board Responsible is

1.90 and median is 2.00. The minimum value for this data set is 1, where maximum is 2.

This independent variable is spread out with a standard deviation of 0.299.

Table 2 Central Tendency and Dispersion of Board Responsible

Table 3 represents the frequency of Board Responsible for carbon emission reduction. From

the table it is observed that 9.9% are in favour of board responsible for carbon emission

7 | P a g e

N Valid 847

Missing 0

Mean 1.90

Median 2.00

Std. Deviation .299

Minimum 1

Maximum 2

not required mostly as compare to other country.

Figure 1 Pie chart- Frequency of countries

Independent Variable:-

Table 2 shows about central tendency and dispersion of independent variable which is

Board Responsible for carbon emission reduction. The mean of the Board Responsible is

1.90 and median is 2.00. The minimum value for this data set is 1, where maximum is 2.

This independent variable is spread out with a standard deviation of 0.299.

Table 2 Central Tendency and Dispersion of Board Responsible

Table 3 represents the frequency of Board Responsible for carbon emission reduction. From

the table it is observed that 9.9% are in favour of board responsible for carbon emission

7 | P a g e

N Valid 847

Missing 0

Mean 1.90

Median 2.00

Std. Deviation .299

Minimum 1

Maximum 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reduction where 90.1% are in favour of individual, other manager and senior manager who

are responsible for carbon emission reduction.

Board Responsible Yes-1, N0-2

Frequency Percent

Valid

Percent

Cumulative

Percent

Valid 1 84 9.9 9.9 9.9

2 763 90.1 90.1 100.0

Total 847 100.0 100.0

Table 3 Frequency of Board Responsible

Figure 2 Figure 2represents pie chart of the frequency of Board Responsible for Carbon

emission reduction. From the figure it can be concluded that Board responsible yes-1 has

less percentage as compare to Board

responsible No-2. The sample shows that

less percentage are in favour of Board

responsible for carbon emission reduction

where higher percentage are in favour of

other to reduce carbon emission.

Figure 2

Pie chart- Frequency of Board Responsible

Dependent Variable:-

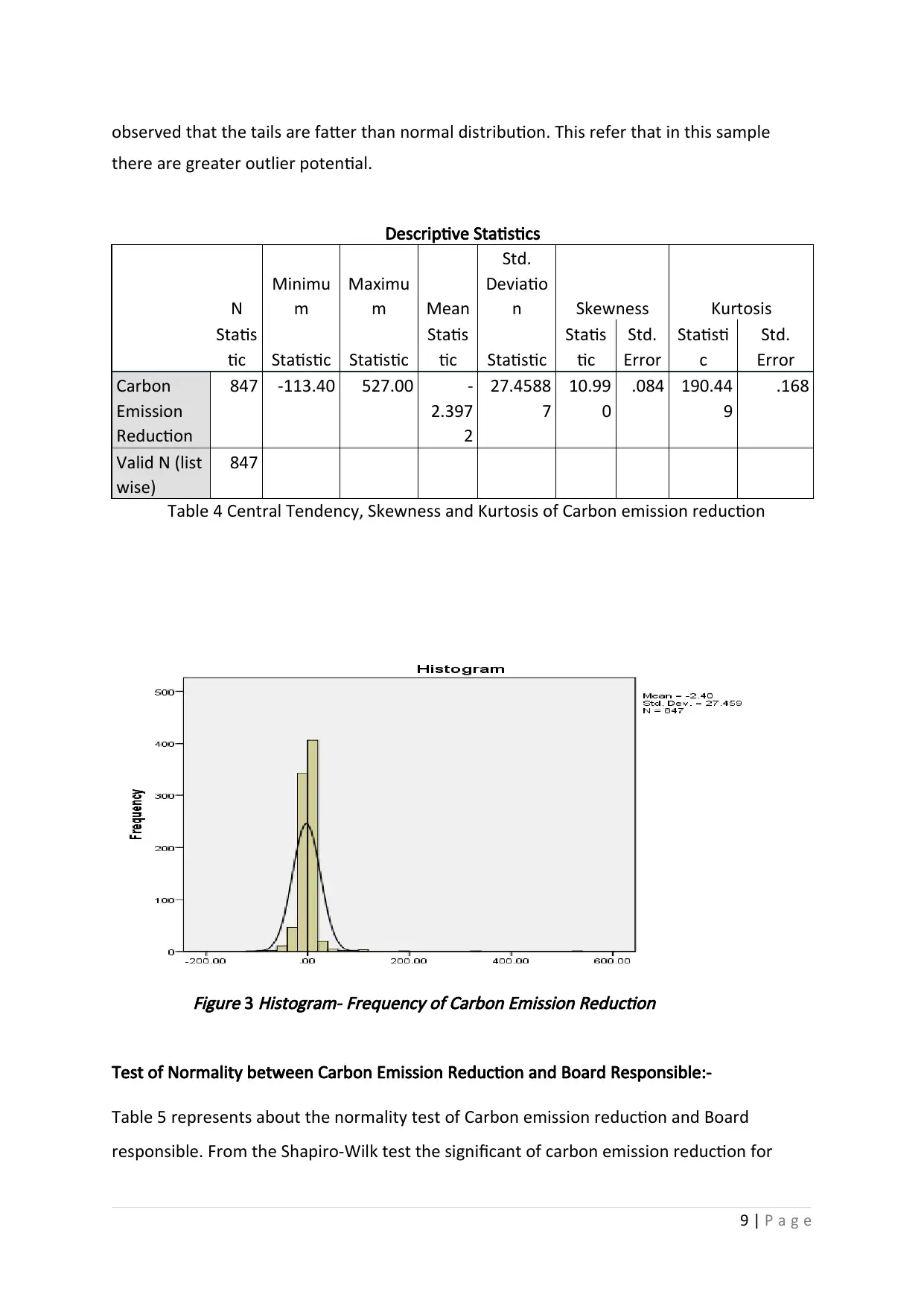

Table 4 shows descriptive Statistics of Carbon Emission Reduction which is dependent

variable. From the sample of 847, the mean of Carbon emission reduction is -2.3972 where

the minimum statistics for this set of data is -113.40 and maximum is 527.00. From the table

we can see carbon emission reduction has a skewness of 10.990 and Kurtosis of 190.449.

The value of the skewness should be between 3 and -3 but in this data it exceed to 3

because of the higher sample. If there is exceed of 3 than kurtosis is known as leptokurtic.

Figure 3 represents histogram of Carbon emission reduction. From figure it can be also

8 | P a g e

are responsible for carbon emission reduction.

Board Responsible Yes-1, N0-2

Frequency Percent

Valid

Percent

Cumulative

Percent

Valid 1 84 9.9 9.9 9.9

2 763 90.1 90.1 100.0

Total 847 100.0 100.0

Table 3 Frequency of Board Responsible

Figure 2 Figure 2represents pie chart of the frequency of Board Responsible for Carbon

emission reduction. From the figure it can be concluded that Board responsible yes-1 has

less percentage as compare to Board

responsible No-2. The sample shows that

less percentage are in favour of Board

responsible for carbon emission reduction

where higher percentage are in favour of

other to reduce carbon emission.

Figure 2

Pie chart- Frequency of Board Responsible

Dependent Variable:-

Table 4 shows descriptive Statistics of Carbon Emission Reduction which is dependent

variable. From the sample of 847, the mean of Carbon emission reduction is -2.3972 where

the minimum statistics for this set of data is -113.40 and maximum is 527.00. From the table

we can see carbon emission reduction has a skewness of 10.990 and Kurtosis of 190.449.

The value of the skewness should be between 3 and -3 but in this data it exceed to 3

because of the higher sample. If there is exceed of 3 than kurtosis is known as leptokurtic.

Figure 3 represents histogram of Carbon emission reduction. From figure it can be also

8 | P a g e

observed that the tails are fatter than normal distribution. This refer that in this sample

there are greater outlier potential.

Descriptive Statistics

N

Minimu

m

Maximu

m Mean

Std.

Deviatio

n Skewness Kurtosis

Statis

tic Statistic Statistic

Statis

tic Statistic

Statis

tic

Std.

Error

Statisti

c

Std.

Error

Carbon

Emission

Reduction

847 -113.40 527.00 -

2.397

2

27.4588

7

10.99

0

.084 190.44

9

.168

Valid N (list

wise)

847

Table 4 Central Tendency, Skewness and Kurtosis of Carbon emission reduction

Figure 3

Histogram- Frequency of Carbon Emission Reduction

Test of Normality between Carbon Emission Reduction and Board Responsible:-

Table 5 represents about the normality test of Carbon emission reduction and Board

responsible. From the Shapiro-Wilk test the significant of carbon emission reduction for

9 | P a g e

there are greater outlier potential.

Descriptive Statistics

N

Minimu

m

Maximu

m Mean

Std.

Deviatio

n Skewness Kurtosis

Statis

tic Statistic Statistic

Statis

tic Statistic

Statis

tic

Std.

Error

Statisti

c

Std.

Error

Carbon

Emission

Reduction

847 -113.40 527.00 -

2.397

2

27.4588

7

10.99

0

.084 190.44

9

.168

Valid N (list

wise)

847

Table 4 Central Tendency, Skewness and Kurtosis of Carbon emission reduction

Figure 3

Histogram- Frequency of Carbon Emission Reduction

Test of Normality between Carbon Emission Reduction and Board Responsible:-

Table 5 represents about the normality test of Carbon emission reduction and Board

responsible. From the Shapiro-Wilk test the significant of carbon emission reduction for

9 | P a g e

board responsible 1-yes has 0.000 which is less than 0.05 so null hypothesis is rejected

whereas for carbon emission reduction for board responsible 2-No has also 0.000 which is

also less than 0.05 due to this null hypothesis is rejected.

Tests of Normality

Board

Responsible Yes-

1, N0-2

Kolmogorov-Smirnova Shapiro-Wilk

Statistic df Sig. Statistic df Sig.

Carbon Emission

Reduction

1 .501 84 .000 .232 84 .000

2 .283 763 .000 .390 763 .000

a. Lilliefors Significance Correction

Table 5 Test of Normality of Carbon emission reduction for Board Responsible

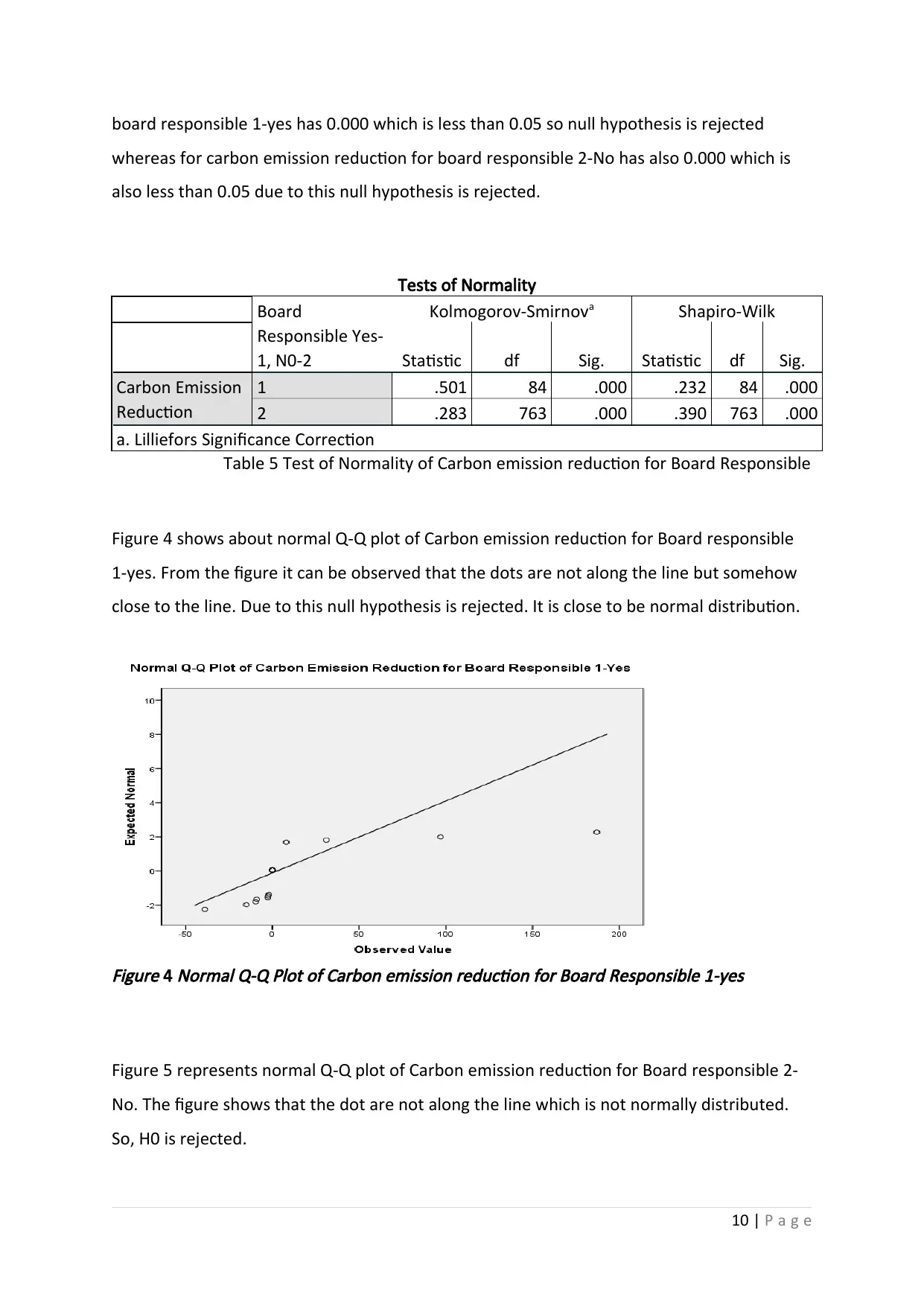

Figure 4 shows about normal Q-Q plot of Carbon emission reduction for Board responsible

1-yes. From the figure it can be observed that the dots are not along the line but somehow

close to the line. Due to this null hypothesis is rejected. It is close to be normal distribution.

Figure 4

Normal Q-Q Plot of Carbon emission reduction for Board Responsible 1-yes

Figure 5 represents normal Q-Q plot of Carbon emission reduction for Board responsible 2-

No. The figure shows that the dot are not along the line which is not normally distributed.

So, H0 is rejected.

10 | P a g e

whereas for carbon emission reduction for board responsible 2-No has also 0.000 which is

also less than 0.05 due to this null hypothesis is rejected.

Tests of Normality

Board

Responsible Yes-

1, N0-2

Kolmogorov-Smirnova Shapiro-Wilk

Statistic df Sig. Statistic df Sig.

Carbon Emission

Reduction

1 .501 84 .000 .232 84 .000

2 .283 763 .000 .390 763 .000

a. Lilliefors Significance Correction

Table 5 Test of Normality of Carbon emission reduction for Board Responsible

Figure 4 shows about normal Q-Q plot of Carbon emission reduction for Board responsible

1-yes. From the figure it can be observed that the dots are not along the line but somehow

close to the line. Due to this null hypothesis is rejected. It is close to be normal distribution.

Figure 4

Normal Q-Q Plot of Carbon emission reduction for Board Responsible 1-yes

Figure 5 represents normal Q-Q plot of Carbon emission reduction for Board responsible 2-

No. The figure shows that the dot are not along the line which is not normally distributed.

So, H0 is rejected.

10 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Figure 5

Normal Q-Q Plot of Carbon emission reduction for Board Responsible 2-No

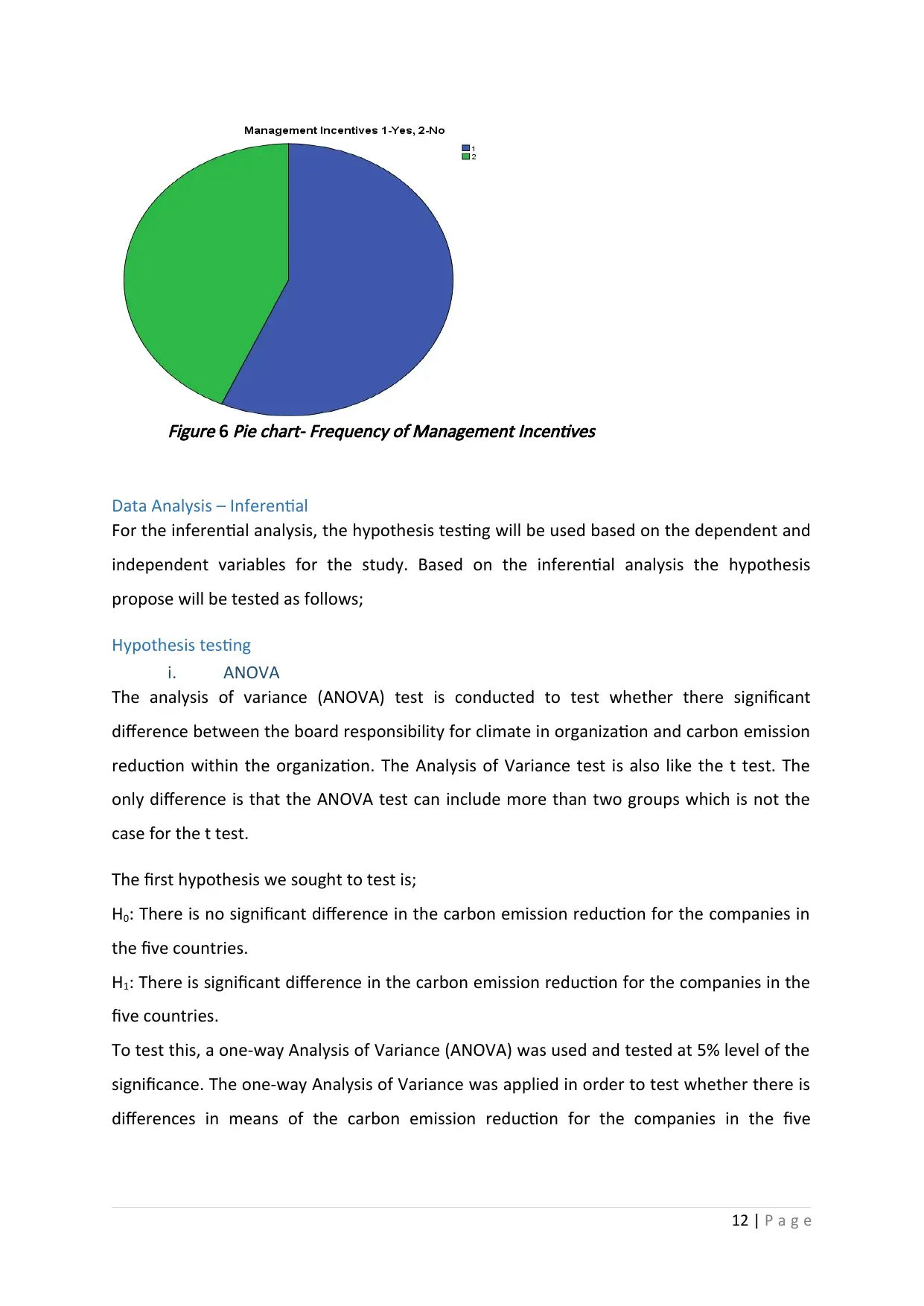

Moderating Variable:-

Table 6 represents frequency of management incentives of 847 sample. From the table we

can observed that frequency of 480 with 56.7% are in favour of management incentives

which helps to reduce carbon emission and 367 with 43.3% are not in favour. But, the tables

shows that if there will be increase in management incentive than there will be reduction in

carbon emission.

Management Incentives

Frequenc

y Percent

Valid

Percent

Cumulative

Percent

Valid 1 480 56.7 56.7 56.7

2 367 43.3 43.3 100.0

Total 847 100.0 100.0

Table 6 Frequency of management incentives

Figure 6 represents pie chart of management incentives. It shows that from 847 sample the

response of yes-1 is in the favour of management incentives to reduce carbon emission

reduction.

11 | P a g e

Normal Q-Q Plot of Carbon emission reduction for Board Responsible 2-No

Moderating Variable:-

Table 6 represents frequency of management incentives of 847 sample. From the table we

can observed that frequency of 480 with 56.7% are in favour of management incentives

which helps to reduce carbon emission and 367 with 43.3% are not in favour. But, the tables

shows that if there will be increase in management incentive than there will be reduction in

carbon emission.

Management Incentives

Frequenc

y Percent

Valid

Percent

Cumulative

Percent

Valid 1 480 56.7 56.7 56.7

2 367 43.3 43.3 100.0

Total 847 100.0 100.0

Table 6 Frequency of management incentives

Figure 6 represents pie chart of management incentives. It shows that from 847 sample the

response of yes-1 is in the favour of management incentives to reduce carbon emission

reduction.

11 | P a g e

Figure 6

Pie chart- Frequency of Management Incentives

Data Analysis – Inferential

For the inferential analysis, the hypothesis testing will be used based on the dependent and

independent variables for the study. Based on the inferential analysis the hypothesis

propose will be tested as follows;

Hypothesis testing

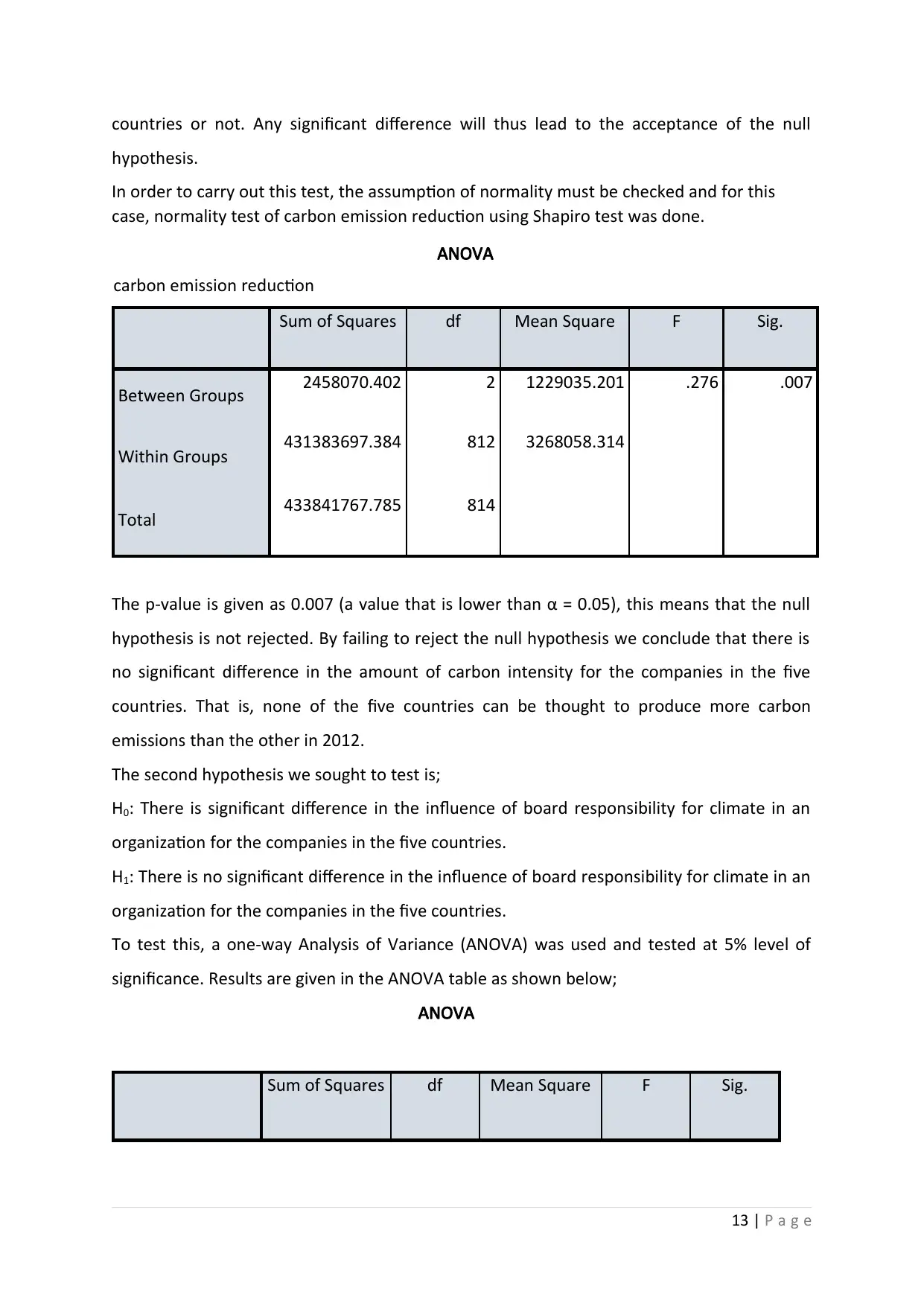

i. ANOVA

The analysis of variance (ANOVA) test is conducted to test whether there significant

difference between the board responsibility for climate in organization and carbon emission

reduction within the organization. The Analysis of Variance test is also like the t test. The

only difference is that the ANOVA test can include more than two groups which is not the

case for the t test.

The first hypothesis we sought to test is;

H0: There is no significant difference in the carbon emission reduction for the companies in

the five countries.

H1: There is significant difference in the carbon emission reduction for the companies in the

five countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of the

significance. The one-way Analysis of Variance was applied in order to test whether there is

differences in means of the carbon emission reduction for the companies in the five

12 | P a g e

Pie chart- Frequency of Management Incentives

Data Analysis – Inferential

For the inferential analysis, the hypothesis testing will be used based on the dependent and

independent variables for the study. Based on the inferential analysis the hypothesis

propose will be tested as follows;

Hypothesis testing

i. ANOVA

The analysis of variance (ANOVA) test is conducted to test whether there significant

difference between the board responsibility for climate in organization and carbon emission

reduction within the organization. The Analysis of Variance test is also like the t test. The

only difference is that the ANOVA test can include more than two groups which is not the

case for the t test.

The first hypothesis we sought to test is;

H0: There is no significant difference in the carbon emission reduction for the companies in

the five countries.

H1: There is significant difference in the carbon emission reduction for the companies in the

five countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of the

significance. The one-way Analysis of Variance was applied in order to test whether there is

differences in means of the carbon emission reduction for the companies in the five

12 | P a g e

countries or not. Any significant difference will thus lead to the acceptance of the null

hypothesis.

In order to carry out this test, the assumption of normality must be checked and for this

case, normality test of carbon emission reduction using Shapiro test was done.

ANOVA

carbon emission reduction

Sum of Squares df Mean Square F Sig.

Between Groups 2458070.402 2 1229035.201 .276 .007

Within Groups 431383697.384 812 3268058.314

Total 433841767.785 814

The p-value is given as 0.007 (a value that is lower than α = 0.05), this means that the null

hypothesis is not rejected. By failing to reject the null hypothesis we conclude that there is

no significant difference in the amount of carbon intensity for the companies in the five

countries. That is, none of the five countries can be thought to produce more carbon

emissions than the other in 2012.

The second hypothesis we sought to test is;

H0: There is significant difference in the influence of board responsibility for climate in an

organization for the companies in the five countries.

H1: There is no significant difference in the influence of board responsibility for climate in an

organization for the companies in the five countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance. Results are given in the ANOVA table as shown below;

ANOVA

Sum of Squares df Mean Square F Sig.

13 | P a g e

hypothesis.

In order to carry out this test, the assumption of normality must be checked and for this

case, normality test of carbon emission reduction using Shapiro test was done.

ANOVA

carbon emission reduction

Sum of Squares df Mean Square F Sig.

Between Groups 2458070.402 2 1229035.201 .276 .007

Within Groups 431383697.384 812 3268058.314

Total 433841767.785 814

The p-value is given as 0.007 (a value that is lower than α = 0.05), this means that the null

hypothesis is not rejected. By failing to reject the null hypothesis we conclude that there is

no significant difference in the amount of carbon intensity for the companies in the five

countries. That is, none of the five countries can be thought to produce more carbon

emissions than the other in 2012.

The second hypothesis we sought to test is;

H0: There is significant difference in the influence of board responsibility for climate in an

organization for the companies in the five countries.

H1: There is no significant difference in the influence of board responsibility for climate in an

organization for the companies in the five countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance. Results are given in the ANOVA table as shown below;

ANOVA

Sum of Squares df Mean Square F Sig.

13 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Between Groups 538.960 2 269.480 .302 .004

Within Groups 185687.185 808 892.727

Total 186226.145 810

Again, the p-value is given as 0.004 which is a value lower than alpha (α) = 0.05. This

therefore implies that the null hypothesis is not rejected. That is, none of the five countries

can be thought to have had a significant change in carbon emissions than the other in 2012.

T-test

The second inferential analysis that was conducted out abased on the hypothesis under

consideration. The T- test is conducted to examine whether there is significance difference

in the mean value between the two different groups. In the current research t-test will help

to analyse the difference in the carbon emission reduction in different types of organization

and for different countries.

The third hypothesis we wish to test is based on the moderating variable which is

management incentive to the employees. The hypothesis to be tested is whether there is

significant difference in the carbon emission reduction between the companies that provide

incentives for the management of climate change issues and those that do not provide

management incentives. The following hypothesis was tested at 5% level significance using

an independent samples t-test.

H0: There is no significant difference in the carbon emissions for the companies that provide

incentives for the management of climate change issues and those that do not provide.

H1: There is significant difference in the carbon emissions for the companies that provide

incentives for the management of climate change issues and those that do not provide. The

results are presented in the table below;

Group Statistics

Management

incentives

N Mean Std.

Deviation

Std. Error

Mean

Yes 523 323.4760 1749.18341 194.35371

14 | P a g e

Within Groups 185687.185 808 892.727

Total 186226.145 810

Again, the p-value is given as 0.004 which is a value lower than alpha (α) = 0.05. This

therefore implies that the null hypothesis is not rejected. That is, none of the five countries

can be thought to have had a significant change in carbon emissions than the other in 2012.

T-test

The second inferential analysis that was conducted out abased on the hypothesis under

consideration. The T- test is conducted to examine whether there is significance difference

in the mean value between the two different groups. In the current research t-test will help

to analyse the difference in the carbon emission reduction in different types of organization

and for different countries.

The third hypothesis we wish to test is based on the moderating variable which is

management incentive to the employees. The hypothesis to be tested is whether there is

significant difference in the carbon emission reduction between the companies that provide

incentives for the management of climate change issues and those that do not provide

management incentives. The following hypothesis was tested at 5% level significance using

an independent samples t-test.

H0: There is no significant difference in the carbon emissions for the companies that provide

incentives for the management of climate change issues and those that do not provide.

H1: There is significant difference in the carbon emissions for the companies that provide

incentives for the management of climate change issues and those that do not provide. The

results are presented in the table below;

Group Statistics

Management

incentives

N Mean Std.

Deviation

Std. Error

Mean

Yes 523 323.4760 1749.18341 194.35371

14 | P a g e

No 307 360.2330 1888.52836 256.99616

Independent Samples Test

Levene's Test

for Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differe

nce

Std.

Error

Differe

nce

95%

Confidence

Interval of the

Difference

Lower Upper

Intensi

ty

Equal

variances

assumed

.084 .772 -.11

6

133 .908 -36.76 317 -664 591

Equal

variances not

assumed

-.11

4

107.63

5

.909 -36.76 322 -675 602

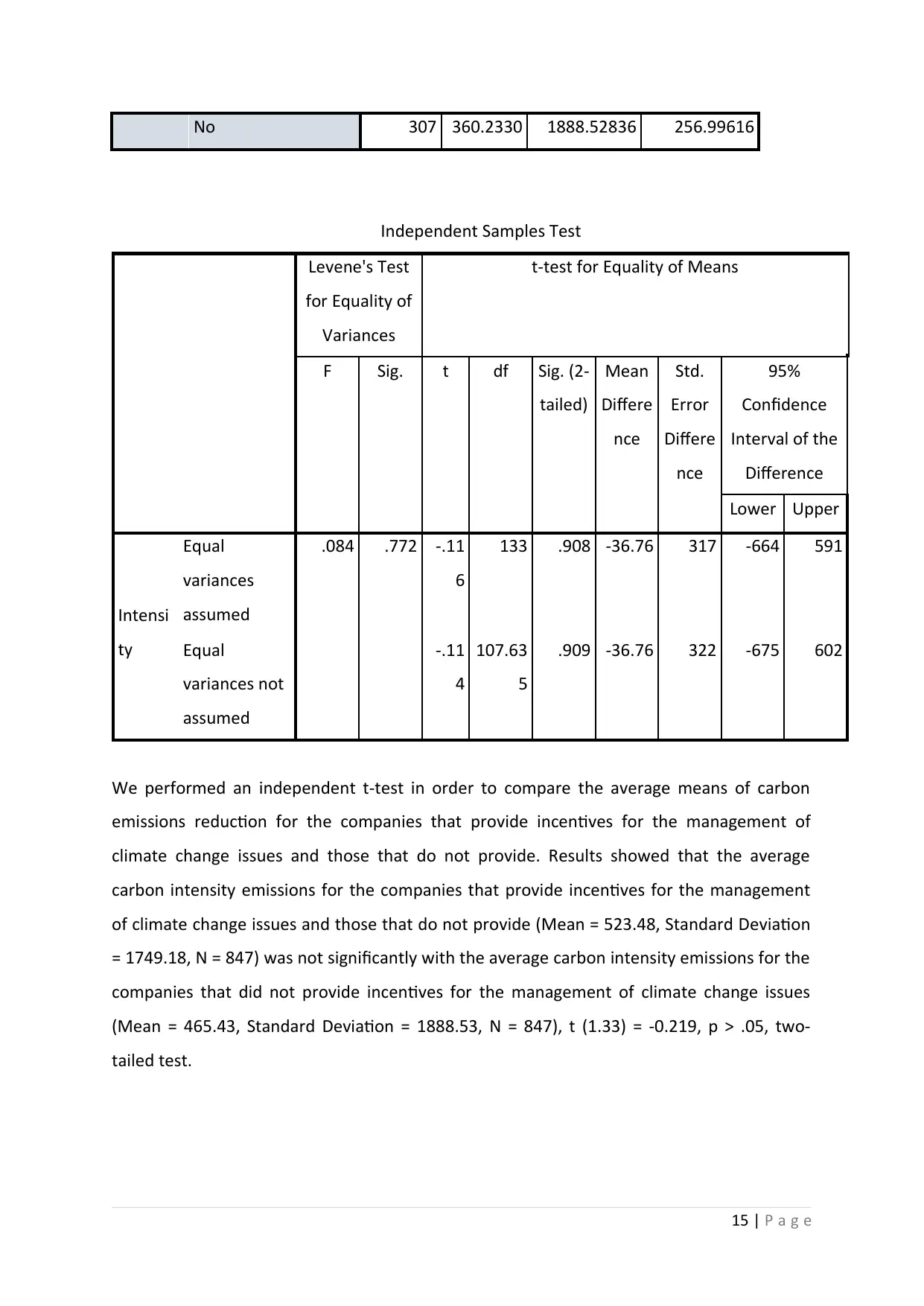

We performed an independent t-test in order to compare the average means of carbon

emissions reduction for the companies that provide incentives for the management of

climate change issues and those that do not provide. Results showed that the average

carbon intensity emissions for the companies that provide incentives for the management

of climate change issues and those that do not provide (Mean = 523.48, Standard Deviation

= 1749.18, N = 847) was not significantly with the average carbon intensity emissions for the

companies that did not provide incentives for the management of climate change issues

(Mean = 465.43, Standard Deviation = 1888.53, N = 847), t (1.33) = -0.219, p > .05, two-

tailed test.

15 | P a g e

Independent Samples Test

Levene's Test

for Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differe

nce

Std.

Error

Differe

nce

95%

Confidence

Interval of the

Difference

Lower Upper

Intensi

ty

Equal

variances

assumed

.084 .772 -.11

6

133 .908 -36.76 317 -664 591

Equal

variances not

assumed

-.11

4

107.63

5

.909 -36.76 322 -675 602

We performed an independent t-test in order to compare the average means of carbon

emissions reduction for the companies that provide incentives for the management of

climate change issues and those that do not provide. Results showed that the average

carbon intensity emissions for the companies that provide incentives for the management

of climate change issues and those that do not provide (Mean = 523.48, Standard Deviation

= 1749.18, N = 847) was not significantly with the average carbon intensity emissions for the

companies that did not provide incentives for the management of climate change issues

(Mean = 465.43, Standard Deviation = 1888.53, N = 847), t (1.33) = -0.219, p > .05, two-

tailed test.

15 | P a g e

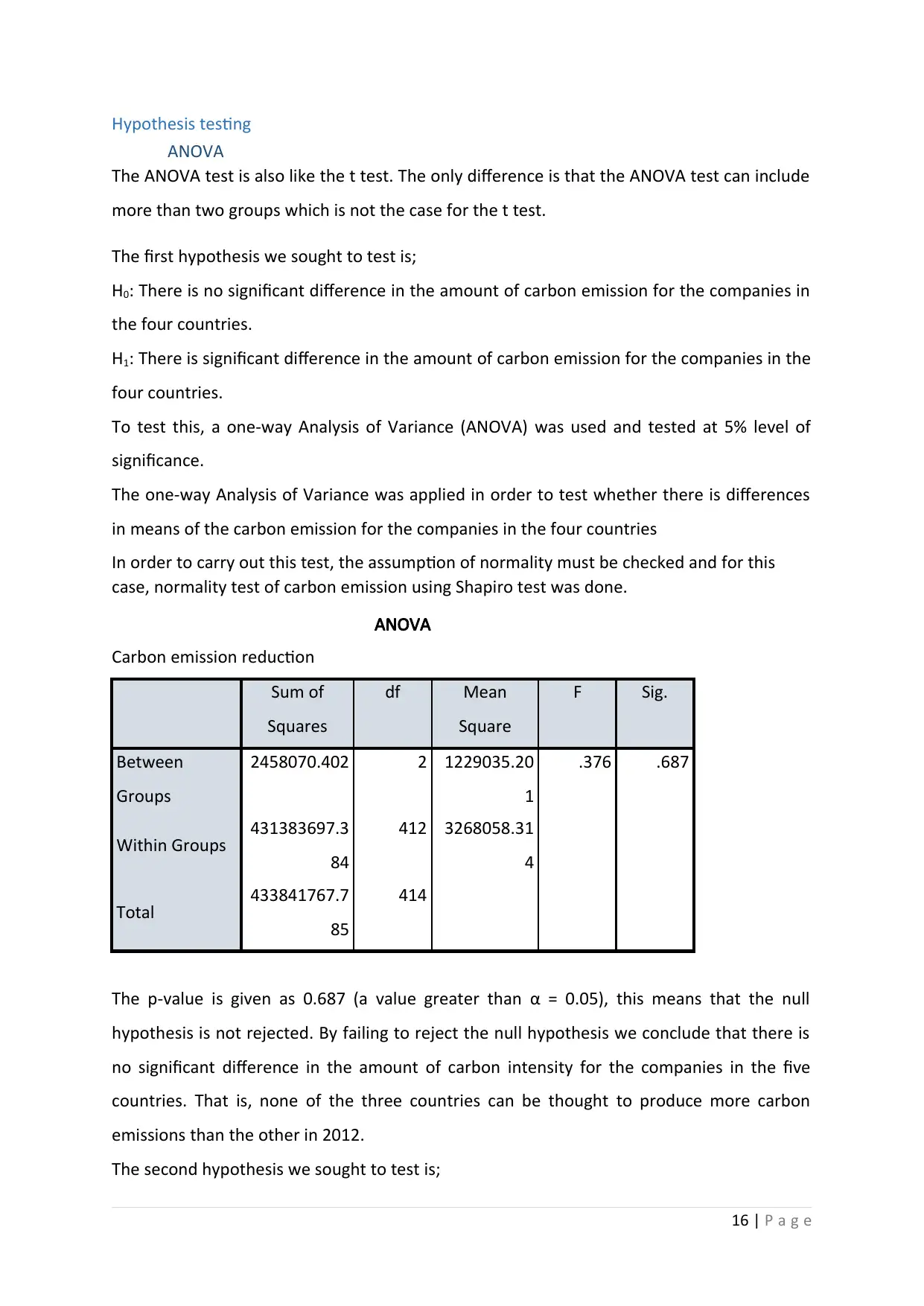

Hypothesis testing

ANOVA

The ANOVA test is also like the t test. The only difference is that the ANOVA test can include

more than two groups which is not the case for the t test.

The first hypothesis we sought to test is;

H0: There is no significant difference in the amount of carbon emission for the companies in

the four countries.

H1: There is significant difference in the amount of carbon emission for the companies in the

four countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance.

The one-way Analysis of Variance was applied in order to test whether there is differences

in means of the carbon emission for the companies in the four countries

In order to carry out this test, the assumption of normality must be checked and for this

case, normality test of carbon emission using Shapiro test was done.

ANOVA

Carbon emission reduction

Sum of

Squares

df Mean

Square

F Sig.

Between

Groups

2458070.402 2 1229035.20

1

.376 .687

Within Groups 431383697.3

84

412 3268058.31

4

Total 433841767.7

85

414

The p-value is given as 0.687 (a value greater than α = 0.05), this means that the null

hypothesis is not rejected. By failing to reject the null hypothesis we conclude that there is

no significant difference in the amount of carbon intensity for the companies in the five

countries. That is, none of the three countries can be thought to produce more carbon

emissions than the other in 2012.

The second hypothesis we sought to test is;

16 | P a g e

ANOVA

The ANOVA test is also like the t test. The only difference is that the ANOVA test can include

more than two groups which is not the case for the t test.

The first hypothesis we sought to test is;

H0: There is no significant difference in the amount of carbon emission for the companies in

the four countries.

H1: There is significant difference in the amount of carbon emission for the companies in the

four countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance.

The one-way Analysis of Variance was applied in order to test whether there is differences

in means of the carbon emission for the companies in the four countries

In order to carry out this test, the assumption of normality must be checked and for this

case, normality test of carbon emission using Shapiro test was done.

ANOVA

Carbon emission reduction

Sum of

Squares

df Mean

Square

F Sig.

Between

Groups

2458070.402 2 1229035.20

1

.376 .687

Within Groups 431383697.3

84

412 3268058.31

4

Total 433841767.7

85

414

The p-value is given as 0.687 (a value greater than α = 0.05), this means that the null

hypothesis is not rejected. By failing to reject the null hypothesis we conclude that there is

no significant difference in the amount of carbon intensity for the companies in the five

countries. That is, none of the three countries can be thought to produce more carbon

emissions than the other in 2012.

The second hypothesis we sought to test is;

16 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

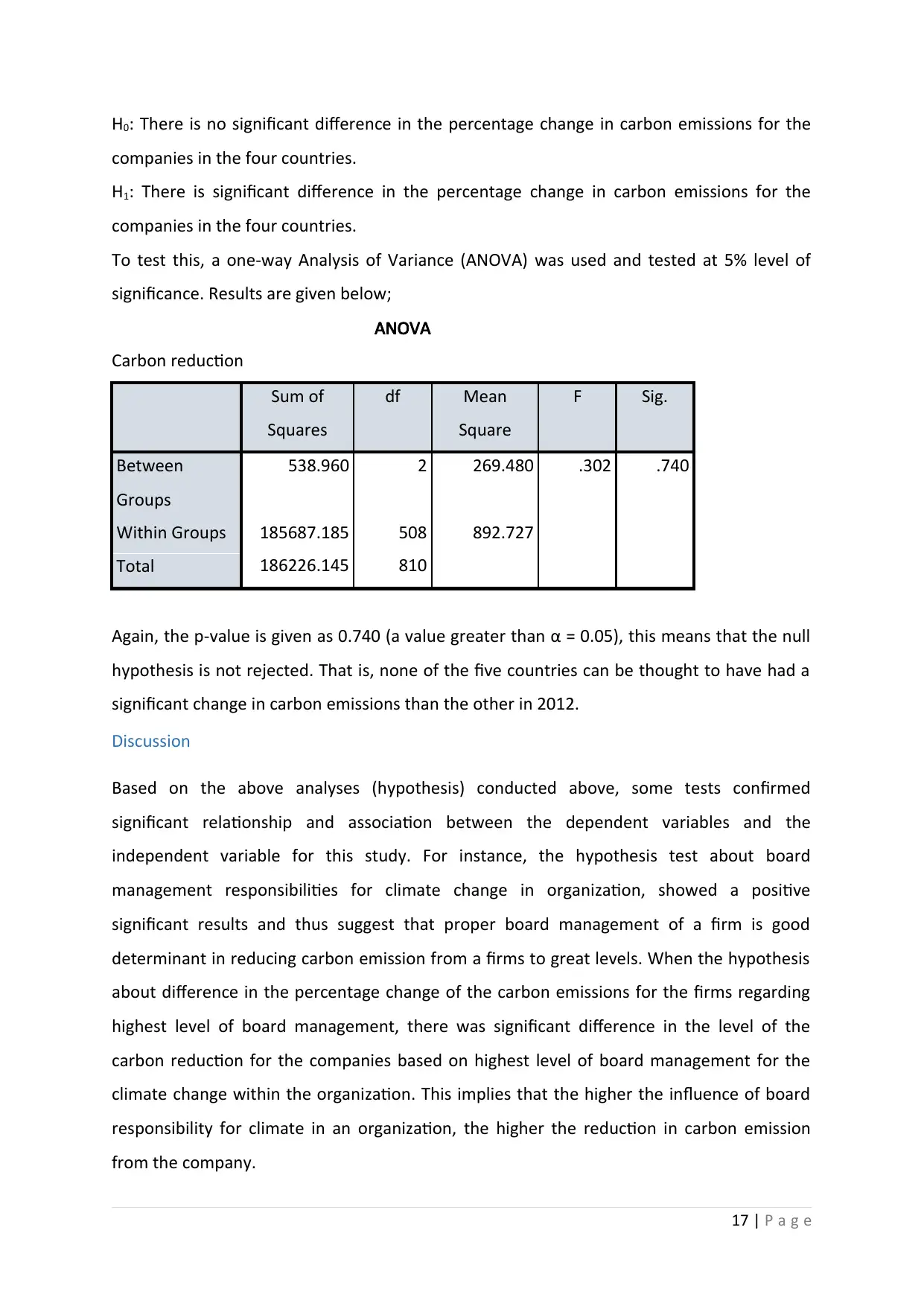

H0: There is no significant difference in the percentage change in carbon emissions for the

companies in the four countries.

H1: There is significant difference in the percentage change in carbon emissions for the

companies in the four countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance. Results are given below;

ANOVA

Carbon reduction

Sum of

Squares

df Mean

Square

F Sig.

Between

Groups

538.960 2 269.480 .302 .740

Within Groups 185687.185 508 892.727

Total 186226.145 810

Again, the p-value is given as 0.740 (a value greater than α = 0.05), this means that the null

hypothesis is not rejected. That is, none of the five countries can be thought to have had a

significant change in carbon emissions than the other in 2012.

Discussion

Based on the above analyses (hypothesis) conducted above, some tests confirmed

significant relationship and association between the dependent variables and the

independent variable for this study. For instance, the hypothesis test about board

management responsibilities for climate change in organization, showed a positive

significant results and thus suggest that proper board management of a firm is good

determinant in reducing carbon emission from a firms to great levels. When the hypothesis

about difference in the percentage change of the carbon emissions for the firms regarding

highest level of board management, there was significant difference in the level of the

carbon reduction for the companies based on highest level of board management for the

climate change within the organization. This implies that the higher the influence of board

responsibility for climate in an organization, the higher the reduction in carbon emission

from the company.

17 | P a g e

companies in the four countries.

H1: There is significant difference in the percentage change in carbon emissions for the

companies in the four countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance. Results are given below;

ANOVA

Carbon reduction

Sum of

Squares

df Mean

Square

F Sig.

Between

Groups

538.960 2 269.480 .302 .740

Within Groups 185687.185 508 892.727

Total 186226.145 810

Again, the p-value is given as 0.740 (a value greater than α = 0.05), this means that the null

hypothesis is not rejected. That is, none of the five countries can be thought to have had a

significant change in carbon emissions than the other in 2012.

Discussion

Based on the above analyses (hypothesis) conducted above, some tests confirmed

significant relationship and association between the dependent variables and the

independent variable for this study. For instance, the hypothesis test about board

management responsibilities for climate change in organization, showed a positive

significant results and thus suggest that proper board management of a firm is good

determinant in reducing carbon emission from a firms to great levels. When the hypothesis

about difference in the percentage change of the carbon emissions for the firms regarding

highest level of board management, there was significant difference in the level of the

carbon reduction for the companies based on highest level of board management for the

climate change within the organization. This implies that the higher the influence of board

responsibility for climate in an organization, the higher the reduction in carbon emission

from the company.

17 | P a g e

Also, while the previous researches have demonstrated that reduction of carbon emissions

and exhibiting good board management environmental performance is very vital for the

companies, none of the study has ever examined the mechanisms of how the environmental

goals are achieved at smaller levels within the firm. We therefore can argue that adoption of

the incentive schemes for the employees should exist in any company that emits carbon as

this will tend to reduce the level and percentage of carbon into the atmosphere McNabb

2015). Out finding have important implications for the public and government suggesting

that non-mandatory guidance or the consideration of a likely introduction of a requirement

may result to higher level of carbon emission and subsequent sustainable actions. The

measurement and the subsequent disclosure of emissions is a tool that can make

management be aware of the need to improve on the terms of the sustainable

developments against climate change.

The analysis of variance (ANOVA) indicates that none of the five countries that can be

thought to have had a significant change in carbon emissions than the other in the year

2013. Also, from the ANOVA test, the p-value is given as 0.003 (a value greater than α =

0.05), this means that the null hypothesis is not rejected. That is, the board responsibility

has great influence in either increasing or reducing carbon emission within an organization.

In addition, with reference to the moderating variable, there was a positive significant value

which implies that provision of management incentives to the employees also contributes

positively to lower levels of carbon emission within an organization.

When an independent sample t-test was performed in order to compare the average means

of carbon emissions for the companies with higher level of board management for the

climate change in an organization, the results showed that the average carbon emissions for

the companies that have better and good level of management tend to have low emission of

carbon from the firms. Moreover, based on the moderating variable, the management

incentives for the employees of climate change issues and those that do not provide, there

was significant difference with the average carbon emissions for the companies that did not

provide incentives for the management of climate change issues based on the two tail test.

The findings therefore suggests that the management incentives and policies enhances

climate change mitigation in many countries across the world by reducing carbon emissions.

Therefore, in this research paper, it can be asserted that the higher the influence of board

18 | P a g e

and exhibiting good board management environmental performance is very vital for the

companies, none of the study has ever examined the mechanisms of how the environmental

goals are achieved at smaller levels within the firm. We therefore can argue that adoption of

the incentive schemes for the employees should exist in any company that emits carbon as

this will tend to reduce the level and percentage of carbon into the atmosphere McNabb

2015). Out finding have important implications for the public and government suggesting

that non-mandatory guidance or the consideration of a likely introduction of a requirement

may result to higher level of carbon emission and subsequent sustainable actions. The

measurement and the subsequent disclosure of emissions is a tool that can make

management be aware of the need to improve on the terms of the sustainable

developments against climate change.

The analysis of variance (ANOVA) indicates that none of the five countries that can be

thought to have had a significant change in carbon emissions than the other in the year

2013. Also, from the ANOVA test, the p-value is given as 0.003 (a value greater than α =

0.05), this means that the null hypothesis is not rejected. That is, the board responsibility

has great influence in either increasing or reducing carbon emission within an organization.

In addition, with reference to the moderating variable, there was a positive significant value

which implies that provision of management incentives to the employees also contributes

positively to lower levels of carbon emission within an organization.

When an independent sample t-test was performed in order to compare the average means

of carbon emissions for the companies with higher level of board management for the

climate change in an organization, the results showed that the average carbon emissions for

the companies that have better and good level of management tend to have low emission of

carbon from the firms. Moreover, based on the moderating variable, the management

incentives for the employees of climate change issues and those that do not provide, there

was significant difference with the average carbon emissions for the companies that did not

provide incentives for the management of climate change issues based on the two tail test.

The findings therefore suggests that the management incentives and policies enhances

climate change mitigation in many countries across the world by reducing carbon emissions.

Therefore, in this research paper, it can be asserted that the higher the influence of board

18 | P a g e

responsibility for the climate change in an organization, the higher will be carbon emission

reduction.

Limitations of the study

In relation to this research, a many caveats were recognized as well. First, our sample is

comprised of only big predominantly multinational organizations from United States, China,

Japan and Russia which can be considered to have achieved greater carbon reduction

leaving out smaller and average firms which have not or are in the process of reducing

carbon emission. It is thus possible that consequences dominated here do not claim for the

smaller firms that are competing locally.

Another limitation to this study is that only five countries data have been examined and also

the data examined is limited to a period of two years. It could be well and reasonable if the

data is analysed over a more than five countries through a longer time frame. This may

result to somewhat different and better findings and outcomes for the future study. All

these will as well form the fruitful areas of the future work.

It also appears that though a general methodology statement describes the figures were

projected, none of the original reference models and data sources are publicly available for

usage. Lastly, the study was only limited to among 847 companies which have achieved

greater carbon reduction and thus may not give overall inference about whole carbon

reduction among firms in different settings.

Lastly, in relation to the analysis conducted based on the dependent and the independent

variable, the dataset used for the analysis had few outliers which were removed. This may

have compromised the nature of the results in general as the data collected was not 100 %

accurate for the analysis.

Future Researches

For the future studies, a relatively bigger sample size of the companies should be considered

for the analysis as this would result to more concrete and reliable findings for better

references. The outcomes in this paper cannot be fully relied upon for future references

since only five world countries and sample of 847 companies from them were selected for

the study and analysis. Moreover, future work should not only aim at bigger predominantly

19 | P a g e

reduction.

Limitations of the study

In relation to this research, a many caveats were recognized as well. First, our sample is

comprised of only big predominantly multinational organizations from United States, China,

Japan and Russia which can be considered to have achieved greater carbon reduction

leaving out smaller and average firms which have not or are in the process of reducing

carbon emission. It is thus possible that consequences dominated here do not claim for the

smaller firms that are competing locally.

Another limitation to this study is that only five countries data have been examined and also

the data examined is limited to a period of two years. It could be well and reasonable if the

data is analysed over a more than five countries through a longer time frame. This may

result to somewhat different and better findings and outcomes for the future study. All

these will as well form the fruitful areas of the future work.

It also appears that though a general methodology statement describes the figures were

projected, none of the original reference models and data sources are publicly available for

usage. Lastly, the study was only limited to among 847 companies which have achieved

greater carbon reduction and thus may not give overall inference about whole carbon

reduction among firms in different settings.

Lastly, in relation to the analysis conducted based on the dependent and the independent

variable, the dataset used for the analysis had few outliers which were removed. This may

have compromised the nature of the results in general as the data collected was not 100 %

accurate for the analysis.

Future Researches

For the future studies, a relatively bigger sample size of the companies should be considered

for the analysis as this would result to more concrete and reliable findings for better

references. The outcomes in this paper cannot be fully relied upon for future references

since only five world countries and sample of 847 companies from them were selected for

the study and analysis. Moreover, future work should not only aim at bigger predominantly

19 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

multinomial organizations which have achieved or have well integrated board management

and business strategy in reducing carbon emission but also, focus on small organizations

which have no or little strategies on carbon reduction. This will compromise the nature of

the results and can lead to poor references about the existing variable and predictors hence

bad results.

References

20 | P a g e

and business strategy in reducing carbon emission but also, focus on small organizations

which have no or little strategies on carbon reduction. This will compromise the nature of

the results and can lead to poor references about the existing variable and predictors hence

bad results.

References

20 | P a g e

Bridoux and Stoelhorst, 2014. Microfoundations for Stakeholder Theory: Managing

Stakeholders with Heterogeneous Motives.

Strategic Management Journal, Volume 35, pp.

107-125.

Fraser, 2012. Fleshing out an engagement with a social accounting technology.

Auditing &

Accountability Journal, Volume 25, pp. 508-534.

Greenwood and Anderson, 2009. i used to be an employee but now i am a

stakeholder:implication of labelling employees as stakeholders.

Asia pacific journal of

human resources.

Hitt, M. and Duane Ireland, R., 2017. The intersection of entrepreneurship and strategic

management research.

The Blackwell handbook of entrepreneurship, pp.45-63.

Giacomo, Guthrie and Farneti, 2017. Environmental management control systems for

carbon emissions.

Creative commons attribution, Volume 1.

Kalu, Buang and Aliagha, 2016. Determinants of carbon emission disclosure and reduction in

corporate real estate companies in Nigeria.

Journal of Environment and Earth Science,

Volume 6.

Kuo, Yah and Yu, 2012. Disclosure of Corporate Social Responsibility and Environmental

Management: Evidence from China.

Corporate Social Responsibility and Environmental

Management, Volume 19(5).

McNabb, D.E., 2015.

Research methods in public administration and nonprofit management.

Routledge.

Moriarty, J., 2014. The connection between stakeholder theory and stakeholder democracy:

An excavation and defense.

Business & Society, 53(6), pp. 820-852.

Lane, 2010. Economic catch-up and emission reductions.

Sustainability Accounting

Management and Policy Journal, Volume 1, pp. 96-102.

Sharp, J.A., Peters, J. and Howard, K., 2017.

The management of a student research project.

Routledge.

Wittneben and Kiyar, 2018. Climate changes basics for managers.

emeraldinsight.

21 | P a g e

Stakeholders with Heterogeneous Motives.

Strategic Management Journal, Volume 35, pp.

107-125.

Fraser, 2012. Fleshing out an engagement with a social accounting technology.

Auditing &

Accountability Journal, Volume 25, pp. 508-534.

Greenwood and Anderson, 2009. i used to be an employee but now i am a

stakeholder:implication of labelling employees as stakeholders.

Asia pacific journal of

human resources.

Hitt, M. and Duane Ireland, R., 2017. The intersection of entrepreneurship and strategic

management research.

The Blackwell handbook of entrepreneurship, pp.45-63.

Giacomo, Guthrie and Farneti, 2017. Environmental management control systems for

carbon emissions.

Creative commons attribution, Volume 1.

Kalu, Buang and Aliagha, 2016. Determinants of carbon emission disclosure and reduction in

corporate real estate companies in Nigeria.

Journal of Environment and Earth Science,

Volume 6.

Kuo, Yah and Yu, 2012. Disclosure of Corporate Social Responsibility and Environmental

Management: Evidence from China.

Corporate Social Responsibility and Environmental

Management, Volume 19(5).

McNabb, D.E., 2015.

Research methods in public administration and nonprofit management.

Routledge.

Moriarty, J., 2014. The connection between stakeholder theory and stakeholder democracy:

An excavation and defense.

Business & Society, 53(6), pp. 820-852.

Lane, 2010. Economic catch-up and emission reductions.

Sustainability Accounting

Management and Policy Journal, Volume 1, pp. 96-102.

Sharp, J.A., Peters, J. and Howard, K., 2017.

The management of a student research project.

Routledge.

Wittneben and Kiyar, 2018. Climate changes basics for managers.

emeraldinsight.

21 | P a g e

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.