MGT723 Research: Impact of Incentives on Carbon Emission in USA

VerifiedAdded on 2023/06/07

|10

|1940

|345

Report

AI Summary

This research project investigates the relationship between incentives provided to companies and their carbon emissions in the USA. A sample of 293 companies was analyzed, examining the percentage change in carbon dioxide emissions as the dependent variable and the presence of incentiv...

Running Head: MGT723 RESEARCH PROJECT

MGT723 Research Project

Assessment Task 2: Data Collection

Name of the Student

Student ID

MGT723 Research Project

Assessment Task 2: Data Collection

Name of the Student

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MGT723 RESEARCH PROJECT

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand

that the source of ideas must be referenced and that quotation marks and a reference are required

when directly quoting anyone else’s words.

Acknowledgement:

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand

that the source of ideas must be referenced and that quotation marks and a reference are required

when directly quoting anyone else’s words.

2MGT723 RESEARCH PROJECT

Introduction

The world is highly devastated with the emission of carbon and that is the reason for the

climatic changes across the globe. Thus, it is of utmost importance to reduce the emissions of

carbon and green-house gases. The management of several companies have provided incentives

to the companies if they are successful in reducing the carbon emissions. The carbon emissions

are also dependent on the countries. Thus, the main aim of this study is to evaluate whether the

companies receiving incentives are emitting lesser carbon than the companies that do not receive

any incentives.

Literature Review – Summary

The emission of carbon dioxide along with other greenhouse gases have been increasing

gradually. This increase in the emissions is responsible for the global warming and as a result of

which, massive climatic changes can be observed across the globe. Thus, urgent actions need to

be taken to reduce the emissions of carbon as well as other greenhouse gases by the companies.

Different nations have called upon different agreements which can be acting as the major

stakeholders and helping the companies to come up with different strategies which will be

helpful in the reduction of the emissions. These strategies can also be integrated into the

economic production of the companies so that their objectives as well as their goals can be

achieved (Cui, et al. 2014, p. 1049). Thus, within different countries, it is required by different

companies to integrate in the processes of their productions, technologies so that the green

economy can be achieved (Dietz, 2009, p. 18454). It can be said from various analyses and

researches that some companies have experienced a reduction in the emission of carbon dioxide

which is much higher than some other companies. Most of the firms overemphasize the

economic growth of the company at the cost of the emission of carbon (Wei, et al. 2013, p. 27).

Introduction

The world is highly devastated with the emission of carbon and that is the reason for the

climatic changes across the globe. Thus, it is of utmost importance to reduce the emissions of

carbon and green-house gases. The management of several companies have provided incentives

to the companies if they are successful in reducing the carbon emissions. The carbon emissions

are also dependent on the countries. Thus, the main aim of this study is to evaluate whether the

companies receiving incentives are emitting lesser carbon than the companies that do not receive

any incentives.

Literature Review – Summary

The emission of carbon dioxide along with other greenhouse gases have been increasing

gradually. This increase in the emissions is responsible for the global warming and as a result of

which, massive climatic changes can be observed across the globe. Thus, urgent actions need to

be taken to reduce the emissions of carbon as well as other greenhouse gases by the companies.

Different nations have called upon different agreements which can be acting as the major

stakeholders and helping the companies to come up with different strategies which will be

helpful in the reduction of the emissions. These strategies can also be integrated into the

economic production of the companies so that their objectives as well as their goals can be

achieved (Cui, et al. 2014, p. 1049). Thus, within different countries, it is required by different

companies to integrate in the processes of their productions, technologies so that the green

economy can be achieved (Dietz, 2009, p. 18454). It can be said from various analyses and

researches that some companies have experienced a reduction in the emission of carbon dioxide

which is much higher than some other companies. Most of the firms overemphasize the

economic growth of the company at the cost of the emission of carbon (Wei, et al. 2013, p. 27).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MGT723 RESEARCH PROJECT

Therefore, from the discussions, it is clear that there is a target for the reduction of carbon

by the companies which they are unable to meet and there are various reasons behind that. These

reasons include the overemphasis of the economic growth at the cost of emission of carbon,

missing data in the reporting of emission of carbon and its effects, lack of the support from the

stakeholders all these have resulted in the less reduction of carbon emissions by the companies

(Druckman, et al. 2011, p. 3579).

Dependent Variable

The dependent variable in this research is the percentage change in the emission of

carbon dioxide.

Independent Variable

The independent variable considered for this study is the incentives provided by the

management to different companies. The answers to this variable are categorical denoting Yes

and No.

Control Variable

The control variable considered in this study is the country which will be considered for

performing this study. For this study, the chosen country is USA.

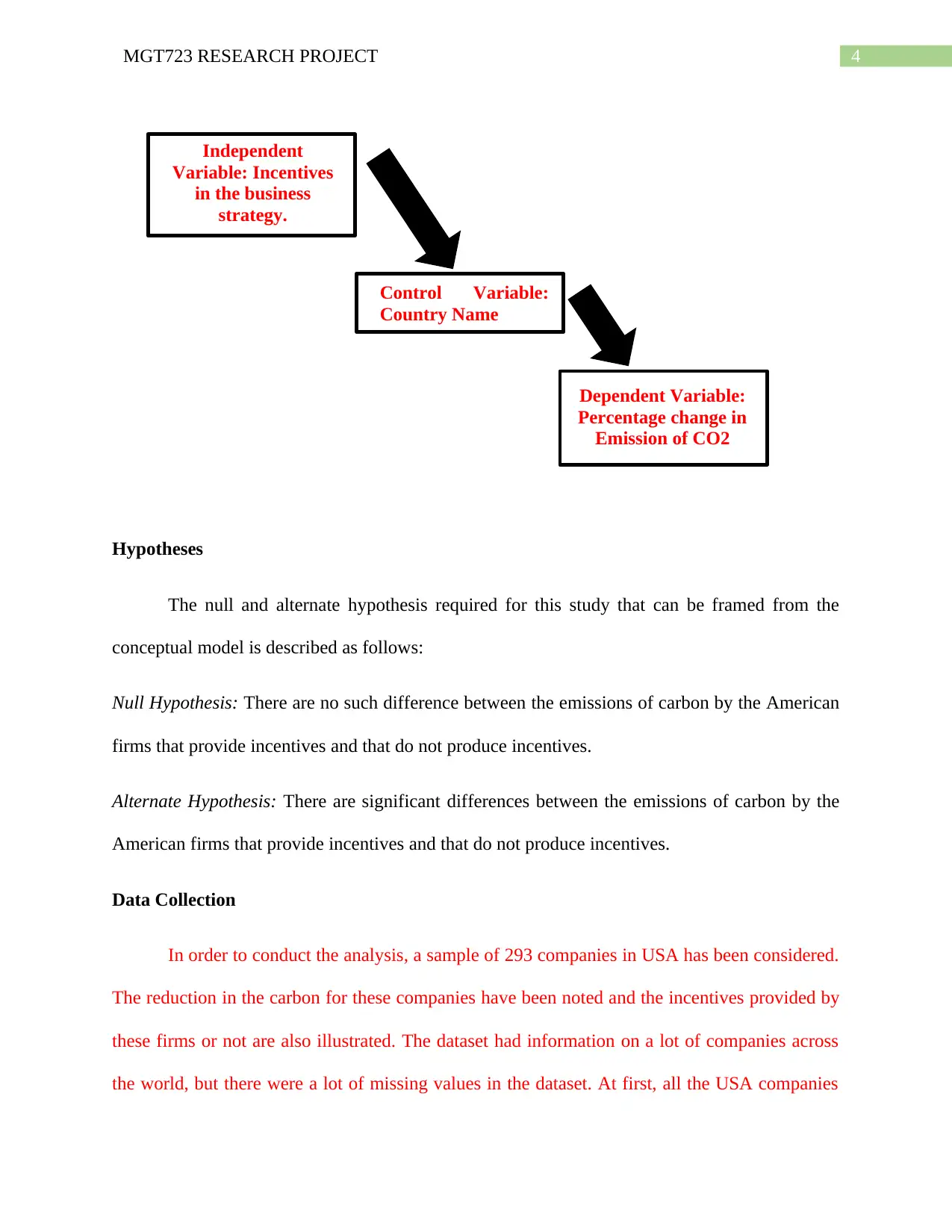

Conceptual Model

Therefore, from the discussions, it is clear that there is a target for the reduction of carbon

by the companies which they are unable to meet and there are various reasons behind that. These

reasons include the overemphasis of the economic growth at the cost of emission of carbon,

missing data in the reporting of emission of carbon and its effects, lack of the support from the

stakeholders all these have resulted in the less reduction of carbon emissions by the companies

(Druckman, et al. 2011, p. 3579).

Dependent Variable

The dependent variable in this research is the percentage change in the emission of

carbon dioxide.

Independent Variable

The independent variable considered for this study is the incentives provided by the

management to different companies. The answers to this variable are categorical denoting Yes

and No.

Control Variable

The control variable considered in this study is the country which will be considered for

performing this study. For this study, the chosen country is USA.

Conceptual Model

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MGT723 RESEARCH PROJECT

Independent

Variable: Incentives

in the business

strategy.

Control Variable:

Country Name

Dependent Variable:

Percentage change in

Emission of CO2

Hypotheses

The null and alternate hypothesis required for this study that can be framed from the

conceptual model is described as follows:

Null Hypothesis: There are no such difference between the emissions of carbon by the American

firms that provide incentives and that do not produce incentives.

Alternate Hypothesis: There are significant differences between the emissions of carbon by the

American firms that provide incentives and that do not produce incentives.

Data Collection

In order to conduct the analysis, a sample of 293 companies in USA has been considered.

The reduction in the carbon for these companies have been noted and the incentives provided by

these firms or not are also illustrated. The dataset had information on a lot of companies across

the world, but there were a lot of missing values in the dataset. At first, all the USA companies

Independent

Variable: Incentives

in the business

strategy.

Control Variable:

Country Name

Dependent Variable:

Percentage change in

Emission of CO2

Hypotheses

The null and alternate hypothesis required for this study that can be framed from the

conceptual model is described as follows:

Null Hypothesis: There are no such difference between the emissions of carbon by the American

firms that provide incentives and that do not produce incentives.

Alternate Hypothesis: There are significant differences between the emissions of carbon by the

American firms that provide incentives and that do not produce incentives.

Data Collection

In order to conduct the analysis, a sample of 293 companies in USA has been considered.

The reduction in the carbon for these companies have been noted and the incentives provided by

these firms or not are also illustrated. The dataset had information on a lot of companies across

the world, but there were a lot of missing values in the dataset. At first, all the USA companies

5MGT723 RESEARCH PROJECT

has been selected and the missing values has been eliminated from the dataset thus reducing the

sample size to 293 companies across USA. The missing values were obtained in the dataset as

some of the companies were not willing to share their information regarding the emission of

carbon. Thus, to make the analysis robust, the missing values are omitted from the dataset.

Data Analysis – Descriptive

In order to understand the nature of the data obtained, a descriptive statistical analysis has

been conducted on the data extracted on the 293 USA companies. These companies have been

selected randomly from the list of all the USA companies. As already discussed, the independent

variable is whether the companies are providing incentives to the customers and the dependent

variable is the percentage change in the emission of carbon dioxide by the companies. It can be

seen very clearly from the analysis conducted that most of the companies have been producing

incentives on reaching the target of reduction in the emission of carbon. Thus, among the 293

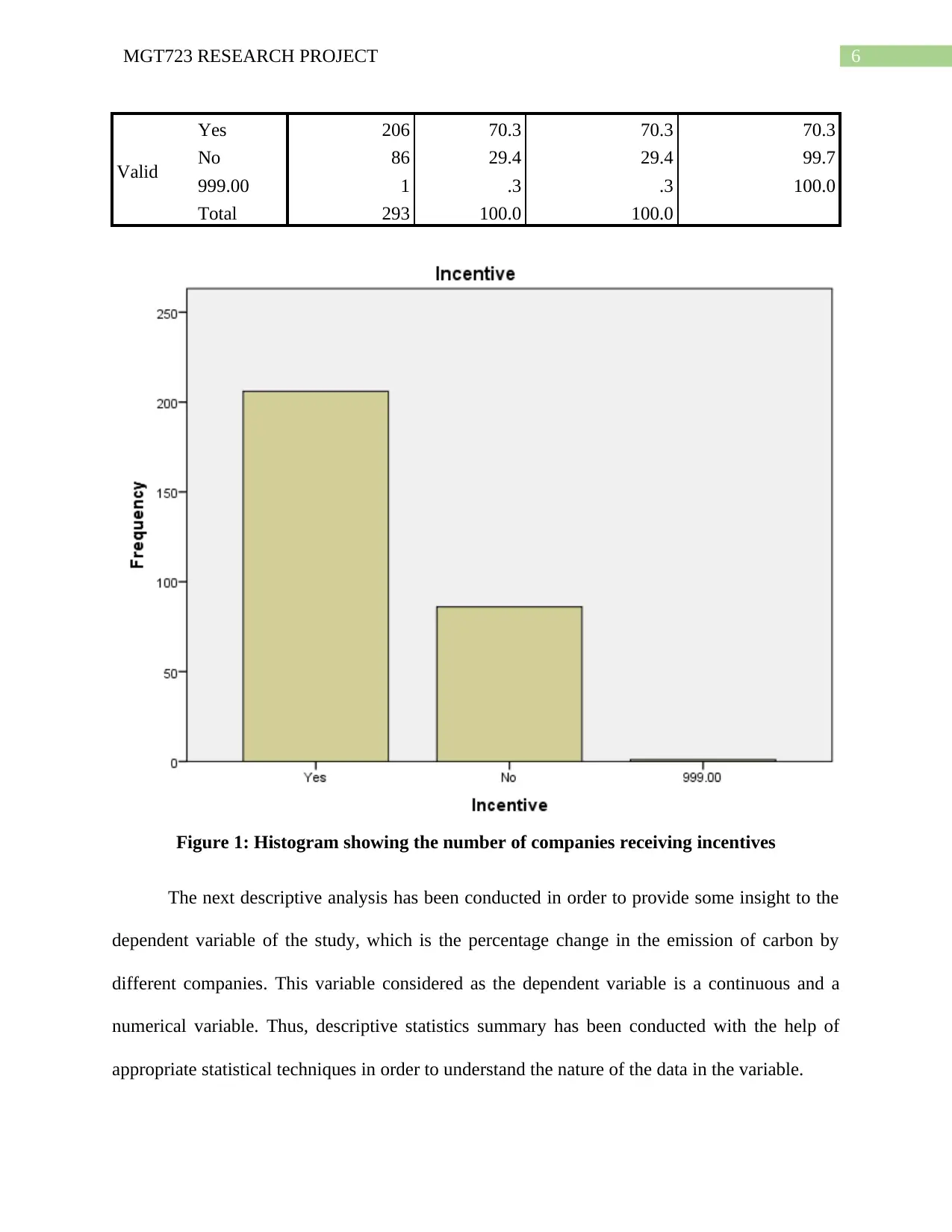

selected companies, it can be seen very clearly that 206 companies have been provided with

incentives by the managements on achieving the set target of reduction in the emissions which

comprise of 70.3 percent of the population. Similarly, 86 companies on the other hand has been

observed not to be receiving incentives from the management of the companies. This non

receiving companies form almost 29.4 percent of the population. It can also be seen from the

table that 1 out of the 293 selected companies did not disclose their information. Thus, from

here, it can be said that a very little proportion of the companies are not interested in disclosing

the information regarding the incentives received form the management or not. The data is

summarized and tabulated in table 1 and illustrated graphically in figure 1.

Table 1: Frequency Distribution of Incentive

Frequency Percent Valid Percent Cumulative Percent

has been selected and the missing values has been eliminated from the dataset thus reducing the

sample size to 293 companies across USA. The missing values were obtained in the dataset as

some of the companies were not willing to share their information regarding the emission of

carbon. Thus, to make the analysis robust, the missing values are omitted from the dataset.

Data Analysis – Descriptive

In order to understand the nature of the data obtained, a descriptive statistical analysis has

been conducted on the data extracted on the 293 USA companies. These companies have been

selected randomly from the list of all the USA companies. As already discussed, the independent

variable is whether the companies are providing incentives to the customers and the dependent

variable is the percentage change in the emission of carbon dioxide by the companies. It can be

seen very clearly from the analysis conducted that most of the companies have been producing

incentives on reaching the target of reduction in the emission of carbon. Thus, among the 293

selected companies, it can be seen very clearly that 206 companies have been provided with

incentives by the managements on achieving the set target of reduction in the emissions which

comprise of 70.3 percent of the population. Similarly, 86 companies on the other hand has been

observed not to be receiving incentives from the management of the companies. This non

receiving companies form almost 29.4 percent of the population. It can also be seen from the

table that 1 out of the 293 selected companies did not disclose their information. Thus, from

here, it can be said that a very little proportion of the companies are not interested in disclosing

the information regarding the incentives received form the management or not. The data is

summarized and tabulated in table 1 and illustrated graphically in figure 1.

Table 1: Frequency Distribution of Incentive

Frequency Percent Valid Percent Cumulative Percent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MGT723 RESEARCH PROJECT

Valid

Yes 206 70.3 70.3 70.3

No 86 29.4 29.4 99.7

999.00 1 .3 .3 100.0

Total 293 100.0 100.0

Figure 1: Histogram showing the number of companies receiving incentives

The next descriptive analysis has been conducted in order to provide some insight to the

dependent variable of the study, which is the percentage change in the emission of carbon by

different companies. This variable considered as the dependent variable is a continuous and a

numerical variable. Thus, descriptive statistics summary has been conducted with the help of

appropriate statistical techniques in order to understand the nature of the data in the variable.

Valid

Yes 206 70.3 70.3 70.3

No 86 29.4 29.4 99.7

999.00 1 .3 .3 100.0

Total 293 100.0 100.0

Figure 1: Histogram showing the number of companies receiving incentives

The next descriptive analysis has been conducted in order to provide some insight to the

dependent variable of the study, which is the percentage change in the emission of carbon by

different companies. This variable considered as the dependent variable is a continuous and a

numerical variable. Thus, descriptive statistics summary has been conducted with the help of

appropriate statistical techniques in order to understand the nature of the data in the variable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MGT723 RESEARCH PROJECT

Table 2 gives the information and the results of the descriptive statistical analysis. It can

be seen from the table that the average change in percentage of the carbon by the companies is -

2.63 percent, which is a negative amount indicating that in most of the firms, there has been a

reduction in the emission of carbon from the previous years and the reductions in the emissions

has dominated the non-reductions in the 86 other firms. On the other hand, it can be seen clearly

from the results that the median percentage change in the carbon emission has also been found to

be negative (- 3.5 percent). This indicates that in 50 percent of the firms, the change in carbon

emission is more than – 3.5 percent, which indicates that in most of the firms there has been a

reduction in the emission of carbon. Thus, there must be outliers present in the data which is

affecting the mean measure. In other words, there are some companies which have been emitting

carbon a lot higher than the previous years and thus the reduced companies are not being affected

by this information. Moreover, it can also be seen from the standard deviation value that the

deviation in the data is extremely high and the values are not at all close to the average

percentage change in carbon emission. The value of skewness shows that the data on percentage

change in the emission of carbon by the companies is skewed positively. That is, more

companies have reduced the emission, while lesser companies have increased the emission.

Table 2: Summary Statistics on Percentage Change in Carbon Emission

Carbon_Reduction

N Valid 293

Missing 0

Mean -2.6289

Std. Error of Mean 2.58926

Median -3.5000

Mode .00

Std. Deviation 44.32092

Variance 1964.344

Skewness 12.512

Std. Error of Skewness .142

Table 2 gives the information and the results of the descriptive statistical analysis. It can

be seen from the table that the average change in percentage of the carbon by the companies is -

2.63 percent, which is a negative amount indicating that in most of the firms, there has been a

reduction in the emission of carbon from the previous years and the reductions in the emissions

has dominated the non-reductions in the 86 other firms. On the other hand, it can be seen clearly

from the results that the median percentage change in the carbon emission has also been found to

be negative (- 3.5 percent). This indicates that in 50 percent of the firms, the change in carbon

emission is more than – 3.5 percent, which indicates that in most of the firms there has been a

reduction in the emission of carbon. Thus, there must be outliers present in the data which is

affecting the mean measure. In other words, there are some companies which have been emitting

carbon a lot higher than the previous years and thus the reduced companies are not being affected

by this information. Moreover, it can also be seen from the standard deviation value that the

deviation in the data is extremely high and the values are not at all close to the average

percentage change in carbon emission. The value of skewness shows that the data on percentage

change in the emission of carbon by the companies is skewed positively. That is, more

companies have reduced the emission, while lesser companies have increased the emission.

Table 2: Summary Statistics on Percentage Change in Carbon Emission

Carbon_Reduction

N Valid 293

Missing 0

Mean -2.6289

Std. Error of Mean 2.58926

Median -3.5000

Mode .00

Std. Deviation 44.32092

Variance 1964.344

Skewness 12.512

Std. Error of Skewness .142

8MGT723 RESEARCH PROJECT

Kurtosis 189.328

Std. Error of Kurtosis .284

Range 772.70

Minimum -98.00

Maximum 674.70

Sum -770.28

Percentiles

25 -9.4000

50 -3.5000

75 .0100

Data Analysis – Inferential

The hypothesis stated above in the hypothesis section can be tested with the help of

necessary inferential statistical techniques. In this case, the data present can be divided into two

different groups, one is the group of companies that receive incentives and the other is the group

of companies that do not receive incentives. The test will be conducted on the difference in the

average percentage change in the reduction of carbon emission between these two groups of

companies. This test can be conducted with the help of independent sample t-test, which is the

most appropriate test to be used for testing the difference in the means of two groups.

Kurtosis 189.328

Std. Error of Kurtosis .284

Range 772.70

Minimum -98.00

Maximum 674.70

Sum -770.28

Percentiles

25 -9.4000

50 -3.5000

75 .0100

Data Analysis – Inferential

The hypothesis stated above in the hypothesis section can be tested with the help of

necessary inferential statistical techniques. In this case, the data present can be divided into two

different groups, one is the group of companies that receive incentives and the other is the group

of companies that do not receive incentives. The test will be conducted on the difference in the

average percentage change in the reduction of carbon emission between these two groups of

companies. This test can be conducted with the help of independent sample t-test, which is the

most appropriate test to be used for testing the difference in the means of two groups.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MGT723 RESEARCH PROJECT

List of References

Cui, L.B., Fan, Y., Zhu, L. and Bi, Q.H., 2014. How will the emissions trading scheme save cost

for achieving China’s 2020 carbon intensity reduction target?. Applied Energy, 136,

pp.1043-1052.

Dietz, T., Gardner, G.T., Gilligan, J., Stern, P.C. and Vandenbergh, M.P., 2009. Household

actions can provide a behavioral wedge to rapidly reduce US carbon

emissions. Proceedings of the National Academy of Sciences, 106(44), pp.18452-18456.

Druckman, A., Chitnis, M., Sorrell, S. and Jackson, T., 2011. Missing carbon reductions?

Exploring rebound and backfire effects in UK households. Energy Policy, 39(6),

pp.3572-3581.

Wei, M., Nelson, J.H., Greenblatt, J.B., Mileva, A., Johnston, J., Ting, M., Yang, C., Jones, C.,

McMahon, J.E. and Kammen, D.M., 2013. Deep carbon reductions in California require

electrification and integration across economic sectors. Environmental Research

Letters, 8(1), p.014038.

List of References

Cui, L.B., Fan, Y., Zhu, L. and Bi, Q.H., 2014. How will the emissions trading scheme save cost

for achieving China’s 2020 carbon intensity reduction target?. Applied Energy, 136,

pp.1043-1052.

Dietz, T., Gardner, G.T., Gilligan, J., Stern, P.C. and Vandenbergh, M.P., 2009. Household

actions can provide a behavioral wedge to rapidly reduce US carbon

emissions. Proceedings of the National Academy of Sciences, 106(44), pp.18452-18456.

Druckman, A., Chitnis, M., Sorrell, S. and Jackson, T., 2011. Missing carbon reductions?

Exploring rebound and backfire effects in UK households. Energy Policy, 39(6),

pp.3572-3581.

Wei, M., Nelson, J.H., Greenblatt, J.B., Mileva, A., Johnston, J., Ting, M., Yang, C., Jones, C.,

McMahon, J.E. and Kammen, D.M., 2013. Deep carbon reductions in California require

electrification and integration across economic sectors. Environmental Research

Letters, 8(1), p.014038.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.