Case Analysis: Business Plan Development for a Nursing Service

VerifiedAdded on 2021/04/16

|11

|3234

|71

Case Study

AI Summary

This case analysis examines the development of a nursing service business plan for a 32-bed general surgical ward in a metropolitan hospital, addressing the restructuring of hospital networks. The analysis identifies essential steps in business plan development, including financial planning, aims and objectives, and stakeholder support. It also discusses the required documents for service profile development, work methodology, and skill-mix issues. Furthermore, the analysis explores the benefits of a cost center budget, different budgeting methods like flexible and zero-based budgeting, and the implications for salaries and wages. The case highlights the importance of proper training, clear segregation of services, and effective cost management strategies within a healthcare setting. The study emphasizes the importance of data collection, efficient resource allocation, and the impact of budgeting methods on decision-making, productivity, and cost control within the context of a hospital's nursing services.

Running head: CASE ANALYSIS

Case Analysis

Name of the Student:

Name of the University:

Author Note

Case Analysis

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CASE ANALYSIS

Table of Contents

Introduction......................................................................................................................................2

Identification of the essential steps in developing a nursing service business plan........................2

The documents that are needed to be collected for the purpose of analyzing and developing a

service profile..................................................................................................................................3

Work methodology..........................................................................................................................4

Skill-mix or staff education issues...................................................................................................4

Benefits of developing a cost centre budget....................................................................................5

Different methods of budgeting.......................................................................................................6

Salaries and Wage budget................................................................................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................2

Identification of the essential steps in developing a nursing service business plan........................2

The documents that are needed to be collected for the purpose of analyzing and developing a

service profile..................................................................................................................................3

Work methodology..........................................................................................................................4

Skill-mix or staff education issues...................................................................................................4

Benefits of developing a cost centre budget....................................................................................5

Different methods of budgeting.......................................................................................................6

Salaries and Wage budget................................................................................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

2CASE ANALYSIS

Introduction

The health care systems that have been established in Australia have exerted pressure of

the highest degree on the growing population of the country. It must be noted here that Australia

has a mixed system of public and private health care provisions that have been regulated at

different levels of governmental proceedings. Furthermore, the understanding of the function and

structure of the health care system along with the factors that result in the elevation of the related

costs is the primary requirement for the establishment of a proper financial management

structure (Kaur 2015).

The issue that has been presented in this question is that a case study where a nurse

manager has been appointed for the purpose of managing a 32 bed general surgical ward that is

placed in a metropolitan hospital in a major city. The particular issue in regards to the

restructuring of the hospital networks in the local Area Health Service is that the general surgical

ward has been asked to be combined with the 12 bed surgical ward that has been specially

constructed for the purpose of short stay.

Identification of the essential steps in developing a nursing service business plan

The steps that are required for the development of a nursing business service plan can be

described in a detailed method. The initial stage involves planning of the business case for the

employment of the organizational fund. Here, it can be understood that the establishment of the

12 bed short stay surgical ward will require sufficient funds. Moreover, the planning should be

carried out in such a way that the general surgical ward is placed adjacent to the short stay ward

without hampering the functioning of both the wards are not hampered by each other (Song, Qiu

and Liu 2016).

The aims and objectives of the expansion should also be clarified in order to determine

the particular service that is being offered to the patients (Song, Qiu and Liu 2016). The required

support from the employees and other stakeholders of business should also be derived for the

implementation of the expansion of the health care facilities (Dafny, Ho and Lee 2017). Next, the

cost that is required for the setting up of the expanded part of the business should be properly

calculated and figured (Dafny, Ho and Lee 2017).

Introduction

The health care systems that have been established in Australia have exerted pressure of

the highest degree on the growing population of the country. It must be noted here that Australia

has a mixed system of public and private health care provisions that have been regulated at

different levels of governmental proceedings. Furthermore, the understanding of the function and

structure of the health care system along with the factors that result in the elevation of the related

costs is the primary requirement for the establishment of a proper financial management

structure (Kaur 2015).

The issue that has been presented in this question is that a case study where a nurse

manager has been appointed for the purpose of managing a 32 bed general surgical ward that is

placed in a metropolitan hospital in a major city. The particular issue in regards to the

restructuring of the hospital networks in the local Area Health Service is that the general surgical

ward has been asked to be combined with the 12 bed surgical ward that has been specially

constructed for the purpose of short stay.

Identification of the essential steps in developing a nursing service business plan

The steps that are required for the development of a nursing business service plan can be

described in a detailed method. The initial stage involves planning of the business case for the

employment of the organizational fund. Here, it can be understood that the establishment of the

12 bed short stay surgical ward will require sufficient funds. Moreover, the planning should be

carried out in such a way that the general surgical ward is placed adjacent to the short stay ward

without hampering the functioning of both the wards are not hampered by each other (Song, Qiu

and Liu 2016).

The aims and objectives of the expansion should also be clarified in order to determine

the particular service that is being offered to the patients (Song, Qiu and Liu 2016). The required

support from the employees and other stakeholders of business should also be derived for the

implementation of the expansion of the health care facilities (Dafny, Ho and Lee 2017). Next, the

cost that is required for the setting up of the expanded part of the business should be properly

calculated and figured (Dafny, Ho and Lee 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CASE ANALYSIS

Lastly, enough initiative should be taken in order to facilitate the successful

establishment of the short stay ward along with the general surgical ward (Singh caes et al.,

2015). The staff who will be required for attending the patients in the short stay ward have to be

trained accordingly (Singh caes et al., 2015). Moreover, the sections in regards to the general

surgical ward and the short stay ward should be clearly segregated and the purpose should be

explained of the expanded facility should be explained to the nurses and other staff of the

hospital (Singh caes et al., 2015)

The documents that are needed to be collected for the purpose of analyzing and developing

a service profile

It must be noted here that in case of a health care facility, the data does not flow into the

entity in a standardized way. A great deal of challenge has to be faced by the health care systems

in terms of collection of data from patients, enrollees and other members. The health care

systems deal in a diverse range of documents like the data collection systems, medical records,

billing records, health plans and other related documents. The data that is essentially required to

develop a service profile are the data in regards to the race and ethnicity of the patients,

individual persona health records and electronic data health records and other systems of data.

It must be noted here that the till that point is reached when the collected data has been

better integrated by the entities, there will be a certain degree of redundancy that will be in the

collection of data in regards to the race, ethnicity and other related patient information.

Moreover, the methods that would be adopted for the collection of information should be

integrated into the data flows that are operating in the current times. The issue in regards to the

efficiency and privacy of the patients should also be considered (Parikh 2017).

Therefore, the documents that should are needed to be collected for the purpose of

analyzing and developing a service profile are the supply market sources document. This

document will help in identifying the suggested external sources that will essentially reflect the

supply market data that will result in the further development of the effective business strategies.

A developing strategic commissioning plans document is also required. Therefore, the

documents that will be required are Guidance on Developing Strategic Commissioning Plans,

Options Appraisal, External Data Sources Template, Registers, Medication journals, Clinic

guidelines, Documents for recording the details of the diseased.

Lastly, enough initiative should be taken in order to facilitate the successful

establishment of the short stay ward along with the general surgical ward (Singh caes et al.,

2015). The staff who will be required for attending the patients in the short stay ward have to be

trained accordingly (Singh caes et al., 2015). Moreover, the sections in regards to the general

surgical ward and the short stay ward should be clearly segregated and the purpose should be

explained of the expanded facility should be explained to the nurses and other staff of the

hospital (Singh caes et al., 2015)

The documents that are needed to be collected for the purpose of analyzing and developing

a service profile

It must be noted here that in case of a health care facility, the data does not flow into the

entity in a standardized way. A great deal of challenge has to be faced by the health care systems

in terms of collection of data from patients, enrollees and other members. The health care

systems deal in a diverse range of documents like the data collection systems, medical records,

billing records, health plans and other related documents. The data that is essentially required to

develop a service profile are the data in regards to the race and ethnicity of the patients,

individual persona health records and electronic data health records and other systems of data.

It must be noted here that the till that point is reached when the collected data has been

better integrated by the entities, there will be a certain degree of redundancy that will be in the

collection of data in regards to the race, ethnicity and other related patient information.

Moreover, the methods that would be adopted for the collection of information should be

integrated into the data flows that are operating in the current times. The issue in regards to the

efficiency and privacy of the patients should also be considered (Parikh 2017).

Therefore, the documents that should are needed to be collected for the purpose of

analyzing and developing a service profile are the supply market sources document. This

document will help in identifying the suggested external sources that will essentially reflect the

supply market data that will result in the further development of the effective business strategies.

A developing strategic commissioning plans document is also required. Therefore, the

documents that will be required are Guidance on Developing Strategic Commissioning Plans,

Options Appraisal, External Data Sources Template, Registers, Medication journals, Clinic

guidelines, Documents for recording the details of the diseased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CASE ANALYSIS

The service demand for the new service level would be that the patients who would need

treatment for a day or two, could be accommodated in the short stay ward and treated

accordingly. However, it must be noted here that the ward has the capacity to accommodate 12

individuals at once. Therefore, the facilities should be arranged in that particular way.

Work methodology

The work methodology that should be utilized for the determination of the supply of

nurses required to staff the new service level are that the nurses already attending the general

surgical ward should be properly trained in order to carry out the attending of the individuals

who will be admitted to the short stay ward. It can be easily deduced from the names that the

patients who will be attending the general surgical ward would be accommodating those patients

that need intense care, as they will be undergoing general and complex surgeries. On the other

hand, the short stay surgical ward will be accommodating those patients who can be cured in a

lesser degree of time and do not hold such complexities in terms of injuries or other diseases.

This means that the nurses who are attending the general surgical ward patients will be readily

able to treat the patients of the short surgical ward. The only providence that should be available

is a proper training and guideline framework for the purpose of distinctly making the process

clear to the nurses and other staff of the hospital in regards to the nature patients in both the

surgical wards and the level of service they need.

Skill-mix or staff education issues

There is no certain concern in regards to the skill-mix or staff education issues for the

purpose of attending to the patients of the short stay surgical ward. This is because the patients of

the general surgical ward need due care and attention as they are suffering from injuries or other

disease that are complex in nature and need surgery. Therefore, the degree of skill that is needed

to attend to the patients of this particular ward will be apparently higher than the skill that is

required to attend the patients of the short stay surgical ward. Thus, it can be deduced that the

nurses and other staff will not be facing any kind of issues in regards to the staff education.

However, it must be noted here that the particular behavior will be different in case of the

patients that are for general and complex surgeries and the patients who are to get well soon in a

shorter period of time. It is the primary duty of the nurse manager to make this clear among the

The service demand for the new service level would be that the patients who would need

treatment for a day or two, could be accommodated in the short stay ward and treated

accordingly. However, it must be noted here that the ward has the capacity to accommodate 12

individuals at once. Therefore, the facilities should be arranged in that particular way.

Work methodology

The work methodology that should be utilized for the determination of the supply of

nurses required to staff the new service level are that the nurses already attending the general

surgical ward should be properly trained in order to carry out the attending of the individuals

who will be admitted to the short stay ward. It can be easily deduced from the names that the

patients who will be attending the general surgical ward would be accommodating those patients

that need intense care, as they will be undergoing general and complex surgeries. On the other

hand, the short stay surgical ward will be accommodating those patients who can be cured in a

lesser degree of time and do not hold such complexities in terms of injuries or other diseases.

This means that the nurses who are attending the general surgical ward patients will be readily

able to treat the patients of the short surgical ward. The only providence that should be available

is a proper training and guideline framework for the purpose of distinctly making the process

clear to the nurses and other staff of the hospital in regards to the nature patients in both the

surgical wards and the level of service they need.

Skill-mix or staff education issues

There is no certain concern in regards to the skill-mix or staff education issues for the

purpose of attending to the patients of the short stay surgical ward. This is because the patients of

the general surgical ward need due care and attention as they are suffering from injuries or other

disease that are complex in nature and need surgery. Therefore, the degree of skill that is needed

to attend to the patients of this particular ward will be apparently higher than the skill that is

required to attend the patients of the short stay surgical ward. Thus, it can be deduced that the

nurses and other staff will not be facing any kind of issues in regards to the staff education.

However, it must be noted here that the particular behavior will be different in case of the

patients that are for general and complex surgeries and the patients who are to get well soon in a

shorter period of time. It is the primary duty of the nurse manager to make this clear among the

5CASE ANALYSIS

nurses and other staff so that they can understand the degree of difference in behavior and

service between the patients of the general surgical ward and the short stay surgical ward (Parikh

2017).

Benefits of developing a cost centre budget

A cost centre budget might be beneficial for the nurse manger to control the expenditures

of the wards (Dafny, Ho and Lee 2017). The advantages of the cost centre budget are that the

implementation of a cost centre budget will help in the comparison of the performance of the

service unit in terms of the short stay surgical ward and the general surgical ward. A cost centre

budget will help the nurse manager in identifying the underperforming parts of the hospital or the

parts that require excessive un-estimated costs. A cost centre budget will help in the

identification of the centers that generate the largest amount of expenditure. The identification of

the cost centers will also facilitate the fact that the management of the hospital will be able to

target these centers as the primary areas where the cost management strategies could be applied.

A cost center budget also helps in improving the reaction speed. This is because the cost center

budget will help in the allocation of the most skilled and responsible staff that will try to reduce

the cost in facilitating such a center, which will in turn improve the reaction, speed. A cost center

budget will also enable the staff and the nurses to make decisions on their part, which will

increase the degree of motivation and thus enhance productivity.

Different methods of budgeting

A flexible budget refers to the particular budget that includes the calculation of the

different levels of expenditure in regards to the variable costs that depends on the changes in the

actual amount of revenue that is incurred. A flexible budget is prepared at the end of each

accounting period and this particular budget involves preparation in accordance to the inputs.

The flexible budget is next compared to the actual revenue incurred for the purpose of

controlling the expenditures. Some of the benefits of the flexible budgets are that a flexible

budget is useful for those businesses whose costs are closely related to the level of business

activity. This particular method of budgeting also is useful in measuring the effectiveness of the

services provided by the employees or the staff. Moreover, a flexible budget can be very easily

updated (Barr and McClellan 2018).

nurses and other staff so that they can understand the degree of difference in behavior and

service between the patients of the general surgical ward and the short stay surgical ward (Parikh

2017).

Benefits of developing a cost centre budget

A cost centre budget might be beneficial for the nurse manger to control the expenditures

of the wards (Dafny, Ho and Lee 2017). The advantages of the cost centre budget are that the

implementation of a cost centre budget will help in the comparison of the performance of the

service unit in terms of the short stay surgical ward and the general surgical ward. A cost centre

budget will help the nurse manager in identifying the underperforming parts of the hospital or the

parts that require excessive un-estimated costs. A cost centre budget will help in the

identification of the centers that generate the largest amount of expenditure. The identification of

the cost centers will also facilitate the fact that the management of the hospital will be able to

target these centers as the primary areas where the cost management strategies could be applied.

A cost center budget also helps in improving the reaction speed. This is because the cost center

budget will help in the allocation of the most skilled and responsible staff that will try to reduce

the cost in facilitating such a center, which will in turn improve the reaction, speed. A cost center

budget will also enable the staff and the nurses to make decisions on their part, which will

increase the degree of motivation and thus enhance productivity.

Different methods of budgeting

A flexible budget refers to the particular budget that includes the calculation of the

different levels of expenditure in regards to the variable costs that depends on the changes in the

actual amount of revenue that is incurred. A flexible budget is prepared at the end of each

accounting period and this particular budget involves preparation in accordance to the inputs.

The flexible budget is next compared to the actual revenue incurred for the purpose of

controlling the expenditures. Some of the benefits of the flexible budgets are that a flexible

budget is useful for those businesses whose costs are closely related to the level of business

activity. This particular method of budgeting also is useful in measuring the effectiveness of the

services provided by the employees or the staff. Moreover, a flexible budget can be very easily

updated (Barr and McClellan 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CASE ANALYSIS

A particular disadvantage of the flexible budget is that the implementation of such a

budget is difficult to administer and formulate. A flexible budget cannot be aligned with any kind

of accounting software making the comparison of the financial statements with the budgeted

statements impossible. Moreover, a flexible budget cannot facilitate the comparison between the

actual revenue and the budgeted revenue due to the fact that the both the numbers are similar

(Barr and McClellan 2018).

Zero based budgeting refers to the particular method of budgeting in which the expenses

that are estimated to be incurred by a particular business entity for a new accounting period is

assumed to be zero. This means that the expenses for the new accounting period are calculated

on the basis of the actual expenses that are incurred rather than on incremental basis. The

advantages of zero based budgeting are that this particular method of budgeting will result in

focused operations, lower degree of costs, a controlled and disciplined execution of the business

strategies in regards to effective cost management. The disadvantages of zero based budgeting

can be listed down to the fact that this particular method of budgeting is resource intensive in

nature. Moreover, a zero based budget is exposed to a high degree of manipulation by the

managers of the organizations as it involves short term planning(Barr and McClellan 2018).

An output based budgeting refers to the particular method of budgeting that is dependent

on the performance by the employees or the staff of the organization. It is that method of

budgeting that ties the measurement of the individual or the departmental performance with the

particular process of budgeting.

The advantage of output based budgeting is that the amount that is allocated to a

particular department has a direct link with the departmental performance. This inspires the

department personnel to increase their all round productivity in order to obtain more monetary

benefits that may be allocated via the output based budgeting method. A disadvantage of the

output based budgeting is that this particular kind of budget is prepared from the baseline of the

organization and construct a request for the budget from each department. However, the ultimate

grant of the budgeted amount depends on the high-ranking officials of the management who may

manipulate the figures or take decisions that are exposed to political influences (Miller 2018).

Among the above mentioned three methods of budgeting, the particular method that

would be most suitable for the nurse manager to implement in the hospital is the flexible budget.

This is because the flexible budget essentially involves the preparation of the budget on the basis

A particular disadvantage of the flexible budget is that the implementation of such a

budget is difficult to administer and formulate. A flexible budget cannot be aligned with any kind

of accounting software making the comparison of the financial statements with the budgeted

statements impossible. Moreover, a flexible budget cannot facilitate the comparison between the

actual revenue and the budgeted revenue due to the fact that the both the numbers are similar

(Barr and McClellan 2018).

Zero based budgeting refers to the particular method of budgeting in which the expenses

that are estimated to be incurred by a particular business entity for a new accounting period is

assumed to be zero. This means that the expenses for the new accounting period are calculated

on the basis of the actual expenses that are incurred rather than on incremental basis. The

advantages of zero based budgeting are that this particular method of budgeting will result in

focused operations, lower degree of costs, a controlled and disciplined execution of the business

strategies in regards to effective cost management. The disadvantages of zero based budgeting

can be listed down to the fact that this particular method of budgeting is resource intensive in

nature. Moreover, a zero based budget is exposed to a high degree of manipulation by the

managers of the organizations as it involves short term planning(Barr and McClellan 2018).

An output based budgeting refers to the particular method of budgeting that is dependent

on the performance by the employees or the staff of the organization. It is that method of

budgeting that ties the measurement of the individual or the departmental performance with the

particular process of budgeting.

The advantage of output based budgeting is that the amount that is allocated to a

particular department has a direct link with the departmental performance. This inspires the

department personnel to increase their all round productivity in order to obtain more monetary

benefits that may be allocated via the output based budgeting method. A disadvantage of the

output based budgeting is that this particular kind of budget is prepared from the baseline of the

organization and construct a request for the budget from each department. However, the ultimate

grant of the budgeted amount depends on the high-ranking officials of the management who may

manipulate the figures or take decisions that are exposed to political influences (Miller 2018).

Among the above mentioned three methods of budgeting, the particular method that

would be most suitable for the nurse manager to implement in the hospital is the flexible budget.

This is because the flexible budget essentially involves the preparation of the budget on the basis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CASE ANALYSIS

of the level of activities that are performed in the field of work. Therefore, this is the suitable

method of budgeting.

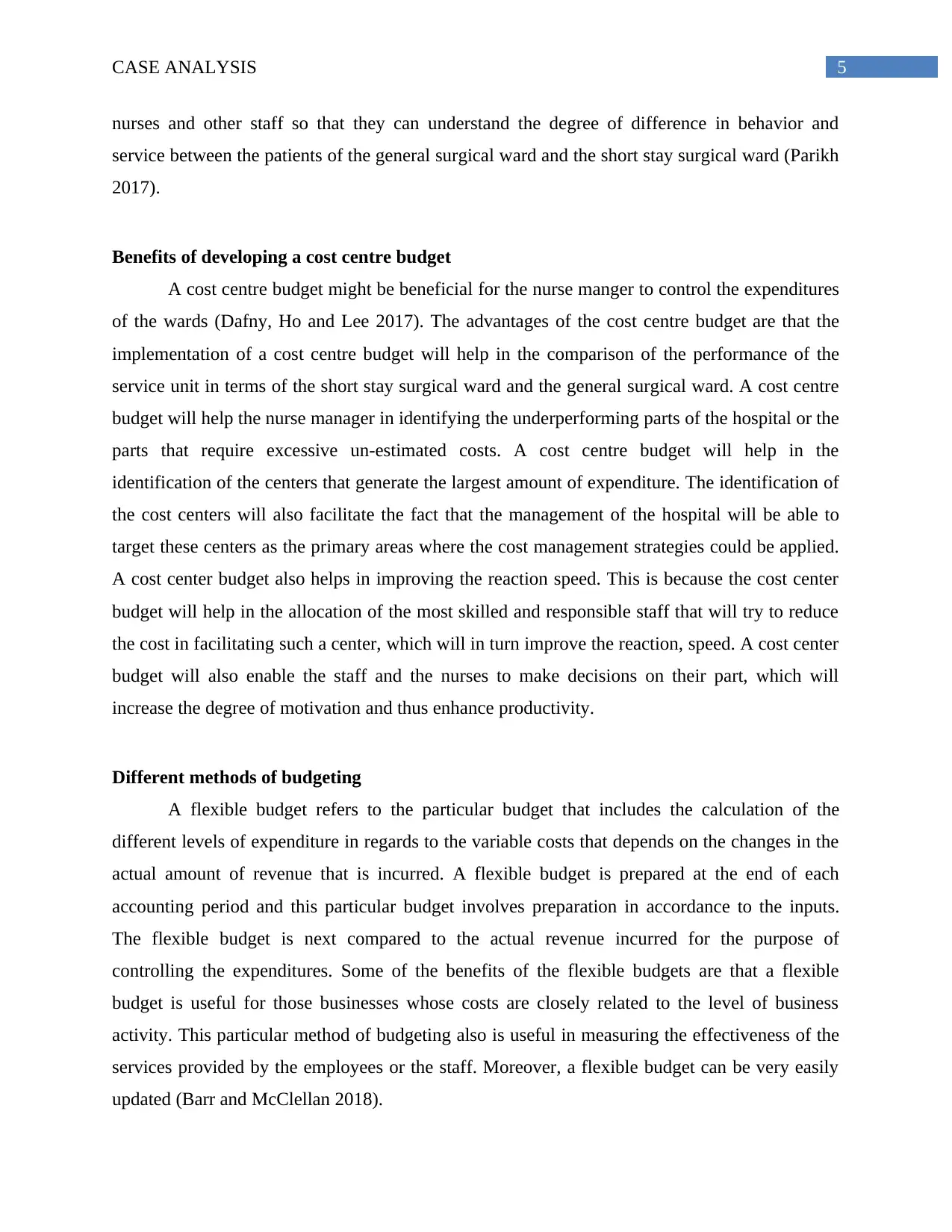

The three main areas of expenditure that may be considered while developing a cost

centre budget are the expenditure related to the different surgeries that might have to be

conducted for the patients in the general surgical ward; the expenditures related to the general

pharmacy that will be installed within the hospital for the welfare of the patients. Moreover, the

third major area that should be considered is that the expenditure in relation to the emergency

ward should also be considered as the most critical medical cases are conducted here. Moreover,

this is the ward where the most valuable medical equipments and applications are placed, the

maintenance of which requires sufficient cost.

An example of the cost center budget has been shown below that may be applied in case

of the private hospital.

Figure: Cost center budget

Source:

Salaries and Wage budget

Salaries and Wage

Budget

Basic Salary 10500

of the level of activities that are performed in the field of work. Therefore, this is the suitable

method of budgeting.

The three main areas of expenditure that may be considered while developing a cost

centre budget are the expenditure related to the different surgeries that might have to be

conducted for the patients in the general surgical ward; the expenditures related to the general

pharmacy that will be installed within the hospital for the welfare of the patients. Moreover, the

third major area that should be considered is that the expenditure in relation to the emergency

ward should also be considered as the most critical medical cases are conducted here. Moreover,

this is the ward where the most valuable medical equipments and applications are placed, the

maintenance of which requires sufficient cost.

An example of the cost center budget has been shown below that may be applied in case

of the private hospital.

Figure: Cost center budget

Source:

Salaries and Wage budget

Salaries and Wage

Budget

Basic Salary 10500

8CASE ANALYSIS

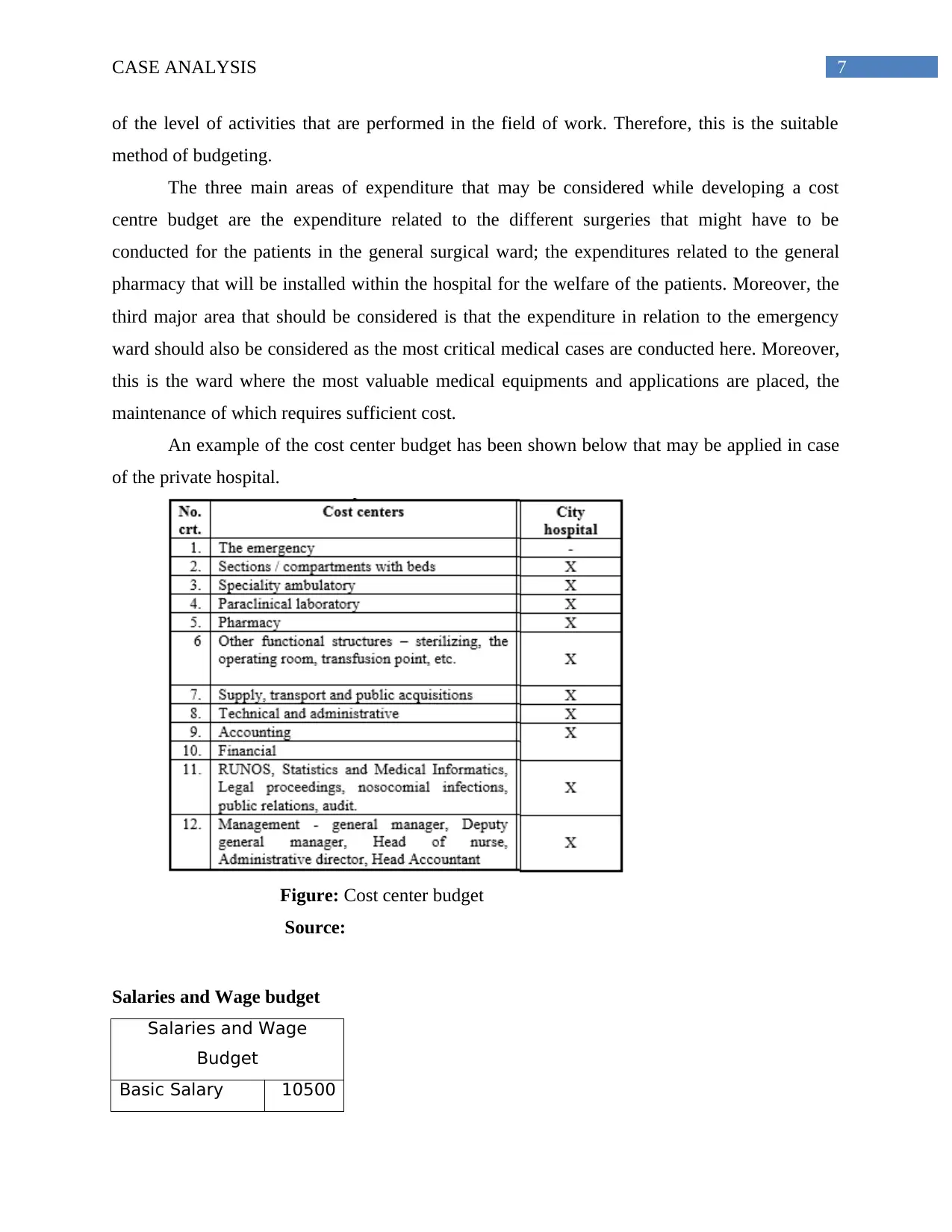

Inflation

Allowance 3000

Night

Allowance

150/

hoour

Technical

Allowance 979

Tiffin Allowance 45

Overtime

Allowance

4086/

day

Dearness

allowance 331

Uniform

Allowance 1350

Total salary 20441

The salaries and wage budget that has been prepared above consist of the mandatory

remuneration components that should be received by a personnel in the health care sector. The

assumptions have been made on the basis of the different salary components that are given by

reputed health care institutions in Australia. Moreover, the overtime allowance that has been

included in this particular table indicates the extra monetary benefit that will be received by the

staff. This is on account of the fact that the nurses might have to do overtime duty on the account

of the fact that the work space now has been expanded into an additional unit of short stay

surgical ward (Dafny, Ho and Lee 2017).

Conclusion

The conclusion that can be arrived at from the discussions in the preceding paragraphs is

that setting up or expanding a health care facility in Australia is a rigorous process. Beginning

from planning the facility to the preparation of the salaries and wage budget requires skilled

analysis and evaluation. However, the service provided by these health care facilities and the

hospitals is commendable and should be praised for the welfare carried out by these entities.

Inflation

Allowance 3000

Night

Allowance

150/

hoour

Technical

Allowance 979

Tiffin Allowance 45

Overtime

Allowance

4086/

day

Dearness

allowance 331

Uniform

Allowance 1350

Total salary 20441

The salaries and wage budget that has been prepared above consist of the mandatory

remuneration components that should be received by a personnel in the health care sector. The

assumptions have been made on the basis of the different salary components that are given by

reputed health care institutions in Australia. Moreover, the overtime allowance that has been

included in this particular table indicates the extra monetary benefit that will be received by the

staff. This is on account of the fact that the nurses might have to do overtime duty on the account

of the fact that the work space now has been expanded into an additional unit of short stay

surgical ward (Dafny, Ho and Lee 2017).

Conclusion

The conclusion that can be arrived at from the discussions in the preceding paragraphs is

that setting up or expanding a health care facility in Australia is a rigorous process. Beginning

from planning the facility to the preparation of the salaries and wage budget requires skilled

analysis and evaluation. However, the service provided by these health care facilities and the

hospitals is commendable and should be praised for the welfare carried out by these entities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CASE ANALYSIS

References

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher education.

John Wiley & Sons.

Dafny, L., Ho, K. and Lee, R.S., 2017. The price effects of cross-market mergers: Theory and

evidence from the hospital industry.

Kalyani, P., 2015. A study on implementation of community health insurance scheme in the

cardiology department of a tertiary care government hospital. JOURNAL OF EVOLUTION OF

MEDICAL AND DENTAL SCIENCES-JEMDS, 4(18), pp.3124-3133.

Kaur, A., 2015. Computerized Hospital Management Information System-Public And Private

Sector. Global Journal of Computer Science Research & Technology, pp.1123-1134.

Kumar, V., Patil, R., Patil, M., Mudbi, S., Kaveri, C. and Patil, S., 2014. Pattern of antibiotics

usage in bidar institute of medical sciences,(BRIMS) teaching hospital, Bidar. Journal of

Evolution of Medical and Dental Sciences, 3(29), pp.8122-8126.

Miller, G., 2018. Performance based budgeting. Routledge.

Ó hAlmhain, O., 2015. Medication safety officer in an Irish hospital: a financial cost-benefit

appraisal (Doctoral dissertation, The Institute of Public Administration).

Poola, D., Garg, S.K., Buyya, R., Yang, Y. and Ramamohanarao, K., 2014, May. Robust

scheduling of scientific workflows with deadline and budget constraints in clouds. In Advanced

Information Networking and Applications (AINA), 2014 IEEE 28th International Conference on

(pp. 858-865). IEEE.

Shah, J.N., 2017. Taking Specialist Surgical Services to the Rural District Hospitals at One Forth

Cost: A Sustainable ‘Return on Investment’Public Health Initiative of Patan Hospital, Patan

Academy of Health Sciences, Nepal. Kathmandu University Medical Journal, 13(2), pp.186-192.

Singh, S., Ahalawat, I., Singh, B., Singh, S. and Chauhan, A., 2015. Study of Cost Analysis of in

House Dieteary Services in a Tertiary Care Academic Hospital.

Song, J., Qiu, Y. and Liu, Z., 2016. Integrating optimal simulation budget allocation and genetic

algorithm to find the approximate Pareto patient flow distribution. IEEE Transactions on

Automation Science and Engineering, 13(1), pp.149-159.

References

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher education.

John Wiley & Sons.

Dafny, L., Ho, K. and Lee, R.S., 2017. The price effects of cross-market mergers: Theory and

evidence from the hospital industry.

Kalyani, P., 2015. A study on implementation of community health insurance scheme in the

cardiology department of a tertiary care government hospital. JOURNAL OF EVOLUTION OF

MEDICAL AND DENTAL SCIENCES-JEMDS, 4(18), pp.3124-3133.

Kaur, A., 2015. Computerized Hospital Management Information System-Public And Private

Sector. Global Journal of Computer Science Research & Technology, pp.1123-1134.

Kumar, V., Patil, R., Patil, M., Mudbi, S., Kaveri, C. and Patil, S., 2014. Pattern of antibiotics

usage in bidar institute of medical sciences,(BRIMS) teaching hospital, Bidar. Journal of

Evolution of Medical and Dental Sciences, 3(29), pp.8122-8126.

Miller, G., 2018. Performance based budgeting. Routledge.

Ó hAlmhain, O., 2015. Medication safety officer in an Irish hospital: a financial cost-benefit

appraisal (Doctoral dissertation, The Institute of Public Administration).

Poola, D., Garg, S.K., Buyya, R., Yang, Y. and Ramamohanarao, K., 2014, May. Robust

scheduling of scientific workflows with deadline and budget constraints in clouds. In Advanced

Information Networking and Applications (AINA), 2014 IEEE 28th International Conference on

(pp. 858-865). IEEE.

Shah, J.N., 2017. Taking Specialist Surgical Services to the Rural District Hospitals at One Forth

Cost: A Sustainable ‘Return on Investment’Public Health Initiative of Patan Hospital, Patan

Academy of Health Sciences, Nepal. Kathmandu University Medical Journal, 13(2), pp.186-192.

Singh, S., Ahalawat, I., Singh, B., Singh, S. and Chauhan, A., 2015. Study of Cost Analysis of in

House Dieteary Services in a Tertiary Care Academic Hospital.

Song, J., Qiu, Y. and Liu, Z., 2016. Integrating optimal simulation budget allocation and genetic

algorithm to find the approximate Pareto patient flow distribution. IEEE Transactions on

Automation Science and Engineering, 13(1), pp.149-159.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CASE ANALYSIS

Sudheer, G., Prabhu, G.R. and Sridhar, M.S., 2015. A study of prescription writing practices of

doctors in geriatric age group patients in a teaching hospital. Jour of Evolution of Medical and

Dental Sciences, 4(3), pp.322-8.

Sudheer, G., Prabhu, G.R. and Sridhar, M.S., 2015. A study of prescription writing practices of

doctors in geriatric age group patients in a teaching hospital. Jour of Evolution of Medical and

Dental Sciences, 4(3), pp.322-8.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.