Corporate Finance: Evaluating Exchange Rate Risk and Hedging Options

VerifiedAdded on 2023/05/30

|4

|1014

|276

Case Study

AI Summary

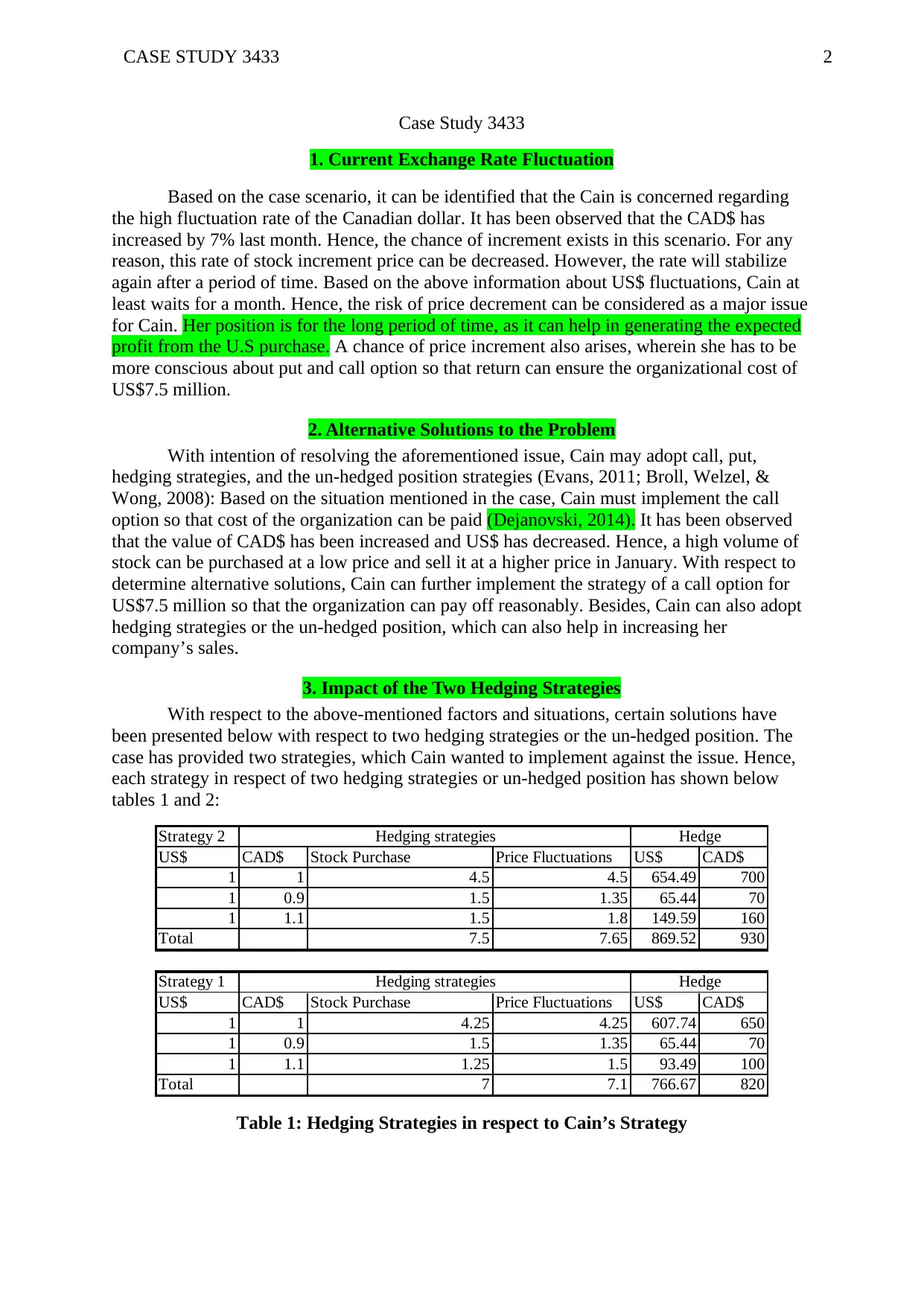

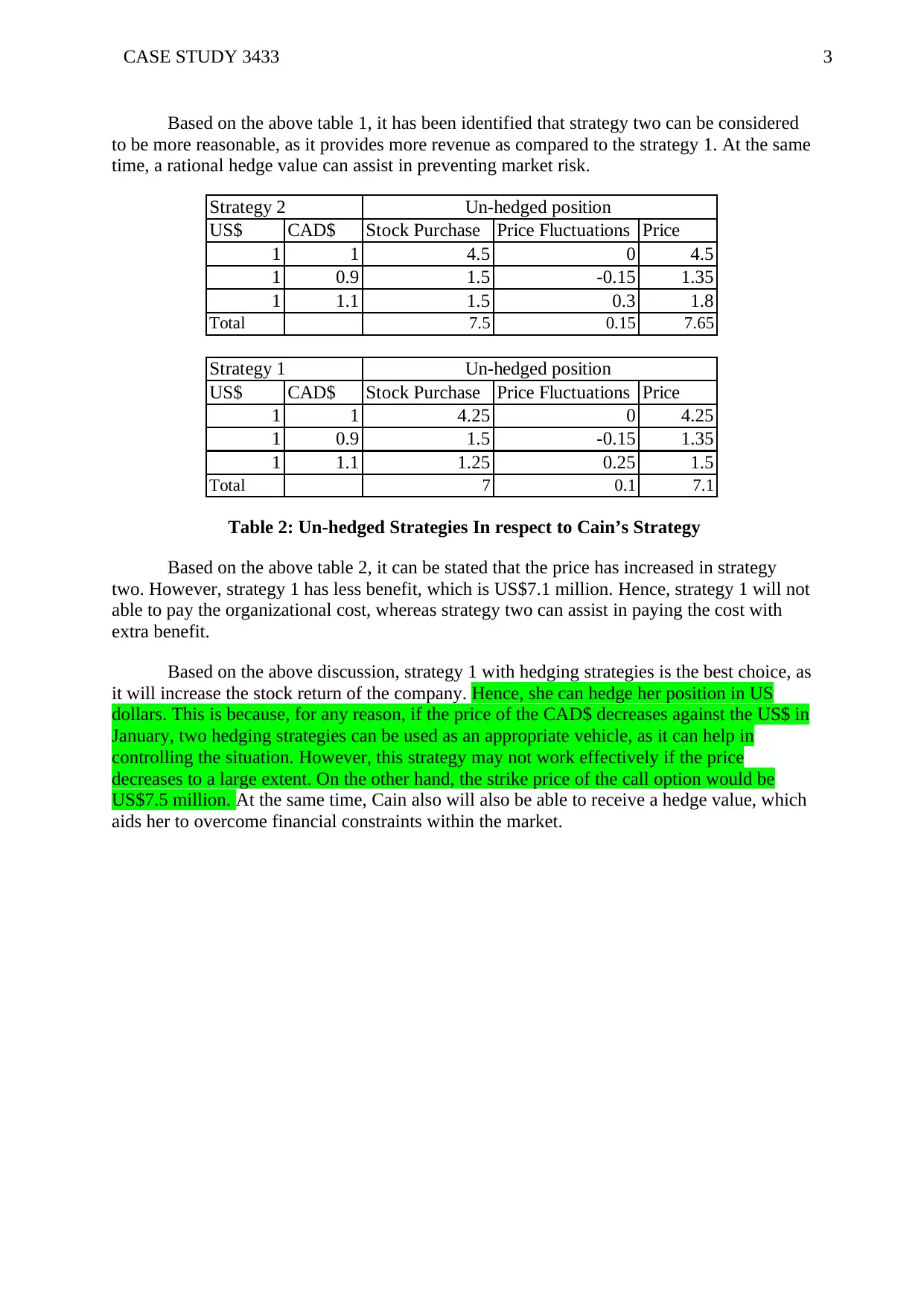

This case study delves into the concerns of Cain regarding the high fluctuation rate of the Canadian dollar and its impact on a U.S. purchase. It identifies the potential risks associated with waiting for the exchange rate to stabilize, including the possibility of price decrement. The study explores alternative solutions such as call options, put options, and hedging strategies to mitigate these risks. It further analyzes the impact of two hedging strategies versus an un-hedged position, concluding that a hedging strategy is the best choice to increase the stock return of the company and manage potential financial constraints. The analysis includes tables illustrating the potential outcomes of different strategies, providing a comprehensive evaluation of the financial implications.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.