Acc200 Case Study: Beztec Limited - Printer Costing and Profitability

VerifiedAdded on 2020/10/22

|10

|2782

|459

Case Study

AI Summary

This case study analyzes the costing methods of Beztec Limited, a company producing two printer models, Lexon and Protox. The report compares traditional costing with activity-based costing (ABC) to determine the profitability of each model and provide recommendations. The analysis includes calculating cost driver rates, determining the cost of each model using ABC, and performing profitability analyses. The study highlights the importance of accurate product costing and addresses the problems associated with traditional costing systems. It also examines ethical considerations, specifically the APES 110 Code of Ethics, and suggests ways to dispose of over/under overhead costs. The conclusion recommends phasing out the less profitable Protox model and emphasizes the importance of ethical decision-making in financial management.

Case Study Acc200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Importance of accurate product costing and problems associated with using traditional

costing system.............................................................................................................................1

2. Cost driver rates for various activities in ABC system...........................................................2

3. Calculation of cost of each model using ABC........................................................................3

4. Profitability analyses...............................................................................................................3

5. Suggestions and Recommendations........................................................................................4

6. Ways to dispose the amount of over/under overhead costs....................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Importance of accurate product costing and problems associated with using traditional

costing system.............................................................................................................................1

2. Cost driver rates for various activities in ABC system...........................................................2

3. Calculation of cost of each model using ABC........................................................................3

4. Profitability analyses...............................................................................................................3

5. Suggestions and Recommendations........................................................................................4

6. Ways to dispose the amount of over/under overhead costs....................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

In this project report, traditional costing and modern costing methods are analysed in

order to provide solutions for the case. According to the given case scenario, Sue Smith is asking

for suggestions and recommendations. The primary aim of this report is to provide a

understanding about importance of activity based costing in this case scenario. Beztec Limited is

producing two types of printers and seek for advice that which model should be phased out.

Issues using traditional costing is discussed in this report along with cost drivers under activity

based costing. In order to analyse this case and develop recommendations various analyses is

performed such as profitability and costing (Ahamadzadeh, Etemadi and Pifeh, 2011). Hence, it

will cover accurate product costing and its importance, cost driver rates, predetermined

overhead, activity based costing framework etc.

MAIN BODY

1. Importance of accurate product costing and problems associated with using traditional costing

system

Product costing:

It is a methodology of managerial accounting which serve organisation to determine cost

involved in every good produced by them. This costing method is considered as significant as it

does not classify according to its nature but according to the related activity. Accurate costing

framework assist an organisation in staying more competitive and helps making smart choices in

relation to business organisation. It is more efficient and effective techniques which can help a

firm in meeting the set outcome in more standard forms meeting the present requirements. In this

case, Beztec Limited is producing two types of printers that is Lexon and Protox. This method is

used to ascertain costs and profit generated from these two models. Not only overall cost but it

also helps to calculate various kinds of cost such as direct material, labour, operating, selling cost

etc. Beztec is currently using traditional costing methods due to which they are facing few issues

as this technique has various drawbacks which are mentioned below:

Inaccurate costs – Traditional costing classifies overall costs into fixed and variable

expenses which is quite unrealistic as all the costs cannot be categorised into only two classes,

due to which it gives inaccurate results (Miller-Nobles, Mattison and Matsumura, 2016).

1

In this project report, traditional costing and modern costing methods are analysed in

order to provide solutions for the case. According to the given case scenario, Sue Smith is asking

for suggestions and recommendations. The primary aim of this report is to provide a

understanding about importance of activity based costing in this case scenario. Beztec Limited is

producing two types of printers and seek for advice that which model should be phased out.

Issues using traditional costing is discussed in this report along with cost drivers under activity

based costing. In order to analyse this case and develop recommendations various analyses is

performed such as profitability and costing (Ahamadzadeh, Etemadi and Pifeh, 2011). Hence, it

will cover accurate product costing and its importance, cost driver rates, predetermined

overhead, activity based costing framework etc.

MAIN BODY

1. Importance of accurate product costing and problems associated with using traditional costing

system

Product costing:

It is a methodology of managerial accounting which serve organisation to determine cost

involved in every good produced by them. This costing method is considered as significant as it

does not classify according to its nature but according to the related activity. Accurate costing

framework assist an organisation in staying more competitive and helps making smart choices in

relation to business organisation. It is more efficient and effective techniques which can help a

firm in meeting the set outcome in more standard forms meeting the present requirements. In this

case, Beztec Limited is producing two types of printers that is Lexon and Protox. This method is

used to ascertain costs and profit generated from these two models. Not only overall cost but it

also helps to calculate various kinds of cost such as direct material, labour, operating, selling cost

etc. Beztec is currently using traditional costing methods due to which they are facing few issues

as this technique has various drawbacks which are mentioned below:

Inaccurate costs – Traditional costing classifies overall costs into fixed and variable

expenses which is quite unrealistic as all the costs cannot be categorised into only two classes,

due to which it gives inaccurate results (Miller-Nobles, Mattison and Matsumura, 2016).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

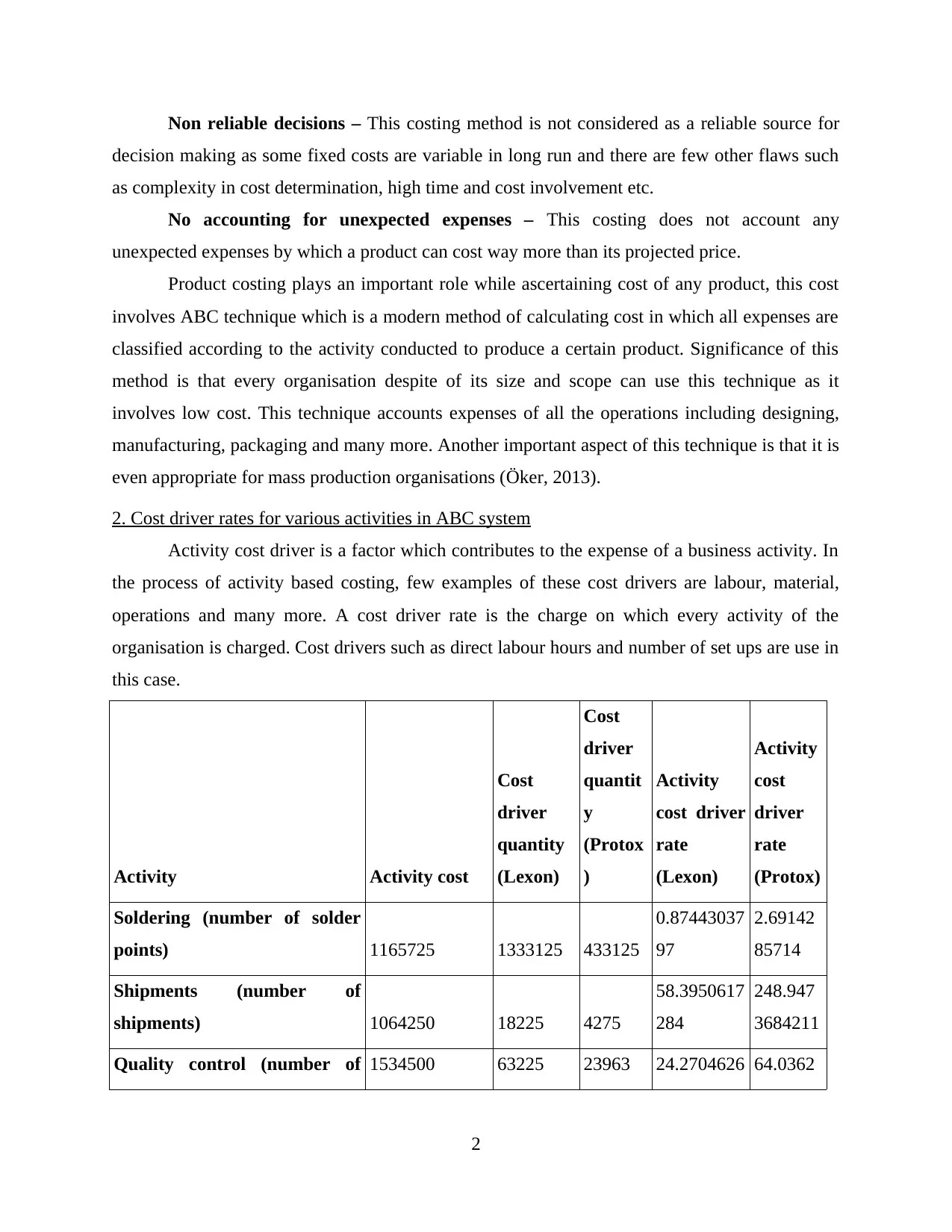

Non reliable decisions – This costing method is not considered as a reliable source for

decision making as some fixed costs are variable in long run and there are few other flaws such

as complexity in cost determination, high time and cost involvement etc.

No accounting for unexpected expenses – This costing does not account any

unexpected expenses by which a product can cost way more than its projected price.

Product costing plays an important role while ascertaining cost of any product, this cost

involves ABC technique which is a modern method of calculating cost in which all expenses are

classified according to the activity conducted to produce a certain product. Significance of this

method is that every organisation despite of its size and scope can use this technique as it

involves low cost. This technique accounts expenses of all the operations including designing,

manufacturing, packaging and many more. Another important aspect of this technique is that it is

even appropriate for mass production organisations (Öker, 2013).

2. Cost driver rates for various activities in ABC system

Activity cost driver is a factor which contributes to the expense of a business activity. In

the process of activity based costing, few examples of these cost drivers are labour, material,

operations and many more. A cost driver rate is the charge on which every activity of the

organisation is charged. Cost drivers such as direct labour hours and number of set ups are use in

this case.

Activity Activity cost

Cost

driver

quantity

(Lexon)

Cost

driver

quantit

y

(Protox

)

Activity

cost driver

rate

(Lexon)

Activity

cost

driver

rate

(Protox)

Soldering (number of solder

points) 1165725 1333125 433125

0.87443037

97

2.69142

85714

Shipments (number of

shipments) 1064250 18225 4275

58.3950617

284

248.947

3684211

Quality control (number of 1534500 63225 23963 24.2704626 64.0362

2

decision making as some fixed costs are variable in long run and there are few other flaws such

as complexity in cost determination, high time and cost involvement etc.

No accounting for unexpected expenses – This costing does not account any

unexpected expenses by which a product can cost way more than its projected price.

Product costing plays an important role while ascertaining cost of any product, this cost

involves ABC technique which is a modern method of calculating cost in which all expenses are

classified according to the activity conducted to produce a certain product. Significance of this

method is that every organisation despite of its size and scope can use this technique as it

involves low cost. This technique accounts expenses of all the operations including designing,

manufacturing, packaging and many more. Another important aspect of this technique is that it is

even appropriate for mass production organisations (Öker, 2013).

2. Cost driver rates for various activities in ABC system

Activity cost driver is a factor which contributes to the expense of a business activity. In

the process of activity based costing, few examples of these cost drivers are labour, material,

operations and many more. A cost driver rate is the charge on which every activity of the

organisation is charged. Cost drivers such as direct labour hours and number of set ups are use in

this case.

Activity Activity cost

Cost

driver

quantity

(Lexon)

Cost

driver

quantit

y

(Protox

)

Activity

cost driver

rate

(Lexon)

Activity

cost

driver

rate

(Protox)

Soldering (number of solder

points) 1165725 1333125 433125

0.87443037

97

2.69142

85714

Shipments (number of

shipments) 1064250 18225 4275

58.3950617

284

248.947

3684211

Quality control (number of 1534500 63225 23963 24.2704626 64.0362

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

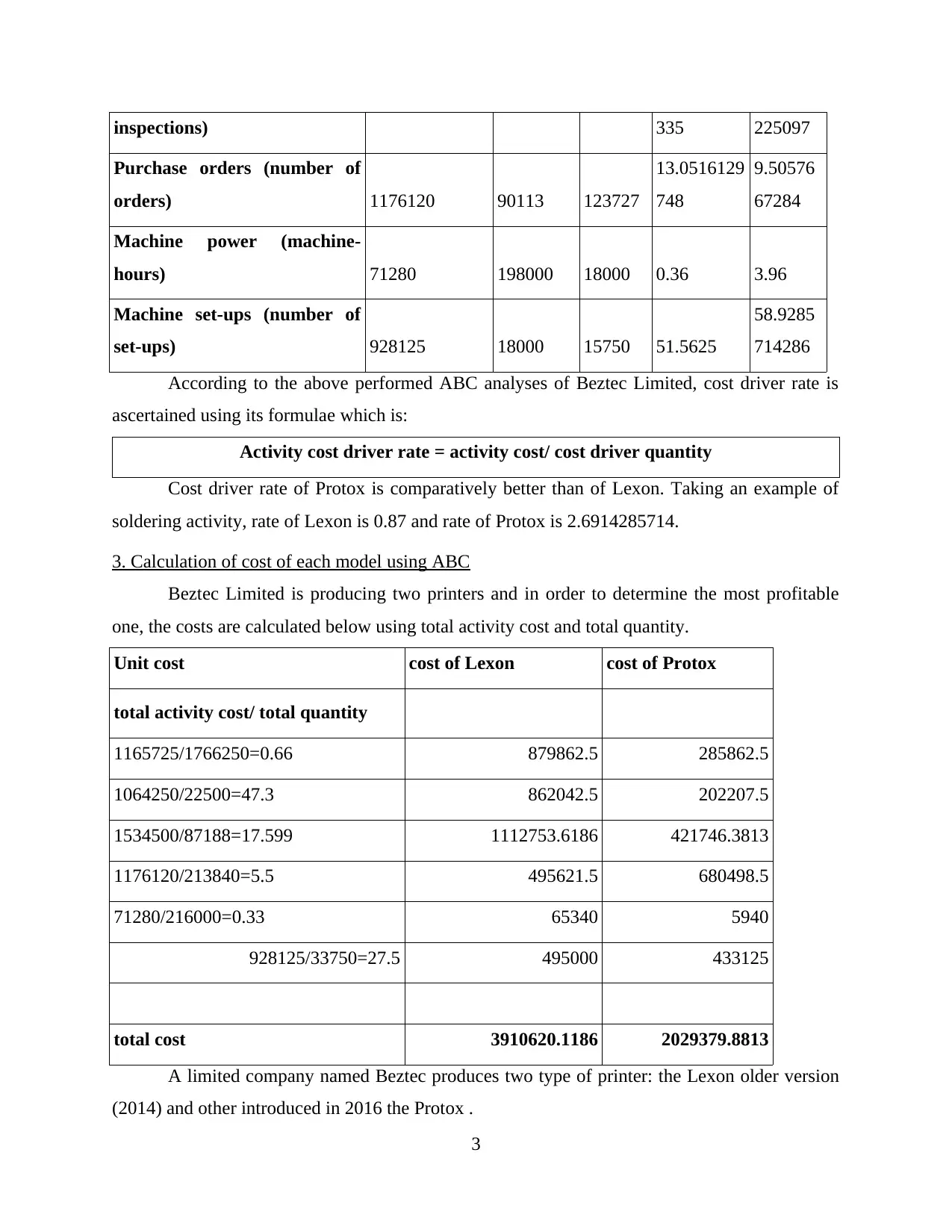

inspections) 335 225097

Purchase orders (number of

orders) 1176120 90113 123727

13.0516129

748

9.50576

67284

Machine power (machine-

hours) 71280 198000 18000 0.36 3.96

Machine set-ups (number of

set-ups) 928125 18000 15750 51.5625

58.9285

714286

According to the above performed ABC analyses of Beztec Limited, cost driver rate is

ascertained using its formulae which is:

Activity cost driver rate = activity cost/ cost driver quantity

Cost driver rate of Protox is comparatively better than of Lexon. Taking an example of

soldering activity, rate of Lexon is 0.87 and rate of Protox is 2.6914285714.

3. Calculation of cost of each model using ABC

Beztec Limited is producing two printers and in order to determine the most profitable

one, the costs are calculated below using total activity cost and total quantity.

Unit cost cost of Lexon cost of Protox

total activity cost/ total quantity

1165725/1766250=0.66 879862.5 285862.5

1064250/22500=47.3 862042.5 202207.5

1534500/87188=17.599 1112753.6186 421746.3813

1176120/213840=5.5 495621.5 680498.5

71280/216000=0.33 65340 5940

928125/33750=27.5 495000 433125

total cost 3910620.1186 2029379.8813

A limited company named Beztec produces two type of printer: the Lexon older version

(2014) and other introduced in 2016 the Protox .

3

Purchase orders (number of

orders) 1176120 90113 123727

13.0516129

748

9.50576

67284

Machine power (machine-

hours) 71280 198000 18000 0.36 3.96

Machine set-ups (number of

set-ups) 928125 18000 15750 51.5625

58.9285

714286

According to the above performed ABC analyses of Beztec Limited, cost driver rate is

ascertained using its formulae which is:

Activity cost driver rate = activity cost/ cost driver quantity

Cost driver rate of Protox is comparatively better than of Lexon. Taking an example of

soldering activity, rate of Lexon is 0.87 and rate of Protox is 2.6914285714.

3. Calculation of cost of each model using ABC

Beztec Limited is producing two printers and in order to determine the most profitable

one, the costs are calculated below using total activity cost and total quantity.

Unit cost cost of Lexon cost of Protox

total activity cost/ total quantity

1165725/1766250=0.66 879862.5 285862.5

1064250/22500=47.3 862042.5 202207.5

1534500/87188=17.599 1112753.6186 421746.3813

1176120/213840=5.5 495621.5 680498.5

71280/216000=0.33 65340 5940

928125/33750=27.5 495000 433125

total cost 3910620.1186 2029379.8813

A limited company named Beztec produces two type of printer: the Lexon older version

(2014) and other introduced in 2016 the Protox .

3

During complete analysis for both printer, company should phased out the production of

Protox printer for a period of time as the actual profit generation rate of Protox (30%) is much

lower than that of Lexon(36.667%) approx. However, the cost of production for Protox is

2029379.8813 which is less than the production cost of Lexon(RS 3910620.1186) because

number of unit produced are much higher of Lexon than those of Protox. So company should

focus to produce more unit of Lexon printer and earn more amount of profit and recover the cost

of production.

4. Profitability analyses

In order to determine the profitability of both the printers, ABC system is used by which

it is ascertained that gross profit for Lexon is 8712000 and for Protox is 2257200.

Gross profit percentage Gross profit / revenue *100

Gross profit percentage for Lexon 8712000/2376000*100 36.67%

Gross profit percentage forProtox 2257200/7524000*100 30.00%

According to the above performed profitability analyses, it has been observed that Lexon

is earning more profit than Protox that is 36.67% and 30.00%. Smith should try to convince Kay

that they should phase out their newly launched printer model that is Protox as it is less

profitable than Lexon.

5. Suggestions and Recommendations

In this case scenario, Sue Smith is an accountant of Beztec Limited who advised CEO of

this company to phase out their new printer model i.e. Protex as it is resulting in decline stage

and losses. Steven Kay, CEO of this company pressurise Smith to come up with an alternative as

this new product printer cannot be phased out because it help in earning bonus to Kay. With the

help of ABC method, Smith has ensured that the newly launched printer is not beneficial for the

organisation and it must be phased out unless there is any other solution (Proctor, 2012). In order

to convince Kay, there are various Code of ethics which are conveyed and they are discussed

below:

4

Protox printer for a period of time as the actual profit generation rate of Protox (30%) is much

lower than that of Lexon(36.667%) approx. However, the cost of production for Protox is

2029379.8813 which is less than the production cost of Lexon(RS 3910620.1186) because

number of unit produced are much higher of Lexon than those of Protox. So company should

focus to produce more unit of Lexon printer and earn more amount of profit and recover the cost

of production.

4. Profitability analyses

In order to determine the profitability of both the printers, ABC system is used by which

it is ascertained that gross profit for Lexon is 8712000 and for Protox is 2257200.

Gross profit percentage Gross profit / revenue *100

Gross profit percentage for Lexon 8712000/2376000*100 36.67%

Gross profit percentage forProtox 2257200/7524000*100 30.00%

According to the above performed profitability analyses, it has been observed that Lexon

is earning more profit than Protox that is 36.67% and 30.00%. Smith should try to convince Kay

that they should phase out their newly launched printer model that is Protox as it is less

profitable than Lexon.

5. Suggestions and Recommendations

In this case scenario, Sue Smith is an accountant of Beztec Limited who advised CEO of

this company to phase out their new printer model i.e. Protex as it is resulting in decline stage

and losses. Steven Kay, CEO of this company pressurise Smith to come up with an alternative as

this new product printer cannot be phased out because it help in earning bonus to Kay. With the

help of ABC method, Smith has ensured that the newly launched printer is not beneficial for the

organisation and it must be phased out unless there is any other solution (Proctor, 2012). In order

to convince Kay, there are various Code of ethics which are conveyed and they are discussed

below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APES 110 Code of Ethics for Professional Accountants are few standards which are

issued by regulatory board. These codes were introduced by APESB which is a individual body

established in 2006 in Australia. These codes were made with an objective to bring similarity in

the accounting books of all the organisation. These standards are quite different from basic

accounting standards as these deals with ethical issues. For example, accountant is said to present

true and fair position and performance of an organisation despite of pressure from superiors.

These codes and standards are applied to all the members. Members of this association are said

to be individuals who are working as an accountant in any organisation (Plank, 2018). Few of

these codes are:

Integrity – According to this code of ethics, an accountant is said to produce reliable and

accurate financial statements. Accountants should be honest and straightforward with their

superior and external audit bodies. This code should be followed in all the organisational

operations. In this case, Smith should not be get pressurised from Kay's orders and follow what

is right.

Objectivity – Under this code of ethics, accountant shall not allow bias or do not interest

any individual due to any reason such as influence or greed. According to this case scenario,

Smith should convey code of ethics to Kay which are needed to be followed by her

(Suthummanon, 2011).

Professional competence – Every accountant should has a reliable knowledge and skills

up to required level so that they can be provide appropriate effective services to their clients.

These skills include diligence and technical knowledge.

Confidentiality – This is considered as the most significant ethical code as it states that

all organisational data should not be disclosed to any other party in order to protect the sensitive

information. Smith has a responsibility to secure the data of Beztec Limited, and do not disclose

it unless there is a legal requirement for that.

Professional behaviour – This code of ethics states that Kay should comply all the laws

and legislations regarding preparation of accounting statements so that she can credit to her

profession (Terpstra, 2014).

6. Ways to dispose the amount of over/under overhead costs

Overhead rate: It is said to be total indirect costs for a particular reporting period

divided by proper allocation measure. It can be comprised of either using actual cost or budgeted

5

issued by regulatory board. These codes were introduced by APESB which is a individual body

established in 2006 in Australia. These codes were made with an objective to bring similarity in

the accounting books of all the organisation. These standards are quite different from basic

accounting standards as these deals with ethical issues. For example, accountant is said to present

true and fair position and performance of an organisation despite of pressure from superiors.

These codes and standards are applied to all the members. Members of this association are said

to be individuals who are working as an accountant in any organisation (Plank, 2018). Few of

these codes are:

Integrity – According to this code of ethics, an accountant is said to produce reliable and

accurate financial statements. Accountants should be honest and straightforward with their

superior and external audit bodies. This code should be followed in all the organisational

operations. In this case, Smith should not be get pressurised from Kay's orders and follow what

is right.

Objectivity – Under this code of ethics, accountant shall not allow bias or do not interest

any individual due to any reason such as influence or greed. According to this case scenario,

Smith should convey code of ethics to Kay which are needed to be followed by her

(Suthummanon, 2011).

Professional competence – Every accountant should has a reliable knowledge and skills

up to required level so that they can be provide appropriate effective services to their clients.

These skills include diligence and technical knowledge.

Confidentiality – This is considered as the most significant ethical code as it states that

all organisational data should not be disclosed to any other party in order to protect the sensitive

information. Smith has a responsibility to secure the data of Beztec Limited, and do not disclose

it unless there is a legal requirement for that.

Professional behaviour – This code of ethics states that Kay should comply all the laws

and legislations regarding preparation of accounting statements so that she can credit to her

profession (Terpstra, 2014).

6. Ways to dispose the amount of over/under overhead costs

Overhead rate: It is said to be total indirect costs for a particular reporting period

divided by proper allocation measure. It can be comprised of either using actual cost or budgeted

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

one. All the indirect costs of fixed expenditure of a business is included such as management and

marketing costs. It is categorising into two parts. Some of them are discussed underneath:

Over applied overhead: It is said to be additional amount of overhead applied during

manufacturing over actual overhead incurred during that particular point of time. On the

other hand, it is the amount that is over estimated from the actual rate for a production

period (Whitecotton, 2011).

Under applied overhead: It is a kind of situation under which overhead applied to work

in progress goods is less than the actual WIP. This is reported on balance sheet as in the

form of prepaid expenses. During the closing period of time, under applied overhead is

being balanced through creating a debit to COGS (Cost of goods sold).

It is necessary to make analyses of over and under applied overhead account that should

end during the period of time. There are various ways to dispose the amount of over and under

applied overhead costs. Some of them are mentioned underneath:

Allocation among WIP (Work in progress), finished goods and COGS: Under this

particular approach, the amount of over and under applied overhead is disposed of through

allocating it within WIP accounts on the basis of overhead applied in every of the account during

that period of time. This approach is more reliable from other methods. The only limitation of

this is that is more time taken activity.

Transfer the whole amount of over or under-applied to cost of goods sold: According

to this method, the company need to transfer all their net amount of over and under applied to

COGS. In this particular situation below mentioned entries must be passed.

In case overhead is under-applied:

Cost of goods sold a/c…………………Dr

To manufacturing overhead A/c………...Cr.

In over-applied:

6

marketing costs. It is categorising into two parts. Some of them are discussed underneath:

Over applied overhead: It is said to be additional amount of overhead applied during

manufacturing over actual overhead incurred during that particular point of time. On the

other hand, it is the amount that is over estimated from the actual rate for a production

period (Whitecotton, 2011).

Under applied overhead: It is a kind of situation under which overhead applied to work

in progress goods is less than the actual WIP. This is reported on balance sheet as in the

form of prepaid expenses. During the closing period of time, under applied overhead is

being balanced through creating a debit to COGS (Cost of goods sold).

It is necessary to make analyses of over and under applied overhead account that should

end during the period of time. There are various ways to dispose the amount of over and under

applied overhead costs. Some of them are mentioned underneath:

Allocation among WIP (Work in progress), finished goods and COGS: Under this

particular approach, the amount of over and under applied overhead is disposed of through

allocating it within WIP accounts on the basis of overhead applied in every of the account during

that period of time. This approach is more reliable from other methods. The only limitation of

this is that is more time taken activity.

Transfer the whole amount of over or under-applied to cost of goods sold: According

to this method, the company need to transfer all their net amount of over and under applied to

COGS. In this particular situation below mentioned entries must be passed.

In case overhead is under-applied:

Cost of goods sold a/c…………………Dr

To manufacturing overhead A/c………...Cr.

In over-applied:

6

Manufacturing overhead A/c……………Dr

To cost of goods sold a/c…………………Cr

This particular method is not so effective for the companies as compare to first method.

Most of the companies can uses this because of economic cost and easy operations. To reduce

per units cost of production, the company has to reduce the unit cost while manufacturing a

product. This will lead to dispose of over and under applied overhead rate within an organisation.

Immaterial balance: In case in the production overhead, costs which are taken into

account are considered as immaterial and is adjusted to COGS. If the outcomes of overhead are

over applied, then it is transferred as credit balance to cost of goods sold. The choice of method

is being associated with the materiality of the records. All the amount that is being analysed in

large amount can made impacts on decisions that are considered to be material (Immaterial

balance, 2015). Immaterial balance can be avoided by using modern techniques of costing such

as Activity based costing.

CONCLUSION

From the above project report, it has been observed that Kay, the CEO of Beztec Limited

is forcing the accountant that is Sue Smith to figure out some way so that they do no have to

phase out their new printer Protox as it helps to gain bonus. After performing various analyses

such as activity based costing and profitability analyses it can be recommended that Smith

should follow the code of ethics and convince their CEO to phase out low profitable printer and

provide evidences of various analyses.

7

To cost of goods sold a/c…………………Cr

This particular method is not so effective for the companies as compare to first method.

Most of the companies can uses this because of economic cost and easy operations. To reduce

per units cost of production, the company has to reduce the unit cost while manufacturing a

product. This will lead to dispose of over and under applied overhead rate within an organisation.

Immaterial balance: In case in the production overhead, costs which are taken into

account are considered as immaterial and is adjusted to COGS. If the outcomes of overhead are

over applied, then it is transferred as credit balance to cost of goods sold. The choice of method

is being associated with the materiality of the records. All the amount that is being analysed in

large amount can made impacts on decisions that are considered to be material (Immaterial

balance, 2015). Immaterial balance can be avoided by using modern techniques of costing such

as Activity based costing.

CONCLUSION

From the above project report, it has been observed that Kay, the CEO of Beztec Limited

is forcing the accountant that is Sue Smith to figure out some way so that they do no have to

phase out their new printer Protox as it helps to gain bonus. After performing various analyses

such as activity based costing and profitability analyses it can be recommended that Smith

should follow the code of ethics and convince their CEO to phase out low profitable printer and

provide evidences of various analyses.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Ahamadzadeh, T., Etemadi, H. and Pifeh, A., 2011. Exploration of factors influencing on choice

the activity-based costing system in Iranian organizations. International Journal of

Business Administration. 2(1). p.61.

Miller-Nobles, T. L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial &

Managerial Accounting: The Managerial Chapters. Pearson.

Öker, F. and Özyapici, H., 2013. A new costing model in hospital management: time-driven

activity-based costing system. The health care manager. 32(1). pp.23-36.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost Systems

(pp. 1-5). Springer Gabler, Wiesbaden.

Proctor, R., 2012. Managerial Accounting: Decision Makling and Performance Management.

FT Press.

Suthummanon, S., Ratanamanee, W., Boonyanuwat, N. and Saritprit, P., 2011. Applying

Activity-Based Costing (ABC) to a parawood furniture factory. The Engineering

Economist. 56(1). pp.80-93.

Terpstra, M. and Verbeeten, F.H., 2014. Customer satisfaction: Cost driver or value driver?

Empirical evidence from the financial services industry. European Management

Journal. 32(3). pp.499-508.

Whitecotton, S., Libby, R. and Phillips, F., 2011. Managerial accounting. McGraw-Hill Irwin.

Online

Immaterial balance. 2015. [Online]. Available through:

<https://www.bayt.com/en/specialties/q/204288/what-if-there-s-a-small-immaterial-

difference-in-a-trial-balance/>

8

Books and Journals

Ahamadzadeh, T., Etemadi, H. and Pifeh, A., 2011. Exploration of factors influencing on choice

the activity-based costing system in Iranian organizations. International Journal of

Business Administration. 2(1). p.61.

Miller-Nobles, T. L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial &

Managerial Accounting: The Managerial Chapters. Pearson.

Öker, F. and Özyapici, H., 2013. A new costing model in hospital management: time-driven

activity-based costing system. The health care manager. 32(1). pp.23-36.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost Systems

(pp. 1-5). Springer Gabler, Wiesbaden.

Proctor, R., 2012. Managerial Accounting: Decision Makling and Performance Management.

FT Press.

Suthummanon, S., Ratanamanee, W., Boonyanuwat, N. and Saritprit, P., 2011. Applying

Activity-Based Costing (ABC) to a parawood furniture factory. The Engineering

Economist. 56(1). pp.80-93.

Terpstra, M. and Verbeeten, F.H., 2014. Customer satisfaction: Cost driver or value driver?

Empirical evidence from the financial services industry. European Management

Journal. 32(3). pp.499-508.

Whitecotton, S., Libby, R. and Phillips, F., 2011. Managerial accounting. McGraw-Hill Irwin.

Online

Immaterial balance. 2015. [Online]. Available through:

<https://www.bayt.com/en/specialties/q/204288/what-if-there-s-a-small-immaterial-

difference-in-a-trial-balance/>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.