Adam & Co Case Study: Evaluating Expenditure Cycle Systems and Risks

VerifiedAdded on 2022/11/01

|17

|3385

|55

Case Study

AI Summary

This report presents a comprehensive analysis of Adam & Co's expenditure cycle, focusing on its purchase, cash disbursement, and payroll systems. It utilizes data flow diagrams and system flowcharts to illustrate the processes within each system. The study delves into the potential risks and weaknesses inherent in these systems, providing a detailed examination of internal control deficiencies. The report aims to assist the Chief Operating Officer (COO) in assessing the risks, processes, and internal controls within Adam & Co's expenditure cycle, offering insights into potential areas for improvement and risk mitigation. The case study covers key aspects such as inventory management, vendor relations, and financial transaction processing.

Case Study – Adam & Co 1

CASE STUDY – ADAM & CO

By (Student’s Name)

Professor’s Name

College

Course

Date

CASE STUDY – ADAM & CO

By (Student’s Name)

Professor’s Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study – Adam & Co 2

Executive Summary

This report has analysed Adam & Co business which is The Royal Bank of Scotland

PLC’s trading division and which caters for the need of private bank clients based on UK.

Adam & Co offers an array of private banking services that include discretionary investment

management alongside financial planning services to many high net worth customers in the

United Kingdom. It has a centralized accounting system with many networking terminals

located in different places in the UK and hence a deeper evaluation of Adam & Co expending

cycle process is essential in this case. The discussion focuses on the constituent system of

expending cycle including cash disbursement system, purchases system as well as payroll

system. The first section presents a brief overview of this report followed by a detailed

discussion of conceptual system data flow diagram (DFD). The last section discusses system

flowchart and summarizes the potential risks and weaknesses of the each of the three

constituent systems.

Executive Summary

This report has analysed Adam & Co business which is The Royal Bank of Scotland

PLC’s trading division and which caters for the need of private bank clients based on UK.

Adam & Co offers an array of private banking services that include discretionary investment

management alongside financial planning services to many high net worth customers in the

United Kingdom. It has a centralized accounting system with many networking terminals

located in different places in the UK and hence a deeper evaluation of Adam & Co expending

cycle process is essential in this case. The discussion focuses on the constituent system of

expending cycle including cash disbursement system, purchases system as well as payroll

system. The first section presents a brief overview of this report followed by a detailed

discussion of conceptual system data flow diagram (DFD). The last section discusses system

flowchart and summarizes the potential risks and weaknesses of the each of the three

constituent systems.

Case Study – Adam & Co 3

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Data Flow Diagram of Purchases and Cash Disbursements Systems........................................4

Purchase System.....................................................................................................................4

Cash Disbursement Systems..................................................................................................7

Data Flow Diagram of Payroll System......................................................................................8

System Flowchart of Purchases System...................................................................................10

System Flowchart of Cash Disbursements System..................................................................12

System Flowchart of Payroll System.......................................................................................13

Internal Control Weaknesses and Risks in Each System.........................................................14

Purchases System.................................................................................................................14

Cash Disbursement Systems................................................................................................14

Payroll Systems....................................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Data Flow Diagram of Purchases and Cash Disbursements Systems........................................4

Purchase System.....................................................................................................................4

Cash Disbursement Systems..................................................................................................7

Data Flow Diagram of Payroll System......................................................................................8

System Flowchart of Purchases System...................................................................................10

System Flowchart of Cash Disbursements System..................................................................12

System Flowchart of Payroll System.......................................................................................13

Internal Control Weaknesses and Risks in Each System.........................................................14

Purchases System.................................................................................................................14

Cash Disbursement Systems................................................................................................14

Payroll Systems....................................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchasing

Department

Inventory

Warehous

e

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory Subsidiary Ledger

Receiving File

Digital purchase order records

Purchase order copy 1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice

Sends invoice

Inventory level

Case Study – Adam & Co 4

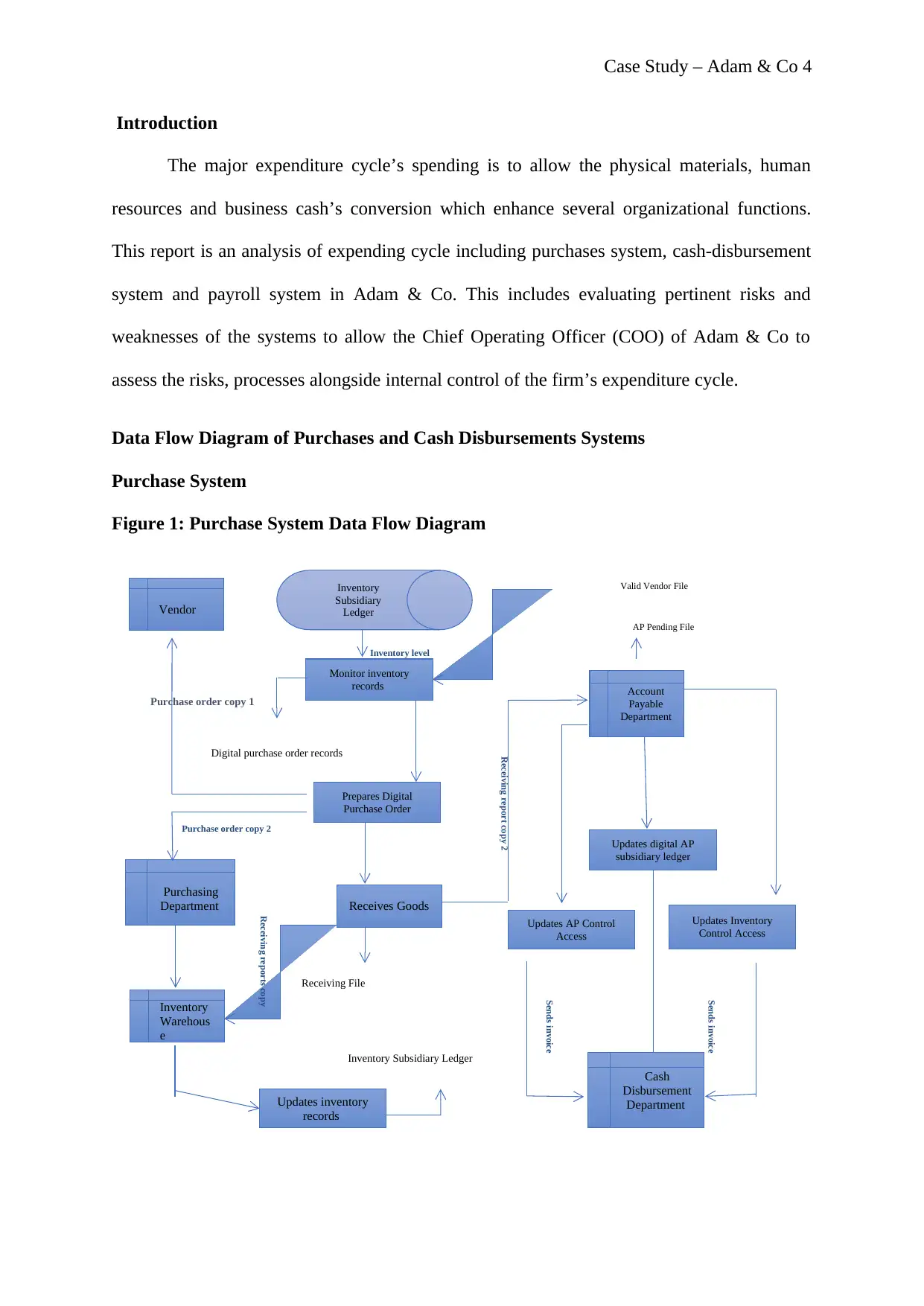

Introduction

The major expenditure cycle’s spending is to allow the physical materials, human

resources and business cash’s conversion which enhance several organizational functions.

This report is an analysis of expending cycle including purchases system, cash-disbursement

system and payroll system in Adam & Co. This includes evaluating pertinent risks and

weaknesses of the systems to allow the Chief Operating Officer (COO) of Adam & Co to

assess the risks, processes alongside internal control of the firm’s expenditure cycle.

Data Flow Diagram of Purchases and Cash Disbursements Systems

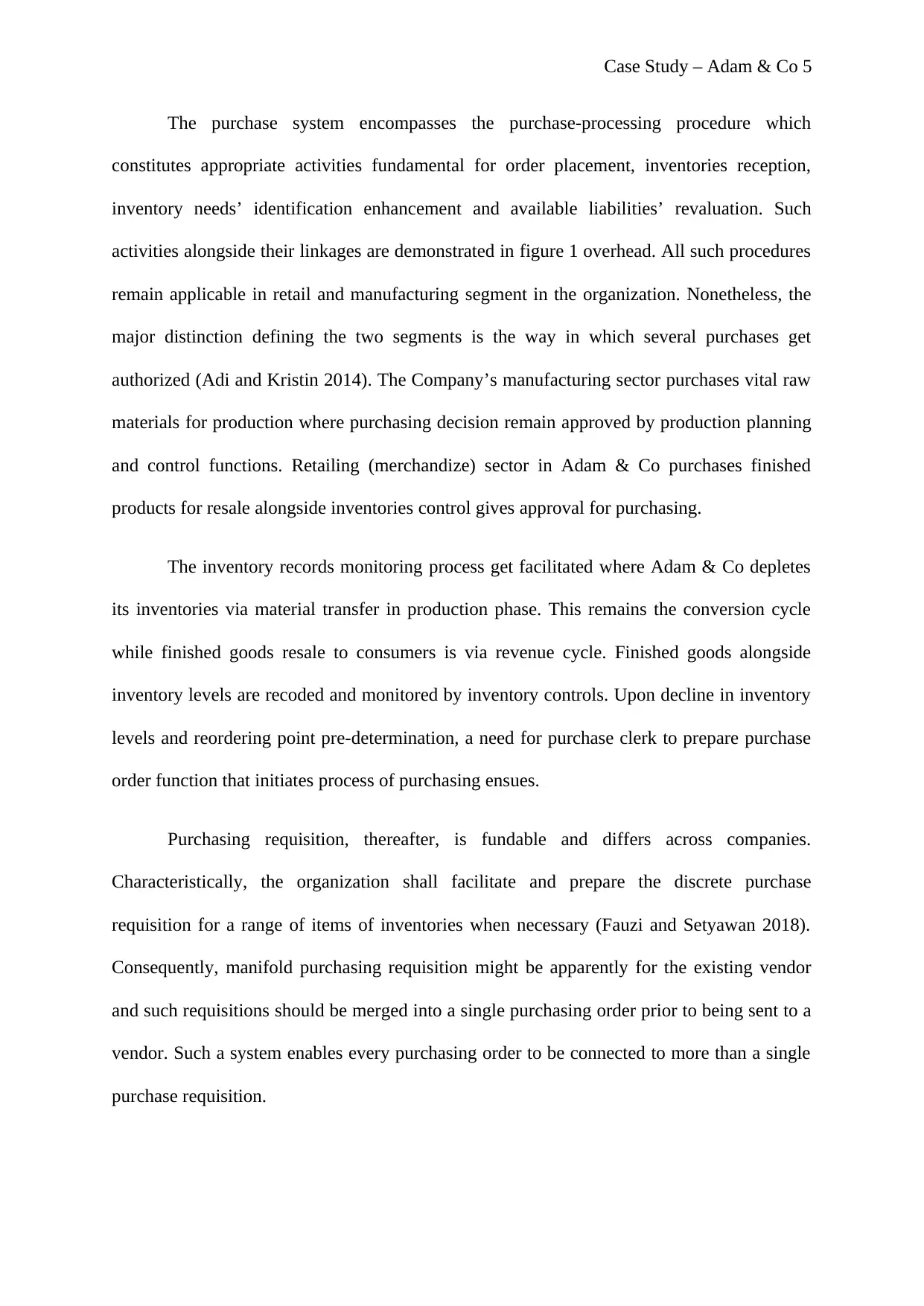

Purchase System

Figure 1: Purchase System Data Flow Diagram

Inventory

Subsidiary

Ledger

Department

Inventory

Warehous

e

Cash

Disbursement

Department

Monitor inventory

records

Updates inventory

records

Receives Goods

Prepares Digital

Purchase Order

Updates Inventory

Control Access

Updates AP Control

Access

Updates digital AP

subsidiary ledger

Valid Vendor File

AP Pending File

Vendor

Account

Payable

Department

Inventory Subsidiary Ledger

Receiving File

Digital purchase order records

Purchase order copy 1

Purchase order copy 2

Receiving reports copy

Receiving report copy 2

Sends invoice

Sends invoice

Inventory level

Case Study – Adam & Co 4

Introduction

The major expenditure cycle’s spending is to allow the physical materials, human

resources and business cash’s conversion which enhance several organizational functions.

This report is an analysis of expending cycle including purchases system, cash-disbursement

system and payroll system in Adam & Co. This includes evaluating pertinent risks and

weaknesses of the systems to allow the Chief Operating Officer (COO) of Adam & Co to

assess the risks, processes alongside internal control of the firm’s expenditure cycle.

Data Flow Diagram of Purchases and Cash Disbursements Systems

Purchase System

Figure 1: Purchase System Data Flow Diagram

Inventory

Subsidiary

Ledger

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study – Adam & Co 5

The purchase system encompasses the purchase-processing procedure which

constitutes appropriate activities fundamental for order placement, inventories reception,

inventory needs’ identification enhancement and available liabilities’ revaluation. Such

activities alongside their linkages are demonstrated in figure 1 overhead. All such procedures

remain applicable in retail and manufacturing segment in the organization. Nonetheless, the

major distinction defining the two segments is the way in which several purchases get

authorized (Adi and Kristin 2014). The Company’s manufacturing sector purchases vital raw

materials for production where purchasing decision remain approved by production planning

and control functions. Retailing (merchandize) sector in Adam & Co purchases finished

products for resale alongside inventories control gives approval for purchasing.

The inventory records monitoring process get facilitated where Adam & Co depletes

its inventories via material transfer in production phase. This remains the conversion cycle

while finished goods resale to consumers is via revenue cycle. Finished goods alongside

inventory levels are recoded and monitored by inventory controls. Upon decline in inventory

levels and reordering point pre-determination, a need for purchase clerk to prepare purchase

order function that initiates process of purchasing ensues.

Purchasing requisition, thereafter, is fundable and differs across companies.

Characteristically, the organization shall facilitate and prepare the discrete purchase

requisition for a range of items of inventories when necessary (Fauzi and Setyawan 2018).

Consequently, manifold purchasing requisition might be apparently for the existing vendor

and such requisitions should be merged into a single purchasing order prior to being sent to a

vendor. Such a system enables every purchasing order to be connected to more than a single

purchase requisition.

The purchase system encompasses the purchase-processing procedure which

constitutes appropriate activities fundamental for order placement, inventories reception,

inventory needs’ identification enhancement and available liabilities’ revaluation. Such

activities alongside their linkages are demonstrated in figure 1 overhead. All such procedures

remain applicable in retail and manufacturing segment in the organization. Nonetheless, the

major distinction defining the two segments is the way in which several purchases get

authorized (Adi and Kristin 2014). The Company’s manufacturing sector purchases vital raw

materials for production where purchasing decision remain approved by production planning

and control functions. Retailing (merchandize) sector in Adam & Co purchases finished

products for resale alongside inventories control gives approval for purchasing.

The inventory records monitoring process get facilitated where Adam & Co depletes

its inventories via material transfer in production phase. This remains the conversion cycle

while finished goods resale to consumers is via revenue cycle. Finished goods alongside

inventory levels are recoded and monitored by inventory controls. Upon decline in inventory

levels and reordering point pre-determination, a need for purchase clerk to prepare purchase

order function that initiates process of purchasing ensues.

Purchasing requisition, thereafter, is fundable and differs across companies.

Characteristically, the organization shall facilitate and prepare the discrete purchase

requisition for a range of items of inventories when necessary (Fauzi and Setyawan 2018).

Consequently, manifold purchasing requisition might be apparently for the existing vendor

and such requisitions should be merged into a single purchasing order prior to being sent to a

vendor. Such a system enables every purchasing order to be connected to more than a single

purchase requisition.

Case Study – Adam & Co 6

The purchase order function preparation acquires the purchasing requisitions which a

vendor organizes when necessary. Consequently, purchase order (PO) copy gets designed for

respective vendors as demonstrated in Data Flow Diagram (DFD) in figure 1 above. Further,

an extra copy gets transferred to department for purchasing for an Account Payable (AP)

functions implied for AP pending files’ temporary filing. Thus, a file’s blind copy is

subsequently sent to receiving goods functions.

Various organizations experience a lag in time between placing order and receiving

goods. At this phase, several copies of PO shall be encompassed in temporary files in

department of account payable, and no execution of any economic aspect. At this pointy,

Adam & Co has neither received any inventories nor incurred any financial obligations. In

this aspect, it is needless to facilitate formal entries making in records of accounting (Fedaghi

2014). However, Adam & Co might decide to effect a memo entry to refer to pending

inventory-linked receipts and obligations.

The subsequent phase involves receipt inventories where goods reach and preparation

of receiving report follows. Such gods are subsequently reconciled with packing slip

alongside digital purchase order (DPO). Copies of such a document entail data on prices and

quantity of received items. The major purpose of such documents is to allow inspection and

inventory counting by receiving clear prior to receiving report drafting. Primarily, receiving

department remains busy and its staff is under pressure to unload delivery vans or sign lading

bills (Gautam 2010). Thus, receiving clerk shall solely be given pertinent data on quantity of

an item and accept products delivery in reference to data provided.

The next phase involves providing update about record of inventory. The inventory

control technique relative to valuation technique differs across companies. A firm which uses

The purchase order function preparation acquires the purchasing requisitions which a

vendor organizes when necessary. Consequently, purchase order (PO) copy gets designed for

respective vendors as demonstrated in Data Flow Diagram (DFD) in figure 1 above. Further,

an extra copy gets transferred to department for purchasing for an Account Payable (AP)

functions implied for AP pending files’ temporary filing. Thus, a file’s blind copy is

subsequently sent to receiving goods functions.

Various organizations experience a lag in time between placing order and receiving

goods. At this phase, several copies of PO shall be encompassed in temporary files in

department of account payable, and no execution of any economic aspect. At this pointy,

Adam & Co has neither received any inventories nor incurred any financial obligations. In

this aspect, it is needless to facilitate formal entries making in records of accounting (Fedaghi

2014). However, Adam & Co might decide to effect a memo entry to refer to pending

inventory-linked receipts and obligations.

The subsequent phase involves receipt inventories where goods reach and preparation

of receiving report follows. Such gods are subsequently reconciled with packing slip

alongside digital purchase order (DPO). Copies of such a document entail data on prices and

quantity of received items. The major purpose of such documents is to allow inspection and

inventory counting by receiving clear prior to receiving report drafting. Primarily, receiving

department remains busy and its staff is under pressure to unload delivery vans or sign lading

bills (Gautam 2010). Thus, receiving clerk shall solely be given pertinent data on quantity of

an item and accept products delivery in reference to data provided.

The next phase involves providing update about record of inventory. The inventory

control technique relative to valuation technique differs across companies. A firm which uses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case Study – Adam & Co 7

a standard cost model might execute its inventories at the pre-determined standardized value

regardless of charges paid to a specific vendor (Bhoite 2012). The presentation of a

standardized inventory ledger triggers appropriate data about the attained quantity. Because

receiving reports encompass data on item quantity, such a file serves this specific purpose.

Therefore, updating major cost inventory ledger triggers additional financial data from

warehouse of inventory. Account payable, during this process, requires a set-up. AP function

thus receives this setting and receiving report temporary files and PO gets filed. Adam & Co

has received such inventories from appropriate vendors and subsequently realized its

obligation for paying for goods received.

To complete the process, the AP clerk requires to assess the exact obligation valuation

up to when he receives invoice (Hooshyar, Yusop and Horng, 2015). For materially improper

estimate, entry adjustment is performed to correct mistakes. Because the received invoice

receipt necessitates AP techniques alongside process, the clerk has to assess all liabilities

unrecorded during time-end closure. When inventories arrive, AP clerk will reconcile the

appropriate financial data with PO and receiving report in existing pending file. This act is

called a 3-way matching which verifies quantity attained and its associated prices (Jarrah

2018). At this point, clerk will progressive update digital account payable (DPO) subsidiary

ledger, AP controls account as well as inventory controls account in Adam & Co general

ledger. Ultimately, the invoice, receiving report and PO get transferred.

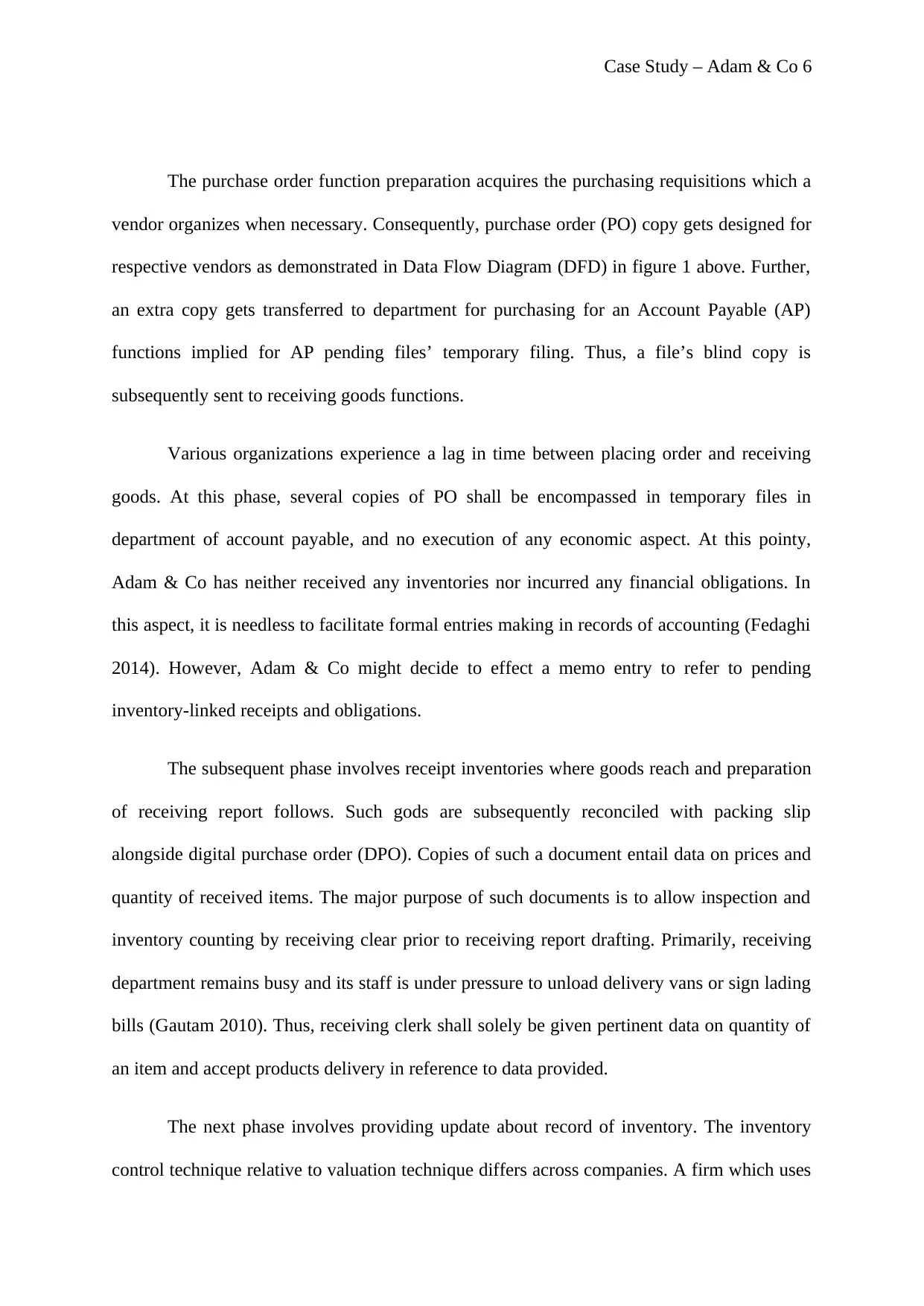

Cash Disbursement Systems

Figure 2: Cash Disbursements Systems Data Flow Diagram

a standard cost model might execute its inventories at the pre-determined standardized value

regardless of charges paid to a specific vendor (Bhoite 2012). The presentation of a

standardized inventory ledger triggers appropriate data about the attained quantity. Because

receiving reports encompass data on item quantity, such a file serves this specific purpose.

Therefore, updating major cost inventory ledger triggers additional financial data from

warehouse of inventory. Account payable, during this process, requires a set-up. AP function

thus receives this setting and receiving report temporary files and PO gets filed. Adam & Co

has received such inventories from appropriate vendors and subsequently realized its

obligation for paying for goods received.

To complete the process, the AP clerk requires to assess the exact obligation valuation

up to when he receives invoice (Hooshyar, Yusop and Horng, 2015). For materially improper

estimate, entry adjustment is performed to correct mistakes. Because the received invoice

receipt necessitates AP techniques alongside process, the clerk has to assess all liabilities

unrecorded during time-end closure. When inventories arrive, AP clerk will reconcile the

appropriate financial data with PO and receiving report in existing pending file. This act is

called a 3-way matching which verifies quantity attained and its associated prices (Jarrah

2018). At this point, clerk will progressive update digital account payable (DPO) subsidiary

ledger, AP controls account as well as inventory controls account in Adam & Co general

ledger. Ultimately, the invoice, receiving report and PO get transferred.

Cash Disbursement Systems

Figure 2: Cash Disbursements Systems Data Flow Diagram

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP Department

Updates

Documents

Document Receipts

Identification

of Liability

Due

Treasurer

Vendor

Preparation of

cheque for invoice

account Signature

Mailing

Receiving

Receiving Report File

Invoice FileCheque Copy

Case Study – Adam & Co 8

Cash disbursement evaluation remains essential in expenditure cycle. The receipt of

appropriate documents by clerk for AP department necessitates filing awaiting payment due

dates. Arrival of due date sees the clerk obligated to draw a cheque referenced to invoiced

account which is sent to treasurer to sigh and mail to vendor. Consequently, cheque register,

AP control account and AP subsidiaries are updated from computer terminal. Records are

finally sent to receiving department which fills the invoice, receive reports, copies of both PO

and cheque.

Data Flow Diagram of Payroll System

Figure 3: Payroll System Data Flow Diagram

Updates

Documents

Document Receipts

Identification

of Liability

Due

Treasurer

Vendor

Preparation of

cheque for invoice

account Signature

Mailing

Receiving

Receiving Report File

Invoice FileCheque Copy

Case Study – Adam & Co 8

Cash disbursement evaluation remains essential in expenditure cycle. The receipt of

appropriate documents by clerk for AP department necessitates filing awaiting payment due

dates. Arrival of due date sees the clerk obligated to draw a cheque referenced to invoiced

account which is sent to treasurer to sigh and mail to vendor. Consequently, cheque register,

AP control account and AP subsidiaries are updated from computer terminal. Records are

finally sent to receiving department which fills the invoice, receive reports, copies of both PO

and cheque.

Data Flow Diagram of Payroll System

Figure 3: Payroll System Data Flow Diagram

Prepares cash

disbursement

vouchers

Payroll DepartmentEmployees Time Cards

Supervisors

Central Payroll SystemTime Card data

Payroll register

Payroll register

Supervisor

AC Department

Write ChequesCheque file

Imprest bank

General ledger

department

Cheque file

Department Employees

Reviews and submits

Hour’s records

Digital Employee Record

Reviews and submits

Deposits

Reviews

Check

Case Study – Adam & Co 9

Adam & Co payroll system is designed to enable workers fill-in time cards thereby

collection data pertinent to total hours worked which is subsequently assessed and reviewed

by supervisor and forwarded to department of payroll. Payroll system gets referenced from

central payroll system situated in department for data processing from where the clear keys-in

data and prints paycheque copies, records of employee copies and payroll register copies.

From department for payroll, clerk files time cards and send the payment cheque for workers

disbursement

vouchers

Payroll DepartmentEmployees Time Cards

Supervisors

Central Payroll SystemTime Card data

Payroll register

Payroll register

Supervisor

AC Department

Write ChequesCheque file

Imprest bank

General ledger

department

Cheque file

Department Employees

Reviews and submits

Hour’s records

Digital Employee Record

Reviews and submits

Deposits

Reviews

Check

Case Study – Adam & Co 9

Adam & Co payroll system is designed to enable workers fill-in time cards thereby

collection data pertinent to total hours worked which is subsequently assessed and reviewed

by supervisor and forwarded to department of payroll. Payroll system gets referenced from

central payroll system situated in department for data processing from where the clear keys-in

data and prints paycheque copies, records of employee copies and payroll register copies.

From department for payroll, clerk files time cards and send the payment cheque for workers

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case Study – Adam & Co 10

to supervisors who distribute and review. The clerk then sends payroll register’s copies to AP

department and other copies containing time cards info to payroll department. The AP clerk

subsequently reviews registers and manually prepares voucher for cash-disbursement and

send payroll register alongside the voucher to department for general ledger. The AP clerk

then draws a cheque for payroll and subsequently deposits it imprest account.

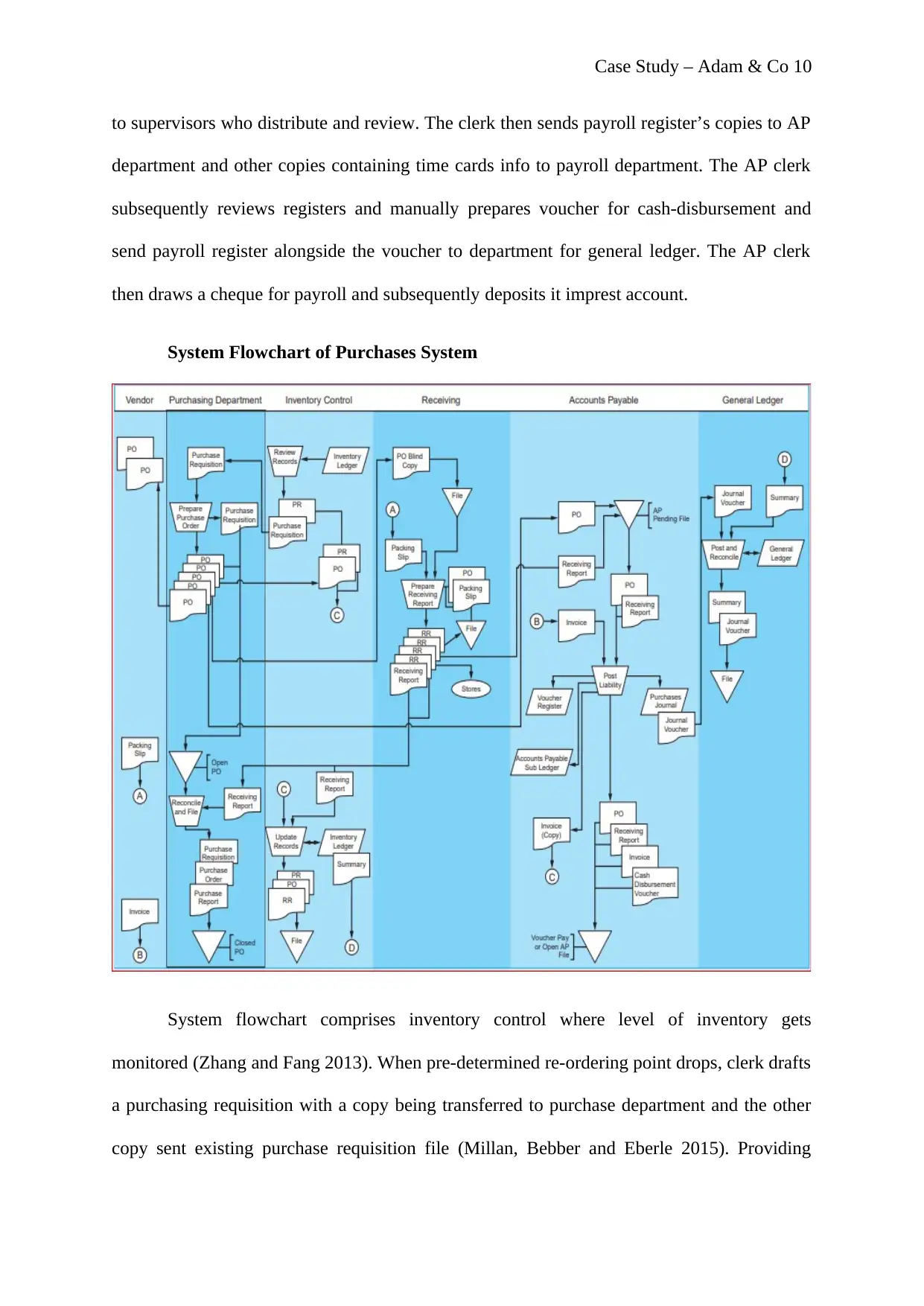

System Flowchart of Purchases System

System flowchart comprises inventory control where level of inventory gets

monitored (Zhang and Fang 2013). When pre-determined re-ordering point drops, clerk drafts

a purchasing requisition with a copy being transferred to purchase department and the other

copy sent existing purchase requisition file (Millan, Bebber and Eberle 2015). Providing

to supervisors who distribute and review. The clerk then sends payroll register’s copies to AP

department and other copies containing time cards info to payroll department. The AP clerk

subsequently reviews registers and manually prepares voucher for cash-disbursement and

send payroll register alongside the voucher to department for general ledger. The AP clerk

then draws a cheque for payroll and subsequently deposits it imprest account.

System Flowchart of Purchases System

System flowchart comprises inventory control where level of inventory gets

monitored (Zhang and Fang 2013). When pre-determined re-ordering point drops, clerk drafts

a purchasing requisition with a copy being transferred to purchase department and the other

copy sent existing purchase requisition file (Millan, Bebber and Eberle 2015). Providing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study – Adam & Co 11

authorization control in inventories control department is distinguished from purchase

department which executes transactions.

The process proceeds purchase requisition, vendor’s sorting and PO preparation for

each vendor in purchasing department. At this point, two purchase order copies get

transferred to a vendor and copy of PO is sent to inventory control to be filed alongside

purchasing requisition available. Goods arising from vendors are subsequently reconciled

with PO’s blind copies. At the completion of the process of physical filing and inspection,

receiving clerk subsequently makes different reports stating the quantity and condition of

inventories (Nakamoto 2017). A copy of receiving reports is then sent to inventory

department alongside physical inventory whereas the other copy is sent to purchase

department where the clerk can reconcile it with existing PO.

In the department for AP, clerk received the incoming invoice where info get

reconciled with existing pending doc file. Afterwards, the relevant transaction is recorded in

journal purchase and points which include AP subsidiary ledger’s preparation. This proceeds

liabilities record where a clerk transfers source doc, receiving reports alongside existing

voucher payable files. At this point, the digital account payable subsidiary ledgers’ update is

performed, which include AP control account alongside inventories control from computer

terminal in general ledger department. Finally, the invoices, receiving reports alongside PO

copies are transferred to department of cash disbursement by the clerk.

authorization control in inventories control department is distinguished from purchase

department which executes transactions.

The process proceeds purchase requisition, vendor’s sorting and PO preparation for

each vendor in purchasing department. At this point, two purchase order copies get

transferred to a vendor and copy of PO is sent to inventory control to be filed alongside

purchasing requisition available. Goods arising from vendors are subsequently reconciled

with PO’s blind copies. At the completion of the process of physical filing and inspection,

receiving clerk subsequently makes different reports stating the quantity and condition of

inventories (Nakamoto 2017). A copy of receiving reports is then sent to inventory

department alongside physical inventory whereas the other copy is sent to purchase

department where the clerk can reconcile it with existing PO.

In the department for AP, clerk received the incoming invoice where info get

reconciled with existing pending doc file. Afterwards, the relevant transaction is recorded in

journal purchase and points which include AP subsidiary ledger’s preparation. This proceeds

liabilities record where a clerk transfers source doc, receiving reports alongside existing

voucher payable files. At this point, the digital account payable subsidiary ledgers’ update is

performed, which include AP control account alongside inventories control from computer

terminal in general ledger department. Finally, the invoices, receiving reports alongside PO

copies are transferred to department of cash disbursement by the clerk.

Case Study – Adam & Co 12

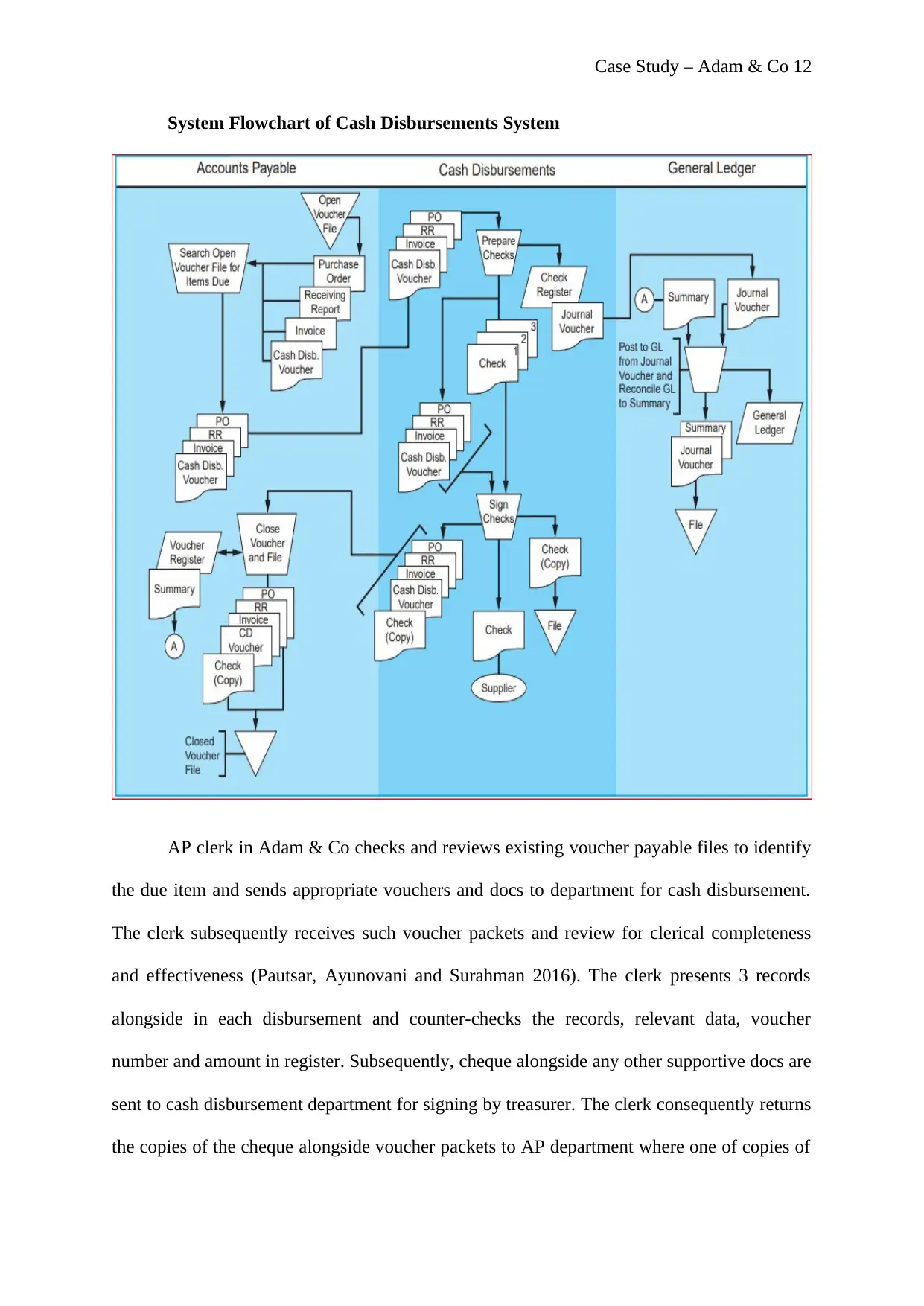

System Flowchart of Cash Disbursements System

AP clerk in Adam & Co checks and reviews existing voucher payable files to identify

the due item and sends appropriate vouchers and docs to department for cash disbursement.

The clerk subsequently receives such voucher packets and review for clerical completeness

and effectiveness (Pautsar, Ayunovani and Surahman 2016). The clerk presents 3 records

alongside in each disbursement and counter-checks the records, relevant data, voucher

number and amount in register. Subsequently, cheque alongside any other supportive docs are

sent to cash disbursement department for signing by treasurer. The clerk consequently returns

the copies of the cheque alongside voucher packets to AP department where one of copies of

System Flowchart of Cash Disbursements System

AP clerk in Adam & Co checks and reviews existing voucher payable files to identify

the due item and sends appropriate vouchers and docs to department for cash disbursement.

The clerk subsequently receives such voucher packets and review for clerical completeness

and effectiveness (Pautsar, Ayunovani and Surahman 2016). The clerk presents 3 records

alongside in each disbursement and counter-checks the records, relevant data, voucher

number and amount in register. Subsequently, cheque alongside any other supportive docs are

sent to cash disbursement department for signing by treasurer. The clerk consequently returns

the copies of the cheque alongside voucher packets to AP department where one of copies of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.