BSc Business Finance Case Study: Performance Indicators and Pricing

VerifiedAdded on 2023/01/11

|11

|2205

|75

Case Study

AI Summary

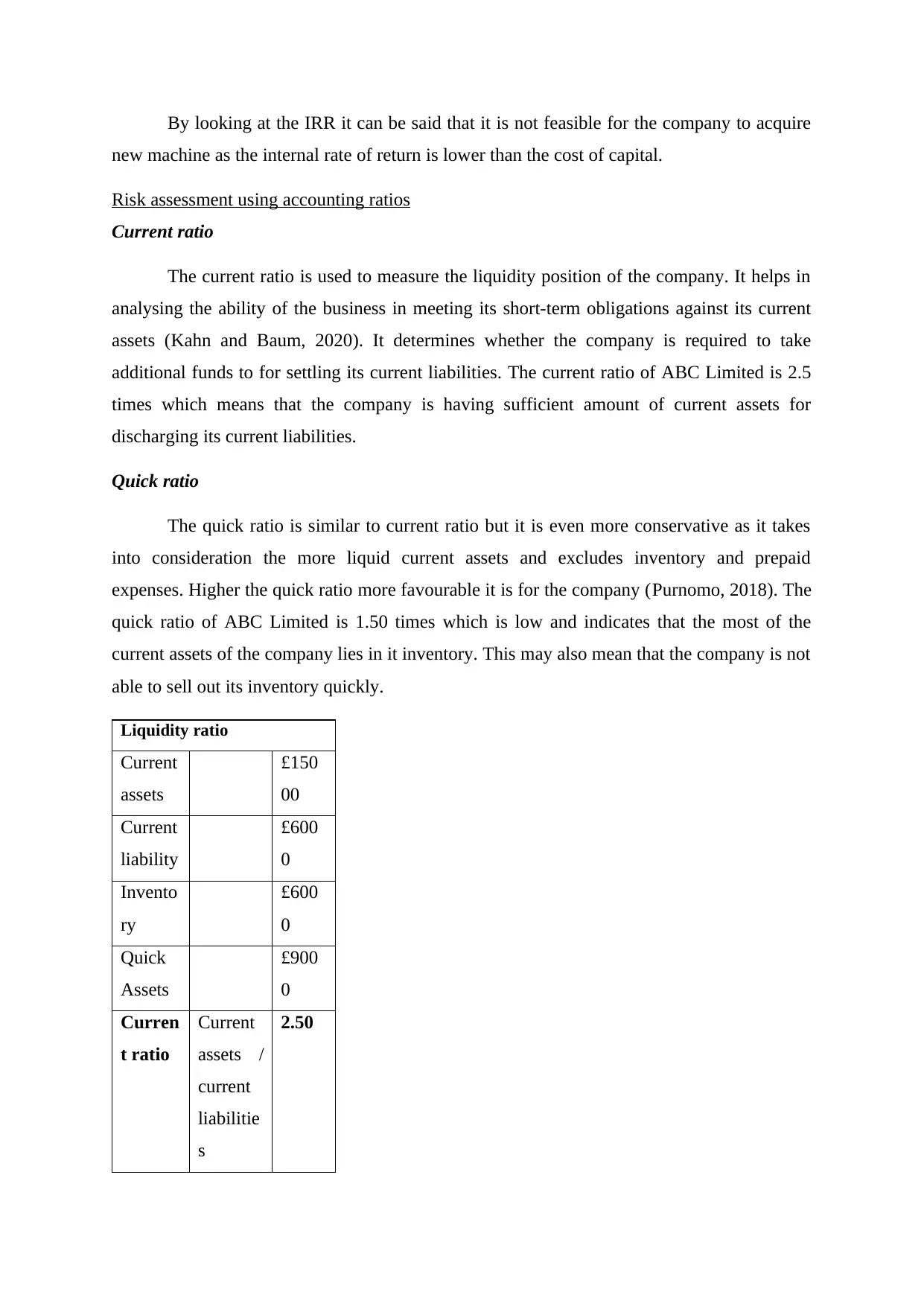

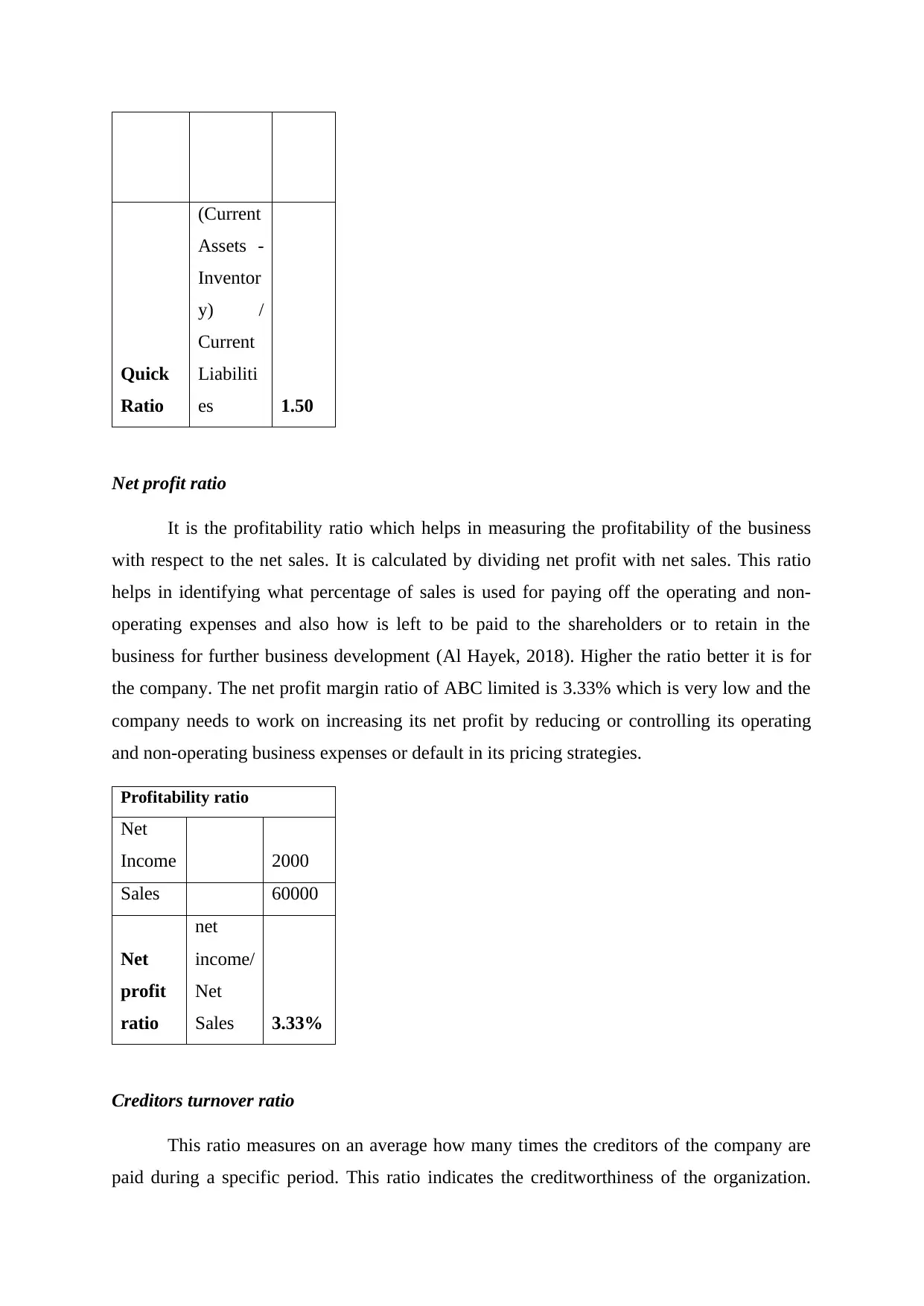

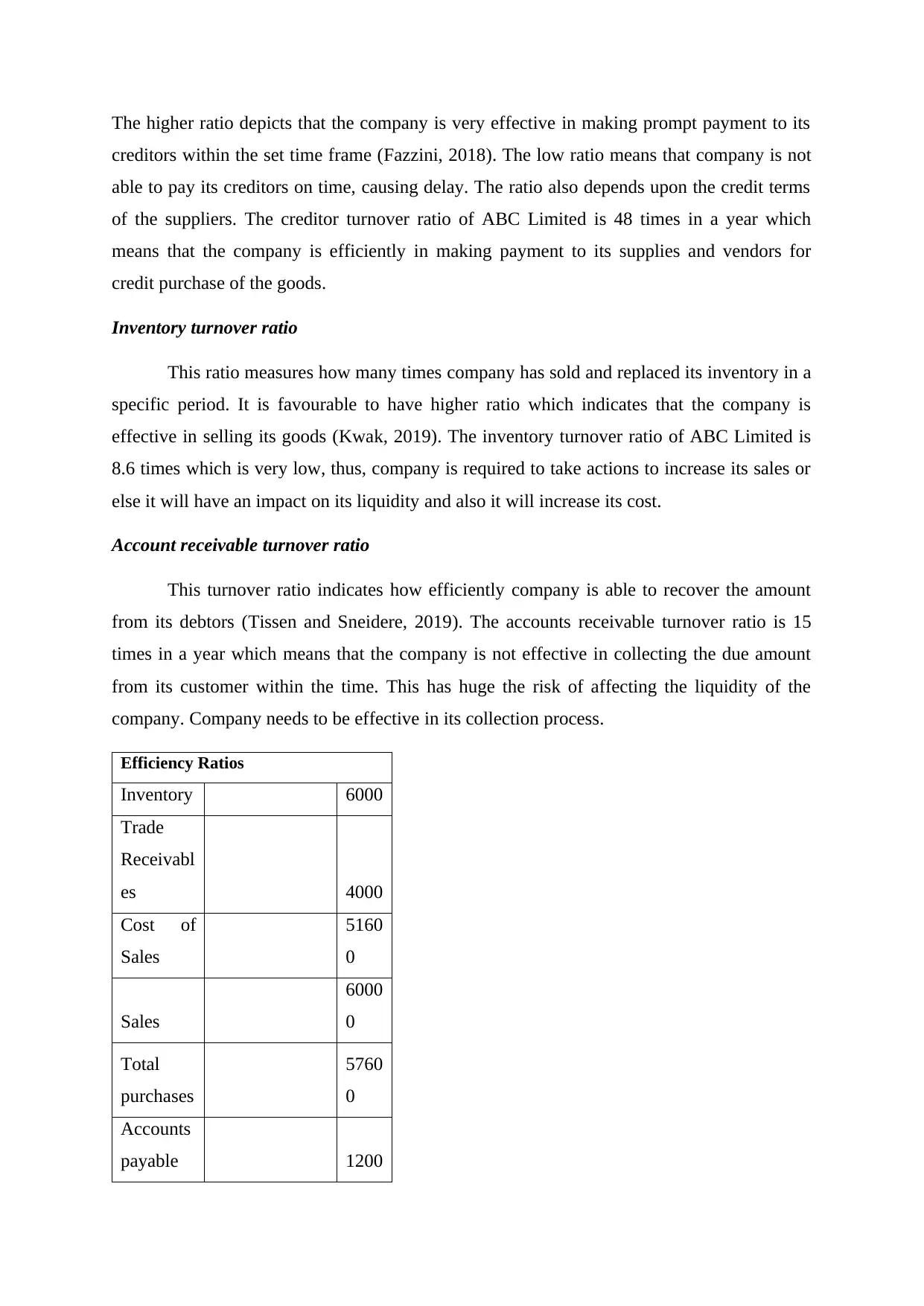

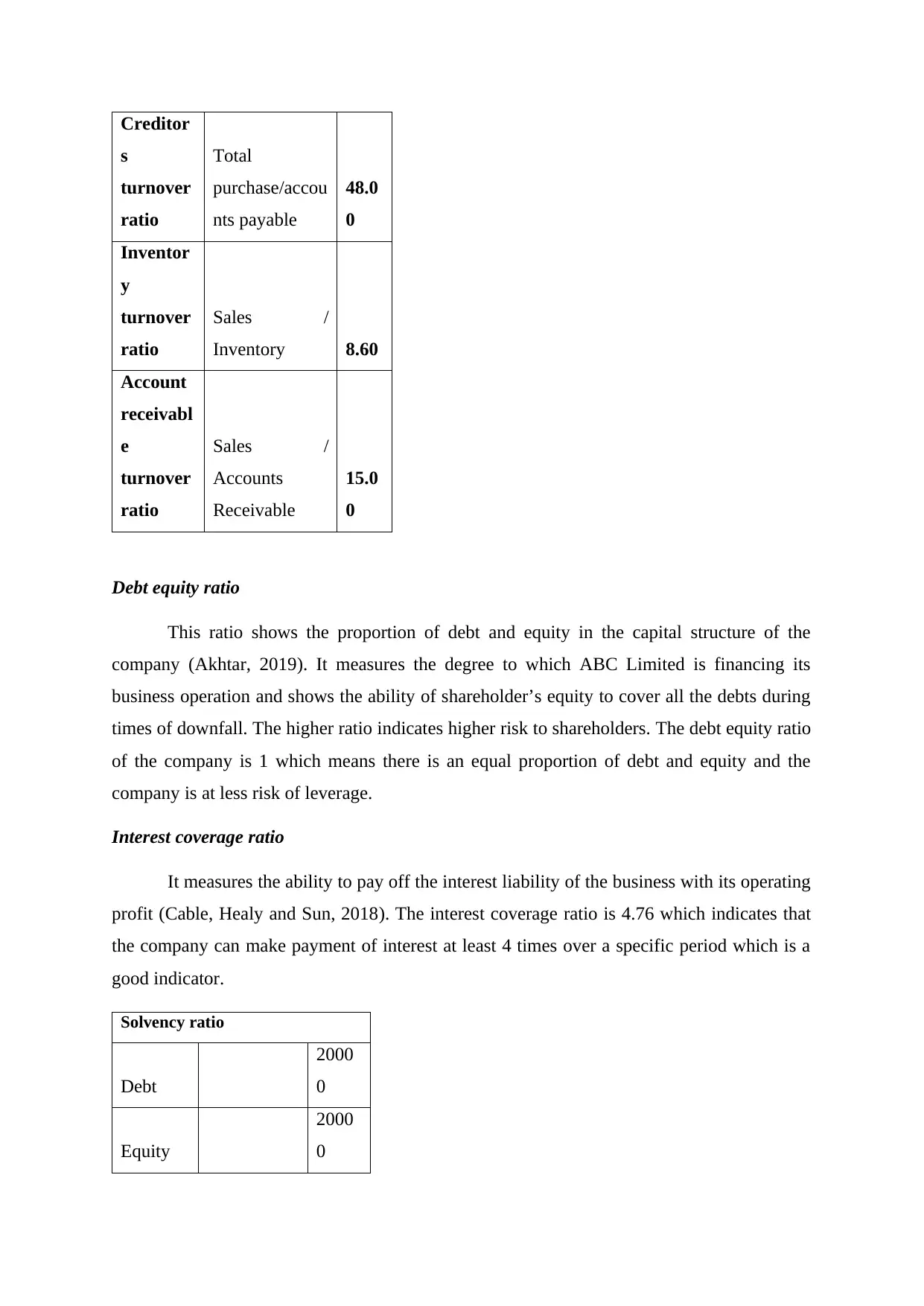

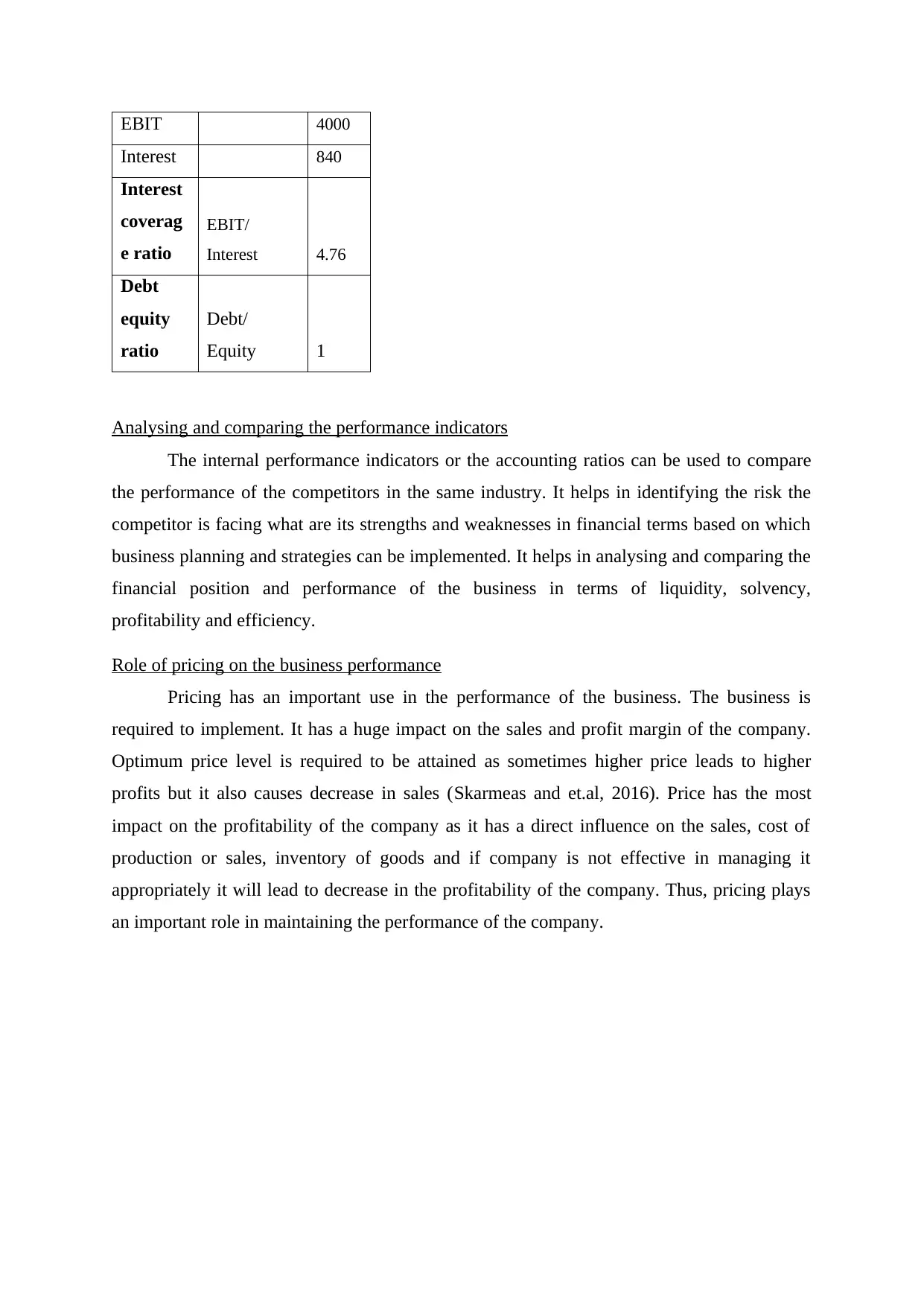

This case study examines investment appraisal techniques and financial performance analysis for a business. It begins with an overview of investment appraisal methods, including the Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR), providing calculations and interpretations for each method. The case study then delves into risk assessment using accounting ratios, covering current ratio, quick ratio, net profit ratio, creditors turnover ratio, inventory turnover ratio, accounts receivable turnover ratio, debt-equity ratio, and interest coverage ratio. Each ratio is calculated, and its implications for the company's financial health are discussed. Furthermore, the case study analyzes and compares performance indicators, highlighting the role of pricing on business performance, emphasizing the importance of optimal pricing strategies for sales, profit margins, and overall financial success. The analysis is supported by references to relevant financial literature.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.