eLoanDocs Case Study: Technology Adoption and Business Challenges

VerifiedAdded on 2019/09/18

|8

|3889

|662

Case Study

AI Summary

The eLoanDocs case study examines the evolution of a software company in the mortgage industry, highlighting its adoption of technology from proprietary systems to cloud computing. The company, initially focused on streamlining the mortgage closing process, faced challenges in scaling its infrastructure and ensuring data security. The case study details eLoanDocs' transition to SaaS, its response to regulatory changes supporting electronic signatures, and its investments in data center redundancy and disaster recovery. It explores the business challenges of a growing company, including the need for significant investment in infrastructure and the importance of adapting to market changes. The case study also highlights the importance of security considerations, the impact of power outages, and the strategic decisions made to maintain a competitive advantage in the market.

Case Study for Chapter 3

ELOANDOCS: Riding the

Tide of Technology without

Wiping Out

Introduction1

On a warm summer evening in Northeast Ohio, Albert Michaels, the Chief Technology Officer

(CTO) of local software company eLoanDocs, was enjoying his evening drive home. Though his

eyes were on the road in front of him, his mind was stuck on the topic of the day behind him: the

“cloud”. How could eLoanDocs take advantage of this emerging and exciting new technology

platform? Cloud computing held the promise of greatly reduced costs and nearly unlimited

scalability for a company like his and seemed like it might be the wave of the future for hosted

software providers. But the barriers to his customers’ adopting the cloud were potentially high.

And if those barriers were overcome, the competitive landscape in which eLoanDocs operated

might shift in unfavorable ways. As a technology professional, adopting the cloud seemed to him

to be a forgone conclusion. But his years of experience had shown him that it’s rarely easy to be

one of the early adopters.

Inefficiencies in the Mortgage Industry

The home mortgage closing process in the early 1990s was slow, paper intensive, and ripe for

innovation. Realtors, mortgage lenders, title companies, and borrowers met and collaborated in

primarily local marketplaces. The myriad documents required to support the mortgage approval

process were exchanged through a combination of fax, mail, courier, and in-person reviews.

Realtors, mortgage brokers, and escrow officers worked together to ensure that all of the

necessary documents were generated, supporting services such as appraisals were ordered and

performed, and required documents were signed by the borrower. The average time between a

consumer application for a mortgage loan and the final closing was about 90 days. Closings were

often delayed or rescheduled when late-breaking changes in the loan terms or associated costs

required the lender to generate new documents. The majority of documents required for the

mortgage closing were generated by the mortgage lender, but these documents were traditionally

reviewed and signed by the borrower at the place of settlement (closing), generally at the title

company. Mortgage lenders sent documents to the title company and to the borrower through

mail, overnight express delivery, or courier. A successful closing required that the mortgage

lender generate final documents and send them to the title company at least one day before the

scheduled closing.

ELOANDOCS: Riding the

Tide of Technology without

Wiping Out

Introduction1

On a warm summer evening in Northeast Ohio, Albert Michaels, the Chief Technology Officer

(CTO) of local software company eLoanDocs, was enjoying his evening drive home. Though his

eyes were on the road in front of him, his mind was stuck on the topic of the day behind him: the

“cloud”. How could eLoanDocs take advantage of this emerging and exciting new technology

platform? Cloud computing held the promise of greatly reduced costs and nearly unlimited

scalability for a company like his and seemed like it might be the wave of the future for hosted

software providers. But the barriers to his customers’ adopting the cloud were potentially high.

And if those barriers were overcome, the competitive landscape in which eLoanDocs operated

might shift in unfavorable ways. As a technology professional, adopting the cloud seemed to him

to be a forgone conclusion. But his years of experience had shown him that it’s rarely easy to be

one of the early adopters.

Inefficiencies in the Mortgage Industry

The home mortgage closing process in the early 1990s was slow, paper intensive, and ripe for

innovation. Realtors, mortgage lenders, title companies, and borrowers met and collaborated in

primarily local marketplaces. The myriad documents required to support the mortgage approval

process were exchanged through a combination of fax, mail, courier, and in-person reviews.

Realtors, mortgage brokers, and escrow officers worked together to ensure that all of the

necessary documents were generated, supporting services such as appraisals were ordered and

performed, and required documents were signed by the borrower. The average time between a

consumer application for a mortgage loan and the final closing was about 90 days. Closings were

often delayed or rescheduled when late-breaking changes in the loan terms or associated costs

required the lender to generate new documents. The majority of documents required for the

mortgage closing were generated by the mortgage lender, but these documents were traditionally

reviewed and signed by the borrower at the place of settlement (closing), generally at the title

company. Mortgage lenders sent documents to the title company and to the borrower through

mail, overnight express delivery, or courier. A successful closing required that the mortgage

lender generate final documents and send them to the title company at least one day before the

scheduled closing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Technology to the Rescue

In 1994, a Cleveland-based title and settlement services company, Premium Title, was

determined to reduce their costs and differentiate their service to the market by adding

technology to the mortgage-closing process. Premium Title’s owners created a separate

company, eLoanDocs, to connect the various parties involved in the process by using

technology. eLoanDocs’ founders wanted to improve the speed and accuracy of the mortgage-

closing process while increasing market share for Premium Title and other connected business

partners. The founders believed that they could create a company that would grow quickly and

that would generate significant return for their investors.

In industries where larger companies with dedicated IT staff existed, standard protocols had

been developed to exchange information electronically. For example, in the automotive industry,

Electronic Data Interchange (EDI) had been used for years to exchange purchasing and billing

information between manufacturers and their suppliers.2 There were no standards for electronic

communication between business partners in the mortgage industry and, since the Internet was

not being used broadly for commercial purposes, intercompany data exchange was dependent on

proprietary communication networks.

eLoanDocs launched a proprietary electronic interchange in 1995 that connected Premium

Title with several mortgage lenders in the Cleveland area along with a few local service

providers such as appraisal vendors and surveyors. Proprietary data formats were defined for title

insurance and appraisal orders, and mortgage documents were delivered electronically using the

common HP Printer Command Language (PCL) print stream data format. The PCL3 is a page

description language (PDL) that allows a document’s appearance to be described at a high level.

This allowed Premium Title, using equipment commonly available at the time, to define the

documents needed in their industry and share them with the necessary business partners.

eLoanDocs purchased off-the-shelf communications software and customized it to their needs;

they also purchased computer servers, network equipment, and modems to run their electronic

interchange. The computer equipment and telephone lines were hosted in their modest office

space in Cleveland, Ohio. The small network of participating companies each installed modems,

standard communication software, and eLoanDocs’ proprietary software application to exchange

documents that represented orders for services and the delivered real estate products such as

appraisals, flood search certificates, and surveys. The electronically delivered documents

replaced slower, lower-quality, or less-reliable courier and fax deliveries. eLoanDocs was

successful in building a network of local mortgage service providers, but struggled to extend the

technology and business model outside of Northeast Ohio.

Right Technology, Right Place, Right Time

In the late 1990s, eLoanDocs realized that the emergence of the Internet as a driver of commerce

would present both a threat to their network and an opportunity to extend their mortgage data

interchange to more parties across the country at a lower cost. In 2000, eLoanDocs re-launched

their mortgage industry electronic collaboration network on the Internet with the debut of their

new software product, Document Posting Service (DPS). DPS used standard communication

protocols such as HTTPS and SFTP over the Internet, which eliminated the need for modems

and proprietary communications software. DPS also featured HTML Web user interfaces for

In 1994, a Cleveland-based title and settlement services company, Premium Title, was

determined to reduce their costs and differentiate their service to the market by adding

technology to the mortgage-closing process. Premium Title’s owners created a separate

company, eLoanDocs, to connect the various parties involved in the process by using

technology. eLoanDocs’ founders wanted to improve the speed and accuracy of the mortgage-

closing process while increasing market share for Premium Title and other connected business

partners. The founders believed that they could create a company that would grow quickly and

that would generate significant return for their investors.

In industries where larger companies with dedicated IT staff existed, standard protocols had

been developed to exchange information electronically. For example, in the automotive industry,

Electronic Data Interchange (EDI) had been used for years to exchange purchasing and billing

information between manufacturers and their suppliers.2 There were no standards for electronic

communication between business partners in the mortgage industry and, since the Internet was

not being used broadly for commercial purposes, intercompany data exchange was dependent on

proprietary communication networks.

eLoanDocs launched a proprietary electronic interchange in 1995 that connected Premium

Title with several mortgage lenders in the Cleveland area along with a few local service

providers such as appraisal vendors and surveyors. Proprietary data formats were defined for title

insurance and appraisal orders, and mortgage documents were delivered electronically using the

common HP Printer Command Language (PCL) print stream data format. The PCL3 is a page

description language (PDL) that allows a document’s appearance to be described at a high level.

This allowed Premium Title, using equipment commonly available at the time, to define the

documents needed in their industry and share them with the necessary business partners.

eLoanDocs purchased off-the-shelf communications software and customized it to their needs;

they also purchased computer servers, network equipment, and modems to run their electronic

interchange. The computer equipment and telephone lines were hosted in their modest office

space in Cleveland, Ohio. The small network of participating companies each installed modems,

standard communication software, and eLoanDocs’ proprietary software application to exchange

documents that represented orders for services and the delivered real estate products such as

appraisals, flood search certificates, and surveys. The electronically delivered documents

replaced slower, lower-quality, or less-reliable courier and fax deliveries. eLoanDocs was

successful in building a network of local mortgage service providers, but struggled to extend the

technology and business model outside of Northeast Ohio.

Right Technology, Right Place, Right Time

In the late 1990s, eLoanDocs realized that the emergence of the Internet as a driver of commerce

would present both a threat to their network and an opportunity to extend their mortgage data

interchange to more parties across the country at a lower cost. In 2000, eLoanDocs re-launched

their mortgage industry electronic collaboration network on the Internet with the debut of their

new software product, Document Posting Service (DPS). DPS used standard communication

protocols such as HTTPS and SFTP over the Internet, which eliminated the need for modems

and proprietary communications software. DPS also featured HTML Web user interfaces for

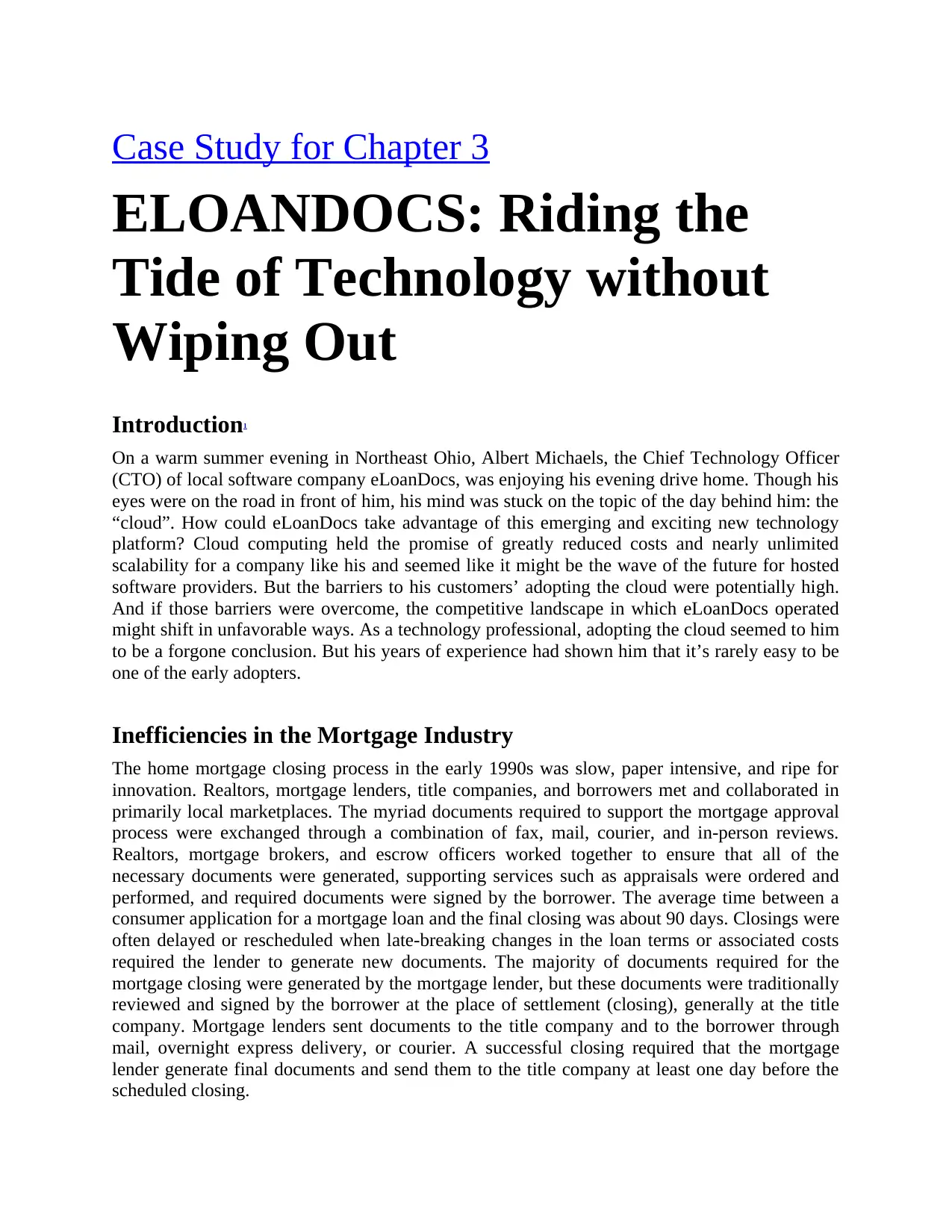

settlement agents to avoid the need for software to be installed at each customer location. DPS

was a multi-tenant application (Figure 3.1) that provided software as a service (SaaS) to the

mortgage industry.

SaaS allows customers to use software that is owned, delivered, and managed remotely by one

(or more) providers.4 This model allows the provider to maintain one set of code and data for

many different customers. In essence, SaaS allows customers to rent software rather than buy it.

The advantages of SaaS for customers include cost savings, scalability, accessibility, upgrades

without disruption, and resilience. Some disadvantages also exist, the primary one being

security.5

Market acceptance for DPS was tremendous, with several major mortgage lenders signing

contracts to deliver all of their closing documents to settlement agents using eLoanDocs. As a

small company facing growth challenges brought on in part by a boom-or-bust mortgage

industry, eLoanDocs took a pragmatic approach to new product development. Product

development investments were guided by immediate opportunities with existing customers that

would lead to short-term revenue and possible broader market appeal. Following this model,

eLoanDocs extended their product line beyond closing-document delivery to include borrower-

disclosure delivery and electronic-signature capability.

Supportive Regulatory Changes

Federal and state legislation in 1999 opened the market for electronic signatures in the real estate

industry, and eLoanDocs developed services to take advantage of this legislation. The Uniform

Electronic Transaction Act (UETA) was first adopted by California and Pennsylvania in

1999.6 At the time of writing in 2015, 47 of the 50 U.S. states have adopted this act. The

remaining three states (New York, Illinois, and Washington) have not adopted the act, but have

statutes pertaining to electronic transactions. The UETA’s purpose is to bring into line the

differing state laws over such areas as retention of paper records and the validity of electronic

signatures to support the validity of electronic contracts as a viable medium of agreement. The

Electronic Signatures in Global and National Commerce Act (ESIGN) is similar to the UETA

with the exception that it pertains to the validity of electronic signatures on the federal level

instead of the state level.7 It also brings validity to signatures for foreign commerce.

The Changing Business Tides

eLoanDocs’ business was growing fast, but the computers that hosted eLoanDocs’ services were

still run out of a small office computer room. On a hot summer day in late July 2000, Cleveland

faced scattered power outages due to heavy draw on the power grid for air conditioning. Power

was lost in eLoanDocs’ office for over eight hours, well beyond the two-hour battery backup that

was in place to support the computer systems. Dave Griffith, data center manager for

eLoanDocs, said “we tried to find portable generators for rent but there was nothing available big

enough and we couldn’t even get the generators close enough to our computer room to run

extension cords” (personal communication). eLoanDocs’ electronic services were unavailable to

customers for most of the day. Customers suffered costly business delays due to this extended

system outage on one of the busiest days of the month for mortgage closings.

was a multi-tenant application (Figure 3.1) that provided software as a service (SaaS) to the

mortgage industry.

SaaS allows customers to use software that is owned, delivered, and managed remotely by one

(or more) providers.4 This model allows the provider to maintain one set of code and data for

many different customers. In essence, SaaS allows customers to rent software rather than buy it.

The advantages of SaaS for customers include cost savings, scalability, accessibility, upgrades

without disruption, and resilience. Some disadvantages also exist, the primary one being

security.5

Market acceptance for DPS was tremendous, with several major mortgage lenders signing

contracts to deliver all of their closing documents to settlement agents using eLoanDocs. As a

small company facing growth challenges brought on in part by a boom-or-bust mortgage

industry, eLoanDocs took a pragmatic approach to new product development. Product

development investments were guided by immediate opportunities with existing customers that

would lead to short-term revenue and possible broader market appeal. Following this model,

eLoanDocs extended their product line beyond closing-document delivery to include borrower-

disclosure delivery and electronic-signature capability.

Supportive Regulatory Changes

Federal and state legislation in 1999 opened the market for electronic signatures in the real estate

industry, and eLoanDocs developed services to take advantage of this legislation. The Uniform

Electronic Transaction Act (UETA) was first adopted by California and Pennsylvania in

1999.6 At the time of writing in 2015, 47 of the 50 U.S. states have adopted this act. The

remaining three states (New York, Illinois, and Washington) have not adopted the act, but have

statutes pertaining to electronic transactions. The UETA’s purpose is to bring into line the

differing state laws over such areas as retention of paper records and the validity of electronic

signatures to support the validity of electronic contracts as a viable medium of agreement. The

Electronic Signatures in Global and National Commerce Act (ESIGN) is similar to the UETA

with the exception that it pertains to the validity of electronic signatures on the federal level

instead of the state level.7 It also brings validity to signatures for foreign commerce.

The Changing Business Tides

eLoanDocs’ business was growing fast, but the computers that hosted eLoanDocs’ services were

still run out of a small office computer room. On a hot summer day in late July 2000, Cleveland

faced scattered power outages due to heavy draw on the power grid for air conditioning. Power

was lost in eLoanDocs’ office for over eight hours, well beyond the two-hour battery backup that

was in place to support the computer systems. Dave Griffith, data center manager for

eLoanDocs, said “we tried to find portable generators for rent but there was nothing available big

enough and we couldn’t even get the generators close enough to our computer room to run

extension cords” (personal communication). eLoanDocs’ electronic services were unavailable to

customers for most of the day. Customers suffered costly business delays due to this extended

system outage on one of the busiest days of the month for mortgage closings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It was clear that eLoanDocs needed to improve their computer hosting infrastructure in order

to maintain a leadership position as a provider of electronic services to the mortgage industry. Up

until this time, eLoanDocs did not have the necessary financial strength or the technical

management experience to bring their computer infrastructure up to the needed levels of

scalability and reliability. With major new customers ready to sign contracts and the memory of

the 2000 power outage fresh in their minds, eLoanDocs management raised the needed capital

and engaged a technology consulting firm to prepare for the next level of capability. In early

2001, eLoanDocs moved their computer servers to a private cage in a dedicated third party co-

location data center in Chicago, Secure Hosting. The Secure Hosting facility in Chicago featured

redundant power feeds, on-site generators, multiple Internet providers, and state-of-the-art

physical and network security. Secure Hosting quickly became eLoanDocs’ most important and

most expensive vendor.

Security Considerations

By 2004, eLoanDocs was doing business with seven of the top 10 mortgage lenders in the US,

and documents and data for over 50% of the mortgages in the country flowed through

eLoanDocs’ systems. eLoanDocs had become a critical part of the mortgage industry, but with

fewer than 50 employees and under $15 million in annual revenue, the company was hundreds of

times smaller than most of its giant financial institution customers.

Given the sensitive nature of the information that eLoanDocs was handling, the attention given

to cybersecurity breaches at well-known companies like Apple, JP Morgan Chase, Target, and

The Home Depot, and the consequences of these breaches,8 many of eLoanDocs’ largest

customers began to demand that it demonstrate the reliability and security of their computer

hosting facility through extensive load testing, system failure testing, and third party security

audits. Some customers sent their own security teams to the eLoanDocs office in Cleveland and

to the Secure Hosting data center in Chicago to review eLoanDocs’ policies, procedures, and

capabilities. Paul Hunter, eLoanDocs CEO, was excited to show off Secure Hosting to the top

mortgage companies: “The first time the National Mortgage security team visited the Secure

Hosting facility they were thrilled to see the biometric security, diesel generators with 3 days of

fuel on-site, and our private cage that was secured on all sides. eLoanDocs finally looks like the

big player that we are” (personal communication).

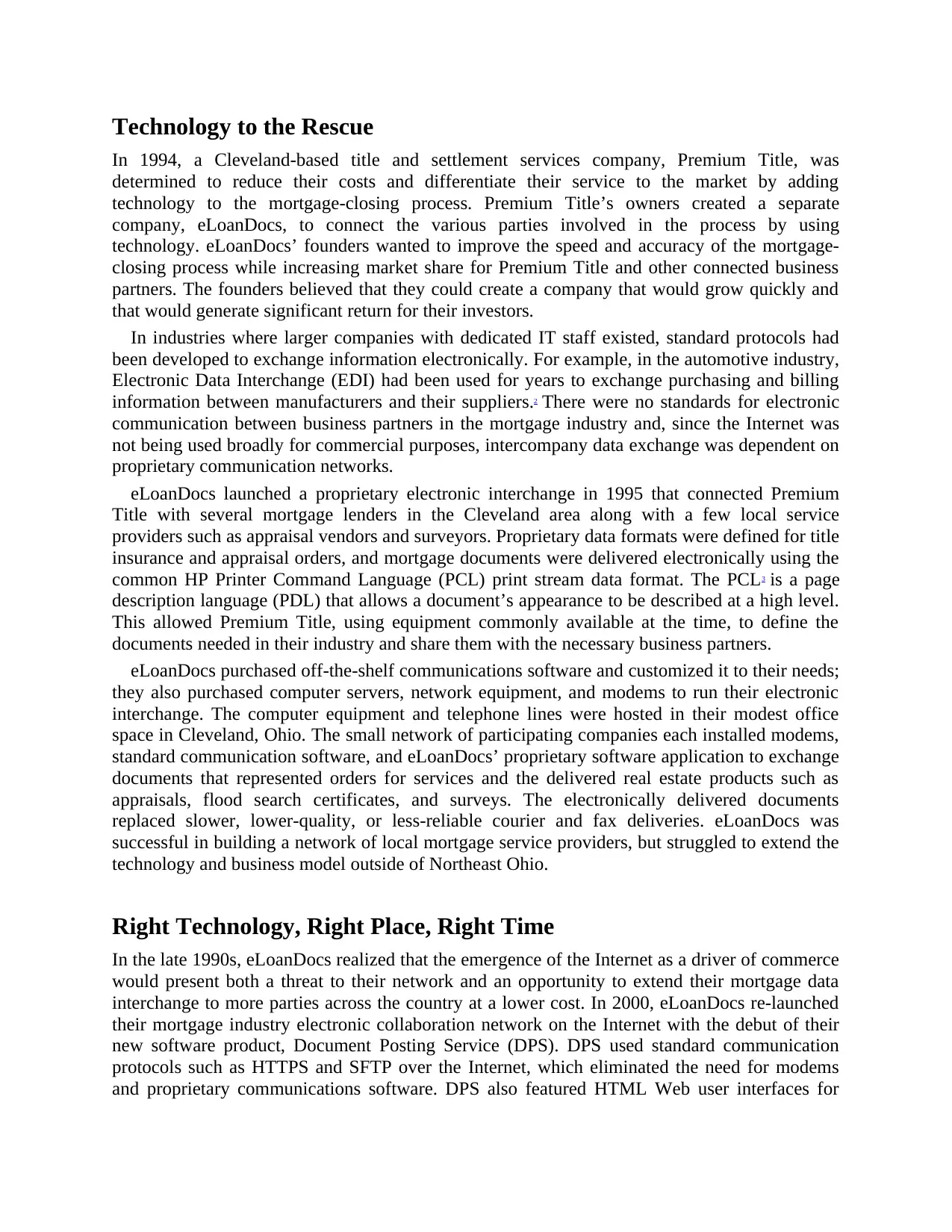

By 2007, demands for additional capacity in the network and customer requirements to

maintain an active disaster recovery data center drove eLoanDocs to make several significant

investments. First, eLoanDocs acquired a competing mortgage technology company based in

Seattle, WA, FastForms. eLoanDocs then moved their primary data center from Secure Hosting

in Chicago to FastForms’s co-location provider in Seattle, SunGuard. Finally, eLoanDocs built

an identical redundant hosting facility in Cleveland using another co-location provider. In late

2009, eLoanDocs completed implementing a highly scalable and virtualized computer hosting

infrastructure in Seattle with real-time replication of all customer documents and data to the

backup site in Cleveland. The Cleveland facility could automatically take over all of eLoanDocs’

services in the event of an extended outage in the Seattle data center (Figure 3.2). The time and

expense required to build and maintain their services in secure and redundant data centers gave

eLoanDocs a significant advantage in the market because few technology providers could make

the necessary investments in infrastructure and software required to compete. In addition,

to maintain a leadership position as a provider of electronic services to the mortgage industry. Up

until this time, eLoanDocs did not have the necessary financial strength or the technical

management experience to bring their computer infrastructure up to the needed levels of

scalability and reliability. With major new customers ready to sign contracts and the memory of

the 2000 power outage fresh in their minds, eLoanDocs management raised the needed capital

and engaged a technology consulting firm to prepare for the next level of capability. In early

2001, eLoanDocs moved their computer servers to a private cage in a dedicated third party co-

location data center in Chicago, Secure Hosting. The Secure Hosting facility in Chicago featured

redundant power feeds, on-site generators, multiple Internet providers, and state-of-the-art

physical and network security. Secure Hosting quickly became eLoanDocs’ most important and

most expensive vendor.

Security Considerations

By 2004, eLoanDocs was doing business with seven of the top 10 mortgage lenders in the US,

and documents and data for over 50% of the mortgages in the country flowed through

eLoanDocs’ systems. eLoanDocs had become a critical part of the mortgage industry, but with

fewer than 50 employees and under $15 million in annual revenue, the company was hundreds of

times smaller than most of its giant financial institution customers.

Given the sensitive nature of the information that eLoanDocs was handling, the attention given

to cybersecurity breaches at well-known companies like Apple, JP Morgan Chase, Target, and

The Home Depot, and the consequences of these breaches,8 many of eLoanDocs’ largest

customers began to demand that it demonstrate the reliability and security of their computer

hosting facility through extensive load testing, system failure testing, and third party security

audits. Some customers sent their own security teams to the eLoanDocs office in Cleveland and

to the Secure Hosting data center in Chicago to review eLoanDocs’ policies, procedures, and

capabilities. Paul Hunter, eLoanDocs CEO, was excited to show off Secure Hosting to the top

mortgage companies: “The first time the National Mortgage security team visited the Secure

Hosting facility they were thrilled to see the biometric security, diesel generators with 3 days of

fuel on-site, and our private cage that was secured on all sides. eLoanDocs finally looks like the

big player that we are” (personal communication).

By 2007, demands for additional capacity in the network and customer requirements to

maintain an active disaster recovery data center drove eLoanDocs to make several significant

investments. First, eLoanDocs acquired a competing mortgage technology company based in

Seattle, WA, FastForms. eLoanDocs then moved their primary data center from Secure Hosting

in Chicago to FastForms’s co-location provider in Seattle, SunGuard. Finally, eLoanDocs built

an identical redundant hosting facility in Cleveland using another co-location provider. In late

2009, eLoanDocs completed implementing a highly scalable and virtualized computer hosting

infrastructure in Seattle with real-time replication of all customer documents and data to the

backup site in Cleveland. The Cleveland facility could automatically take over all of eLoanDocs’

services in the event of an extended outage in the Seattle data center (Figure 3.2). The time and

expense required to build and maintain their services in secure and redundant data centers gave

eLoanDocs a significant advantage in the market because few technology providers could make

the necessary investments in infrastructure and software required to compete. In addition,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

eLoansDocs implemented best practices for disaster recovery (DR) planning including risk

assessment and business impact analysis and training for and testing of the DR plan.9

With the new infrastructure in place, eLoanDocs met customer service level agreements

(SLAs) for 99.9% uptime of services in 2011 and 2012. eLoanDocs had developed a mature set

of policies and procedures around information security and had published results of a third party

SSAE 16 Type II compliance audit twice a year to customers. The organization had six full-time

staff dedicated to data center operations and a full-time information security officer. Their

internal staff had accumulated significant expertise in data center operations, but the company

experienced, on average, a 20 percent annual turnover rate due to an active job market for their

staff members’ highly sought-after skills. One eLoanDocs employee was recruited to manage

networks for Microsoft’s hosting facilities in Washington. Michelle Fletcher, eLoanDocs’

Director of Technical Operations, complained “I’m having a hard time keeping my best people

working here at eLoanDocs. We just don’t have enough scale to keep these people challenged

and there is no way that eLoanDocs can match the pay of the big guys.” (personal

communication).

eLoanDocs’ annual vendor expenses for data center hosting, data networks, computer

hardware maintenance, and software support subscriptions were nearly US$2 million per year.

Employee costs and third party audit expenses brought the overall cost of eLoanDocs’ data

center hosting, security, and compliance to about US$3.5 million annually.

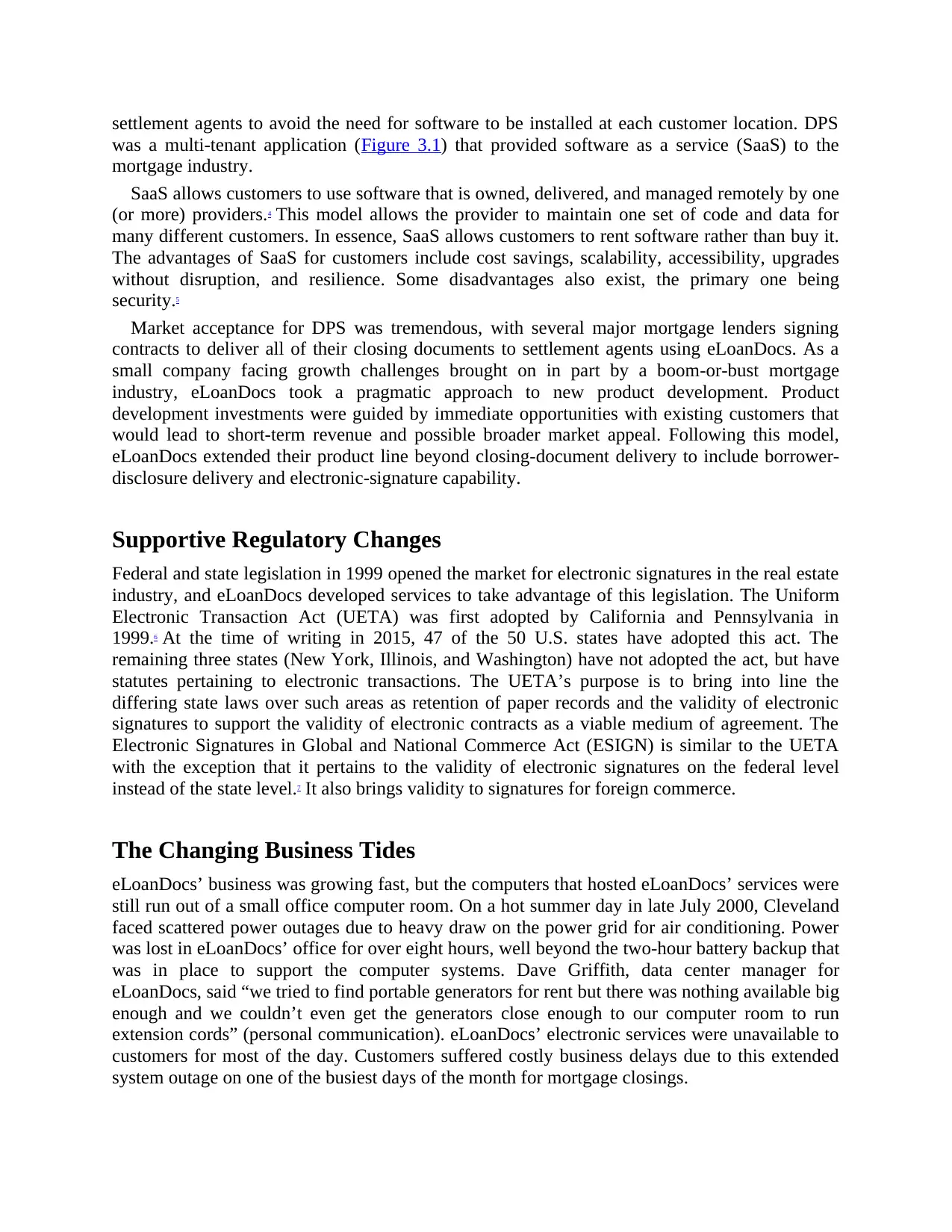

Clouds Ahead?

Just as the rise of the Internet enabled eLoanDocs’ explosive growth in the 2000’s, technological

changes beginning in 2010 led to new opportunities and competitive challenges for the company.

Giant technology vendors such as Amazon began to offer comprehensive computer hosting

services with a new model: cloud computing (see Figure 3.3). Amazon, Microsoft, Google, and

other companies built data centers at massive scale that were designed to allow them to sell

computing capacity to the market at prices significantly below what companies could achieve on

their own.10 Cloud computing vendors offered a model where a company could simply purchase

the needed amount of processing power, memory, disk storage, and Internet bandwidth on a

monthly subscription model. Customers could increase or decrease their usage on demand.

Public cloud providers also offered high availability, multi-site data replication, and full disaster

recovery capabilities as optional or standard services.11

Using a cloud hosting service such as Amazon Web Services (AWS), a small software vendor

could launch a new service with twice the computing capacity of eLoanDocs in a matter of days.

Matt Pittman, VP of Sales for eLoanDocs, said: “I can’t compete on price with mortgage

technology competitors like EchoSign that launched their products hosted at Amazon. Their

costs are so low that they are giving away basic services with a freemium model. I just hope that

companies like this don’t start cutting into our core client base” (personal communication).

Services like AWS were examples of the “public cloud”—inexpensive computing capacity

that can be purchased on demand, with many different customers’ workloads and information

intermingled on the same computer servers and storage devices. Cost advantages available to

customers of public cloud services were enhanced by aggressive competition in the industry,

which sparked an ongoing price war between providers. Amazon reduced their prices a total of

assessment and business impact analysis and training for and testing of the DR plan.9

With the new infrastructure in place, eLoanDocs met customer service level agreements

(SLAs) for 99.9% uptime of services in 2011 and 2012. eLoanDocs had developed a mature set

of policies and procedures around information security and had published results of a third party

SSAE 16 Type II compliance audit twice a year to customers. The organization had six full-time

staff dedicated to data center operations and a full-time information security officer. Their

internal staff had accumulated significant expertise in data center operations, but the company

experienced, on average, a 20 percent annual turnover rate due to an active job market for their

staff members’ highly sought-after skills. One eLoanDocs employee was recruited to manage

networks for Microsoft’s hosting facilities in Washington. Michelle Fletcher, eLoanDocs’

Director of Technical Operations, complained “I’m having a hard time keeping my best people

working here at eLoanDocs. We just don’t have enough scale to keep these people challenged

and there is no way that eLoanDocs can match the pay of the big guys.” (personal

communication).

eLoanDocs’ annual vendor expenses for data center hosting, data networks, computer

hardware maintenance, and software support subscriptions were nearly US$2 million per year.

Employee costs and third party audit expenses brought the overall cost of eLoanDocs’ data

center hosting, security, and compliance to about US$3.5 million annually.

Clouds Ahead?

Just as the rise of the Internet enabled eLoanDocs’ explosive growth in the 2000’s, technological

changes beginning in 2010 led to new opportunities and competitive challenges for the company.

Giant technology vendors such as Amazon began to offer comprehensive computer hosting

services with a new model: cloud computing (see Figure 3.3). Amazon, Microsoft, Google, and

other companies built data centers at massive scale that were designed to allow them to sell

computing capacity to the market at prices significantly below what companies could achieve on

their own.10 Cloud computing vendors offered a model where a company could simply purchase

the needed amount of processing power, memory, disk storage, and Internet bandwidth on a

monthly subscription model. Customers could increase or decrease their usage on demand.

Public cloud providers also offered high availability, multi-site data replication, and full disaster

recovery capabilities as optional or standard services.11

Using a cloud hosting service such as Amazon Web Services (AWS), a small software vendor

could launch a new service with twice the computing capacity of eLoanDocs in a matter of days.

Matt Pittman, VP of Sales for eLoanDocs, said: “I can’t compete on price with mortgage

technology competitors like EchoSign that launched their products hosted at Amazon. Their

costs are so low that they are giving away basic services with a freemium model. I just hope that

companies like this don’t start cutting into our core client base” (personal communication).

Services like AWS were examples of the “public cloud”—inexpensive computing capacity

that can be purchased on demand, with many different customers’ workloads and information

intermingled on the same computer servers and storage devices. Cost advantages available to

customers of public cloud services were enhanced by aggressive competition in the industry,

which sparked an ongoing price war between providers. Amazon reduced their prices a total of

41 times between 2008 and late 2013. CFO Marty Buckley had calculated that, by switching to a

public cloud provider for all of their data center needs, eLoanDocs’ annual technology costs

(including expected staff reductions) would be $750,000 less than current spending levels.

Public cloud providers also maintained strict security policies and published third party

security audit results, but large financial institutions were not ready to trust their most critical

information and systems to the public cloud as of 2013. eLoanDocs’ security officer Randy

Wallace had his doubts about the viability of cloud hosting for eLoanDocs: “I just finished

another grueling vendor audit from a giant mortgage lender’s security team. These guys want

visibility into all of our processes and they want to make sure that eLoanDocs has control over

every aspect of our systems. I just don’t know how we could ever convince them that a cloud

service is secure” (personal communication).

Concerns regarding the security of data stored in the cloud continue to be an on-going

challenge for many IT executives.12

Recognizing the need for more-secure and more-flexible cloud computing options, computer

hosting vendors such as Rackspace began to offer private cloud solutions to the market.

Rackspace provisioned and supported a set of dedicated hardware to any customer that wanted to

keep their applications and information segregated from other customers. The private cloud

offerings used the same technologies as public cloud providers and still provided cost advantages

due to economies of scale. Buckley had calculated a US$350,000 annual savings should

eLoanDocs move to a private cloud solution. However, Albert Michaels was concerned about

service availability and uptime with a third party private cloud solution: “With our services

hosted in our data centers I know 100% for certain that my team can find the source of any

problem and fix it within minutes, helping us to meet our customer SLAs. How do I know that a

cloud provider will have the same ability and motivation to get things back up and running when

there’s a problem?” (personal communication).

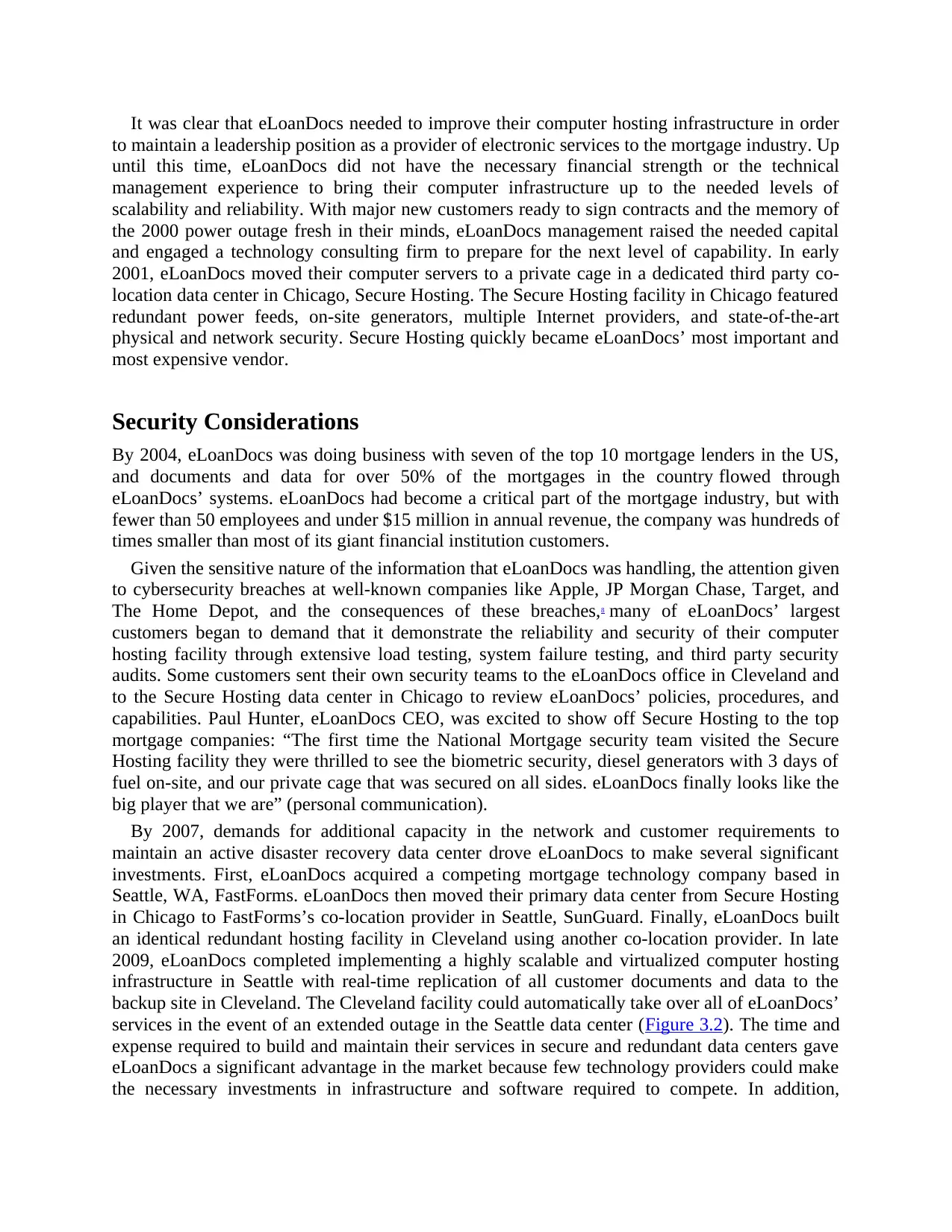

A third cloud hosting model appeared called hybrid cloud (Figure 3.4). This model allowed

customers to take a measured approach to moving some of their computing to outsourced cloud

providers. With a hybrid cloud offering such as VMware’s vCloud, a software company could

easily host some of their applications and data on their internal servers while moving their

development, test, or disaster recovery systems to the cloud. Hybrid cloud solutions offered

many of the security benefits of internally hosted systems while also providing scalability on

demand. Arlene Christianson, eLoanDocs’ VP of Operations, felt that hybrid cloud was not a

good fit for eLoanDocs because “if we go with a hybrid cloud solution, we will need two

separate security and compliance audits and sets of controls” (personal communication). Buckley

estimated that moving to a hybrid cloud solution would reduce eLoanDocs’ technology costs by

about US$200,000 per year.

public cloud provider for all of their data center needs, eLoanDocs’ annual technology costs

(including expected staff reductions) would be $750,000 less than current spending levels.

Public cloud providers also maintained strict security policies and published third party

security audit results, but large financial institutions were not ready to trust their most critical

information and systems to the public cloud as of 2013. eLoanDocs’ security officer Randy

Wallace had his doubts about the viability of cloud hosting for eLoanDocs: “I just finished

another grueling vendor audit from a giant mortgage lender’s security team. These guys want

visibility into all of our processes and they want to make sure that eLoanDocs has control over

every aspect of our systems. I just don’t know how we could ever convince them that a cloud

service is secure” (personal communication).

Concerns regarding the security of data stored in the cloud continue to be an on-going

challenge for many IT executives.12

Recognizing the need for more-secure and more-flexible cloud computing options, computer

hosting vendors such as Rackspace began to offer private cloud solutions to the market.

Rackspace provisioned and supported a set of dedicated hardware to any customer that wanted to

keep their applications and information segregated from other customers. The private cloud

offerings used the same technologies as public cloud providers and still provided cost advantages

due to economies of scale. Buckley had calculated a US$350,000 annual savings should

eLoanDocs move to a private cloud solution. However, Albert Michaels was concerned about

service availability and uptime with a third party private cloud solution: “With our services

hosted in our data centers I know 100% for certain that my team can find the source of any

problem and fix it within minutes, helping us to meet our customer SLAs. How do I know that a

cloud provider will have the same ability and motivation to get things back up and running when

there’s a problem?” (personal communication).

A third cloud hosting model appeared called hybrid cloud (Figure 3.4). This model allowed

customers to take a measured approach to moving some of their computing to outsourced cloud

providers. With a hybrid cloud offering such as VMware’s vCloud, a software company could

easily host some of their applications and data on their internal servers while moving their

development, test, or disaster recovery systems to the cloud. Hybrid cloud solutions offered

many of the security benefits of internally hosted systems while also providing scalability on

demand. Arlene Christianson, eLoanDocs’ VP of Operations, felt that hybrid cloud was not a

good fit for eLoanDocs because “if we go with a hybrid cloud solution, we will need two

separate security and compliance audits and sets of controls” (personal communication). Buckley

estimated that moving to a hybrid cloud solution would reduce eLoanDocs’ technology costs by

about US$200,000 per year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

questions

By the middle of 2014, the computer systems that eLoanDocs had installed in 2009 were nearing

the end of their useful life and had no more capacity for expansion. As eLoanDocs prepares for

their next generation of data center hosting architecture for 2015 and beyond, the choices they

face are complex and will have significant implications for the future of the company.

1. Should eLoanDocs continue with their current model of designing, building, and

managing their own computer hosting infrastructure using their co-location partners?

2. Would eLoanDocs’ financial institution customers accept a move of eLoanDocs’

services to a public or private cloud provider?

3. How should eLoanDocs go about choosing a cloud hosting provider?

As Albert Michaels considered his options, his mind was roiled by a number of questions:

4. Will eLoanDocs’ customers—with their focus on data security—accept a cloud-based

solution? If so, to what degree? And how many customers would accept some form of

cloud-based solution?

5. If customers do accept one of the cost-saving cloud services solutions, what barriers

exist to prevent new competitors from rapidly entering the market and eroding

eLoanDocs’ market share?

6. What is the value that customers believe they are receiving from eLoanDocs?

7. Could it be that customers actually value the secure environment that they can visit

and audit in person? If so, might convincing those customers to adopt a cloud-based

solution to their document delivery problems actually be a damaging move to

eLoanDocs in the long term?

8. Speaking of security, which solution actually provides better protection of customers’

data? Though ownership of the hosting hardware enables eLoanDocs to literally pull

the plug if a breach is detected, how does that compare to the security benefits

associated with outsourcing to a cloud provider? Is one solution more likely than the

other to be targeted for attack? Is either solution better able to detect and prevent

intrusions?

9. Assuming that the system will be attacked at some point, what ability will

eLoanDocs have to identify the compromised data? How might that ability change if

hosting services are outsourced to a cloud provider?

10. How robust is the existing disaster recovery strategy? Which solution best fits the

redundancy needs of eLoanDocs?

11. How might the eLoanDocs employees react to adoption of a cloud-based hosting

solution?

As Albert considered these and other questions, the only answer he felt sure about was that it was

an exciting time to be alive and working in the technology industry.

(Pigni 385)

By the middle of 2014, the computer systems that eLoanDocs had installed in 2009 were nearing

the end of their useful life and had no more capacity for expansion. As eLoanDocs prepares for

their next generation of data center hosting architecture for 2015 and beyond, the choices they

face are complex and will have significant implications for the future of the company.

1. Should eLoanDocs continue with their current model of designing, building, and

managing their own computer hosting infrastructure using their co-location partners?

2. Would eLoanDocs’ financial institution customers accept a move of eLoanDocs’

services to a public or private cloud provider?

3. How should eLoanDocs go about choosing a cloud hosting provider?

As Albert Michaels considered his options, his mind was roiled by a number of questions:

4. Will eLoanDocs’ customers—with their focus on data security—accept a cloud-based

solution? If so, to what degree? And how many customers would accept some form of

cloud-based solution?

5. If customers do accept one of the cost-saving cloud services solutions, what barriers

exist to prevent new competitors from rapidly entering the market and eroding

eLoanDocs’ market share?

6. What is the value that customers believe they are receiving from eLoanDocs?

7. Could it be that customers actually value the secure environment that they can visit

and audit in person? If so, might convincing those customers to adopt a cloud-based

solution to their document delivery problems actually be a damaging move to

eLoanDocs in the long term?

8. Speaking of security, which solution actually provides better protection of customers’

data? Though ownership of the hosting hardware enables eLoanDocs to literally pull

the plug if a breach is detected, how does that compare to the security benefits

associated with outsourcing to a cloud provider? Is one solution more likely than the

other to be targeted for attack? Is either solution better able to detect and prevent

intrusions?

9. Assuming that the system will be attacked at some point, what ability will

eLoanDocs have to identify the compromised data? How might that ability change if

hosting services are outsourced to a cloud provider?

10. How robust is the existing disaster recovery strategy? Which solution best fits the

redundancy needs of eLoanDocs?

11. How might the eLoanDocs employees react to adoption of a cloud-based hosting

solution?

As Albert considered these and other questions, the only answer he felt sure about was that it was

an exciting time to be alive and working in the technology industry.

(Pigni 385)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pigni, Gabriele Piccoli + F. Information Systems for Managers with Cases, Edition 3.1, 3rd

Edition. Prospect Press, 2015-12-28. VitalBook file.

Edition. Prospect Press, 2015-12-28. VitalBook file.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.