ABC Ltd Case Study: Financial Problems & Management Accounting System

VerifiedAdded on 2020/10/22

|13

|3948

|112

Case Study

AI Summary

This case study delves into the management accounting practices of ABC Ltd, a medium-sized manufacturing company. It examines various management accounting systems such as job costing, inventory management, and cost accounting, highlighting their benefits in decision-making and operational efficiency. The study explores different types of management accounting reports, including job cost, budget, and accounts receivable reports, emphasizing their role in evaluating profitability, controlling costs, and managing cash flow. It also discusses the advantages and disadvantages of planning tools like sales budgets, illustrating their use in resource allocation and performance evaluation. Furthermore, the case study applies marginal and absorption costing techniques to analyze ABC Ltd's financial performance, providing insights into profitability under different costing methods. Finally, it underscores how a robust management accounting system can help ABC Ltd address financial problems and improve its overall financial health. Desklib provides access to similar solved assignments and past papers for students.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and various kinds of accounting systems............................................3

Various kinds of management accounting reporting..................................................................3

Benefits of management accounting system...............................................................................4

Integration of management accounting system and reporting system........................................5

TASK 2............................................................................................................................................5

Practical.......................................................................................................................................5

TASK 3............................................................................................................................................8

Advantages and disadvantages of planning tools........................................................................8

Use of different planning tools ...................................................................................................9

TASK 4............................................................................................................................................9

Use of management accounting system to respond to the financial problems...........................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and various kinds of accounting systems............................................3

Various kinds of management accounting reporting..................................................................3

Benefits of management accounting system...............................................................................4

Integration of management accounting system and reporting system........................................5

TASK 2............................................................................................................................................5

Practical.......................................................................................................................................5

TASK 3............................................................................................................................................8

Advantages and disadvantages of planning tools........................................................................8

Use of different planning tools ...................................................................................................9

TASK 4............................................................................................................................................9

Use of management accounting system to respond to the financial problems...........................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Managerial accounting or the management accounting may be defined as the use of the

accounting information and all the financial statements in order to make the decisions for the

company and its growth. This case study is on the company ABC Ltd which is a medium sized

company in the manufacturing sector. The present study will discuss about the different kinds of

the management accounting system along with the different types of management accounting

reporting (Alsharari, Dixon and Youssef, 2015). Further it will outline some advantages and the

disadvantages of the planning tools and their use in the company. At last it will highlight that

how management accounting system helps in solving the financial problems.

TASK 1

Management accounting and various kinds of accounting systems

The management accounting is a concept wherein the management of the company takes

the important decisions regarding the operations and the working of the company with help of

analysis and evaluation of the financial information and the financial statements. There are many

kinds of management accounting system which are discussed in the following points-

Job costing system- the job costing relates to the estimation of cost of every job in the

production process to ascertain the actual cost of producing the product. The job costing system

works in gathering three types of cost that is direct labor, overhead cost and direct materials. This

is required by ABC Ltd in order to maintain all the cost relating to the job.

Inventory management system- this involves the management of the inventory in the

business through the recording of the inflow and outflow of the raw material and finished goods.

This helps in the planning of the production of goods by production department. This is required

by ABC Ltd in order to maintain all the cost relating to the inventory and the finished goods.

Cost accounting system- it refers to the recording of the cost of production of any

product. This system is used by the company in order to estimate all the cost which may be

incurred by the company relating to the products like production cost, management cost,

inventory cost and many other costs. This is required by ABC Ltd in order to maintain all the

cost relating to the whole organization.

Various kinds of management accounting reporting

The management accounting reports are the documents or the reports which are prepared

in order to store and record all the data relating to management and operations of the company

Managerial accounting or the management accounting may be defined as the use of the

accounting information and all the financial statements in order to make the decisions for the

company and its growth. This case study is on the company ABC Ltd which is a medium sized

company in the manufacturing sector. The present study will discuss about the different kinds of

the management accounting system along with the different types of management accounting

reporting (Alsharari, Dixon and Youssef, 2015). Further it will outline some advantages and the

disadvantages of the planning tools and their use in the company. At last it will highlight that

how management accounting system helps in solving the financial problems.

TASK 1

Management accounting and various kinds of accounting systems

The management accounting is a concept wherein the management of the company takes

the important decisions regarding the operations and the working of the company with help of

analysis and evaluation of the financial information and the financial statements. There are many

kinds of management accounting system which are discussed in the following points-

Job costing system- the job costing relates to the estimation of cost of every job in the

production process to ascertain the actual cost of producing the product. The job costing system

works in gathering three types of cost that is direct labor, overhead cost and direct materials. This

is required by ABC Ltd in order to maintain all the cost relating to the job.

Inventory management system- this involves the management of the inventory in the

business through the recording of the inflow and outflow of the raw material and finished goods.

This helps in the planning of the production of goods by production department. This is required

by ABC Ltd in order to maintain all the cost relating to the inventory and the finished goods.

Cost accounting system- it refers to the recording of the cost of production of any

product. This system is used by the company in order to estimate all the cost which may be

incurred by the company relating to the products like production cost, management cost,

inventory cost and many other costs. This is required by ABC Ltd in order to maintain all the

cost relating to the whole organization.

Various kinds of management accounting reporting

The management accounting reports are the documents or the reports which are prepared

in order to store and record all the data relating to management and operations of the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on daily basis and then analyzing that data in order to take the decision (Armstrong, 2014). These

types of reports are then used to interpret and evaluate the data and to take the decision relating

to management. The different types of management accounting reports are as follows-

Job cost reports- these are the types of reports which are prepared in respect of a

particular job or project (Boučková, 2015). This report helps the management of the ABC Ltd in

knowing and evaluating the requirements and the profitability of all the jobs and their operations.

Budget reports- these are the most crucial for the company which is to be prepared. This

is because of the reason that it helps the owners of the company ABC Ltd in beforehand

understand and control all the estimated cost so that losses can be minimized.

Account receivable report- the accounts receivable reports shows the cash flow within

the company ABC Ltd. By the continuous evaluation of the accounts receivable reports the

company can handle its collections effectively and there can be no overlooking of the debtors.

Benefits of management accounting system

The management accounting system refers to a system which is internal to the

organization and is used to manage the company and takes the decisions for the growth and the

betterment of the company. With the application of the management accounting the company can

have many benefits. Some benefits are as follows-

The management accounting systems like job costing, cost accounting etc. helps the

business in doing proper planning relating to the business because the budget helps the

company in taking more effective and efficient decisions (Quattrone, 2016).

With the help of the management accounting system much information can be depicted in

the form of charts, bar, diagrams so it helps in proper forecasting, analyzing and

evaluating the managerial policies and strategies used.

Through the management accounting system there is two way communication in ABC

Ltd. The top management plans and delegates work to lower staff. Also, lower staff

prepares reports and submit it to top management. This two way communication induces

sense of responsibility and also improves work conditions.

Because of the proper recording and reporting of data on time there is always timely data

available as and when needed which increases the functionality of task there by

improving efficiency of organization.

(Kaplan and Atkinson, 2015).

types of reports are then used to interpret and evaluate the data and to take the decision relating

to management. The different types of management accounting reports are as follows-

Job cost reports- these are the types of reports which are prepared in respect of a

particular job or project (Boučková, 2015). This report helps the management of the ABC Ltd in

knowing and evaluating the requirements and the profitability of all the jobs and their operations.

Budget reports- these are the most crucial for the company which is to be prepared. This

is because of the reason that it helps the owners of the company ABC Ltd in beforehand

understand and control all the estimated cost so that losses can be minimized.

Account receivable report- the accounts receivable reports shows the cash flow within

the company ABC Ltd. By the continuous evaluation of the accounts receivable reports the

company can handle its collections effectively and there can be no overlooking of the debtors.

Benefits of management accounting system

The management accounting system refers to a system which is internal to the

organization and is used to manage the company and takes the decisions for the growth and the

betterment of the company. With the application of the management accounting the company can

have many benefits. Some benefits are as follows-

The management accounting systems like job costing, cost accounting etc. helps the

business in doing proper planning relating to the business because the budget helps the

company in taking more effective and efficient decisions (Quattrone, 2016).

With the help of the management accounting system much information can be depicted in

the form of charts, bar, diagrams so it helps in proper forecasting, analyzing and

evaluating the managerial policies and strategies used.

Through the management accounting system there is two way communication in ABC

Ltd. The top management plans and delegates work to lower staff. Also, lower staff

prepares reports and submit it to top management. This two way communication induces

sense of responsibility and also improves work conditions.

Because of the proper recording and reporting of data on time there is always timely data

available as and when needed which increases the functionality of task there by

improving efficiency of organization.

(Kaplan and Atkinson, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As the management reports are prepared from time- to- time so it helps the company in

keeping eye over all the business and if any non performing activities are identified then

corrective actions are taken in order to improve those activities.

As the management accounting system involves the division of work between various

authorities it helps the authorities in knowing the responsibility and acting accordingly.

This management accounting system helps the ABC Ltd in managing there all the costs like the

material, variable, fixed or the overhead cost with help of different management accounting

system like inventory management costing, job costing, cost accounting and many more. Also,

the application of management accounting system in ABC Ltd helps in properly plan and execute

activities for maintaining and improving the future of the company.

Integration of management accounting system and reporting system

The managerial accounting refers to as the process through which the managers takes the

decisions by taking in consideration the accounting information and the financial statements. On

the other hand, the management reporting refers to as the preparation of the report in which all

the related data is stored and analyzed (Vasarhelyi, Kogan and Tuttle, 2015). The management

accounting reporting and the management accounting system both are very crucial and important

in the business. With the integration of both these systems there is easy flow of information

through reporting and accounting and because of this the goals and objectives of the company

are accomplished properly and efficiently. The integrated use of both the management

accounting and the reports improves the responsibility, accountability and present-ability in

organization and its employees.

TASK 2

Practical

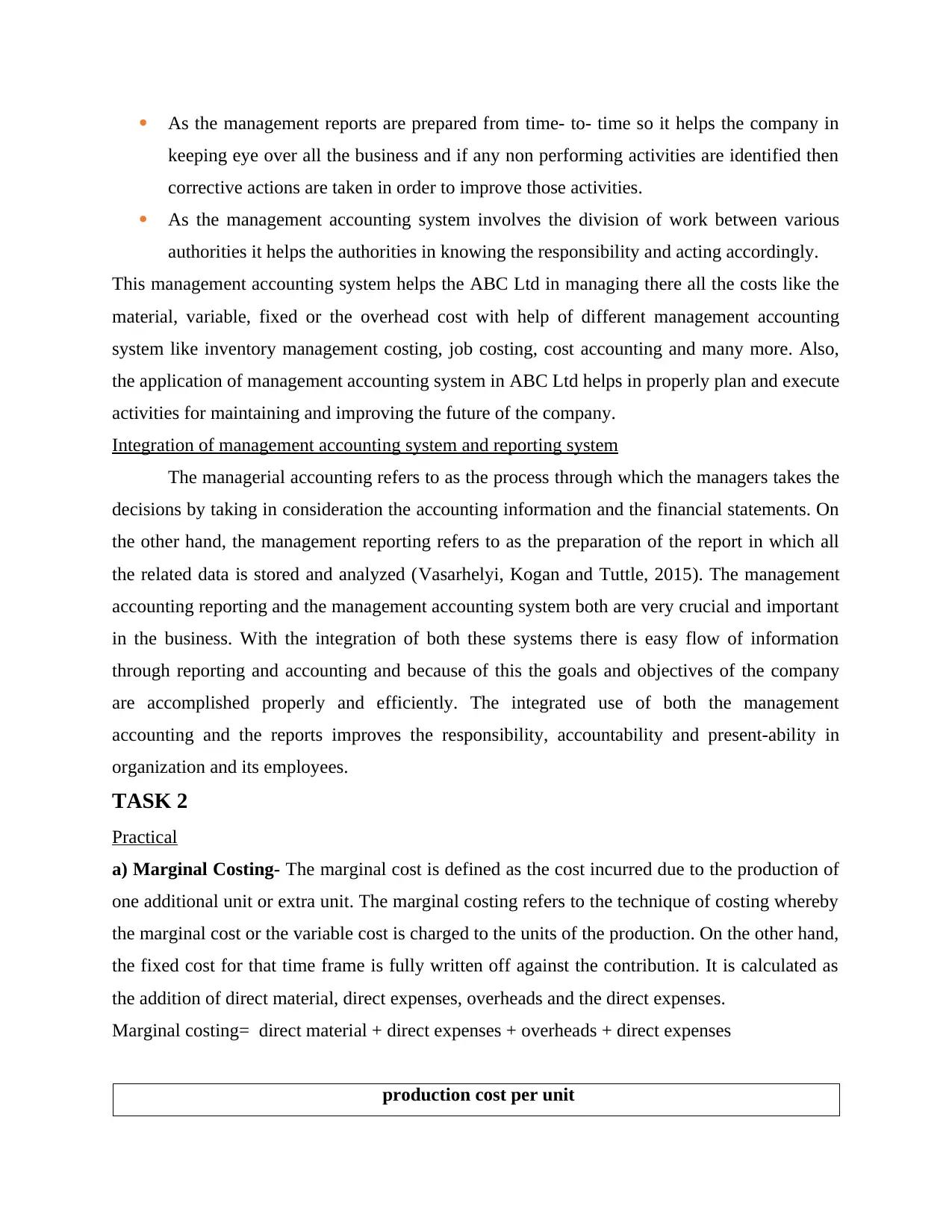

a) Marginal Costing- The marginal cost is defined as the cost incurred due to the production of

one additional unit or extra unit. The marginal costing refers to the technique of costing whereby

the marginal cost or the variable cost is charged to the units of the production. On the other hand,

the fixed cost for that time frame is fully written off against the contribution. It is calculated as

the addition of direct material, direct expenses, overheads and the direct expenses.

Marginal costing= direct material + direct expenses + overheads + direct expenses

production cost per unit

keeping eye over all the business and if any non performing activities are identified then

corrective actions are taken in order to improve those activities.

As the management accounting system involves the division of work between various

authorities it helps the authorities in knowing the responsibility and acting accordingly.

This management accounting system helps the ABC Ltd in managing there all the costs like the

material, variable, fixed or the overhead cost with help of different management accounting

system like inventory management costing, job costing, cost accounting and many more. Also,

the application of management accounting system in ABC Ltd helps in properly plan and execute

activities for maintaining and improving the future of the company.

Integration of management accounting system and reporting system

The managerial accounting refers to as the process through which the managers takes the

decisions by taking in consideration the accounting information and the financial statements. On

the other hand, the management reporting refers to as the preparation of the report in which all

the related data is stored and analyzed (Vasarhelyi, Kogan and Tuttle, 2015). The management

accounting reporting and the management accounting system both are very crucial and important

in the business. With the integration of both these systems there is easy flow of information

through reporting and accounting and because of this the goals and objectives of the company

are accomplished properly and efficiently. The integrated use of both the management

accounting and the reports improves the responsibility, accountability and present-ability in

organization and its employees.

TASK 2

Practical

a) Marginal Costing- The marginal cost is defined as the cost incurred due to the production of

one additional unit or extra unit. The marginal costing refers to the technique of costing whereby

the marginal cost or the variable cost is charged to the units of the production. On the other hand,

the fixed cost for that time frame is fully written off against the contribution. It is calculated as

the addition of direct material, direct expenses, overheads and the direct expenses.

Marginal costing= direct material + direct expenses + overheads + direct expenses

production cost per unit

Cost of Direct material 10

Cost of direct labour 20

variable production overhead 5

Fixed production overhead costs 5

40

Total production cost

Units produced 18000

cost per unit 40

Total production costs 720000

Total cost of sales

Direct material 10

Direct labour 20

variable overhead costs 5

Fixed overhead cots 5

18000*40 720000

less closing stock 2000*40 80000

Cost of sales 640000

profit or loss statement for the month January

Marginal costing (Budgeted)

Details Amount(£)

Sales 800000

Less: Direct material 18000*10 180000

Cost of direct labour 20

variable production overhead 5

Fixed production overhead costs 5

40

Total production cost

Units produced 18000

cost per unit 40

Total production costs 720000

Total cost of sales

Direct material 10

Direct labour 20

variable overhead costs 5

Fixed overhead cots 5

18000*40 720000

less closing stock 2000*40 80000

Cost of sales 640000

profit or loss statement for the month January

Marginal costing (Budgeted)

Details Amount(£)

Sales 800000

Less: Direct material 18000*10 180000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

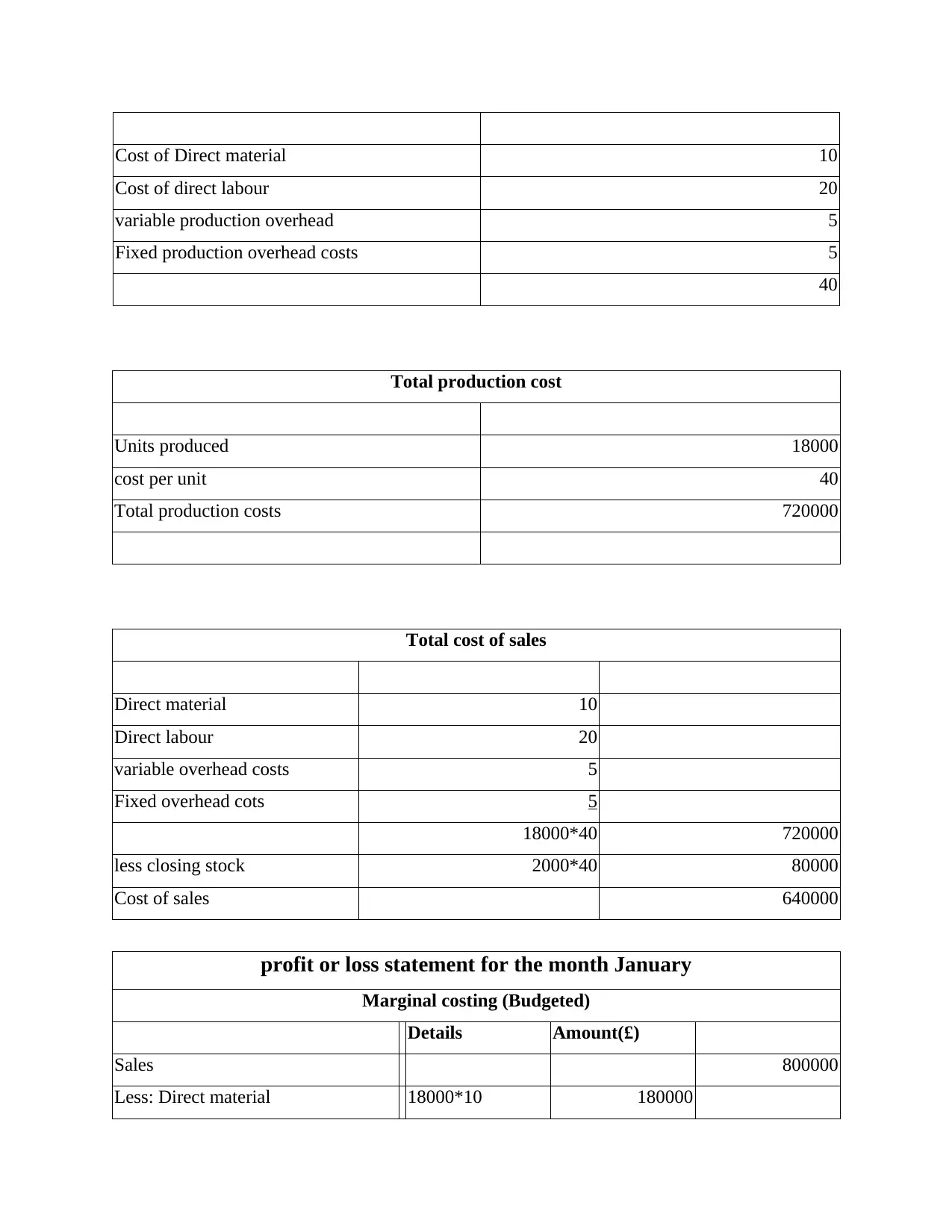

Direct labour 18000*20 360000

variable cost of production 18000*5 90000

630000 -630000

1430000

Less: closing inventory 2000*35 70000 -70000

contribution 1500000

Less fixed costs 18000*5 90000 -90000

1590000

profit or loss statement for the month January

Marginal costing (Actual)

Details Amount(£)

Sales 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of production 19000*5 95000

665000 -665000

1465000

Less: closing inventory 3000*35 105000 -105000

contribution 1570000

Less fixed cost of production 19000*5 95000 -95000

Profit . 1665000

b) Absorption Costing- the absorption costing means that all the cost relating to the

manufacturing are been absorbed or being assigned to all the units produced or manufactured

(Padovani, Orelli and Young, 2014). It is a method of valuing the inventory by the process of

assigning all the variable and the fixed cost which are incurred at time of production.

variable cost of production 18000*5 90000

630000 -630000

1430000

Less: closing inventory 2000*35 70000 -70000

contribution 1500000

Less fixed costs 18000*5 90000 -90000

1590000

profit or loss statement for the month January

Marginal costing (Actual)

Details Amount(£)

Sales 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of production 19000*5 95000

665000 -665000

1465000

Less: closing inventory 3000*35 105000 -105000

contribution 1570000

Less fixed cost of production 19000*5 95000 -95000

Profit . 1665000

b) Absorption Costing- the absorption costing means that all the cost relating to the

manufacturing are been absorbed or being assigned to all the units produced or manufactured

(Padovani, Orelli and Young, 2014). It is a method of valuing the inventory by the process of

assigning all the variable and the fixed cost which are incurred at time of production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

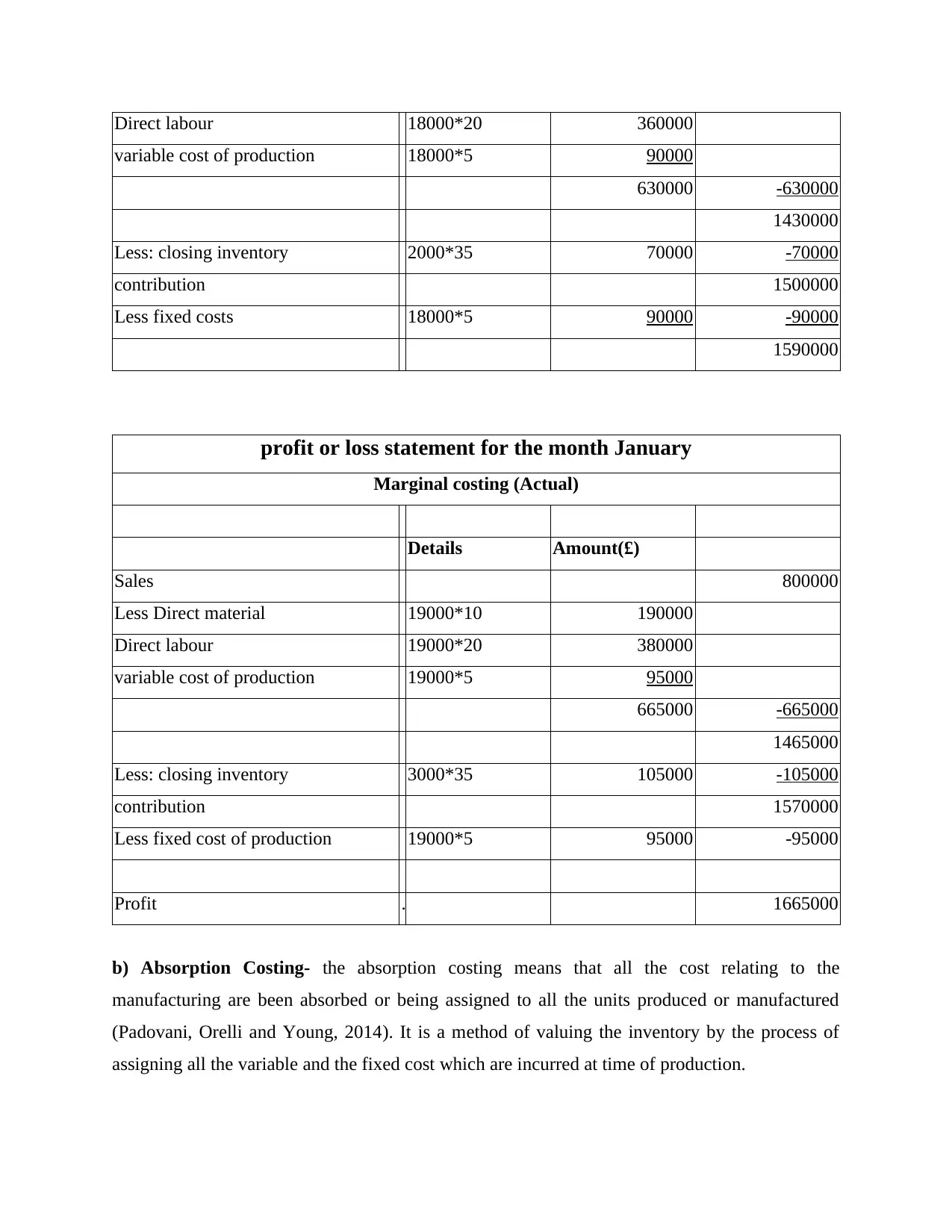

profit or loss statement for the month January

Absorption costing (Budgeted)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 18000*10 180000

Direct labour 18000*20 360000

variable cost of

production 18000*5 90000

Less fixed cost of

production 18000*5 90000

720000 720000

Less: closing inventory 2000*40 80000

640000 640000

560000

profit or loss statement for the month January

Absorption costing (Actual)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of

production 19000*5 95000

Less fixed cost of

production 19000*5 95000

760000 760000

Less: closing inventory 3000*40 120000

80000

Absorption costing (Budgeted)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 18000*10 180000

Direct labour 18000*20 360000

variable cost of

production 18000*5 90000

Less fixed cost of

production 18000*5 90000

720000 720000

Less: closing inventory 2000*40 80000

640000 640000

560000

profit or loss statement for the month January

Absorption costing (Actual)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of

production 19000*5 95000

Less fixed cost of

production 19000*5 95000

760000 760000

Less: closing inventory 3000*40 120000

80000

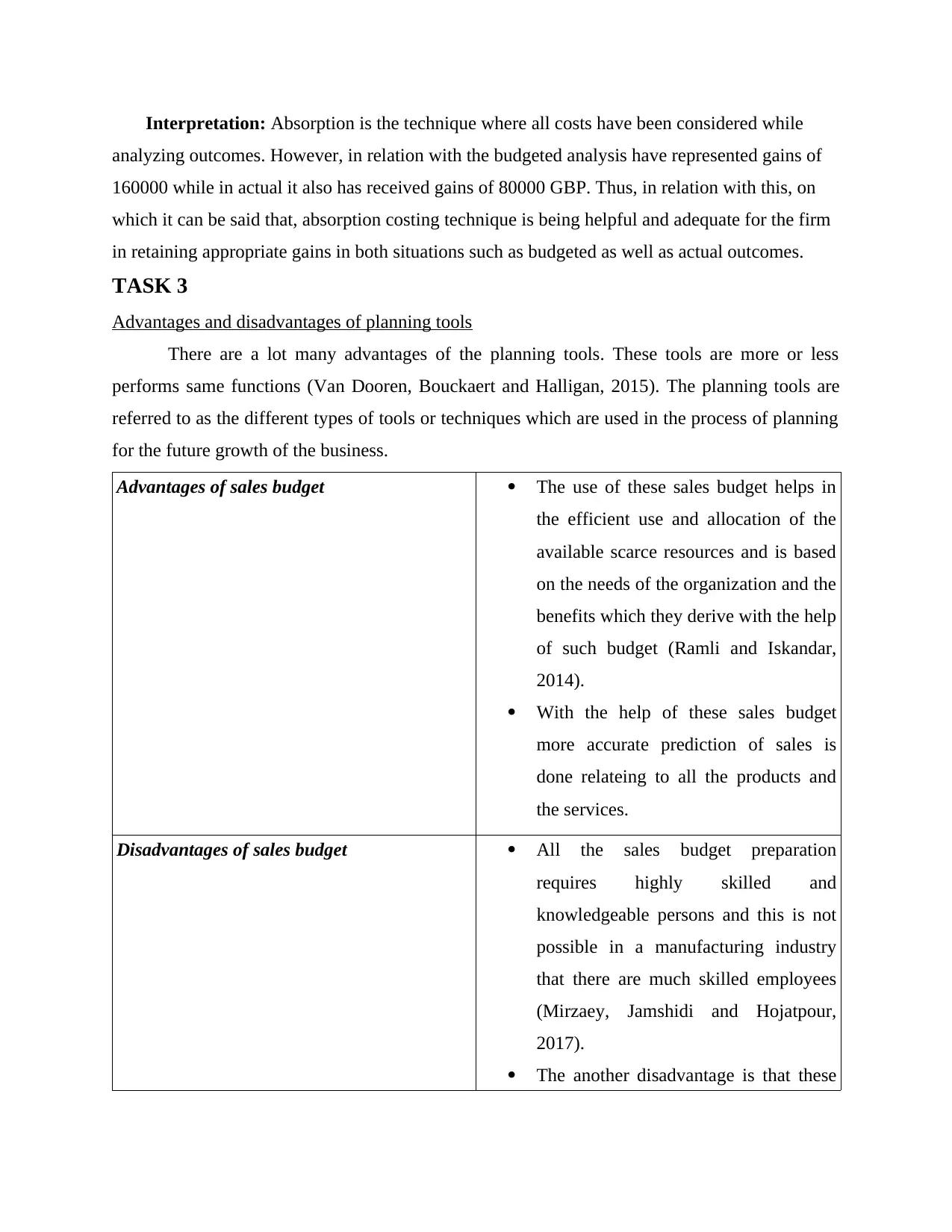

Interpretation: Absorption is the technique where all costs have been considered while

analyzing outcomes. However, in relation with the budgeted analysis have represented gains of

160000 while in actual it also has received gains of 80000 GBP. Thus, in relation with this, on

which it can be said that, absorption costing technique is being helpful and adequate for the firm

in retaining appropriate gains in both situations such as budgeted as well as actual outcomes.

TASK 3

Advantages and disadvantages of planning tools

There are a lot many advantages of the planning tools. These tools are more or less

performs same functions (Van Dooren, Bouckaert and Halligan, 2015). The planning tools are

referred to as the different types of tools or techniques which are used in the process of planning

for the future growth of the business.

Advantages of sales budget The use of these sales budget helps in

the efficient use and allocation of the

available scarce resources and is based

on the needs of the organization and the

benefits which they derive with the help

of such budget (Ramli and Iskandar,

2014).

With the help of these sales budget

more accurate prediction of sales is

done relateing to all the products and

the services.

Disadvantages of sales budget All the sales budget preparation

requires highly skilled and

knowledgeable persons and this is not

possible in a manufacturing industry

that there are much skilled employees

(Mirzaey, Jamshidi and Hojatpour,

2017).

The another disadvantage is that these

analyzing outcomes. However, in relation with the budgeted analysis have represented gains of

160000 while in actual it also has received gains of 80000 GBP. Thus, in relation with this, on

which it can be said that, absorption costing technique is being helpful and adequate for the firm

in retaining appropriate gains in both situations such as budgeted as well as actual outcomes.

TASK 3

Advantages and disadvantages of planning tools

There are a lot many advantages of the planning tools. These tools are more or less

performs same functions (Van Dooren, Bouckaert and Halligan, 2015). The planning tools are

referred to as the different types of tools or techniques which are used in the process of planning

for the future growth of the business.

Advantages of sales budget The use of these sales budget helps in

the efficient use and allocation of the

available scarce resources and is based

on the needs of the organization and the

benefits which they derive with the help

of such budget (Ramli and Iskandar,

2014).

With the help of these sales budget

more accurate prediction of sales is

done relateing to all the products and

the services.

Disadvantages of sales budget All the sales budget preparation

requires highly skilled and

knowledgeable persons and this is not

possible in a manufacturing industry

that there are much skilled employees

(Mirzaey, Jamshidi and Hojatpour,

2017).

The another disadvantage is that these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

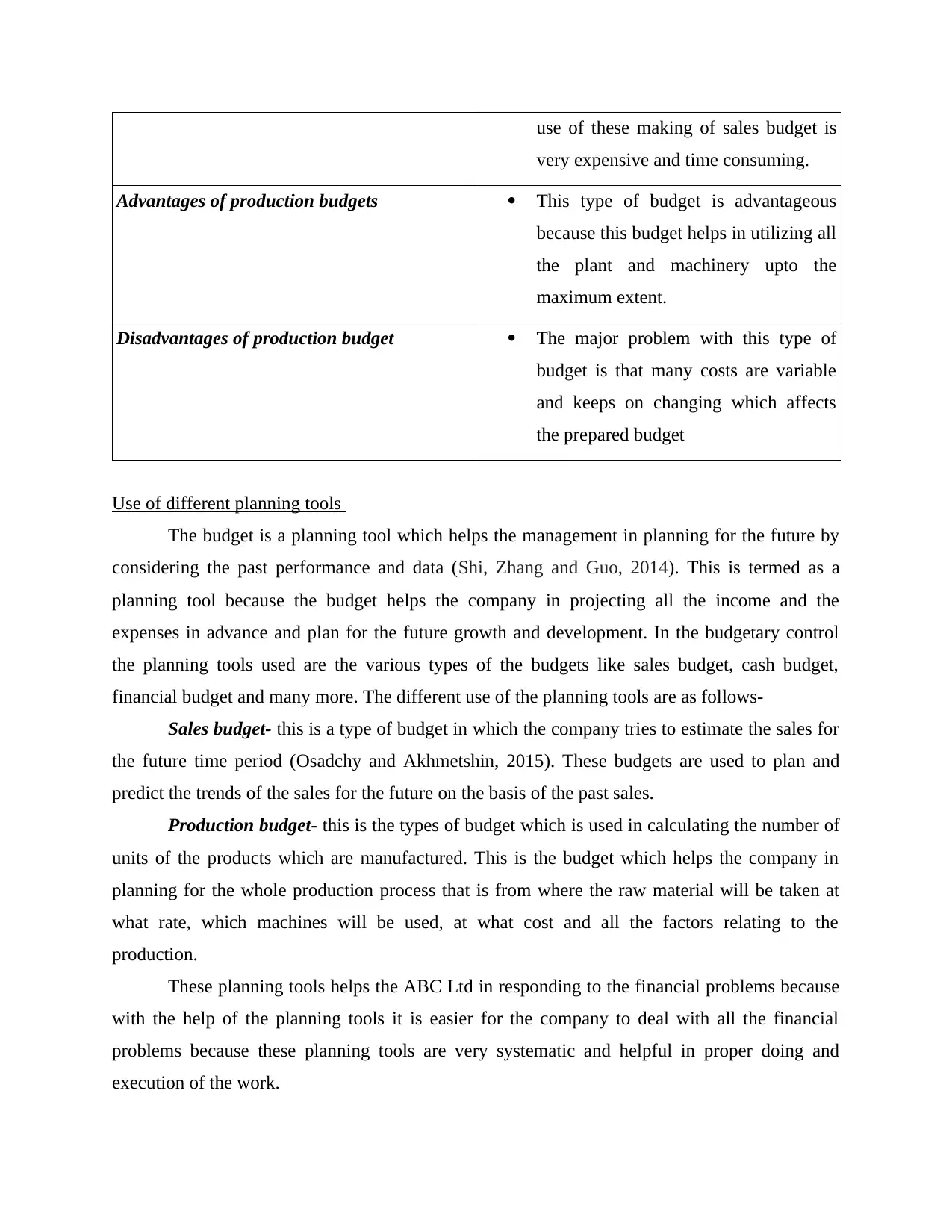

use of these making of sales budget is

very expensive and time consuming.

Advantages of production budgets This type of budget is advantageous

because this budget helps in utilizing all

the plant and machinery upto the

maximum extent.

Disadvantages of production budget The major problem with this type of

budget is that many costs are variable

and keeps on changing which affects

the prepared budget

Use of different planning tools

The budget is a planning tool which helps the management in planning for the future by

considering the past performance and data (Shi, Zhang and Guo, 2014). This is termed as a

planning tool because the budget helps the company in projecting all the income and the

expenses in advance and plan for the future growth and development. In the budgetary control

the planning tools used are the various types of the budgets like sales budget, cash budget,

financial budget and many more. The different use of the planning tools are as follows-

Sales budget- this is a type of budget in which the company tries to estimate the sales for

the future time period (Osadchy and Akhmetshin, 2015). These budgets are used to plan and

predict the trends of the sales for the future on the basis of the past sales.

Production budget- this is the types of budget which is used in calculating the number of

units of the products which are manufactured. This is the budget which helps the company in

planning for the whole production process that is from where the raw material will be taken at

what rate, which machines will be used, at what cost and all the factors relating to the

production.

These planning tools helps the ABC Ltd in responding to the financial problems because

with the help of the planning tools it is easier for the company to deal with all the financial

problems because these planning tools are very systematic and helpful in proper doing and

execution of the work.

very expensive and time consuming.

Advantages of production budgets This type of budget is advantageous

because this budget helps in utilizing all

the plant and machinery upto the

maximum extent.

Disadvantages of production budget The major problem with this type of

budget is that many costs are variable

and keeps on changing which affects

the prepared budget

Use of different planning tools

The budget is a planning tool which helps the management in planning for the future by

considering the past performance and data (Shi, Zhang and Guo, 2014). This is termed as a

planning tool because the budget helps the company in projecting all the income and the

expenses in advance and plan for the future growth and development. In the budgetary control

the planning tools used are the various types of the budgets like sales budget, cash budget,

financial budget and many more. The different use of the planning tools are as follows-

Sales budget- this is a type of budget in which the company tries to estimate the sales for

the future time period (Osadchy and Akhmetshin, 2015). These budgets are used to plan and

predict the trends of the sales for the future on the basis of the past sales.

Production budget- this is the types of budget which is used in calculating the number of

units of the products which are manufactured. This is the budget which helps the company in

planning for the whole production process that is from where the raw material will be taken at

what rate, which machines will be used, at what cost and all the factors relating to the

production.

These planning tools helps the ABC Ltd in responding to the financial problems because

with the help of the planning tools it is easier for the company to deal with all the financial

problems because these planning tools are very systematic and helpful in proper doing and

execution of the work.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

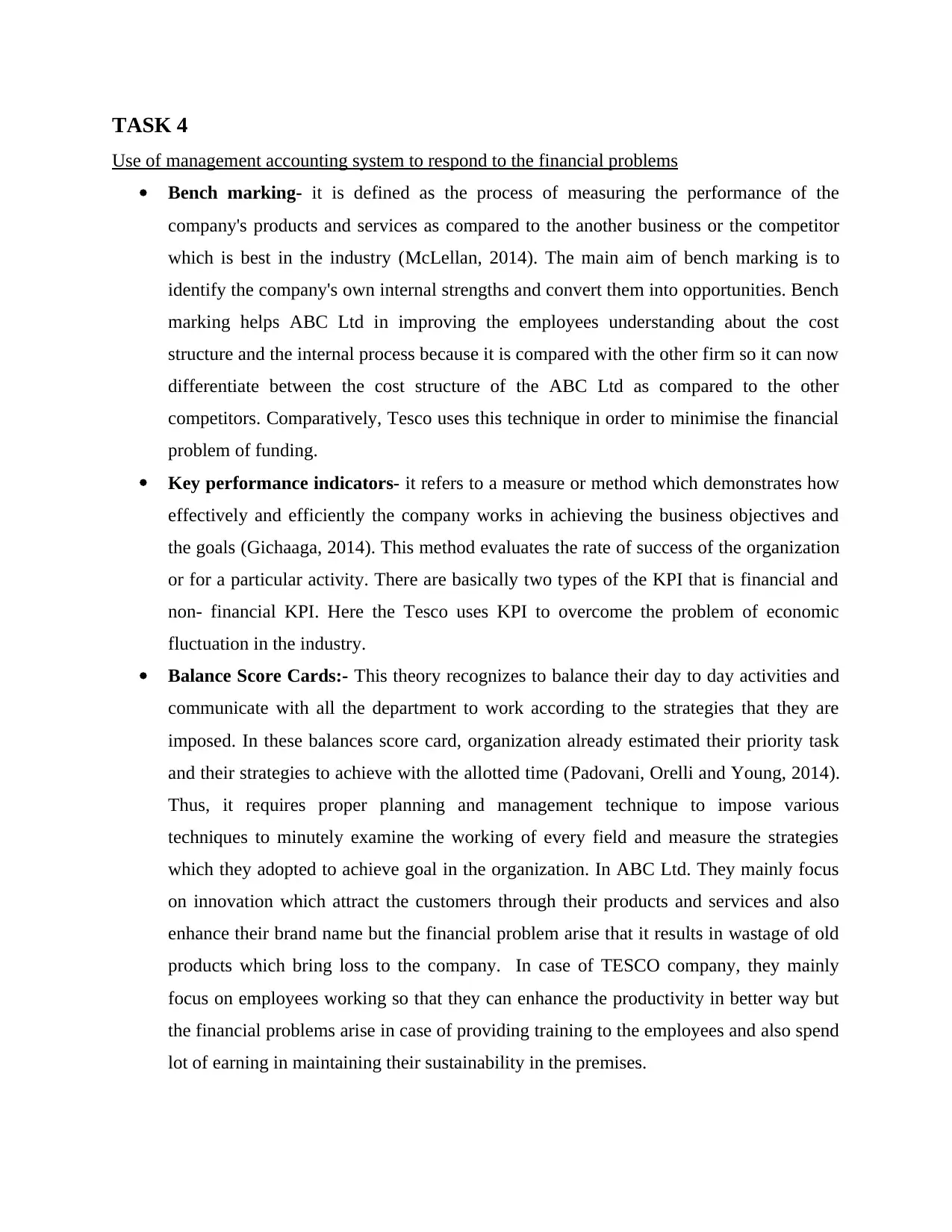

Use of management accounting system to respond to the financial problems

Bench marking- it is defined as the process of measuring the performance of the

company's products and services as compared to the another business or the competitor

which is best in the industry (McLellan, 2014). The main aim of bench marking is to

identify the company's own internal strengths and convert them into opportunities. Bench

marking helps ABC Ltd in improving the employees understanding about the cost

structure and the internal process because it is compared with the other firm so it can now

differentiate between the cost structure of the ABC Ltd as compared to the other

competitors. Comparatively, Tesco uses this technique in order to minimise the financial

problem of funding.

Key performance indicators- it refers to a measure or method which demonstrates how

effectively and efficiently the company works in achieving the business objectives and

the goals (Gichaaga, 2014). This method evaluates the rate of success of the organization

or for a particular activity. There are basically two types of the KPI that is financial and

non- financial KPI. Here the Tesco uses KPI to overcome the problem of economic

fluctuation in the industry.

Balance Score Cards:- This theory recognizes to balance their day to day activities and

communicate with all the department to work according to the strategies that they are

imposed. In these balances score card, organization already estimated their priority task

and their strategies to achieve with the allotted time (Padovani, Orelli and Young, 2014).

Thus, it requires proper planning and management technique to impose various

techniques to minutely examine the working of every field and measure the strategies

which they adopted to achieve goal in the organization. In ABC Ltd. They mainly focus

on innovation which attract the customers through their products and services and also

enhance their brand name but the financial problem arise that it results in wastage of old

products which bring loss to the company. In case of TESCO company, they mainly

focus on employees working so that they can enhance the productivity in better way but

the financial problems arise in case of providing training to the employees and also spend

lot of earning in maintaining their sustainability in the premises.

Use of management accounting system to respond to the financial problems

Bench marking- it is defined as the process of measuring the performance of the

company's products and services as compared to the another business or the competitor

which is best in the industry (McLellan, 2014). The main aim of bench marking is to

identify the company's own internal strengths and convert them into opportunities. Bench

marking helps ABC Ltd in improving the employees understanding about the cost

structure and the internal process because it is compared with the other firm so it can now

differentiate between the cost structure of the ABC Ltd as compared to the other

competitors. Comparatively, Tesco uses this technique in order to minimise the financial

problem of funding.

Key performance indicators- it refers to a measure or method which demonstrates how

effectively and efficiently the company works in achieving the business objectives and

the goals (Gichaaga, 2014). This method evaluates the rate of success of the organization

or for a particular activity. There are basically two types of the KPI that is financial and

non- financial KPI. Here the Tesco uses KPI to overcome the problem of economic

fluctuation in the industry.

Balance Score Cards:- This theory recognizes to balance their day to day activities and

communicate with all the department to work according to the strategies that they are

imposed. In these balances score card, organization already estimated their priority task

and their strategies to achieve with the allotted time (Padovani, Orelli and Young, 2014).

Thus, it requires proper planning and management technique to impose various

techniques to minutely examine the working of every field and measure the strategies

which they adopted to achieve goal in the organization. In ABC Ltd. They mainly focus

on innovation which attract the customers through their products and services and also

enhance their brand name but the financial problem arise that it results in wastage of old

products which bring loss to the company. In case of TESCO company, they mainly

focus on employees working so that they can enhance the productivity in better way but

the financial problems arise in case of providing training to the employees and also spend

lot of earning in maintaining their sustainability in the premises.

Variance analysis:- In this analysis it determines the actual results between the estimated

results. As mainly organization adopted this strategy so that they prepared themselves to

take risk in the market. Through this analysis they maintain a control in the business

regarding the expenses which incurred without any use. In case of ABC Ltd., they can

solve their financial problem through this strategy (Mirzaey, Jamshidi and Hojatpour,

2017).In case of ABC Ltd. they use the estimated strategy to make budget, this is helpful

for them to examine the income and losses occurred during the financial year and also

reflect the strong financial stability similarly in cases of Tesco company they mainly

focus on actual analysis, which mainly results in loss to the company as the market

usually fluctuates due to changes in tax rates.

Cost-Volume-Profits Analysis:- In this planning tool, companies can examine the cost

incurred and the profits raised from such products and through this process the exact

volume is examined. Thus, it includes the sale prices, the cost which is fixed for the

products and the prices which raises from the sale of such products to recognize the

volume of the products. In this analysis it firstly recognizes the amount of sales which is

left as the fixed cost and then it is deducted in terms of profits (Vasarhelyi, Kogan and

Tuttle, 2015). In case of ABC Ltd. they can analyse the sales costs are fixed and then the

profits which they earned through their activities but in relation to Tesco company they

use the sales cost as variable which affects their financial matters in case of fluctuation in

prices or resources availability.

As from the above planning tool, Balance score card is useful for the ABC Ltd. to solve

their financial matters. As they can refer the strategy for various department and also impose

strategic position to work accordingly. They minutely examined the working of the employees,

so that they can save for future use (Quattrone, 2016).

CONCLUSION

According to the above study it can be concluded that management accounting helps the

organisation to manage their internal activities which helps in taking effective decisions. As if

the accounts are managed in appropriate way it guides the other department to use various

strategies to achieve goal for longer term (Management accounting). It also reflects the stability

of the company if it is made in proper way as many investors and lender watches the stability and

integrity of the company if they mange their internal team effectively. It is the duty of the

results. As mainly organization adopted this strategy so that they prepared themselves to

take risk in the market. Through this analysis they maintain a control in the business

regarding the expenses which incurred without any use. In case of ABC Ltd., they can

solve their financial problem through this strategy (Mirzaey, Jamshidi and Hojatpour,

2017).In case of ABC Ltd. they use the estimated strategy to make budget, this is helpful

for them to examine the income and losses occurred during the financial year and also

reflect the strong financial stability similarly in cases of Tesco company they mainly

focus on actual analysis, which mainly results in loss to the company as the market

usually fluctuates due to changes in tax rates.

Cost-Volume-Profits Analysis:- In this planning tool, companies can examine the cost

incurred and the profits raised from such products and through this process the exact

volume is examined. Thus, it includes the sale prices, the cost which is fixed for the

products and the prices which raises from the sale of such products to recognize the

volume of the products. In this analysis it firstly recognizes the amount of sales which is

left as the fixed cost and then it is deducted in terms of profits (Vasarhelyi, Kogan and

Tuttle, 2015). In case of ABC Ltd. they can analyse the sales costs are fixed and then the

profits which they earned through their activities but in relation to Tesco company they

use the sales cost as variable which affects their financial matters in case of fluctuation in

prices or resources availability.

As from the above planning tool, Balance score card is useful for the ABC Ltd. to solve

their financial matters. As they can refer the strategy for various department and also impose

strategic position to work accordingly. They minutely examined the working of the employees,

so that they can save for future use (Quattrone, 2016).

CONCLUSION

According to the above study it can be concluded that management accounting helps the

organisation to manage their internal activities which helps in taking effective decisions. As if

the accounts are managed in appropriate way it guides the other department to use various

strategies to achieve goal for longer term (Management accounting). It also reflects the stability

of the company if it is made in proper way as many investors and lender watches the stability and

integrity of the company if they mange their internal team effectively. It is the duty of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.