Financial Planning Report: FIN3CP, Retirement Planning Analysis

VerifiedAdded on 2020/03/23

|26

|5253

|42

Report

AI Summary

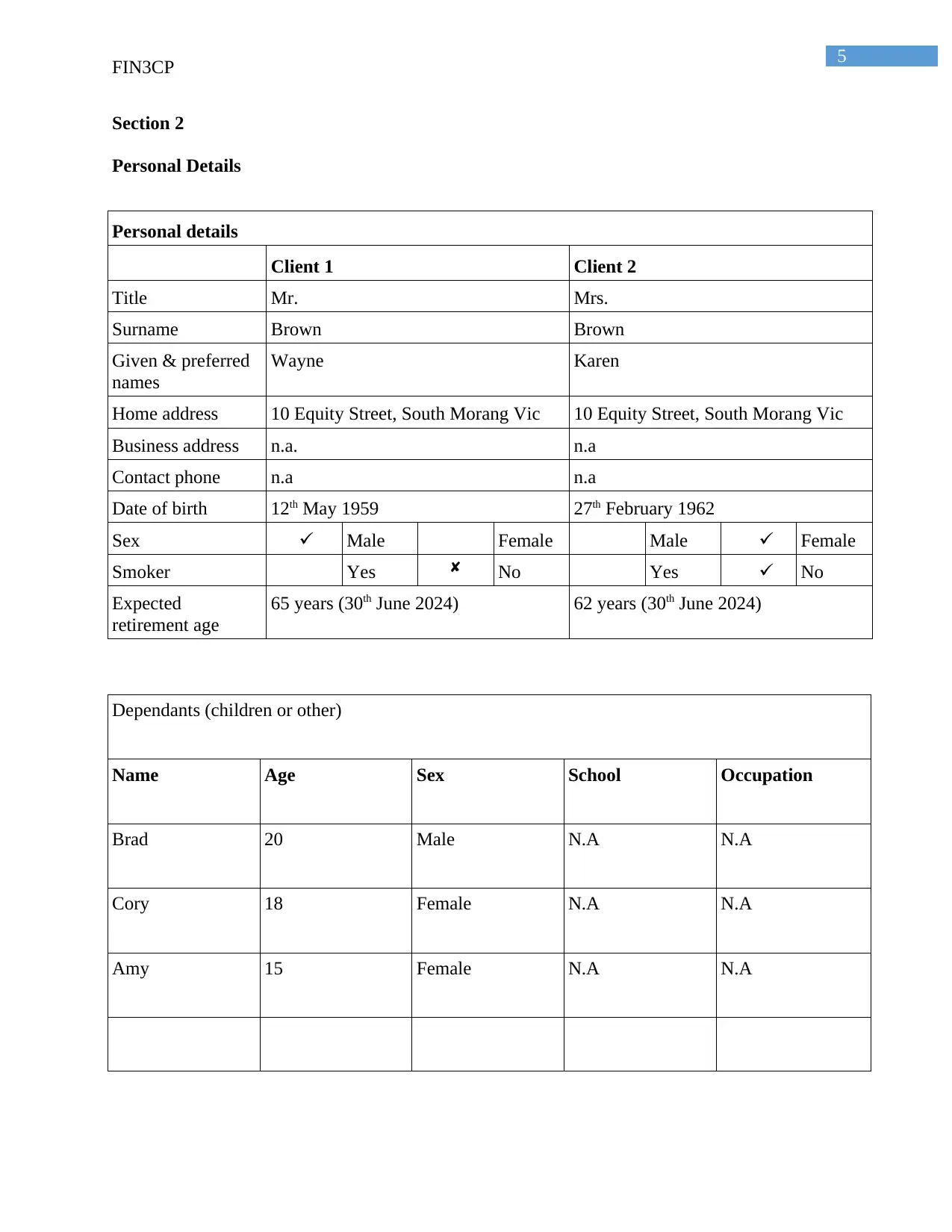

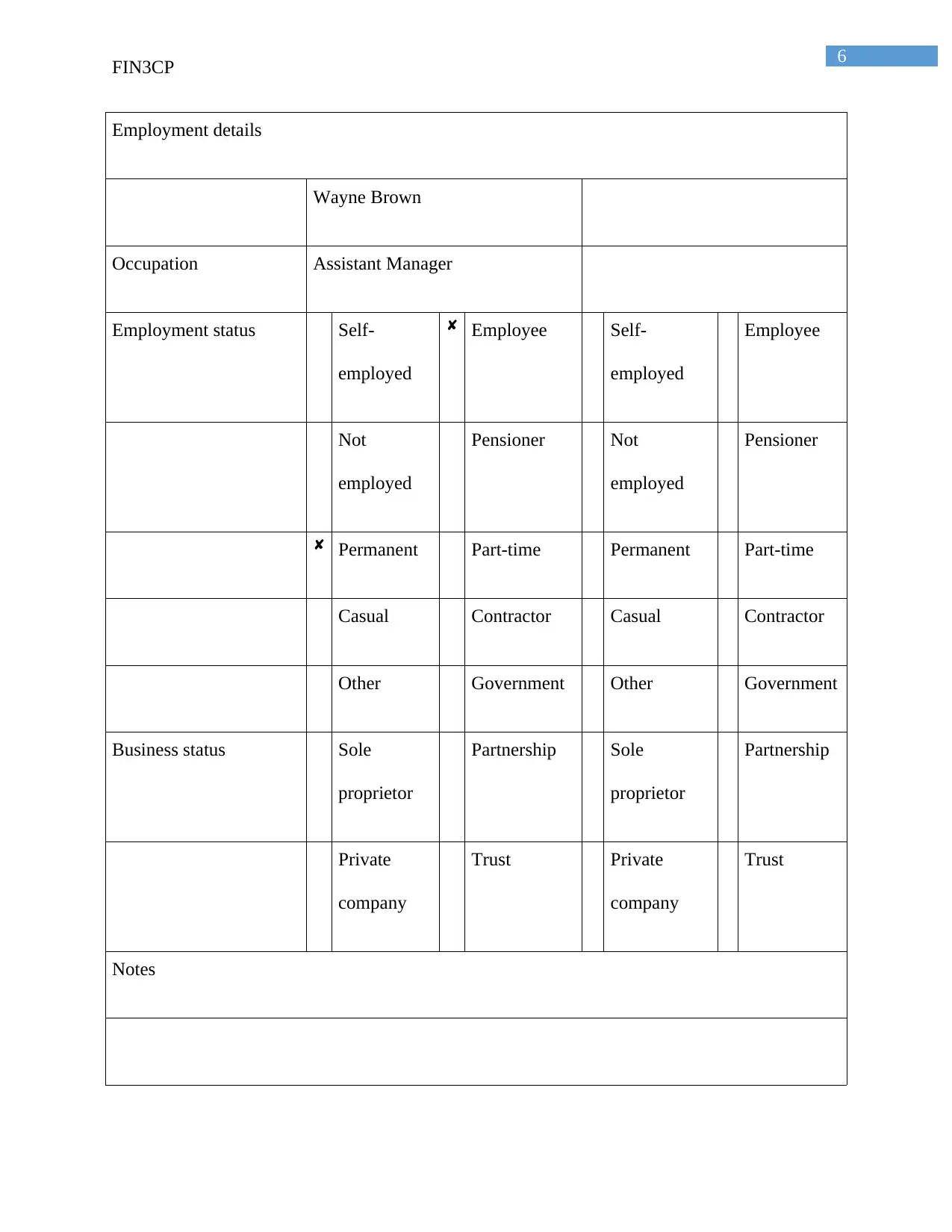

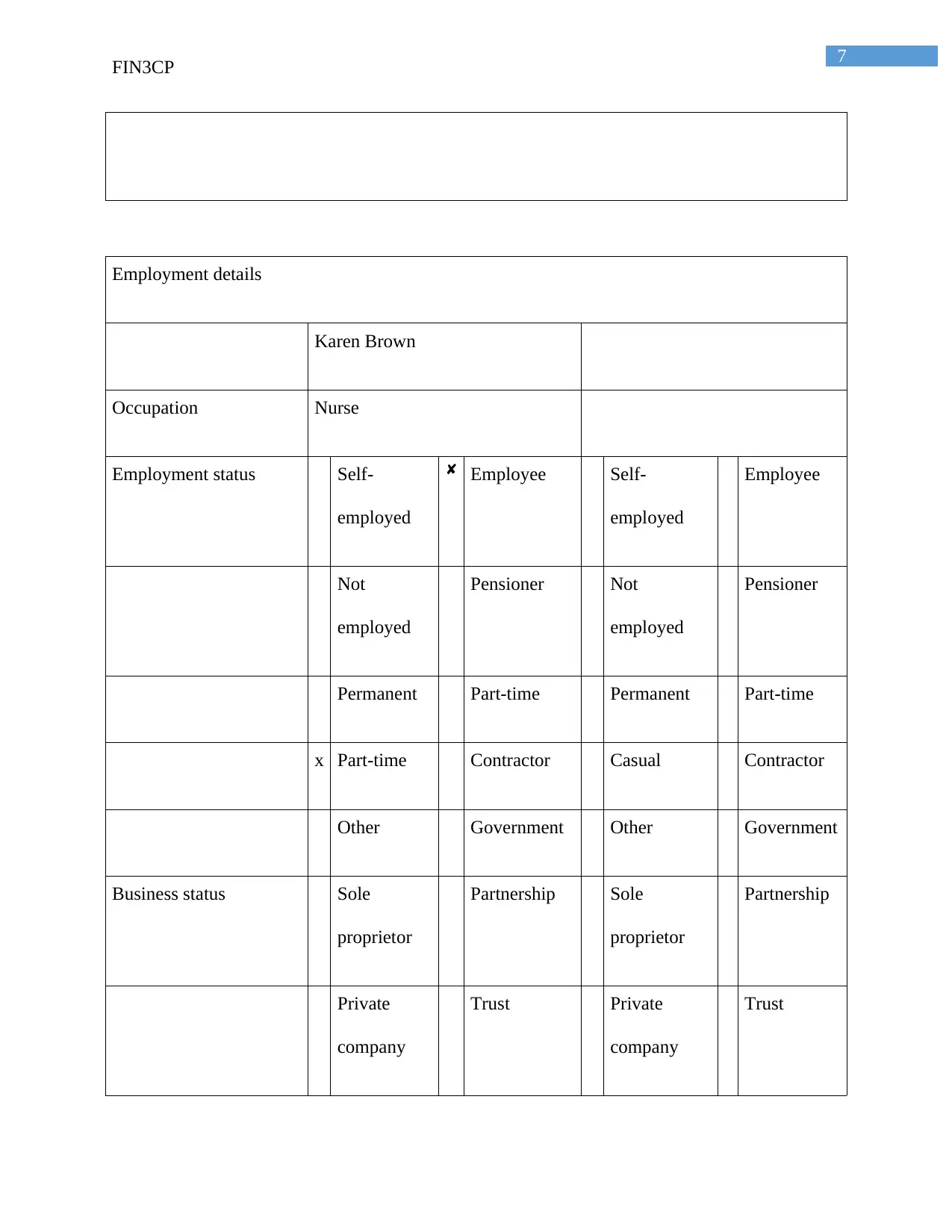

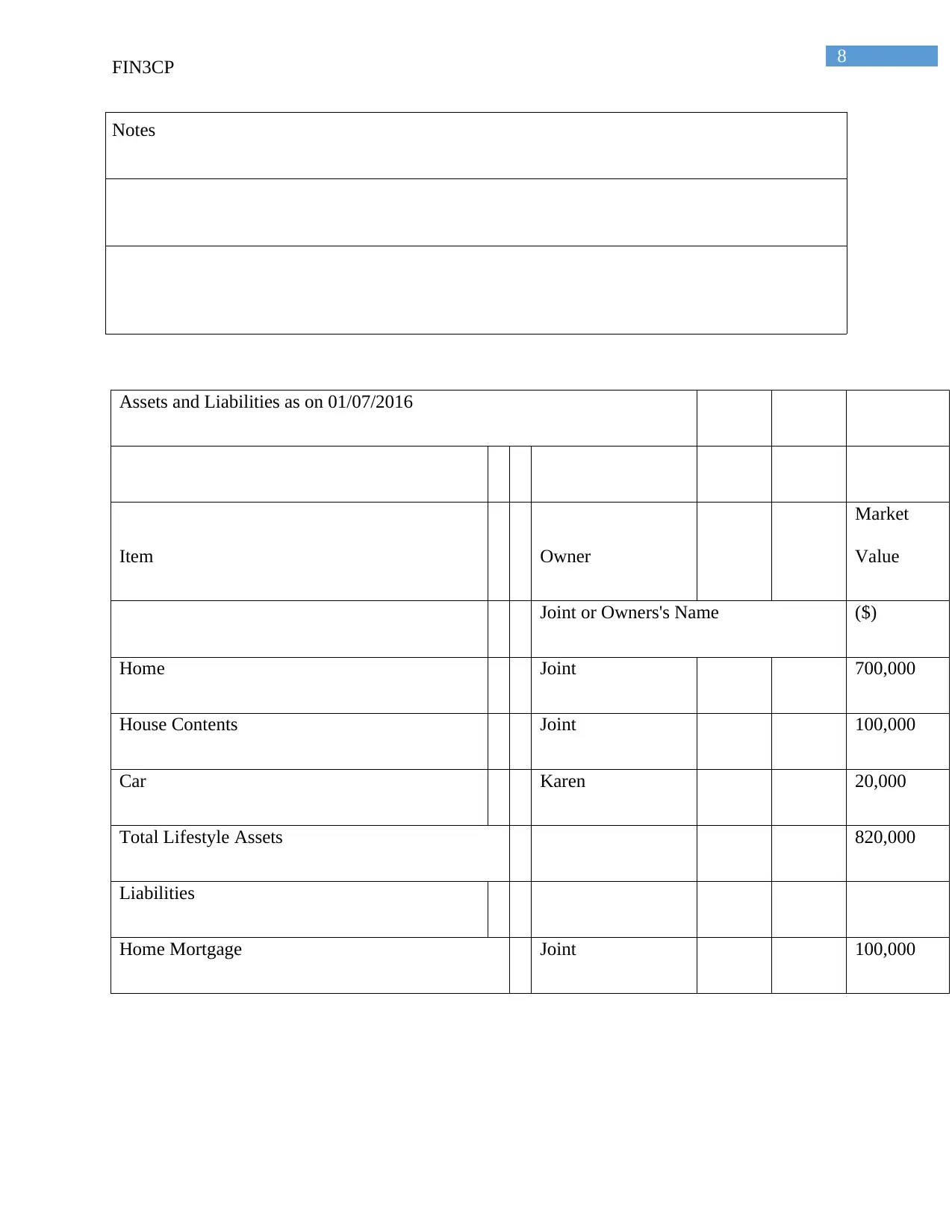

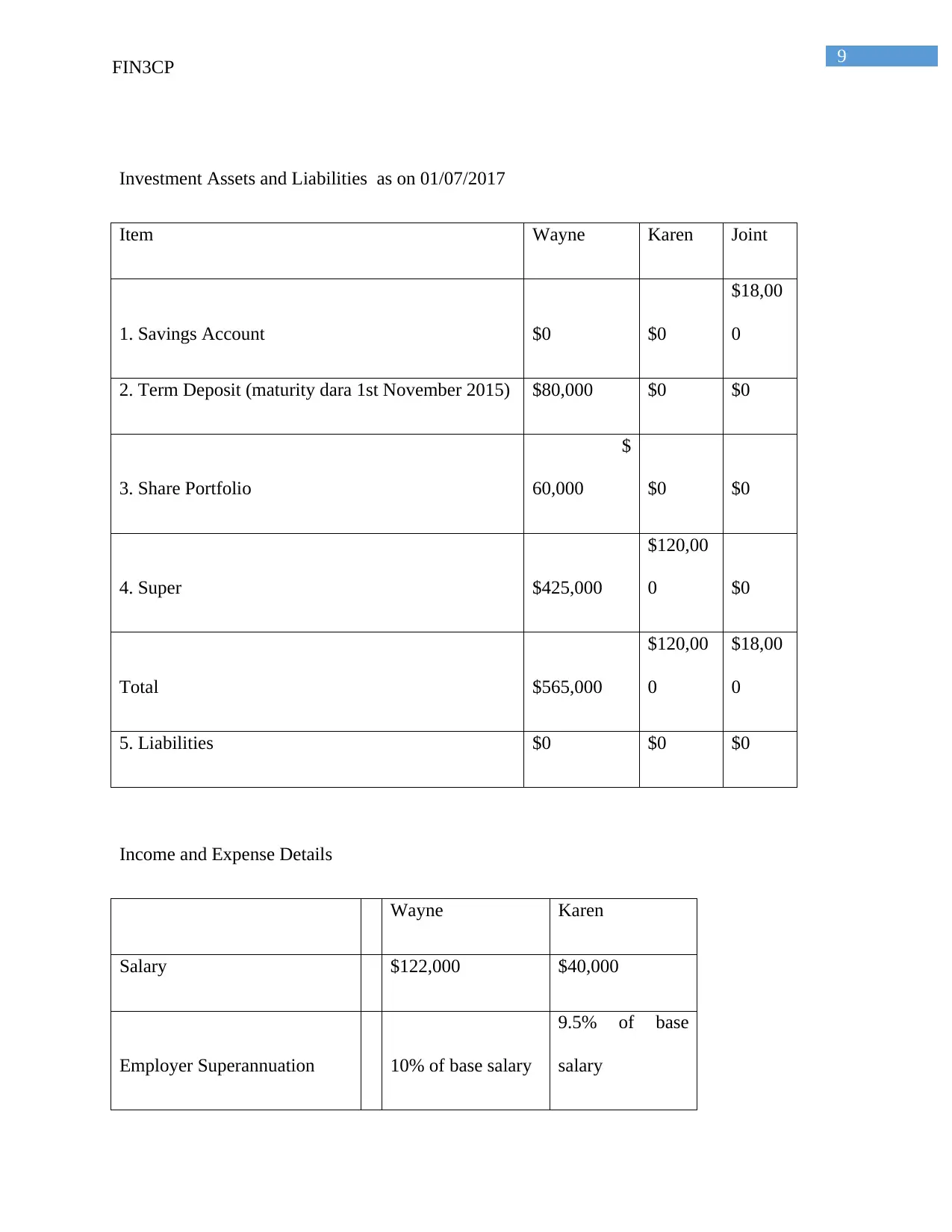

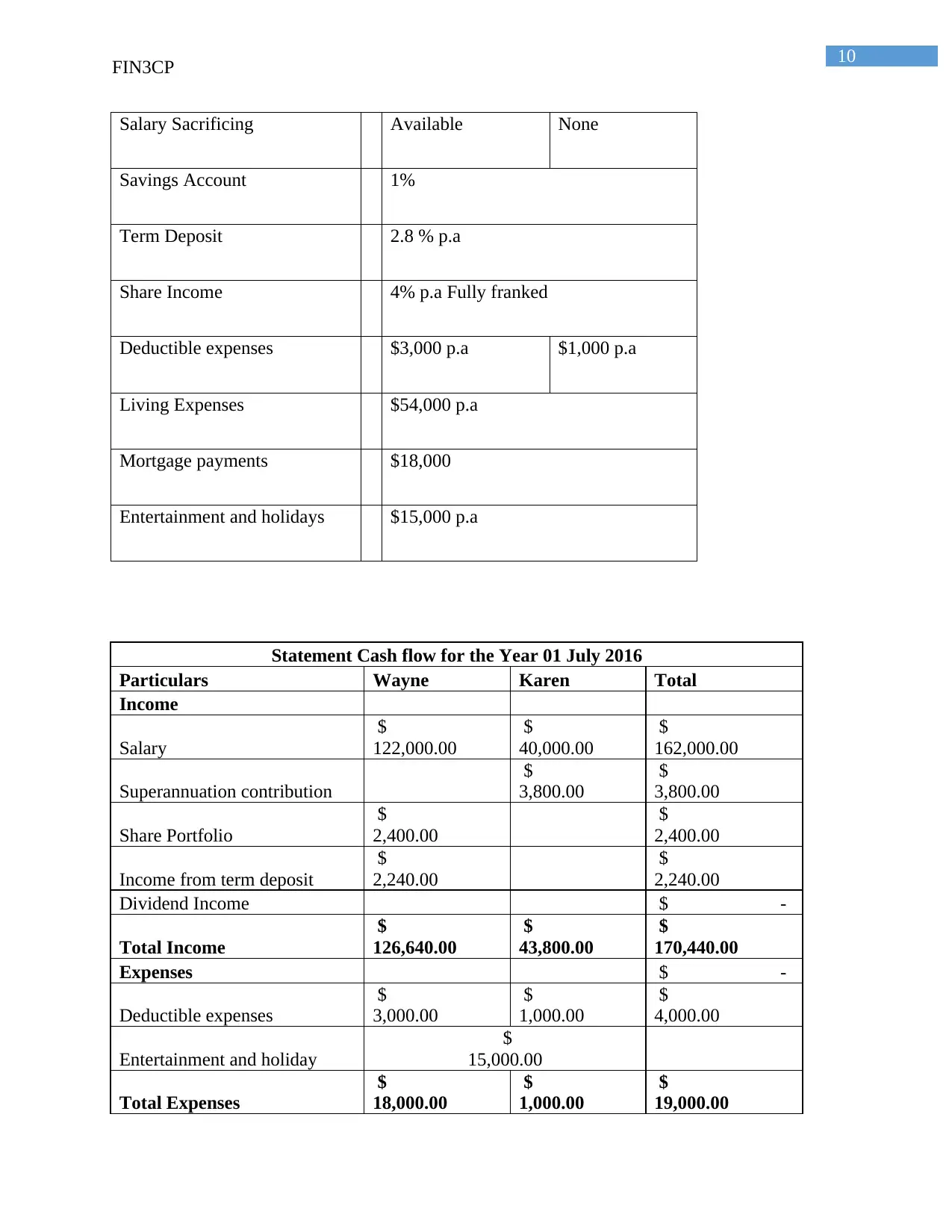

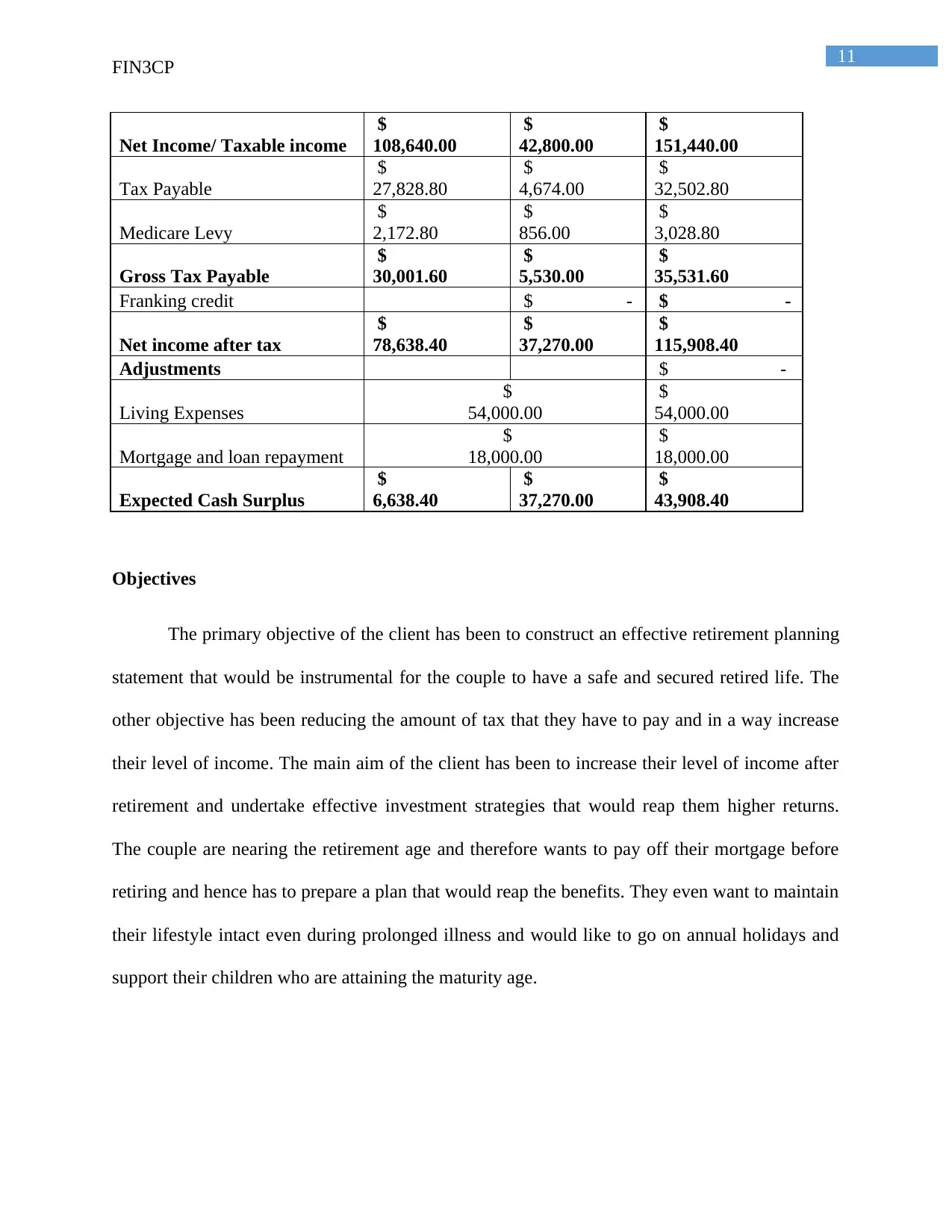

This comprehensive financial report, prepared for the FIN3CP course, analyzes the retirement planning needs of clients Wayne and Karen Brown. It begins with an executive summary, covering personal and financial details, including income, expenses, assets, and liabilities. The report outlines the clients' objectives, which include securing a comfortable retirement, reducing tax liabilities, and generating income through effective investment strategies. It evaluates the clients' risk profile and investment allocation strategies. The analysis includes future projections, strategies for retirement planning, and an amended cash flow statement. Investment suggestions and recommendations are provided, along with details on associated charges and disclaimers. The report focuses on salary sacrifice and investment strategies to optimize retirement income and minimize tax implications. The report also includes sections on risk assessment, investment allocation, and future projections to help clients make informed financial decisions. The objective of the client is to have a safe and secured retired life, reduce the amount of tax that they have to pay and increase their level of income, and undertake effective investment strategies that would reap higher returns.

1 out of 26

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.