Business Finance Case Study: Costing, Budgeting, and Variance

VerifiedAdded on 2023/01/12

|10

|2148

|33

Case Study

AI Summary

This case study analyzes a business's financial performance, beginning with the calculation of the break-even point (BEP) and margin of safety to assess profitability. It then compares income statements using both marginal and absorption costing methods, highlighting the impact of different costing techniques on profit calculation. The study further examines various cost types (fixed and variable) and their relevance to pricing decisions. It includes the calculation of material, labor, and fixed overhead variances to evaluate cost control effectiveness. Finally, the case study presents the preparation of a budget to control operations, including sales forecasting and inventory management, providing a comprehensive overview of financial management principles and their practical application within a business context. This case study is a valuable resource for students studying business finance, offering insights into key concepts and practical applications.

CASE STUDY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of break- even point and margin of safety...............................................................3

Income using absorption and marginal costing...........................................................................4

PART B............................................................................................................................................6

Understanding of different types of cost and there relevance in pricing decision......................6

Calculation of all variance..........................................................................................................7

Preparation of budget to control operation..................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Calculation of break- even point and margin of safety...............................................................3

Income using absorption and marginal costing...........................................................................4

PART B............................................................................................................................................6

Understanding of different types of cost and there relevance in pricing decision......................6

Calculation of all variance..........................................................................................................7

Preparation of budget to control operation..................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Managing the finance is the most important thing for the company and its success. This is

majorly because of the fact that if the money will be manages and allocated in proper manner

then this will increase the profitability of the company to a great extent (Klopotan, Zoroja and

Meško, 2018). Hence, the present report will start by calculating the BEP in order to know the

profitability of the company. Further, the income on basis of both marginal and absorption

costing will be calculated. Also in next part the different types of cost and their relevance over

the pricing decision will be highlighted. Further the different types of variance will be calculated

and after that budget for operational control will be made.

PART A

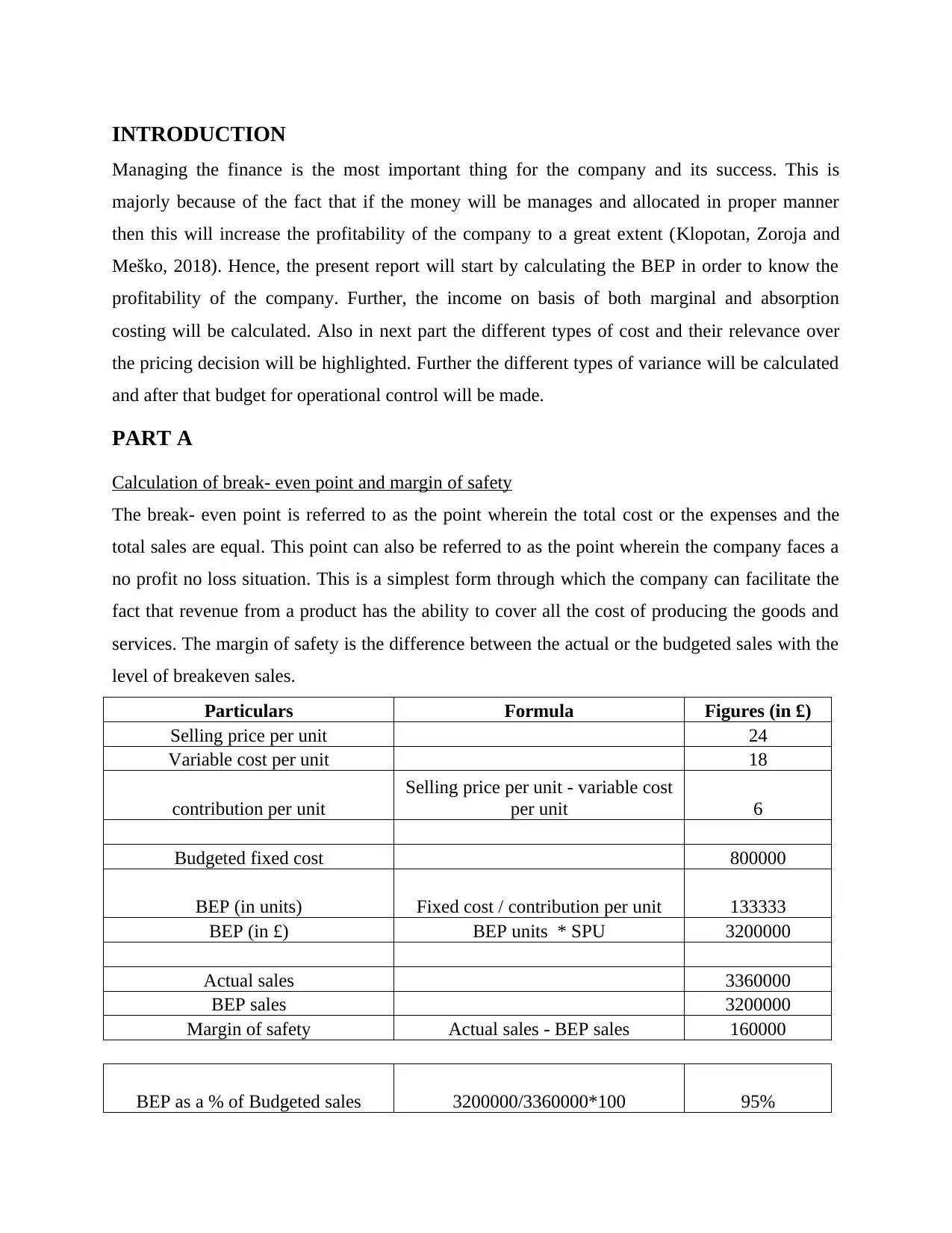

Calculation of break- even point and margin of safety

The break- even point is referred to as the point wherein the total cost or the expenses and the

total sales are equal. This point can also be referred to as the point wherein the company faces a

no profit no loss situation. This is a simplest form through which the company can facilitate the

fact that revenue from a product has the ability to cover all the cost of producing the goods and

services. The margin of safety is the difference between the actual or the budgeted sales with the

level of breakeven sales.

Particulars Formula Figures (in £)

Selling price per unit 24

Variable cost per unit 18

contribution per unit

Selling price per unit - variable cost

per unit 6

Budgeted fixed cost 800000

BEP (in units) Fixed cost / contribution per unit 133333

BEP (in £) BEP units * SPU 3200000

Actual sales 3360000

BEP sales 3200000

Margin of safety Actual sales - BEP sales 160000

BEP as a % of Budgeted sales 3200000/3360000*100 95%

Managing the finance is the most important thing for the company and its success. This is

majorly because of the fact that if the money will be manages and allocated in proper manner

then this will increase the profitability of the company to a great extent (Klopotan, Zoroja and

Meško, 2018). Hence, the present report will start by calculating the BEP in order to know the

profitability of the company. Further, the income on basis of both marginal and absorption

costing will be calculated. Also in next part the different types of cost and their relevance over

the pricing decision will be highlighted. Further the different types of variance will be calculated

and after that budget for operational control will be made.

PART A

Calculation of break- even point and margin of safety

The break- even point is referred to as the point wherein the total cost or the expenses and the

total sales are equal. This point can also be referred to as the point wherein the company faces a

no profit no loss situation. This is a simplest form through which the company can facilitate the

fact that revenue from a product has the ability to cover all the cost of producing the goods and

services. The margin of safety is the difference between the actual or the budgeted sales with the

level of breakeven sales.

Particulars Formula Figures (in £)

Selling price per unit 24

Variable cost per unit 18

contribution per unit

Selling price per unit - variable cost

per unit 6

Budgeted fixed cost 800000

BEP (in units) Fixed cost / contribution per unit 133333

BEP (in £) BEP units * SPU 3200000

Actual sales 3360000

BEP sales 3200000

Margin of safety Actual sales - BEP sales 160000

BEP as a % of Budgeted sales 3200000/3360000*100 95%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

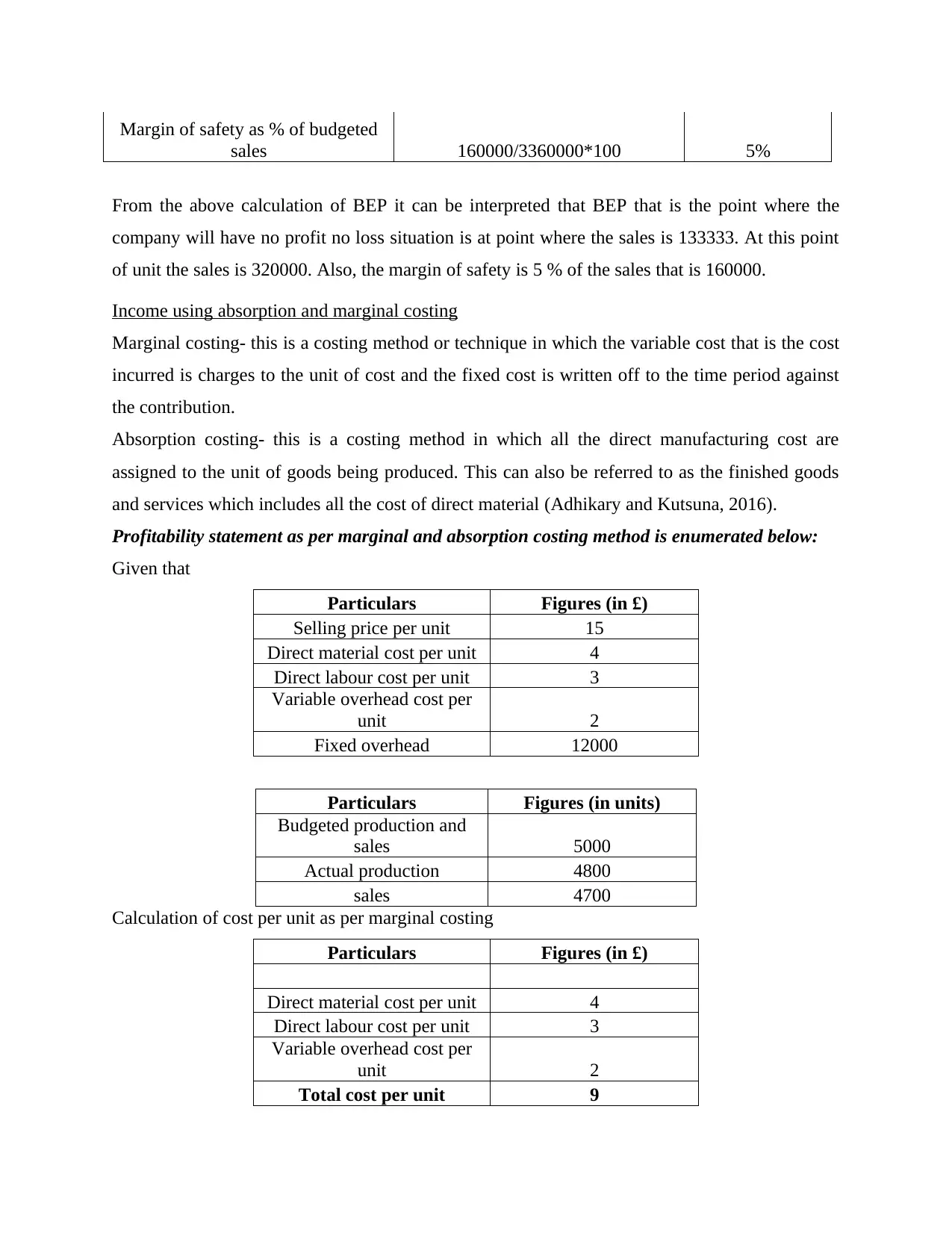

Margin of safety as % of budgeted

sales 160000/3360000*100 5%

From the above calculation of BEP it can be interpreted that BEP that is the point where the

company will have no profit no loss situation is at point where the sales is 133333. At this point

of unit the sales is 320000. Also, the margin of safety is 5 % of the sales that is 160000.

Income using absorption and marginal costing

Marginal costing- this is a costing method or technique in which the variable cost that is the cost

incurred is charges to the unit of cost and the fixed cost is written off to the time period against

the contribution.

Absorption costing- this is a costing method in which all the direct manufacturing cost are

assigned to the unit of goods being produced. This can also be referred to as the finished goods

and services which includes all the cost of direct material (Adhikary and Kutsuna, 2016).

Profitability statement as per marginal and absorption costing method is enumerated below:

Given that

Particulars Figures (in £)

Selling price per unit 15

Direct material cost per unit 4

Direct labour cost per unit 3

Variable overhead cost per

unit 2

Fixed overhead 12000

Particulars Figures (in units)

Budgeted production and

sales 5000

Actual production 4800

sales 4700

Calculation of cost per unit as per marginal costing

Particulars Figures (in £)

Direct material cost per unit 4

Direct labour cost per unit 3

Variable overhead cost per

unit 2

Total cost per unit 9

sales 160000/3360000*100 5%

From the above calculation of BEP it can be interpreted that BEP that is the point where the

company will have no profit no loss situation is at point where the sales is 133333. At this point

of unit the sales is 320000. Also, the margin of safety is 5 % of the sales that is 160000.

Income using absorption and marginal costing

Marginal costing- this is a costing method or technique in which the variable cost that is the cost

incurred is charges to the unit of cost and the fixed cost is written off to the time period against

the contribution.

Absorption costing- this is a costing method in which all the direct manufacturing cost are

assigned to the unit of goods being produced. This can also be referred to as the finished goods

and services which includes all the cost of direct material (Adhikary and Kutsuna, 2016).

Profitability statement as per marginal and absorption costing method is enumerated below:

Given that

Particulars Figures (in £)

Selling price per unit 15

Direct material cost per unit 4

Direct labour cost per unit 3

Variable overhead cost per

unit 2

Fixed overhead 12000

Particulars Figures (in units)

Budgeted production and

sales 5000

Actual production 4800

sales 4700

Calculation of cost per unit as per marginal costing

Particulars Figures (in £)

Direct material cost per unit 4

Direct labour cost per unit 3

Variable overhead cost per

unit 2

Total cost per unit 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

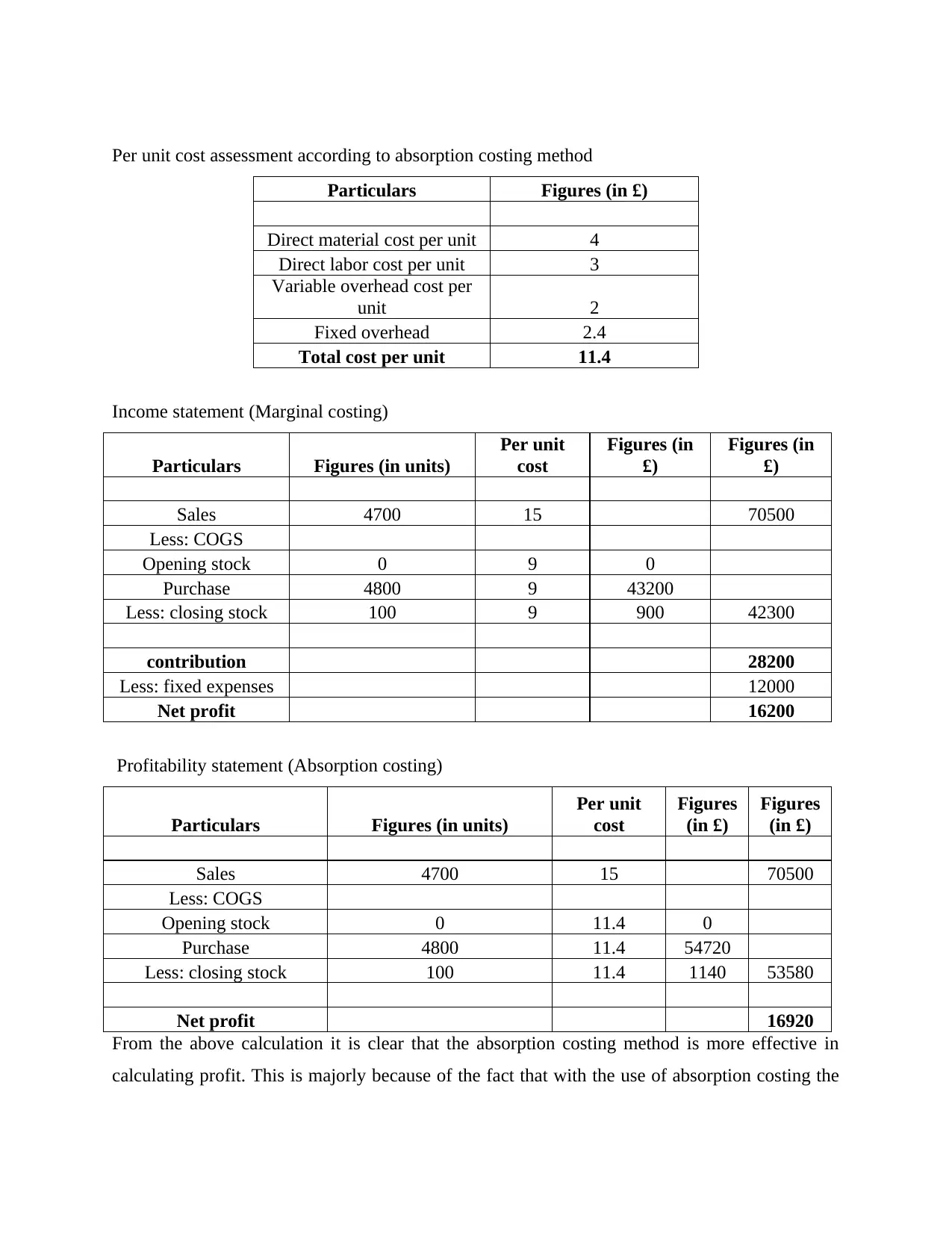

Per unit cost assessment according to absorption costing method

Particulars Figures (in £)

Direct material cost per unit 4

Direct labor cost per unit 3

Variable overhead cost per

unit 2

Fixed overhead 2.4

Total cost per unit 11.4

Income statement (Marginal costing)

Particulars Figures (in units)

Per unit

cost

Figures (in

£)

Figures (in

£)

Sales 4700 15 70500

Less: COGS

Opening stock 0 9 0

Purchase 4800 9 43200

Less: closing stock 100 9 900 42300

contribution 28200

Less: fixed expenses 12000

Net profit 16200

Profitability statement (Absorption costing)

Particulars Figures (in units)

Per unit

cost

Figures

(in £)

Figures

(in £)

Sales 4700 15 70500

Less: COGS

Opening stock 0 11.4 0

Purchase 4800 11.4 54720

Less: closing stock 100 11.4 1140 53580

Net profit 16920

From the above calculation it is clear that the absorption costing method is more effective in

calculating profit. This is majorly because of the fact that with the use of absorption costing the

Particulars Figures (in £)

Direct material cost per unit 4

Direct labor cost per unit 3

Variable overhead cost per

unit 2

Fixed overhead 2.4

Total cost per unit 11.4

Income statement (Marginal costing)

Particulars Figures (in units)

Per unit

cost

Figures (in

£)

Figures (in

£)

Sales 4700 15 70500

Less: COGS

Opening stock 0 9 0

Purchase 4800 9 43200

Less: closing stock 100 9 900 42300

contribution 28200

Less: fixed expenses 12000

Net profit 16200

Profitability statement (Absorption costing)

Particulars Figures (in units)

Per unit

cost

Figures

(in £)

Figures

(in £)

Sales 4700 15 70500

Less: COGS

Opening stock 0 11.4 0

Purchase 4800 11.4 54720

Less: closing stock 100 11.4 1140 53580

Net profit 16920

From the above calculation it is clear that the absorption costing method is more effective in

calculating profit. This is majorly because of the fact that with the use of absorption costing the

profit of the company was 16920 which is only 16200 in case of marginal costing. Thus, the use

of absorption costing is more profitable for the operations and calculation of cost and profit.

PART B

Understanding of different types of cost and there relevance in pricing decision

The cost the value of money which is being uncured by the company at time of executing of the

activities of the business. Without incurring cost no business or any other activity can be run as

without money no business can operate or perform any other activity. There are many different

types of cost which can be used and incurred by the company when they operate in the business

environment. The various type of cost being used by the Sydney Company are as follows-

Fixed cost- this is a type of cost which remains fixed even if there is no production of any

business activity being undertaken. The fixed cost remain same at every level of production

whether be it low, medium or large scale production. This type of cost is very relevant to be

analysed at time of pricing decision because this cost is charged in the price expected from the

consumers. So the fixed cost is always added in the price which is charged to the consumers.

This is majorly charged because of the reason that the fixed cost is always there and even if the

production is not there then also this cost is charged to the consumer price.

Variable cost- this is the cost which is dependant over the level of production. If the production

is low then the cost will also be low and if the production will be high then the cost of production

will also be high. This cost has not much impact on the pricing decision because of the fact that

if the production will be there then only the cost will be incurred. Hence, this type of cost does

not have much impact over the prices of consumer as if the production will take place then this

cost will be added in the price and otherwise not.

Role of budget

The budget is referred to as the estimation of the income and expenses of the company in order

to manage the working of the company in effective manner. The role of budget is to provide the

guidance to the employees that how they have to manage the work in proper and effective

manner. Also, another major role of budget in working of company is that this help the

employees in estimating the fact that how much money they have to allocate in the business

activities and they have to manage the work in that particular amount of money only.

Calculation of all variance

of absorption costing is more profitable for the operations and calculation of cost and profit.

PART B

Understanding of different types of cost and there relevance in pricing decision

The cost the value of money which is being uncured by the company at time of executing of the

activities of the business. Without incurring cost no business or any other activity can be run as

without money no business can operate or perform any other activity. There are many different

types of cost which can be used and incurred by the company when they operate in the business

environment. The various type of cost being used by the Sydney Company are as follows-

Fixed cost- this is a type of cost which remains fixed even if there is no production of any

business activity being undertaken. The fixed cost remain same at every level of production

whether be it low, medium or large scale production. This type of cost is very relevant to be

analysed at time of pricing decision because this cost is charged in the price expected from the

consumers. So the fixed cost is always added in the price which is charged to the consumers.

This is majorly charged because of the reason that the fixed cost is always there and even if the

production is not there then also this cost is charged to the consumer price.

Variable cost- this is the cost which is dependant over the level of production. If the production

is low then the cost will also be low and if the production will be high then the cost of production

will also be high. This cost has not much impact on the pricing decision because of the fact that

if the production will be there then only the cost will be incurred. Hence, this type of cost does

not have much impact over the prices of consumer as if the production will take place then this

cost will be added in the price and otherwise not.

Role of budget

The budget is referred to as the estimation of the income and expenses of the company in order

to manage the working of the company in effective manner. The role of budget is to provide the

guidance to the employees that how they have to manage the work in proper and effective

manner. Also, another major role of budget in working of company is that this help the

employees in estimating the fact that how much money they have to allocate in the business

activities and they have to manage the work in that particular amount of money only.

Calculation of all variance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

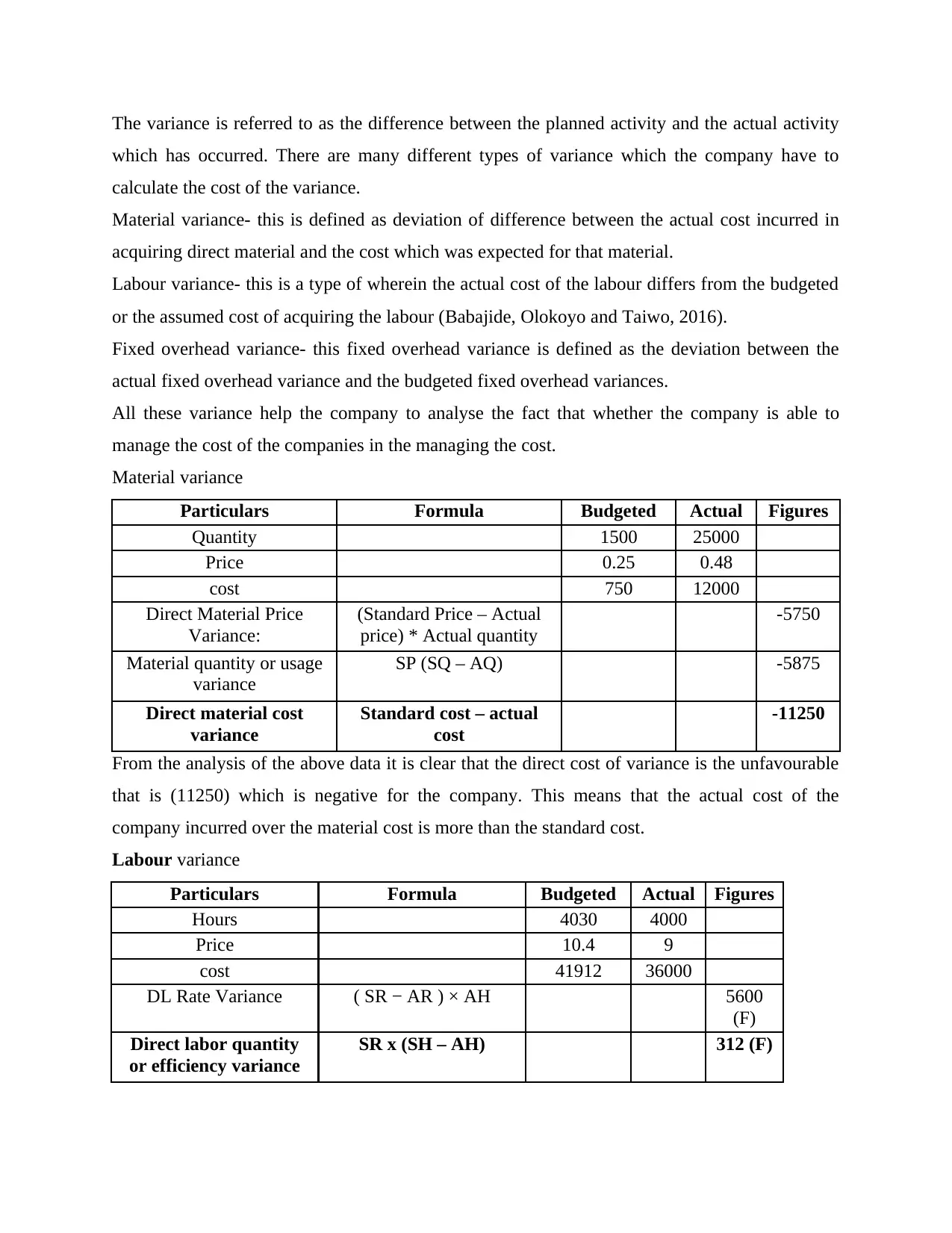

The variance is referred to as the difference between the planned activity and the actual activity

which has occurred. There are many different types of variance which the company have to

calculate the cost of the variance.

Material variance- this is defined as deviation of difference between the actual cost incurred in

acquiring direct material and the cost which was expected for that material.

Labour variance- this is a type of wherein the actual cost of the labour differs from the budgeted

or the assumed cost of acquiring the labour (Babajide, Olokoyo and Taiwo, 2016).

Fixed overhead variance- this fixed overhead variance is defined as the deviation between the

actual fixed overhead variance and the budgeted fixed overhead variances.

All these variance help the company to analyse the fact that whether the company is able to

manage the cost of the companies in the managing the cost.

Material variance

Particulars Formula Budgeted Actual Figures

Quantity 1500 25000

Price 0.25 0.48

cost 750 12000

Direct Material Price

Variance:

(Standard Price – Actual

price) * Actual quantity

-5750

Material quantity or usage

variance

SP (SQ – AQ) -5875

Direct material cost

variance

Standard cost – actual

cost

-11250

From the analysis of the above data it is clear that the direct cost of variance is the unfavourable

that is (11250) which is negative for the company. This means that the actual cost of the

company incurred over the material cost is more than the standard cost.

Labour variance

Particulars Formula Budgeted Actual Figures

Hours 4030 4000

Price 10.4 9

cost 41912 36000

DL Rate Variance ( SR − AR ) × AH 5600

(F)

Direct labor quantity

or efficiency variance

SR x (SH – AH) 312 (F)

which has occurred. There are many different types of variance which the company have to

calculate the cost of the variance.

Material variance- this is defined as deviation of difference between the actual cost incurred in

acquiring direct material and the cost which was expected for that material.

Labour variance- this is a type of wherein the actual cost of the labour differs from the budgeted

or the assumed cost of acquiring the labour (Babajide, Olokoyo and Taiwo, 2016).

Fixed overhead variance- this fixed overhead variance is defined as the deviation between the

actual fixed overhead variance and the budgeted fixed overhead variances.

All these variance help the company to analyse the fact that whether the company is able to

manage the cost of the companies in the managing the cost.

Material variance

Particulars Formula Budgeted Actual Figures

Quantity 1500 25000

Price 0.25 0.48

cost 750 12000

Direct Material Price

Variance:

(Standard Price – Actual

price) * Actual quantity

-5750

Material quantity or usage

variance

SP (SQ – AQ) -5875

Direct material cost

variance

Standard cost – actual

cost

-11250

From the analysis of the above data it is clear that the direct cost of variance is the unfavourable

that is (11250) which is negative for the company. This means that the actual cost of the

company incurred over the material cost is more than the standard cost.

Labour variance

Particulars Formula Budgeted Actual Figures

Hours 4030 4000

Price 10.4 9

cost 41912 36000

DL Rate Variance ( SR − AR ) × AH 5600

(F)

Direct labor quantity

or efficiency variance

SR x (SH – AH) 312 (F)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

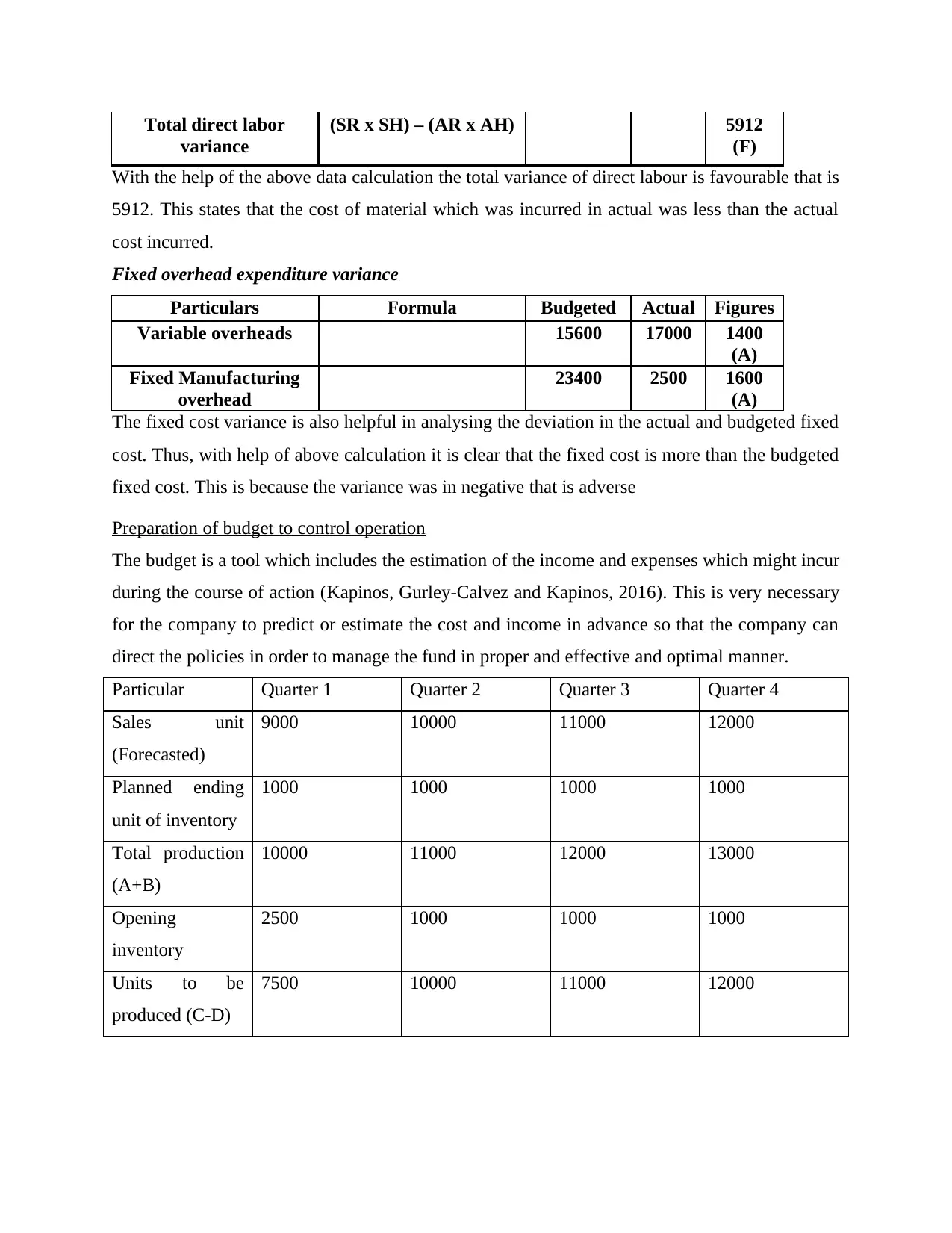

Total direct labor

variance

(SR x SH) – (AR x AH) 5912

(F)

With the help of the above data calculation the total variance of direct labour is favourable that is

5912. This states that the cost of material which was incurred in actual was less than the actual

cost incurred.

Fixed overhead expenditure variance

Particulars Formula Budgeted Actual Figures

Variable overheads 15600 17000 1400

(A)

Fixed Manufacturing

overhead

23400 2500 1600

(A)

The fixed cost variance is also helpful in analysing the deviation in the actual and budgeted fixed

cost. Thus, with help of above calculation it is clear that the fixed cost is more than the budgeted

fixed cost. This is because the variance was in negative that is adverse

Preparation of budget to control operation

The budget is a tool which includes the estimation of the income and expenses which might incur

during the course of action (Kapinos, Gurley-Calvez and Kapinos, 2016). This is very necessary

for the company to predict or estimate the cost and income in advance so that the company can

direct the policies in order to manage the fund in proper and effective and optimal manner.

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales unit

(Forecasted)

9000 10000 11000 12000

Planned ending

unit of inventory

1000 1000 1000 1000

Total production

(A+B)

10000 11000 12000 13000

Opening

inventory

2500 1000 1000 1000

Units to be

produced (C-D)

7500 10000 11000 12000

variance

(SR x SH) – (AR x AH) 5912

(F)

With the help of the above data calculation the total variance of direct labour is favourable that is

5912. This states that the cost of material which was incurred in actual was less than the actual

cost incurred.

Fixed overhead expenditure variance

Particulars Formula Budgeted Actual Figures

Variable overheads 15600 17000 1400

(A)

Fixed Manufacturing

overhead

23400 2500 1600

(A)

The fixed cost variance is also helpful in analysing the deviation in the actual and budgeted fixed

cost. Thus, with help of above calculation it is clear that the fixed cost is more than the budgeted

fixed cost. This is because the variance was in negative that is adverse

Preparation of budget to control operation

The budget is a tool which includes the estimation of the income and expenses which might incur

during the course of action (Kapinos, Gurley-Calvez and Kapinos, 2016). This is very necessary

for the company to predict or estimate the cost and income in advance so that the company can

direct the policies in order to manage the fund in proper and effective and optimal manner.

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales unit

(Forecasted)

9000 10000 11000 12000

Planned ending

unit of inventory

1000 1000 1000 1000

Total production

(A+B)

10000 11000 12000 13000

Opening

inventory

2500 1000 1000 1000

Units to be

produced (C-D)

7500 10000 11000 12000

CONCLUSION

In the end it is concluded that finance and its proper allocation in the business is very

necessary for increasing the profitability of the company. With this it is clear that managing the

money within the company is very necessary for the company to manage all the calculation in

proper manner as this help the company in assessing that whether the company is doing well or

not.

In the end it is concluded that finance and its proper allocation in the business is very

necessary for increasing the profitability of the company. With this it is clear that managing the

money within the company is very necessary for the company to manage all the calculation in

proper manner as this help the company in assessing that whether the company is doing well or

not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research. 4. pp.1-21.

Babajide, A.A., Olokoyo, F.O. and Taiwo, J.N., 2016. Evaluation of effects of banking

consolidation on small business finance in Nigeria. In Proceedings of the 23rd

International Business Information Management Association Conference (pp. 12522-

12540).

Kapinos, P., Gurley-Calvez, T. and Kapinos, K., 2016. (Un) expected housing price changes:

Identifying the drivers of small business finance. Journal of Economics and

Business. 84. pp.79-94.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management. 10. p.1847979018797013.

Books and Journals

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research. 4. pp.1-21.

Babajide, A.A., Olokoyo, F.O. and Taiwo, J.N., 2016. Evaluation of effects of banking

consolidation on small business finance in Nigeria. In Proceedings of the 23rd

International Business Information Management Association Conference (pp. 12522-

12540).

Kapinos, P., Gurley-Calvez, T. and Kapinos, K., 2016. (Un) expected housing price changes:

Identifying the drivers of small business finance. Journal of Economics and

Business. 84. pp.79-94.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management. 10. p.1847979018797013.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.