Accounting for R&D Projects: A Case Study of Technology Enterprise

VerifiedAdded on 2020/12/24

|10

|2785

|367

Case Study

AI Summary

This case study analyzes the accounting treatment of a research and development (R&D) project undertaken by Technology Enterprise Ltd, focusing on the application of IAS 38 (Intangible Assets). The report examines how the project's costs should be accounted for, distinguishing between research and development phases, and detailing the criteria for recognizing intangible assets. It explores how the rules and restrictions within AASB 138/IAS 38 might reduce the comparability of financial statements across different companies and countries. Furthermore, the study provides recommendations to the CEO of Technology Enterprise, addressing concerns about investor interpretations of financial information and the efficient market hypothesis, suggesting how the company can mitigate potential negative impacts on investor perception. The report concludes by emphasizing the importance of adhering to accounting standards to ensure transparency and comparability in financial reporting, thereby maintaining investor trust and confidence.

Case study report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Recording, interpreting, reporting and disclosing of the financial information is the

process of financial accounting.IAS 38 provides for the recognition, measurement and disclosure

of the tangible assets which are not governed or which are not dealt with any other standard.

R&D project of Technology Enterprise is recognisable as it meets the above mentioned criteria.

The project will provide the economic benefit for 10 years. If the intangible asset has been

generated internally after meeting all the recognition conditions, is measured at the cost which is

ascertained by adding all the expenditure incurred from the date when intangible asset first met

the recognition criteria.*If either of the conditions would not have been fulfilled by the

intangible asset, all the costs of the R&D asset will be treated as expenditure as if they were

incurred for the motive of research only. IFRS adoption by many countries has resulted in the

amendment in the ways regarding how companies account for and report financial information in

their financial statements. If any intangible does not meet these criteria, then such assets will not

be considered as the intangible asset and the cost of acquiring or developing such asset will be

treated as expenses and will not be capitalisedAASB 13B/IAS 38 are the accounting standards

provides guidelines about the recognition and measurement and disclosure of various intangible

assets held by a business organisation. Further, with the help of adopting AASB 13B/IAS 38,

Technology Enterprise can determine the most appropriate amount of generation of intangible

assets to be capitalised or to be shown as expenses in such a way so that it shall not result in

misguiding the investors for the purpose of deciding the certain amount to be invested in the

company. In this regard, company's reputation in the market may go downwards.

Recording, interpreting, reporting and disclosing of the financial information is the

process of financial accounting.IAS 38 provides for the recognition, measurement and disclosure

of the tangible assets which are not governed or which are not dealt with any other standard.

R&D project of Technology Enterprise is recognisable as it meets the above mentioned criteria.

The project will provide the economic benefit for 10 years. If the intangible asset has been

generated internally after meeting all the recognition conditions, is measured at the cost which is

ascertained by adding all the expenditure incurred from the date when intangible asset first met

the recognition criteria.*If either of the conditions would not have been fulfilled by the

intangible asset, all the costs of the R&D asset will be treated as expenditure as if they were

incurred for the motive of research only. IFRS adoption by many countries has resulted in the

amendment in the ways regarding how companies account for and report financial information in

their financial statements. If any intangible does not meet these criteria, then such assets will not

be considered as the intangible asset and the cost of acquiring or developing such asset will be

treated as expenses and will not be capitalisedAASB 13B/IAS 38 are the accounting standards

provides guidelines about the recognition and measurement and disclosure of various intangible

assets held by a business organisation. Further, with the help of adopting AASB 13B/IAS 38,

Technology Enterprise can determine the most appropriate amount of generation of intangible

assets to be capitalised or to be shown as expenses in such a way so that it shall not result in

misguiding the investors for the purpose of deciding the certain amount to be invested in the

company. In this regard, company's reputation in the market may go downwards.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. How the R&D project should be accounted for in the financial statements............................1

2. To what extent might the rules or restrictions in AASB 138/ IAS 38 reduce the

comparability of financial statements..........................................................................................3

3. Providing response to CEO over the understanding about AASB 13B/IAS 38 and the

efficient market hypothesis along with recommendations for company to mitigate their

concern about investor's interpretation........................................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. How the R&D project should be accounted for in the financial statements............................1

2. To what extent might the rules or restrictions in AASB 138/ IAS 38 reduce the

comparability of financial statements..........................................................................................3

3. Providing response to CEO over the understanding about AASB 13B/IAS 38 and the

efficient market hypothesis along with recommendations for company to mitigate their

concern about investor's interpretation........................................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Recording, interpreting, reporting and disclosing of the financial information is the

process of financial accounting. The accounting of the financial transactions has to be done in

such a way as prescribed the accounting standards so as to facilitate the comparability. The

present project report is concerned with Technology Enterprise Ltd, which is listed company

undertaking a project of research and development for amending the method of recharging

batteries in its products. The report will highlight how the project should be accounted in the

financial statements in accordance with AASB 13B/IAS 38. Further, it will be shown that to

what limit does the rules of AASB 13B/IAS 38 reduce the comparability of financial statements

and lastly, recommendations on how the organisation can mitigate their concerns regarding

investor's interpretation of information provided in financial statements.

MAIN BODY

1. How the R&D project should be accounted for in the financial statements

IAS 38 provides for the recognition, measurement and disclosure of the tangible assets

which are not governed or which are not dealt with any other standard.

Recognition of item to be termed as intangible asset whioch is generated internally must

meet the following criteria:

identifiable

control over the item by the company

existence of economic benefits that will arise in the future

its ability to use or sell the intangible asset (De Villiers and Sharma, 2017)

the ability of measuring reliably the expenditure which is attributable to use or sell the

asset

the availability of all types of resources for completing the development and for using

and selling the intangible asset.

R&D project of Technology Enterprise is recognisable as it meets the above mentioned

criteria. The project will provide the economic benefit for 10 years. It is identifiable as it has

been applied for patent design and the firm has control over this resource.

IAS 38 has specifically restricted or prohibited the some internally generated intangible

assets from being recognised. These are :

goodwill

1

Recording, interpreting, reporting and disclosing of the financial information is the

process of financial accounting. The accounting of the financial transactions has to be done in

such a way as prescribed the accounting standards so as to facilitate the comparability. The

present project report is concerned with Technology Enterprise Ltd, which is listed company

undertaking a project of research and development for amending the method of recharging

batteries in its products. The report will highlight how the project should be accounted in the

financial statements in accordance with AASB 13B/IAS 38. Further, it will be shown that to

what limit does the rules of AASB 13B/IAS 38 reduce the comparability of financial statements

and lastly, recommendations on how the organisation can mitigate their concerns regarding

investor's interpretation of information provided in financial statements.

MAIN BODY

1. How the R&D project should be accounted for in the financial statements

IAS 38 provides for the recognition, measurement and disclosure of the tangible assets

which are not governed or which are not dealt with any other standard.

Recognition of item to be termed as intangible asset whioch is generated internally must

meet the following criteria:

identifiable

control over the item by the company

existence of economic benefits that will arise in the future

its ability to use or sell the intangible asset (De Villiers and Sharma, 2017)

the ability of measuring reliably the expenditure which is attributable to use or sell the

asset

the availability of all types of resources for completing the development and for using

and selling the intangible asset.

R&D project of Technology Enterprise is recognisable as it meets the above mentioned

criteria. The project will provide the economic benefit for 10 years. It is identifiable as it has

been applied for patent design and the firm has control over this resource.

IAS 38 has specifically restricted or prohibited the some internally generated intangible

assets from being recognised. These are :

goodwill

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

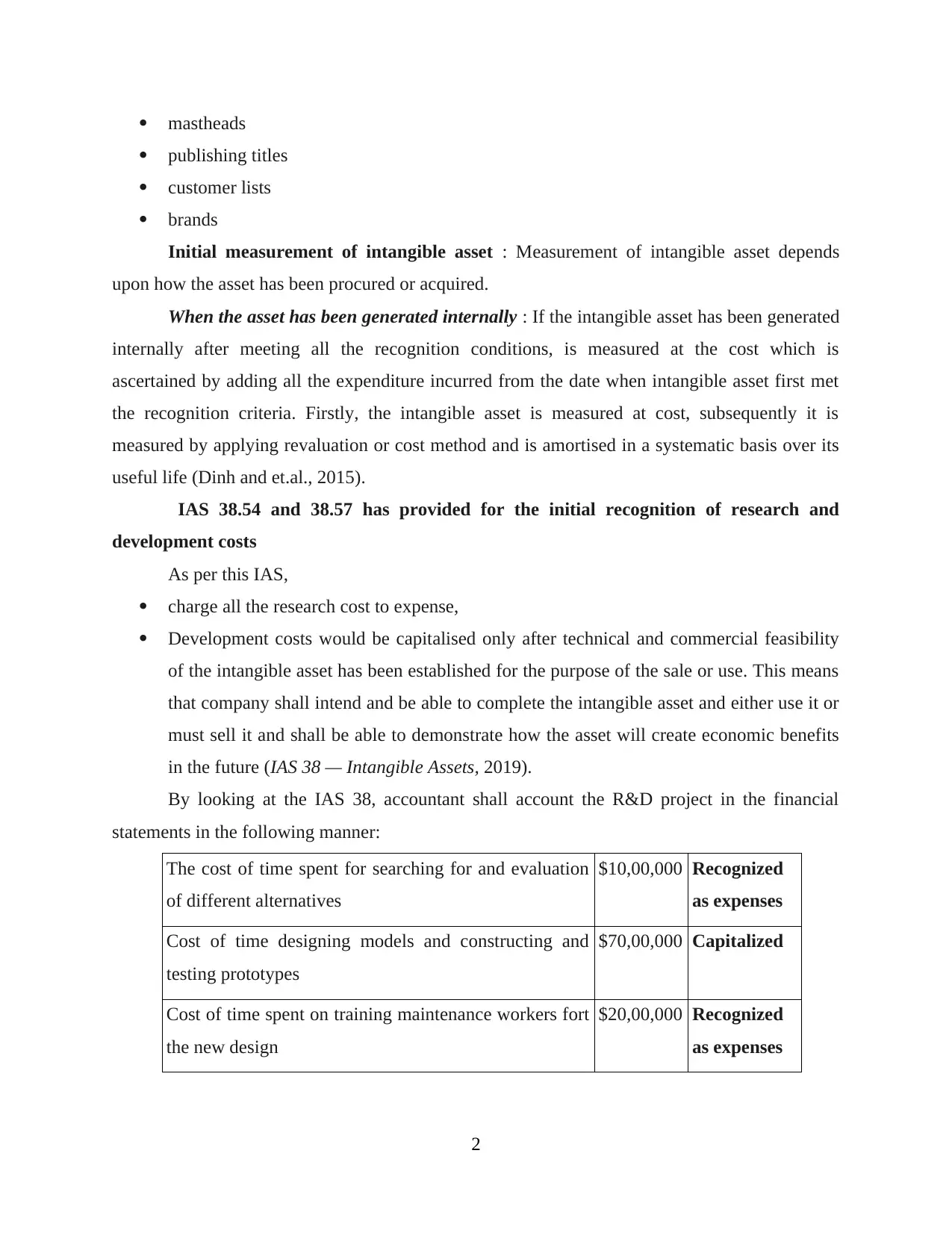

mastheads

publishing titles

customer lists

brands

Initial measurement of intangible asset : Measurement of intangible asset depends

upon how the asset has been procured or acquired.

When the asset has been generated internally : If the intangible asset has been generated

internally after meeting all the recognition conditions, is measured at the cost which is

ascertained by adding all the expenditure incurred from the date when intangible asset first met

the recognition criteria. Firstly, the intangible asset is measured at cost, subsequently it is

measured by applying revaluation or cost method and is amortised in a systematic basis over its

useful life (Dinh and et.al., 2015).

IAS 38.54 and 38.57 has provided for the initial recognition of research and

development costs

As per this IAS,

charge all the research cost to expense,

Development costs would be capitalised only after technical and commercial feasibility

of the intangible asset has been established for the purpose of the sale or use. This means

that company shall intend and be able to complete the intangible asset and either use it or

must sell it and shall be able to demonstrate how the asset will create economic benefits

in the future (IAS 38 — Intangible Assets, 2019).

By looking at the IAS 38, accountant shall account the R&D project in the financial

statements in the following manner:

The cost of time spent for searching for and evaluation

of different alternatives

$10,00,000 Recognized

as expenses

Cost of time designing models and constructing and

testing prototypes

$70,00,000 Capitalized

Cost of time spent on training maintenance workers fort

the new design

$20,00,000 Recognized

as expenses

2

publishing titles

customer lists

brands

Initial measurement of intangible asset : Measurement of intangible asset depends

upon how the asset has been procured or acquired.

When the asset has been generated internally : If the intangible asset has been generated

internally after meeting all the recognition conditions, is measured at the cost which is

ascertained by adding all the expenditure incurred from the date when intangible asset first met

the recognition criteria. Firstly, the intangible asset is measured at cost, subsequently it is

measured by applying revaluation or cost method and is amortised in a systematic basis over its

useful life (Dinh and et.al., 2015).

IAS 38.54 and 38.57 has provided for the initial recognition of research and

development costs

As per this IAS,

charge all the research cost to expense,

Development costs would be capitalised only after technical and commercial feasibility

of the intangible asset has been established for the purpose of the sale or use. This means

that company shall intend and be able to complete the intangible asset and either use it or

must sell it and shall be able to demonstrate how the asset will create economic benefits

in the future (IAS 38 — Intangible Assets, 2019).

By looking at the IAS 38, accountant shall account the R&D project in the financial

statements in the following manner:

The cost of time spent for searching for and evaluation

of different alternatives

$10,00,000 Recognized

as expenses

Cost of time designing models and constructing and

testing prototypes

$70,00,000 Capitalized

Cost of time spent on training maintenance workers fort

the new design

$20,00,000 Recognized

as expenses

2

Out of these costs, costs of searching and evaluating different alternatives of $10,00,000

and cost of time spent for providing training to workers for the use of new design of $20,00,000

will be recognised as expenses as per the IAS 38.54. This means that $30,00,000 will be charged

to the income statement of the Technology Enterprise Ltd., for the year ending on June 30,

2018. These expenses will be deducted from the profits generated during the year.

The cost of development of the R & D asset of $ 70,00,000 will be capitalised as per the

IAS 38.57. This means that amount of $70,00,000 will shown in the asset side of the balance

sheet for the year ending on June 2018 under the name of intangible asset. In the subsequent

years, amortised amount will be deducted from the intangible asset and such amortised amount

will be treated as expense and will get deducted from subsequent year's profits.

This amount has been capitalised because the company had the intention of using the

asset in their business which would yield them the economic benefits for the next 10 years. Also,

the cost of research is separable from the cost of development of intangible asset by which both

of the conditions are fulfilled by the company.

*If either of the conditions would not have been fulfilled by the intangible asset, all the

costs of the R&D asset will be treated as expenditure as if they were incurred for the motive of

research only.

Hence, the accounting treatment if the R&D asset will be done in the above mentioned way.

2. To what extent might the rules or restrictions in AASB 138/ IAS 38 reduce the comparability

of financial statements

IFRS adoption by many countries has resulted in the amendment in the ways regarding

how companies account for and report financial information in their financial statements. The

accounting standards are established in relation to IAS 38 for intangible assets, IAS 16 for

measurement of fixed assets IAS 40 for investment property etc.

IAS poses some rules that have to followed by the Australasian companies as this

accounting standard is equivalent to the AASB 138 which provides rules for the recognition,

measurement and disclosure of intangible asset in the financial statements. The IAS 38 has laid

certain conditions according to which the intangible assets has to be account for in the financial

statements which are :

identifiable

3

and cost of time spent for providing training to workers for the use of new design of $20,00,000

will be recognised as expenses as per the IAS 38.54. This means that $30,00,000 will be charged

to the income statement of the Technology Enterprise Ltd., for the year ending on June 30,

2018. These expenses will be deducted from the profits generated during the year.

The cost of development of the R & D asset of $ 70,00,000 will be capitalised as per the

IAS 38.57. This means that amount of $70,00,000 will shown in the asset side of the balance

sheet for the year ending on June 2018 under the name of intangible asset. In the subsequent

years, amortised amount will be deducted from the intangible asset and such amortised amount

will be treated as expense and will get deducted from subsequent year's profits.

This amount has been capitalised because the company had the intention of using the

asset in their business which would yield them the economic benefits for the next 10 years. Also,

the cost of research is separable from the cost of development of intangible asset by which both

of the conditions are fulfilled by the company.

*If either of the conditions would not have been fulfilled by the intangible asset, all the

costs of the R&D asset will be treated as expenditure as if they were incurred for the motive of

research only.

Hence, the accounting treatment if the R&D asset will be done in the above mentioned way.

2. To what extent might the rules or restrictions in AASB 138/ IAS 38 reduce the comparability

of financial statements

IFRS adoption by many countries has resulted in the amendment in the ways regarding

how companies account for and report financial information in their financial statements. The

accounting standards are established in relation to IAS 38 for intangible assets, IAS 16 for

measurement of fixed assets IAS 40 for investment property etc.

IAS poses some rules that have to followed by the Australasian companies as this

accounting standard is equivalent to the AASB 138 which provides rules for the recognition,

measurement and disclosure of intangible asset in the financial statements. The IAS 38 has laid

certain conditions according to which the intangible assets has to be account for in the financial

statements which are :

identifiable

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

control over the item by the company

existence of economic benefits that will arise in the future

If any intangible does not meet these criteria, then such assets will not be considered as

the intangible asset and the cost of acquiring or developing such asset will be treated as expenses

and will not be capitalised (André, Dionysiou and Tsalavoutas, 2018).

Such strict rules does not allow the flexibility in accounting, recording and disclosing of

the information related to intangible asset reduces the comparability of financial statements of

the companies with other companies in different countries operating in the same industry who

have not adopted the same rules of IAS 38. When companies in the same industry does not

follow same AS then it becomes difficult for then to compare their financial statements with each

other.

Further, as IAS 38 is part of international accounting standards. These standards are

being followed by those business entities that performing their business activities in the global

level (Herman and Fields, 2017). In addition, as these are not similar to the local accounting

standards, books of accounts prepared by following guidelines of IAS, looses their comparability

with the those company's books that prepared through local accounting standards.

3. Providing response to CEO over the understanding about AASB 13B/IAS 38 and the efficient

market hypothesis along with recommendations for company to mitigate their concern

about investor's interpretation

AASB 13B/IAS 38 are the accounting standards provides guidelines about the

recognition and measurement and disclosure of various intangible assets held by a business

organisation. By following the guidelines mentioned in the AASB 13B/IAS 38, a firm becomes

able to build a better control over all the intangible asset held by the company (SILVA, 2017).

Further, it also enhances the reliability of the value of intangible assets held by the company

through which company's actual position could be shown to its investors.

Further, the IAS and AASB provides some strict guidelines to be followed by each firms

that adopts these standards while preparing their books of accounts. It provides various standards

on the basis of which a company can appropriately value its intangible assets. It improves the

compatibility of the books of accounts and their accountability as well (Janic Loftus- Financial

Reporting, 2nd Edition, 2017).

4

existence of economic benefits that will arise in the future

If any intangible does not meet these criteria, then such assets will not be considered as

the intangible asset and the cost of acquiring or developing such asset will be treated as expenses

and will not be capitalised (André, Dionysiou and Tsalavoutas, 2018).

Such strict rules does not allow the flexibility in accounting, recording and disclosing of

the information related to intangible asset reduces the comparability of financial statements of

the companies with other companies in different countries operating in the same industry who

have not adopted the same rules of IAS 38. When companies in the same industry does not

follow same AS then it becomes difficult for then to compare their financial statements with each

other.

Further, as IAS 38 is part of international accounting standards. These standards are

being followed by those business entities that performing their business activities in the global

level (Herman and Fields, 2017). In addition, as these are not similar to the local accounting

standards, books of accounts prepared by following guidelines of IAS, looses their comparability

with the those company's books that prepared through local accounting standards.

3. Providing response to CEO over the understanding about AASB 13B/IAS 38 and the efficient

market hypothesis along with recommendations for company to mitigate their concern

about investor's interpretation

AASB 13B/IAS 38 are the accounting standards provides guidelines about the

recognition and measurement and disclosure of various intangible assets held by a business

organisation. By following the guidelines mentioned in the AASB 13B/IAS 38, a firm becomes

able to build a better control over all the intangible asset held by the company (SILVA, 2017).

Further, it also enhances the reliability of the value of intangible assets held by the company

through which company's actual position could be shown to its investors.

Further, the IAS and AASB provides some strict guidelines to be followed by each firms

that adopts these standards while preparing their books of accounts. It provides various standards

on the basis of which a company can appropriately value its intangible assets. It improves the

compatibility of the books of accounts and their accountability as well (Janic Loftus- Financial

Reporting, 2nd Edition, 2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In addition, the IAS provides additional information regarding maintenance of the self

generated intangible assets. It improves can help Technology enterprise in improving the

transparency and accountability of the statements of financial statements. It also helps it in

recognizing the actual book value of the intangible assets at the time of selling them into the

market so that the firm could gain the appropriate return from the sale.

Furthermore, AASB 13B/IAS 38 also contains various clauses for the amount to be

capitalised by the company and amount to be shown as expenses in the books of company. In

order to this, company adoption of these accounting standards can develop the ability of the firm

in maintenance and recording of various assets at the most appropriate rates.

Moreover, AASB 13B/IAS 38 gives various standards on the basis of which the

business organisation can evaluate and show the actual financial position of the company in front

of the inventors (enciu and Ienciu, 2016). It leads in enhancing the reliability of investors for the

company. In this regard, adoption of these accounting standards helps in gaining trust of

investors and maintaining them with the company for long period of time.

Recommendation

In this regard, from the analysis of the AASB 13B/IAS 38, it can be recommend to the

CEO of Technology Enterprise that they should adopt these standards while preparing company's

books of accounts. It will help the firm in providing the most appropriate business information

to the company through which trust and faith of the investors and other external users of the

company's books of accounts could be gained. It would help the business in maintaining and

enhancing the ability of raising funds from the market for running its business operations.

Further, with the help of adopting AASB 13B/IAS 38, Technology Enterprise can

determine the most appropriate amount of generation of intangible assets to be capitalised or to

be shown as expenses in such a way so that it shall not result in misguiding the investors for the

purpose of deciding the certain amount to be invested in the company. As by showing these

amounts in such a way so that company;s financial position could be shown at its highest can

miguid the shareholders and other investors by showing extra ordinary positive position of the

company. Although, it would result in gaining the maximum attraction of the investors and

shareholders towards the company, but it would surely provide disappointment to them after a

certain period of time, as the company would not be able to provide the return to them as per

their expectation on the basis of misguided information. In this regard, company's reputation in

5

generated intangible assets. It improves can help Technology enterprise in improving the

transparency and accountability of the statements of financial statements. It also helps it in

recognizing the actual book value of the intangible assets at the time of selling them into the

market so that the firm could gain the appropriate return from the sale.

Furthermore, AASB 13B/IAS 38 also contains various clauses for the amount to be

capitalised by the company and amount to be shown as expenses in the books of company. In

order to this, company adoption of these accounting standards can develop the ability of the firm

in maintenance and recording of various assets at the most appropriate rates.

Moreover, AASB 13B/IAS 38 gives various standards on the basis of which the

business organisation can evaluate and show the actual financial position of the company in front

of the inventors (enciu and Ienciu, 2016). It leads in enhancing the reliability of investors for the

company. In this regard, adoption of these accounting standards helps in gaining trust of

investors and maintaining them with the company for long period of time.

Recommendation

In this regard, from the analysis of the AASB 13B/IAS 38, it can be recommend to the

CEO of Technology Enterprise that they should adopt these standards while preparing company's

books of accounts. It will help the firm in providing the most appropriate business information

to the company through which trust and faith of the investors and other external users of the

company's books of accounts could be gained. It would help the business in maintaining and

enhancing the ability of raising funds from the market for running its business operations.

Further, with the help of adopting AASB 13B/IAS 38, Technology Enterprise can

determine the most appropriate amount of generation of intangible assets to be capitalised or to

be shown as expenses in such a way so that it shall not result in misguiding the investors for the

purpose of deciding the certain amount to be invested in the company. As by showing these

amounts in such a way so that company;s financial position could be shown at its highest can

miguid the shareholders and other investors by showing extra ordinary positive position of the

company. Although, it would result in gaining the maximum attraction of the investors and

shareholders towards the company, but it would surely provide disappointment to them after a

certain period of time, as the company would not be able to provide the return to them as per

their expectation on the basis of misguided information. In this regard, company's reputation in

5

the market may go downwards. In this order, it can be recommended to the Technology

Enterprise that its should develop its financial records on the basis of the guidelines provided by

AASB 13B/IAS 38.

CONCLUSION

From the analysis of above study it can be concluded that AASB 13B/IAS 38 contains

guidelines and rules that are being followed by the business organisation in order to maintaining

the record of all the intangible assets of the company. It contains several measures that helps the

company in recording all the expenses relating to the intangible assets at the most appropriate

rate. Further, the study has concluded that maintenance of books of accounts as pr the accounting

standards leads in enhancing the effectiveness and accountability of the books. It enables the

business in maintaining and improving the trust of investors.

6

Enterprise that its should develop its financial records on the basis of the guidelines provided by

AASB 13B/IAS 38.

CONCLUSION

From the analysis of above study it can be concluded that AASB 13B/IAS 38 contains

guidelines and rules that are being followed by the business organisation in order to maintaining

the record of all the intangible assets of the company. It contains several measures that helps the

company in recording all the expenses relating to the intangible assets at the most appropriate

rate. Further, the study has concluded that maintenance of books of accounts as pr the accounting

standards leads in enhancing the effectiveness and accountability of the books. It enables the

business in maintaining and improving the trust of investors.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on

analysts’ forecasts. Applied Economics. 50(7). pp.707-725.

Dinh, T and et.al., 2015. Research and development, uncertainty, and analysts’ forecasts: The

case of IAS 38. Journal of International Financial Management & Accounting. 26(3).

pp.257-293.

De Villiers, C. and Sharma, U., 2017. A critical reflection on the future of financial, intellectual

capital, sustainability and integrated reporting. Critical Perspectives on Accounting.

Herman, M. and Fields, J., 2017. Work Session.

SILVA, E. B. D., 2017. Propriedades físico-químicas, nutricionais e funcionais de farinhas de

olerícolas e seu potencial de aplicação no desenvolvimento de fish burguers.

Ienciu, N. M. and Ienciu, I. A., 2016. New inflection points identified in the evolution of IAS 38

Intangible Assets: a critical approach. International Journal of Critical Accounting. 8(3-4).

pp.321-344.

Online

IAS 38 — Intangible Assets.2019. [Online]. Available through

<https://www.iasplus.com/en/standards/ias/ias38>

Janic Loftus- Financial Reporting, 2nd Edition.2017. [Online]. Available through

<https://www.bookdepository.com/Financial-Reporting-2nd-Edition-Janice-Loftus/

9780730350538>

7

Books and Journals

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on

analysts’ forecasts. Applied Economics. 50(7). pp.707-725.

Dinh, T and et.al., 2015. Research and development, uncertainty, and analysts’ forecasts: The

case of IAS 38. Journal of International Financial Management & Accounting. 26(3).

pp.257-293.

De Villiers, C. and Sharma, U., 2017. A critical reflection on the future of financial, intellectual

capital, sustainability and integrated reporting. Critical Perspectives on Accounting.

Herman, M. and Fields, J., 2017. Work Session.

SILVA, E. B. D., 2017. Propriedades físico-químicas, nutricionais e funcionais de farinhas de

olerícolas e seu potencial de aplicação no desenvolvimento de fish burguers.

Ienciu, N. M. and Ienciu, I. A., 2016. New inflection points identified in the evolution of IAS 38

Intangible Assets: a critical approach. International Journal of Critical Accounting. 8(3-4).

pp.321-344.

Online

IAS 38 — Intangible Assets.2019. [Online]. Available through

<https://www.iasplus.com/en/standards/ias/ias38>

Janic Loftus- Financial Reporting, 2nd Edition.2017. [Online]. Available through

<https://www.bookdepository.com/Financial-Reporting-2nd-Edition-Janice-Loftus/

9780730350538>

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.