Taxation Law Australia Case Study 2022

VerifiedAdded on 2022/10/15

|12

|2471

|13

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issue:

The readings of this case is concerned with the entitlements associated to the input tax

credit which the taxpayer in the current case may be considered eligible for certain

transaction.

Laws:

The goods and service tax came into the existence during July 2000 and it replaced

the numerous indirect taxes that also included the whole sale tax and the indirect state taxes.

GST is treated as the tax on final consumption inside Australia and imports that are made

inside the Australia. With regard to

“sec 7-1 GST Act”, GST is generally considered payable

on the assessable supplies and the assessable imports (Hellerstein 2015). GST is usually

lowered through input tax credits related to the creditable purpose and creditable imports.

Under

“sec 9-10 (1)”, GST Act there must be a supply of goods and service by the

supplier. The term supply refers to any type of supply of any kind (May 2016). Particularly it

comprises of goods and services, advice or information, rights associated to the real property

and an entry in or release from any form of obligation.

“Sec 9-5, GST Act” defines the

taxable supply as;

a. There should be a supply

b. The supply is made by the taxpayer for consideration

c. The supply has the connection with Australia

d. The supply is made by the taxpayer during the ordinary business course and for

continuance of a business activity

Answer to question 1:

Issue:

The readings of this case is concerned with the entitlements associated to the input tax

credit which the taxpayer in the current case may be considered eligible for certain

transaction.

Laws:

The goods and service tax came into the existence during July 2000 and it replaced

the numerous indirect taxes that also included the whole sale tax and the indirect state taxes.

GST is treated as the tax on final consumption inside Australia and imports that are made

inside the Australia. With regard to

“sec 7-1 GST Act”, GST is generally considered payable

on the assessable supplies and the assessable imports (Hellerstein 2015). GST is usually

lowered through input tax credits related to the creditable purpose and creditable imports.

Under

“sec 9-10 (1)”, GST Act there must be a supply of goods and service by the

supplier. The term supply refers to any type of supply of any kind (May 2016). Particularly it

comprises of goods and services, advice or information, rights associated to the real property

and an entry in or release from any form of obligation.

“Sec 9-5, GST Act” defines the

taxable supply as;

a. There should be a supply

b. The supply is made by the taxpayer for consideration

c. The supply has the connection with Australia

d. The supply is made by the taxpayer during the ordinary business course and for

continuance of a business activity

3TAXATION LAW

e. The supplier is treated as registered for GST or they are under obligation of obtaining

registration for GST.

It is necessary for a taxable supply to have the consideration. This would immediately

include the price which is inclusive of GST. The relation between consideration and supply is

given in

“paragraph 9-5 of the GST Act”. According to the

“paragraph 9-5 (a)” it

requires that for a taxable supply a taxpayer makes the supply for consideration (Millar

2014). As understood from the above given explanation, the meaning of consideration under

“sec 195-1” includes the payment that is made in relation with the supply. As held in the case

of

“AP Group Ltd v Commissioner of Taxation [2013]” the law court verdict denoted that

the consideration should have connection with supply however the supply should also be

made for consideration.

Apart from the taxable supply there is also an area that taxpayers needs to place

emphasis as well. This includes the reverse charge mechanism. Under this method the

receiver of goods or services is under obligation of paying GST rather than the supplier. The

rules of the reverse charge says that things apart from the goods and services will be the

subject of GST when the Australian business makes purchase and things are done out of

Australia or it is made with the help of business that is carried on by seller out of Australia

(Feria 2019). The rules of reverse charge is applicable if the purchase is successful in meeting

both the conditions and circumstances that are given below

The reverse charge rule is applicable on the conditions that taxpayer has purchased a

thing that is completely for business they are carrying on Australia

The sale is exchange for payment

The receiver is registered for GST or they are required to be registered for GST.

e. The supplier is treated as registered for GST or they are under obligation of obtaining

registration for GST.

It is necessary for a taxable supply to have the consideration. This would immediately

include the price which is inclusive of GST. The relation between consideration and supply is

given in

“paragraph 9-5 of the GST Act”. According to the

“paragraph 9-5 (a)” it

requires that for a taxable supply a taxpayer makes the supply for consideration (Millar

2014). As understood from the above given explanation, the meaning of consideration under

“sec 195-1” includes the payment that is made in relation with the supply. As held in the case

of

“AP Group Ltd v Commissioner of Taxation [2013]” the law court verdict denoted that

the consideration should have connection with supply however the supply should also be

made for consideration.

Apart from the taxable supply there is also an area that taxpayers needs to place

emphasis as well. This includes the reverse charge mechanism. Under this method the

receiver of goods or services is under obligation of paying GST rather than the supplier. The

rules of the reverse charge says that things apart from the goods and services will be the

subject of GST when the Australian business makes purchase and things are done out of

Australia or it is made with the help of business that is carried on by seller out of Australia

(Feria 2019). The rules of reverse charge is applicable if the purchase is successful in meeting

both the conditions and circumstances that are given below

The reverse charge rule is applicable on the conditions that taxpayer has purchased a

thing that is completely for business they are carrying on Australia

The sale is exchange for payment

The receiver is registered for GST or they are required to be registered for GST.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

There are also the circumstances of purchase that must be made for reverse charge

mechanism

The sale is related to Australia because the things purchase is having the right or

option of acquiring another thing (Scandroglio 2015).

The things purchased by the business is for the activities done out of Australia.

Application:

As obvious from the case that City Sky Co is the registered GST Company and hence

the company can be said as eligible to access the input tax credit as when needed. During the

year the company bought a vacant land on which it has the plan of building 15 apartments for

sell. In the current case of City Sky Co, land is an immovable property. It can neither be

regarded as the goods nor will the land be viewed as service. Consequently, no GST is

required to be paid on the land and also no GST is applied while purchasing the land. The

intention of building apartment falls inside the black credit provision. In other words the land

received by City Sky Co for the construction of immovable property whether in the ordinary

business course is not considered eligible for claiming input tax credit.

Later it is noticed that City Sky Co has availed the service of an advocate and paid a

sum of $33,000. The service from Maurice Blackburn regarding the developmental of

building on vacant land is a supply under

“sec 9-10 (1), GST Act”. The legal services falls

under the reverse charge mechanism for City Sky Co and the company will be considered for

paying the GST on the services received (Pfeiffer 2017). Referring to the case of

“AP Group

Ltd v Commissioner of Taxation [2013]” the consideration holds connection with the

supply and it is exclusively for the business purpose of City Sky Co. The company will be

treated eligible for claiming the input tax credit from services availed from Maurice

Blackburn.

There are also the circumstances of purchase that must be made for reverse charge

mechanism

The sale is related to Australia because the things purchase is having the right or

option of acquiring another thing (Scandroglio 2015).

The things purchased by the business is for the activities done out of Australia.

Application:

As obvious from the case that City Sky Co is the registered GST Company and hence

the company can be said as eligible to access the input tax credit as when needed. During the

year the company bought a vacant land on which it has the plan of building 15 apartments for

sell. In the current case of City Sky Co, land is an immovable property. It can neither be

regarded as the goods nor will the land be viewed as service. Consequently, no GST is

required to be paid on the land and also no GST is applied while purchasing the land. The

intention of building apartment falls inside the black credit provision. In other words the land

received by City Sky Co for the construction of immovable property whether in the ordinary

business course is not considered eligible for claiming input tax credit.

Later it is noticed that City Sky Co has availed the service of an advocate and paid a

sum of $33,000. The service from Maurice Blackburn regarding the developmental of

building on vacant land is a supply under

“sec 9-10 (1), GST Act”. The legal services falls

under the reverse charge mechanism for City Sky Co and the company will be considered for

paying the GST on the services received (Pfeiffer 2017). Referring to the case of

“AP Group

Ltd v Commissioner of Taxation [2013]” the consideration holds connection with the

supply and it is exclusively for the business purpose of City Sky Co. The company will be

treated eligible for claiming the input tax credit from services availed from Maurice

Blackburn.

5TAXATION LAW

Conclusion:

The case analysis contributes to the fact that City Sky Co is eligible for accessing the

input tax credit for the development services since it meets the conditions and circumstances

of the reverse charge mechanism.

Answer to question 2:

Under

“sec 104-10(4)” the disposal proceeds obtained from selling the asset is

compared with the cost base of the CGT asset. As a general note there are five elements of

the cost base. The detailed elements of cost base are as follows;

Element 1: The money that a taxpayer has to pay for purchasing the asset or the market value

of any other property that is given to purchase the CGT asset under

“sec 110.25 (2)”.

Element 2: This element mainly deals with the acquisition cost and sale of CGT asset. Under

“sec 110.25 (3)” this element includes the stamp duty, legal expenses, agent commission etc.

to buy or sell the asset (Duncan et al. 2018).

Element 3: This element includes the non-capital cost that is paid by the taxpayer for the

asset ownership that does not qualifies for deduction.

“Sec 110.25 (4)” includes the land tax,

repairs, insurance, rates and interest on borrowings that are non-deductible.

Element 4: This element mainly deals with the expenses that are occurred by the taxpayer in

increasing the value of CGT asset. Under

“sec 110.25 (1)” the expenses include, capital

improvements such as renovations or extension (Mahar 2016).

Element 5: This element involves capital outgoings that are occurred in preserving,

defending the title or rights to the CGT-assets under

“sec 110.25 (6), ITA Act 97”.

Conclusion:

The case analysis contributes to the fact that City Sky Co is eligible for accessing the

input tax credit for the development services since it meets the conditions and circumstances

of the reverse charge mechanism.

Answer to question 2:

Under

“sec 104-10(4)” the disposal proceeds obtained from selling the asset is

compared with the cost base of the CGT asset. As a general note there are five elements of

the cost base. The detailed elements of cost base are as follows;

Element 1: The money that a taxpayer has to pay for purchasing the asset or the market value

of any other property that is given to purchase the CGT asset under

“sec 110.25 (2)”.

Element 2: This element mainly deals with the acquisition cost and sale of CGT asset. Under

“sec 110.25 (3)” this element includes the stamp duty, legal expenses, agent commission etc.

to buy or sell the asset (Duncan et al. 2018).

Element 3: This element includes the non-capital cost that is paid by the taxpayer for the

asset ownership that does not qualifies for deduction.

“Sec 110.25 (4)” includes the land tax,

repairs, insurance, rates and interest on borrowings that are non-deductible.

Element 4: This element mainly deals with the expenses that are occurred by the taxpayer in

increasing the value of CGT asset. Under

“sec 110.25 (1)” the expenses include, capital

improvements such as renovations or extension (Mahar 2016).

Element 5: This element involves capital outgoings that are occurred in preserving,

defending the title or rights to the CGT-assets under

“sec 110.25 (6), ITA Act 97”.

6TAXATION LAW

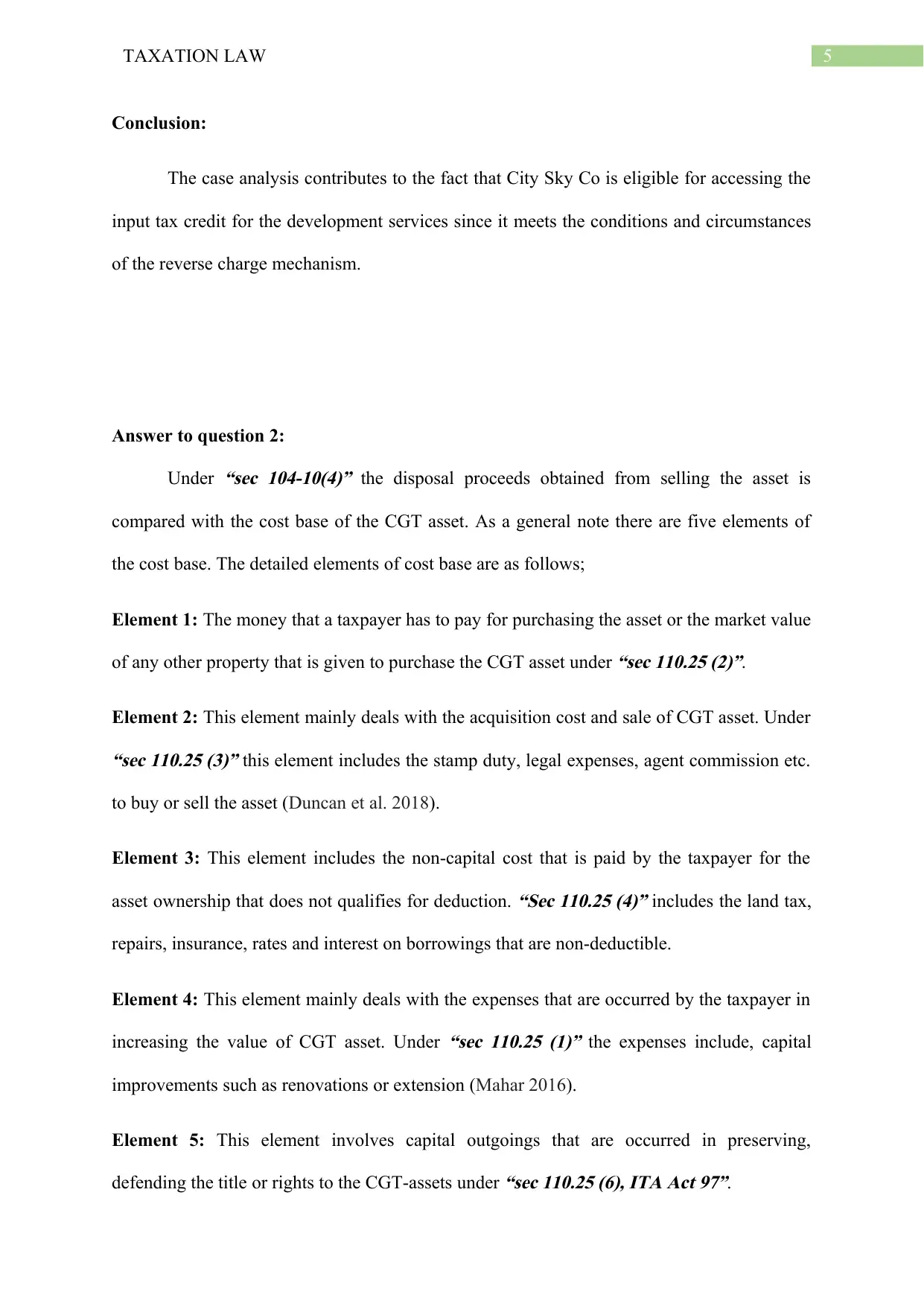

Emma is selling her block of land for $1,000,000 while the purchase price paid was

$250,000 for acquiring the land. Under the Element 1 of cost base the price paid for acquiring

the land will be included based on the legislative provision of

“sec 110-25 (2)”. During

purchase Emma paid $5000 for stamp duty and $10,000 for legal fees. Therefore, under

“sec.110.25 (3)” these expenses are incidental cost of purchasing the block of land incurred

by Emma which will be included in element 2 cost base of land. She further paid council and

water rates, insurance and interest on loan which amounted $22,000 and $32,000

respectively. So under

“sec 110.25 (4)” these costs will be included in element 3 of the cost

base of land as non-capital ownership cost. A disputed was reported by Emma on property

with neighbours and the settlement of disputed cost Emma $5000. Under

“sec 110.25 (6)”, it

is capital expense occurred by Emma in defending her rights on the land and will be included

in element 5 cost base of asset. Finally, she reported an expense of $$27,000 for removing the

pine trees on land (Huizinga, Voget and Wagner 2018). Under

“sec 110.25 (5)” this cost will

be included in element 4 of the cost base of land as a capital improvement cost.

Referring to

“s104-10 (4)” the proceeds of land following disposal is compared with

cost base for CGT purpose.

Emma is selling her block of land for $1,000,000 while the purchase price paid was

$250,000 for acquiring the land. Under the Element 1 of cost base the price paid for acquiring

the land will be included based on the legislative provision of

“sec 110-25 (2)”. During

purchase Emma paid $5000 for stamp duty and $10,000 for legal fees. Therefore, under

“sec.110.25 (3)” these expenses are incidental cost of purchasing the block of land incurred

by Emma which will be included in element 2 cost base of land. She further paid council and

water rates, insurance and interest on loan which amounted $22,000 and $32,000

respectively. So under

“sec 110.25 (4)” these costs will be included in element 3 of the cost

base of land as non-capital ownership cost. A disputed was reported by Emma on property

with neighbours and the settlement of disputed cost Emma $5000. Under

“sec 110.25 (6)”, it

is capital expense occurred by Emma in defending her rights on the land and will be included

in element 5 cost base of asset. Finally, she reported an expense of $$27,000 for removing the

pine trees on land (Huizinga, Voget and Wagner 2018). Under

“sec 110.25 (5)” this cost will

be included in element 4 of the cost base of land as a capital improvement cost.

Referring to

“s104-10 (4)” the proceeds of land following disposal is compared with

cost base for CGT purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

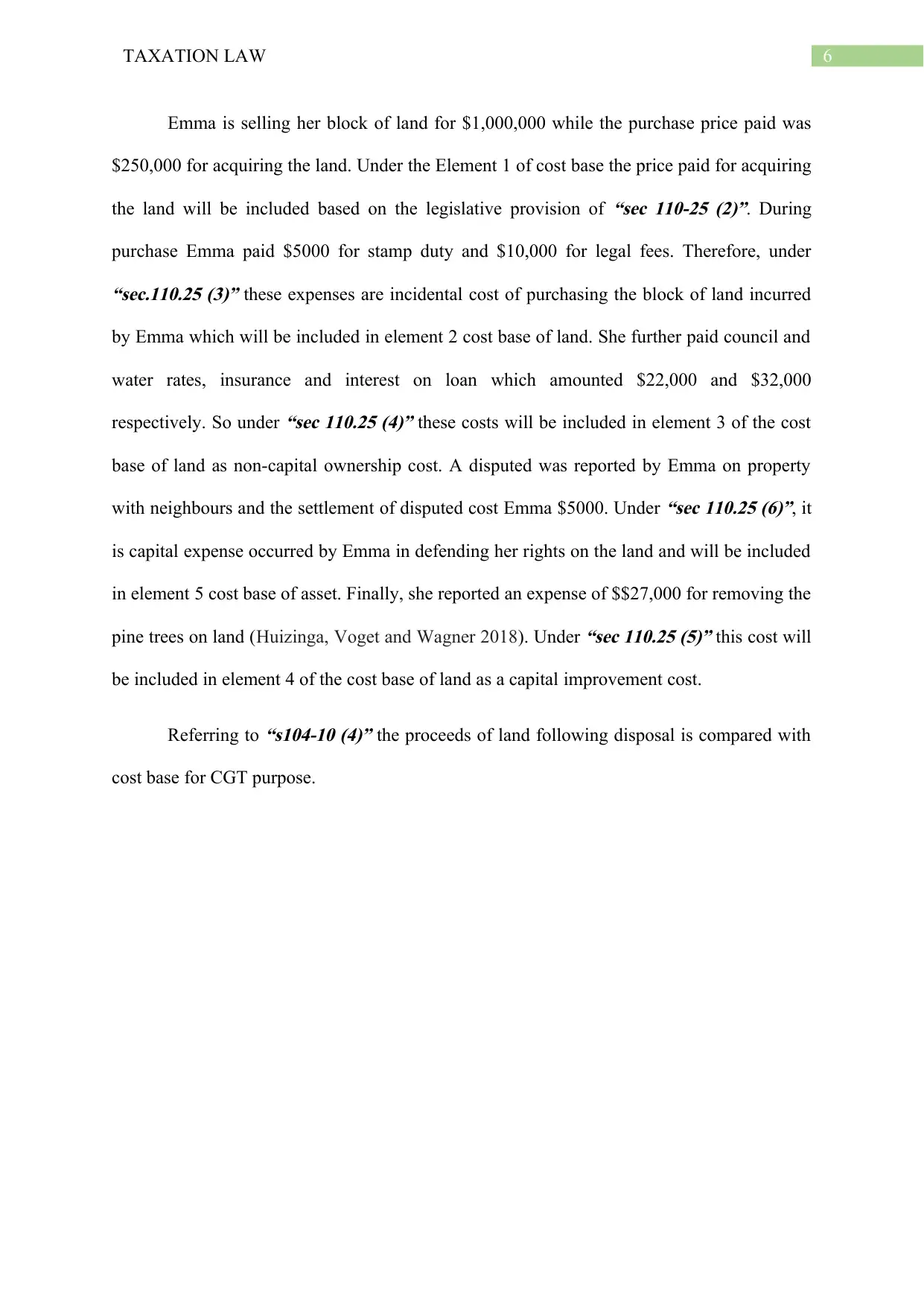

Sell of Emma’s share in Rio Tinto:

The general provision of the CGT is implemented on assets that are acquired or events

that are taking place on or after the date of 20 September 1985. In order to refer the assets or

in regard to any event that are taking place before or after that date the word pre-CGT and

post-CGT is used (Kirchner 2014). Only those gains are taxed where events takings place

after 20 September 1985. Emma has sold the 1000 shares of Rio Tinto in 2015. The sells

price fetched for each shares were $50.85 however it was bought in 1982 for $3.85. These

shares must be classified as pre-CGT asset since Emma purchased it earlier to introduction of

CGT regime. So the capital gains made are exempted from CGT.

Sell of Emma’s share in Rio Tinto:

The general provision of the CGT is implemented on assets that are acquired or events

that are taking place on or after the date of 20 September 1985. In order to refer the assets or

in regard to any event that are taking place before or after that date the word pre-CGT and

post-CGT is used (Kirchner 2014). Only those gains are taxed where events takings place

after 20 September 1985. Emma has sold the 1000 shares of Rio Tinto in 2015. The sells

price fetched for each shares were $50.85 however it was bought in 1982 for $3.85. These

shares must be classified as pre-CGT asset since Emma purchased it earlier to introduction of

CGT regime. So the capital gains made are exempted from CGT.

8TAXATION LAW

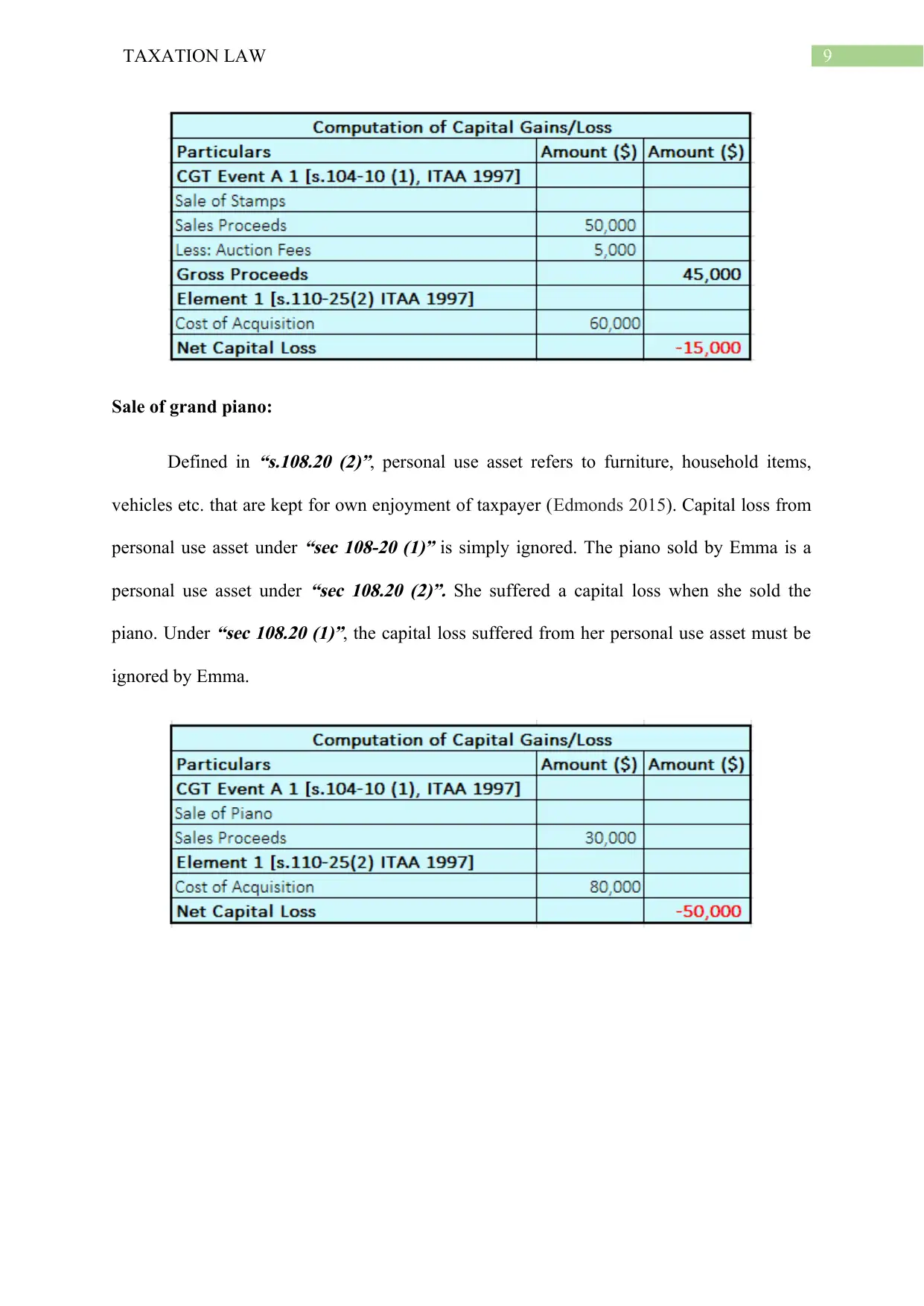

Sale of Stamp collections:

When a taxpayer enters in the contract for sale then a “CGT event A1” happens under

“sec 104-10 (3)”. Defined in

“sec 108.10(2)” collectables are specifically items such as

antiques, artwork, jewellery etc. that is kept for private use and satisfaction (Gitman, Juchau

and Flanagan 2015). Other special rules that are applied on collectables is that capital loss

from collectables is permitted only for offset against the capital gains from other collectables

under

“sec 108.40 (4)”.

The stamps were sold by Emma in auction for a sale price of $50,000 while the

stamps were purchased for $60,000 in 2015. The stamps are falling within the meaning of

collectables under

“sec 108.10(2)”. When Emma entered in the contract for sale of Stamps

then a

“CGT event A1” happened under

“sec 104-10 (3)” (Clark 2014). The stamps yielded

capital loss. So under special rules of

“sec 108.10 (4)” the capital loss is not allowed for

offset against any gains, instead Emma should carry forward to next year because no

alternative capital gains from collectables were reported.

Sale of Stamp collections:

When a taxpayer enters in the contract for sale then a “CGT event A1” happens under

“sec 104-10 (3)”. Defined in

“sec 108.10(2)” collectables are specifically items such as

antiques, artwork, jewellery etc. that is kept for private use and satisfaction (Gitman, Juchau

and Flanagan 2015). Other special rules that are applied on collectables is that capital loss

from collectables is permitted only for offset against the capital gains from other collectables

under

“sec 108.40 (4)”.

The stamps were sold by Emma in auction for a sale price of $50,000 while the

stamps were purchased for $60,000 in 2015. The stamps are falling within the meaning of

collectables under

“sec 108.10(2)”. When Emma entered in the contract for sale of Stamps

then a

“CGT event A1” happened under

“sec 104-10 (3)” (Clark 2014). The stamps yielded

capital loss. So under special rules of

“sec 108.10 (4)” the capital loss is not allowed for

offset against any gains, instead Emma should carry forward to next year because no

alternative capital gains from collectables were reported.

9TAXATION LAW

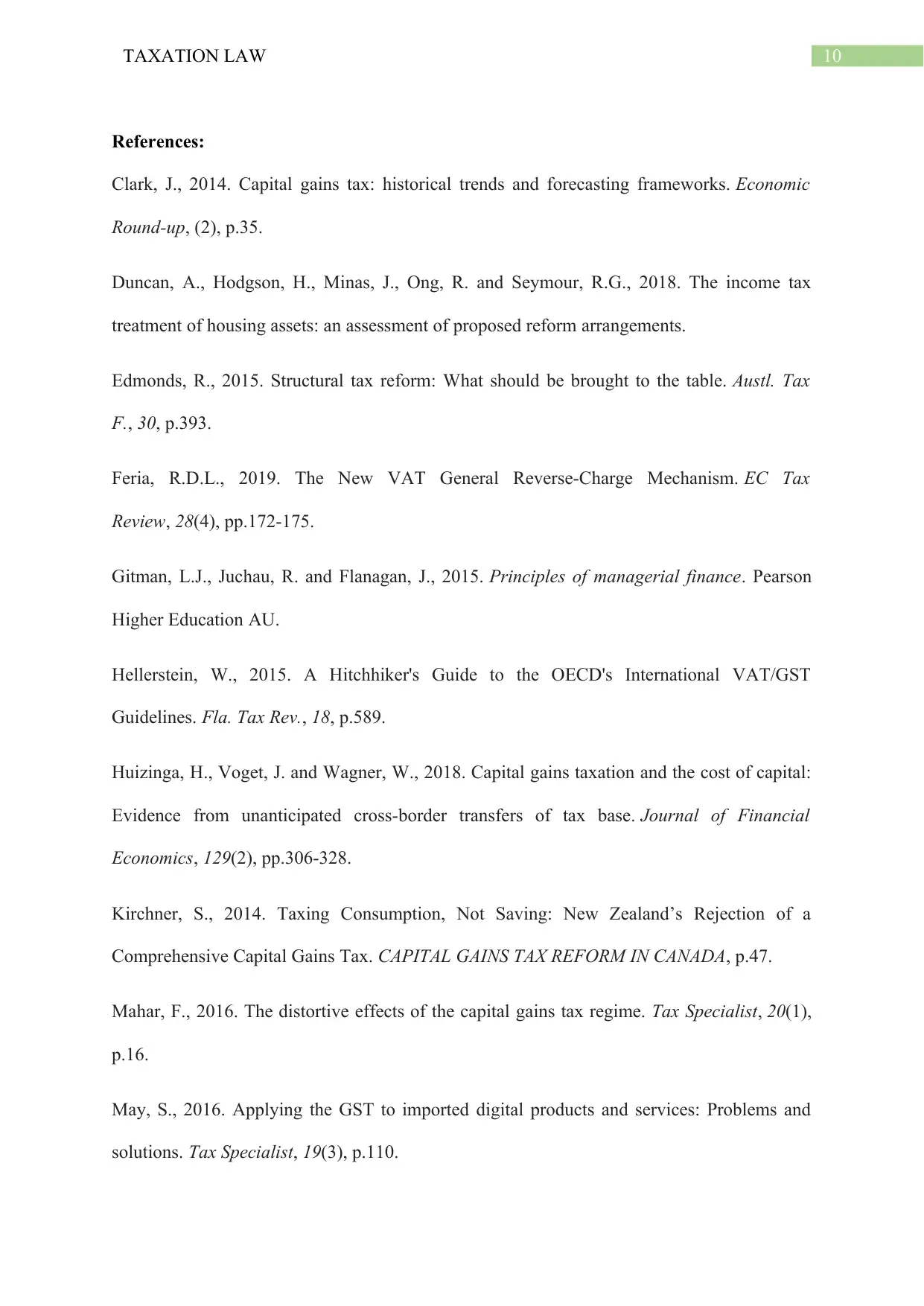

Sale of grand piano:

Defined in

“s.108.20 (2)”, personal use asset refers to furniture, household items,

vehicles etc. that are kept for own enjoyment of taxpayer (Edmonds 2015). Capital loss from

personal use asset under

“sec 108-20 (1)” is simply ignored. The piano sold by Emma is a

personal use asset under

“sec 108.20 (2)”. She suffered a capital loss when she sold the

piano. Under

“sec 108.20 (1)”, the capital loss suffered from her personal use asset must be

ignored by Emma.

Sale of grand piano:

Defined in

“s.108.20 (2)”, personal use asset refers to furniture, household items,

vehicles etc. that are kept for own enjoyment of taxpayer (Edmonds 2015). Capital loss from

personal use asset under

“sec 108-20 (1)” is simply ignored. The piano sold by Emma is a

personal use asset under

“sec 108.20 (2)”. She suffered a capital loss when she sold the

piano. Under

“sec 108.20 (1)”, the capital loss suffered from her personal use asset must be

ignored by Emma.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

References:

Clark, J., 2014. Capital gains tax: historical trends and forecasting frameworks. Economic

Round-up, (2), p.35.

Duncan, A., Hodgson, H., Minas, J., Ong, R. and Seymour, R.G., 2018. The income tax

treatment of housing assets: an assessment of proposed reform arrangements.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax

F., 30, p.393.

Feria, R.D.L., 2019. The New VAT General Reverse-Charge Mechanism. EC Tax

Review, 28(4), pp.172-175.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hellerstein, W., 2015. A Hitchhiker's Guide to the OECD's International VAT/GST

Guidelines. Fla. Tax Rev., 18, p.589.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Kirchner, S., 2014. Taxing Consumption, Not Saving: New Zealand’s Rejection of a

Comprehensive Capital Gains Tax. CAPITAL GAINS TAX REFORM IN CANADA, p.47.

Mahar, F., 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

p.16.

May, S., 2016. Applying the GST to imported digital products and services: Problems and

solutions. Tax Specialist, 19(3), p.110.

References:

Clark, J., 2014. Capital gains tax: historical trends and forecasting frameworks. Economic

Round-up, (2), p.35.

Duncan, A., Hodgson, H., Minas, J., Ong, R. and Seymour, R.G., 2018. The income tax

treatment of housing assets: an assessment of proposed reform arrangements.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax

F., 30, p.393.

Feria, R.D.L., 2019. The New VAT General Reverse-Charge Mechanism. EC Tax

Review, 28(4), pp.172-175.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hellerstein, W., 2015. A Hitchhiker's Guide to the OECD's International VAT/GST

Guidelines. Fla. Tax Rev., 18, p.589.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Kirchner, S., 2014. Taxing Consumption, Not Saving: New Zealand’s Rejection of a

Comprehensive Capital Gains Tax. CAPITAL GAINS TAX REFORM IN CANADA, p.47.

Mahar, F., 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

p.16.

May, S., 2016. Applying the GST to imported digital products and services: Problems and

solutions. Tax Specialist, 19(3), p.110.

11TAXATION LAW

Millar, R., 2014. VAT/GST in a Global Digital Economy: Looking Ahead-Potential

Solutions and the Framework to Make Them Work. Sydney Law School Research Paper,

(16/30).

Pfeiffer, S., 2017. A VAT/GST Perspective on Crowdfunding. In VAT and Financial

Services (pp. 223-255). Springer, Singapore.

Scandroglio, R., 2015. Recent developments in international VAT/GST tax policy. Global

Trends in VAT/GST and Direct Taxation: Schriftenreihe IStR Band 93, 93, p.1.

Millar, R., 2014. VAT/GST in a Global Digital Economy: Looking Ahead-Potential

Solutions and the Framework to Make Them Work. Sydney Law School Research Paper,

(16/30).

Pfeiffer, S., 2017. A VAT/GST Perspective on Crowdfunding. In VAT and Financial

Services (pp. 223-255). Springer, Singapore.

Scandroglio, R., 2015. Recent developments in international VAT/GST tax policy. Global

Trends in VAT/GST and Direct Taxation: Schriftenreihe IStR Band 93, 93, p.1.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.